Silver Iodide Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

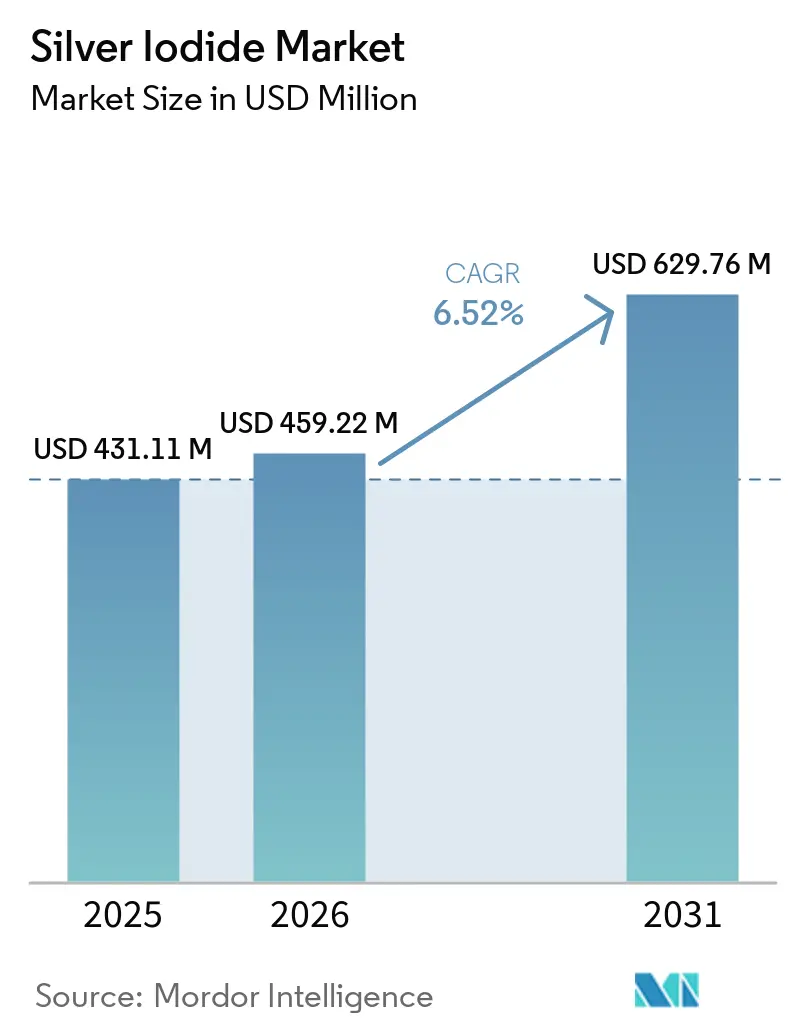

| Market Size (2026) | USD 459.22 Million |

| Market Size (2031) | USD 629.76 Million |

| Growth Rate (2026 - 2031) | 6.52% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Silver Iodide Market Analysis by Mordor Intelligence

The silver iodide market size is projected to be USD 431.11 million in 2025, USD 459.22 million in 2026, and reach USD 629.76 million by 2031, growing at a CAGR of 6.52% from 2026 to 2031. Demand widens as arid governments escalate cloud-seeding flights, hospitals specify AgI antimicrobial coatings, and semiconductor fabs evaluate AgI memristors for neuromorphic logic. The silver iodide market benefits from TU Wien’s 2025 atomic-scale study that validated AgI ice-nucleation, easing regulatory approvals. Premium crystalline grades capture price premiums because their lattice closely matches hexagonal ice, while colloidal grades gain traction in sensor inks. Moderate supplier concentration and a 200-fold purity-price spread allow regional chemists to coexist with multinationals even as input volatility in silver and iodine constraints keep margins under pressure.

Key Report Takeaways

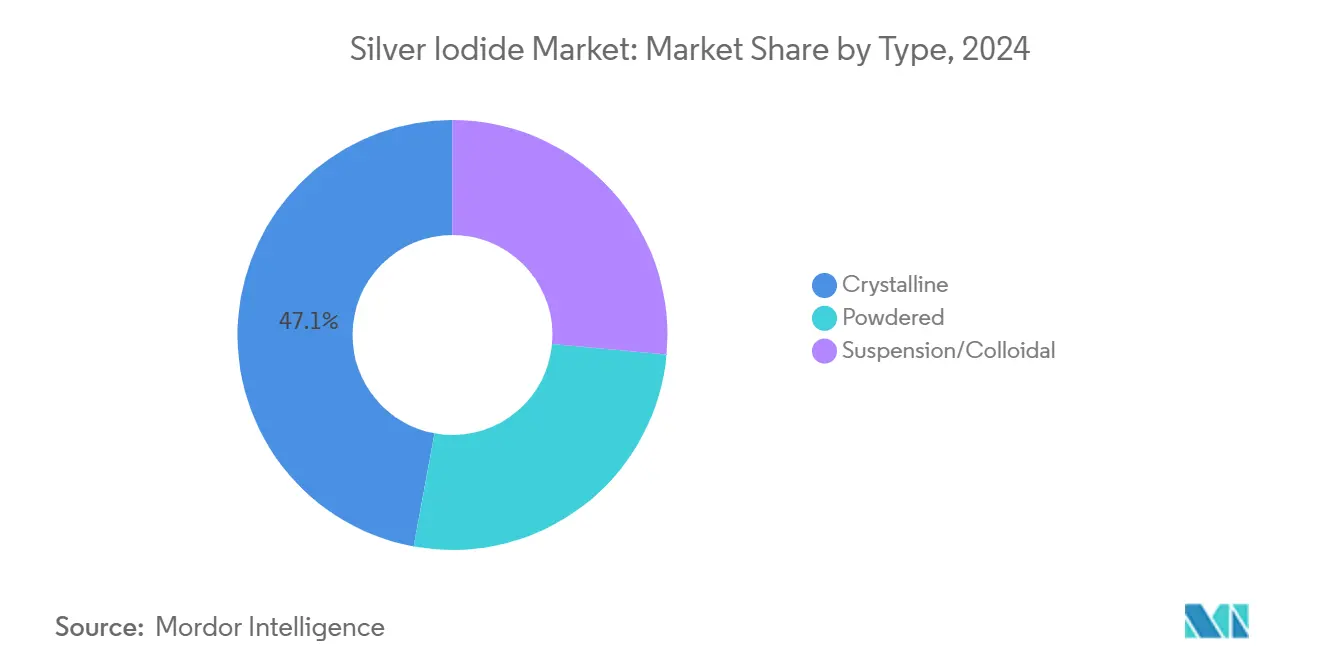

- By type, crystalline compounds led with 47.11% of the silver iodide market share in 2025, while suspension/colloidal variants are projected to expand at a 7.68% CAGR through 2031.

- By application, cloud seeding retained a 42.69% revenue share in 2025; electro-chemical and sensor uses are forecast to register the fastest 7.83% CAGR to 2031.

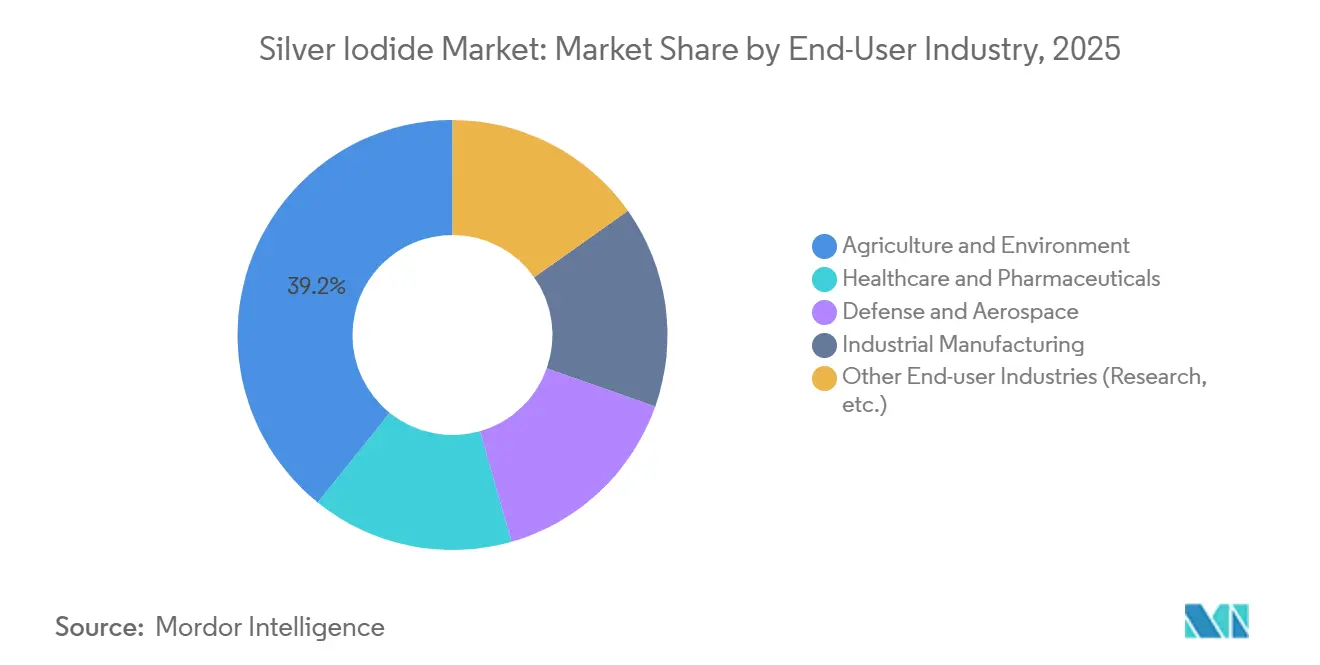

- By end-user industry, agriculture and environment commanded 39.22% of the 2025 revenue pool, whereas defense and aerospace are poised to grow at a 7.94% CAGR through 203.

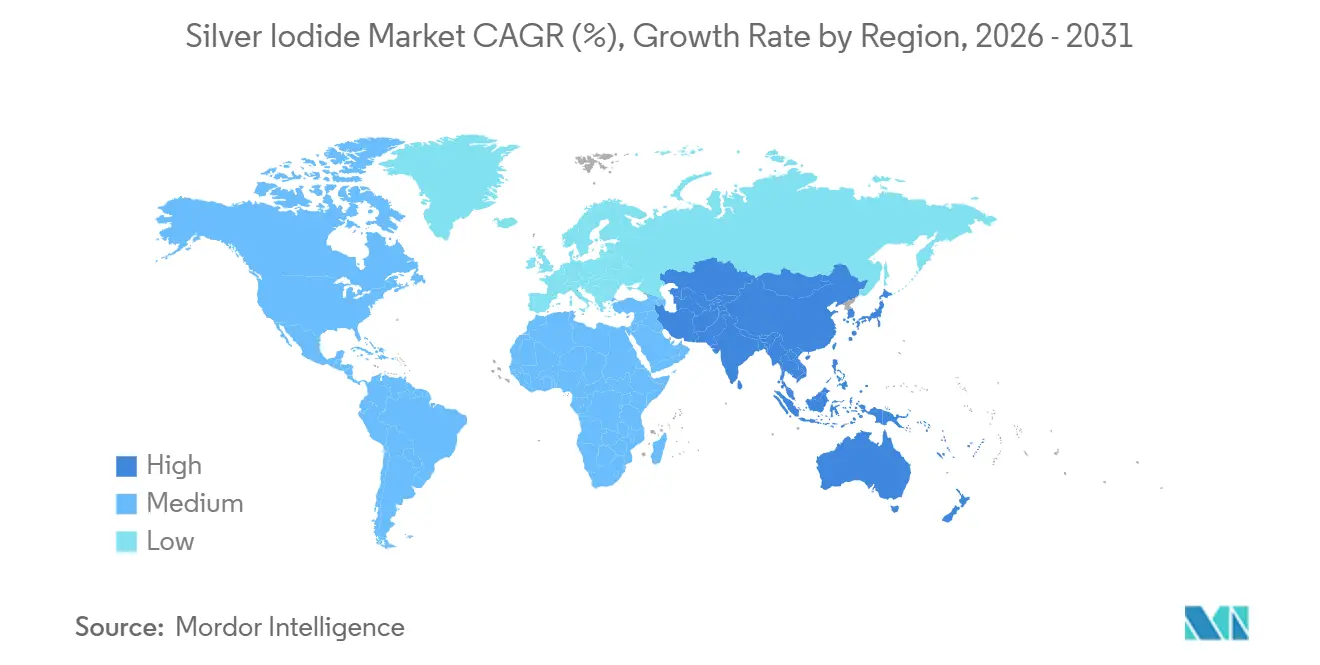

- By geography, Asia-Pacific contributed 37.15% to global revenue in 2025 and is expected to advance at a leading 7.76% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Silver Iodide Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand for antimicrobial and antiseptic coatings | +1.2% | Global, concentrated in North America, Europe, APAC | Medium term (2-4 years) |

| Expansion of silver-iodide-based sensors in industrial IoT | +1.0% | APAC core, spill-over to North America, Europe | Medium term (2-4 years) |

| Renewed use in analogue and instant-film photography | +0.7% | North America, Europe, Japan | Short term (≤2 years) |

| Tailored AgI nanoparticles for neuromorphic and memristor devices | +0.8% | APAC, North America | Long term (≥4 years) |

| Breakthrough integration in perovskite and thin-film PV cells | +0.7% | Global, with early adoption in China, Europe, the Middle East | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for Antimicrobial and Antiseptic Coatings

Hospital systems are adopting silver iodide (AgI)-based surface films, which release ions for 6-12 months, to manage infection costs. These films have a longer functional lifespan compared to colloidal silver[1]Malik et al., “Gelatinous silver iodide composite antimicrobial coatings,” pubmed.ncbi.nlm.nih.gov. Silver iodide coatings have met the International Organization for Standardization (ISO) 10993 cytotoxicity thresholds and comply with the European Union Medical Device Regulation (EU MDR). Procurement increased after the United States Food and Drug Administration (US FDA) implemented stricter aseptic guidance in 2024. Consequently, the silver iodide market is experiencing consistent demand, particularly from retrofit programs in operating rooms. Suppliers report a 25-30% reduction in infection rates to support premium pricing.

Expansion of Silver-Iodide-Based Sensors in Industrial IoT

Graphene layers integrated with AgI nanocrystals detect iodine vapor at 0.5 parts per million (ppm) with millisecond response time while consuming 40% less power compared to metal-oxide sensors. Japan and South Korea have included halogen sensing in their 2025 smart-factory roadmaps. Wind-farm operators are adopting battery nodes with these sensors, contributing to the growth of the silver iodide market in offshore projects. Clinical groups are utilizing AgI electrodes for non-invasive urinary iodine tests, expanding the application in the healthcare sector. Furthermore, the integration of these sensors into 5G gateways is driving demand for colloidal precursors.

Renewed Use in Analogue and Instant-Film Photography

Fujifilm Instax sold over 10 million cameras in 2025 as millennials pursued tactile imagery. Polaroid’s relaunch fuels artisanal demand for silver-halide emulsions, where silver iodide provides speed and archival stability. Wet-plate collodion studios order photographic-grade AgI at USD 150-200 per kilogram, insulating the silver iodide market during economic downturns. Growth, while niche, offers suppliers counter-cyclical revenue and showcases sustainability because instant films are less e-waste-intensive.

Tailored AgI Nanoparticles for Neuromorphic and Memristor Devices

Vertical AgI devices demonstrate six-order resistance ratios, enabling the implementation of multi-bit synaptic weights[2]Advanced Materials, “Single-crystalline AgI nanoflakes,” wiley.com. TSMC and Samsung are testing AgI memristors for 3 nm edge-AI chips, targeting autonomous vehicles that require on-device learning capabilities. Ionic switching operates at less than 1 V, reducing energy consumption by 70% compared to static random-access memory (SRAM) arrays. The silver iodide market is experiencing growth, as memristor purity thresholds exceeding 99.999% are increasing average selling prices. With cycle endurance currently below 1 million writes, material engineers are working on lattice-defect control to address this limitation.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Environmental and ethical opposition to weather-modification trials | -0.5% | North America, Europe | Short term (≤2 years) |

| Rapid progress of bio-based ice-nucleating proteins as substitutes | -0.7% | Global, early in the UAE, Australia, EU | Medium term (2-4 years) |

| High purity AgI feed-stock price volatility and hedging costs | -0.8% | Global, acute in North America, Europe | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Environmental and Ethical Opposition to Weather-Modification Trials

Idaho House Bill 23 proposes a ban on cloud seeding, citing concerns about silver residue deposition in watersheds. Similar legislative discussions are ongoing in Iowa, with non-governmental organizations (NGOs) referencing precautionary principles. Insurance providers are delaying decisions due to the absence of clear liability frameworks, resulting in halted equipment orders. If such bans expand, North American demand could decrease by 15%, affecting the silver iodide market, which represents its largest application. Cloud seeding companies are requesting Environmental Protection Agency (EPA) guidelines to address these concerns and restore market confidence.

Rapid Progress of Bio-Based Ice-Nucleating Proteins as Substitutes

Virginia Tech has isolated fungal ice-nucleating proteins (INPs) that trigger ice formation at temperatures between -4.8°C and -5.9°C. These findings are significant as they align closely with the performance of silver iodide (AgI) while being biodegradable. The UAE has allocated USD 1.5 million to support the refinement of graphene-infused bio-nucleants. Field trials conducted by CSIRO in Tasmania have demonstrated a 10-15% increase in rainfall. If the Environmental Protection Agency (EPA) or the European Chemicals Agency (ECHA) grants expedited approval for these bio-agents, they could account for 25% of cloud seeding expenditure by 2030. This development could impact the silver iodide market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Crystalline Dominance Anchored in Ice-Nucleation Efficacy

Crystalline grades captured 47.11% revenue in 2025 because their lattice parameter of 4.592 angstroms mirrors that of hexagonal ice and lowers the nucleation barrier. Powdered forms occupied 28% and grew steadily among ground-based seeding cooperatives. Suspension and colloidal variants expanded at 7.68%, catalyzed by sensor ink demand.

Crystalline suppliers leverage closed-loop systems to satisfy REACH dossiers, crowding out smaller rivals. Colloidal innovators tap solution-phase routes to engineer nanoflakes for spin-coated memristor stacks. Tokyo Chemical Industry scales 10 g/L suspensions for research and development, while Merck bundles AgI with test-grade acetylene black to create drop-in conductive pastes. These moves diversify revenue while lifting average selling prices, underpinning the silver iodide market.

By Application: Cloud Seeding Anchors Demand, Sensors Surge

In 2025, cloud seeding accounted for 42.69% of the market value, as 30 aircraft and 250 generators from China addressed drought-prone skies. Among various applications, electrochemical and sensor uses led with a 7.83% CAGR, driven by industrial IoT's focus on monitoring iodine leaks and urinary diagnostics. Photography maintains a niche presence, while antimicrobial coatings, holding an 18% market share, are growing alongside hospital retrofits.

Sensor manufacturers utilize colloidal AgI for its capability to spin-coat liquid precursors onto flexible substrates at sub-150°C temperatures, ensuring polymer backplanes remain intact. Seeding companies are developing hybrid flares that combine AgI with potassium perchlorate to enhance plume density. These advancements support the growth of advanced silver iodide formulations while maintaining the stability of traditional segments.

By End-User Industry: Agriculture Leads, Defense Accelerates

Agriculture and environment users accounted for 39.22% sales in 2025 as India budgeted USD 50 million for monsoon seeding. The category is stable yet exposed to bio-agent substitution. Defense and aerospace climb at 7.94% because weather modification re-enters military playbooks amid climate stress. The silver iodide market share held by defense could reach 12% by 2031 if classified programs move from pilot to operational. Healthcare and pharmaceuticals maintain 22% share thanks to stricter infection-control standards.

Industrial manufacturing, covering sensors and semiconductors, follows the overall CAGR as fabs quantify AgI demand for memristor prototypes. Research institutions and academic labs round out demand, safeguarding a baseline for ultra-high-purity suppliers.

Geography Analysis

Asia-Pacific generated 37.15% revenue in 2025 and accelerated at 7.76% through 2031 as China deploys the world’s largest weather-modification network, and Japan scales IoT sensor manufacturing. India’s Infinium Pharmachem adds 500 tons of annual capacity, sharpening regional price competition. South Korea and Taiwan explore AgI memristors for 3 nm processes, potentially adding USD 100 million incremental demand by 2028. ASEAN pilots, though tiny today, may expand if haze-control mandates gain funding.

In 2025, North America demonstrated significant market activity, driven by western U.S. seeding initiatives that enhanced snowpack levels. While legislative resistance in Idaho and Iowa presents challenges, adoption by hospitals and research and development (R&D) entities supports market stability. Canada and Mexico operate sporadic programs, with U.S. laboratories leading in the consumption of ultra-pure AgI for federally backed nanodevice projects.

Europe, led by Germany, the U.K., and France, maintained a strong presence in the market. The stringent REACH registration increases entry barriers and consolidates influence among established players like Merck KGA-MERCK.COM. Although cloud-seeding budgets are limited, the market benefits from advancements in perovskite R&D and antimicrobial applications. Nordic countries are utilizing AgI for offshore wind blade coatings to enhance resistance to salt fog.

South America and the Middle East & Africa regions exhibited notable developments. The UAE conducted numerous missions in 2025, reporting improved rainfall outcomes. Saudi Arabia initiated a national program in 2024, with Morocco exploring similar strategies. Brazil is testing ground-based generators to protect soybean yields, though financial constraints remain a consideration. South Africa is evaluating AgI seeding to support Cape Town's reservoirs. These regions, despite starting from smaller bases, contribute to the growth of the global silver iodide market.

Competitive Landscape

The Silver Iodide market is moderately concentrated. Merck KGaA, Thermo Fisher Scientific, and American Elements lead the market for greater than or equal to 99.99% purity products, which are preferred for their traceability. Regional players such as Infinium Pharmachem and Deep-Water Chemicals supply 99.0-99.5% grades at 20-30% lower prices, primarily targeting agricultural users. Tokyo Chemical Industry supplies research lots globally, while Nanoshel and ESPI Metals are focusing on nanoparticle dispersions for applications like sensor inks.

Silver Iodide Industry Leaders

Merck KGaA

Thermo Fisher Scientific (incl. Alfa Aesar)

American Elements

Deep Water Chemicals

Infinium Pharmachem Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: The United Arab Emirates (UAE) Rain Enhancement Programme allocated USD 1.5 million to three global teams to advance nanocomposite seeding agents, aimed at enhancing the efficiency of silver iodide in weather modification applications.

- February 2025: Researchers at TU Wien have visualized the interactions between Silver Iodide (AgI) lattices and ice, contributing to advancements in cloud seeding technologies and supporting regulatory considerations.

Global Silver Iodide Market Report Scope

Silver iodide (AgI) is a bright yellow, highly photosensitive inorganic solid that darkens upon exposure to light. It is widely used in cloud seeding to induce rain, as a photographic material, and as an antiseptic. Due to its unique structure, it acts as an efficient nucleating agent for ice formation in atmospheric water.

The Silver Iodide market is segmented by type, application, end-use industry, and geography. By type, the market is segmented into crystalline, powdered, and suspension/colloidal. By application type, the market is segmented into cloud seeding, antiseptic and antimicrobial agents, photography and imaging, electrochemical and sensor applications, research and military uses, and other applications (synthesis, coatings). By end-use industry, the market is segmented into agriculture and environment, healthcare and pharmaceuticals, defense and aerospace, industrial manufacturing, and other end-user industries (research, etc.). The report also covers the market size and forecasts for silver iodide in 17 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Crystalline |

| Powdered |

| Suspension/Colloidal |

| Cloud Seeding |

| Antiseptic and Antimicrobial Agents |

| Photography and Imaging |

| Electro-chemical and Sensor Applications |

| Research and Military Uses |

| Other Applications (Synthesis, Coatings) |

| Agriculture and Environment |

| Healthcare and Pharmaceuticals |

| Defense and Aerospace |

| Industrial Manufacturing |

| Other End-user Industries (Research, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Crystalline | |

| Powdered | ||

| Suspension/Colloidal | ||

| By Application | Cloud Seeding | |

| Antiseptic and Antimicrobial Agents | ||

| Photography and Imaging | ||

| Electro-chemical and Sensor Applications | ||

| Research and Military Uses | ||

| Other Applications (Synthesis, Coatings) | ||

| By End-User Industry | Agriculture and Environment | |

| Healthcare and Pharmaceuticals | ||

| Defense and Aerospace | ||

| Industrial Manufacturing | ||

| Other End-user Industries (Research, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current value of the silver iodide market?

It stands at USD 431.11 million for 2025 and is projected to reach USD 629.76 million by 2031.

Which region grows fastest in demand for silver iodide?

Asia-Pacific posts the highest CAGR at 7.76% through 2031 due to large cloud-seeding and sensor manufacturing programs.

How large is cloud seeding within the overall demand?

Cloud seeding represented 42.69% of 2025 revenue, maintaining the largest single application share.

Why are crystalline grades preferred for weather modification?

Their hexagonal lattice nearly matches that of ice, promoting nucleation at warmer cloud temperatures.

Page last updated on: