Shrimp Feed Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 7.88 Billion |

| Market Size (2031) | USD 10.22 Billion |

| Growth Rate (2026 - 2031) | 5.35% CAGR |

| Fastest Growing Market | Africa |

| Largest Market | Asia Pacific |

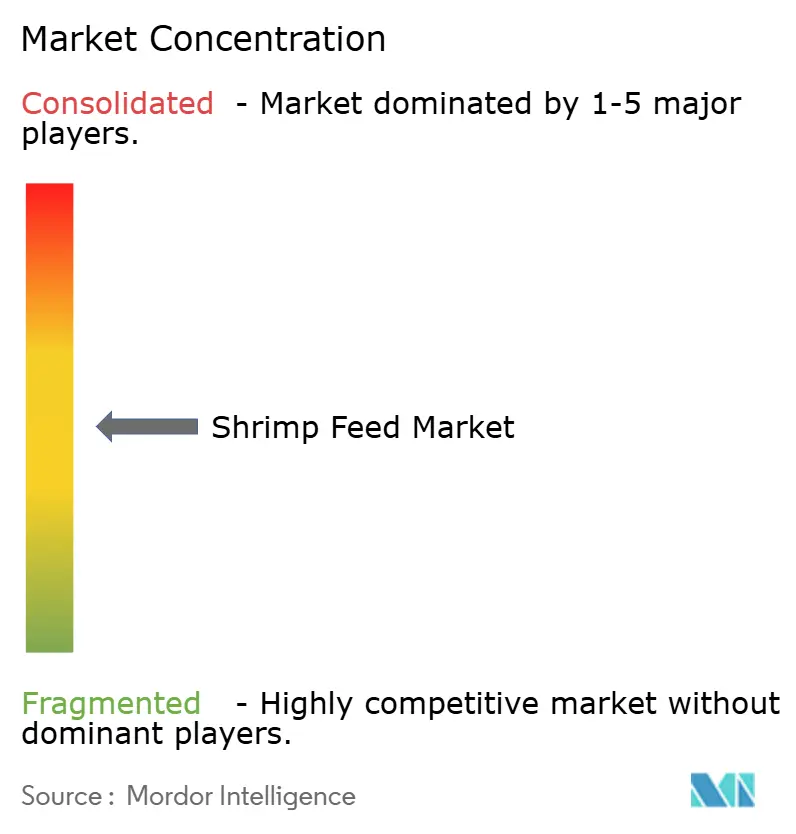

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Shrimp Feed Market Analysis by Mordor Intelligence

The shrimp feed market was valued at USD 7.5 billion in 2025 and is projected to grow from USD 7.88 billion in 2026 to USD 10.22 billion by 2031, registering a CAGR of 5.35% during the forecast period from 2026 to 2031. Growth is driven by the intensification of aquaculture in Asia-Pacific and South America, increasing demand for protein-rich seafood among middle-income consumers, and the adoption of functional additives that reduce disease-related losses in high-density systems. Precision nutrition platforms utilizing real-time sensor inputs are improving feed efficiency, while the incorporation of insect and algae proteins in commercial formulas helps mitigate the impact of fishmeal price fluctuations. However, recurring disease outbreaks and volatile marine raw material costs continue to pressure producer margins and limit short-term growth in the shrimp feed market.

Key Report Takeaways

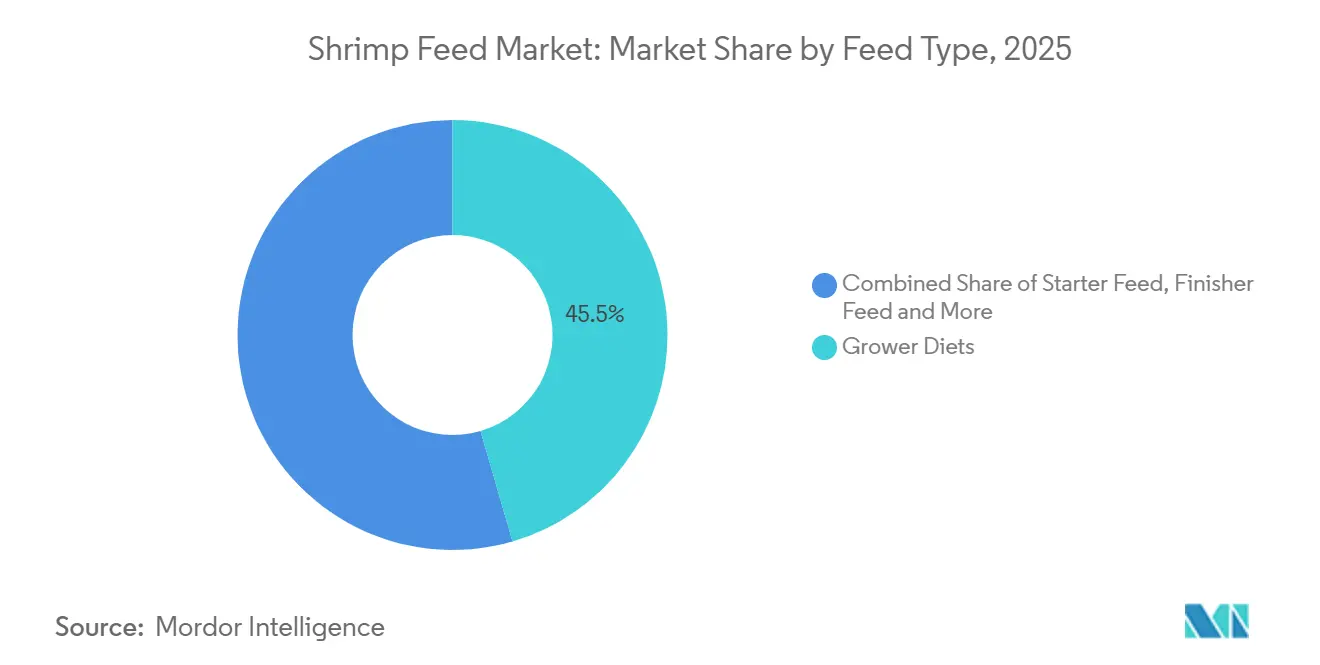

- By feed type, grower feed accounted for the largest 45.5% market share of the shrimp feed market in 2025, while the functional and medicated feed market size is projected to grow at the fastest CAGR of 9.0% from 2026 to 2031.

- By form, pellets accounted for the largest 66% market share of the shrimp feed market in 2025, while the liquid feed market size is projected to grow at the fastest CAGR of 10.0% from 2026 to 2031.

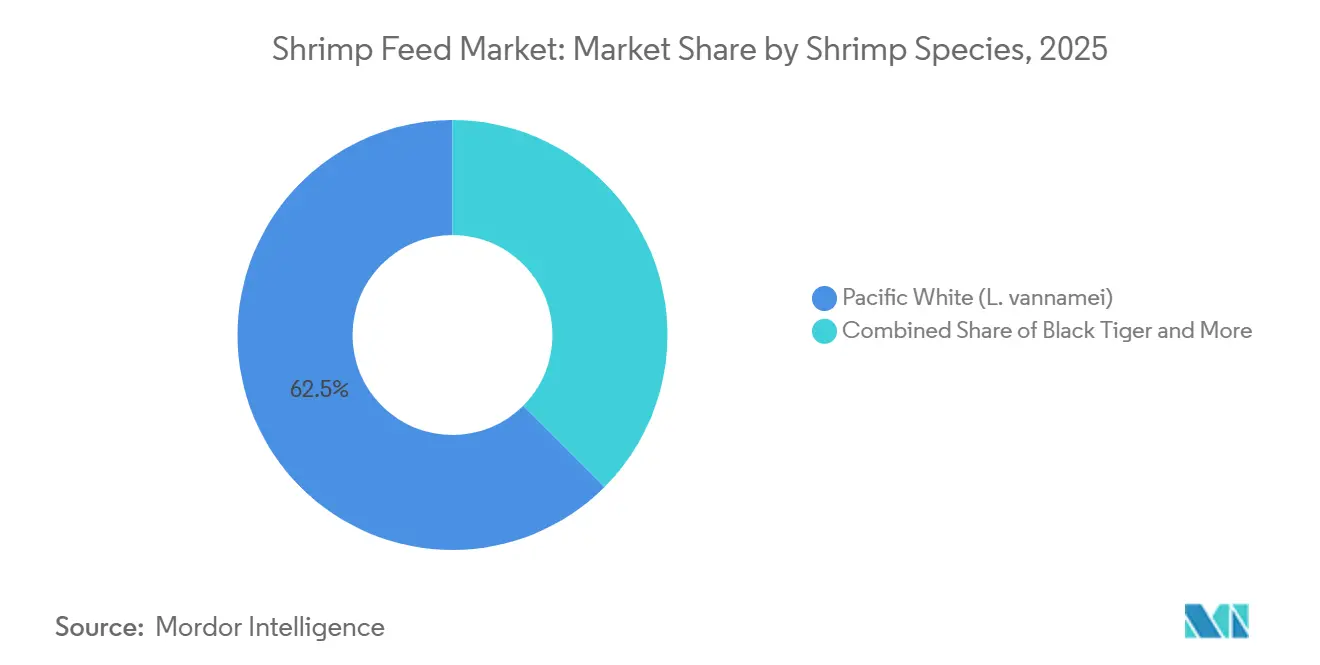

- By shrimp species, Pacific white feed accounted for the largest 62.5% market share of the shrimp feed market in 2025, while the black tiger market size is projected to grow at the fastest CAGR of 7.6% from 2026 to 2031.

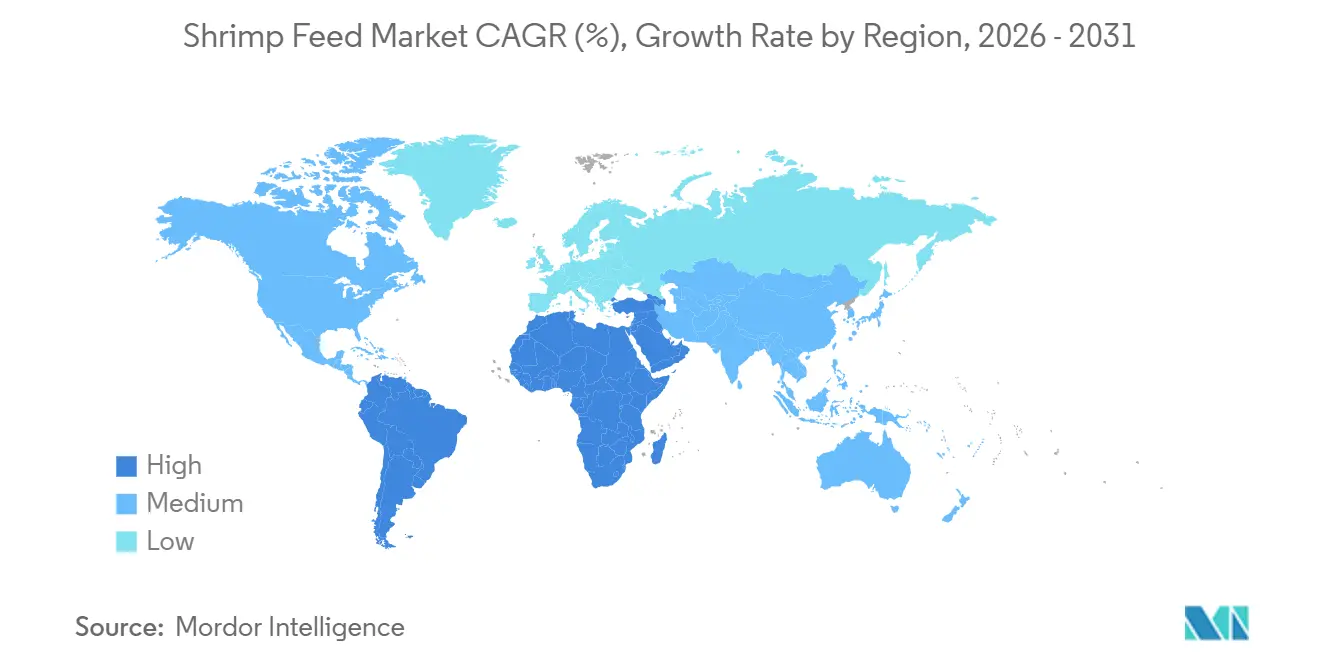

- By geography, Asia-Pacific accounted for the largest 70% market share of the shrimp feed market in 2025, while the Africa market size is projected to grow at the fastest CAGR of 9.0% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Shrimp Feed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising seafood consumption and protein-rich diet demand | +1.2% | Global focus in Asia-Pacific, North America, and Europe | Medium term (2–4 years) |

| Expansion of intensive shrimp aquaculture in key regions | +1.5% | China, India, Vietnam, Indonesia, Ecuador, and Brazil | Long term (≥ 4 years) |

| Advances in functional additives and immunostimulants usage | +0.9% | Vietnam, Thailand, Ecuador, and global roll-out | Medium term (2–4 years) |

| Adoption of AI-enabled precision feeding systems | +0.6% | Ecuador, Vietnam, Thailand, pilot scale in China and India | Short term (≤ 2 years) |

| Carbon labeling driving insect and algae protein adoption | +0.4% | Europe, North America, and spillover to Asia-Pacific exporters | Long term (≥ 4 years) |

| Demand for specialized feeds for disease-resistant larvae | +0.7% | India, Vietnam, Indonesia, and Ecuador | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Seafood Consumption and Protein-Rich Diet Demand

Global shrimp feed demand is supported by rising aquaculture output, with farmed shrimp production reaching around 6 million metric tons in 2025[1]Source: Food and Agriculture Organization (FAO), “Shifts in the Global Shrimp Trade and Production,” fao.org. The shrimp feed market has directly benefited as farmers increase stocking densities and adopt high-protein diets to accelerate grow-out cycles. Ecuador’s shrimp exports reached 1.39 million metric tons in 2025, with China accounting for approximately 48% of total shipments, underscoring Asia’s significant role in driving global shrimp consumption growth. Feed manufacturers are incorporating probiotics and immunostimulants to reduce antibiotic usage and comply with sustainability standards in the European Union and the United States.

Expansion of Intensive Shrimp Aquaculture in Key Regions

Indonesia is developing an integrated aquaculture hub focused on shrimp farming and feed production to decrease feed imports and enhance value chain efficiency. In 2025, Vietnam is focusing on expanding recirculating aquaculture systems in Ca Mau, particularly for shrimp farming, with an emphasis on obtaining Best Aquaculture Practices (BAP) certification. Similarly, China is adopting biofloc pond systems to enhance shrimp farming, aiming to improve water quality and feed utilization efficiency. Meanwhile, Ecuador's commercial shrimp farms are striving to optimize feed-conversion ratios, and pilot ponds in India for black tiger shrimp farming are setting new efficiency benchmarks.

Advances in Functional Additives and Immunostimulants Usage

Advancements in functional additives and immunostimulants are driving growth in the shrimp feed market by enhancing disease resistance and improving farm productivity. A 2024 study published in Aquaculture Reports demonstrated that β-glucan supplementation significantly increased shrimp survival rates under Vibrio harveyi challenge, underscoring its role in boosting immune response and mitigating pathogen effects. These enhancements in survival and health outcomes support improved production efficiency and profitability, promoting the broader use of functional feed additives among shrimp farmers.

Adoption of AI-Enabled Precision Feeding Systems

Producers in Ecuador, Vietnam, and Thailand utilize smart blowers connected to dissolved-oxygen probes and camera systems that halt feeding when activity decreases. Nutreco N.V. (Skretting)'s 360 Plus suite improves feeding efficiency by utilizing precision feeding, real-time data analytics, and automated feeding systems. These features help optimize feed usage and minimize overfeeding losses. A research and development center in Singapore, managed by the Singapore Food Agency and supported by organizations including Singapore Aquaculture Technologies, is developing machine-learning algorithms for tropical aquaculture systems. The focus areas include predictive analytics, feeding optimization, and water quality management.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in fishmeal and fish oil prices | -0.8% | Asia-Pacific and South America | Short term (≤ 2 years) |

| Disease outbreaks disrupting shrimp feed demand | -0.6% | Vietnam, India, Indonesia, China, and Ecuador | Short term (≤ 2 years) |

| Stricter antibiotic and additive regulations in markets | -0.4% | United States, European Union, and Japan | Medium term (2–4 years) |

| Anti-dumping risks on key amino acid inputs | -0.3% | North America and European Union supply chains | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Volatility in Fishmeal and Fish Oil Prices

Peru's fishmeal free-on-board quotations have been rising over the past few years. The prospect of lower supply in the final quarter created a "new normal" for higher fishmeal prices. In December 2025, fishmeal prices continued to rise, even with the revised USD 1.63 million mt quota. This is primarily due to reduced anchovy quotas, which constrained the supply of raw materials[3]Source: Food and Agriculture Organization (FAO), “Quarterly Fishmeal and Fish Oil Analysis”, fao.org. China accounts for a significant share of global supply, maintaining a higher price floor than earlier levels. Avanti Feeds reported that domestic fishmeal prices have risen substantially over time. These price surges have compressed profit margins and driven a shift toward alternative protein sources such as soybean, insect, and single-cell proteins.

Disease Outbreaks Disrupting Shrimp Feed Demand

Disease outbreaks have a substantial impact on shrimp feed demand by adversely affecting shrimp health, survival rates, and feeding behavior. A 2024 study published by researchers from the University of Malaya found that infected shrimp often exhibit anorexia (reduced feeding), lethargy, and impaired growth, leading to decreased feed intake and inefficient feed utilization during disease events. These health issues diminish overall productivity and profitability, leading farmers to reduce stocking densities or delay production cycles. Consequently, feed consumption decreases during and after outbreaks, leading to demand fluctuations and hindering consistent market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Feed Type: Functional Blends Outpace Commodity Diets

Grower feed is projected to account for the largest market share of 45.5% in the shrimp feed market by 2025, as it corresponds to the longest production phase when daily feed intake is at its peak. The functional and medicated feed market size is projected to grow at the fastest CAGR of 9.0% from 2026 to 2031, driven by stricter residue limits in the United States and European Union, which encourage the use of additives that boost immunity. Starter formulas, while generating lower revenue, command premium pricing due to the high mortality risk during the initial days. Feed mills, such as Grobest, have reported field feed-conversion ratios below 1.3 when using proprietary functional ingredients, demonstrating the economic benefits that support their continued adoption.

Functional blends contribute to improved manufacturer margins. Vietnamese ponds utilizing beta-glucan fortified diets have demonstrated profitability, highlighting farmers' readiness to invest in disease mitigation strategies. In India, the growing production of black tiger post-larvae is projected to drive demand for nursery diets with customized amino acid profiles. While finisher diets remain a niche segment, they are being reformulated to enhance pigmentation and flesh firmness, attributes increasingly sought by premium retailers. These developments collectively signify a qualitative transformation in the shrimp feed market.

By Form: Liquid Delivery Gains Traction

Pellets are projected to account for the largest market share of 66% in the shrimp feed market by 2025, driven by established extrusion processes and compatibility with automated feeders. However, the liquid feed market size is anticipated to grow at the fastest CAGR of 10.0% from 2026 to 2031. The spray-coating process enables the addition of heat-sensitive vitamins, enzymes, and probiotics after extrusion, preserving the bioactivity of these ingredients. Additionally, precision dosing minimizes leaching, which is particularly beneficial in recirculating systems where water stability is critical.

AI-enabled blowers are capable of metering liquid shots based on real-time biomass estimates, contributing to reduced feed usage. Indonesia's newly established integrated hub focuses on liquid supplements tailored for its biofloc modules. Crumbles are designed for post-larvae and early juveniles, with optimized particle sizes enhancing ingestion rates, while powdered diets remain limited to hatchery Artemia replacement. The high service intensity and additive content of liquid feeds support premium pricing, expanding the value potential within the shrimp feed market.

By Shrimp Species: Black Tiger Resurgence Widens Species Mix

The Pacific white shrimp is projected to account for the largest market share of 62.5% in the shrimp feed market by 2025. However, the market share for Pacific white shrimp may experience a slight contraction as farmers diversify to mitigate species-related risks. Meanwhile, the black tiger shrimp market size is projected to grow at the fastest CAGR of 7.6% from 2026 to 2031. This growth surpasses the overall market, driven by advancements in specific-pathogen-free genetics. Additionally, Indian shrimp production has increased, with corresponding feed volumes rising proportionally.

Premium export prices partly offset higher stocking costs and create opportunities for the adoption of pigment-enhanced diets, which are increasingly preferred for their ability to enhance shrimp quality. Revival programs in the Philippines replicate this approach, ensuring a steady rise in incremental demand for shrimp feed. Kuruma and other niche shrimp species continue to serve as specialty products in markets like Japan and Australia, where they utilize customized feeds tailored to their specific needs, though they contribute only modest volumes.

Geography Analysis

In 2025, the Asia-Pacific region accounted for the largest market share of 70% in the shrimp feed market. This dominance was driven by China’s target and India’s increasing shift toward black tiger shrimp production. Vietnam introduced recirculating ponds, while Indonesia invested in a shrimp production hub, contributing to structural volume growth. Regional governments are promoting antibiotic-free protocols to meet European Union and United States market standards, encouraging the adoption of functional feeds. Multinational feed mills are expanding their capacities in China, Vietnam, and India, reinforcing Asia’s leading position in the shrimp feed market.

The African shrimp market size is projected to grow at a CAGR of 9.0% from 2026 to 2031. Tanzania’s World Bank-funded TASFAM program, launched in 2026, aims to expand aquaculture production, including shrimp output, while Egypt continues to dominate continental aquaculture[2]Source: World Bank, “Tanzania Scaling-up Sustainable Marine Fisheries and Aquaculture Management Project (TASFAM)”, worldbank.org. New feed plants in Nigeria and Kenya are reducing supply chain distances and freight costs, making commercial shrimp diets more accessible to small-scale farmers. With low baseline adoption, incremental capacity increases directly translate into new demand, positioning Africa as a key growth frontier in the shrimp feed market.

South America ranks as the second-largest shrimp feed market, with Ecuador achieving shipment growth in 2025. Precision feeding systems are becoming widespread, reducing feed conversion ratios and driving formulation improvements across the region. Brazil’s northeast coast is expanding semi-intensive shrimp ponds to meet domestic retail demand, while Central American farms are shifting toward value-added headless-shell-on shrimp packs, which require specific diet pigmentation. These advancements solidify South America’s position as the fastest-growing mature market for shrimp feed.

Competitive Landscape

The shrimp feed market is moderately concentrated, with five leading companies dominating the landscape, which includes Charoen Pokphand Foods Public Company Limited, Cargill, Incorporated, Skretting (Nutreco N.V.), Guangdong Haid Group Co., Ltd., and Tongwei Co., Ltd. In April 2025, Charoen Pokphand completed the buy-out of C.P. Pokphand’s minority shareholders, gaining full control over Vietnamese and Chinese feed-to-food chains. This move enabled streamlined research and development budgeting.

Technology has emerged as a critical competitive factor in the shrimp feed market. Skretting (Nutreco N.V.)’s 360 Plus data platform integrates sensors, predictive analytics, and smart blowers to enhance water quality and minimize feed waste, thereby strengthening customer retention. In July 2025, Grobest Holdings Limited achieved Vietnam’s first Aquaculture Stewardship Council feed certification, positioning itself as a key compliance partner for exporters navigating European traceability regulations.

Guangdong Haid Group Co., Ltd. expanded its international presence in late 2025 by establishing overseas facilities such as an animal health products site in Vietnam, a complete feed facility in Cambodia, and a mixed diets plant in Nigeria. The company has set a target of achieving significant overseas sales by 2030, reflecting its ambitious global growth strategy. Meanwhile, mid-tier companies such as Avanti Feeds Limited are investing in Ecuador to leverage regional opportunities. Additionally, start-ups specializing in insect and algae-based proteins are testing alternative solutions that may challenge the raw material advantages of established players.

Shrimp Feed Industry Leaders

Charoen Pokphand Foods Public Company Limited

Cargill, Incorporated

Skretting (Nutreco N.V.)

Guangdong Haid Group Co., Ltd.

Tongwei Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Avanti Feeds Limited approved a USD 3 million investment to acquire a 10% stake in Thai Union Group Public Company Limited Ecuador. This marks the company's official entry into the South American market and positions it to capitalize on Ecuador's significant shrimp industry growth.

- December 2025: Skretting (Nutreco N.V.) has partnered with Longyang Fresh to strengthen its presence in major shrimp farming regions. This collaboration focuses on developing advanced, region-specific shrimp feed aimed at improving feed efficiency and farm productivity.

- October 2025: Skretting (Nutreco N.V.) has launched the next generation of its flagship shrimp feeds, Lorica and Optiline. These products are the first in Skretting (Nutreco N.V.)'s shrimp portfolio to incorporate EDGEOS PhytoComplexes.

Global Shrimp Feed Market Report Scope

Shrimp feed is a formulated diet that supplies essential nutrients, including proteins, lipids, vitamins, and minerals, necessary for the growth, survival, and productivity of farmed shrimp. The global shrimp feed market report is segmented by feed type (starter feed, grower feed, finisher feed, and functional/medicated feed), by form (pellets, crumbles, powder, and liquid feed), by shrimp species (pacific white, black tiger, and other species), and by geography (north america, south america, europe, asia-pacific, middle east, and africa). The market forecasts are provided in terms of value (USD).

| Starter Feed |

| Grower Feed |

| Finisher Feed |

| Functional / Medicated Feed |

| Pellets |

| Crumbles |

| Powder |

| Liquid Feed |

| Pacific White |

| Black Tiger |

| Other Species |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Ecuador | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Vietnam | |

| Indonesia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | Egypt |

| South Africa | |

| Rest of Africa |

| By Feed Type | Starter Feed | |

| Grower Feed | ||

| Finisher Feed | ||

| Functional / Medicated Feed | ||

| By Form | Pellets | |

| Crumbles | ||

| Powder | ||

| Liquid Feed | ||

| By Shrimp Species | Pacific White | |

| Black Tiger | ||

| Other Species | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Ecuador | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Vietnam | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | Egypt | |

| South Africa | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the forecast value of the shrimp feed market by 2031?

It is projected to reach USD 10.22 billion by 2031 at a 5.35% CAGR from USD 7.88 billion in 2026.

Which region accounts for the largest share of shrimp feed demand?

Asia-Pacific held the largest market share of 70% of global revenue in 2025 due to large-scale farming in China, India, Vietnam, and Indonesia.

Which feed form is growing the fastest?

Liquid feed is advancing at the fastest 10.0% CAGR from 2026 to 2031 as spray-coating enables precise delivery of heat-sensitive additives.

How are fishmeal price swings affecting feed makers?

Volatile marine raw-material costs push formulators toward soybean, insect, and single-cell proteins, raising reliance on costly amino-acid supplements.

Page last updated on: