Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 24 Billion |

| Market Size (2026) | USD 25.29 Billion |

| Market Size (2031) | USD 32.82 Billion |

| Growth Rate (2026 - 2031) | 5.36% CAGR |

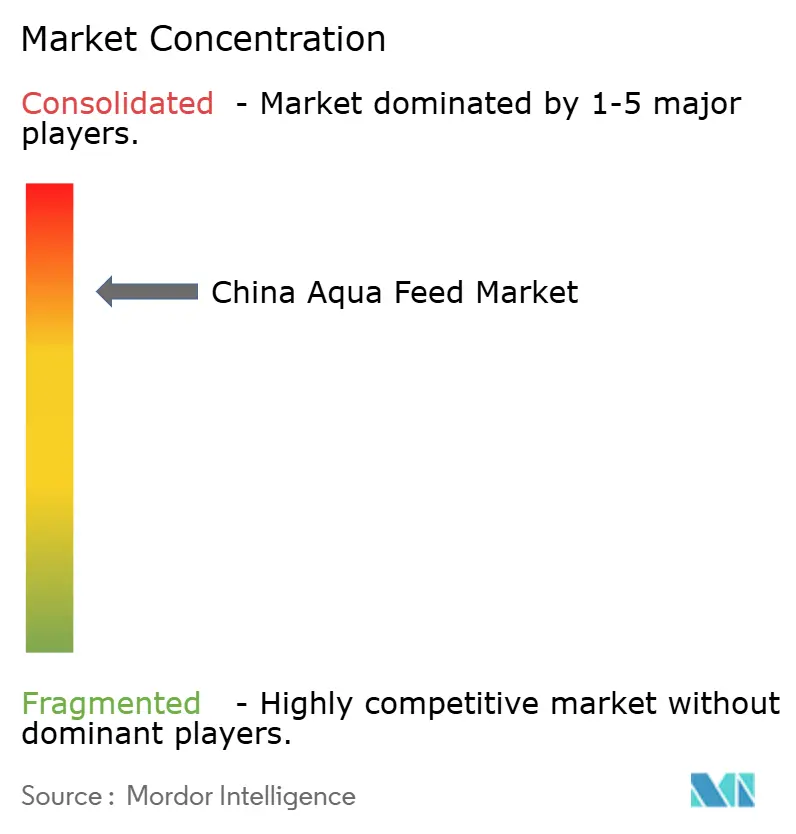

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Aqua Feed Market Analysis by Mordor Intelligence

The China aquafeed market size in 2026 is estimated at USD 25.29 billion, growing from 2025 value of USD 24 billion with 2031 projections showing USD 32.82 billion, growing at 5.36% CAGR over 2026-2031. This expansion stems from Beijing’s Dual Circulation policy, large-scale feed-mill consolidation, and the rapid onboarding of alternative proteins that cushion ingredient cost swings[1]Source: Ministry of Agriculture and Rural Affairs, “China Fisheries Statistical Yearbook 2024,” MOA.gov.cn . Strong per-capita seafood demand in 2024 keeps carp and crustacean producers on an investment footing, while export-oriented clusters in Guangdong and Fujian turn to antibiotic-free formulations that earn price premiums in North America and the European Union[2]Source: National Bureau of Statistics of China, “Per-Capita Consumption Expenditure 2024,” Stats.gov.cn. Ingredient innovation is another tailwind; insect meal and microbial proteins are forecast to post double-digit growth as Calysta’s FeedKind wins regulatory clearance and black soldier fly facilities reach commercial scale. On the processing front, twin-screw extrusion lines curb feed waste and improve digestibility, prompting large operators to shift away from lower-priced pellets despite higher capital outlays.

Key Report Takeaways

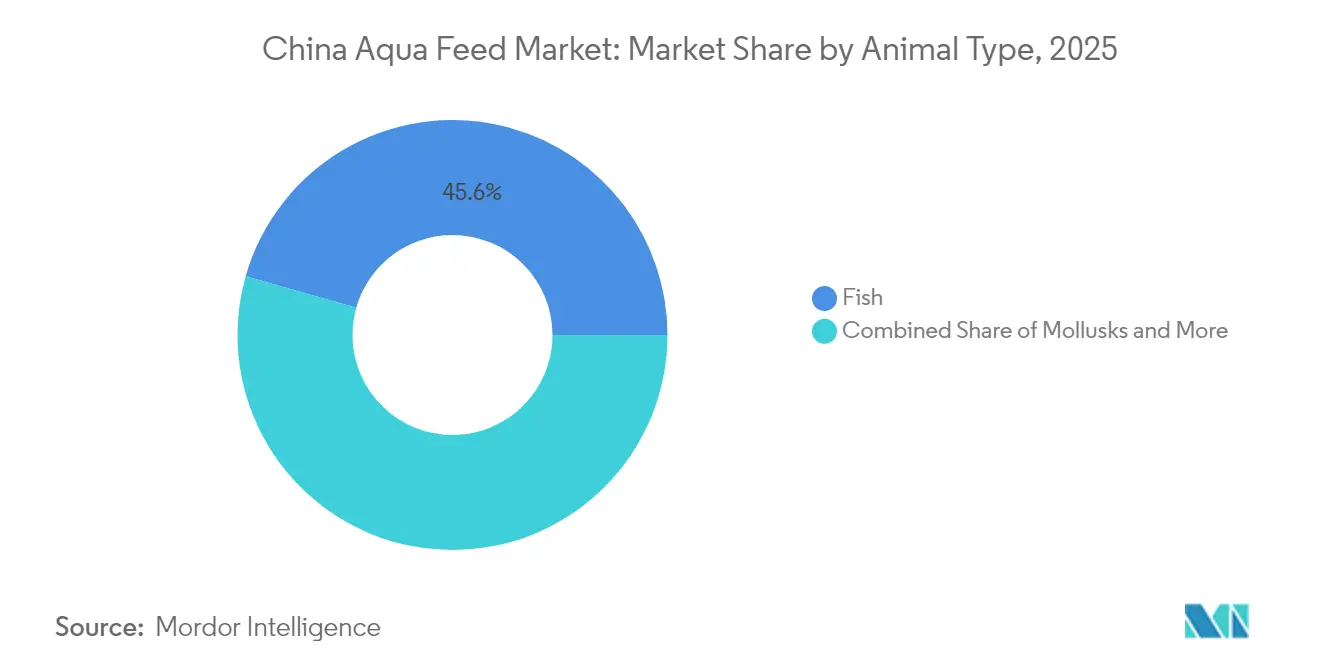

- By animal type, fish feeds held 45.60% of the China aquafeed market size in 2025, while crustacean feeds are tracking a 7.45% CAGR through 2031.

- By ingredient type, cereals and grains represented a 37.55% share of the 2025 China aquafeed market, whereas alternative proteins are expanding at an 10.6% CAGR.

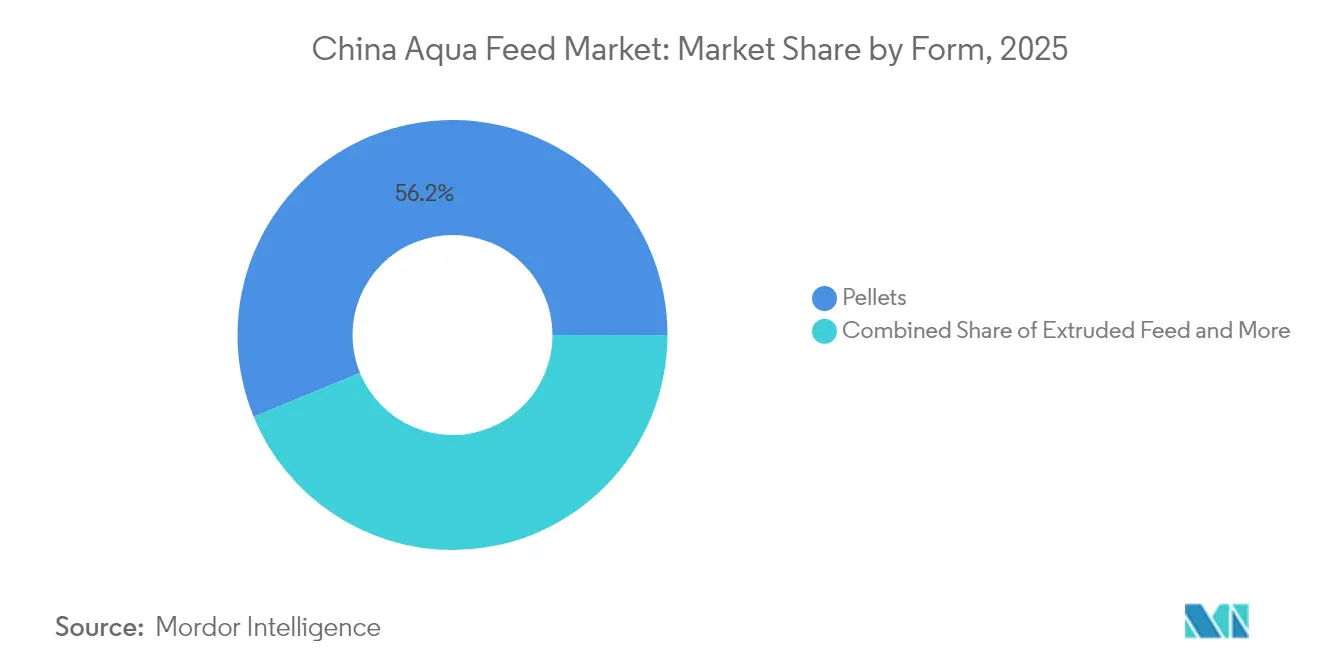

- By form, pellets captured 56.20% of the 2025 China aquafeed market, while extruded offerings are projected to grow at a 9.15% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Aqua Feed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding domestic seafood consumption per-capita | +1.2% | National, with urban clusters in Yangtze River Delta and Pearl River Delta leading | Medium term (2-4 years) |

| Government Dual Circulation policy supporting agritech | +0.9% | National, prioritizing inland provinces for production self-sufficiency | Long term (≥4 years) |

| Rising export-oriented aquaculture clusters in coastal provinces | +0.8% | Coastal provinces, Guangdong, Fujian, Shandong, Zhejiang | Medium term (2-4 years) |

| Rapid consolidation of feed mills boosting capacity utilization | +0.7% | National, concentrated in Jiangsu, Guangdong, Shandong | Short term (≤2 years) |

| Deployment of AI-based smart feeders in large ponds | +0.6% | Early adoption in Chongqing, Hubei, Jiangsu, and scaling to southern provinces | Medium term (2-4 years) |

| Commercialization of insect-based proteins | +0.5% | Pilot clusters in Guangdong, Shandong, and national rollout underway | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Expanding Domestic Seafood Consumption Per Capita

Urban households consumed 41.6 kilograms of seafood in 2024, up 9.5% from 2020, as cold-chain networks extend shelf life and e-commerce improves access. Demand is shifting toward shrimp, tilapia, and salmon, species that require nutrient-dense feeds with higher fishmeal inclusion, thereby increasing revenue per metric ton for premium formulations[3]Source: China Chain Store and Franchise Association, “Cold-Chain Logistics Report 2024,” CCFA.org.cn. Coastal residents already exceed 50 kilograms, while inland consumers average 30 kilograms, indicating runway for volume in the central provinces. Subsidies under the “Big Food” plan offset pond-modernisation costs, steering farmers toward high-quality extruded diets that shorten grow-out cycles. Online platforms such as JD Fresh booked 30% year-on-year seafood sales growth in 2024, validating a logistics-driven consumption shift.

Government Dual Circulation Policy Supporting Agritech

The 14th Five-Year Plan earmarked CNY 15 billion (USD 2.1 billion) in subsidies for feed-mill automation, breeding upgrades, and recirculating aquaculture systems, accelerating technology adoption. Provincial pilots that blend Internet of Things (IoT) sensors with automated feeders cut labor costs by 40% and feed conversion ratios by 15% on demonstration farms. Regulators now require that 80% of commercial feeds meet national quality standards by 2026, squeezing out sub-scale mills and propelling consolidation. Tongwei and Guangdong Haid Group tapped these incentives to launch extrusion lines exceeding 100,000 metric tons per year, capturing energy savings near 25%. The policy’s focus on domestic ingredient self-sufficiency has spurred soybean-crushing capacity and insect-protein pilots, buffering firms against import volatility.

Rising Export-oriented Aquaculture Clusters in Coastal Provinces

Guangdong, Fujian, and Shandong shipped USD 9.2 billion of seafood in 2024, demanding antibiotic-free feeds that comply with European Union residue ceilings. Shrimp operators in Zhanjiang pay 10% premiums for GlobalG.A.P. certified diets that underpin access to high-margin markets. Sea-cucumber farms in Shandong rely on algae-based formulations supplied via joint ventures between local distributors and Scandinavian nutrition firms. China-ASEAN tariff cuts on fishmeal and rice bran trimmed coastal input costs by up to 12% in 2024, reinforcing competitiveness

Rapid Consolidation of Feed Mills Boosting Capacity Utilization

Licensed aquafeed mills fell to 950 in 2024 from 1,200 in 2020 as stricter effluent and quality rules hit sub-50,000 metric-ton plants hardest. Average capacity utilization rose to 76%, driving fixed-cost dilution and freeing cash for automation. Tongwei acquired three mid-sized facilities that added 600,000 metric tons of throughput, while Guangdong Haid Group shuttered under-scale mills and redirected production to logistics hubs. New Hope Liuhe filled idle lines through contract manufacturing, stabilizing margins in volatile raw-material cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility of fishmeal and soybean prices | -0.8% | National, with coastal mills most exposed to fishmeal imports | Short term (≤2 years) |

| Outbreaks of aquatic animal diseases | -0.6% | Southern provinces, Guangdong, Guangxi, Hainan, and Yangtze basin | Short term (≤2 years) |

| Smallholder reluctance toward high-performance extruded feed | -0.5% | Inland provinces, Hubei, Hunan, Jiangxi, with fragmented farm structures | Medium term (2-4 years) |

| Environmental carrying-capacity limits in major delta regions | -0.4% | Yangtze River Delta, Pearl River Delta | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Volatility of Fishmeal and Soybean Prices

Peruvian fishmeal traded from USD 1,500 to USD 1,600 per metric ton in 2024 as El Niño cut anchovy quotas, knocking 200 to 300 basis points off mill margins during the Q2 price spike. Soybean meal fluctuated between USD 450 and USD 550 amid Brazilian harvest uncertainty and U.S.–China policy shifts, forcing mills on 30-day inventory cycles to ration working capital. Larger players lock supply through hedging and long-term contracts, but smaller independents face acute cash-flow stress that fuels consolidation.

Outbreaks of Aquatic Animal Diseases

Early hepatopancreatic necrosis syndrome clipped shrimp survival to 40% in parts of Guangdong and Guangxi, wiping out USD 500 million in output in 2024. Tilapia lake virus caused another USD 300 million in losses in Hainan and Fujian, curbing feed demand as farmers cut stockings. Feed suppliers now layer beta-glucans and probiotics to counter pathogen pressure and sustain volumes during outbreaks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Animal Type - Carp Strength Masks Crustacean Momentum

Fish feeds underpinned 45.60% of 2025 revenue, sustained by resilient demand in Hubei, Hunan, and Jiangxi. The crustacean category is the fastest riser, projected at a 7.45% CAGR due to vannamei shrimp intensification in Guangdong and Guangxi. The China aquafeed market size for crustacean diets is set to outpace herbivorous species as export premiums justify higher fishmeal inclusion rates. Tilapia feeds, servicing 1.8 million metric tons of harvest in 2024, retain export tailwinds but face disease risks that squeeze margins. Land-based salmon farms in Shandong turned out 15,000 metric tons and require high-protein formulations priced 30% above carp equivalents, a niche with strong upside. Trout diets in Qinghai and Gansu, though minor, command premium pricing tied to cold-water lipid profiles. Mollusk and miscellaneous species together hold under 10% of demand, yet open micro-algae additive opportunities.

Technological upgrades in breeding drove an 8% to 10% gain in conversion efficiency for improved carp and tilapia strains approved in 2024. Meanwhile, crustacean diets wrestle with balancing >25% fishmeal inclusion against profit margins. Companies investing in species-specific research and joint breeding programs can tap segments where nutritional precision commands price premiums. Consequently, the China aquafeed market share for high-value species feeds should rise even as carp maintains volumetric dominance.

By Ingredient Type - Alternative Proteins Challenge Cereal Incumbency

Cereals and grains retained 37.55% volume share in 2025 and remain the backbone energy source for omnivorous fish. Fishmeal is indispensable for carnivores, but its share is sliding as poultry by-product meal, hydrolysates, and enzyme-treated soy gain ground. The China aquafeed market size tied to alternative proteins is on track for an 10.6% CAGR as insect, microbial, and single-cell sources win buyer confidence. Calysta’s FeedKind delivers a fishmeal-like amino profile and sidesteps marine resource constraints, while black soldier fly meal posted commercial volumes over 70,000 metric tons in 2024. Yeast and bacterial proteins are entering pilot diets for marine finfish.

Enzyme technology also lowers anti-nutritional factors in soybean meal, letting mills push fishmeal replacement nearer 50% in grass carp diets without efficiency loss. Mills that lock multi-year supply contracts with alternative-protein producers and run in-house research and development (R&D) to fine-tune inclusion rates can buffer against commodity price shocks and lift margins. Enhanced traceability further boosts acceptance among export-driven farms.

By Form – Extruded Feed Gains Ground Despite Cost Barriers

Pellets controlled 56.20% of 2025 sales because smallholders prize lower upfront cost. Yet extruded diets, which deliver 10% to 15% better conversion, are accelerating at a 9.15% CAGR. The China aquafeed market size for extruded formats should therefore expand markedly as subsidies cover 10% of big-farm purchases and environmental rules favour low-waste feeds. Twin-screw technology tunes pellet density, a must for carnivores like mandarin fish that strike at mid-water depth. Powder feeds occupy the hatchery niche, while liquid feeds remain tiny due to cold-chain demands.

Even so, payback calculations delay broad smallholder uptake. A 100-hectare farm saves USD 300 per hectare annually on ratios but still faces a 24- to 36-month cost-recovery window. Suppliers that offer hybrid semi-extruded formats and flexible credit terms can tilt the adoption curve and gain share ahead of full conversion.

Geography Analysis

Coastal provinces absorbed maximum percentage of 2024 demand. Guangdong alone bought 2.8 million metric tons of feed, with shrimp formulations fetching 25% premiums thanks to high fishmeal content. Shandong drew 2.2 million metric tons focused on sea cucumber and marine fish, where average selling prices topped USD 1,500 per metric ton. Fujian consumed 1.5 million metric tons, but disease outbreaks present headwinds. The Yangtze River Delta, limited by pond caps, sustains 3.5 million metric tons through recirculating and cage systems.

Inland provinces accounted for 8 million metric tons of mostly carp diets, with Hubei leveraging an extensive reservoir network. Sichuan benefits from Tongwei’s integrated supply chain, which trims logistics costs and speeds formula tweaks. The Pearl River Delta posts 4 million metric tons of demand yet faces regulatory pond-density cuts that may shave 2% to 3% volume growth through 2027. Northern provinces such as Liaoning add niche cold-water demand but are constrained by shorter seasons. Policy guidance issued in 2024 urges capacity migration westward to ease coastal environmental stress, suggesting gradual geographic rebalancing of the China aquafeed market over the next decade. The Ministry of Agriculture and Rural Affairs' regional aquaculture development plans, published in 2024, prioritize capacity expansion in central and western provinces to alleviate environmental pressure on coastal deltas, signaling a gradual geographic rebalancing of feed demand over the next decade.

Competitive Landscape

The top five suppliers, Tongwei, Guangdong Haid Group, New Hope Liuhe, Cargill, and Charoen Pokphand Foods, held maximum percentage of 2024 turnover. Tongwei leverages IoT-enabled plants and blockchain traceability to trim labor by 35% and align formulations with pond-level data. Guangdong Haid Group deepened vertical integration by buying a Vietnamese hatchery, locking post-larvae supply and feed offtake. New Hope Liuhe pairs automation with contract manufacturing to utilize idle capacity, buffering against raw-material shocks.

Cargill files patents on enzyme-treated plant proteins and micro-encapsulation, winning 20% premiums in premium segments. Nutreco’s Skretting brand targets disease-prone shrimp farms with functional feeds laced with immunostimulants. Emerging disruptors include INSPRO and Calysta, which partner with incumbents to co-develop insect- and microbial-protein diets, leveraging established sales channels to overcome farmer skepticism.

Technology bundling precision feeders, mobile dashboards, and embedded sensors has become a decisive factor in account retention as large farms seek integrated performance gains. Regional independents under 100,000 metric-tons capacity face rising compliance costs and ingredient volatility, accelerating takeover candidacy.

China Aqua Feed Industry Leaders

Tongwei Co. Ltd.

Guangdong Haid Group Co. Ltd.

New Hope Liuhe Co. Ltd.

Cargill Inc.

Charoen Pokphand Foods PCL

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Skretting has expanded its footprint in China by launching a new premix production line in Zhuhai, boosting aquafeed capacity to 15,000 metric tons annually. The company also signed a strategic trout partnership with Longyang Fresh to drive sustainable aquaculture growth in China.

- August 2025: Sprintex has entered the Chinese aquaculture market through a supply agreement for its patented protein ingredient. This agreement underscores China's increasing adoption of alternative and sustainable feed solutions in aquaculture.

- February 2024: China has approved Calysta’s FeedKind alternative protein for use in aquaculture feeds, aiming to reduce dependence on fishmeal and soy. This regulatory approval aligns with China’s efforts to promote sustainable aquaculture growth and expand feed ingredient options.

China Aqua Feed Market Report Scope

Aqua feed is a mixture of raw materials and other supplements sourced from natural or synthetic sources and fed to farmed fish. The aqua feed market is segmented by animal type including fish, crustaceans, mollusks, trout, and other animal types. The report offers market size and forecasts in value (USD) and volume (Metric Tons) for all the above segments.

By Animal Type

| Fish | Carp |

| Tilapia | |

| Salmon | |

| Catfish | |

| Other Fish Species | |

| Crustaceans | Shrimps and Prawns |

| Crabs | |

| Mollusks | Oysters |

| Mussels | |

| Scallops | |

| Trout | |

| Other Animal Types |

By Ingredient Type

| Cereals and Grains | |

| Fishmeal | |

| Soymeal | |

| Additives | Vitamins |

| Minerals | |

| Enzymes | |

| Alternative Proteins (e.g., insect, microbial) |

By Form

| Pellets |

| Extruded Feed |

| Powder |

| Liquid |

| By Animal Type | Fish | Carp |

| Tilapia | ||

| Salmon | ||

| Catfish | ||

| Other Fish Species | ||

| Crustaceans | Shrimps and Prawns | |

| Crabs | ||

| Mollusks | Oysters | |

| Mussels | ||

| Scallops | ||

| Trout | ||

| Other Animal Types | ||

| By Ingredient Type | Cereals and Grains | |

| Fishmeal | ||

| Soymeal | ||

| Additives | Vitamins | |

| Minerals | ||

| Enzymes | ||

| Alternative Proteins (e.g., insect, microbial) | ||

| By Form | Pellets | |

| Extruded Feed | ||

| Powder | ||

| Liquid | ||

Key Questions Answered in the Report

How large is the China aquafeed market in 2026?

The China aquafeed market size reached USD 25.29 billion in 2026 and is forecast at USD 32.82 billion by 2031.

Which animal segment is expanding fastest?

Crustacean feeds, mainly for vannamei shrimp, are forecast to grow at a 7.45% CAGR through 2031.

What drives the shift toward extruded feed?

Superior feed conversion ratios, government subsidies, and tighter environmental standards are pushing operators toward extruded formats despite higher upfront costs.

How are ingredient risks being managed?

Mills hedge fishmeal and soybean costs, diversify into insect and microbial proteins, and adopt enzyme treatments that allow higher plant-protein inclusion rates.

Page last updated on: