High Content Screening Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.14 Billion |

| Market Size (2031) | USD 2.84 Billion |

| Growth Rate (2026 - 2031) | 5.83% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

High Content Screening Market Analysis by Mordor Intelligence

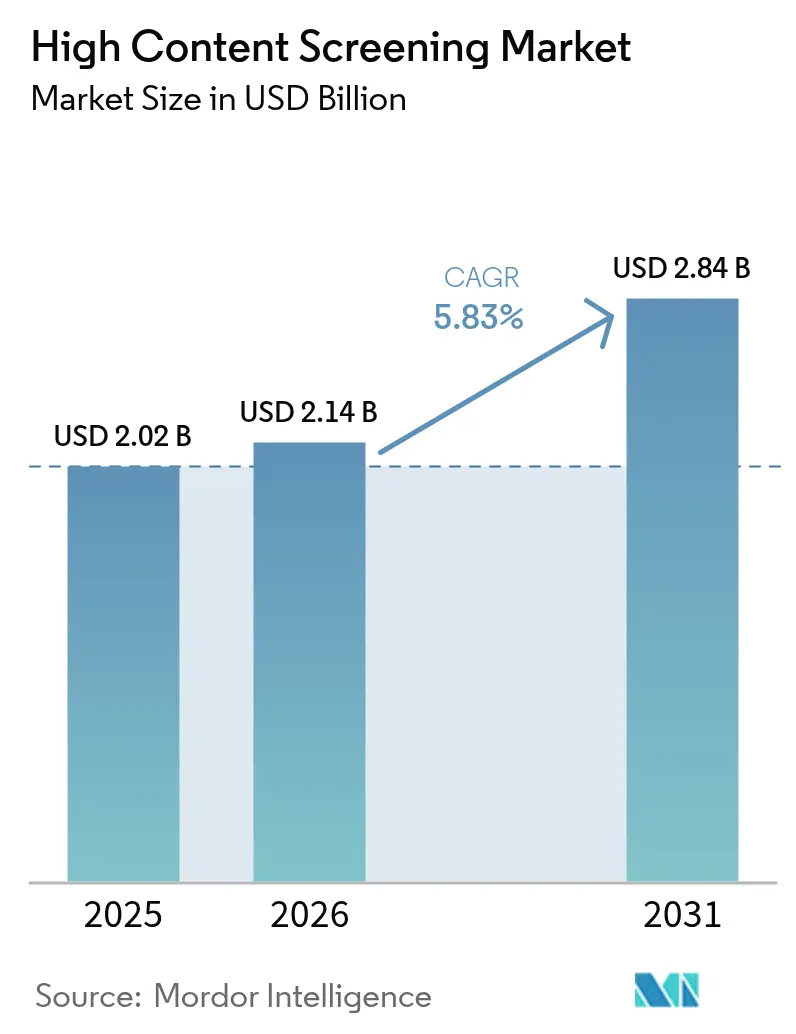

The High Content Screening market size is expected to grow from USD 2.02 billion in 2025 to USD 2.14 billion in 2026 and is forecast to reach USD 2.84 billion by 2031 at 5.83% CAGR over 2026-2031. This expansion is underpinned by rapid AI integration, automated imaging innovations, and the need to accelerate drug-candidate triage while curbing R&D expenses. Pharmaceutical companies now deploy scalable cloud-connected instruments that analyze millions of phenotypic images daily, unlocking deeper insights from existing compound libraries and shortening pre-clinical timelines. Competitive dynamics favor vendors capable of combining robust optics with containerized AI pipelines, while regional growth increasingly shifts to Asia-Pacific as local regulators streamline IND approvals and multinational sponsors broaden trial footprints. Instruments still account for the largest revenue block, yet software subscriptions eclipse all other categories in velocity as laboratories migrate analytics to elastic computing environments. End-user outsourcing to contract research organizations (CROs) intensifies, granting smaller biotechs turnkey access to high-throughput phenotypic data and supporting the rise of virtual R&D models.

Key Report Takeaways

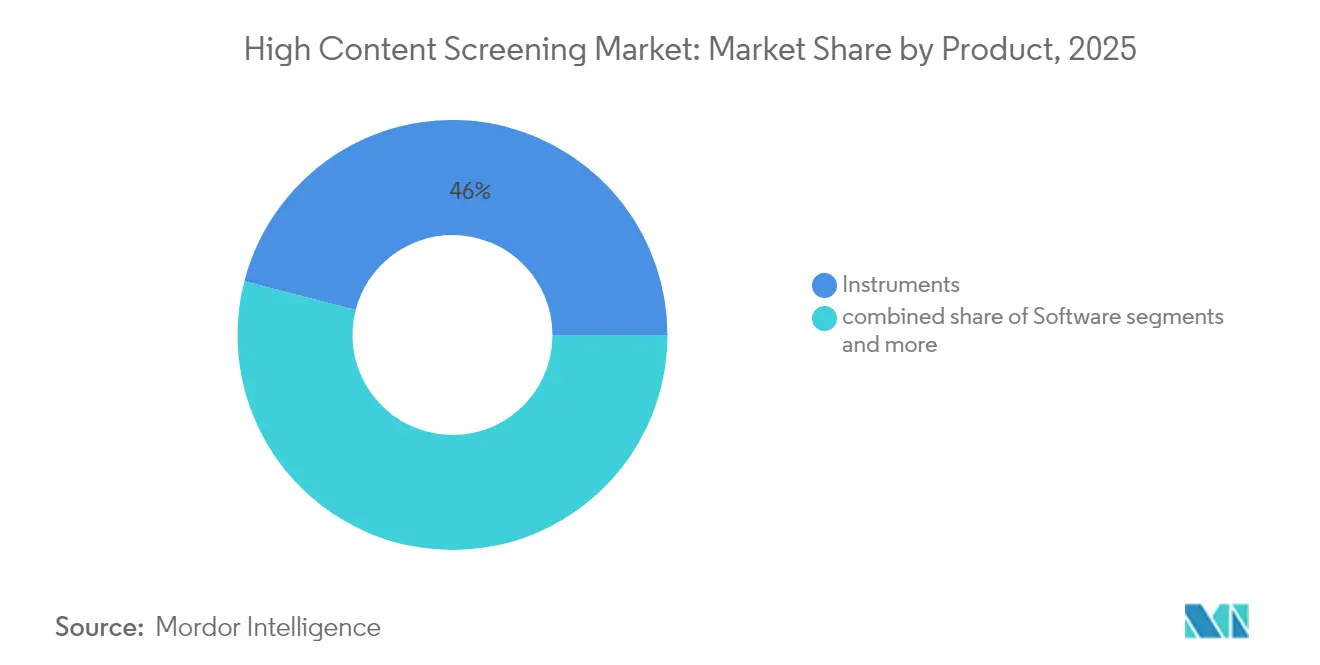

- By product category, instruments held 45.98% of the High Content Screening market share in 2025; software is projected to expand at a 5.93% CAGR through 2031.

- By application, primary and secondary screening captured 38.62% of the High Content Screening market size in 2025 and phenotypic screening for 3D organoids is advancing at a 6.02% CAGR through 2031.

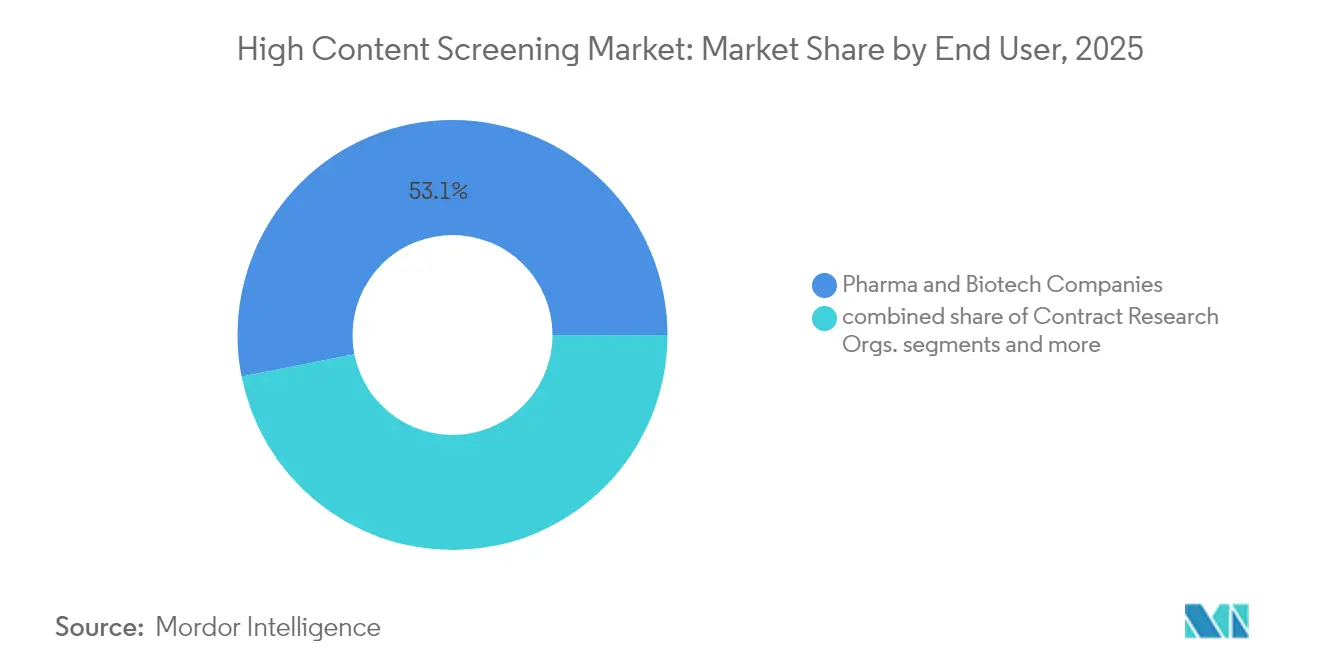

- By end-user, pharmaceutical and biotechnology companies controlled 53.10% of the High Content Screening market share in 2025, while CROs register the highest projected CAGR at 6.74% to 2031.

- By geography, North America led with 41.78% revenue share in 2025; Asia-Pacific posts the fastest regional CAGR at 6.17% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of High Content Screening Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost-effective drug discovery imperatives | +1.2% | North America, EU dominant; global relevance | Medium term (2-4 years) |

| AI-powered image-analysis advancements | +0.9% | North America lead, APAC rapidly scaling | Short term (≤2 years) |

| Oncology-focused funding surge | +0.8% | North America and EU; APAC emerging | Medium term (2-4 years) |

| Phenotypic screening adoption for 3D organoids | +0.7% | Early adoption in developed markets; global spread | Long term (≥4 years) |

| Cloud-connected instruments | +0.5% | Broad global uptake | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Cost-effective Drug Discovery Imperatives

Escalating R&D outlays and persistent late-stage attrition compel drug makers to embrace High Content Screening market solutions that streamline hit-to-lead decision making. Cloud labs drastically lower capital barriers by shifting image acquisition and analysis workloads to pay-as-you-go infrastructures, allowing smaller firms to interrogate large libraries without owning microscopes or robotics. Multinational sponsors reallocate budgets from brick-and-mortar buildouts toward flexible AI subscriptions that scale with portfolio needs, and CROs respond by bundling phenotypic profiling with medicinal chemistry to deliver turnkey asset incubation. Collectively, these shifts reinforce sustainable demand growth across mature and emerging economies.

AI-powered Image-analysis Advancements

Deep convolutional networks now extract subtle morphological signatures from multiplexed fluorescent images, lifting hit-identification rates to 23.8% within the top 1% of ranked compounds. Vendors launch platforms that embed pre-trained models and secure on-prem inference to satisfy data-residency mandates. Pharmaceutical teams leverage these engines to map compound-response trajectories, revealing pathway cross-talk and mechanistic liabilities earlier than legacy pipelines allowed. The net result is faster cycle times, optimized reagent usage, and enriched lead diversity.

Oncology-focused Funding Surge for Cell-based Research

Cancer programs dominate phenotypic screening demand as precision medicine shifts toward patient-specific models. Patient-derived tumor organoids display 87.5% successful culture establishment, supporting relevant drug-response readouts. Venture and partnership capital flows intensify, exemplified by Orionis Biosciences securing USD 105 million upfront and milestone gates above USD 2 billion with Genentech to unlock molecular glues that exploit synthetic lethality. The FDA initiative to curtail animal models further accelerates human-relevant assays, cementing oncology as a long-run growth pillar.

Phenotypic Screening Adoption for 3D Organoids

Three-dimensional cultures replicate extracellular matrices and vascular gradients, enabling more predictive efficacy-toxicity correlations than flat monolayers. Instrument makers integrate dual spinning-disk optics, high-sensitivity sCMOS sensors, and adaptive autofocus to capture volumetric stacks at low phototoxicity. High Content Screening market users apply these datasets to uncover resistance mechanisms, optimizing combination regimens before clinical dosing. Over the forecast horizon, organoid libraries evolve into stratified disease atlases that support patient-matched therapeutic selection.

Restraints Impact Analysis of High Content Screening Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital expenditure for HCS platforms | -0.8% | Global, most pronounced in emerging markets | Medium term (2-4 years) |

| Shortage of data-science talent for HCS analytics | -0.6% | Global, particularly acute in North America & EU | Long term (≥ 4 years) |

| Massive image-data storage & compliance burdens | -0.5% | Global, with stricter requirements in North America & EU | Medium term (2-4 years) |

| Inter-vendor software interoperability gaps | -0.4% | Global, affecting all markets with multiple vendor ecosystems | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital Expenditure for HCS Platforms

State-of-the-art automated imagers, robotics, and controlled-environment incubators can exceed USD 3 million per suite, deterring adoption among resource-constrained biotechs. U.S. life-science fit-out costs averaged USD 846 per square foot in 2025, climbing 4.3% year over year and squeezing new-build budgets. To mitigate sticker shock, vendors promote lease-to-own plans, modular add-ons, and outcome-based service contracts that spread expenses across multiyear projects. CROs capitalize by offering pay-per-screen options, effectively converting capex to opex for clients needing episodic throughput.

Shortage of Data-science Talent for HCS Analytics

High Content Screening industry stakeholders struggle to recruit professionals adept at Python, R, and advanced imaging pipelines. Bioprocess employers report persistent vacancy rates for algorithm and model-validation roles despite expanding headcounts. Companies respond with in-house academies and joint master’s curricula, yet supply lags demand. Consequently, fully automated analysis suites that abstract coding complexity gain traction, and partnerships with AI startups accelerate algorithm deployment to frontline scientists.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

High Content Screening Market Segment Analysis

By Product:

Instruments Lead Despite Software’s Rapid AscentIn 2025, instruments accounted for 45.98% of the High Content Screening market share, reflecting entrenched demand for high-resolution optics and integrated liquid-handling. Software subscriptions, however, post a 5.93% CAGR through 2031 as laboratories prioritize AI workflows that extend the productive life of existing hardware. The High Content Screening market size attributed to software is projected to add USD 183 million by 2031, largely through tiered analytics packages and cloud compute credits. Leading launches such as Yokogawa’s CellVoyager CQ3000 pair dual spinning-disk confocal modules with onboard GPUs, while Sartorius’ iQue 5 HTS marries 27-channel cytometry with continuous unattended runs. Accessories and reagents maintain steady mid-single-digit growth, while services expand in tandem with instrument complexity, ensuring lifecycle uptime and regulatory documentation.

As AI pipelines mature, stand-alone analysis suites integrate container orchestration, automated version control, and audit-ready reporting, meeting FDA 21 CFR Part 11 stipulations. Vendors who bundle hardware, analytics, and validation services position themselves as one-stop partners, locking in multi-year annuity streams and elevating switching barriers.

By Application:

Primary Screening Dominance Challenged by Organoid InnovationPrimary and secondary assays contributed 38.62% of 2025 revenues, cementing their role as front-line triage tools. Nonetheless, phenotypic screening of 3D organoids accelerates at 6.02% CAGR and could eclipse target-centric assays by the late 2020s. The High Content Screening market size addition from organoid workflows approaches USD 232 million over the forecast interval, underwritten by oncology pipelines and rare-disease programs seeking translational fidelity. AI-enabled models such as PAIRWISE outperform heuristic approaches when ranking combination regimens, fostering uptake in resistant tumor indications.

Toxicity studies ride regulatory shifts away from animal testing, with liver and cardiac organoids delivering earlier safety checkpoints. Target identification and validation screens integrate CRISPR perturbations with phenomic endpoints, compressing timeline from hit discovery to mechanism confirmation. Compound profiling assays further exploit multiplexed staining to map off-target liabilities, reinforcing decision quality before costly scale-up.

By End-User:

CRO Growth Outpaces Pharma ExpansionPharmaceutical and biotech firms retained 53.10% of the High Content Screening market share in 2025 due to inward integration of core discovery tasks. CROs, however, post the fastest 6.74% CAGR as venture-backed biotechs and mid-cap pharmas outsource phenotypic expertise to control burn rates. Chinese service providers benefit from cost arbitrage and streamlined regulatory pathways, capturing an expanding slice of global contracts. Academic and government institutes grow modestly, leveraging grant inflows into oncology and pandemic preparedness, while still contributing pioneering protocols that commercial entities later scale. Diagnostic laboratories and specialized service shops form a long-tail of demand, applying high-content imaging to companion diagnostic and biomarker discovery projects.

Geography Analysis

North America and APAC High Content Screening Market

North America generated 41.78% of 2025 revenues, anchored by entrenched biopharma clusters and robust venture funding. Asia-Pacific grows at 6.17% CAGR through 2031, powered by China’s IND surge from 688 filings in 2019 to 2,298 in 2023 with 83.5% approval. Regional governments invest in GMP-compliant cell-manufacturing suites and digital regulatory portals, reducing approval latency and attracting multinational trial sponsors.

EMEA and South America High Content Screening Market

Europe maintains a steady expansion path, with the European Health Data Space fostering interoperable AI projects that integrate clinical, imaging, and molecular datasets. South America and Middle East & Africa collectively contribute a small but rising share as local contract sites expand capacity for multinational phase I–III trials.

Regulatory Landscape

High content screening (HCS) platforms typically fall under broader governance for model-informed drug development (MIDD), AI-enabled analysis, and new approach methodologies (NAMs) used to support regulatory submissions, rather than under HCS-specific statutes. In January 2026, the International Council for Harmonisation (ICH) adopted the M15 guideline on general principles for MIDD, which raises expectations around data quality, traceability, and documentation practices that shape how HCS-derived datasets and image-analytics outputs are curated for regulated decision-making. In parallel, FDA programs such as ISTAND provide a pathway to qualify NAMs for a defined Context of Use, and the EMA Innovation Task Force is used for early dialogue on innovative methods, emphasizing the need for well-defined assay performance characteristics and data governance when HCS is used to generate translational evidence.

Operational compliance for HCS laboratories is anchored in facility and laboratory standards covering chemical and biosafety practices and laboratory accreditation. In the United States, laboratories are subject to OSHA 29 CFR 1910.1450 and associated Chemical Hygiene Plan requirements, and biosafety obligations can extend to frameworks such as Federal Select Agent Program guidance depending on materials handled. Accreditation requirements also shape lab quality systems, including the 2026 Comprehensive Accreditation Manual for Laboratory and point-of-care testing released by The Joint Commission, which raises the bar for documentation, process control, and competency practices that intersect with instrument validation, audit trails, and electronic record controls for high-throughput imaging environments.

Value Chain Analysis

The high content screening value chain spans upstream inputs (cell lines, plates, fluorescent probes and cell-painting kits, optical components and precision mechanics), core platform manufacturing (automated microscopes, incubators, robotics, flow-based imaging and cytometry systems), and downstream informatics (image analysis, AI model deployment, data storage, and compliance-ready reporting). Critical hardware inputs include high-quality glass and fused silica for objectives, specialty coatings and illumination components, and precision stage assemblies, while reagents and consumables drive recurring demand and protocol standardization across assays. Software has also become a key value capture point as laboratories adopt containerized AI pipelines, implement version control, and generate audit-ready reporting that aligns with electronic record expectations.

Go-to-market routes typically mix direct sales and application support for large pharmaceutical and biotechnology accounts with distributors and integrators serving academia and smaller laboratories, while services contribute through installation, method development, and lifecycle maintenance. Partnerships increasingly connect model providers and analytics developers with screening-service organizations and instrument vendors, including 2026 collaborations such as Axxam with Tessara Therapeutics to incorporate RealBrain 3D neural micro-tissues into HCS workflows, Carl Zeiss Microscopy with EDGE Biotechnologies to integrate AI-accelerated analysis into 3D high-content analysis, and Navinci Diagnostics with Uppsala University, SciLifeLab, and Pixl Bio to develop high-throughput spatial interactomics workflows. These linkages shorten time-to-assay for end users and support more standardized, human-relevant phenotypic readouts across distributed R&D footprints.

Competitive Landscape

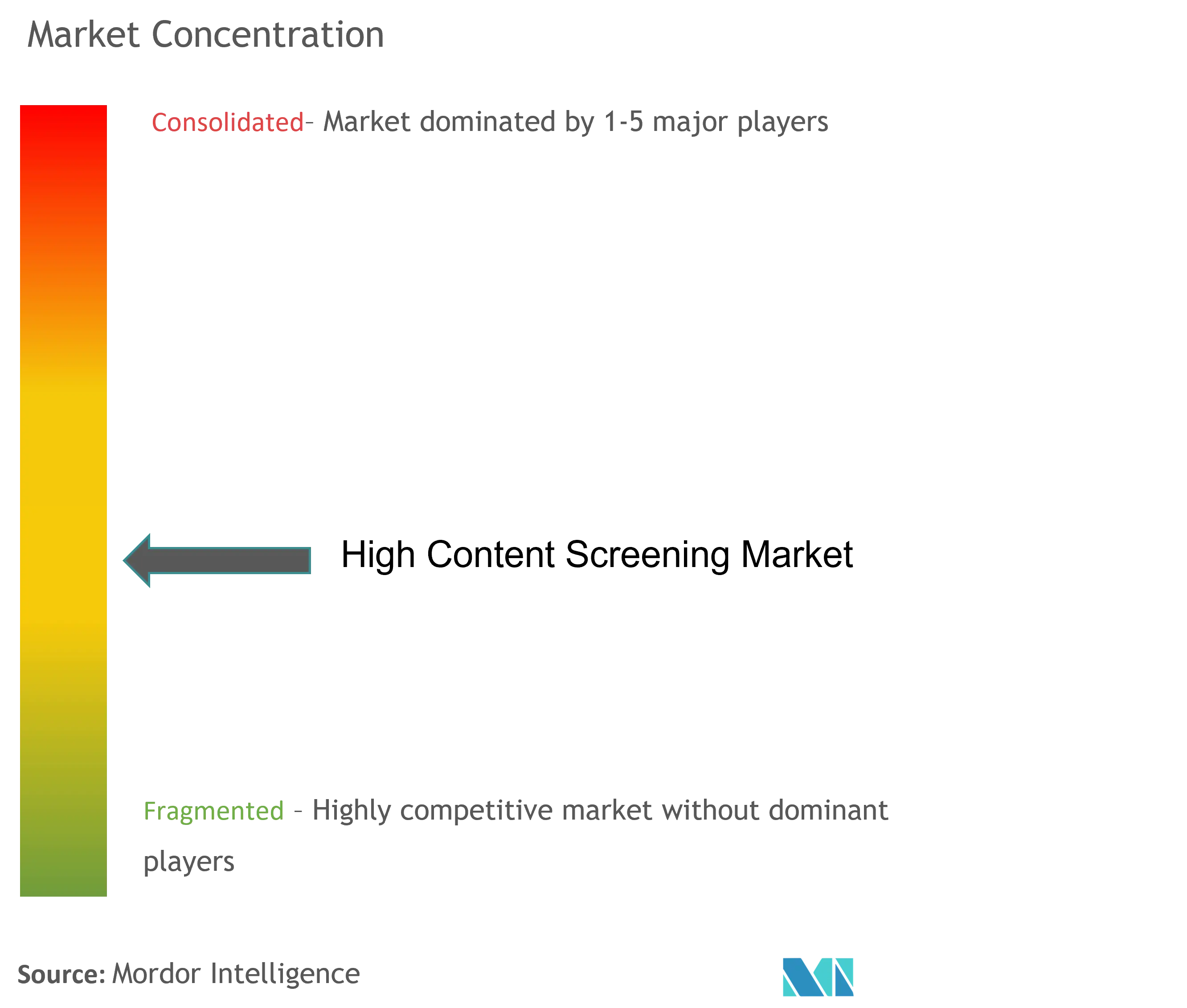

High Content Screening market competition is moderate. Top suppliers integrate hardware excellence with cloud-native analytics and regulatory templates, differentiating on total workflow value rather than standalone optics. Thermo Fisher’s USD 4.1 billion purchase of Solventum’s purification and filtration unit broadens its bioproduction ecosystem, bolstering cell-therapy media supply vital for phenotypic assays. Danaher couples imaging platforms with organoid co-development partnerships at academic medical centers, translating clinical hypotheses into validated screens. BD’s agreement with Biosero automates flow-cytometer plate handling, cutting hands-on time and variance.

Emerging challengers emphasize vertical SaaS for image analysis, instrument-agnostic data fabrics, and pay-as-you-screen marketplaces that connect compound owners with laboratory capacity. Barriers to entry include capital intensity, GMP and 21 CFR Part 11 compliance, and the necessity of multidisciplinary teams. Technology roadmaps converge on high-speed objective changers, multi-modality illumination, and low-phototoxicity optics, wrapped by secure APIs that let sponsors ingest results into FAIR-compliant repositories.

High Content Screening Industry Leaders

Perkinelmer Inc.

Danaher Corporation

Thermo Fisher Scientific Inc.

Agilent Technologies

BD (Becton, Dickinson and Company)

- *Disclaimer: Major Players sorted in no particular order

High Content Screening Market Companies Covered in this Report

- Thermo Fisher Scientific

- Danaher

- Revvity, Inc.

- GE HealthCare Technologies Inc.

- Beckton Dickinson

- Yokogawa Electric

- Agilent Technologies

- Olympus

- Sartorius

- Tecan Group

- Merck

- Bio-Rad Laboratories

- Huawei Technologies Co., Ltd. (HCS AI modules)

- Cell Signaling Technology

- ThermoGenesis

- Alpha-Med Scientific, Inc.

- Arrayjet Ltd.

- Bitplane AG (Oxford Instruments)

Market Opportunities and Future Outlook

A primary opportunity area is scaling human-relevant 3D biology and multi-omic phenotyping into routine, high-throughput decision-making, where HCS can standardize complex organoid and spheroid workflows and reduce variability across sites. Method advances that operationalize optical pooled screening and multimodal phenotyping expand addressable use cases beyond classic image-only endpoints, as reflected in the Brieflow pipeline (May 2026) for end-to-end analysis of optical pooled screening data and OttoSeq (April 2026), which integrates automated fluid handling with computational workflows to complete genome-wide optical pooled screens in eight days. This opens space for vendors and CROs to package validated assay kits, reference datasets, and compliance-ready analytics that lower barriers for smaller biotechs without dedicated image-data science teams.

Another opportunity is tighter coupling between discovery screening outputs and downstream development and manufacturing ecosystems, especially as CROs and CDMOs broaden modular capabilities that reduce handoffs across the R&D chain. Named investments in 2026 point to a wider push toward scalable, technology-enabled capacity, including Icosagen completing a EUR 45 million expansion in Tartu, Estonia to integrate therapeutic protein discovery, development, and GMP manufacturing, and Evonik committing USD 100 million over five years to modernize its Lafayette, Indiana drug substance site with an emphasis on automation and efficiency. For HCS vendors and service providers, these moves support integrated offerings that connect phenotypic screening data to developability and CMC decisions, reinforcing demand for interoperable data fabrics, secure cloud or on-prem deployment options, and standardized reporting that can be used across partner organizations.

Recent Industry Developments in High Content Screening Market

- May 2026: InSphero AG completed the acquisition of PhenoVista Biosciences, expanding its high-content imaging and phenotypic assay capabilities alongside its 3D cell-based assay portfolio. The combination supports end-to-end offerings for organoid and spheroid screening, strengthening more predictive, human-relevant workflows for drug discovery and safety testing.

- April 2026: Agilent Technologies launched the BioTek Cytation 9 cell imaging multimode reader, combining multimode microplate reading with high-content cell imaging and citing higher imaging speed versus earlier models. The release targets laboratories that want to consolidate assay readouts on a single platform while scaling throughput for primary and secondary screening.

- July 2024: Danaher partnered with Stanford University through the Danaher Beacon program to pursue next-generation smart microscopes for cancer drug screening. The collaboration highlights how instrument roadmaps are increasingly tied to AI-enabled imaging and translational oncology use cases, influencing competitive differentiation in high content screening systems.

High Content Screening Market Report Scope and Research Methodology

Market Definition and Coverage

This market covers the revenues earned from high content screening workflows that combine automated microscopy or imaging with software-driven image analysis to quantify cell-level changes for research decisions.

Scope exclusions: It does not count general purpose microscopes or basic plate readers that are sold without high content screening software and related screening workflows.

Segments Covered in This Report

- By Product

- Instruments

- Cell Imaging and Analysis Systems

- Flow Cytometers

- Consumables & Reagents

- Reagents and Assay Kits

- Microplates

- Other Consumables

- Software

- Services

- Accessories

- Instruments

- By Application

- Primary & Secondary Screening

- Target Identification & Validation

- Toxicity Studies

- Compound Profiling

- Other Emerging Applications

- By End-User

- Pharmaceutical & Biotechnology Companies

- Contract Research Organizations (CROs)

- Academic & Government Institutes

- Other End-Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the outer limits of the market and to ensure we were counting only screening-driven HCS spending, rather than broad life science imaging spend. We relied on public sources such as NIH and other national research funding databases, FDA and EMA public guidance and approvals context, OECD health and R&D indicators, and World Bank macro series to explain where demand is structurally stronger.

To ground pricing and shipment direction without overfitting the model, we also reviewed sources such as company annual reports, investor presentations, and scientific journals that describe phenotypic screening and assay trends. We then used association and conference materials to understand adoption patterns by lab type and geography. Where useful, paid subscriptions for company financials and intelligence, patent databases, and a news and financials feed were used to cross-check timelines and product focus. These examples are not exhaustive, and many other public and internal reference sources were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on verifying what gets purchased for real HCS workflows, how budgets split between instruments, consumables, and software, and how quickly labs refresh imaging capacity. We spoke with a mix of instrument and reagent stakeholders, software and service providers, and end users including pharma and biotech labs, CRO teams, and academic or government institutes across major regions. This helped correct assumptions from desk research where purchasing behavior and software attachment were not consistent with secondary sources.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 13% | APAC: 49% |

| Mid tier: 41% | Functional/Unit leaders: 27% | EMEA: 31% |

| Smaller Players: 22% | Managers: 60% | Americas: 20% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where the demand pool is reconstructed from life science R&D intensity and screening activity, and then translated into HCS spend using adoption and budget-allocation factors gathered from interviews. The totals were checked with selective bottom-up approximations, including sampled average selling price ranges for imaging systems, typical annual consumables pull-through per active system, and channel checks on replacement cycles. This reduced the impact of outliers before finalizing.

Key inputs that moved the model included the installed base refresh rhythm for automated imaging, the mix shift between instruments and recurring software or services, utilization trends in phenotypic screening versus targeted assays, outsourcing share moving toward CROs, and regional funding momentum in translational research. For the forecast, scenario analysis was used because demand can swing with funding cycles and drug pipeline priorities, and the scenarios were anchored to what experts expect for automation adoption and software attachment over the next five years. When bottom-up signals were missing for smaller countries or niche applications, gaps were handled by using region-level adoption proxies and then scaling with local R&D and lab infrastructure indicators.

Data Validation & Update Cycle

Outputs were validated through multiple checks, starting with variance testing across regions and across the instrument, consumables, and software splits so unusual jumps could be explained with a clear driver. The model was also compared with independent signals such as research funding direction, HCS publication and assay activity, and procurement patterns described by interviewees. A second analyst then reviewed the methodology and the final outputs before sign-off.

The dataset and assumptions are refreshed on an annual cycle, and interim updates are triggered when material events occur, such as major platform launches, regulatory changes affecting screening demand, or sharp currency moves. Before delivery, a final pass is completed so clients receive the most current view based on the latest public releases and re-contacts where something no longer lines up.

Mordor Intelligence's High Content Screening Hts Market Sizing Compared With Other Published Estimates

Published market sizes for high content screening often disagree because each publisher counts a slightly different spend pool and uses different timing for pricing and currency conversion. Differences also show up when forecasts assume faster automation uptake, or when software and services are treated as an add-on instead of a core part of the workflow.

The main gap comes from whether general lab imaging and adjacent analysis tools are mixed into the total. In its sizing, Mordor Intelligence counts revenue only when it is tied to high content screening workflows across instruments, consumables, software, and services, and then validates the split using replacement-cycle and consumables pull-through checks.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.14 B (2026) | |

| Global Consultancy A | USD 1.72 B (2025) | Uses an earlier base year and a longer horizon, and the spend pool is typically shaped more by platform adoption narratives, with less visibility on software attachment and consumables pull-through by active systems. |

| Trade Journal B | USD 2.07 B (2025) | Often presented as a press style total with limited scope notes, which can blend different product groupings and apply broad CAGR logic without showing how pricing and replacement cycles are handled. |

The spread in values is largely explained by year alignment and what gets counted inside the HCS spend pool, especially around software, services, and recurring consumables. By keeping inputs tied to measurable lab activity and by cross-checking totals with practical price and utilization signals, the sizing stays traceable and repeatable for planning.

Key Questions Answered in the Report

How big is the High Content Screening Market?

The High Content Screening Market size is expected to reach USD 2.14 billion in 2026 and grow at a CAGR of 5.83% to reach USD 2.84 billion by 2031.

What is the current High Content Screening Market size?

In 2026, the High Content Screening Market size is expected to reach USD 2.14 billion.

Who are the key players in High Content Screening Market?

Perkinelmer Inc., Danaher Corporation, Thermo Fisher Scientific Inc., Agilent Technologies and BD (Becton, Dickinson and Company) are the major companies operating in the High Content Screening Market.

Which is the fastest growing region in High Content Screening Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in High Content Screening Market?

In 2025, the North America accounts for the largest market share in High Content Screening Market.

What years does this High Content Screening Market cover, and what was the market size in 2025?

In 2025, the High Content Screening Market size was estimated at USD 2.14 billion. The report covers the High Content Screening Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the High Content Screening Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: