Market Overview

| Study Period | 2020 - 2031 |

|---|---|

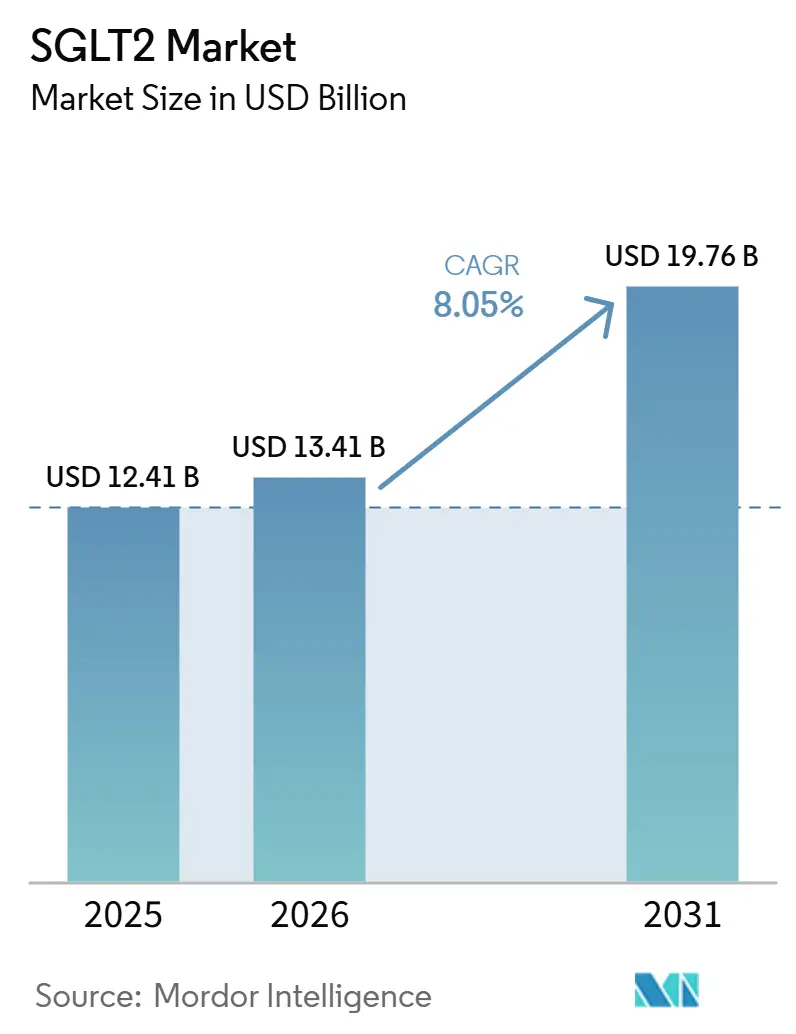

| Market Size (2026) | USD 13.41 Billion |

| Market Size (2031) | USD 19.76 Billion |

| Growth Rate (2026 - 2031) | 8.05% CAGR |

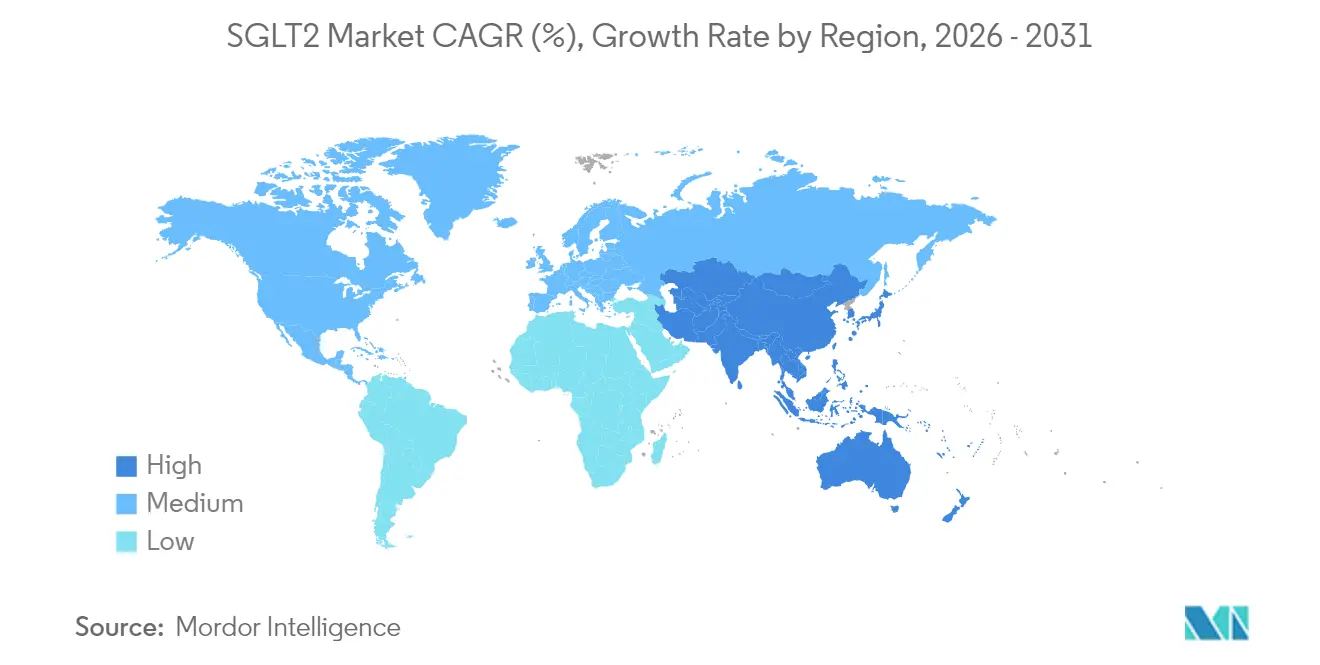

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

SGLT2 Market Analysis by Mordor Intelligence

The SGLT2 Market size is projected to be USD 12.41 billion in 2025, USD 13.41 billion in 2026, and reach USD 19.76 billion by 2031, growing at a CAGR of 8.05% from 2026 to 2031.

Strong cardiovascular and renal outcome data now position these agents as core cardiorenal therapies, not just glucose-lowering drugs. Sotagliflozin cut combined heart-attack and stroke events by 23% in patients with type 2 diabetes and chronic kidney disease, underscoring class-wide therapeutic breadth. FDA expansion of empagliflozin for heart failure with any ejection fraction broadened first-line use beyond endocrinology and into cardiology and nephrology practices[1]The Medical Letter, “Empagliflozin: Expanded Indication for Heart Failure,” medicalletter.org. Growth is also propelled by strategic patent portfolio extensions in China, where dapagliflozin still generated USD 500 million in sales after the compound patent expiry. Manufacturing scale-up—such as AstraZeneca’s multi-billion-dollar U.S. facility ensures capacity for rising demand while signaling sustained long-term commitment.

Key Report Takeaways

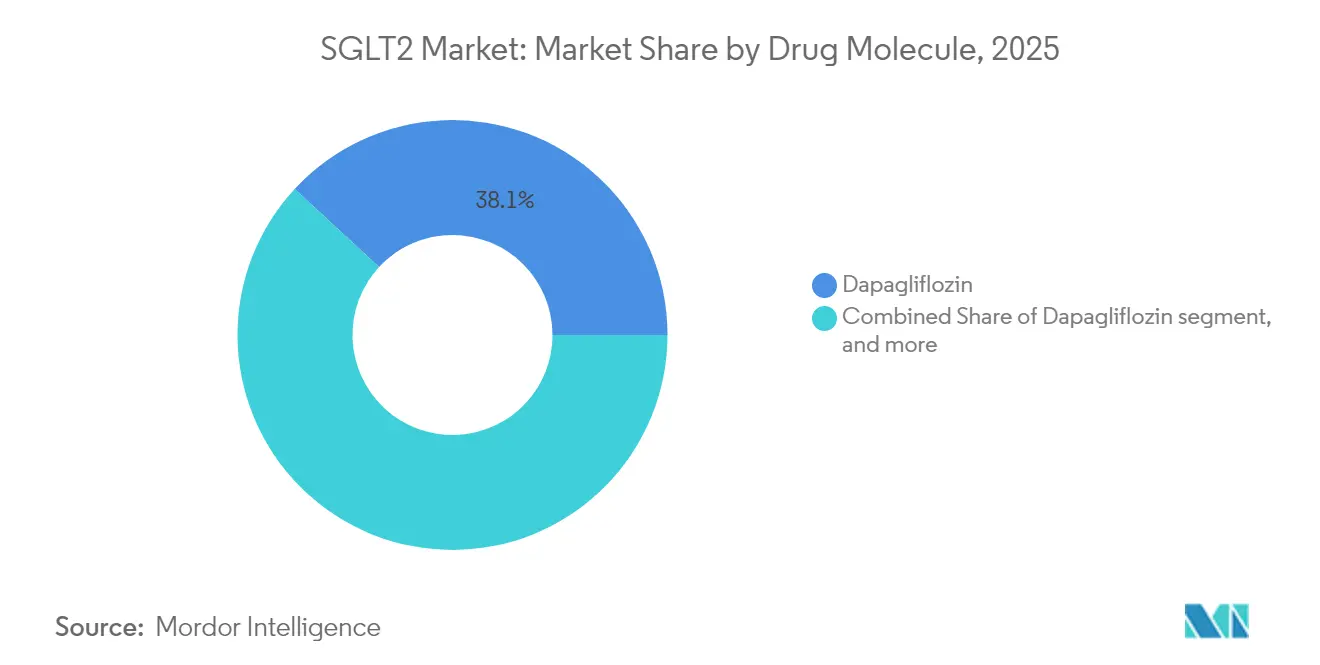

- By drug molecule, dapagliflozin led with 38.12% SGLT2 market share in 2025; ertugliflozin posted the highest projected CAGR at 10.02% through 2031.

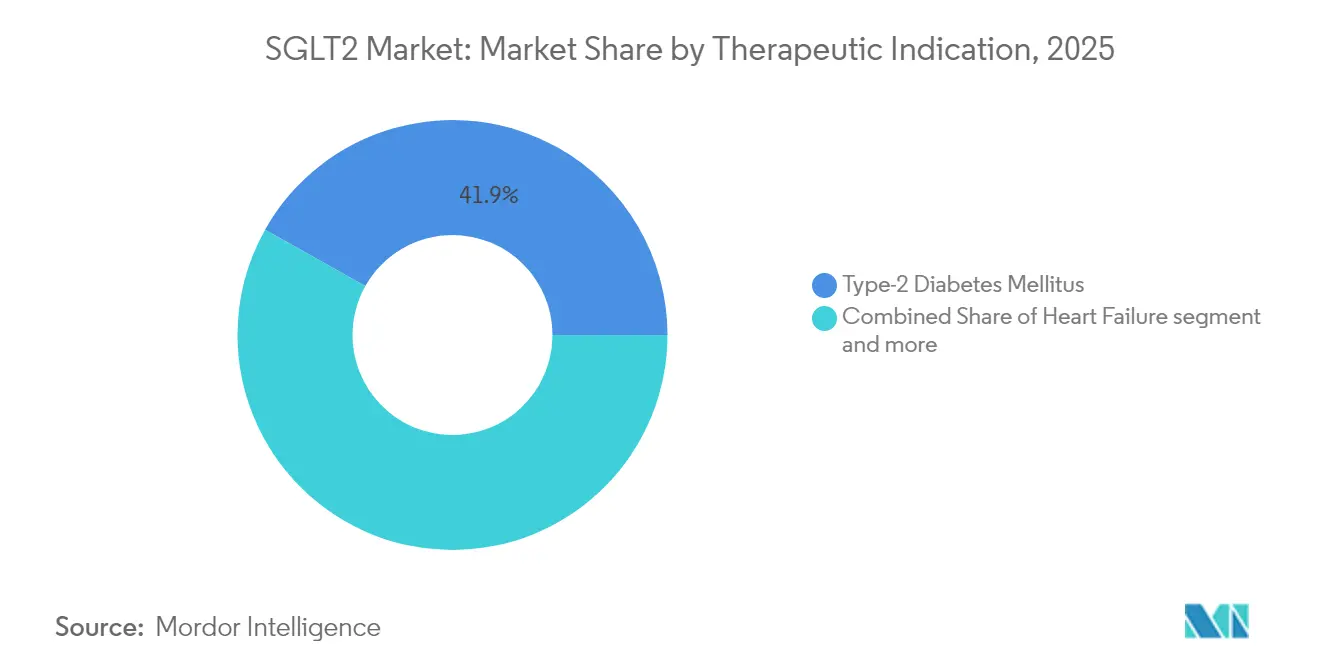

- By therapeutic indication, chronic kidney disease advanced at a 10.15% CAGR to 2031, whereas type 2 diabetes mellitus retained a 41.85% share of the SGLT2 market size in 2025.

- By distribution channel, online pharmacies advanced at a CAGR of 10.29%, whereas hospital pharmacies retained a 45.02% share of the SGLT2 market size in 2025.

- By geography, North America accounted for 42.75% of the SGLT2 market in 2025, while the Asia-Pacific region is expected to expand at a 9.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global SGLT2 Market Trends and Insights

Driver Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing global diabetes burden | +2.1% | Global with APAC highest growth | Long term (≥ 4 years) |

| Expanding cardiovascular and renal benefit evidence | +1.8% | North America & EU | Medium term (2-4 years) |

| Diversifying therapeutic indications beyond glycemic control | +1.5% | Global | Long term (≥ 4 years) |

| Strategic collaborations and co-marketing alliances | +1.2% | Global | Medium term (2-4 years) |

| Favorable clinical-practice guideline recommendations | +1.0% | North America & EU | Short term (≤ 2 years) |

| Growing adoption of oral combination therapies | +0.8% | Global with emerging-market focus | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Global Diabetes Burden

Rising prevalence sustains long-run volume expansion for the SGLT2 market. In India, 60.69% of type 2 diabetes patients still forgo these drugs mainly due to 41.45% cost barriers, revealing wide headroom for uptake[2].A. Sharma et al., “Cost Barriers Limit SGLT2 Use in India,” Journal of Diabetology, journalofdiabetology.org A PLoS Medicine microsimulation projected disability-adjusted life years falling from 2.20 to 1.25 when SGLT2 agents are introduced broadly across low- and middle-income countries. Thailand showed 57.13% price cuts are needed for dapagliflozin to clear national reimbursement thresholds, highlighting price elasticity challenges. Japan’s super-aged cohort demands strict safety screening to avoid adverse events in frail elders. Collectively, the diabetes wave keeps baseline demand rising even as affordability hurdles persist, strengthening the sglt2 market.

Expanding Cardiovascular and Renal Benefit Evidence

Large randomized trials now cement cardiorenal protection as a class hallmark. KDIGO 2024 guidelines recommend SGLT2 agents early in chronic kidney disease based on 37% slower kidney-function decline and 23% lower acute-kidney-injury risk regardless of diabetes status[3]KDIGO Guideline Committee, “2024 CKD Management Guidelines,” kidney-international.org. A meta-analysis of 78,607 participants showed 9% fewer major adverse cardiovascular events with the class, driven by heart-failure and sudden-death reductions. FDA approvals for dapagliflozin in heart failure with preserved or reduced ejection fraction widened addressable populations. Canagliflozin improved renal oxygenation within five days in BOLD-MRI studies, illustrating rapid organ-level benefits. These multidimensional outcomes encourage wider prescribing across specialties, enlarging the market and reinforcing gains in sglt2 market share.

Diversifying Therapeutic Indications Beyond Glycemic Control

Evidence now spans liver, obesity and neurodegeneration pathways. Eighteen randomized controlled NAFLD trials confirmed meaningful falls in liver-fat surrogate markers among 1,330 participants on the class. In preclinical work, canagliflozin cleared senescent cells and lengthened lifespan in mice via AMPK activation, hinting at geroscience potential . The SNIFF trial tests intranasal insulin with e mpagliflozin for early Alzheimer’s, expanding metabolic-brain therapy frontiers. OTID explores GLP-1 plus SGLT2 regimens for obese type 1 diabetes patients, reflecting weight-management synergies. Such pipelines distribute revenue risk across multiple high-value diseases beyond glucose control, strengthening long-term SGLT2 inhibitor industry resilience.

Strategic Collaborations and Co-Marketing Alliances

Partnering multiplies drug-life-cycle value. AstraZeneca’s USD 1.85 billion global license for ECC5004, an oral GLP-1, positions future fixed-dose combinations with dapagliflozin that bundle weight and glucose benefits. More than 33 API suppliers cover empagliflozin, giving Boehringer Ingelheim dual sourcing flexibility, GMP compliance and geopolitical risk hedging. In Korea, AstraZeneca copromotes Sidapvia with HK Inno.N, immediately leveraging general-hospital access after approval. Boehringer’s 11,000-patient EASi-KIDNEY study with empagliflozin and novel agent BI 690517 shows co-development depth. These alliances create global reach, speed indication expansion and enhance competitive separation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium pricing and access barriers in emerging markets | -1.8% | APAC, MEA, Latin America | Long term (≥ 4 years) |

| Ongoing safety and tolerability concerns | -1.2% | Global with regulatory variations | Medium term (2-4 years) |

| Patent expiration and generic-competition pressure | -1.5% | North America, Europe, Japan | Medium term (2-4 years) |

| Regulatory setbacks for new indications | -1.0% | North America and select APAC markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Premium Pricing and Access Barriers in Emerging Markets

Affordability gaps slow therapeutic penetration in lower-income settings. Monthly empagliflozin runs INR 1,539-1,602 in India versus INR 326-1,088 for dapagliflozin, placing both outside sustainable out-of-pocket levels for many patients. Médecins Sans Frontières estimated feasible cost-based prices near USD 1.30-3.45 per month—an order of magnitude below retail—exposing pricing latitude. Quadruple therapy studies across 21 countries revealed SGLT2 components least accessible in low-income economies, with Pakistan and Bangladesh lowest and the United States highest in price. Brand cost ratios hit 10.79 for dapagliflozin 5 mg, highlighting extreme intra-market variations. Unless differential pricing or broad tender-discount programs expand, penetration lags will temper the SGLT2 market CAGR.

Ongoing Safety and Tolerability Concerns

Regulators and prescribers remain alert to diabetic ketoacidosis (DKA) and genitourinary infection risks. FDA declined sotagliflozin’s type 1 diabetes label in December 2024 after panel debate on DKA despite cardiovascular benefits. Japan’s Pharmacovigilance Program mandates extra monitoring in elderly multi-morbid patients receiving the class. The Medical Letter continues to warn of volume-depletion hypotension, obliging clinicians to counsel on fluid intake and sick-day rules. ATTEMPT trial risk-mitigation in adolescents limited DKA to 1 mild event among 98 subjects, illustrating feasibility of prevention protocols. Yet persistent headlines may dissuade cautious physicians, slowing adoption in certain cohorts and moderating SGLT2 market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Molecule: Dapagliflozin Dominates While Ertugliflozin Accelerates

Dapagliflozin retained a 38.12% SGLT2 market share in 2025 and anchored sales of USD 500 million in China, even after compound-patent expiry, through evergreen portfolio tactics. Ertugliflozin grows fastest at a 10.02% CAGR to 2031, fuelled by Merck’s combination product SEGLUROMET with USD 1.275 billion potential forecast.

Empagliflozin, with €5.8 billion in 2022 revenue, supplied a 52.60% global molecule share, benefiting from Boehringer Ingelheim and Eli Lilly’s co-detailing scale and early cardiovascular outcome wins. Canagliflozin faces a slower trajectory under competitive pressure. Sotagliflozin’s dual SGLT1/2 profile promises unique event-reduction angles, yet it awaits broader regulatory alignment following the U.S. type 1 setback. Patent cliff maps indicate that Farxiga's generic risk will emerge by June 2030 and Invokana's by November 2031, incentivizing innovators to pivot toward fixed-dose combinations and new indications. API production remains concentrated, with 65% of global canagliflozin bulk originating in India or China. The raw prices range from USD 20 to USD 80 per gram, depending on purity and contract terms. Such supply-chain centralization offers cost economies, yet it exposes firms to geopolitical risk, which they counter by dual sourcing within free-trade partners. Emerging bexagliflozin secured FDA approval in January 2025 and retails at USD 50 per 30-day course through Cost Plus Drugs, creating price-point disruption for cash-pay segments . Overall, continual molecule evolution fortifies the SGLT2 market against future generic erosion.

By Therapeutic Indication: Diabetes Foundation Supports CKD Expansion

Type 2 diabetes mellitus held 41.85% of the SGLT2 market size in 2025, supplying the foundational prescription base, insurance pathways and physician familiarity. Chronic kidney disease volumes, however, advance at a 10.15% CAGR to 2031 as KDIGO 2024 promotes class use irrespective of glycemic status, effectively doubling eligible patient pools.

Heart-failure use shot ahead after empagliflozin became first to win across the ejection-fraction spectrum, with dapagliflozin gaining matching clearance soon after. Non-alcoholic fatty liver disease studies involving 1,330 participants point to transaminase and fibrosis-score improvements that will underwrite future label expansions. Obesity pipelines pairing SGLT2 with GLP-1 agonists seek additive weight and cardiometabolic control, while early Alzheimer’s trials hint at neuroprotective potential. Regulatory lag differs: metabolic and cardiac indications may clear in 2-3 years via priority-review data packages, whereas neurodegeneration could need longer observation. Consequently, indication diversity safeguards the SGLT2 market against over-reliance on a single disease area.

By Distribution Channel: Hospital Pharmacies Dominates the Market

Hospital pharmacies remain the pivotal distribution point for SGLT2 inhibitors because many patients first receive these agents during inpatient care for acute heart-failure or chronic-kidney-disease exacerbations, in line with recent guideline directives that recommend class initiation at or soon after hospitalization. Retail pharmacies then capture continuing prescriptions once patients transition to outpatient management, supported by established insurance reimbursement and pharmacist counseling services. E-commerce and mail-order channels, while still niche, are gaining traction among younger, tech-savvy diabetics seeking home delivery and price transparency, trends amplified by direct-to-consumer platforms that now list low-cost bexagliflozin. Together, these channels form an integrated supply chain that moves patients from hospital initiation through long-term community dispensing, ensuring broad access to SGLT2 therapies without significant disruption to existing pharmacy workflows while supporting continued expansion of the sglt2 market.

Geography Analysis

North America accounted for 42.75% of SGLT2 market share in 2025, reflecting guideline alignment, broad insurance coverage and rapid cardiology uptake. Medicare Part D and major commercial insurers reimburse class drugs for heart-failure indications, supporting continued dominance.

Asia-Pacific, expanding at 9.12% CAGR, combines high diabetes growth with strategic patent maneuvers. China’s national drug reimbursement listing catapulted dapagliflozin to USD 500 million revenue in 2024 despite generic threats; AstraZeneca’s 190 million-yuan line expansion ensures domestic supply. India shows unmet demand constrained by price, yet rapidly urbanizing middle-class cohorts signal latent volume potential once differential-pricing or generic entries lower costs.

Europe maintains steady uptake through EMA class approvals and national HTA assessments that weigh cardiovascular benefit against price. Price-volume agreements temper margins yet secure high formulary penetration. Japan’s aged demographic and strict pharmacovigilance produce cautious but clinically targeted use, balancing safety and efficacy imperatives. Latin America, Middle East and Africa lag in wallet share due to limited payer budgets but constitute long-term frontier growth arenas once cost hurdles abate.

Competitive Landscape

Market concentration is moderate: the top five innovators hold an estimated 68% combined revenue, with AstraZeneca, Boehringer Ingelheim, Eli Lilly, Janssen and Merck leading. AstraZeneca leverages broad indications and patent-evergreening; its upcoming U.S. mega-plant underpins global supply needs. Boehringer and Lilly ride empagliflozin’s early outcome-trial halo and extensive cardiology detailing. Janssen protects canagliflozin through life-cycle management though faces steeper erosion risk.

TheracosBio breaks price ceilings with bexagliflozin, appealing to cost-sensitive markets and PBM value tiers. Lexicon positions sotagliflozin as a differentiated dual-mechanism option aimed at further cardiovascular-event reduction once safety concerns resolve. API makers in India and China provide cost leverage, while Western CMOs handle high-purity needs for combination-tablet layering.

Strategic moves intensify: AstraZeneca’s ECC5004 deal seeds oral GLP-1 plus SGLT2 co-formulations; Boehringer initiates EASi-KIDNEY to pair empagliflozin with BI 690517. Digital-health collaborations integrate remote fluid-status monitoring to tailor dosing and improve adherence, reinforcing brand stickiness. Patent-litigation data show 63% of challenges succeed, so innovators focus on differentiated combos to sustain exclusivity. Overall, competition revolves around indication breadth, combination science and manufacturing scale, factors that collectively uphold premium positions while generic countdowns approach.

SGLT2 Industry Leaders

Janssen Pharmaceuticals

Boehringer Ingelheim

Eli Lilly and Company

Astellas Pharma

AstraZeneca

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: AstraZeneca began a Phase III trial of baxdrostat plus dapagliflozin to lower cardiovascular death and heart-failure events in type 2 diabetes patients.

- May 2025: AstraZeneca licensed ECC5004 from Eccogene for USD 185 million upfront plus milestones up to USD 1.825 billion.

- February 2025: Mount Sinai researchers documented a 23% cardiovascular-event reduction with sotagliflozin in The Lancet Diabetes & Endocrinology.

- January 2025: FDA cleared bexagliflozin (Brenzavvy) for type 2 diabetes after reviewing 23 trials in 5,000 adults.

Global SGLT2 Market Report Scope

A family of glucose transporters is known as sodium-dependent glucose co-transporters (also known as sodium-glucose linked transporters or SGLT2). Only the proximal renal tubules express it, which is responsible for 90% of glucose reabsorption from tubular fluid. Sodium-dependent Glucose Co-transporter 2 (SGLT 2) Market is segmented into drugs (Invokana, Jardiance, Farxiga/Forxiga, and Suglat) and Geography. The report offers the value (in USD) and volume (in Units) for the above segments.

By Drug Molecule

| Canagliflozin |

| Dapagliflozin |

| Empagliflozin |

| Ertugliflozin |

| Ipragliflozin |

| Sotagliflozin |

| Other SGLT2 Inhibitors |

By Therapeutic Indication

| Type-2 Diabetes Mellitus |

| Heart Failure (HFrEF/HFmrEF) |

| Chronic Kidney Disease |

| Obesity / Weight Management |

| Other Therapeutic Indications |

By Distribution Channel

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Molecule | Canagliflozin | |

| Dapagliflozin | ||

| Empagliflozin | ||

| Ertugliflozin | ||

| Ipragliflozin | ||

| Sotagliflozin | ||

| Other SGLT2 Inhibitors | ||

| By Therapeutic Indication | Type-2 Diabetes Mellitus | |

| Heart Failure (HFrEF/HFmrEF) | ||

| Chronic Kidney Disease | ||

| Obesity / Weight Management | ||

| Other Therapeutic Indications | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the SGLT2 market in 2026?

The SGLT2 market size reaches USD 13.41 billion in 2026 with an 8.05% CAGR forecast to 2031.

Which region grows fastest for SGLT2 inhibitors?

Asia-Pacific leads growth with a 9.12% CAGR through 2031 thanks to rising diabetes incidence and improved drug access policies.

Which molecule dominates current sales?

Dapagliflozin holds 38.12% share, supported by multi-indication approvals and strong patent-life management.

What is the biggest therapeutic growth segment?

Chronic kidney disease prescriptions advance fastest at 10.15% CAGR, driven by KDIGO guideline endorsement and broad FDA labels.

How are companies addressing future competition?

Innovators invest in combination therapies, manufacturing scale and geographic expansion to sustain margins as key patents near expiry.

Page last updated on: