Serum-free Media Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

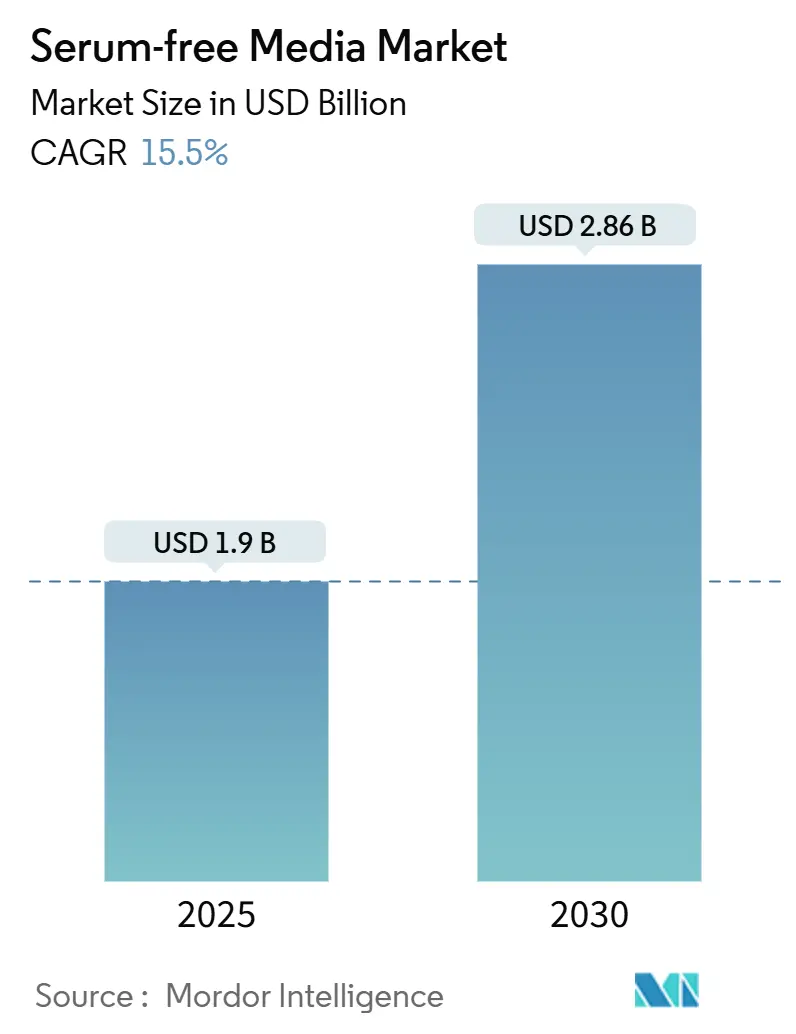

| Market Size (2025) | USD 1.9 Billion |

| Market Size (2030) | USD 2.86 Billion |

| Growth Rate (2025 - 2030) | 15.50% CAGR |

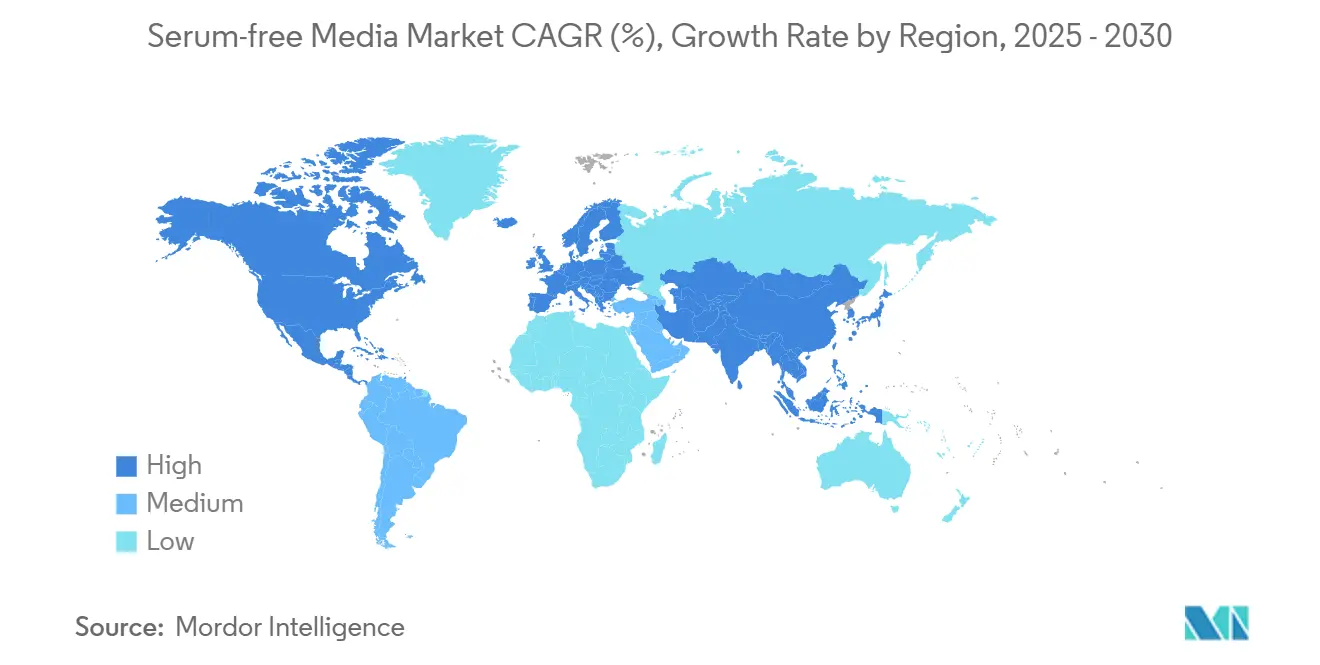

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Serum-free Media Market Analysis by Mordor Intelligence

The serum-free media market size stood at USD 1.90 billion in 2025 and, propelled by a strong 15.5% CAGR, is forecast to climb to USD 2.86 billion by 2030. Uptake is fuelled by regulators phasing out animal-derived inputs, the sharp rise in cell- and gene-therapy trials, and the scale-up of monoclonal antibody plants that now dominate global biologics capacity. Food-tech start-ups developing cultivated meat add an entirely new demand pool, while artificial-intelligence tools shorten formulation cycles and improve batch consistency. Suppliers that integrate recombinant-protein production and single-use bioreactor know-how are widening the performance gap over legacy competitors, even as supply bottlenecks for transferrin and growth factors persist. Pricing remains a hurdle, yet mandated compliance timelines in North America, Europe and parts of Asia give the serum-free media market a predictable demand floor through 2030.

Key Report Takeaways

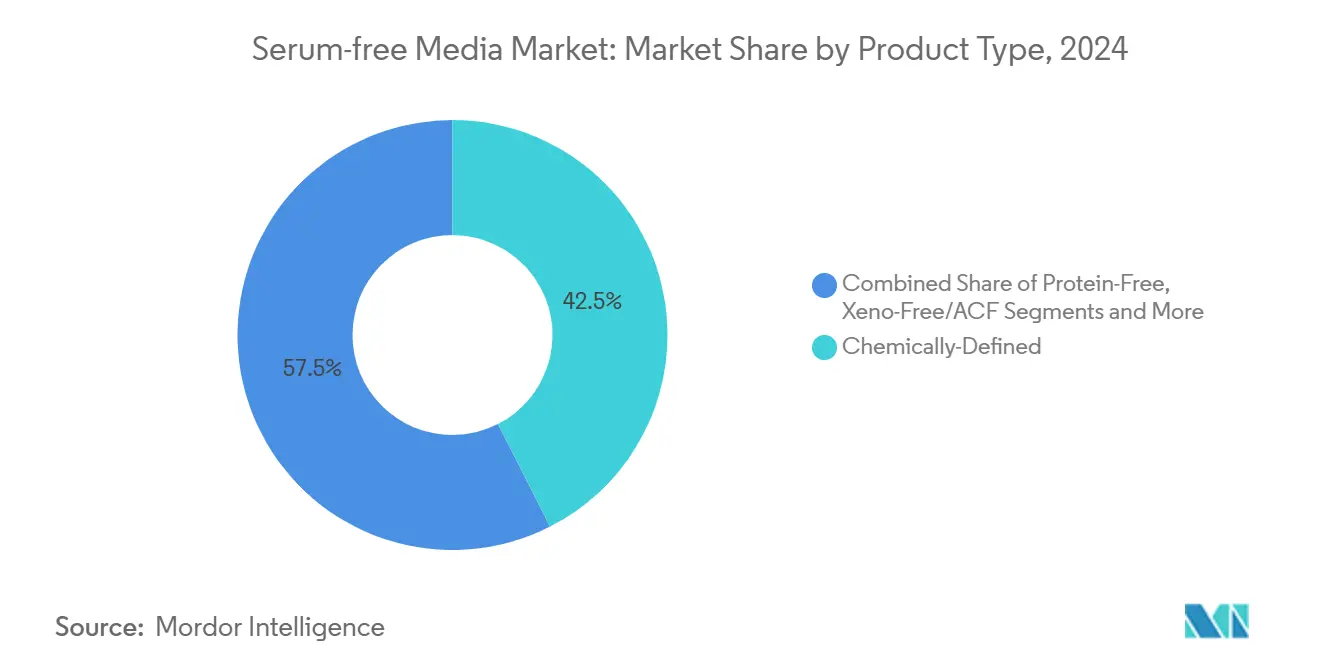

- By product type, chemically-defined formulations led with 42.5% of serum-free media market share in 2024; xeno-free and animal-component-free media is accelerating at a 14.2% CAGR to 2030.

- By application, biopharmaceutical production accounted for 38.2% of the serum-free media market size in 2024, while gene and cell therapy manufacturing is advancing at an 18.5% CAGR through 2030.

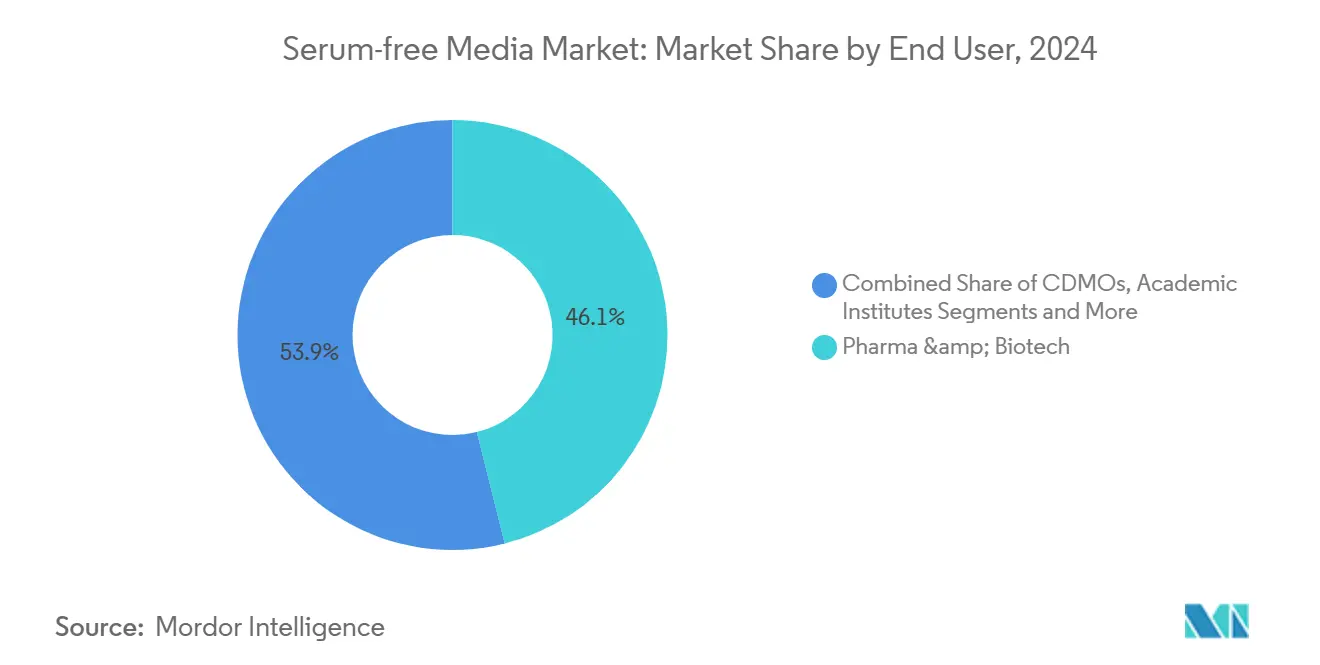

- By end user, pharmaceutical and biotechnology companies held 46.1% of serum-free media market share in 2024; food-tech firms are expanding at a 14.0% CAGR to 2030.

- By cell-type formulation, CHO media captured 51.6% of the serum-free media market size in 2024, whereas mesenchymal stem-cell media is growing fastest at 16.1% CAGR.

Global Serum-free Media Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Expansion Of Cell & Gene Therapy Clinical Pipeline | +3.90% | Global, with concentration in North America & EU | Medium term (2-4 years) |

| Regulatory Push For Animal-Component-Free Bioprocessing | +3.10% | Global, led by FDA and EMA regulations | Short term (≤ 2 years) |

| Biopharma Scale-Up Of Monoclonal Antibody Production | +2.80% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Cost-Reduction Breakthroughs In Cultivated-Meat Media | +2.30% | North America & EU, early adoption in Singapore | Long term (≥ 4 years) |

| AI-Driven, High-Throughput Nutrient-Mix Optimisation | +1.90% | Global, with technology hubs leading adoption | Medium term (2-4 years) |

| Shift Toward Closed, Single-Use Bioreactor Platforms | +1.60% | Global, particularly in emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of Cell & Gene Therapy Clinical Pipeline

More than 3,000 active cell- and gene-therapy studies now require strictly defined, animal-free growth environments that legacy serum media cannot deliver. Fifteen cell therapies cleared regulators in 2024 alone, each needing bespoke nutrient cocktails that preserve potency at commercial scale.[1]U.S. Food & Drug Administration, “Guidance for Industry: Animal-Derived Component Risks,” fda.govDevelopers, therefore, prioritize media optimization early in process design, aware that culture conditions directly influence therapeutic yield and cost-of-goods. Demand is centred in the United States and Europe, yet authorized products are increasingly manufactured in lower-cost Asian plants, further globalizing supply requirements. Custom-media service providers have responded with platform libraries covering CAR-T, TCR-T, and viral-vector workflows, reducing time-to-clinic for small sponsors. As clinical pipelines mature into licensed products, the serum-free media market gains a non-cyclical revenue stream anchored in long-term commercial supply agreements.

Regulatory Push for Animal-Component-Free Bioprocessing

The FDA’s 2024 guidance mandates serum-free production for new biologics license applications, eliminating the residual cost advantage of serum-supplemented processes.[2]U.S. Food & Drug Administration, “Guidance for Industry #293: FDA Enforcement Policy for AAFCO-Defined Animal Feed Ingredients,” U.S. Food & Drug Administration, fda.govThe European Medicines Agency adopted parallel language the same year, creating a harmonized trans-Atlantic rule set that discourages regional arbitrage. Similar frameworks are emerging in China, South Korea, and Brazil, largely to ease market-entry barriers for local firms exporting to the United States or European Union. Compliance deadlines are short, forcing manufacturers to phase out serum stocks and validate new media within existing filing windows. Suppliers with ready-to-use, chemically-defined blends therefore benefit from accelerated qualification cycles. Although smaller research institutes lobby for price relief, regulators show little appetite for exemptions, ensuring that the serum-free media market maintains regulatory pull across all therapeutic classes.

Biopharma Scale-Up of Monoclonal Antibody Production

Global stainless-steel and single-use bioreactor capacity expanded by more than 1.5 million L in 2024, led by Lonza’s USD 1.2 billion acquisition of Genentech’s Vacaville mega-site with 330,000 L of tanks. Mature blockbuster antibodies now share floor space with next-generation bispecifics, each relying on CHO cultures optimized in serum-free feeds. With demand for antibodies growing at roughly 8% a year, operators require media that sustains high cell densities while limiting by-product accumulation to simplify downstream purification. CHO-specific innovations, such as controlled amino-acid release and iron chelation, give premium suppliers an edge. The expansion wave spreads to Singapore, Ireland, and South Korea, embedding the serum-free media market in every central biologic’s corridor.

Cost-Reduction Breakthroughs in Cultivated-Meat Media

Pilot plants producing chicken, pork, and seafood analogues have slashed growth-medium cost from USD 400 to under USD 50 per L, inching toward the sub-USD 10 benchmark needed for mainstream retail pricing.[3]AGC Biologics, “Denmark Single-Use Capacity Expansion,” biopharminternational.com Source: Singapore Food Agency, “Approval of Cultivated Meat Products,” sfa.gov.sg Singapore’s 2024 authorization of cultivated chicken nuggets triggered heavy venture funding and a dozen additional license applications. Unlike pharmaceutical products, food cells must differentiate into muscle, fat, and connective tissue simultaneously, demanding unique vitamin and growth-factor ratios. The opportunity pulls specialty suppliers that have never served pharma, widening the competitive field and injecting price pressure. As commercial facilities ramp up after 2027, the serum-free media market sees a volume surge that partially offsets lower per-litre margins.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium Pricing Versus Serum-Containing Media | -1.20% | Global, particularly impacting emerging markets | Short term (≤ 2 years) |

| Cell-Line Adaptation & Performance Variability | -0.90% | Global, affecting all therapeutic applications | Medium term (2-4 years) |

| Recombinant-Protein Supply Bottlenecks | -0.80% | Global, concentrated in specialized protein markets | Short term (≤ 2 years) |

| IP Fragmentation Around Novel Growth-Factor Cocktails | -0.60% | North America & EU, affecting innovation centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Premium Pricing Versus Serum-Containing Media

Serum-free formulations can cost three to ten times more than fetal-bovine-serum blends, straining budgets for academics and emerging-market contract manufacturers. While large biopharma firms view the premium as a regulatory compliance fee, smaller players may delay media conversion or negotiate hybrid feeds, slowing penetration. Volume growth in cultivated meat could unlock scale efficiencies, but price parity is unlikely before 2028. Suppliers mitigate the barrier with bulk-buy discounts, powder formats that lower freight costs, and tiered-performance ranges that match different purity needs. Nonetheless, price sensitivity keeps some cost-driven applications—such as diagnostics or veterinary vaccines—on legacy serum feeds for the near term.

Cell-Line Adaptation & Performance Variability

Transitioning an established clone from serum-supplemented to serum-free conditions often requires six to twelve months of iterative passaging, during which growth rates and protein glycosylation can fluctuate. Any drift demands comparability studies that add expense and delay filings. Especially in late-stage programmes, developers worry about regulatory scrutiny if product attributes shift. Media vendors now offer stepwise adaptation kits and on-site technical support, but the learning curve remains steep for companies with limited process-development bandwidth. Performance risk, therefore, tempers the otherwise strong pull of the serum-free media market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Chemically Defined Media Underpin Regulatory Confidence

Chemically defined blends dominated the 2024 serum-free media market with a 42.5% share, reflecting global preference for reproducible, animal-origin-free formulations that simplify validation dossiers. Their appeal lies in narrow lot-to-lot variation and transparent certificates of analysis, attributes now insisted upon by most biologics’ sponsors. The segment benefits from broad applicability across CHO, HEK, and insect systems, making it a one-stop solution for multi-platform CDMOs.

Demand for xeno-free and animal-component-free products rises at a 14.2% CAGR as regulators outlaw bovine components even in ancillary processing steps. Protein-free variants carve a niche in recombinant protein production, where downstream purification drives cost-of-goods. Custom-media co-development, often using AI modelling, emerges as a premium service line commanding double-digit margins. Supplemented transition kits continue to sell into academia, offering a managed pathway from serum to full chemical definition. Collectively, these dynamics keep the serum-free media market size for product-type offerings on an upward trajectory.

By Application: Gene Therapy Manufacturing Surges Ahead

Traditional biologics retained 38.2% of the serum-free media market size in 2024, yet growth is briskest in gene and cell therapy facilities, expanding at an 18.5% CAGR through 2030. Viral-vector operations require high-density HEK293 cultures with stringent impurity controls, pushing media optimization to the forefront of process economics.

COVID-19 accelerated demand for vaccines and viral-vector media capable of rapid scale-up under emergency timelines. Stem-cell laboratories adopt pluripotent-supporting blends for organoids and regenerative implants, while cultivated meat pioneers demand cost-down innovations for muscle and fat cell differentiation. These new verticals broaden the serum-free media market, lessen its dependence on monoclonal antibodies, and deepen supplier specialization in cell-specific performance drivers.

By End User: Food-Tech Injects Non-Pharma Dynamism

Pharmaceutical and biotechnology firms held 46.1% of the serum-free media market share in 2024, a testament to entrenched purchase volumes and multi-year supply contracts. Yet the fastest-growing customer set is food-tech, where cultivated-meat ventures log a 14.0% CAGR as they shift from pilot to 10,000-L bioreactors.

CDMOs expand sourcing volumes to serve small biopharma entrants lacking in-house manufacturing, while academic labs remain price-sensitive but influential as early adopters of novel cell lines. Contract research organizations standardize media across multiple sponsors, indirectly steering broader adoption. Collectively, this end-user mosaic diversifies revenue and insulates the serum-free media industry against single-sector downturns.

By Cell-Type Formulation: CHO Media Remains King but MSC Demand Rises

CHO media accounted for 51.6% of the serum-free media market size in 2024, tied to its unrivalled role in therapeutic antibody output. Suppliers refine amino-acid profiles and feed strategies to chase incremental titre gains that translate directly into lower cost per gram.

Mesenchymal stem-cell blends, growing at 16.1% CAGR, underpin regenerative products targeting osteoarthritis, cardiac repair and aesthetic procedures. HEK293 media dominates transient backbones for adeno-associated-virus vectors, while hybridoma and primary-cell mixes serve discovery and tissue-engineering niches. Each formulation track demands unique growth-factor suites, reinforcing supplier specialization and further segmenting the serum-free media market.

Geography Analysis

North America retained 41.2% of global revenue in 2024, buoyed by the FDA’s stringent stance on animal-component elimination and continuous investment in large-scale antibody plants such as Vacaville and Worcester. The region’s venture ecosystem also backs dozens of cell-therapy start-ups, extending demand beyond Big Pharma. Capital-expenditure cycles through 2030 suggest sustained media volumes irrespective of individual product launch success.

Asia Pacific is the growth pacesetter with a 12.6% CAGR, driven by China’s biomanufacturing buildout, India’s CRO boom, and Singapore’s first-in-the-world approval of cultivated meat. Governments provide tax holidays for serum-free facilities, and local reagent makers are closing quality gaps, eroding import dependence. Japanese, Korean, and Australian clusters add steady premium-grade demand, making the region both a production hub and an end market for high-spec media.

Europe, though mature, shows resilient uptake as the EMA aligns fully with FDA guidance on serum elimination. Germany’s bio-manufacturing scale, the United Kingdom’s regenerative-medicine focus, and France’s vaccine leadership sustain core volumes. Eastern Europe offers lower-cost fill-finish sites, which are now upgrading to single-use systems, a shift that indirectly increases serum-free media penetration. Collectively, these geographic drivers round out a balanced demand profile for the serum-free media market.

Competitive Landscape

Market concentration is moderate: the top five suppliers hold an estimated 45-50% share, while dozens of regional players fill niche gaps. Global leaders differentiate through end-to-end platforms that pair media with single-use bags, filters, and analytics, enabling turnkey process packages for CDMOs. Vertical integration into recombinant protein expression has reduced lead times for critical growth factors, a decisive advantage during the 2024-2025 supply crunch for transferrin.

Strategic partnerships proliferate. Lonza links the Stein and Vacaville media suites to contract development services, locking clients into proprietary feeds. Thermo Fisher licenses its machine-learning engine to mid-tier firms, embedding digital optimization into the purchasing decision. WuXi Biologics bundles media with bioreactor build-outs for Chinese domestic clients and export-oriented Western sponsors.

White-space entrants target cultivated meat, formulating food-grade cytokines at one-tenth pharma pricing. Patent clustering around novel plant-based growth-factor cocktails creates licensing revenues for early movers but raises barriers for late entrants. The competitive race increasingly hinges on data: suppliers offering real-time nutrient-depletion dashboards strengthen customer lock-in and command price premiums, reshaping value capture across the serum-free media industry.

Serum-free Media Industry Leaders

Thermo Fisher Scientific

Merck KGaA (MilliporeSigma)

Lonza Group

Danaher Corporation

FUJIFILM Irvine Scientific

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Multus Media launched Proliferum P serum-free growth medium specifically designed for porcine stem cells, targeting cultivated pork production with cost-optimized formulations.

- January 2025: Bio-Techne launched ExCellerate B Cell Media targeting the cell therapy manufacturing segment, featuring xeno-free formulations optimized for B cell expansion protocols required for CAR-B cell therapies.

- January 2025: STEMCELL Technologies introduced ImmunoCult serum-free media for T cell therapy applications, achieving a 25% cost reduction compared to competitor products while meeting clinical manufacturing requirements.

- October 2024: FUJIFILM Irvine Scientific launched BalanCD CHO Growth A serum-free media achieving 40% higher cell density compared to traditional formulations while maintaining therapeutic protein quality standards.

Global Serum-free Media Market Report Scope

| Chemically-Defined Media |

| Protein-Free Media |

| Xeno-Free / Animal-Component-Free Media |

| Custom / Tailored Media Services |

| Supplemented SFM Kits & Additives |

| Biopharmaceutical Production |

| Gene & Cell Therapy Manufacturing |

| Vaccine & Viral Vector Production |

| Stem-cell & Regenerative-medicine Research |

| Cultivated Meat & Alternative Proteins |

| Pharmaceutical & Biotechnology Companies |

| Contract Development & Manufacturing Organizations (CDMOs) |

| Academic & Research Institutes |

| Contract Research Organizations (CROs) |

| Food-tech & Cultivated-meat Companies |

| CHO Cell Media |

| HEK293 Media |

| Hybridoma Media |

| Mesenchymal Stem-cell Media |

| Primary & Other Mammalian Cell Media |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Chemically-Defined Media | |

| Protein-Free Media | ||

| Xeno-Free / Animal-Component-Free Media | ||

| Custom / Tailored Media Services | ||

| Supplemented SFM Kits & Additives | ||

| By Application | Biopharmaceutical Production | |

| Gene & Cell Therapy Manufacturing | ||

| Vaccine & Viral Vector Production | ||

| Stem-cell & Regenerative-medicine Research | ||

| Cultivated Meat & Alternative Proteins | ||

| By End User | Pharmaceutical & Biotechnology Companies | |

| Contract Development & Manufacturing Organizations (CDMOs) | ||

| Academic & Research Institutes | ||

| Contract Research Organizations (CROs) | ||

| Food-tech & Cultivated-meat Companies | ||

| By Cell-type Specific Formulation | CHO Cell Media | |

| HEK293 Media | ||

| Hybridoma Media | ||

| Mesenchymal Stem-cell Media | ||

| Primary & Other Mammalian Cell Media | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the serum-free media market?

The serum-free media market size reached USD 1.90 billion in 2025 and is projected to hit USD 2.86 billion by 2030.

Which segment is expanding the fastest?

Gene and cell therapy manufacturing is set to grow at an 18.5% CAGR through 2030, the highest among all application segments.

Why are chemically-defined formulations preferred?

They eliminate animal components, reduce batch variability and align with FDA and EMA guidance, helping sponsors accelerate regulatory approval.

Which region shows the strongest growth potential?

Asia Pacific leads with a 12.6% CAGR, driven by Chinas capacity build-out and Singapores leadership in cultivated meat.

How does pricing compare with serum-containing media?

Serum-free blends remain 310 times more expensive per litre, though scaling and cultivated-meat demand are narrowing the gap.

Who are the leading suppliers?

Global leadership is shared among Lonza, Thermo Fisher, Fujifilm, Merck Millipore and Cytiva, together capturing almost half of worldwide sales.

Page last updated on: