South America Factory Automation And Industrial Controls Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

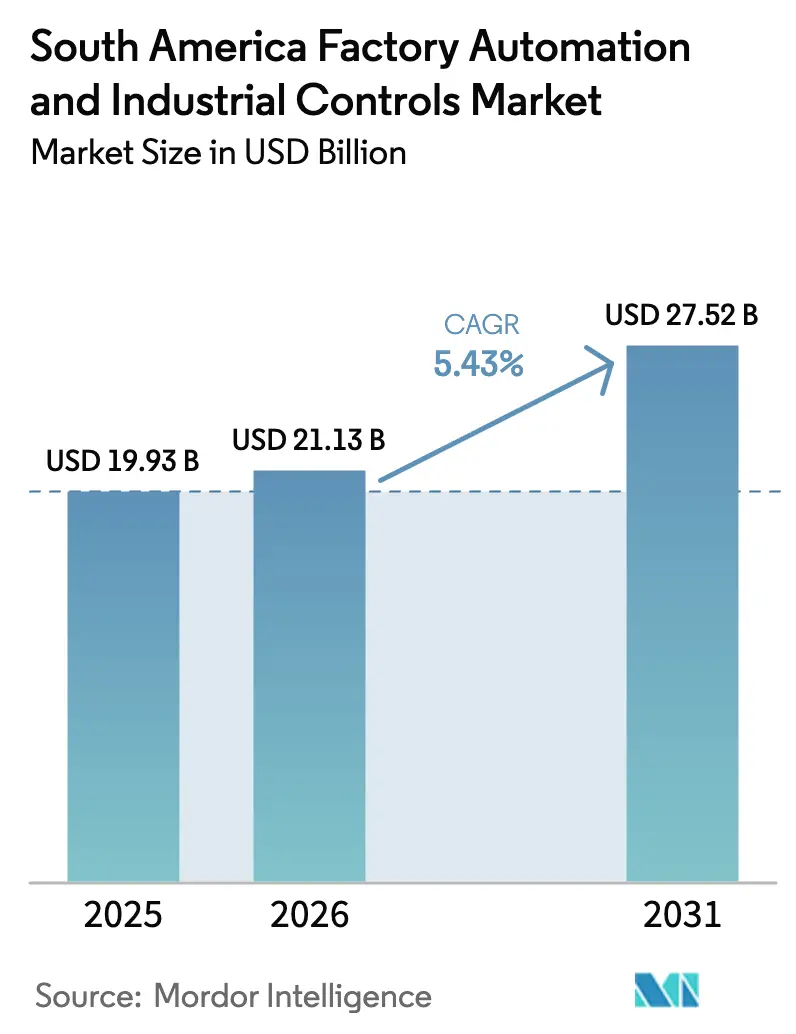

| Base Year Market Size (2025) | USD 19.93 Billion |

| Market Size (2026) | USD 21.13 Billion |

| Market Size (2031) | USD 27.52 Billion |

| Growth Rate (2026 - 2031) | 5.43% CAGR |

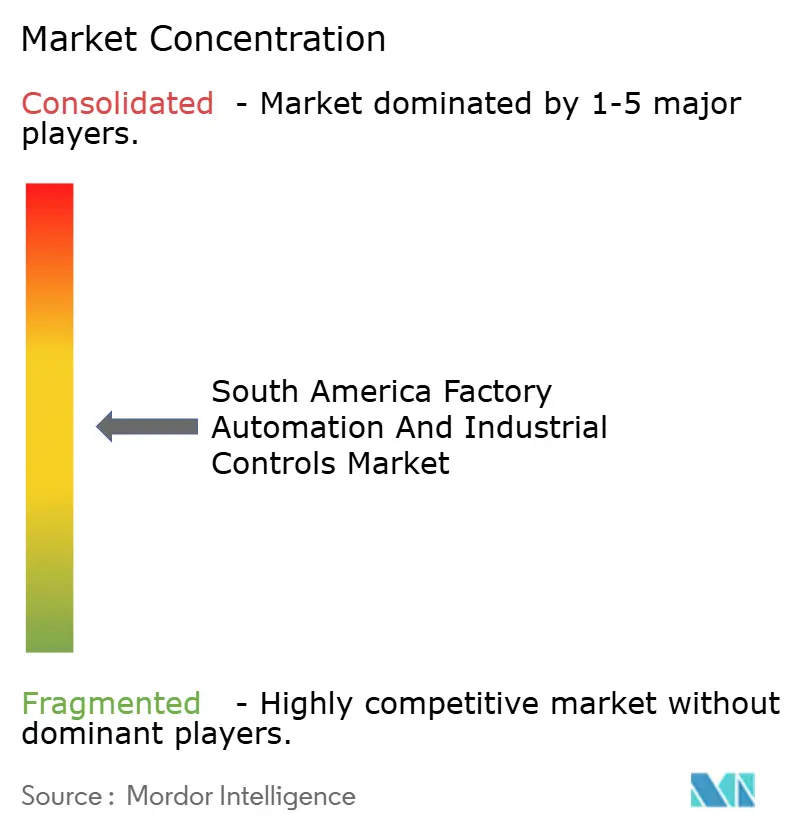

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Factory Automation And Industrial Controls Market Analysis by Mordor Intelligence

The South America Factory Automation And Industrial Controls Market size is expected to grow from USD 19.93 billion in 2025 to USD 21.13 billion in 2026 and is forecast to reach USD 27.52 billion by 2031 at 5.43% CAGR over 2026-2031.

Currency volatility and capital-expenditure caution among small and medium enterprises (SMEs) are muting headline growth, yet federal smart-factory grants in Brazil, rising near-shoring flows into Mexico, and export-driven pharmaceutical upgrades in Argentina are creating pockets of double-digit outlays. Vendors are pivoting from one-time hardware sales to outcome-based contracts that bundle predictive maintenance, managed cybersecurity, and remote commissioning. Cloud-native analytics and low-code orchestration are lowering the payback horizon for brownfield retrofits, while abundant renewable electricity in Brazil is attracting energy-intensive metals, pulp, and data-center projects that embed advanced process control from day one. Moderate competitive intensity, with the top five suppliers holding roughly 40% share, leaves room for regional specialists to win sector-specific deals in pulp-and-paper, mining, and chemicals.

Key Report Takeaways

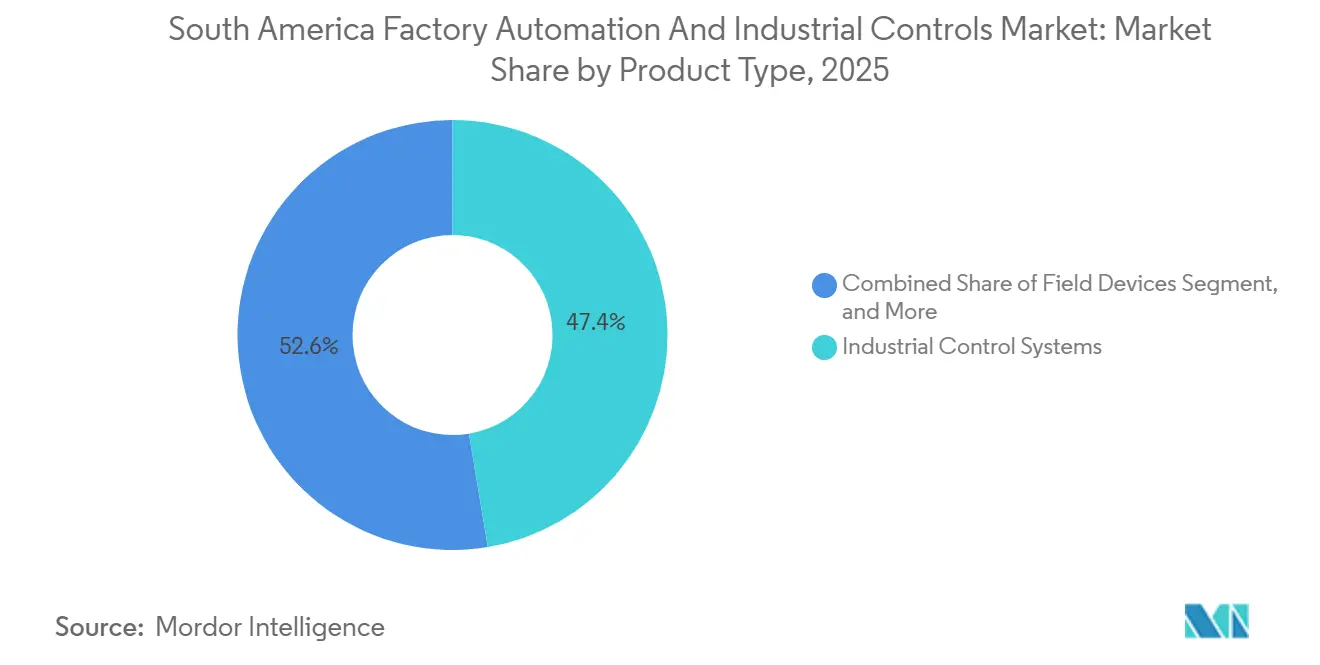

- By product type, industrial control systems led with 47.38% revenue share in 2025, while software platforms are forecast to expand at a 7.32% CAGR through 2031.

- By component type, hardware accounted for 61.27% of 2025 spending, whereas services are projected to grow at an 8.07% CAGR to 2031.

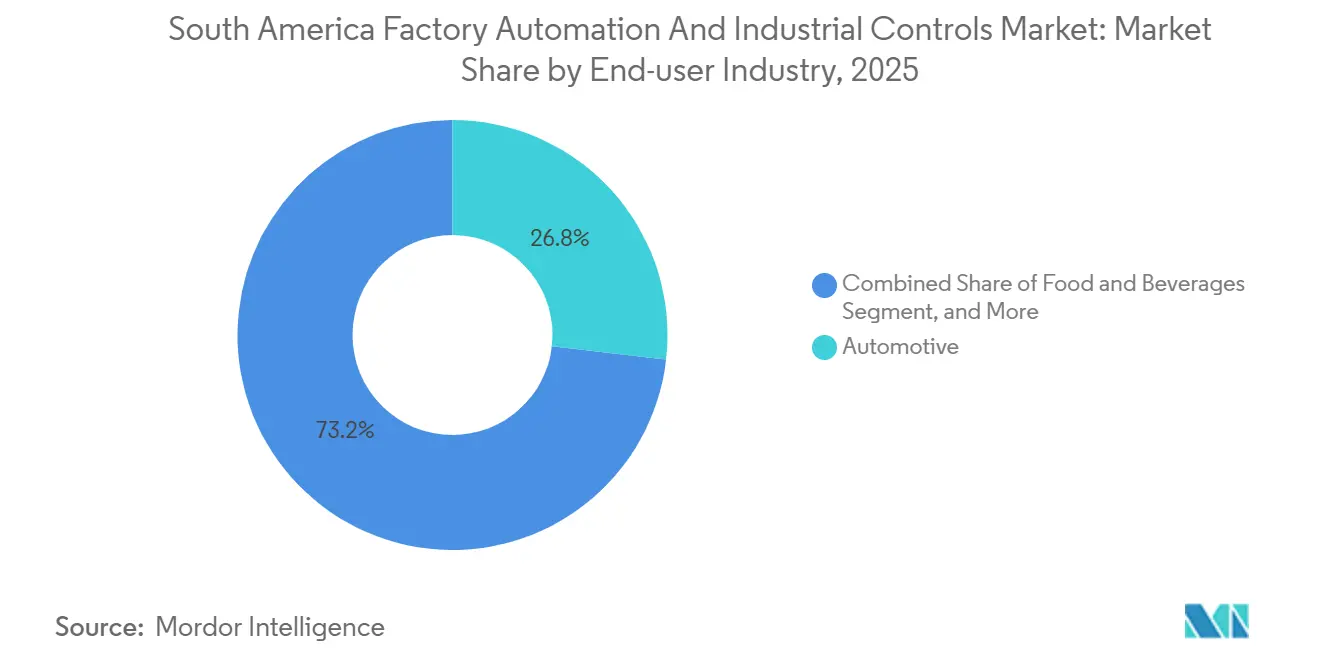

- By end-user industry, automotive commanded a 26.81% share in 2025, yet pharmaceutical manufacturing is advancing at a 6.79% CAGR to 2031.

- By deployment mode, on-premise installations held 67.53% outlay in 2025, while cloud solutions are surging at a 9.64% CAGR through 2031.

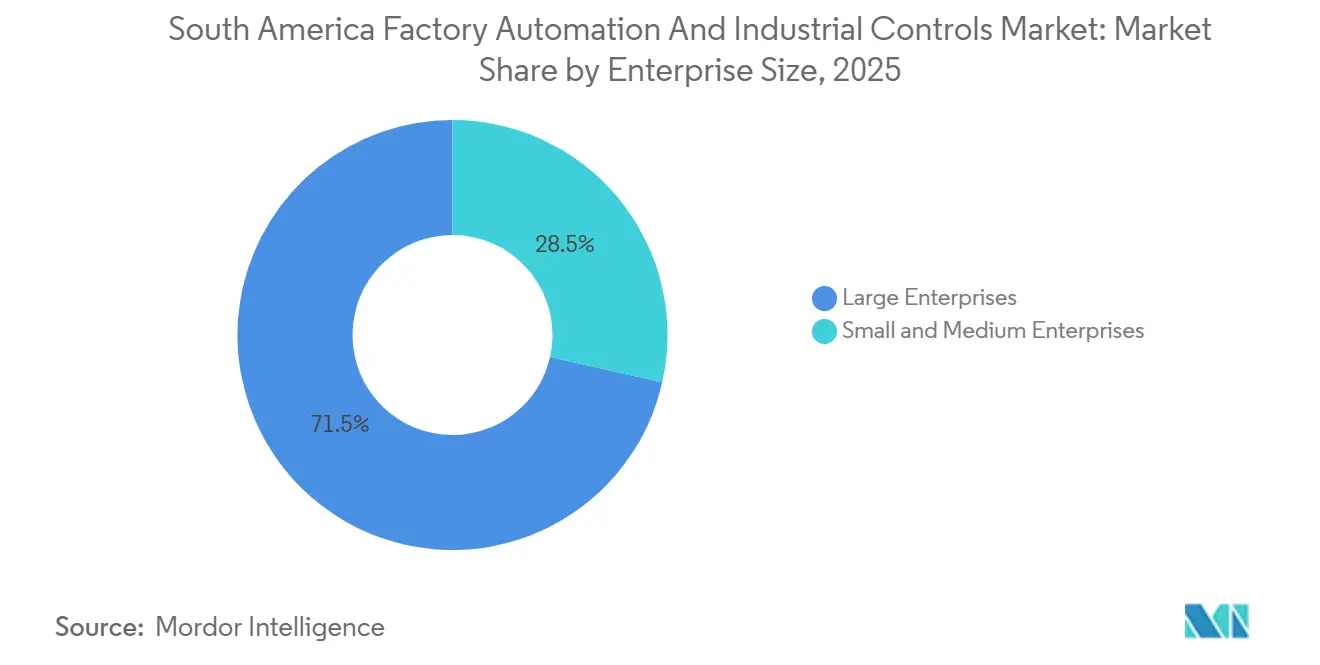

- By enterprise size, large enterprises controlled 71.46% spending in 2025, but SMEs are expanding at a 7.86% CAGR between 2026-2031.

- By country, Brazil secured 38.92% revenue in 2025, whereas Argentina is set to grow fastest at a 6.54% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Factory Automation And Industrial Controls Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Adoption of Industry 4.0 and IIoT Ecosystems | +1.2% | Brazil, Mexico, Argentina, Chile | Medium term (2-4 years) |

| Government Incentives Accelerating Smart-Factory Investments | +1.5% | Brazil, Argentina, Colombia | Short term (≤ 2 years) |

| Cost-Pressure and Productivity Optimisation Mandates | +0.9% | Brazil and Mexico | Long term (≥ 4 years) |

| Renewable-Power Advantages Attracting Powershoring to Brazil | +0.6% | Brazil, Uruguay | Long term (≥ 4 years) |

| Near-Shoring and Maquiladora Expansion Increasing Automation in Mexico | +0.8% | Mexico | Medium term (2-4 years) |

| AI-Enabled Digital Twin Pilots Accelerating Brownfield Optimisation | +0.7% | Brazil, Mexico, Chile | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Industry 4.0 and IIoT Ecosystems

Manufacturers are rolling out sensor networks, edge gateways, and cloud dashboards to close the visibility gap between shop-floor equipment and enterprise systems. Brazil’s National IoT Plan subsidized connectivity hardware across 70 industrial parks in 2024, enabling real-time overall-equipment-effectiveness tracking. Mexico’s tier-1 automotive suppliers added more than 12,000 IIoT endpoints during 2025 to satisfy just-in-time traceability rules. Argentina’s pharmaceutical exporters deployed cold-chain sensors that meet World Health Organization pre-qualification, preventing batch losses after USD 22 million in temperature excursions during 2024.[1]World Health Organization, “Cold-Chain Compliance Standards,” WHO.INT Chile’s Codelco piloted low-latency wireless links for autonomous haulage, boosting ore recovery by 14% at El Teniente in 2025. These projects are accelerating demand for industrial Ethernet, 5G private networks, and edge compute that keep latency under ten milliseconds.

Government Incentives Accelerating Smart-Factory Investments

Tax credits, subsidized loans, and accelerated depreciation are compressing payback periods. Brazil’s Nova Industria Brasil program earmarked BRL 300 billion (USD 60 billion) from 2024-2027, covering up to 40% of eligible automation spend. Argentina cut depreciation on control hardware to three tax years, unlocking USD 180 million in PLC and MES purchases during 2025. Colombia’s Bancóldex extended USD 120 million in 4% loans for Industry 4.0 projects in 2025. Mexico’s USMCA compliance rules now tie maquiladora tax benefits to proof of regional value content tracked by serialized HMI data. Such incentives are front-loading demand despite macro volatility.

Cost-Pressure and Productivity Optimization Mandates

Industrial wages in Brazil rose 8.2% in 2025, squeezing margins and triggering investments in robotics and variable-frequency drives that reduce energy use by up to 14% per finished unit. Mexican automakers faced a 12% electricity tariff hike, prompting energy-management system rollouts that shaved nine to fourteen percent off consumption per vehicle. Argentine food processors deployed robotic palletizers and automated guided vehicles to cut headcount by 22%, achieving payback in 16 months. Chilean copper smelters introduced AI-driven furnace controls that lifted metal recovery 3.5% and cut energy intensity 7%. Continuous cost pressure is thus accelerating automation adoption across discrete and process industries.

Renewable-Power Advantages Attracting Power shoring to Brazil

Hydroelectric, wind, and solar assets deliver industrial power at USD 0.06-0.08 per kWh, roughly one-third below fossil-based grids in Europe and North America. Norsk Hydro committed USD 370 million to expand an aluminum smelter in Pará during 2025, citing low-carbon power availability.[2]Norsk Hydro, “Pará Smelter Expansion,” HYDRO.COM ThyssenKrupp retrofitted Rio-based steel mills with real-time energy optimization, reducing per-ton consumption by 8%. Pulp-and-paper facilities now integrate predictive maintenance to hedge hydropower seasonality. The power advantage is also drawing hyperscale data centers that co-locate industrial AI workloads, reinforcing demand for edge automation hardware.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Capex and ROI Uncertainty for SMEs | -0.8% | Argentina, Colombia, Brazil | Short term (≤ 2 years) |

| Severe Skilled-Labour Shortage for Advanced Automation Roles | -0.6% | Brazil and Mexico | Long term (≥ 4 years) |

| Local-Currency Volatility Causing Investment Deferral | -0.7% | Argentina, Brazil | Medium term (2-4 years) |

| Rising Cyber-Physical Attacks on Industrial Control Systems | -0.4% | Brazil, Mexico, Chile | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capex and ROI Uncertainty for SMEs

SMEs supply 65% of manufacturing jobs yet account for only 28% of automation spend. Textile mills in Argentina postponed USD 95 million in PLC and vision upgrades during 2025 as peso depreciation distorted payback models.[3]Financial Times, “SME Capex Deferrals in Argentina,” FT.COM Vendors are countering with starter kits priced below USD 50,000 that bundle compact PLCs, HMIs, and six-month analytics subscriptions. Colombia’s Bancóldex loans remain under-drawn because borrowers lack integration talent. Pay-per-use robotics in Mexican maquiladoras are easing balance-sheet stress, but contract complexity still deters late adopters.

Severe Skilled-Labor Shortage for Advanced Automation Roles

The region lacks about 85,000 qualified automation engineers. Brazil’s SENAI institutes graduated 12,400 technicians in 2025, only one-third of market demand.[4]SENAI, “Automation Technician Supply-Demand Gap,” SENAI.BR Mexican automotive suppliers report 22% vacancy for robotics technicians, prompting creation of in-house academies. Argentine pharma companies collaborated with Universidad Tecnológica Nacional on a master’s program in MES but the first cohort will not finish until 2027. Skills gaps raise project timelines and integration costs, tempering rollout velocity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Software Platforms Accelerate While Controls Retain Scale

Industrial control systems accounted for 47.38% of the South America factory automation and industrial controls market share in 2025, anchoring large process plants. Yet software platforms are on course for a 7.32% CAGR and are projected to capture an expanded slice of the South America factory automation and industrial controls market size by 2031. Vendors are packaging low-code IIoT hubs, AI-driven predictive maintenance, and mobile HMIs that retrofit installed PLCs instead of replacing them. Machine-vision demand is climbing in automotive and pharmaceutical lines where zero-defect mandates prevail. Edge-ready 5G cores tested in Brazilian and Mexican factories during 2025 prove sub-ten-millisecond loop times, encouraging latency-sensitive closed-loop deployments.

Distributed control system incumbents, including Emerson’s DeltaV and Honeywell’s Experion, still dominate oil, gas, and chemicals but now offer modular configurations with 40% fewer engineering hours. PLC environments are migrating toward IEC 61131-3 compliance, easing cross-vendor code portability. MES and product lifecycle tools are merging, giving line engineers end-to-end digital threads. Mobile augmented-reality headsets that overlay maintenance steps are reducing mean-time-to-repair, especially in remote mines. As a result, the South America factory automation and industrial controls market is witnessing a shift in revenue mix from hardware to digital platforms without cannibalizing the core control install base.

By Component Type: Services Capture Recurring Wallet Share

Hardware represented 61.27% of 2025 revenue, yet replacement cycles are stretching from seven to ten years as predictive maintenance becomes mainstream. Services, however, are expanding at 8.07% CAGR, reflecting the appetite for remote diagnostics, cybersecurity patches, and performance guarantees that peg vendor revenue to asset uptime. The South America factory automation and industrial controls market size linked to services is widening as OEMs rebundle training, firmware, and analytics into subscription tiers.

ABB, Schneider Electric, and Siemens each added more than 1,200 regional service subscribers in 2025, while integrators such as Festo launched automation-as-a-service for SMEs, charging throughput-indexed fees that remove capex hurdles. Managed detection and response for operational-technology networks is emerging as its own category, spurred by a 47% rise in ransomware incidents targeting manufacturers during 2024-2025. Training centers in São Paulo and Mexico City graduated over 3,500 technicians last year, helping close, but not yet eliminate, the skills gap.

By End-User Industry: Pharmaceuticals Lead Growth While Automotive Dominates Scale

Automotive plants held 26.81% revenue in 2025, driven by Brazil’s 2.3 million vehicle output and Mexico’s 3.8 million units. Nonetheless, pharmaceutical facilities are on track for a 6.79% CAGR, the highest among verticals in the South America factory automation and industrial controls industry, as serialization and cold-chain traceability become mandatory for export to the United States and Europe. Food and beverages, chemicals, and oil and gas each account for 10-14% share, underpinned by hygiene, safety, and yield mandates.

Argentina’s exporters invested USD 240 million in MES and track-and-trace systems across 2024-2025. Electronics assemblers in Mexico deployed more than 3,200 industrial robots in 2025 to hit sub-50-ppm defect thresholds demanded by global brands, highlighting discrete manufacturing’s capital intensity. Mining automation in Chile and Peru showcases autonomous haulage and tele-remote drilling, while pulp-and-paper mills in Brazil apply advanced process control to reduce fiber use.

By Deployment Mode: Hybrid Wins the Pragmatic Middle Ground

On-premise installations retained 67.53% of spending in 2025 because deterministic latency and intellectual-property concerns keep core control loops local. Cloud subscriptions, though, are growing at 9.64% CAGR as manufacturers move historians, analytics, and digital twins to hyperscale platforms. The South America factory automation and industrial controls market now sees hybrid topologies dominate, marrying plant-floor reliability with cloud elasticity.

Sixty-two percent of EcoStruxure and MindSphere sign-ups in 2025 were hybrid, not pure cloud. Automotive suppliers in Brazil cut finished-goods inventory by 19% by synchronizing cloud-based scheduling with on-premise PLC logic. Cloud-native MES in Argentina slashed compliance costs 28% by enabling remote audit access. Remote commissioning via over-the-air firmware is shaving four to six weeks off project timelines, a tangible win during technician shortages.

By Enterprise Size: SMEs Close the Productivity Gap

Large corporations still generated 71.46% of 2025 revenue, yet SME outlays are expanding at 7.86% CAGR, above the South America factory automation and industrial controls market average. Modular starter kits priced under USD 8,000 per line, paired with twelve-month analytics subscriptions, are delivering 11-16% throughput gains for small food processors in Argentina. Leasing models for collaborative robots, pioneered in Colombia and Mexico, transfer obsolescence risk to vendors and align cash flow with output.

Brazil’s SEBRAE agency offered grants covering 40% of equipment and training, catalyzing 200 SME projects in 2025. Consortium buying among Argentine pharma SMEs lowered MES license fees 34%, proving that scale advantages can be shared. Although large enterprises are channeling budgets into AI and digital twins, SME momentum keeps the overall South America factory automation and industrial controls market on its steady 5.43% CAGR path.

Geography Analysis

Brazil captured 38.92% of the South America factory automation and industrial controls market in 2025 thanks to its diversified base across automotive, food processing, mining, and pulp. Abundant hydro and growing wind-solar fleets keep industrial power at USD 0.06-0.08 per kWh, luring aluminum smelters and steel rerollers that deploy advanced process control to shift loads during peak generation. Nova Industria Brasil funnels BRL 300 billion (USD 60 billion) into modernization grants through 2027, spurring PLC and MES orders nationwide. BYD, Stellantis, and GM each outfitted electric-vehicle lines with collaborative robots and AGVs during 2025, while pulp mills retrofitted digesters with AI controllers that trim fiber use 4%.

Argentina is the fastest climber, set for a 6.54% CAGR from 2026-2031 despite peso volatility. USD 240 million flowed into track-and-trace and cold-chain platforms that unlock USD 1.8 billion in pharma exports. Lithium-brine miners in Catamarca and Jujuy are automating extraction units, a move expected to triple output by 2028. Accelerated depreciation rules, introduced in 2024, cut tax recovery from seven to three years, igniting PLC sales across food and textiles.

Mexico held about 32% share in 2025, anchored in the maquiladora corridor. Near-shoring added USD 1.2 billion in automation capex during 2024-2025 as OEMs race to comply with USMCA regional content ratios. Electronics assemblers installed over 3,200 robots last year, while Schneider Electric opened a USD 65 million competency center in Monterrey that graduated 1,200 technicians. Chile’s mining complexes and Colombia’s refineries continue to adopt remote-operations centers, whereas Uruguay and Paraguay remain nascent but show early interest in grid-automation pilots.

Competitive Landscape

The South America factory automation and industrial controls market is moderately concentrated; Siemens, ABB, Rockwell Automation, Schneider Electric, and Emerson control roughly 40% of 2025 revenue. Their strategies converge on three pillars: multi-layer platform ecosystems, service-heavy revenue models, and modular hardware that lowers SME entry barriers. Siemens’ Xcelerator and Schneider Electric’s EcoStruxure each added more than 1,200 new regional subscribers in 2025, bundling edge gateways with AI-driven analytics. Rockwell and Emerson now derive 38% of regional turnover from multi-year service contracts that guarantee uptime, insulating cash flow from hardware replacement cycles.

Regional challengers are carving niches. Brazil-based WEG Industrias bundled variable-frequency drives with Schneider PLCs and proprietary energy dashboards to capture 9% domestic share, pricing 18-22% below multinationals. Low-code application vendors Mendix and OutSystems enable plant engineers to build custom HMIs in days rather than weeks, eroding integrator margins. Cybersecurity differentiation is sharpening: Honeywell and Fortinet launched managed detection and response tailored for operational technology, reacting to a 47% rise in ransomware incidents in 2024-2025.

Patent filings in edge compute and digital twins jumped 34% in 2024 as Mitsubishi Electric and Yokogawa submitted designs that partition AI inference between plant and cloud to honor data-sovereignty rules. Mergers remain selective; vendors prefer joint ventures and co-innovation labs that de-risk R&D while preserving capital. The resulting competitive field provides customers with choice across price points, support models, and technology road maps, sustaining the South America factory automation and industrial controls market’s steady expansion.

South America Factory Automation And Industrial Controls Industry Leaders

Siemens AG

ABB Ltd

Rockwell Automation Inc.

Schneider Electric SE

Emerson Electric Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Siemens commissioned a USD 180 million digital-factory showcase in São Paulo, integrating Xcelerator, edge computing, and AI predictive maintenance suites.

- December 2025: ABB secured a USD 95 million robotics and AGV contract for BYD’s EV plant in Bahia, Brazil.

- November 2025: Rockwell Automation partnered with Embraer on FactoryTalk analytics and digital twins at the São José dos Campos aircraft plant.

- October 2025: Schneider Electric opened a USD 65 million automation competency center in Monterrey, Mexico, graduating 1,200 technicians in six months.

South America Factory Automation And Industrial Controls Market Report Scope

The South America Factory Automation and Industrial Controls Market Report is Segmented by Product Type (Industrial Control Systems, Field Devices, Automation Software Platforms, and Connectivity and Networking), Component Type (Hardware, Software, and Services), End-user Industry (Automotive, Food and Beverages, Oil and Gas, Chemical and Petrochemical, Power and Utilities, Pharmaceutical, Electronics and Electrical, Mining and Metals, Pulp and Paper, and Other End-user Industries), Deployment Mode (On-premise, Cloud, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), and Geography (Brazil, Mexico, Argentina, Chile, Colombia, and Rest of South America). The Market Forecasts are Provided in Terms of Value (USD).

| Industrial Control Systems | Distributed Control System (DCS) |

| Programmable Logic Controller (PLC) | |

| Supervisory Control and Data Acquisition (SCADA) | |

| Manufacturing Execution System (MES) | |

| Product Lifecycle Management (PLM) | |

| Human Machine Interface (HMI) | |

| Enterprise Resource Planning (ERP) | |

| Field Devices | Machine Vision |

| Industrial Robotics | |

| Sensors and Transmitters | |

| Motors and Drives | |

| Relays and Switches | |

| Automation Software Platforms | Edge and Cloud IIoT Platforms |

| AI-Powered Predictive Maintenance Suites | |

| Low-Code Industrial Apps | |

| Connectivity and Networking | Industrial Ethernet |

| 5G Private Networks | |

| Wireless Sensor Networks |

| Hardware |

| Software |

| Services |

| Automotive |

| Food and Beverages |

| Oil and Gas |

| Chemical and Petrochemical |

| Power and Utilities |

| Pharmaceutical |

| Electronics and Electrical |

| Mining and Metals |

| Pulp and Paper |

| Other End-user Industries |

| On-premise |

| Cloud |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Brazil |

| Mexico |

| Argentina |

| Chile |

| Colombia |

| Rest of South America |

| By Product Type | Industrial Control Systems | Distributed Control System (DCS) |

| Programmable Logic Controller (PLC) | ||

| Supervisory Control and Data Acquisition (SCADA) | ||

| Manufacturing Execution System (MES) | ||

| Product Lifecycle Management (PLM) | ||

| Human Machine Interface (HMI) | ||

| Enterprise Resource Planning (ERP) | ||

| Field Devices | Machine Vision | |

| Industrial Robotics | ||

| Sensors and Transmitters | ||

| Motors and Drives | ||

| Relays and Switches | ||

| Automation Software Platforms | Edge and Cloud IIoT Platforms | |

| AI-Powered Predictive Maintenance Suites | ||

| Low-Code Industrial Apps | ||

| Connectivity and Networking | Industrial Ethernet | |

| 5G Private Networks | ||

| Wireless Sensor Networks | ||

| By Component Type | Hardware | |

| Software | ||

| Services | ||

| By End-user Industry | Automotive | |

| Food and Beverages | ||

| Oil and Gas | ||

| Chemical and Petrochemical | ||

| Power and Utilities | ||

| Pharmaceutical | ||

| Electronics and Electrical | ||

| Mining and Metals | ||

| Pulp and Paper | ||

| Other End-user Industries | ||

| By Deployment Mode | On-premise | |

| Cloud | ||

| Hybrid | ||

| By Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| By Country | Brazil | |

| Mexico | ||

| Argentina | ||

| Chile | ||

| Colombia | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the forecast value of the South America factory automation and industrial controls market by 2031?

It is projected to reach USD 27.52 billion, reflecting a 5.43% CAGR from 2026-2031.

Which country is growing the fastest in factory automation across South America?

Argentina is forecast to expand at a 6.54% CAGR, driven by pharmaceutical exports and lithium-mining automation.

Which end-user segment shows the highest growth momentum?

Pharmaceutical manufacturing leads with a 6.79% CAGR through 2031 as export regulations demand serialization and cold-chain traceability.

How are SMEs financing automation investments?

SMEs increasingly use starter kits, vendor leases, and pay-per-use robotics that shift spending from capex to opex, shortening payback to under 18 months.

Why are hybrid deployment models gaining popularity?

Hybrid architectures keep latency-sensitive control loops on-premise while moving analytics and digital twins to the cloud, blending reliability with scalability.

What role do services play in revenue growth?

Managed maintenance, cybersecurity, and remote diagnostics are expanding at 8.07% CAGR and now represent a growing slice of recurring vendor income.

Page last updated on: