Silver Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

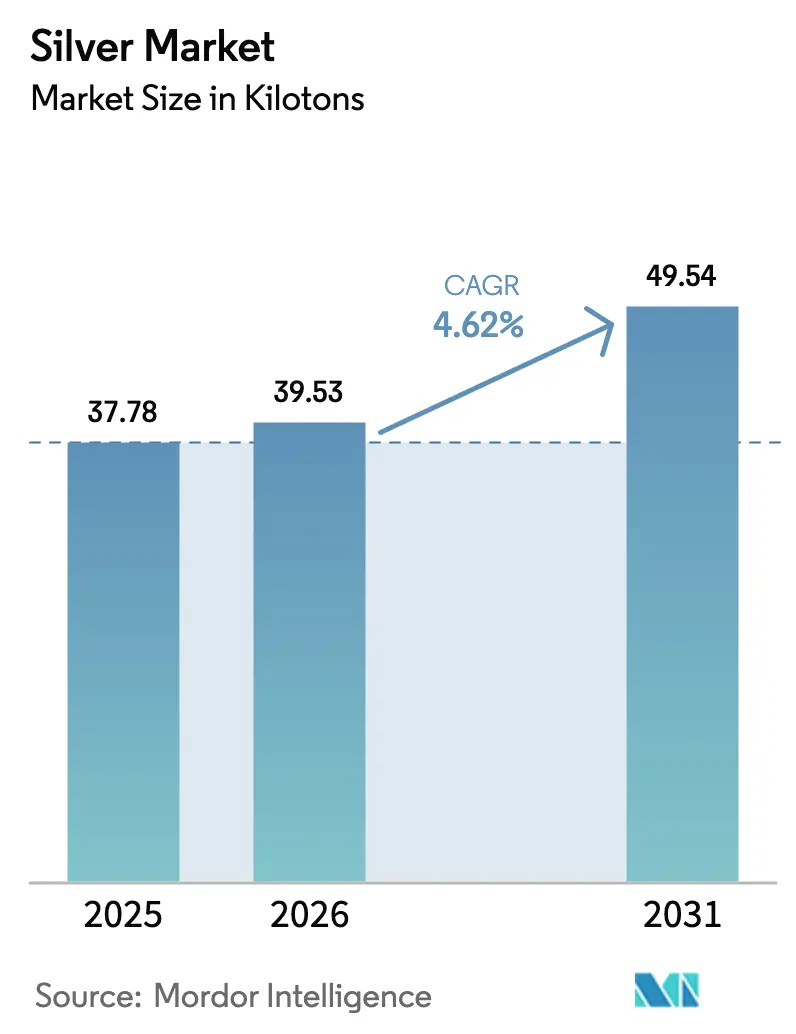

| Market Volume (2026) | 39.53 kilotons |

| Market Volume (2031) | 49.54 kilotons |

| Growth Rate (2026 - 2031) | 4.62% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Silver Market Analysis by Mordor Intelligence

The Silver Market size is expected to grow from 37.78 kilotons in 2025 to 39.53 kilotons in 2026 and is forecast to reach 49.54 kilotons by 2031 at a 4.62% CAGR over 2026-2031. Demand continues to tilt toward industrial fabrication, which already represents a significant portion of total consumption as photovoltaic cell metallization, 5G base-station roll-outs, and high-voltage direct-current (HV-DC) fast-charge connectors together absorbed a considerable amount in 2024. Mexico remained the largest mine producer in 2024, while Peru controls the world’s biggest reserves, equal to a notable share of identified resources. Electronics miniaturization, utility-scale solar additions, and the adoption of silver-based antimicrobial coatings are sustaining a healthy forward orderbook for refined bullion, even as manufacturers aggressively thrift silver loading per photovoltaic cell to protect margins during price spikes. Regulatory tightening on heavy-metal discharge, especially in Latin America, is pushing up compliance costs and extending lead times on new mine approvals, which could constrain fresh supply. At the same time, copper- and aluminum-based substitutes in wiring and PV ribbons are beginning to shave incremental demand, underscoring the delicate balance between technology, cost, and sustainability that will shape the silver market during the next decade.

Key Report Takeaways

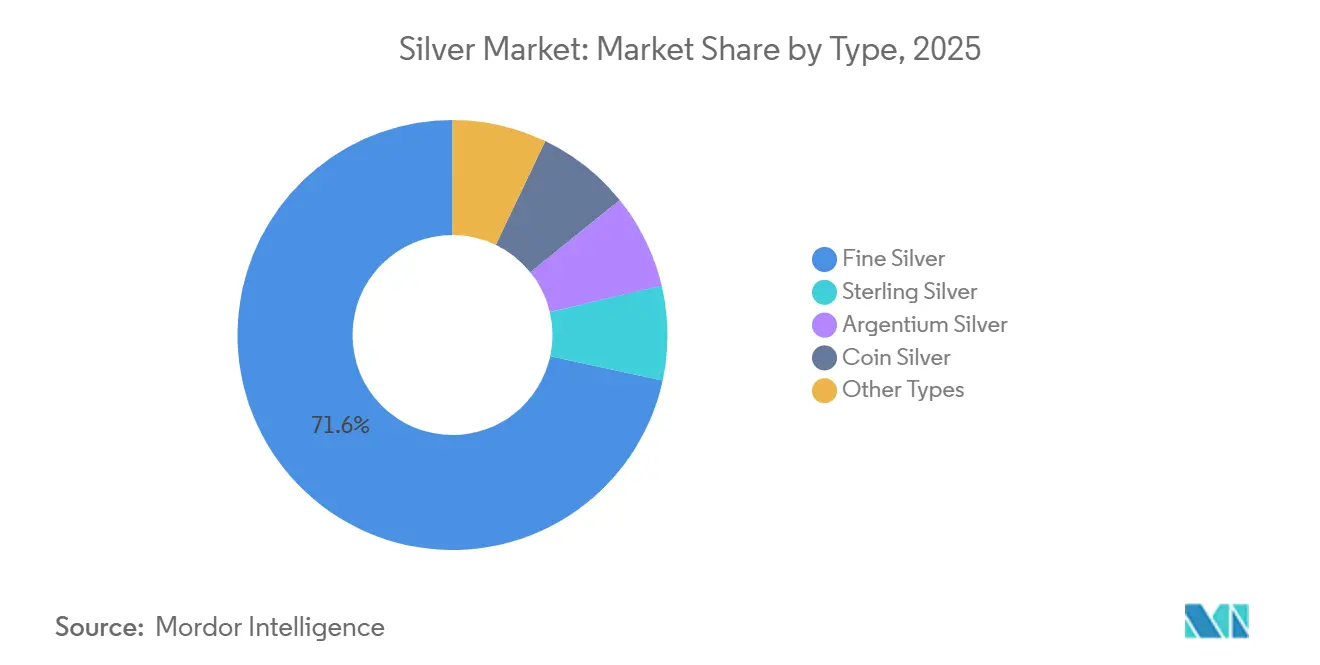

- By type, fine silver led with 71.62% of silver market share in 2025, while argentium silver is forecast to expand at 4.74% CAGR through 2031.

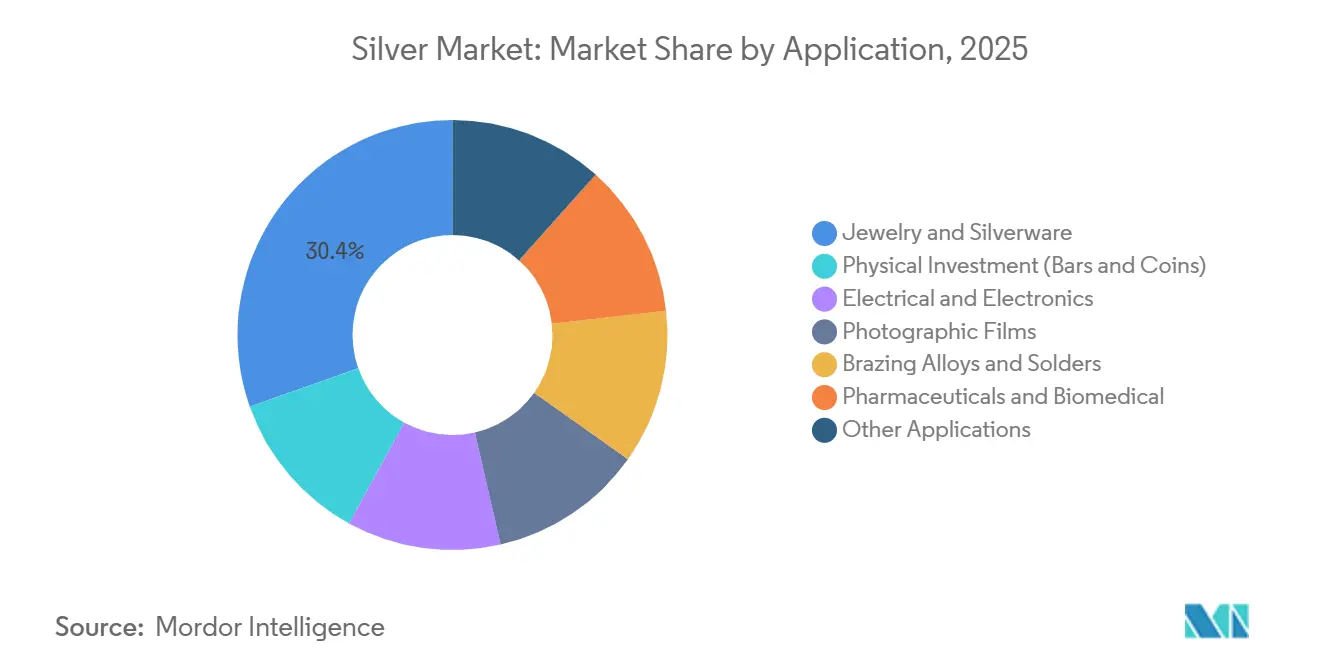

- By application, jewelry and silverware captured 30.41% of the silver market size in 2025, whereas electrical and electronics are projected to advance at a 4.65% CAGR between 2026 and 2031.

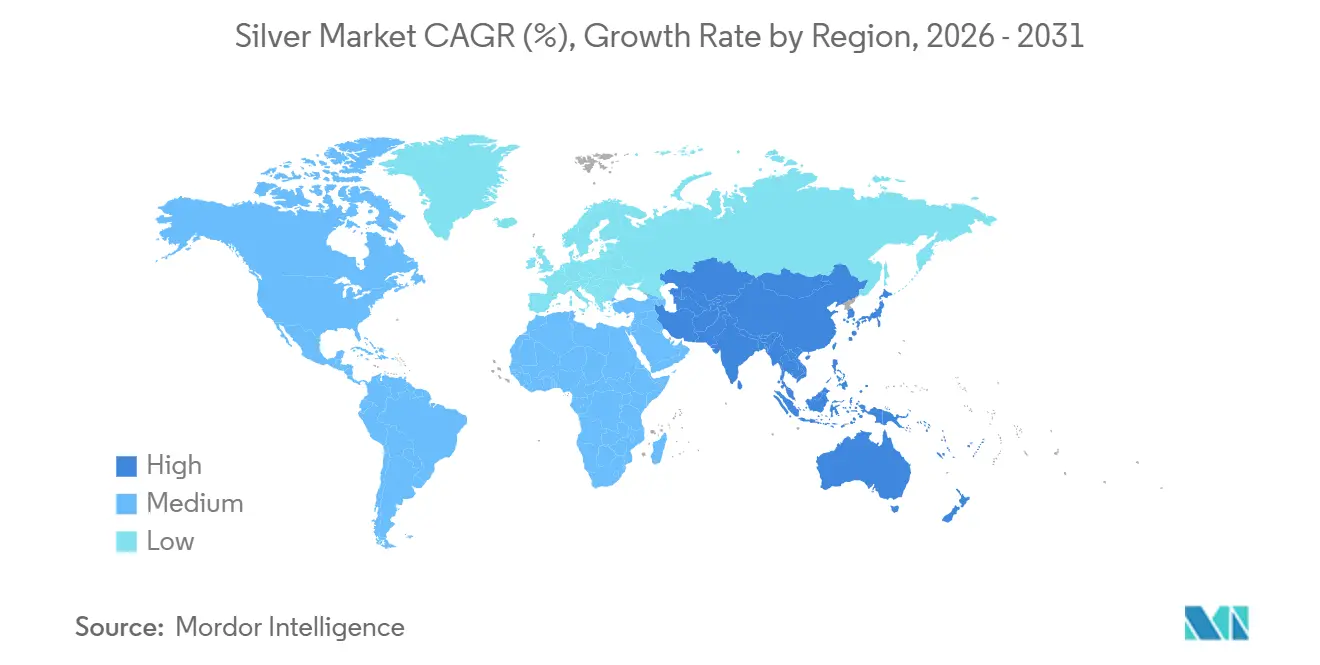

- By geography, Asia-Pacific commanded 57.44% of global consumption in 2025, and is expected to post the fastest growth at 4.91% CAGR during the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Silver Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electronics miniaturisation and 5G component demand | +1.2% | Global, concentrated in Asia-Pacific and North America | Medium term (2-4 years) |

| Utility-scale photovoltaic (PV) build-out | +1.8% | Global, led by China, India, United States, and Europe | Long term (≥ 4 years) |

| Recovery in medical X-ray / photographic film in EMs | +0.3% | Emerging markets in Asia-Pacific, Latin America, and Africa | Short term (≤ 2 years) |

| Silver-based antimicrobial coatings for food packaging | +0.5% | North America, Europe, with adoption spreading to Asia-Pacific | Medium term (2-4 years) |

| HV-DC fast-charging connectors in Electric Vehicle infrastructure | +0.7% | China, Europe, North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Electronics Miniaturization and 5G Component Demand

The global expansion of 5G, both through macro and small-cell sites, is driving up the demand for ultra-high-conductivity paste. This paste is crucial for multilayer ceramic capacitors, thick-film conductors, and radio-frequency shielding. Silver, with an electrical conductivity of 63 × 10⁶ S/m at 20 °C, minimizes insertion loss at millimeter-wave frequencies above 24 GHz[1]IEEE, “Silver Conductivity Standards for RF Components,” ieee.org. This property solidifies silver's role in antenna arrays and power amplifiers. In 2025, component manufacturers from Korea and Taiwan boosted their paste orders, gearing up for the dense urban deployments of 5G. However, profit margins face pressure, especially where copper-based inks are adequate for designs under 6 GHz. As research into 6G continues, silver's role is becoming more pronounced, especially for chiplet interconnects that demand a bulk resistivity below 1.6 µΩ·cm. This trend suggests a sustained demand for silver well into 2030.

Utility-Scale Photovoltaic Build-Out

In 2025, solar installations added new capacity, with a significant portion being utility-scale. This surge solidified photovoltaics as the leading consumer of silver slurry for front-side metallization. Historically, each time solar capacity doubles, silver usage per watt drops. However, the newer n-type TOPCon and heterojunction cells, which utilize dual-sided collectors, have momentarily increased silver requirements per cell. Manufacturers aim to reduce silver usage per cell by 2030, employing techniques like finer screen meshes and hybrid copper plating. Thanks to Beijing's subsidies for export-bound modules, the Asia-Pacific region remains the focal point for silver powder demand. Furthermore, the emerging panel-recycling ecosystem is projected to satisfy a substantial portion of silver needs driven by photovoltaics by the middle of the century.

Recovery in Medical X-Ray/Photographic Film in Emerging Markets

In rural areas of India, Bangladesh, and Nigeria, government-funded basic radiography suites continue to depend on analog film, hampered by unstable power and limited IT infrastructure. Thanks to the addition of new mobile clinics under India's National Health Mission in 2025, global consumption of photographic film remained steady. While this represents only a small fraction of total silver consumption, it has the potential to influence spot demand, especially during tight supply chain periods. Although a shift to digital is on the horizon, the affordability of film and its autonomy from network dependencies offer a crucial, albeit temporary, solution for these underserved regions.

Silver-Based Antimicrobial Coatings for Food Packaging

Retailers pursuing lower spoilage rates are piloting silver nanoparticle liners that cut microbial growth by up to 40% during chilled transport. North American grocery chains began commercial roll-outs in 2025, while the European Commission now requires cradle-to-grave life-cycle assessments for such coatings starting in 2027 to address nanoparticle discharge concerns. The application remains niche but shows a steep adoption curve in prepared-meal logistics and online grocery channels.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heavy-metal discharge caps in mining permits | -0.8% | Latin America (Peru, Chile, Mexico), North America, Poland | Long term (≥ 4 years) |

| Copper/aluminium substitution in wiring and PV ribbons | -1.1% | Global, most acute in Asia-Pacific solar manufacturing | Medium term (2-4 years) |

| High price volatility limiting long-term contracts | -0.6% | Global, affecting industrial fabricators and investment demand | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Heavy-Metal Discharge Caps in Mining Permits

In 2024, the U.S. Environmental Protection Agency slashed the dissolved-silver limits in tailings discharge[2]U.S. Environmental Protection Agency, “Effluent Limitations Guidelines 2024,” epa.gov. This move has led to a doubling of water-treatment costs for several polymetallic mines in Nevada and Alaska. Following suit, Peru imposed even more stringent zero-liquid-discharge mandates in regions like Áncash. This has resulted in capital costs surging and has stalled the introduction of new annual capacity. By elevating the hurdle rate on marginal projects, these environmental regulations jeopardize the growth of primary-mine output. This could leave the silver market in a precarious position, especially when industrial demand sees an uptick.

Copper/Aluminum Substitution in Wiring and PV Ribbons

Engineers are increasingly opting for copper over silver in bus ribbons and mid-temperature solders, driven by the fact that a kilogram of copper costs less than two percent of its equivalent conductive mass in silver, provided the efficiency trade-off is acceptable. Chinese module maker LONGi unveiled a copper-silver hybrid metallization strategy, targeting a significant reduction in silver usage per cell. Concurrently, aluminum ribbons are capturing a larger share on the rear sides of bifacial panels. If these trajectories persist, silver's dominance in PV metallization could decline significantly by decade's end, leading to a notable decrease in annual demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type – Fine Silver Retains Dominance amid Purity Demand

Fine Silver secured a 71.62% share of the volume, solidifying its status as the primary feedstock for industrial powders, investment bars, and exchange-traded inventories. Ultra-high-purity grades are being utilized for RF filters and next-gen chip packaging, further bolstering Fine Silver’s prominence as electronics fabrication expands. Sterling Silver remains a staple in classic jewelry due to its hardness and hallmarked branding. However, Indian retail volumes faced a price-induced dip. Argentium Silver, known for its tarnish resistance in humid conditions, is increasingly favored for low-maintenance luxury goods and marine fittings, explaining its forecast 4.74% CAGR to 2031. While Coin Silver and niche alloys collectively account for a smaller share, they maintain relevance in numismatics, solders, and medical catalysts.

As photovoltaics continue to evolve, there's a heightened emphasis on purity thresholds for paste inputs. This trend ensures Fine Silver's sub-segment retains its dominant position in the silver market for the foreseeable future. Despite Argentium's relative growth rate outpacing the broader market, its expansion will be limited by the constrained supply of germanium, a vital component. Meanwhile, Coin Silver faces stagnation as central banks halt the bulk minting of 90%-silver coins, and investors shift their preference towards .999 fine rounds. Across the board, while recyclers are increasingly targeting jewelry scrap and electronic waste, their current contribution remains modest.

By Application – Electronics Outpace Jewelry While Investment Stays Cyclical

Jewelry and silverware represented 30.41% of the 2025 volume, but rising prices dampened discretionary spending among younger Asian buyers, particularly in India, resulting in a contraction. Meanwhile, the electrical and electronics sector, buoyed by multilayer ceramic capacitors, PV cell grids, and HV-DC connectors, is registering a 4.65% CAGR. These components elevated their share of the silver market. Physical investments surged during times of monetary-policy uncertainty, which heightened the demand for bullion hedges. While photographic film now constitutes a small portion of silver fabrication, it demonstrates resilience, particularly in emerging-market healthcare.

Brazing alloys and solders, though stable in tonnage as a mature end-use, are gradually ceding market share to lead-free copper-phosphorus alternatives, especially in HVAC and white-goods manufacturing. Pharmaceuticals and biomedical applications, such as antimicrobial wound dressings and coated catheters, may see increased demand due to the aging global population. Silver's pairing with zinc in battery chemistries finds niche adoption in aerospace, albeit with a reliance on defense budgets. Collectively, these non-jewelry industrial avenues bolster a demand floor, providing stability to the silver market during dips in investor interest.

Geography Analysis

Asia-Pacific accounted for a commanding 57.44% of global consumption in 2025 and should sustain a 4.91% CAGR through 2031, bolstered by China's robust polysilicon value chain and India's growing import appetite. Despite significant mining activity in 2024, China turned to imports, seeking refined metal to satisfy its electronics and solar demands. This highlights the region's deficit stance. In 2025, India's Union Budget cut import duties, triggering a spike in refined-silver inflows. However, elevated local prices dampened jewelry sales. Meanwhile, Japan and South Korea, together accounting for a portion of the region's consumption, focus on semiconductor packaging, still predominantly using silver wire-bond interconnects, despite testing coated copper alternatives.

North America claimed a notable share of global consumption in 2025. The U.S., with its mining output, found itself consuming nearly threefold that amount across sectors like electronics, medical devices, and bullion investments, highlighting a structural shortfall. Mexico's production saw only a fraction consumed domestically, with the majority exported, mainly to the U.S. and India. Europe, holding a significant share, leans on Germany, Italy, and the U.K. for silverware and industrial needs. Notably, outside of Poland's output in 2024, regional mining contributions remain scant.

South America, accounting for a portion of global consumption, is driven by Brazil's electronics sector and Argentina's budding investment interest. The Middle-East and Africa, together consuming about a small share, are poised for modest growth. This is largely due to Saudi Arabia's push into utility-scale solar, which relies on silver-rich heterojunction modules. On the supply front, 2024 saw global mine production fall short of fabrication demand. Recycled scrap and withdrawals from above-ground stocks filled this gap. The pronounced geographical divide, with Latin American supply and Asian demand, not only sustains long-haul trade routes but also amplifies vulnerabilities to maritime disruptions and tariff fluctuations.

Mordor Intelligence provides coverage of the silver market across other key regional markets. Detailed country-level analysis extends to Indonesia incorporating local coverage and market participation, as required.

Competitive Landscape

The silver market exhibits a highly fragmented. Technology upgrades, including sensor-based ore sorting and bacterial oxidation, boosted recovery at Coeur Mining’s Rochester expansion, illustrating how incremental metallurgical gains can add millions of ounces with minimal new footprints. ESG pressures are reshaping capital access; companies certified under ISO 14001 and the Cyanide Code now command lower financing spreads and preferred offtake contracts, nudging laggards toward faster compliance. Looking ahead, the silver market could see gradual consolidation as mid-tier miners merge to pool ESG spending and counter volatile margins, yet the prevalence of by-product output will keep true oligopoly out of reach.

Silver Industry Leaders

Fresnillo plc

KGHM

Newmont Corporation

Hindustan Zinc

Pan American Silver Corp

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Hindustan Zinc Limited (HZL) has announced plans to invest approximately INR 12,000 crore (~USD 135.18 million) to double its production capacity in silver and other metal verticals. The project is expected to be completed within 36 months.

- February 2025: Coeur Mining has finalized the acquisition of the Las Chispas mine, enhancing its silver production portfolio and reinforcing its position within Mexico's mining sector. The integration of Las Chispas is expected to drive Coeur's silver output to 20 million ounces by 2025, a significant rise from 11 million ounces recorded last year.

Global Silver Market Report Scope

Silver is a soft, white, lustrous transition metal that exhibits the highest electrical conductivity, thermal conductivity, and reflectivity of any metal. Silver is typically found in nature in conjunction with other metals or in minerals containing silver compounds, most commonly in the form of sulfides.

The silver market is segmented by type, application, and geography. By type, the market is segmented into fine silver, sterling silver, argentium silver, coin silver, and other types. By application, the market is segmented into physical investment (bars and coins), electrical and electronics, photographic films, brazing alloys and solder, jewelry and silverware, pharmaceuticals and biomedical, and other applications. The report also covers the market size and forecasts for the silver market in 16 countries across major regions. For each segment, market sizing and forecasts have been done based on volume (Tons).

| Fine Silver |

| Sterling Silver |

| Argentium Silver |

| Coin Silver |

| Other Types |

| Physical Investment (Bars and Coins) |

| Electrical and Electronics |

| Photographic Films |

| Brazing Alloys and Solders |

| Jewelry and Silverware |

| Pharmaceuticals and Biomedical |

| Other Applications |

| Production Analysis | United States | |

| Argentina | ||

| Australia | ||

| Bolivia | ||

| Chile | ||

| China | ||

| India | ||

| Mexico | ||

| Peru | ||

| Poland | ||

| Russia | ||

| Rest of the World | ||

| Consumption Analysis | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

| By Type | Fine Silver | ||

| Sterling Silver | |||

| Argentium Silver | |||

| Coin Silver | |||

| Other Types | |||

| By Application | Physical Investment (Bars and Coins) | ||

| Electrical and Electronics | |||

| Photographic Films | |||

| Brazing Alloys and Solders | |||

| Jewelry and Silverware | |||

| Pharmaceuticals and Biomedical | |||

| Other Applications | |||

| By Geography | Production Analysis | United States | |

| Argentina | |||

| Australia | |||

| Bolivia | |||

| Chile | |||

| China | |||

| India | |||

| Mexico | |||

| Peru | |||

| Poland | |||

| Russia | |||

| Rest of the World | |||

| Consumption Analysis | Asia-Pacific | China | |

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| Italy | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle-East and Africa | Saudi Arabia | ||

| South Africa | |||

| Rest of Middle-East and Africa | |||

Key Questions Answered in the Report

What is the projected silver market size in 2031?

It is forecast to reach 49.54 kilotons by 2031, expanding at a 4.62% CAGR over 2026-2031, from 39.53 kilotons.

Which region will lead consumption growth through 2031?

Asia-Pacific, supported by Chinese photovoltaic manufacturing and Indian imports, is projected to grow at a 4.91% CAGR.

Which segment holds the largest silver market share?

Fine Silver commanded 71.62% of volume in 2025 because of its role in industrial and investment flows.

Why is silver critical for next-generation EV charging?

HV-DC fast chargers rely on silver-plated contacts to handle currents above 500 A without overheating, leveraging silver’s 429 W/m·K thermal conductivity.

How are environmental regulations affecting mine supply?

Tighter discharge standards in the U.S., Peru, and Chile are increasing capex and delaying projects, curbing primary-mine output.

Page last updated on: