Technetium 99m Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

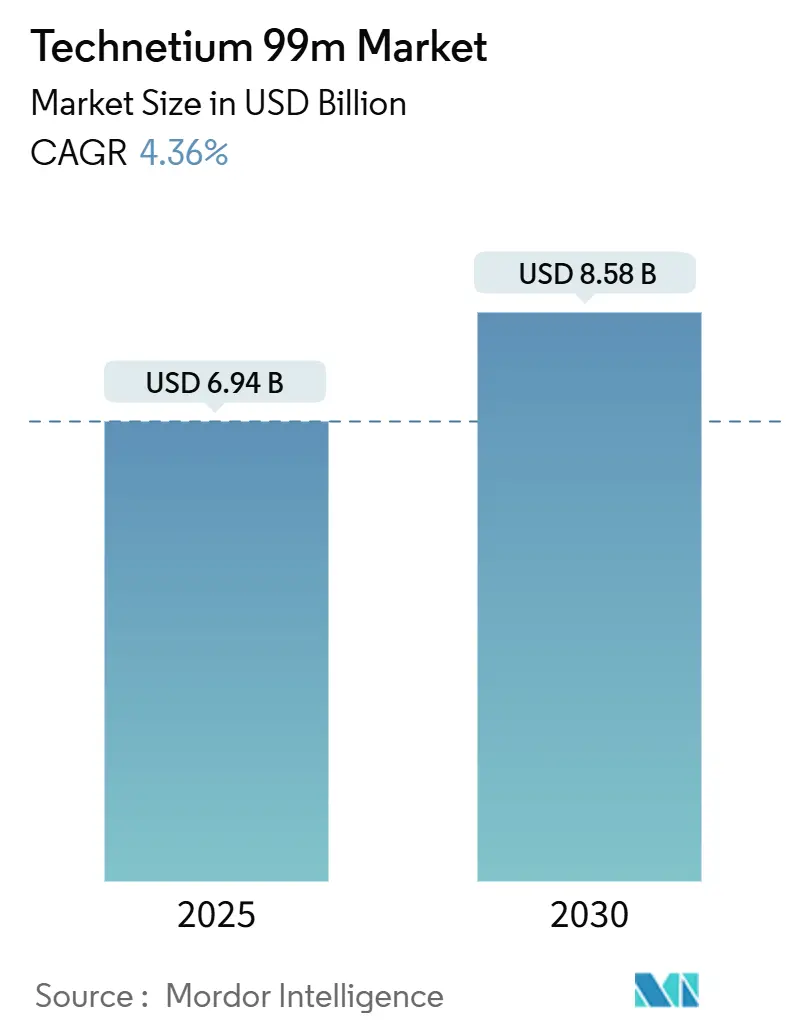

| Market Size (2025) | USD 6.94 Billion |

| Market Size (2030) | USD 8.58 Billion |

| Growth Rate (2025 - 2030) | 4.36% CAGR |

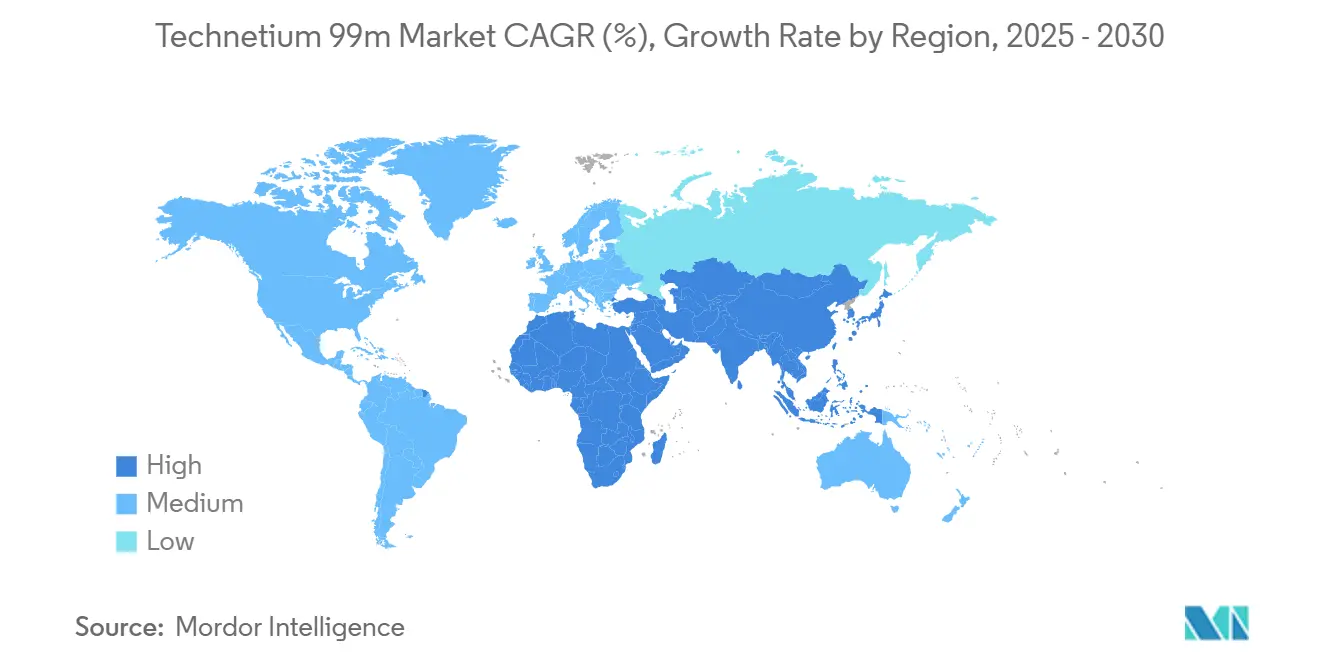

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Technetium 99m Market Analysis by Mordor Intelligence

The technetium-99m market size stands at USD 6.94 billion in 2025 and is forecast to reach USD 8.58 billion by 2030, reflecting a CAGR of 4.36%. Strong clinical reliance on the radioisotope underpins this expansion, as the nucleus of more than 80% of diagnostic nuclear‐medicine procedures worldwide. Hospitals value the 6-hour half-life because it delivers crisp Single Photon Emission Computed Tomography (SPECT) images while limiting patient radiation, supporting growing use across cardiology, oncology and neurology. Supply-chain diversification, led by domestic molybdenum-99 (Mo-99) programs in the United States, Canada and parts of Europe, is improving resilience after past reactor outages. Technology upgrades such as hybrid SPECT/CT systems and mini-cyclotrons inside tertiary hospitals broaden procedure capacity, while reimbursement reforms in the United States and Europe remove financial barriers that once curtailed nuclear cardiology. Together these factors sustain a healthy competitive arena where established generator suppliers face new entrants betting on cyclotron and linear-accelerator routes.

Key Report Takeaways

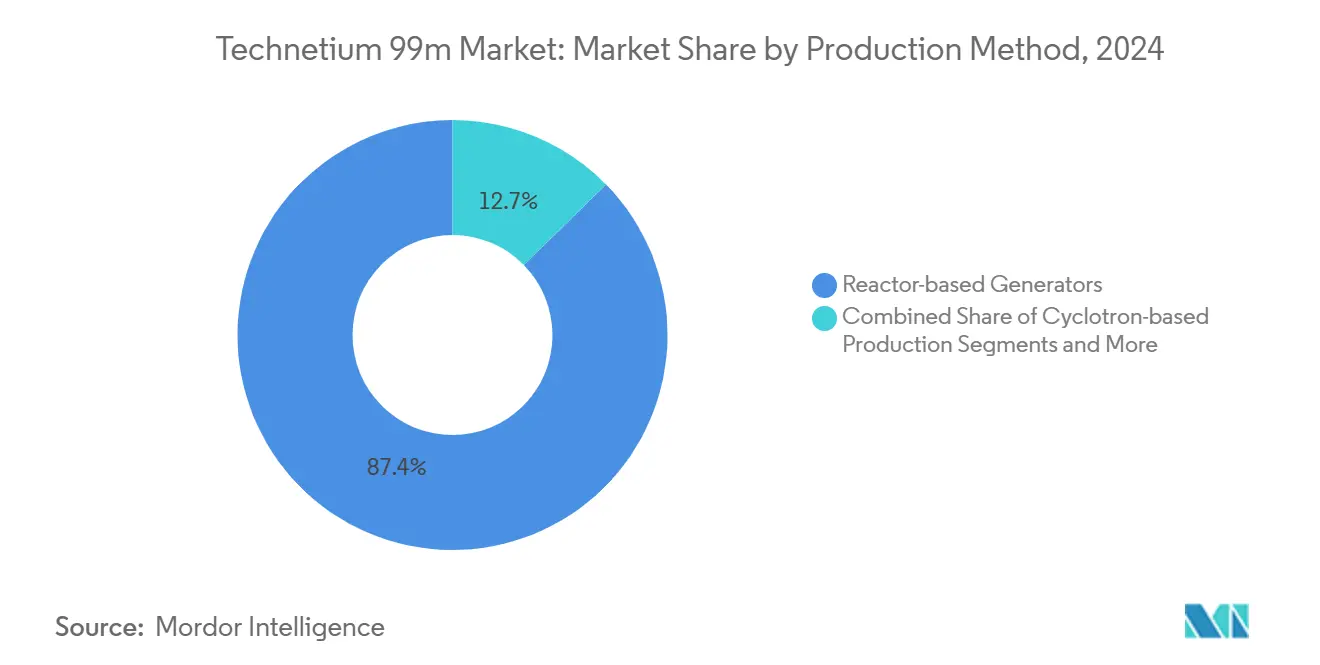

- By production method, reactor-based generators led with 87.35% technetium-99m market share in 2024, whereas cyclotron-based production is projected to expand at 8.24% CAGR through 2030.

- By application, cardiology imaging commanded 51.46% of the technetium-99m market size in 2024; oncology imaging is advancing at a 7.78% CAGR through 2030.

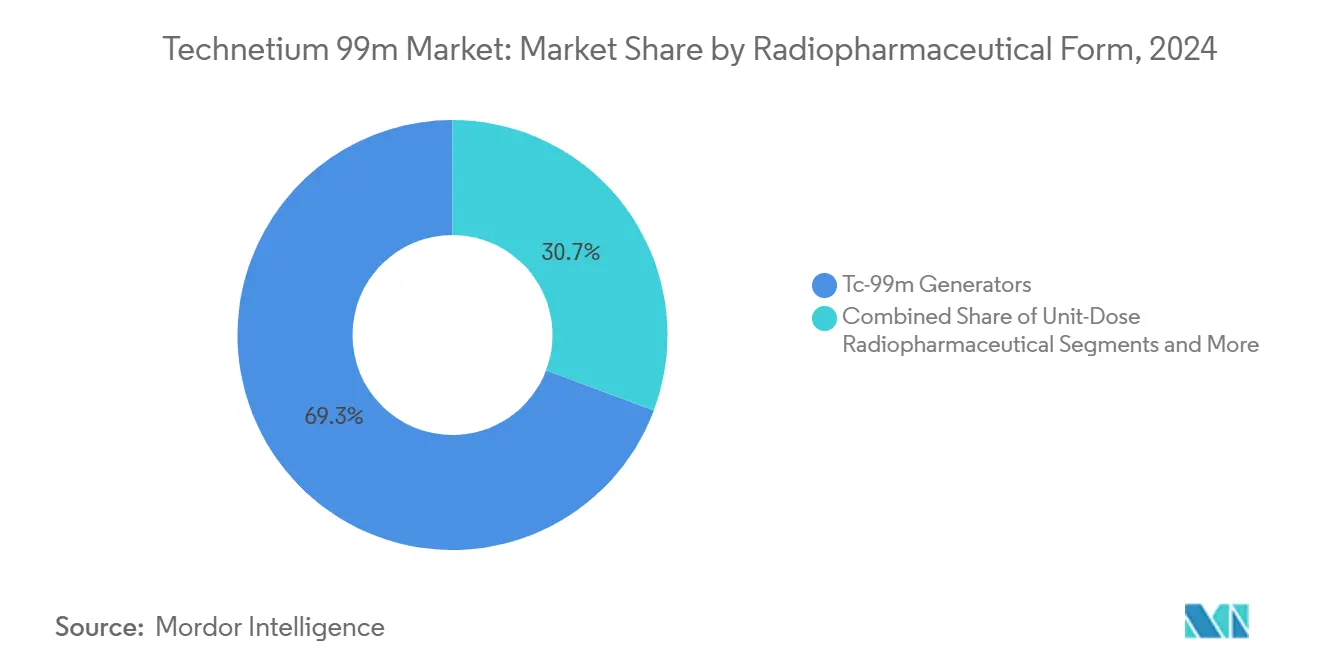

- By radiopharmaceutical form, Tc-99m generators held 69.28% share of the technetium-99m market size in 2024, while unit-dose radiopharmaceuticals are forecast to grow at 8.89% CAGR between 2025-2030.

- By end user, hospitals accounted for 51.38% of technetium-99m market share in 2024; contract radiopharmacies exhibit the fastest CAGR at 8.36% through 2030.

- By geography, north america maintained 37.67% share of the technetium-99m market size in 2024; Asia-Pacific is set to rise at 6.24% CAGR to 2030.

Global Technetium 99m Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging Population & Surge In SPECT Procedures | +0.6% | Global, concentrated in North America & Europe | Long term (≥ 4 years) |

| Rapid Rise In Oncology Imaging Demand | +0.5% | Global, with APAC acceleration | Medium term (2-4 years) |

| Cardiology Reimbursement Expansions | +0.4% | North America & Europe | Short term (≤ 2 years) |

| Government Mo-99 Supply-Security Programs | +0.4% | North America, Europe, APAC core | Medium term (2-4 years) |

| Commercialization Of Non-Reactor Mo-99 Technologies | +0.3% | North America & Europe | Long term (≥ 4 years) |

| Mini-Cyclotron Adoption In Tertiary Hospitals | +0.3% | Global, early adoption in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aging Population & Surge in SPECT Procedures

Growing cohorts aged 65 plus require more cardiovascular, oncologic and neurologic diagnostics, pushing nuclear‐medicine departments to expand capacity with hybrid SPECT/CT scanners. Hospitals in the United States, Germany and Japan are refurbishing suites to meet higher procedure volumes, and teaching centers now embed radiopharmacy coursework in geriatric curricula. TRIUMF’s CycloMed99 program recently supplied technetium-99m doses for 500 patients from a single 6-hour cyclotron run, proving local production scalability. Aging-driven utilization is largely insensitive to macroeconomic cycles because chronic disease monitoring is medically mandatory. Consequently, procedure growth anchored to demographics provides a structural tailwind for the technetium-99m market. Cardiology and oncology, which require repeat scans for therapy titration, gain disproportionate upside from this demographic shift.

Rapid Rise in Oncology Imaging Demand

Escalating cancer screening campaigns worldwide, alongside personalized oncology protocols, lift demand for technetium-99m bone, lymph-node and receptor imaging. The Journal of Nuclear Medicine highlighted new prostate-cancer peptide conjugates that exploit technetium-99m labeling for high-contrast tumor detection.[1]Truc T. Pham, “Advances in 99mTc-Labeled Agents for Prostate Imaging,” Journal of Nuclear Medicine, snmjournals.orgCompanion‐diagnostic strategies for novel radioligand therapies also amplify imaging volumes because clinicians need baseline and follow-up scans. Asia-Pacific health ministries, particularly in China and India, added technetium-based whole-body bone scans to national cancer guidelines during 2024-2025, multiplying dose requisitions from provincial hospitals. Unit-dose suppliers benefit most because oncology protocols demand strict activity control and low radiation to healthy tissue. The trend consequently accelerates revenue diversification for cyclotron operators positioned near oncology centers.

Cardiology Reimbursement Expansions

The November 2024 U.S. Centers for Medicare & Medicaid Services rule carved out separate payment for diagnostic radiopharmaceuticals priced above USD 630, removing a decade-long cost barrier that suppressed nuclear cardiology volumes.[2]Jeff Shuren, “From Our Perspective: FDA’s Role in Radiopharmaceutical Payment Reform,” U.S. Food & Drug Administration, fda.gov Hospitals now recoup full radiopharmaceutical costs instead of absorbing them within the procedure bundle, prompting many systems to reopen or enlarge SPECT suites. European payers are replicating the policy in outpatient settings, further widening access. Vendor order books for stress-perfusion tracers such as tetrofosmin climbed sharply from early 2025, reflecting newfound budget certainty in cardiology departments. Short-term procedure growth is thus strongest in the United States and Germany, driving immediate dose demand and boosting generator utilization rates.

Government Mo-99 Supply-Security Programs

National security concerns catalyze public funding for domestic Mo-99 capacity using low-enriched uranium (LEU) or accelerator technology. The U.S. Department of Energy’s National Nuclear Security Administration (NNSA) reports that SHINE Technologies will cover more than 75% of U.S. Mo-99 needs once its Wisconsin plant reaches steady-state output.[3]Jill Hruby, “NNSA’s Molybdenum-99 Program: Establishing a Reliable Domestic Supply of Mo-99 Produced Without Highly Enriched Uranium,” U.S. Department of Energy, energy.gov Canada’s government invested to expand cyclotron capacity in Vancouver, while the European Commission funds LEU conversion at existing reactors. Such programs reduce outage risk, encourage private investors to back new players and compress dependence on aging foreign reactors. They also speed regulatory approvals for non-reactor production lines, which, in turn, inject fresh competition into the technetium-99m market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reactor Outages & Fragile Supply Chain | -0.5% | Global, acute in regions dependent on few reactors | Short term (≤ 2 years) |

| Stringent Radio-Isotope Transport Regulations | -0.4% | Global, complex in cross-border shipments | Medium term (2-4 years) |

| PET Tracers Cannibalizing SPECT Volumes | -0.4% | North America & Europe, emerging in APAC | Long term (≥ 4 years) |

| Capital Intensity Of LEU Conversion Projects | -0.3% | Global, concentrated in reactor-operating countries | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Reactor Outages & Fragile Supply Chain

Five aging research reactors still account for most global Mo-99 output, so unplanned maintenance forces procedure cancellations and costly rescheduling. A recent European outage triggered dose rationing across 12 countries within 48 hours. Because Mo-99 decays in 66 hours, any hold-up in production or transit renders batches useless. Eden Radioisotopes is building a dedicated Mo-99 reactor leveraging Sandia National Laboratories’ design to relieve U.S. bottlenecks, while the University of Missouri’s NextGen MURR project aims to expand domestic capacity. Until new assets come online, service disruptions remain a near-term drag on the technetium-99m market.

Stringent Radio-Isotope Transport Regulations

International Atomic Energy Agency code, plus diverse national rules, mandate special Type-A and Type-B packaging, driver certification and real-time tracking for radioactive consignments. Compliance raises freight charges and complicates multi-stop itineraries, particularly in Africa and Latin America where logistical networks are thin. Small distributors face disproportionate paperwork and insurance costs, encouraging consolidation around global couriers with established expertise. Delays erode usable activity because technetium-99m has a 6-hour half-life, so protracted customs clearance directly destroys inventory. The burden remains a mid-term headwind for new market entrants.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Production Method: Reactor Dominance Faces Cyclotron Challenge

Reactor-based generators controlled an 87.35% share of the technetium-99m market size in 2024 as decades-old supply chains and scale efficiencies kept unit costs lower than alternatives. Despite that lead, cyclotron production is on track for 8.24% CAGR through 2030, propelled by decentralized hospital strategies that shorten supply lines and sidestep reactor outages. The technetium-99m market benefits as British Columbia allocated USD 50.5 million to a Vancouver cyclotron and radiopharmacy complex that will secure regional isotope demand. Linear-accelerator and LEU processes presently hold niche footprints, yet technology pilots at national labs suggest meaningful long-term upside once capital costs decline.

Hospitals, regulators and investors increasingly prize reliability over minimal cost, creating fertile ground for accelerator venues that offer same-day isotope delivery. Cyclotrons directly attached to tertiary centers enable flexible production aligned with daily operating lists, cutting waste from radioactive decay. Countries such as the Netherlands and South Korea now evaluate public–private partnerships to spread capital investment across health systems. As more centers install compact cyclotrons, the technetium-99m market will gradually rebalance, eroding the historical near-monopoly of reactor producers while preserving multi-path redundancy preferred by clinicians.

By Application: Cardiology Leadership Meets Oncology Growth

Cardiology imaging commanded 51.46% technetium-99m market share in 2024 because SPECT perfusion remains a front-line modality for ischemia detection and viability assessment. Enhanced reimbursement moved procedure volumes sharply higher in 2025, and the segment is likely to post steady midsingle-digit growth through the decade. In contrast, oncology imaging is the fastest riser, with a 7.78% CAGR outlook and expanding portfolio that spans bone metastasis staging, sentinel lymph-node mapping and receptor-specific tracers. Oncology’s rise means its slice of the technetium-99m market size will widen year by year as cancer screening campaigns accelerate across Asia-Pacific.

Expanded theranostic paradigms weave diagnostic scans together with targeted therapies, locking in recurrent imaging needs throughout patient lifecycles. Hospitals in India built integrated cancer hubs that house both SPECT and radioligand therapy suites, illustrating converging diagnostic–therapeutic workflows. Neurology, endocrine, renal and pulmonary applications remain stable, catering to specialized indications such as brain perfusion, thyroid assessment and ventilation–perfusion mismatch. Collectively these clinical segments support balanced demand diversification, insulating the technetium-99m market from volatility in any single disease area.

By Radiopharmaceutical Form: Generators Dominate Despite Unit-Dose Surge

Tc-99m generators supplied 69.28% of 2024 dose demand thanks to their long-proven convenience for on-site elution. That said, unit-dose preparations are climbing at 8.89% CAGR because complex oncology and cardiology protocols favor factory quality control and pre-calibrated activities. Customized cold-kit labeling retains relevance for routine bone and thyroid scans, offering budget flexibility to smaller hospitals. Advanced robotics under development at Argonne promise to slash manual handling, a key step toward scaling unit-dose lines cost-effectively.

Production modernization mirrors broader health-system emphasis on traceability and regulatory compliance. Central pharmacies can now integrate electronic batch records that feed directly into hospital electronic health records, simplifying audits. For generator suppliers, rising unit-dose penetration signals the need to bundle service or logistics add-ons to protect share. Conversely, cyclotron operators view unit-dose as a natural extension because in-house vialing aligns with same-day production workflows, further reinforcing the growth narrative for decentralized models within the technetium-99m market.

By End User: Hospital Dominance Challenged by Contract Services

Hospitals consumed 51.38% of technetium-99m doses in 2024, yet many now outsource compounding to contract radiopharmacies that promise 24/7 delivery and stringent quality-assurance protocols. Those specialty providers exhibit an 8.36% CAGR outlook, supported by payer pressures to curb fixed overheads. Diagnostic imaging centers, often physician-owned, constitute a robust secondary channel, particularly for ambulatory cardiology and bone scans. Academic institutes pioneer novel tracer trials, while ambulatory surgical centers embrace low-dose protocols to maintain day-case throughput.

Aspirus Wausau Hospital’s USD 227 million expansion demonstrates that marquee medical centers still invest heavily in on-site nuclear medicine capacity. Simultaneously, smaller regional facilities prefer third-party services to avoid radiation-safety staffing burdens. The resulting hybrid ecosystem preserves hospital leadership while fostering specialist suppliers whose scale and logistics acumen deliver consistent product. Such diversity enlarges overall technetium-99m market access, ensuring patient appointments proceed whether doses originate in-house or arrive by early-morning courier.

Geography Analysis

North America held 37.67% technetium-99m market share in 2024, anchored by strong reimbursement, mature imaging infrastructure and decisive federal backing for domestic Mo-99. SHINE Technologies’ Wisconsin facility will soon satisfy 75% of U.S. isotope demand, while the University of Missouri’s NextGen MURR reactor adds another safety buffer. Canada reinforces continental self-sufficiency through TRIUMF’s cyclotron innovations, and leading hospital networks integrate new SPECT/CT scanners that support cardiology and oncology program growth. Such capacity‐building initiatives ensure continuous isotope flow, sustaining procedure volumes and revenue for suppliers.

Asia-Pacific is the fastest-growing territory, poised for 6.24% CAGR through 2030 as China, India and Japan pour capital into nuclear-medicine modernization. China’s five-year health plan earmarks funds for domestic radioisotope chains to lessen reliance on imports, and provincial cancer institutes rush to adopt SPECT/CT for community screening. Japan’s national insurance expanded coverage for sentinel-node mapping in early 2025, spurring higher technetium-99m demand at surgical oncology centers. India’s state governments subsidize gamma-camera purchases for district hospitals, broadening rural access. Multinational dose suppliers form joint ventures with local pharma groups to navigate licensing and distribution, thereby onboarding new end users into the technetium-99m market.

Europe maintains stable mid-single-digit growth, bolstered by long-established diagnostics protocols and cohesive regulatory frameworks that mandate LEU conversion for non-proliferation compliance. Reactor outages at Petten and HFR in 2024 prompted EU funding calls for alternative supply paths, including accelerator facilities in France and the Czech Republic. CERN-MEDICIS produces unconventional isotopes, exemplifying regional scientific depth. Although stringent transport rules raise logistics costs, harmonized radiation standards enable predictable cross-border dose movement inside the Schengen zone. Middle East & Africa and South America represent emerging pockets; Gulf states invest in tertiary centers replete with hybrid imaging suites, whereas Brazil and Argentina harness public–private partnerships to refurbish legacy reactors. Collectively, these initiatives broaden geographic diversification, buoying the technetium-99m market against isolated regional disruptions.

Competitive Landscape

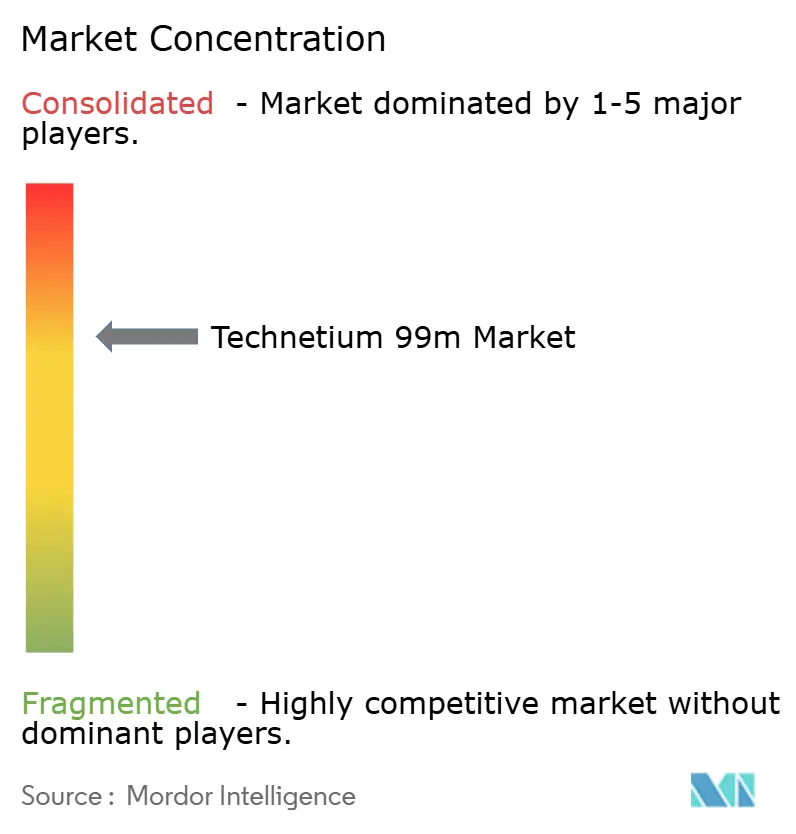

The technetium-99m market displays moderate concentration: GE HealthCare, Curium Pharma and Cardinal Health command pronounced positions through vertically integrated operations spanning Mo-99 sourcing, generator manufacturing and last-mile distribution. Combined, the top five hold roughly 55-60% global share, leaving headroom for challengers. Established players emphasize reliability, evidenced by long-term supply contracts with hospital networks and investments to secure LEU-based Mo-99. Cardinal Health, for instance, upgraded its national radio-pharmacy fleet with electronic chain-of-custody systems to assure compliant deliveries.

New entrants leverage technology niches and regional strategies. SHINE Technologies scales fusion‐driven Mo-99 production, expecting commercial shipments in 2026. In Europe, Eckert & Ziegler partners with hospital groups on mini-cyclotron pilots, offering service contracts that bundle uptime guarantees with isotope supply. Asian conglomerates, notably China National Pharmaceutical Group, integrate radiopharmaceutical lines into broader oncology portfolios. Patent activity centers on accelerator target design, radionuclide purification and automated compounding robots, with academic–industry consortia filing incremental improvements that aim to lower per-curie costs or increase specific activity.

M&A momentum continues: SHINE agreed in May 2025 to acquire Lantheus’ SPECT business, adding Tc-99m and xenon-133 products plus a manufacturing campus to its growing footprint. Such consolidation aligns with buyer ambitions to secure demand across therapeutic and diagnostic pipelines. Competitive intensity consequently shifts from price to security of supply, with vendors touting diversified production footprints in tender documents. Over the next five years the technetium-99m market will likely tilt toward hybrid business models, where suppliers bundle isotopes, instruments, software and clinical-training packages into holistic service propositions.

Technetium 99m Industry Leaders

GE HealthCare

Curium Pharma

Cardinal Health

Siemens Healthineers

Lantheus Medical Imaging

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: SHINE Technologies agreed to acquire Lantheus’ single-photon business, including technetium-99m and xenon-133 product lines plus manufacturing assets, accelerating SHINE’s push toward vertically integrated isotope supply.

- January 2025: Aspirus Wausau Hospital announced a USD 227 million expansion that adds advanced PET/CT scanners and upgraded nuclear imaging suites, reducing patient travel for critical diagnostics.

- September 2024: The FDA approved flurpiridaz F-18 for cardiac PET imaging, the first new cardiac PET tracer in decades, heightening competition for technetium-99m myocardial perfusion scans.

- January 2024: The British Columbia government committed USD 50.5 million to a new cyclotron and radiopharmacy laboratory in Vancouver to boost regional technetium-99m production capacity.

Global Technetium 99m Market Report Scope

| Reactor-based Generators |

| Cyclotron-based Production |

| Linear-Accelerator Production |

| LEU / Non-HEU Processes |

| Third-party Imports |

| Cardiology Imaging |

| Oncology Imaging |

| Neurology Imaging |

| Endocrine / Thyroid Imaging |

| Renal Imaging |

| Pulmonary Imaging |

| Tc-99m Cold Kits |

| Tc-99m Generators |

| Unit-Dose Radiopharmaceuticals |

| Hospitals |

| Diagnostic Imaging Centers |

| Contract Radiopharmacies |

| Academic & Research Institutes |

| Ambulatory Surgical Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Production Method | Reactor-based Generators | |

| Cyclotron-based Production | ||

| Linear-Accelerator Production | ||

| LEU / Non-HEU Processes | ||

| Third-party Imports | ||

| By Application | Cardiology Imaging | |

| Oncology Imaging | ||

| Neurology Imaging | ||

| Endocrine / Thyroid Imaging | ||

| Renal Imaging | ||

| Pulmonary Imaging | ||

| By Radiopharmaceutical Form | Tc-99m Cold Kits | |

| Tc-99m Generators | ||

| Unit-Dose Radiopharmaceuticals | ||

| By End User | Hospitals | |

| Diagnostic Imaging Centers | ||

| Contract Radiopharmacies | ||

| Academic & Research Institutes | ||

| Ambulatory Surgical Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current global value of the technetium-99m market?

The technetium-99m market size is valued at USD 6.94 billion in 2025 and is projected to reach USD 8.58 billion by 2030.

Which clinical area uses technetium-99m most extensively?

Cardiology imaging leads, accounting for 51.46% of global demand in 2024 due to widespread nuclear stress and perfusion testing.

Why are cyclotrons gaining traction for technetium-99m production?

Mini-cyclotrons enable on-demand local isotope supply, mitigating reactor outage risks and supporting an 8.24% CAGR for cyclotron-produced doses through 2030.

How did U.S. reimbursement changes affect nuclear cardiology?

The 2024 CMS policy allowing separate payment for radiopharmaceuticals over USD 630 eliminated historic cost barriers, prompting hospitals to expand cardiology SPECT programs.

Which region is forecast to grow fastest in technetium-99m adoption?

Asia-Pacific is expected to expand at a 6.24% CAGR to 2030 as China, India and Japan invest heavily in nuclear-medicine modernization.

What competitive strategies dominate the technetium-99m supplier landscape?

Leading firms emphasize vertically integrated supply chains and LEU-based Mo-99 security, while new entrants focus on accelerator technologies and regional penetration.

Page last updated on: