Titanium Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

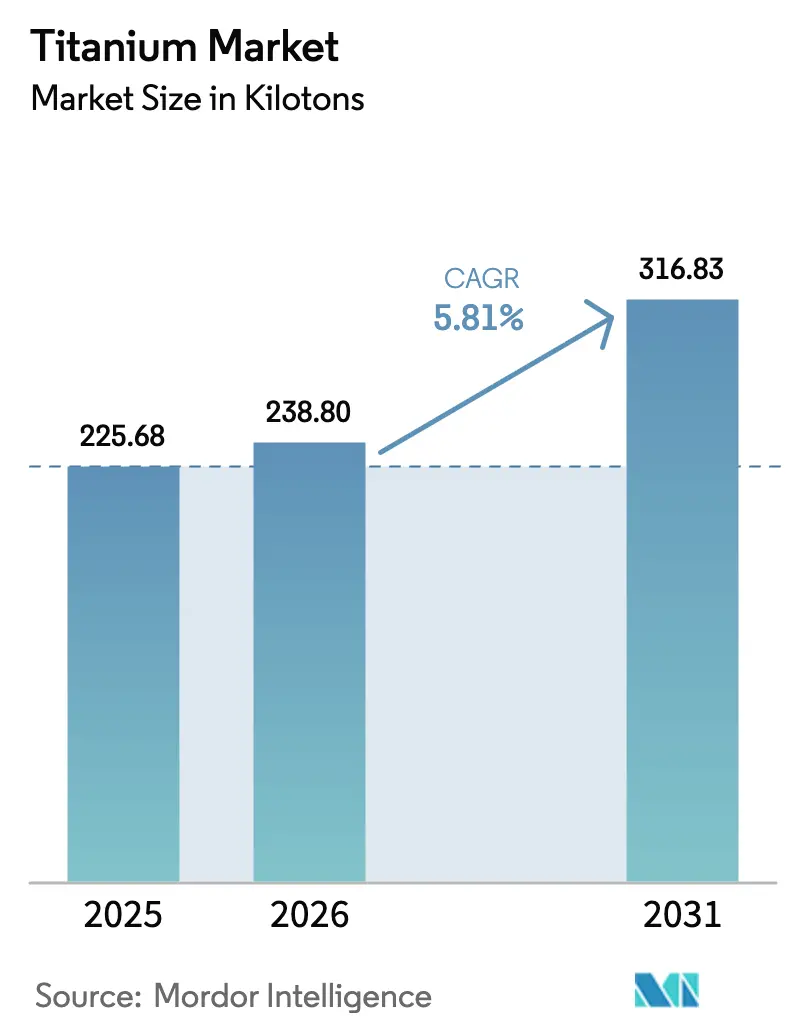

| Market Volume (2026) | 238.8 kilotons |

| Market Volume (2031) | 316.83 kilotons |

| Growth Rate (2026 - 2031) | 5.81% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Titanium Market Analysis by Mordor Intelligence

The Titanium Market size is expected to grow from 225.68 kilotons in 2025 to 238.8 kilotons in 2026 and is forecast to reach 316.83 kilotons by 2031 at 5.81% CAGR over 2026-2031. Rising defense procurement, electrified mobility, and offshore renewable-energy installations reinforce demand visibility, while continuing investments in production capacity widen the material’s addressable opportunity set. Although titanium production is energy intensive, advances in furnace efficiency and sponge recycling temper cost inflation and support margin stability for integrated producers. Aerospace backlogs stabilize after pandemic-era disruptions, medical device approvals for 3-D printed implants accelerate, and environmental regulations tighten corrosion-resistance specifications in chemical processing, all of which sustain multi-year buying cycles. Supply diversification programs in the United States and the Middle East reduce geopolitical dependence on traditional producers and underpin long-term resilience in the titanium market.

Key Report Takeaways

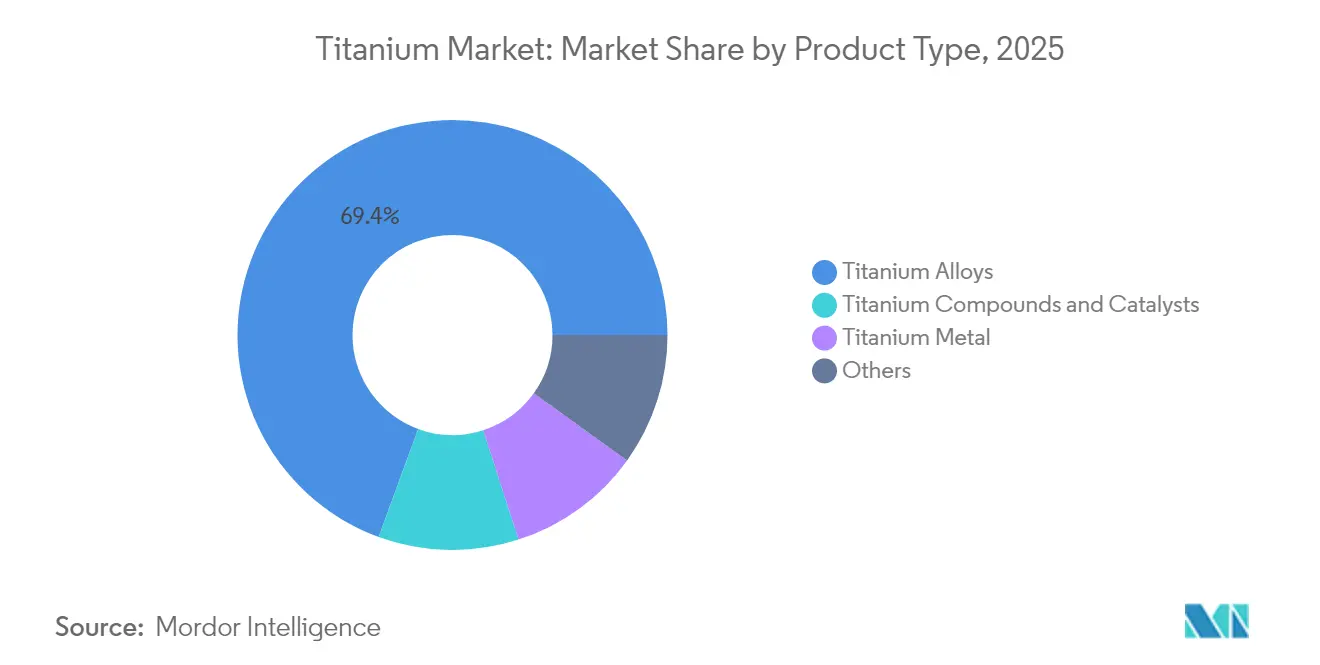

- By product category, titanium alloys led with 69.42% revenue share of the titanium market in 2025, while titanium compounds and catalysts are advancing at a 5.95% CAGR through 2031.

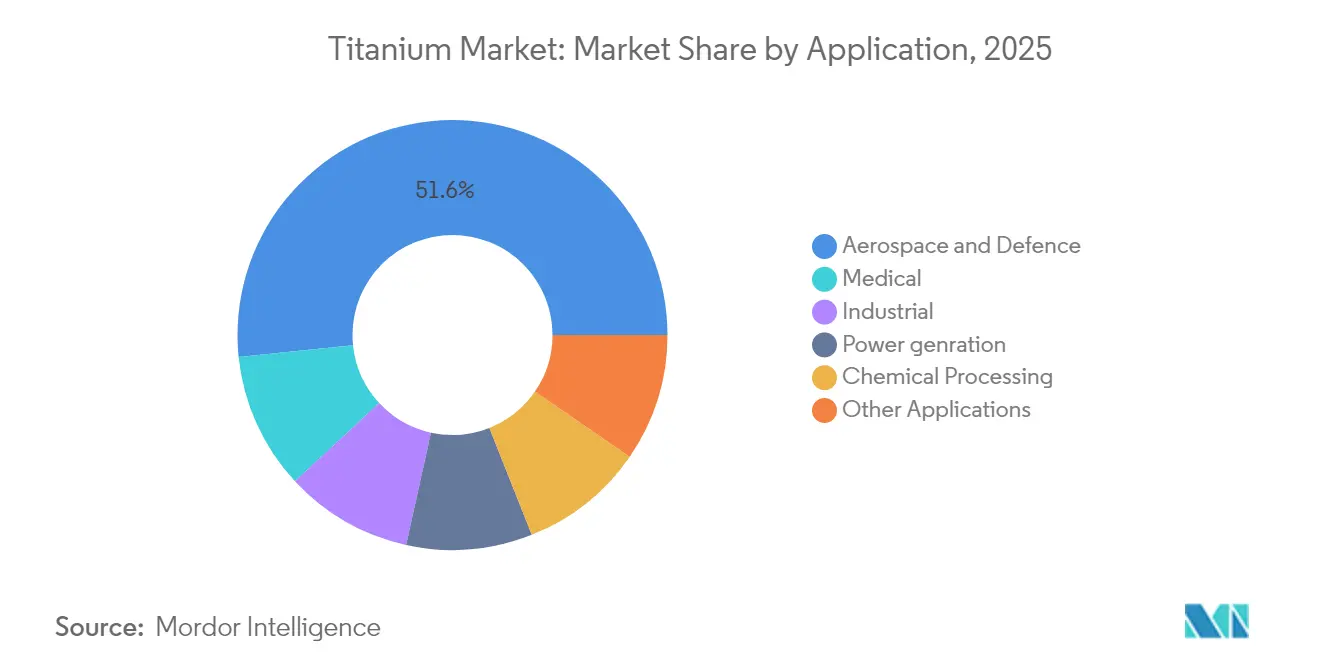

- By application, aerospace and defense retained 51.63% of the titanium market share in 2025; the medical segment is projected to grow at a 6.15% CAGR to 2031.

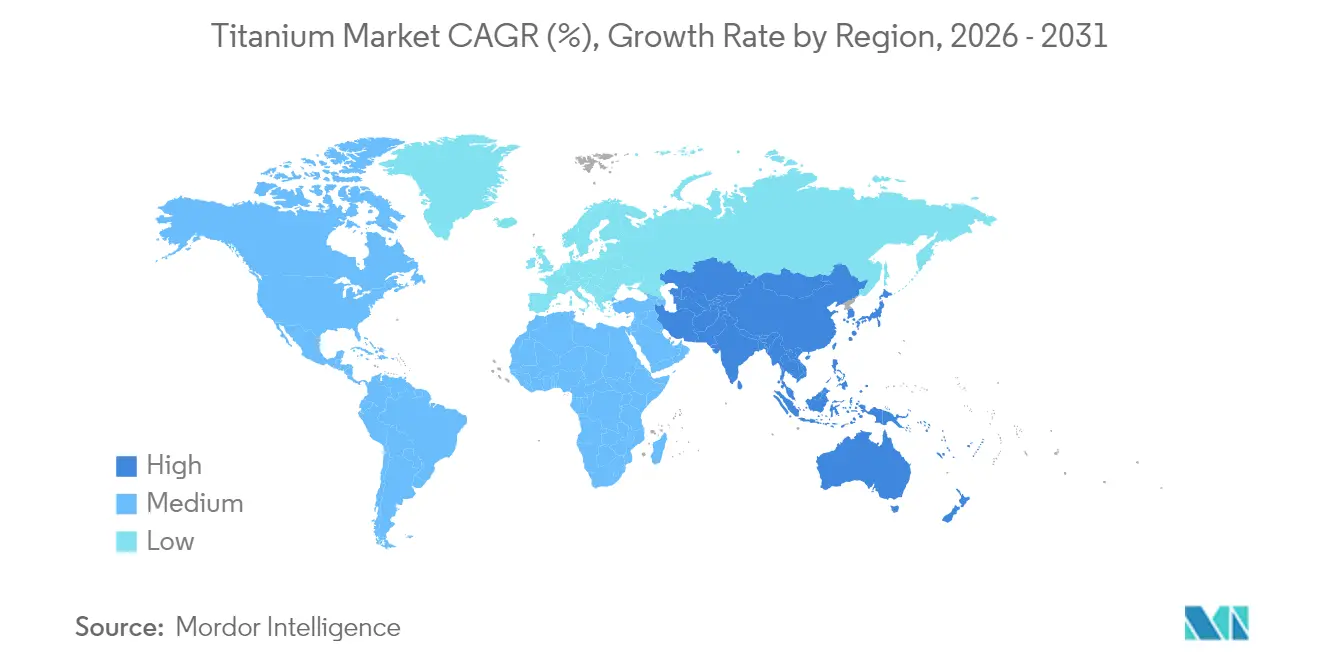

- By geography, Asia-Pacific accounted for 42.55% of the titanium market in 2025, and the region is forecast to expand at a 5.85% CAGR over the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Titanium Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing aerospace and defense backlog | +1.2% | North America, Europe, Global | Medium term (2–4 years) |

| Weight-to-strength advantage in e-mobility platforms | +0.8% | Asia-Pacific, North America, Europe | Long term (≥ 4 years) |

| Surging offshore wind-turbine demand | +0.6% | Europe, Asia-Pacific, North America | Medium term (2–4 years) |

| Titanium hydride use in solid-state batteries | +0.5% | Asia-Pacific, North America | Long term (≥ 4 years) |

| Biomedical 3-D printed implant approvals rising | +0.5% | North America, Europe, Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Aerospace and Defense Backlog

Strong order books for next-generation commercial jets broaden titanium demand as airframe builders integrate weight-saving alloys into fuselage sections, landing-gear components, and advanced engines that run hotter for fuel efficiency. The Airbus A350 and Boeing 787 families each incorporate more than 70 metric tons of titanium, and their multi-year production schedules anchor predictable offtake in the titanium market. NATO defense-modernization programs add incremental volumes for armor plating, missile casings, and naval systems that rely on corrosion-resistant grades. Certification cycles in aerospace extend 15–25 years, so once an alloy is approved, procurement remains sticky, encouraging upstream producers to maintain stringent quality-control regimes. Long-run visibility allows mills to execute capital plans for additional electron-beam furnaces that lift yield, reduce scrap, and strengthen supply reliability.

Weight-to-Strength Advantage in E-Mobility Platforms

As battery-pack densities plateau, electric-vehicle designers shift attention to chassis, motor housings, and fasteners for incremental weight savings. Tesla demonstrated titanium-reinforced drive-units that handle higher torque loads without mass penalties, a design that adds range without enlarging battery packs. Premium Chinese manufacturers such as BYD and NIO integrate titanium bolts and structural inserts in performance models to secure occupant safety while meeting acceleration targets. The transition to 800 V architectures elevates thermal-management requirements; titanium’s low thermal expansion and high specific strength meet those thresholds, limiting vibration and joint loosening during repeated charging. Adoption trends cascade from flagship vehicles into mid-segment offerings over five to seven model-year cycles, broadening the titanium market’s automotive footprint.

Surging Offshore Wind-Turbine Demand

Marine developers specify titanium alloys for monopile connectors, splash-zone ladders, and heat-exchanger tubing to combat aggressive chloride attack and biofouling. Twenty-five-year lifetime studies from North Sea projects show minimal pitting in titanium fasteners, justifying up-front cost premiums. Larger 15-MW turbines feature longer blades and deeper water foundations that amplify structural loads, further validating titanium’s fatigue tolerance. Europe’s leadership in floating-wind pilot farms accelerates adoption, while China’s coastal provinces target 65 GW of offshore capacity by 2030, expanding regional pull for titanium supply[1]Journal of Catalysis, “Titanium-Based Catalysts Propel Green Chemistry,” ScienceDirect, sciencedirect.com . Knowledge transfer to the United States under the Inflation Reduction Act expands procurement frameworks for corrosion-resistant alloys, reallocating portion of titanium supply toward green-energy infrastructure.

Biomedical 3-D Printed Implant Approvals Rising

Streamlined FDA pathways and CE marking frameworks for patient-matched orthopedic implants propel medical-grade titanium powder demand. Stryker and Zimmer Biomet each expanded additive-manufacturing lines to supply lattice-structured hip cups and spinal cages that accelerate osseointegration and reduce revision surgery rates. Aging populations in the United States, Europe, and Japan widen addressable patient pools, while emerging markets adopt titanium implants as healthcare spending rises. Hospitals leverage 3-D printing for faster surgical scheduling and lower inventory, embedding titanium alloys deeper within orthopedic value chains.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production and energy costs | −0.9% | Global, especially Europe | Short term (≤ 2 years) |

| Limited global sponge-capacity concentration | −0.7% | China, Japan, Global | Medium term (2–4 years) |

| ESG scrutiny on chloride waste streams | −0.4% | Europe, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Global Sponge-Capacity Concentration

China controls roughly 60% of sponge output, and Japan’s Toho Titanium and Osaka Titanium account for the bulk of aerospace-grade purity. The United States imports more than 95% of its sponge, leaving domestic mills vulnerable to shipment delays and trade-policy friction[2]United States Geological Survey, “Titanium Statistics and Information,” USGS, usgs.gov . Recent defense-production grants support a 15.6 kilo-ton facility restart, yet ramp-up timelines extend beyond two years due to qualification testing. Saudi Arabia’s ATTM joint venture with Toho brings an additional supply node online, but capacity remains small relative to growing global demand. Until these projects mature, procurement managers hedge with multi-year contracts and strategic stockpiles, restraining flexibility in the titanium market.

ESG Scrutiny on Chloride Waste Streams

Chloride-based ore-refining routes generate acidic tailings that face tougher disposal controls under Europe’s Waste Framework Directive and anticipated U.S. EPA updates. Permitting for greenfield plants lengthens as communities demand closed-loop effluent systems, boosting capital expenditures. Producers pilot chlor-alkali by-product valorization to offset compliance costs and shift toward sulfate-free routes, yet commercialization remains nascent. These regulations slow capacity additions in mature economies and incentivize relocation to regions with lenient standards, complicating supply-chain audits for aerospace primes and medical device firms that adhere to strict environmental disclosure frameworks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Alloys Dominate Despite Compounds Growth

Titanium alloys held a dominant 69.42% slice of the titanium market in 2025, driven by legacy aerospace reliance on Ti-6Al-4V and derivative grades certified over multiple decades. Volume predictability secures sizeable mill production runs, lowering per-unit costs compared with specialty forms. The aerospace sector requires fracture-toughness and fatigue-resistance benchmarks that pure metal often cannot meet, bolstering demand for alloyed chemistries. Strict traceability under AS9100 standards raises entry barriers for new mills, favoring incumbents with established metallurgical credentials.

Titanium compounds and catalysts, though a smaller base, register the highest 5.95% CAGR as specialty chemicals, water-treatment developers, and green-hydrogen start-ups adopt titanium tetrachloride and photocatalysts to meet environmental performance goals. This shift underscores market maturation as end-users explore the corrosion resistance, Lewis-acid character, and semiconductor band-gap benefits beyond classical aerospace alloys. Pure-metal consumption remains steady in marine heat exchangers and pickling equipment, where chloride corrosion erodes stainless steels. Powder metallurgy, especially in additive manufacturing, opens new pathways to high-value niches such as lattice orthopedic implants and rocket engine components, widening the titanium market size for advanced forms without proportionally increasing sponge requirements.

By Application: Medical Segment Accelerates Beyond Aerospace Leadership

Aerospace retained 51.63% of titanium market share in 2025, yet its mid-single-digit growth trails the medical segment’s 6.15% CAGR through 2031, signaling a gradual broadening of demand. Passenger jet deliveries normalize to pre-2020 trajectories, and engine OEMs adopt lighter fan-blade designs that use reduced titanium mass, moderating volume growth despite ongoing program expansions. Defense orders partially offset this tempering, especially in naval submarines and hypersonic platforms where titanium’s high-temperature capabilities are essential.

Medical applications outpace overall market growth due to demographic pressure and technological leaps in 3-D printed implants. Personalized hip and knee replacements incorporate trabecular structures that mimic bone stiffness, reducing stress shielding. Dental implants leverage osseointegration to achieve faster recovery, commanding premium prices per gram of material. Regulatory harmonization in Latin America and Southeast Asia accelerates procedure adoption, while powder-bed-fusion equipment costs decline, democratizing access for regional orthopedic labs. Industrial, power-generation, and chemical-processing uses add baseload demand, particularly in geothermal plants and chlor-alkali units requiring lifetime corrosion resistance that stainless steel cannot deliver at comparable longevity.

Geography Analysis

Asia-Pacific dominated the titanium market with 42.55% share in 2025 and is projected to expand at 5.85% CAGR through 2031. China’s vertically integrated ecosystem, from ilmenite mining in Sichuan to sponge and mill product fabrication along the Yangtze delta, enables cost leadership. Domestic aerospace programs such as COMAC’s C919 and CR929 secure local titanium orders, while wind-turbine OEMs scale corrosion-resistant component use in offshore clusters along the East China Sea. Japan’s Toho Titanium maintains premium positioning in high-purity sponge, supplying jet-engine makers that require ultra-low trace elements for fatigue-critical parts.

North America ranks as a mature yet strategically important consumption base given its large commercial-jet assembly footprint and world-leading orthopedic-implant producers. The United States depends on imports for more than 95% of sponge requirements, prompting federal initiatives to restart idled furnaces and co-invest in new capacity adjacent to aerospace clusters in Washington and Pennsylvania. ATI’s electron-beam furnace expansion, slated for first melt in late 2025, targets aerospace-grade billets and medical powders, reducing reliance on Japanese feedstock.

Europe preserves a high-value titanium footprint anchored by Airbus, Rolls-Royce, and Safran. However, elevated power prices risk eroding regional smelter competitiveness. Recycling initiatives gain momentum in Germany and the Netherlands to reclaim turnings and off-cuts from machining operations, supplying secondary feed for alloy producers.

Competitive Landscape

The titanium market remains moderately fragmented. Technology differentiation is increasingly critical. ATI invested in a dedicated powder-atomization facility that manufactures spherical titanium powders for laser-powder-bed fusion printers, targeting orthopedic implants and space-launch brackets. Strategic moves include multi-year offtake contracts with turbine OEMs that guarantee volume and pricing floors, mitigating raw-material volatility. Producers also pursue sustainability metrics by integrating solar or geothermal power at sponge plants, responding to aerospace primes’ Scope 3 emissions reduction targets.

Titanium Industry Leaders

ATI

Corporation VSMPO-AVISMA

Timet (Precision Castparts Corp.)

Toho Titanium Co., Ltd.

Tronox Holdings Plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Tronox Holdings announced plans to idle its 90,000 tons per year titanium-dioxide plant in Botlek, Netherlands, to rebalance its European capacity.

- February 2025: The Chemours Company introduced Ti-Pure TS-6706, a TMP- and TME-free version of its benchmark Ti-Pure R-706 pigment to meet low-VOC coatings requirements.

Global Titanium Market Report Scope

Titanium is a hard, silvery-grey metal that naturally occurs as a compound in various minerals, most notably in ilmenite (FeTiO3) and rutile (TiO2). Valued for its low density, high strength, and excellent corrosion resistance, titanium boasts impressive properties. Additionally, its modulus of elasticity is half that of stainless steel, contributing to its durability and shock resistance. These minerals are more commonly found in sand or soil than in hard rock as ilmenite and rutile. Other minerals containing titanium include perovskite, titanite, anatase, and brookite. Major deposits of these titanium minerals are located in China, Australia, Canada, India, Norway, South Africa, Ukraine, and the USA.

The Titanium Market is Segmented by product type, application, and geography. By product type, the market is segmented into Titanium metal, Titanium alloy, Titanium compounds and catalysts, and Others. By application, it is segmented into Aerospace, Industrial, Power Generation, Chemical Processing, Medical, and Other Applications. The report offers market size forecasts for the titanium market in over 27 countries across major regions. For each segment, the market sizing and forecasts have been made on the basis of volume (tons).

| Titanium Metal |

| Titanium Alloys |

| Titanium Compounds and Catalysts |

| Others |

| Aerospace and Defence |

| Industrial |

| Power genration |

| Chemical Processing |

| Medical |

| Other Applications |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Thailand | |

| Malaysia | |

| Indonesia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Turkey | |

| Nordics | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Egypt | |

| Nigeria | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product Type | Titanium Metal | |

| Titanium Alloys | ||

| Titanium Compounds and Catalysts | ||

| Others | ||

| By Application | Aerospace and Defence | |

| Industrial | ||

| Power genration | ||

| Chemical Processing | ||

| Medical | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| Thailand | ||

| Malaysia | ||

| Indonesia | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Turkey | ||

| Nordics | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Egypt | ||

| Nigeria | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected volume for global titanium demand by 2031?

Forecasts point to 316.83 kilo tons by 2031, up from 238.8 kilo tons in 2026.

Which application contributes most to titanium consumption today?

Aerospace and defense account for 51.63% of global demand, reflecting jet-engine and airframe requirements.

Why is titanium pivotal in medical implants?

Its biocompatibility and ability to bond with bone enable durable, patient-specific orthopedic and dental devices.

How concentrated is titanium sponge production?

China and Japan jointly supply around 60% of global sponge, with the United States importing over 95% of its needs.

What is driving titanium adoption in electric vehicles?

The metal offers superior strength-to-weight ratios that offset battery mass and withstand high-thermal loads in next-gen powertrains.

How are producers mitigating ESG concerns in titanium refining?

Investments in renewable energy integration and closed-loop chloride management lower carbon footprints and waste outputs.

Page last updated on: