Silver Paste Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 2.85 Billion |

| Market Size (2031) | USD 3.61 Billion |

| Growth Rate (2026 - 2031) | 4.82% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

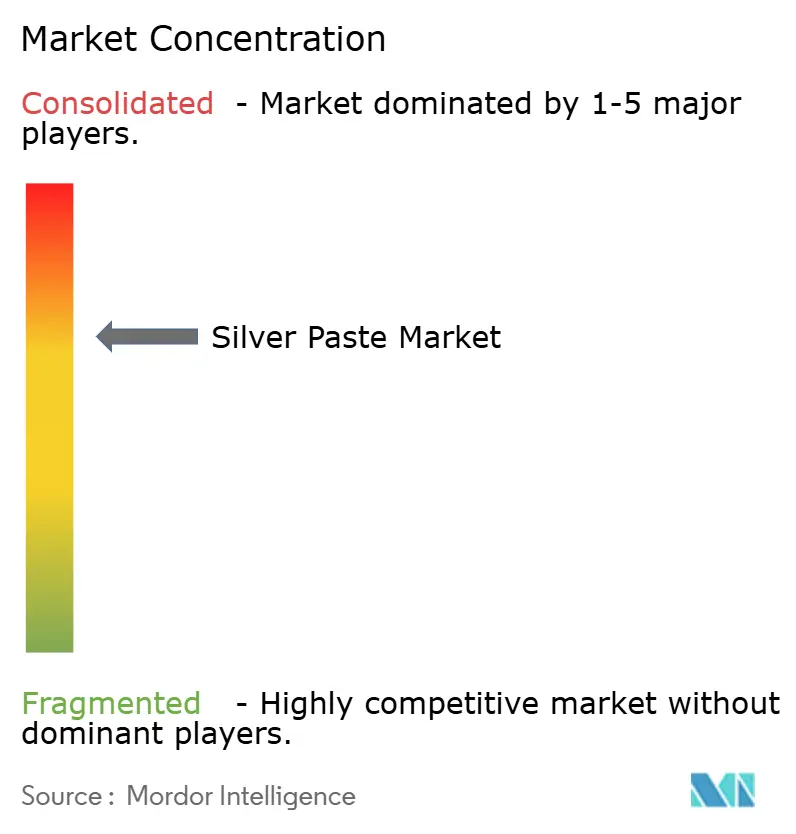

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Silver Paste Market Analysis by Mordor Intelligence

The Silver Paste Market size was valued at USD 2.72 billion in 2025 and is estimated to grow from USD 2.85 billion in 2026 to reach USD 3.61 billion by 2031, at a CAGR of 4.82% during the forecast period (2026-2031). Despite a surge in demand from end-users, especially in electric-vehicle power electronics and flexible-hybrid electronics, revenue growth has been muted. This is primarily due to the rising preference for copper-hybrid metallization and a significant move toward conserving silver. The Asia-Pacific region holds a dominant position, bolstered by a remarkable four-year surge in China's photovoltaic output. Furthermore, regional formulators are poised to benefit from a projected significant growth in silver-powder capacity by 2029. In a strategic pivot, Automotive Tier 1 suppliers are now opting for multi-year supply contracts linked to COMEX prices, stepping away from conventional spot buying. Meanwhile, European regulations on nano-silver emissions have tightened. This shift in regulations has led to varying compliance costs, with an advantage for suppliers who can effectively document their particle-size distributions and maintain 'safe-and-sustainable-by-design' credentials. The concept of a circular economy is gaining momentum: while recycled silver has carved out a significant niche in the global supply, the recycling of paste-grade lags behind bullion recovery. This gap exposes formulators to potential price swings during metal rallies.

Key Report Takeaways

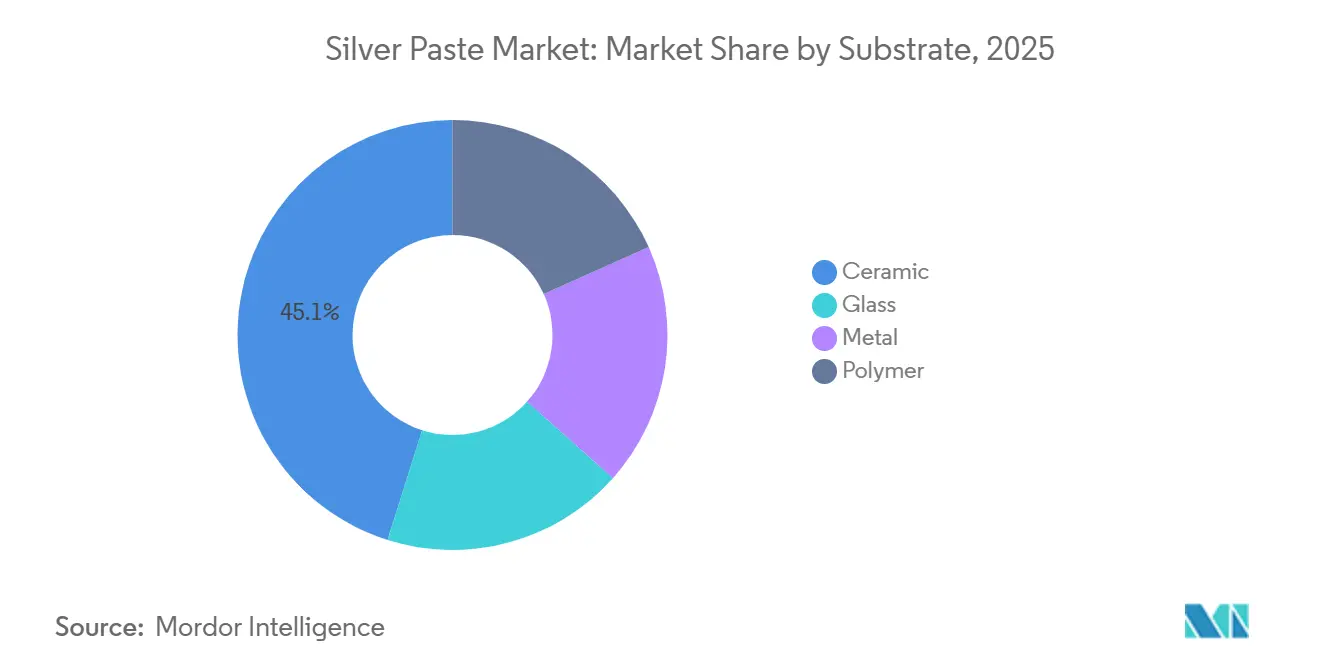

- By substrate, ceramic commanded 45.11% of the silver paste market share in 2025, while polymer recorded the highest 5.33% CAGR (2026-2031).

- By composition, silver flakes held 47.89% share of the silver paste market size in 2025, and silver nanoparticles posted the fastest 5.97% CAGR (2026-2031).

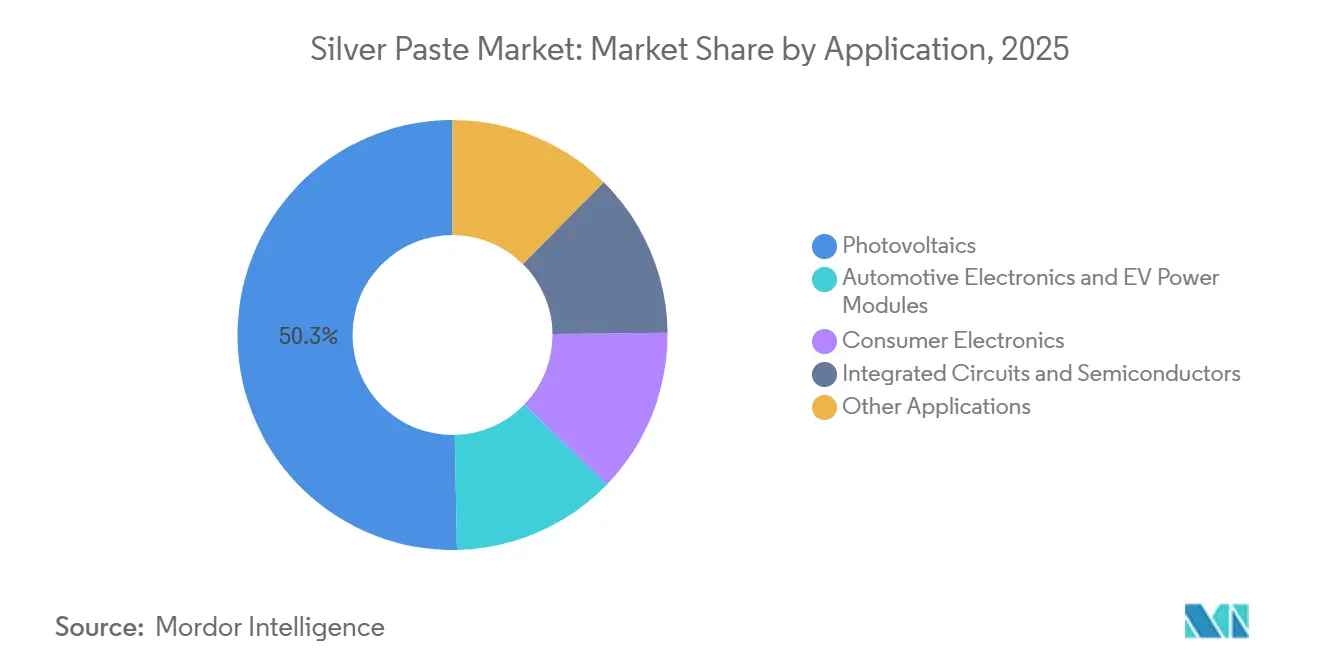

- By application, photovoltaics led with 50.34% revenue share in 2025; automotive electronics and EV power modules are set to expand at 7.12% CAGR (2026-2031).

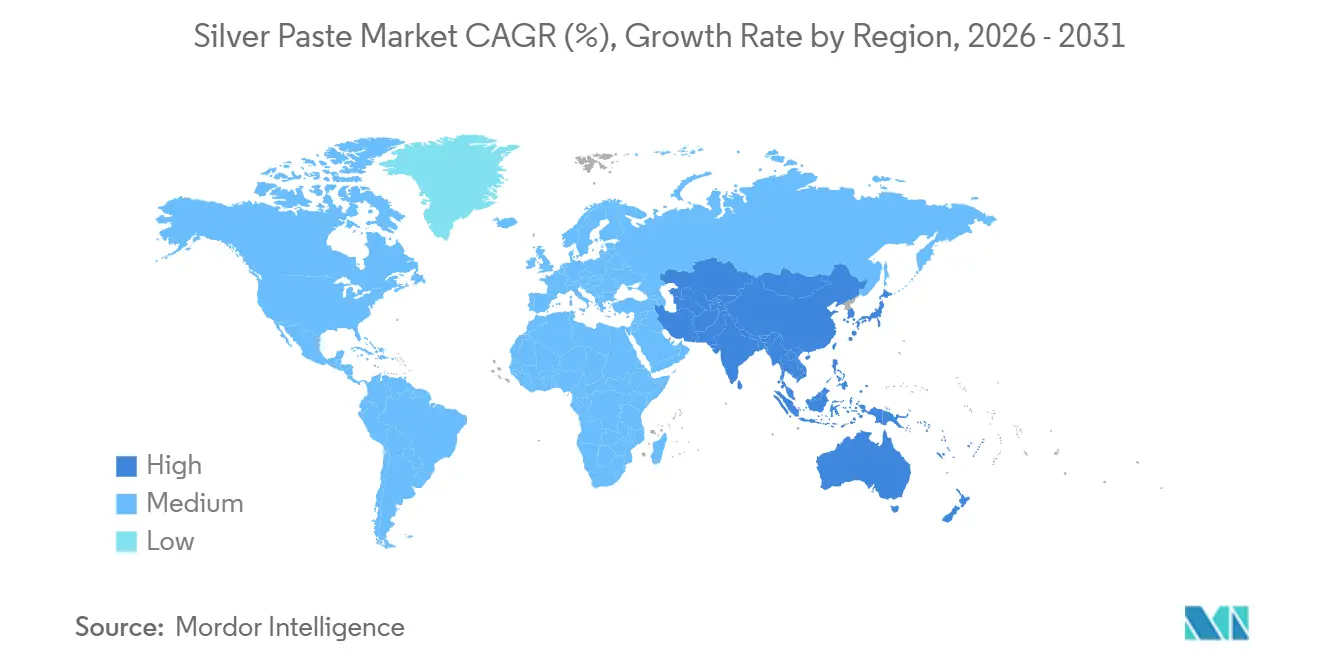

- By geography, Asia-Pacific accounted for 64.11% of the silver paste market share in 2025 and is advancing at a 6.33% CAGR (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Silver Paste Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of automotive and Electric Vehicle power-electronics integration | +1.8% | Global, concentrated in Asia-Pacific (China, South Korea, Japan) and Europe (Germany) | Medium term (2-4 years) |

| Boom in printed and flexible electronics manufacturing | +1.2% | Global, early adoption in North America and Asia-Pacific (South Korea, Japan, Taiwan) | Medium term (2-4 years) |

| Shift to sintered-silver attach in SiC/GaN power devices | +1.0% | Global, led by Asia-Pacific and Europe automotive hubs | Long term (≥4 years) |

| Emergence of low-temperature Ag₂O pastes for wearables and µLEDs | +0.7% | North America, Asia-Pacific (South Korea, Japan, China) | Long term (≥4 years) |

| Circular-economy push for silver-paste recovery and recycling | +0.5% | Europe (regulatory-driven), Asia-Pacific (supply security), North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of Automotive and Electric Vehicle Power-Electronics Integration

By 2025, battery-electric vehicles (BEVs) outpaced their internal-combustion engine (ICE) counterparts in silver consumption. Sintered-silver joints, now meeting IATF 16949 reliability standards, endure thousands of thermal cycles, spanning from -40 °C to 175 °C[1]“QuickSinter QS815-AR Product Data Sheet,” Indium Corporation, indium.com. In June 2025, LG Chem and Noritake introduced a room-temperature-stable nano-silver paste. This breakthrough extends the paste's shelf life from mere weeks to several months, negating the necessity for cold-chain logistics. Consequently, Tier 1 suppliers are increasingly opting for multi-year offtake agreements tied to metal futures - a fresh strategy in the silver paste arena. Moreover, with shear-strength retention proving resilient post-rigorous cycling, there is a marked surge in SiC adoption for traction inverters. These advancements are propelling the demand for automotive silver paste and bolstering consistent margin growth for adept suppliers.

Boom in Printed and Flexible Electronics Manufacturing

Wearable medical patches, curved displays, and polymer substrates now depend on conductive traces that cure at temperatures below 150 °C for their protection. Transparent silver pastes, after a 20-minute cure at 140 °C, achieve low sheet resistance, facilitating in-cell OLED driver integration. Meanwhile, copper-silver core-shell inks reach nearly identical conductivity levels but with a marked reduction in silver usage. This shift encourages formulators to reserve pure-silver systems for designs prioritizing performance. Although the silver paste market has seen a value boost from high-performance niches, its volume growth has not kept pace with device output, thanks to strides in material efficiency. Even as unit counts have surged in smart packaging, structural sensors, and foldable smartphones, leading to only modest tonnage increases, revenue growth has outstripped tonnage, fueled by rising average selling prices.

Shift to Sintered-Silver Attach in SiC/GaN Power Devices

Pressureless sintering has removed the clamp pressure constraint, which previously limited silver usage to thick dies. Heraeus's patented neodecanoate-coated particles, after a specific temperature treatment for a set duration, achieve high shear strength on bare copper. The resulting bondlines not only showcase superior thermal conductivity but also exhibit electrical resistivity that outperforms the SAC305 solder. This technology, initially adopted for EV traction inverters, has now expanded its reach to industrial drives and data center power supplies. As SiC MOSFETs gain traction across diverse end-markets, suppliers of silver paste, particularly those offering low-void formulations, are witnessing a surge in demand. This trend is expected to bolster mid-term growth projections for the silver paste market during the forecast period of 2026–2031.

Emergence of Low-Temperature Ag₂O Pastes for Wearables and µLEDs

Ag₂O and nano-silver chemistries, which sinter at temperatures between 110-150 °C, play a pivotal role in a range of applications, including PET and polyimide, as well as textile substrates. A newly developed stretchable paste can elongate by more than 100% and maintain its conductivity, even after multiple laundry cycles. Patents in the micro-LED domain underscore the precision of micro-printing, highlighting the use of silver inks to fill vias smaller than 50 µm. Integrated printed silver-zinc batteries have achieved significant advancements, powering epidermal sensors for extended durations. These innovations not only expand the silver paste market's traditional focus on rigid electronics but also introduce lucrative high-margin applications.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from lower-cost Cu/Al conductive materials | -1.5% | Global, most acute in Asia-Pacific (China) PV sector | Short term (≤2 years) |

| Supply-chain risk from limited silver-paste recycling capacity | -0.8% | Global, concentrated impact in Asia-Pacific and Europe | Medium term (2-4 years) |

| Stringent environmental regulations on nano-silver emissions | -0.6% | Europe (EU REACH, cosmetics ban), potential spillover to North America | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Competition from Lower-Cost Cu/Al Conductive Materials

Chinese cell manufacturers have transitioned silver-coated copper pilots from laboratories to production lines, successfully reducing silver usage per TOPCon wafer without compromising efficiency[2]“Solar Cell Copper Metallization Outlook 2026,” Silver Institute, silverinstitute.org. LONGi's adoption of fully copper-electroplated fingers indicates a potential reduction in silver usage per module. Similarly, RFID technology, touch screens, and disposable sensors are shifting toward copper-hybrid inks, meeting electrical standards while significantly reducing costs. While photovoltaics experience a direct revenue dip, the broader silver paste market is also impacted - formulators now face a critical choice between pursuing innovation and confronting the risk of commoditization.

Supply-Chain Risk from Limited Silver-Paste Recycling Capacity

In January 2026, when silver prices peaked, unhedged formulators faced significant margin declines. The scarcity of industrial-scale paste-grade recycling facilities has delayed the processing of collected scrap, prolonging its reintroduction as powder. Although a recycled feedstock initiative presents a promising solution, most suppliers in the Asia-Pacific region still rely on virgin metal, leaving them susceptible to price surges. To counteract risks in the silver paste market, it is crucial to establish dedicated refining lines swiftly.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Substrate: Ceramic Dominance Anchored in Power Electronics

In 2025, ceramics, driven by robust demand for direct-bonded-copper power modules requiring bondline conductivity exceeding 200 W/m·K, accounted for 45.11% of the revenue. This segment led the silver paste market share in 2025. Meanwhile, polymer substrates, due to their roles in flexible sensors, smart textiles, and foldable displays, recorded a 5.33% compound annual growth rate (CAGR) - the highest among substrates during the forecast period of 2026–2031.

Withstanding temperatures exceeding 250 °C and offering electrical isolation up to 10 kV, ceramics have cemented their position in electric vehicle (EV) inverters and industrial drives. However, innovations in form factors for polyimide and polyethylene terephthalate (PET) have tapped into a new market, surpassing the conventional thick-film hybrid-circuit sector. As formulators introduced low-temperature curing chemistries, polymer adoption increased significantly, all while maintaining healthy profit margins. This growth has notably benefited the silver paste market, particularly in the flexible electronics segment.

By Composition: Silver Flakes Lead, Nanoparticles Gain in Sintering

In 2025, silver flakes, widely recognized for their role in screen-printing hardware for solar cells, generated 47.89% of the market's revenue. On the other hand, silver nanoparticles, increasingly favored due to the rising adoption of SiC and GaN die-attach, are projected to expand at an annual rate of 5.97% during the forecast period of 2026–2031. This dynamic underscores the interplay of established technologies and emerging innovations in the silver paste market.

While silver flakes provide a cost-effective solution for high-volume photovoltaics, silver nanoparticle pastes stand out for their pressureless sintering capabilities and heightened reliability, especially in the automotive and aerospace sectors. Silver-coated copper hybrid particles strike a balance, offering a budget-friendly alternative with decent performance. This diverse array of options pushes suppliers to strategically segment their portfolios, ensuring they maintain healthy margins and a solid foothold in the silver paste market.

By Application: Photovoltaics Under Margin Pressure, Automotive Accelerating

In 2025, photovoltaics accounted for 50.34% of total revenue. However, as silver usage per watt fell below 70 mg, this share began to decline. At the same time, automotive electronics and EV power modules, which have been growing at a CAGR of 7.12% (2026-2031), have started to fill this gap. This shift is also expanding the silver paste market, particularly in high-reliability segments.

Die-attach pastes, specifically designed for 300 °C silicon carbide (SiC) junctions, command a premium price. This pricing strategy results in faster revenue growth compared to tonnage increases. The rising demand from data-center power and artificial intelligence (AI) infrastructure, which mirrors the thermal profiles observed in the automotive sector, presents new opportunities for expansion. Conversely, the increasing adoption of copper-hybrid inks in radio-frequency identification (RFID) and consumer displays limits potential volume growth for pure silver. As a result, the silver paste market is increasingly shifting toward performance-centric niches, with growth projected during the forecast period of 2026–2031.

Geography Analysis

In 2025, the Asia-Pacific region dominated the silver paste market, accounting for 64.11% of the revenue and projecting a growth rate of 6.33%. In 2025, driven by advancements to next-generation TOPCon lines, China's domestic sales of silver paste saw a notable surge. By 2029, as silver-powder production capacity is set to reach significant levels, the region not only solidifies its supply resilience but also faces heightened geopolitical risks.

Japan leads in technological innovations. A prominent company, utilizing proprietary atomization, dominates the market, supplying over 50% of the global PV-grade silver powder. Simultaneously, industry leaders like Kyocera, TANAKA, and Asahi Kagaku are at the forefront, offering specialty pastes with conductivity levels surpassing 240 W/m·K. In South Korea, LG Chem and Noritake's partnership is eyeing the automotive SiC attachment, leveraging the country's expanding EV battery landscape. While India and ASEAN nations act as economic assembly centers for commodity solar pastes, their dependence on imports for high-purity nanopowders highlights a limited scope for upstream diversification in the foreseeable future.

North America is establishing its presence through innovative strides. Indium Corporation and MacDermid Alpha have expanded their portfolios to include pressureless sintering. Meanwhile, Henkel has introduced inks with recycled silver, aligning with Scope 3 sustainability benchmarks. Europe adopts a more cautious stance, implementing bans on nano-silver in cosmetics and heeding the European Food Safety Authority's warnings about E 174. This regulatory push aims to curtail broader workplace exposures, prompting EU suppliers to adopt 'safe-by-design' strategies. Germany, fortified by Bosch and ZF's inverter lines, emerges as Europe's dominant volume player. Conversely, South America and the Middle-East predominantly depend on imported pastes for their photovoltaic initiatives. Although these regions hold promise for future growth, they currently lack significant revenue impact on the silver paste market.a

Competitive Landscape

The silver paste market is moderately consolidated. In a strategic move, suppliers are increasingly backward integrating into silver-powder production. This approach aims to challenge DOWA’s dominance and to mitigate potential supply disruptions. Concurrently, innovators such as Bert Thin Films, with their copper-hybrid solutions, pose a challenge by potentially capping silver volumes in cost-sensitive sectors. This situation compels established vendors to emphasize performance credentials and total cost of ownership to maintain their market position in silver paste.

Silver Paste Industry Leaders

Heraeus Electronics

DuPont

Giga Solar Materials Corp.

Henkel AG & Co. KGaA

MacDermid Alpha Electronics Solutions

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: LG Chem and Noritake developed a high-performance silver paste for automotive power semiconductors. The paste contains nano-sized silver particles that eliminate cold storage requirements while delivering enhanced heat resistance and thermal conductivity for silicon carbide chip bonding applications.

- May 2025: MacDermid Alpha Electronics Solutions expanded its Singapore production facility for Argomax silver sintering paste. The expansion, supported by the Singapore Economic Development Board, aims to address the increasing global demand from the electric vehicle industry and strengthen the company's next-generation material innovation capabilities.

Global Silver Paste Market Report Scope

Silver paste is defined as a highly conductive, viscous material composed of silver particles, such as flakes, powder, or nanoparticles, along with binders and solvents. It is widely used in the electronics sector for screen printing, enabling the formation of conductive pathways on substrates like ceramics, glass, and polymers. This material is essential for applications in photovoltaics, automotive sensors, and microelectronics.

The conductive silver paste market is segmented by substrate, composition, application, and geography. By substrate, the market is segmented into ceramic, glass, metal, and polymer. By composition, the market is segmented into silver flakes, silver nanoparticles, silver powders, and other compositions. By application, the market is segmented into photovoltaics (solar cells), automotive electronics and EV power modules, consumer electronics (displays, wearables), integrated circuits and semiconductors, and other applications (RFID, LEDs, medical devices). The report also covers the market size and forecasts for the market in 17 countries across major regions. For each segment, the market sizing and forecasts are done based on value (USD).

| Ceramic |

| Glass |

| Metal |

| Polymer |

| Silver Flakes |

| Silver Nano Particles |

| Silver Powders |

| Other Composition |

| Photovoltaics (Solar Cells) |

| Automotive Electronics and EV Power Modules |

| Consumer Electronics (displays, wearables) |

| Integrated Circuits and Semiconductors |

| Other Applications (RFID, LEDs, medical devices) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Substrate | Ceramic | |

| Glass | ||

| Metal | ||

| Polymer | ||

| By Composition | Silver Flakes | |

| Silver Nano Particles | ||

| Silver Powders | ||

| Other Composition | ||

| By Application | Photovoltaics (Solar Cells) | |

| Automotive Electronics and EV Power Modules | ||

| Consumer Electronics (displays, wearables) | ||

| Integrated Circuits and Semiconductors | ||

| Other Applications (RFID, LEDs, medical devices) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is global silver paste revenue expected to be by 2031?

Forecasts point to USD 3.61 billion in 2031, up from USD 2.85 billion in 2026, registering a 4.82% CAGR in the 2026-2031 period.

Which end-use is on track for the quickest silver paste growth through 2031?

Automotive electronics and EV power modules are projected to rise at a 7.12% CAGR (2026-2031), the fastest among all applications.

Why is Asia-Pacific set to remain the dominant buyer of silver paste?

China’s surging photovoltaic output and regional powder capacity increase underpin a 6.33% CAGR (2026-2031) for the region.

What impact do tightening EU rules have on nano-silver paste makers?

The 2025 ban on colloidal nano-silver in cosmetics and EFSA’s safety concerns are driving extra testing, labeling, and documentation costs for European suppliers.

Which materials innovation is shaping paste choices for high-temperature EV power modules?

Pressureless nano-silver sintering that endures 300 °C junctions is displacing traditional solder in SiC and GaN devices.

Page last updated on: