Testosterone Replacement Therapy Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

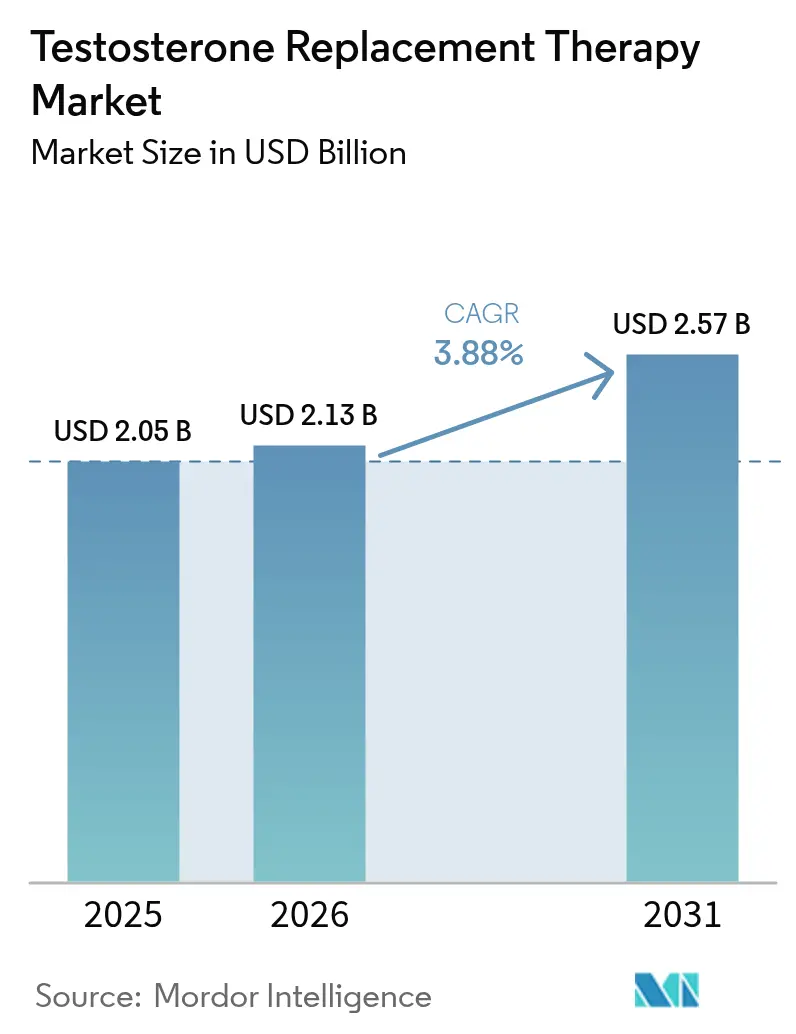

| Market Size (2026) | USD 2.13 Billion |

| Market Size (2031) | USD 2.57 Billion |

| Growth Rate (2026 - 2031) | 3.88% CAGR |

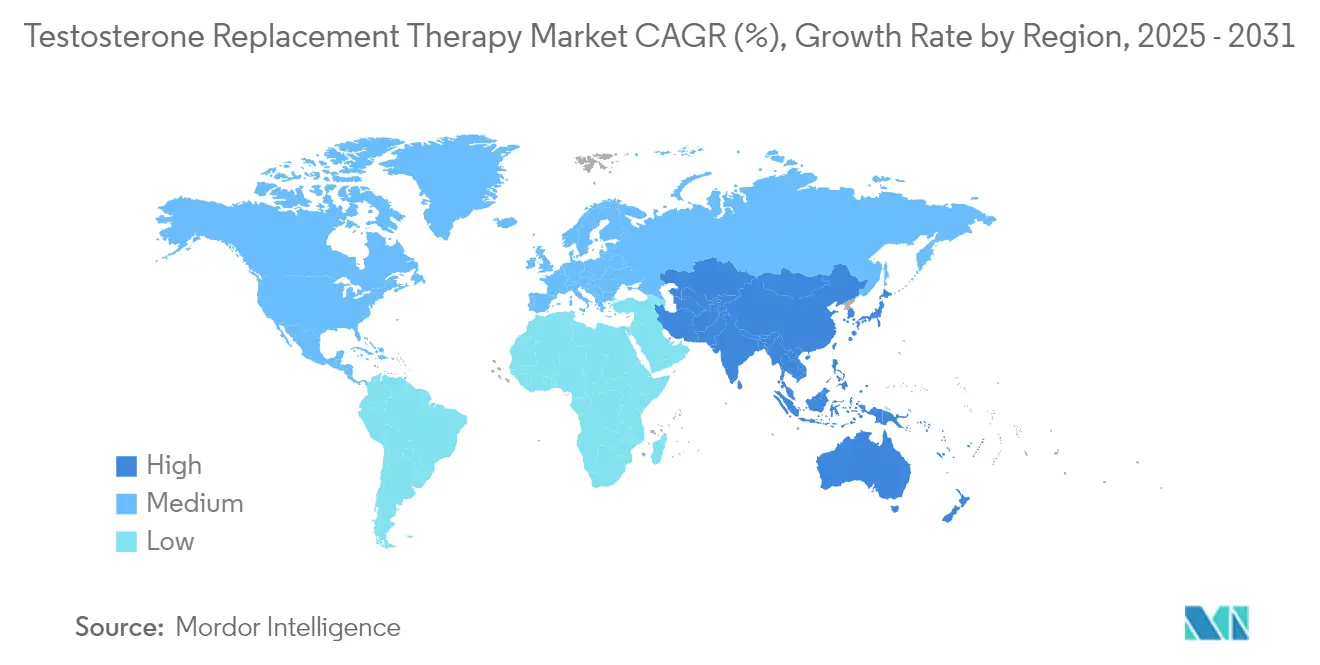

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Testosterone Replacement Therapy Market Analysis by Mordor Intelligence

The testosterone replacement therapy market size was valued at USD 2.05 billion in 2025 and estimated to grow from USD 2.13 billion in 2026 to reach USD 2.57 billion by 2031, at a CAGR of 3.88% during the forecast period (2026-2031). Momentum stems from the FDA’s February 2025 decision to remove the cardiovascular black-box warning from testosterone labels while adding blood-pressure monitoring requirements, a move that widens prescriber confidence and patient eligibility[1]U.S. Food and Drug Administration, “FDA Issues Class-Wide Labeling Changes for Testosterone Products,” fda.gov. Growth is further reinforced by a 39% prevalence of testosterone deficiency among men older than 45 in the United States sec.gov and direct-to-consumer telehealth spending exceeding USD 400 million in 2024, indicating strong demand for convenient care models[2]Joshua A. Halpern et al., “Guideline-Discordant Care Among Direct-to-Consumer Testosterone Therapy Platforms,” JAMA Internal Medicine, jamanetwork.com. Injectables retain market leadership, but oral formulations are advancing fastest on the back of new absorption technologies, while Asia Pacific delivers the highest regional CAGR at 5.3% through 2030. Together, these forces keep the testosterone replacement therapy market on a steady upward path despite maturing growth in North America and Western Europe.

Key Report Takeaways

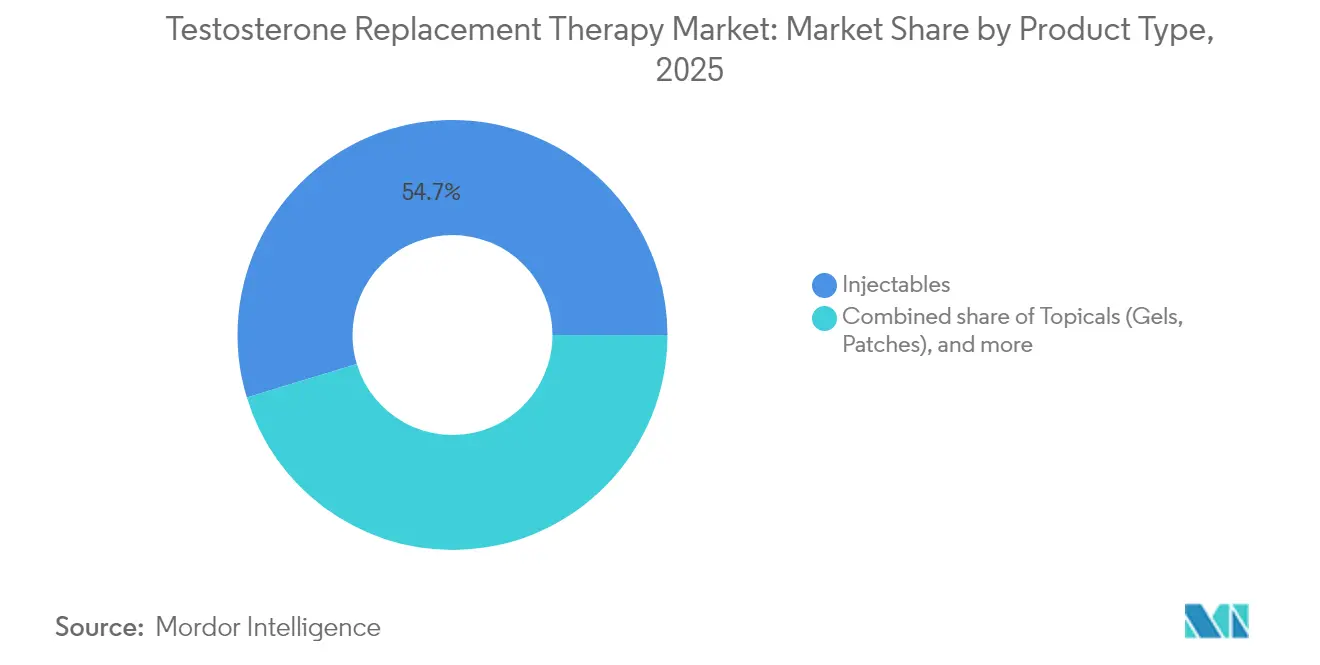

- By product type, injectables held 54.70% testosterone replacement therapy market share in 2025, whereas oral capsules/soft-gels are projected to grow at a 5.57% CAGR to 2031.

- By delivery duration, long-acting formulations accounted for 61.30% of the testosterone replacement therapy market size in 2025, with short-acting products expanding at 5.03% CAGR between 2026-2031.

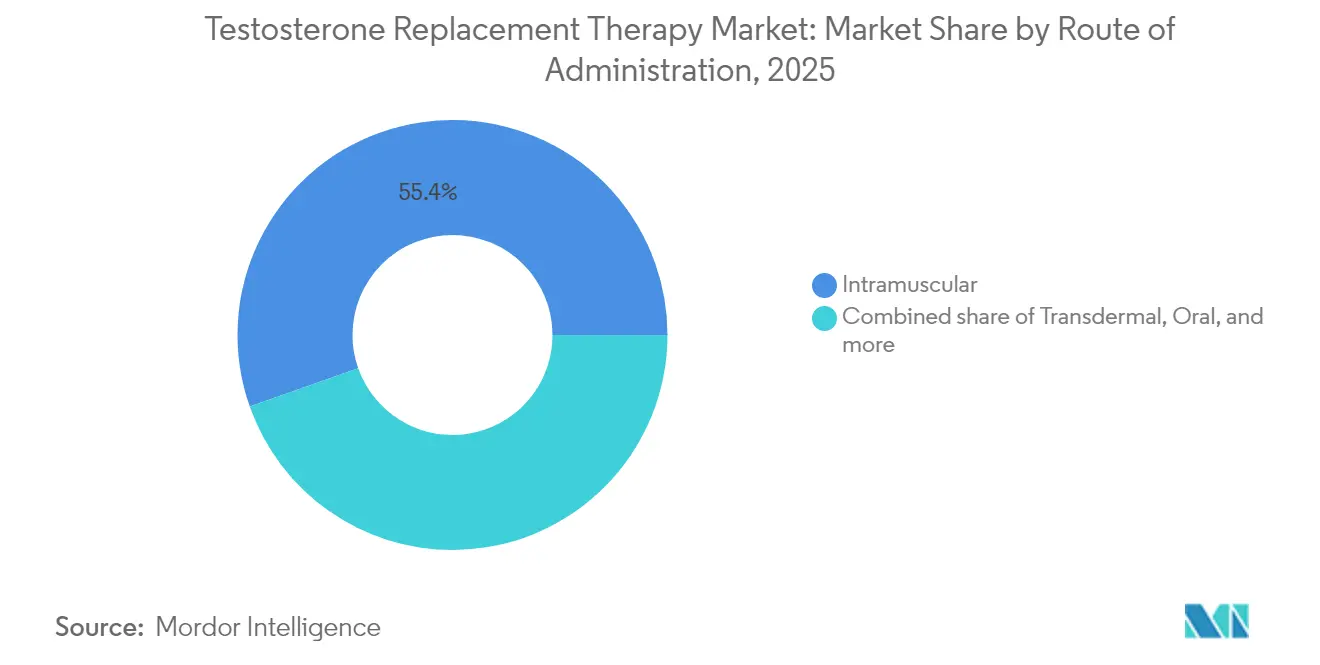

- By route of administration, intramuscular injections led with 55.40% share in 2025; subcutaneous systems show the fastest growth at 5.33% CAGR.

- By end user, hospitals captured 59.25% revenue share in 2025, while telehealth and other non-traditional settings post a 5.88% CAGR through 2031.

- By geography, North America commanded 47.60% of the testosterone replacement therapy market in 2025; Asia Pacific remains the fastest-growing region at 5.12% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Testosterone Replacement Therapy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing prevalence of age-related hypogonadism | +1.2% | North America & Europe | Long term (≥ 4 years) |

| Expanding insurance and reimbursement coverage | +0.8% | North America, Europe, developed Asia | Medium term (2-4 years) |

| Advances in long-acting and patient-friendly delivery systems | +1.0% | Global | Medium term (2-4 years) |

| Product line extensions & lifecycle management by leading pharma players | +0.6% | Global | Medium term (2-4 years) |

| Rising consumer expenditure on male health & wellness programs | +0.7% | North America, Europe, urban Asia Pacific | Medium term (2-4 years) |

| Proliferation of telehealth platforms streamlining TRT access & monitoring | +0.9% | North America, Europe, urban Asia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Prevalence of Age-Related Hypogonadism in Developed Economies

Age-related hypogonadism now affects about 20% of men over 60, and metabolic comorbidities such as obesity and diabetes further enlarge the pool of candidates for therapy. The TRAVERSE trial confirmed that testosterone does not elevate major adverse cardiac event risk, easing physician concerns and encouraging earlier treatment. In countries with rapidly aging populations, demand for physiologic hormone replacement is becoming embedded in routine men’s health screening. As a result, the testosterone replacement therapy market is expected to sustain long-term volume growth even as pricing pressure intensifies.

Expanding Insurance & Reimbursement Coverage for Testosterone Deficiency Therapies

Medicare now covers testosterone therapy for symptomatic hypogonadism rooted in primary or secondary gland dysfunction, provided biochemical confirmation is secured through two separate tests[3]Centers for Medicare & Medicaid Services, “Treatment of Males with Low Testosterone (L39086),” cms.gov. Commercial insurers have broadly followed suit, shrinking patient out-of-pocket obligations and lifting prescription volumes. Clear coverage criteria have also spurred drug developers to refine diagnostic algorithms and companion testing kits. Over the medium term, expanding reimbursement breadth should help the testosterone replacement therapy market penetrate underserved demographics without undermining payer cost controls.

Advances in Long-Acting & Patient-Friendly Drug-Delivery Technologies

Subcutaneous autoinjectors such as XYOSTED deliver stable serum levels with self-administration convenience, attracting adherence-challenged patients. Oral undecanoate capsules like KYZATREX employ lymphatic uptake to bypass hepatic first-pass metabolism and demonstrated 88% normalization in Phase 3 trials. Research into transdermal niosome-based testosome shows promise for better skin permeation with minimal irritation. Collectively, these technologies address pain, fluctuation, and safety barriers, underpinning continued expansion of the testosterone replacement therapy market.

Proliferation of Telehealth Platforms Streamlining TRT Access & Monitoring

More than 85% of direct-to-consumer clinics offer testosterone to patients who do not always satisfy guideline thresholds, effectively broadening the addressable base. Virtual consultations lower overhead, accelerate lab ordering, and improve privacy, which has historically deterred men from seeking care. Integrated platforms now bundle diagnostics, e-prescriptions, and medication shipment, enabling national reach even in underserved rural areas. As telemedicine regulations stabilize, the channel is expected to remain a high-growth pillar of the testosterone replacement therapy market.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory scrutiny on cardiovascular safety of TRT products | -0.7% | North America & Europe | Short term (≤ 2 years) |

| High therapy costs and limited reimbursement in emerging markets | -0.9% | Asia Pacific, MEA, South America | Medium term (2-4 years) |

| Risk of misuse for performance enhancement driving controlled substance policies | -0.5% | Global | Medium term (2-4 years) |

| Supply disruptions and API price volatility impacting generic manufacturers | -0.4% | Global, higher impact in emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Scrutiny on Cardiovascular Safety of TRT Products

Although the FDA removed the black-box warning, updated labels still demand blood-pressure monitoring and caution against off-label use for age-related hypogonadism. European regulators released a parallel statement endorsing safety for well-selected patients, yet emphasize ongoing surveillance. These guardrails deter indiscriminate prescribing and impose added compliance costs on manufacturers and clinicians, tempering near-term sales acceleration within the testosterone replacement therapy market.

High Therapy Costs and Limited Reimbursement in Emerging Markets

A three-month TRT course can cost up to USD 1,059 on some online platforms, a prohibitive amount for middle-income populations. In India, where testosterone deficiency prevalence reaches 21.67% among older men, limited insurance coverage restricts treatment uptake despite heightened awareness. Compounded formulations offer lower prices but raise regulatory and quality concerns. Cost barriers are therefore expected to weigh on adoption across several high-growth geographies, moderating the overall trajectory of the testosterone replacement therapy market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Oral Formulations Gain Momentum

Injectables generated the largest portion of the testosterone replacement therapy market size in 2025, reaching 54.70% share on the strength of proven efficacy and affordability. The segment received a boost from Azmiro, the first prefilled testosterone cypionate syringe designed for safe in-office or at-home use. In parallel, oral capsules and soft-gels are expanding at 5.57% CAGR due to lymphatic absorption technologies that minimize hepatic risk and simplify dosing. Patients seeking discreet, pill-based regimens are gravitating toward KYZATREX, which restored normal serum levels in 96% of men during extension trials.

Topical gels and patches retain meaningful share but face hurdles around dermal transfer and variable absorption, prompting manufacturers to incorporate permeation enhancers and quick-dry solutions. Niche formats such as subdermal pellets and intranasal sprays fill specialized needs for long-lasting release or rapid peak levels but contribute limited revenue. Continued innovation across oral and subcutaneous options is expected to shift prescribing patterns without displacing core injectable volumes, preserving balanced growth within the broader testosterone replacement therapy market.

By Delivery Duration: Patient Adherence Drives Formulation Evolution

Long-acting products control 61.30% share, underscoring patient preference for less frequent dosing that maintains steady hormone levels. Partnerships like Likarda-VitalTE aim to introduce next-generation extended-release injectables that could sustain therapeutic concentrations for several weeks. Meanwhile, short-acting alternatives deliver a 5.03% CAGR as clinicians tailor flexible regimens for dose titration or temporary supplementation.

Real-world persistence data from Ontario show oral therapy with the longest median continuation at 383 days, highlighting the interplay between convenience and adherence. Development programs such as nanoTconsign, financed via an NIH grant, target uniform release across four weeks to merge the adherence benefits of monthly dosing with the pharmacokinetic profile of daily therapy. These innovations should keep duration strategies central to competitive positioning in the testosterone replacement therapy market.

By Route of Administration: Subcutaneous Delivery Disrupts Traditional Methods

Intramuscular injections represent the backbone of the testosterone replacement therapy market with 55.40% share thanks to predictable kinetics and low cost. Nevertheless, subcutaneous autoinjectors exhibit the highest CAGR at 5.33% as self-injection comfort and reduced site pain attract new users.

Transdermal gels continue to serve patients who prefer noninvasive administration yet must manage skin irritation. Oral agents now bypass first-pass metabolism via lipid encapsulation, broadening appeal to men wary of needles. Intranasal formulations occupy a small but growing niche, valued for rapid absorption and discretion. As patient segmentation intensifies, multi-route offerings will remain critical to sustaining competitiveness and share capture within the testosterone replacement therapy market.

By End User: Non-Traditional Settings Expand Market Reach

Hospital systems controlled 59.25% of total prescriptions in 2025, driven by complex case management and integrated specialist care. Specialty urology and men’s health clinics leverage focused expertise and typically faster appointment access, capturing a meaningful share without matching hospital scale.

The fastest-growing channel at 5.88% CAGR is the “other end users” category, led by telehealth, retail health clinics, and wellness centers. The Vitamin Shoppe’s Whole Health Rx platform now dispenses KYZATREX alongside nutritional supplements, illustrating how consumer-facing brands are entering the testosterone replacement therapy market. Evidence shows virtual care reduces costs, enhances privacy, and extends reach to rural populations, positioning these channels as pivotal growth drivers for the next decade.

Geography Analysis

North America generated 47.60% of the testosterone replacement therapy market size in 2025, supported by high diagnosis rates, broad insurance coverage, and rapid adoption of novel delivery systems. The FDA’s label revision is expected to lift initiation rates further by alleviating cardiovascular risk concerns, though mandatory blood-pressure monitoring adds a layer of clinical oversight. Direct-to-consumer spend surpassed USD 400 million as telehealth firms capitalized on patient demand for convenient hormone management.

Europe remains a sizeable market with heterogeneous reimbursement policies that influence country-level uptake. Acceptance has grown following release of the European Expert Panel statement affirming cardiovascular safety under proper monitoring. An aging demographic and incremental telehealth adoption continue to propel steady demand despite stricter prescribing norms compared with the United States.

Asia Pacific posts the fastest regional CAGR at 5.12%, buoyed by urbanization, rising health expenditures, and a documented 21.67% prevalence of testosterone deficiency among older Indian men. High therapy costs and limited reimbursement temper penetration, yet expanding private insurance coverage and telehealth penetration are mitigating barriers. The Middle East, Africa, and South America trail in absolute spending yet exhibit pockets of rapid growth in Gulf states and Brazil where income levels and healthcare access are improving. Telemedicine models are increasingly important in rural UK and Latin American markets where specialist density is low. These diverse regional trends collectively underpin ongoing global expansion of the testosterone replacement therapy market.

Regulatory Landscape

In the United States, testosterone products remain regulated as prescription drugs. The FDA continues to frame approved TRT use for men with hypogonadism tied to specific medical conditions, and labels still caution against broad off-label use. In February 2025, the FDA implemented class-wide labeling changes that removed the cardiovascular boxed warning while adding blood-pressure related language, and it incorporated TRAVERSE trial information, shifting compliance emphasis toward monitoring rather than generalized cardiovascular risk statements.

In Europe, safety oversight continues through EMA processes, including PSUSA-driven harmonization and CMDh implementation of updated product information. A compliance anchor is the January 2026 implementation deadline referenced by CMDh documentation for variations for non-topical testosterone formulations, including updates addressing pulmonary oil microembolism (POME) risk and interactions (including with SGLT-2 inhibitors). Overall, these moves reinforce the region's focus on standardized pharmacovigilance and labeling alignment across member states.

Competitive Landscape

The testosterone replacement therapy market features a blend of large biopharma incumbents and focused innovators. AbbVie, Pfizer, and Eli Lilly leverage established brands and distribution, while Marius Pharmaceuticals and Halozyme compete through differentiated delivery technologies. The Vitamin Shoppe’s partnership with Marius to dispense KYZATREX through Whole Health Rx exemplifies convergence between retail wellness and prescription therapeutics.

Patent strategy remains pivotal. Marius secured a sixth US patent for KYZATREX extending exclusivity to 2040, raising entry barriers in the oral space. Halozyme’s XYOSTED benefits from proprietary ENHANZE technology that promotes consistent sub-Q absorption, differentiating it from intramuscular competitors. White-space efforts include non-steroidal agents under development at Acesis Holdings that aim to stimulate endogenous testosterone production, introducing potential future competition.

Digital health partnerships are reshaping market access. WellSync integrates laboratory testing, teleconsultations, and home delivery, streamlining the care journey and capturing data to refine adherence programs. Tolmar’s collaboration with a telemedicine network extends reach for injectable therapies in the United States. Companies are also exploring peri-operative indications, as seen in Marius’s Duke University collaboration to assess KYZATREX for muscle preservation in surgical patients. This multidimensional competition is expected to sustain innovation and keep the testosterone replacement therapy market dynamic through 2030.

Testosterone Replacement Therapy Industry Leaders

AbbVie Inc

Endo Pharmaceuticals Inc

Pfizer, Inc

Eli Lilly and Company

Bayer AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A near-term opportunity is taking shape through indication expansion pathways that US regulators are actively signaling. In April 2026, the FDA initiated a formal process around a potential new indication for testosterone therapy to treat low libido in men with idiopathic hypogonadism and invited sponsors to engage on supplemental NDA requirements. For manufacturers with established TRT platforms, this creates a clearer regulatory route to pursue broader labeled use within defined patient subsets.

Formulation and delivery innovation also continues to open whitespace beyond legacy intramuscular injections and transdermal gels, particularly where patient convenience and safety monitoring drive adoption. Peer-reviewed 2026 work on enabling oral and long-acting approaches, including a solid-state self-microemulsifying drug delivery system (S-SMEDDS) for testosterone reported as scalable on standard pharmaceutical equipment, supports differentiated oral products and lifecycle management. At the same time, the commercial channel mix continues to widen through telehealth and retail-linked care models already visible in the market, reinforcing demand for patient-friendly regimens that integrate diagnostics, prescribing, and monitoring workflows.

Recent Industry Developments

- April 2026: The US FDA opened a formal pathway for a potential new label indication for testosterone therapy to treat low libido in men with idiopathic hypogonadism and encouraged NDA holders to contact the agency on supplemental application requirements. This step elevates label expansion from informal discussion to a structured regulatory process, increasing incentives for sponsors to generate targeted evidence and pursue sNDA filings.

- February 2025: The FDA implemented class-wide labeling changes for testosterone products, removing the cardiovascular boxed warning while adding blood-pressure related warnings and monitoring language based on postmarket data and TRAVERSE trial findings. The update shifts the risk-management framework toward hypertension surveillance, affecting prescribing protocols and manufacturer labeling obligations across the category.

- December 2024: Likarda partnered with VitalTE to develop extended-release injectable hormone therapies. The collaboration supports product-development activity aimed at longer dosing intervals, aligning with the market shift toward long-acting formulations that compete on adherence and patient convenience.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the market covers prescription testosterone replacement therapy used to restore testosterone levels in patients diagnosed with testosterone deficiency, and it includes the value of therapy products sold through formal healthcare channels.

Scope exclusions: Non-prescription testosterone boosters and dietary supplements are excluded, and compounded testosterone that is dispensed without market authorization is also excluded.

Segmentation Overview

- By Product Type

- Injectables

- Topicals (Gels, Patches)

- Oral Capsules / Soft-Gels

- Other Product Types

- By Delivery Duration

- Short-Acting Formulations

- Long-Acting Formulations

- By Route of Administration

- Intramuscular

- Transdermal

- Oral

- Subcutaneous

- Intranasal

- By End User

- Hospitals

- Specialty & Urology Clinics

- Other End Users

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle-East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the baseline demand and supply context before the model was finalized. We started with public health and regulatory references that explain how TRT is prescribed and monitored. Sources reviewed include FDA drug labels and safety communications, CDC health statistics, WHO health data, and OECD health indicators, along with selected publications in peer reviewed medical journals.

To keep assumptions realistic, we also reviewed company annual reports, investor presentations, and credible press coverage describing therapy portfolio focus, geographic footprint, and major policy changes. Where needed, paid subscriptions for company financials and intelligence, patent databases, and a news and financials service were used to cross-check product launches, portfolio changes, and reported revenue direction. These examples are not exhaustive, and other public sources were also used during the work for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating which patient pools are actively treated, how product mix is shifting across injectables and topical forms, and how access pathways are changing between clinics, hospitals, and retail channels. We spoke with a mix of manufacturers, distributors, prescribing clinicians, and pharmacy side participants across APAC, EMEA, and the Americas so the model assumptions could be stress-tested against real prescribing and supply patterns.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 15% | APAC: 48% |

| Mid tier: 43% | Functional/Unit leaders: 34% | EMEA: 30% |

| Smaller Players: 22% | Managers: 51% | Americas: 22% |

Market-Sizing & Forecasting

Market sizing was built using a top-down approach where diagnosed and treated testosterone deficiency pools are reconstructed by country, then filtered through therapy adoption, typical dosing patterns, and price levels to reach an annual value. To make sure totals do not drift away from reality, the result is corroborated with selective bottom-up approximations such as sampled product volumes by formulation and a price per therapy unit check across channels.

Key inputs used in the model include the estimated prevalence of testosterone deficiency in adult male cohorts, testing and diagnosis rates, treated share versus diagnosed share, formulation mix shifts between injectables and transdermal products, and reference prices that reflect manufacturer selling price trends in major markets. Since access can change quickly, we also tracked how prescribing caution and follow-up practices influence treatment persistence. In particular, safety label updates and monitoring requirements were treated as potential drivers of near-term adoption and continuation.

Forecasting uses a scenario-based build supported by multivariate regression. The drivers are linked to demographics, diagnosis intensity, treatment continuation, and price progression by formulation. When country-level input data is missing or uneven, we used peer-country analogs and range checks with clinicians and channel participants before final numbers were locked.

Data Validation & Update Cycle

Validation is done through repeated cross-checks between the model output and independent signals such as therapy uptake direction, product mix indicators, and public health statistics that can explain demand movement. Large variances are flagged, assumptions are revisited, and follow-up calls are triggered when a mismatch cannot be explained through a clear market event.

Before sign-off, the model and written insights go through multi-step analyst review so the arithmetic, logic, and scope remain consistent across countries and years. The report is refreshed annually, and interim updates are made when material events occur. After those updates, a final pre-delivery review is run so clients receive the latest view available at that time.

Mordor Intelligence's Testosterone Replacement Therapy Market Size Compared Against Other Published Estimates

It is normal to see different market values for testosterone replacement therapy because firms do not always count the same products, countries, and value points, and they also pick different base years. Differences also come from how pricing is handled, whether patient driven demand is used, and how frequently assumptions are refreshed.

Dietary supplement testosterone boosters sit outside Mordor Intelligence's scope, and that exclusion alone can widen the spread versus estimates that blend prescription therapy with broader wellness spending. Gaps also show up when one source reports a 2024 base and another reports 2026, or when currency conversion timing and manufacturer level pricing versus retail level pricing are treated differently. Even with similar volume assumptions, those choices can shift the final totals.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.13 B (2026) | |

| Global Consultancy A | USD 2.07 B (2024) | Uses an earlier base year and applies a broader indication set in its taxonomy, which can pull in adjacent testosterone uses beyond the treated deficiency pool counted in prescription TRT. |

| Industry Publisher B | USD 1.90 B (2024) | Anchors on 2024 pricing and does not clearly state whether values are manufacturer-level or retail-level, which can compress totals when channel margins and formulation price differences are not normalized. |

Looking across the figures, most of the gap is explained by year alignment and what is counted as therapy spend, followed by how prices are converted and normalized across formulations. By keeping the scope tied to authorized prescription TRT and then validating adoption and persistence assumptions with field inputs, we can provide a number that is easier to trace back to clear demand and pricing drivers.

Key Questions Answered in the Report

What is the current Global Testosterone Replacement Therapy Market size?

The testosterone replacement therapy market stands at USD 2.13 billion in 2026 and is on track to reach USD 2.57 billion by 2031.

How fast is the testosterone replacement therapy market expected to grow?

The market is projected to expand at a 3.88% CAGR between 2026 and 2031, driven by regulatory tailwinds, aging populations, and telehealth adoption.

Which product category leads sales today?

Injectable formulations hold 54.70% market share owing to physician familiarity and cost advantages, although oral capsules are the fastest-growing segment at 5.57% CAGR.

How did the 2025 FDA label change affect the market?

By removing the cardiovascular black-box warning and mandating blood-pressure monitoring, the FDA eased safety concerns and broadened access, supporting prescribing growth.

What role does telehealth play in TRT adoption?

Direct-to-consumer platforms cut stigma and geographic barriers, already surpassing USD 400 million in US spending and contributing meaningfully to market expansion.

Page last updated on: