Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

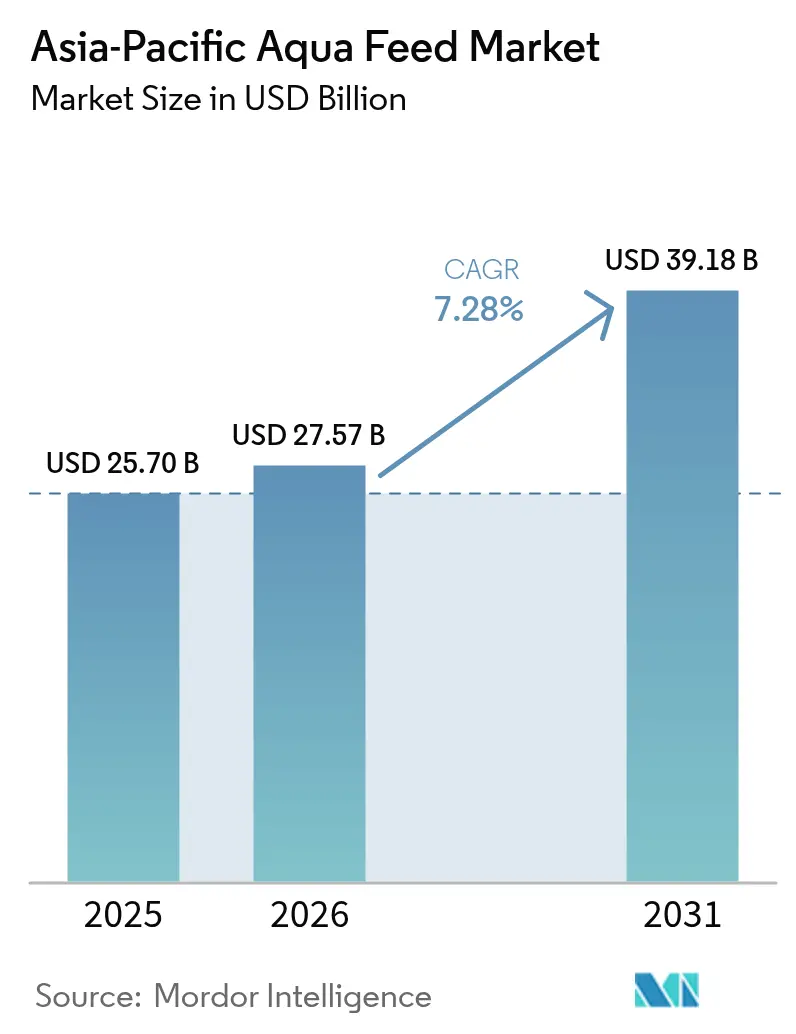

| Base Year Market Size (2025) | USD 25.7 Billion |

| Market Size (2026) | USD 27.57 Billion |

| Market Size (2031) | USD 39.18 Billion |

| Growth Rate (2026 - 2031) | 7.28% CAGR |

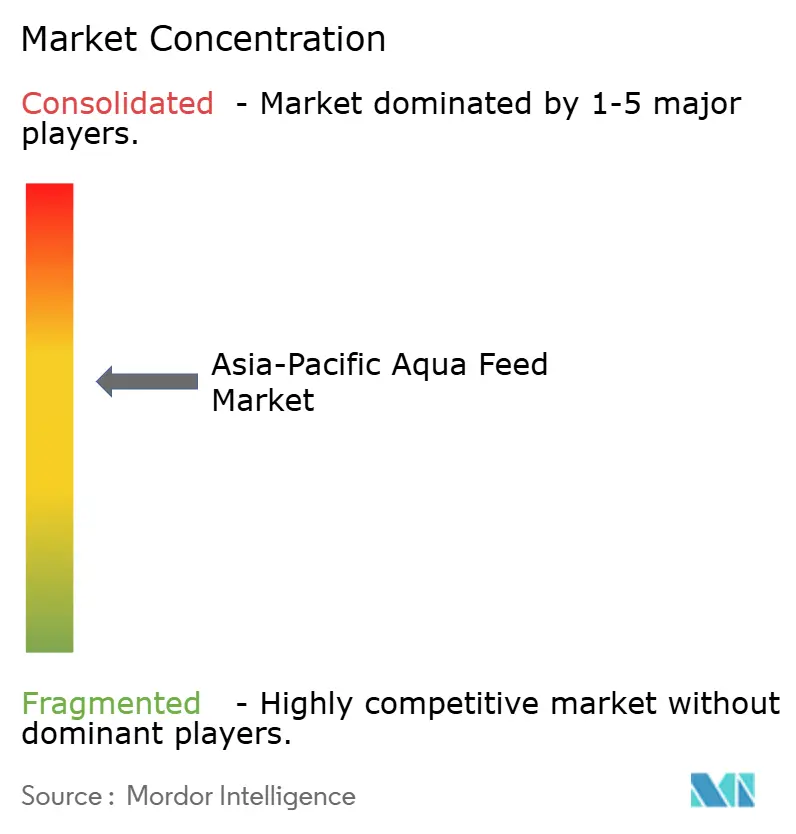

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Aqua Feed Market Analysis by Mordor Intelligence

Asia-Pacific aquafeed market size in 2026 is estimated at USD 27.57 billion, growing from 2025 value of USD 25.7 billion with 2031 projections showing USD 39.18 billion, growing at 7.28% CAGR over 2026-2031. This growth is driven by the anticipated increase in consumption of aquatic animal products, with Asia representing the largest market share.[1]OECD, “Aquaculture Production Statistics 2024,” OECD, oecd.org Robust demand emerges from sharply rising fish and shrimp output, tighter government food-security agendas, and a decisive shift toward high-performance feed formulas that limit disease losses and lower environmental footprints. Intensifying production targets in China and India now blend with stronger urban seafood demand, spurring investments in extruded feed technology, functional additives, and precision nutrition research. Meanwhile, soaring ingredient volatility around fishmeal and fish oil propels soybean meal and novel proteins into core feed rations, even as regulators clamp down on phosphorus discharge. Taken together, these forces position the Asia-Pacific aquafeed market for steady value growth while widening the gap between technology-enabled suppliers and purely volume-based producers.

Key Report Takeaways

- By species, fish feed held 51.35% of the Asia-Pacific aquafeed market share in 2025, and crustaceans are advancing at an 8.22% CAGR through 2031.

- By ingredient, soybean meal captured 33.20% of the Asia-Pacific aquafeed market size in 2025, and functional additives are forecast to post a 9.85% CAGR to 2031.

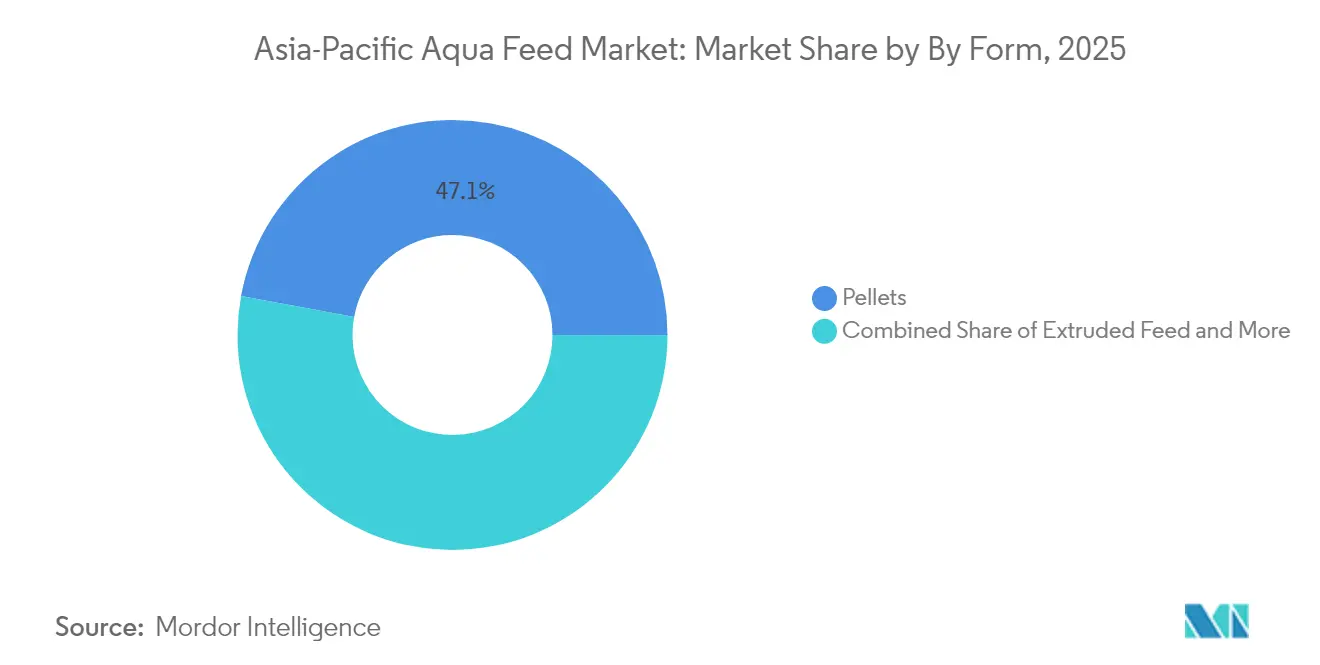

- By form, pellets led with 47.10% revenue share in 2025, and extruded feed is projected to expand at a 9.22% CAGR between 2026 and 2031.

- By geography, China accounted for 42.05% of the Asia-Pacific aquafeed market size in 2025, and India is primed for a 6.84% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Aqua Feed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying aquaculture production in China and India | +2.10% | China and India with spillover to Vietnam and Thailand | Medium term (2-4 years) |

| Rising seafood consumption driven by income growth | +1.80% | Urban centers across core Asia-Pacific markets | Long term (≥ 4 years) |

| Advances in nutritionally balanced, species-specific formulations | +1.20% | China, India, and Vietnam | Medium term (2-4 years) |

| Increasing adoption of extruded aquafeed for improved digestibility | +0.90% | China, Thailand, Vietnam, and Indonesia | Short term (≤ 2 years) |

| Government push for integrated multi-trophic aquaculture | +0.60% | India and China with pilot rollouts in Thailand and Vietnam | Long term (≥ 4 years) |

| Expansion of offshore cage farming | +0.40% | China and Vietnam with early interest in Indonesia and Thailand | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Intensifying Aquaculture Production in China and India

China’s aquaculture output in 2024 represented a modest year-over-year rise and underscores Beijing’s policy commitment to diversifying national protein sources. India mirrors that focus but wrestles with disease-linked losses each year. Larger pond stocking densities and expanding shrimp estates, therefore, compel feed makers to deliver higher amino-acid precision and stronger immune additives. Local supply chain investments in Vietnam and Thailand benefit as regional processing hubs capture a portion of surging raw-feed demand. Enforcement of stricter ingredient standards by China’s Ministry of Agriculture and Rural Affairs raises compliance hurdles, favoring producers that can document nutrient consistency and traceability.

Rising Seafood Consumption Driven by Income Growth

Seafood demand in the Asia-Pacific is flourishing, lifted by swelling middle-class wallets and fast-urbanizing diets. Domestic buyers across Shanghai, Mumbai, and Jakarta fuel a premium shift that rewards feed with superior digestibility, flavor, and shelf-life performance. As producers command higher farm-gate prices, they allocate bigger budgets toward functional additives that protect stock health, reinforcing a virtuous spending loop for quality formulations. Indonesia’s goal of 2 million metric tons of shrimp output galvanizes local hatcheries, even if timelines appear optimistic in light of infrastructure gaps.

Advances in Nutritionally Balanced, Species-Specific Formulations

Research showing 15-20% feed-conversion improvement through tailored amino-acid profiles is accelerating precision nutrition adoption. Probiotics such as Bacillus coagulans increasingly feature in Asian formulas to fortify gut health and lower antibiotic reliance. SHV Holding's (Skretting) Hezhoubei facility exemplifies deep investment in local species trials, while phosphorus-discharge caps push formulators to minimize waste without compromising growth. As regulators monitor nitrogen effluent more closely, balanced profiles that raise digestibility become economic necessities. Premium pricing gains acceptance when documented through growth trials, solidifying a shift away from cost-only buying criteria.

Increasing Adoption of Extruded Aquafeed for Improved Digestibility

Extruded feed raises protein digestibility by roughly 10-15% and reduces in-pond disintegration, lowering waste in systems where feed can exceed half of operating costs[2]Bonnie Waycott, “A Singular Focus: Making Single-Cell Proteins a Fixture on the Aquaculture Feed Ingredient Menu,” Global Seafood Alliance, globalseafood.org. Early adopters in Thailand and Vietnam retrofit lines to keep pace with shrimp and finfish farms demanding tighter pellet durability. Output gains translate into faster harvest cycles that justify the unit-cost premium. Regulators also favor extrusion due to improved water quality, limiting feed-loss fines. Suppliers integrating ozone-nanobubble biofloc demonstrate additional water clarity and health benefits, widening the performance gap with classic pellet products.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile fishmeal and fish-oil prices | -1.40% | China, Vietnam, and Thailand | Short term (≤ 2 years) |

| Disease outbreaks leading to temporary stocking cuts | -1.10% | India, Vietnam, Indonesia, and Thailand | Short term (≤ 2 years) |

| Regulatory caps on phosphorus discharge from feed | -0.70% | China, India, and Vietnam | Medium term (2-4 years) |

| Competition from single-cell protein alternatives | -0.30% | China with gradual regional rollout | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Fishmeal and Fish-Oil Prices

Spot fishmeal averaged USD 1,504 to USD 1,882 per metric ton in 2024, whipsawing margins and complicating inventory planning. Smaller Asian mills lacking hedging tools scramble for soybean meal substitutions, but carnivorous species still require concentrated marine amino acids. Fish-oil turbulence echoes meal swings and fuels algae-oil pilots despite higher upfront costs. Vietnamese and Thai exporters face thin price flexibility against global buyers, magnifying the squeeze. Broad substitution accelerates R&D toward microbial and insect oils that soothe price shocks but retain essential fatty-acid profiles.

Disease Outbreaks Leading to Temporary Stocking Cuts

Annual disease losses in India underscore biosecurity gaps that ripple across feed demand. Tilapia Parvovirus flare-ups compel emergency harvests, collapsing local feed call-offs for months. Southeast Asian shrimp ponds confront Aeromonas and Vibrio waves, forcing antibiotic-free remedies and lower stocking densities that depress feed volumes. Recovery periods often stretch 6-12 months as farmers rebuild broodstock and confidence. Yet outbreaks also spur specialty diets fortified with immunostimulants, cushioning losses for agile suppliers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Species: Fish Dominance Drives Volume Growth

Fish diets generated 51.35% of the Asia-Pacific aquafeed market share in 2025, confirming the segment’s volume supremacy within the Asia-Pacific aquafeed market. Carp, tilapia, catfish, and diverse marine finfish underpin China’s mammoth output, with each species requiring unique amino-acid ratios to hit optimal feed-conversion benchmarks. The Asia-Pacific aquafeed market size attached to crustaceans remains smaller today, yet is rising quickly as shrimp estates in Vietnam, Thailand, and Indonesia pursue intensification and higher protein feeds. Crustaceans are estimated to grow at the highest rate, with an estimated CAGR of 8.22% from 2026 to 2031, reflecting strong demand momentum.

Mollusk feed sees steady orders from Chinese coastal polyculture schemes that recycle excess nutrients through bivalves. Emerging eel and ornamental species stay in niche but command premium prices, enabling specialty manufacturers to charge higher margins. Precision-nutrition gains, delivering up to 20% feed-conversion efficiencies, allow growers to trim feeding days while lifting survival rates. Producers calibrate vitamin and mineral packs against water-temperature swings to mitigate stress-related diseases. Ultimately, wide species variety ensures sustained tonnage growth while inviting tailored feed niches that cushion producers from commodity price pressure.

By Ingredient: Soybean Meal Leadership Faces Alternative Protein Pressure

Soybean meal represented 33.20% of the Asia-Pacific aquafeed market size in 2025 and remains the backbone of many formulations thanks to established logistics networks and attractive protein ratios. Despite this edge, functional additives are projected to capture the fastest incremental value at a 9.85% CAGR (2026-2031) as disease mitigation rises to board-level priority. Fishmeal retains irreplaceable roles for marine carnivores and hatchery diets, though price spikes force partial substitution with corn-gluten meal and poultry by-product hydrolysate. Single-cell proteins, led by Calysta’s methane-fed technology, enter commercial rations for shrimp and freshwater fish in China, reducing reliance on volatile marine inputs.

Microalgae products such as Spirulina and Chlorella widen the functional-nutrition toolkit by delivering pigments, antioxidants, and essential fatty acids that lift flesh coloration and shelf life. Feed makers also explore insect meal sourced from black soldier fly larvae in Thailand and Vietnam, whose chitin content confers gut-health benefits. Suppliers refine enzymes to unlock greater digestibility from plant proteins, slicing inclusion levels of marine raw materials without compromising growth. With sustainability audits expanding across export markets, lower-carbon protein ingredients gain traction and may erode soybean meal’s share over the next decade.

By Form: Pellets Maintain Leadership Despite Extruded Feed Innovation

Pellets controlled 47.10% of 2025 revenue, reflecting the format’s entrenched infrastructure and budget appeal across the Asia-Pacific aquafeed market. Easy manufacturing, broad farmer familiarity, and low power requirements keep pellets popular in semi-intensive ponds. Yet extruded feed, posting a 9.22% CAGR, steadily chips away at that lead. Extrusion expands starch gelatinization, improving protein availability and limiting nutrient leaching, attributes now prized in high-density recirculating aquaculture systems.

Digital twin modeling within modern extrusion plants optimizes temperature and pressure settings, achieving tighter pellet uniformity and lower energy consumption. Powder meal maintains a foothold in hatcheries requiring micro-size particles for larval stages; technology advances now allow cold-set micro-encapsulation of sensitive vitamins. Overall, format diversification supports feed makers’ ability to match differing farming intensities while sustaining margins through value-added specifications.

Geography Analysis

China’s aquafeed leadership rests on unmatched output scale, deep ingredient pools, and rising offshore cage projects that stretch technical feed demands. China accounted for 42.05% of the Asia-Pacific aquafeed market in 2025, solidifying its dominance. Government environmental rules now incentivize low-phosphorus feeds, nudging suppliers toward enzyme supplementation and high-digestibility proteins. High-specification shrimp diets form a vibrant premium segment serving Guangdong processors that supply Japanese and U.S. retailers.

India’s catch-up path relies on integrated multi-trophic regulations that balance pond ecology, a policy cocktail that pulls novel functional-additive suppliers into the market. India is estimated to grow at a CAGR of 6.84% from 2026 to 2031, driven by increased focus on value-added inputs. Tilapia Parvovirus episodes sharpen India’s appetite for immune-boosting ingredients and real-time pond monitoring tools, embedding quality considerations into procurement norms once driven purely by price.

Vietnam’s export-oriented industry benefits from free-trade pacts that favor compliance with sustainability certifications, putting pressure on feed makers to provide traceable formulas with lower fishmeal inclusion. The country’s Mekong Delta hubs are increasingly pilot automatic feeding barges that link to cloud-based biomass estimations. Indonesia’s archipelagic geography complicates logistics, yet recent pellet plant investments along Java’s northern coast shorten lead times and curb freight costs. Thailand continues to set regional standards for Good Aquaculture Practices certification, expanding market access and feeding demand for pathogen-controlled feed lots. Smaller Asia-Pacific islands progressively adopt seaweed-and-bivalve integrations, supplying eco-certified stocks to tourism hotspots and adding incremental feed demand for tropical marine fish.

Competitive Landscape

The Asia-Pacific aquafeed market sits at moderate consolidation, as the top five firms command the majority of revenue. Charoen Pokphand Foods PCL exploits vertically integrated operations from broodstock to retail-branded seafood, allowing internal feed usage forecasts to align plant scheduling and hedge cost shocks.

Chinese champions Tongwei Group Co., Ltd. cashes in proprietary probiotic strains and AI-driven nutrient modeling, differentiating offerings from generic peers. Norway-based SHV Holdings (Skretting) scales local production in Long An, Vietnam,[3]Skretting, “Our History,” skretting.com to bring European formulation experience closer to Asian grow-out conditions. De Heus Animal Nutrition chips away in Indonesia with modular mill designs that can be expanded in phases, balancing risk and growth.

As integrated producers broaden into branded seafood, feed quality becomes a competitive focal point that links farm survival rates to supermarket shelf margins. Overall, firms that marry nutrient science with digital management tools earn premium pricing power and foster stickier contracts.

Asia-Pacific Aqua Feed Industry Leaders

Charoen Pokphand Foods PCL

Tongwei Group Co., Ltd.

Guangdong HAID Group Co., Ltd.

Cargill, Inc.

New Hope Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: SHV Holdings subsidiary Skretting China has opened its first LifeStart production line in Asia, marking a strategic expansion into China's aquaculture sector. The facility, located in Zhuhai, was launched alongside five new hatchery feed products targeting species including salmon, tilapia, golden pompano, snakehead, and catfish.

- January 2024: Calysta's FeedKind protein has received formal approval from China's Ministry of Agriculture and Rural Affairs (MARA) for use in aquaculture feeds. The approval follows an extensive evaluation process and enables the protein's use in fish and shrimp feeds. Calysseo, a joint venture between Calysta and Adisseo, will distribute the single cell protein through Adisseo's sales network in China.

Asia-Pacific Aqua Feed Market Report Scope

Aqua feed forms an integral part of commercial and personal aquaculture and provides a wholesome and balanced diet for farmed fish. Aqua feed is primarily sourced from vegetables, grains, oilseeds, and other significant components. The Asia-Pacific aqua feed market is segmented by species into Litopenaeus vannamei, Penaeus monodon, Pangasius, Carp, Catfish, Tilapia, and Other Species and by Geography into India, Vietnam, Thailand, Indonesia, and the Philippines. A detailed country-wise analysis of every species type is provided in the report. The report offers an estimation and forecast of the market in value (USD million) for the abovementioned segments.

By Species

| Fish |

| Crustaceans |

| Mollusks |

| Others (Eels, etc.) |

By Ingredient

| Soybean Meal |

| Fishmeal |

| Fish-oil |

| Functional Additives |

| Others (Corn Gluten, etc.) |

By Form

| Pellets |

| Extruded Feed |

| Powdered Meal |

| Liquid Feed |

By Country

| China |

| India |

| Indonesia |

| Vietnam |

| Thailand |

| Rest of Asia-Pacific |

| By Species | Fish |

| Crustaceans | |

| Mollusks | |

| Others (Eels, etc.) | |

| By Ingredient | Soybean Meal |

| Fishmeal | |

| Fish-oil | |

| Functional Additives | |

| Others (Corn Gluten, etc.) | |

| By Form | Pellets |

| Extruded Feed | |

| Powdered Meal | |

| Liquid Feed | |

| By Country | China |

| India | |

| Indonesia | |

| Vietnam | |

| Thailand | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

How large is the Asia Pacific aquafeed market today?

The market is valued at USD 27.57 billion in 2026 and is projected to reach USD 39.18 billion by 2031.

Which species segment uses the most feed across Asia Pacific?

Fish diets represent 51.35% of total feed value, making them the largest consuming segment.

What ingredient dominates Asia Pacific feed formulations?

Soybean meal leads with a 33.20% share, though functional additives are the fastest-growing category.

Why are extruded feeds gaining popularity?

Extruded pellets improve protein digestibility by 10-15% and reduce waste, which lowers overall production costs.

What is driving interest in single-cell proteins?

Regulatory approval in China and more predictable pricing than fishmeal makes single-cell proteins an attractive alternative.

Page last updated on: