Culture Media Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 7.77 Billion |

| Market Size (2031) | USD 15.05 Billion |

| Growth Rate (2026 - 2031) | 14.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Culture Media Market Analysis by Mordor Intelligence

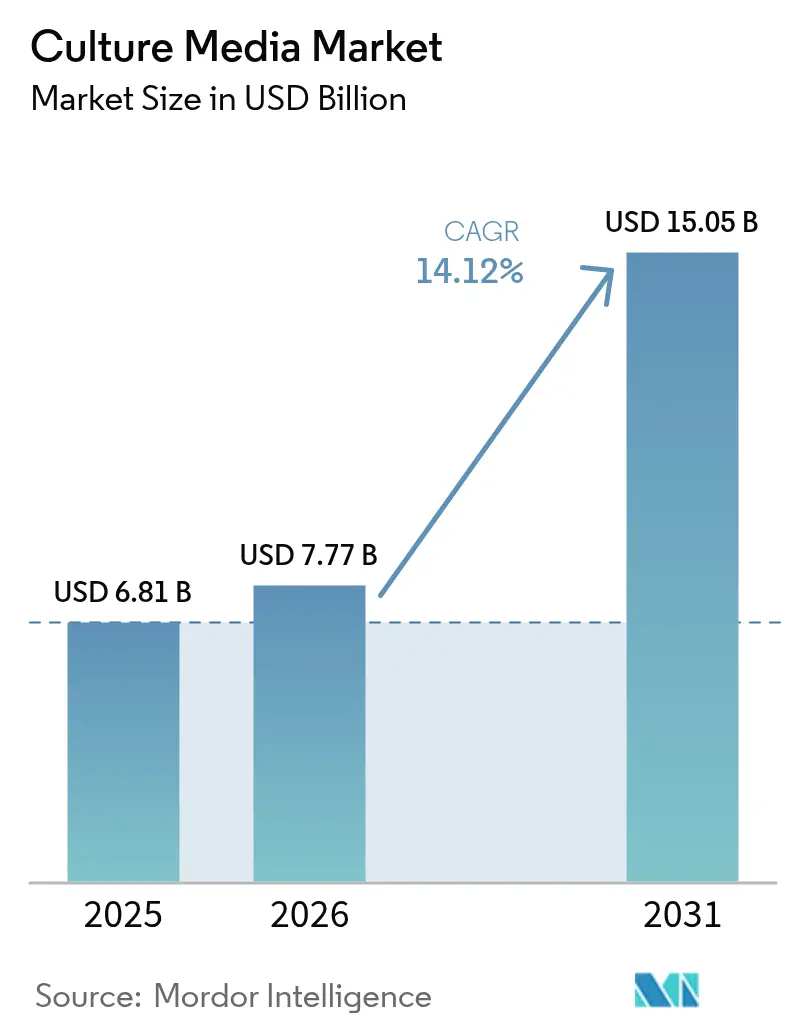

The Culture Media Market size is expected to increase from USD 6.81 billion in 2025 to USD 7.77 billion in 2026 and reach USD 15.05 billion by 2031, growing at a CAGR of 14.12% over 2026-2031.

This strong trajectory reflects the sector-wide shift to animal-component-free formulations, the repurposing of pandemic-era mRNA and viral-vector vaccine capacity, and the accelerating biosimilar pipeline that relies on bulk, pharmaceutical-grade ingredients. Regulatory agencies now favor chemically-defined media, pushing suppliers toward fully traceable raw materials and spurring investments in automated preparation systems that curb contamination risk and labor overhead. North America maintains a dominant manufacturing footprint, but Asia-Pacific expansion—backed by Chinese self-sufficiency mandates and Indian CDMO growth—will close the gap as regional suppliers capture localized demand. Tight raw-material supply chains, particularly for amino acids and recombinant proteins, threaten near-term margins, yet vertical integration and multi-site sourcing strategies are already under way among the top manufacturers.

Key Report Takeaways

- By media type, dehydrated culture media led with 51.55% of the culture media market share in 2025, while prepared ready-to-use formats are set to advance at a 15.25% CAGR through 2031.

- By formulation, serum-free products accounted for 47.53% share of the culture media market size in 2025, and chemically-defined media is forecast to grow at 15.75% CAGR to 2031.

- By physical state, liquid preparations dominated with 65.15% share in 2025, whereas semi-solid and gel media are progressing at a 15.82% CAGR to 2031.

- By end user, pharmaceutical and biotechnology firms held 36.65% revenue in 2025, but CDMOs record the fastest pace at 15.32% CAGR through 2031.

- By automation, closed-system equipment captured 55.23% of the culture media market size in 2025 and is climbing at 16.42% CAGR to 2031.

- By bioprocess application, monoclonal antibodies led with 42.23% share of the culture media market size in 2025, while cell and gene therapy is expanding at 17.82% CAGR through 2031.

- By geography, North America commanded 38.23% share in 2025; Asia-Pacific posts the quickest growth at 15.42% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Culture Media Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift from serum-based to animal-component-free media | +2.8% | Global, with early adoption in North America & EU, accelerating in Asia-Pacific | Medium term (2-4 years) |

| Rapid, large-scale mRNA / viral-vector vaccine capacity expansions | +2.5% | North America, Europe, Asia-Pacific (Australia, China, India), spillover to South America | Short term (≤2 years) |

| Biosimilar manufacturing boom creating bulk-media demand | +2.2% | Global, concentrated in India, South Korea, China, with expansion to Middle East & Africa | Medium term (2-4 years) |

| Adoption of fully-automated media-preparation systems in CDMOs & Big Pharma | +1.9% | North America & EU core markets, spillover to Asia-Pacific manufacturing hubs | Long term (≥4 years) |

| Intensified perfusion bioreactors driving high-nutrient media innovation | +1.6% | North America, Western Europe, early adoption in Singapore and South Korea | Medium term (2-4 years) |

| Region-specific halal / kosher certification opening new market pockets | +0.8% | Middle East (GCC), Southeast Asia (Malaysia, Indonesia), North Africa, niche demand in EU & North America | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Shift From Serum-Based to Animal-Component-Free Media Reshapes Supplier Landscape

Regulators now recommend chemically-defined formulations to mitigate adventitious agent risk, prompting companies to re-validate legacy processes despite per-line costs that can exceed USD 2 million. Serum volatility and stringent guidelines have accelerated adoption, with serum-free or chemically-defined preparations supporting more than 60% of new cell line adaptations in monoclonal antibody and vaccine facilities. Beyond compliance, the tighter component control improves glycosylation consistency and reduces aggregate formation, directly enhancing therapeutic efficacy. Suppliers with turnkey platforms—Thermo Fisher’s Gibco OpTmizer and Merck’s Cellvento—have captured sizable gains, while niche players such as CellGenix tailor GMP-grade mixes for CAR-T and iPSC workflows.

Rapid mRNA and Viral-Vector Vaccine Capacity Expansions Sustain Media Demand

Post-pandemic infrastructure is redeploying toward oncology and infectious-disease pipelines, maintaining elevated consumption of high-density suspension media. Moderna’s USD 1.8 billion Melbourne site exemplifies the manufacturing build-out that locks in multi-year supply contracts for nutrient-rich formulations. Viral-vector gene therapy plants require elevated glucose, lipid, and glutamine profiles, creating specialized niches for suppliers with proprietary feed strategies. Perfusion systems operating above 100 million cells per milliliter demand long-duration media that minimize osmolarity spikes, an engineering challenge now addressed through metabolite-balanced recipes validated under the FDA’s Emerging Technology Program.

Biosimilar Manufacturing Boom Generates Bulk-Media Demand in Emerging Markets

More than 150 biosimilar molecules are in clinical trials, and India’s manufacturers are ramping capacity 30% annually to capture cost-sensitive regions, favoring dehydrated formulations packed in bulk to cut freight costs. South Korean CDMOs likewise insist on logistical efficiency and redundant sourcing as geopolitical risk mitigation, awarding long-term contracts to vendors with regional production footprints. WHO guidance has shortened emerging-market approval cycles, translating pipeline momentum directly into culture media off-take.

Adoption of Fully-Automated Media-Preparation Systems Reduces Contamination and Labor Costs

Closed-system robotics now prepare more than half of commercial-scale batches, cutting technician time by 75% and delivering traceable e-batch records that pass GMP inspections with minimal remediation. Capital costs repay within two years where high-value therapies are involved. Vendors have responded with modular skids scaling from 50-2,000 liters, enabling CDMOs to standardize utilities and validation scripts across multi-suite campuses.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pharmaceutical-grade raw-material inflation & supply-chain fragility | -1.5% | Global, acute in Asia-Pacific due to China sourcing dependence, secondary impact in North America & EU | Short term (≤2 years) |

| Batch-to-batch variability hampers regulatory approvals for complex media | -1.0% | Global, most severe in emerging markets (India, China, Brazil) with limited analytical infrastructure | Medium term (2-4 years) |

| Global shortage of skilled media-optimization scientists | -0.8% | North America, Europe, Asia-Pacific (Japan, South Korea), particularly acute in cell & gene therapy sector | Long term (≥4 years) |

| End-user reluctance to validate media for continuous-processing GMP runs | -0.6% | North America & EU (early continuous manufacturing adopters), emerging in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Pharmaceutical-Grade Raw-Material Inflation Squeezes Margins and Delays Capacity Expansions

Amino acid prices spiked up to 40% from 2023-2025 as Chinese chemical-plant curbs and a European contamination shutdown hit supply, forcing vendors to renegotiate contracts and pass costs downstream. Recombinant growth factors remain an oligopoly led by Merck, Thermo Fisher, and Sino Biological, amplifying input price risk for smaller suppliers. Vertical integration—exemplified by Ajinomoto’s Thai fermentation expansion—aims to stabilize access but will require time to influence pricing.

Batch-to-Batch Variability in Complex Media Delays Regulatory Filings

Formulations containing 60 components face measurement drift in trace metals and lipid oxidation, extending validation by up to a year while developers rerun comparability studies under ICH Q11 guidance[1]International Council for Harmonisation, “ICH Q11: Development and Manufacture of Drug Substances,” ich.org . Top-tier suppliers deploy mass spectrometry and metabolomics to narrow spec windows, yet smaller regional producers struggle to fund equivalent analytics, widening quality disparities and limiting export opportunities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Media Type: Ready-to-Use Formats Gain Momentum Among GMP Producers

Dehydrated powders held 51.55% of the culture media market in 2025, buoyed by 24-month shelf lives and 30-40% lower landed costs for research labs and diagnostics facilities. Prepared liquids, however, post a 15.25% CAGR to 2031 as CDMOs and Big Pharma push contamination risk toward zero and integrate direct-connect bag systems with automated mixers. Ready-to-use bags shorten batch prep by eight hours and cut microbial excursions by an estimated 60%, satisfying regulators while freeing headcount for higher-value tasks.

Demand for chromogenic plates in clinical microbiology is reviving semi-solid variants, yet dehydrated products keep traction in emerging economies where cold-chain uncertainty favors on-site reconstitution. Hybrid concentrates—thick liquids that dilute to final strength—are bridging cost and convenience divides, letting mid-tier CDMOs sidestep sterile-filter constraints without paying full ready-to-use premiums. As continuous manufacturing proliferates, predictable just-in-time liquid feeds will reinforce the ascent of prepared products, reshaping procurement cycles across the culture media market.

By Formulation: Chemically-Defined Preparations Secure Regulatory Preference

Serum-free mixes captured 47.53% share in 2025, transitioning most monoclonal antibody and vaccine suites away from animal-derived supplements. Chemically-defined recipes, though, are expanding at 15.75% CAGR—more than triple serum-based growth—as agencies demand full traceability and xeno-free status for advanced therapies. Improvements in amino acid balance and lipid carriers now let chemically-defined media match or exceed serum-supplemented titers, shrinking performance hesitation among process engineers[2]European Medicines Agency, “Advanced Therapy Medicinal Products Overview,” europa.eu.

Stem-cell and organoid research provides a high-margin niche where GMP-grade, small-batch orders prevail; vendors such as FUJIFILM Irvine Scientific leverage premium pricing here for formulations certified across multiple pluripotent lines. For commodity biologics, serum-based legacy lines persist, but each facility shutdown for capacity expansion or technology transfer increasingly emerges with a chemically-defined process, permanently tilting the culture media market toward traceable components.

By Physical State: Semi-Solid Gel Media Benefit From Diagnostic Infrastructure Spending

Liquid media held 65.15% share in 2025, aligning with perfusion and fed-batch bioreactors that dominate biologics output. Still, semi-solid and gel formats race ahead at 15.82% CAGR as hospitals enlarge infectious-disease labs and food-safety agencies modernize surveillance with chromogenic plates delivering results within one day. Powdered blends maintain relevance in field testing and resource-scarce geographies, but rising labor costs even in Asia-Pacific are tipping procurement toward ready-to-pour agar dishes that remove preparation bottlenecks.

Perfusion trends reinforce liquid demand: automated skids now dose bioreactors continuously, devouring hundreds of liters weekly per line. Suppliers bundling liquid bags with closed-loop connectors secure multi-year volume commitments, fostering vendor lock-in that stabilizes revenue cycles across the culture media market.

By End User: Outsourcing Wave Elevates CDMOs to Fastest-Growing Customer Base

Pharma and biotech innovators accounted for 36.65% consumption in 2025, yet capital-preservation pressures move early-stage firms toward outsourced production, driving CDMOs at a 15.32% CAGR to 2031. Consolidated CDMO buying power squeezes per-liter pricing but guarantees volume, compelling suppliers to expand technical-service arms that optimize client processes in-house.

Academic institutes and public health labs, representing roughly one-fifth of the market, remain price sensitive and gravitate toward dehydrated powders. Diagnostic centers, fueled by anti-microbial resistance programs, widen agar and chromogenic media usage, sustaining mid-margin demand. The culture media market thus bifurcates: high-spec GMP liquids for commercial therapeutics, and cost-focused powders for research and testing.

By Preparation Automation: Closed Systems Dominate GMP Suites

Automated media lines controlled 55.23% revenue in 2025 and grow at 16.42% CAGR on the back of gene and cell therapy plants where a single contamination event can wipe out USD 50 million in product. Inline sensors verify pH and osmolality, while electronic batch records expedite audits. Manual prep persists in academia and low-tier biosimilar workshops, but mounting labor costs and regulatory scrutiny will accelerate migration, pushing automated skids deeper into the culture media market by decade’s end.

By Bioprocess Application: Cell and Gene Therapy Propel High-Growth Demand

Monoclonal antibodies still generate 42.23% of volume, yet cell and gene therapy surges at 17.82% CAGR as CAR-T approvals proliferate and allogeneic platforms seek scalable expansion media. These autologous processes demand xeno-free cytokines and enzymes that preserve phenotype while delivering clinical-grade sterility, granting premium pricing latitude.

Vaccine developers continue leveraging pandemic-era assets; oncology-focused mRNA candidates necessitate high-density HEK293 media, reinforcing predictable baseline consumption. Recombinant enzyme producers add steady, if slower, volumes that smooth supplier capacity utilization cycles across the broader culture media market.

Geography Analysis

North America led the culture media market with 38.23% share in 2025, concentrating large-scale biologics facilities and pioneering continuous bioprocessing adoption. The U.S. federal advanced-therapy initiatives and a robust venture capital ecosystem further insulate demand, anchoring multi-year supply contracts that favor established vendors. Canada contributes niche demand via regenerative-medicine clusters in Ontario and British Columbia, where provincial grants support early-stage stem-cell programs.

Europe maintains mature but steady growth, leveraging stringent EMA quality standards and a dense CDMO corridor stretching from Ireland through Germany to Switzerland. The region’s push toward green biomanufacturing also stimulates interest in media formulations with reduced carbon footprints, opening procurement pilots for plant-based hydrolysate alternatives. Government incentives for pandemic-preparedness keep mRNA vaccine capacity online, buttressing baseline liquid-media consumption.

Asia-Pacific advances at 15.42% CAGR—the fastest worldwide—driven by China’s self-reliance policies mandating domestic sourcing and India’s cost-competitive CDMO sector securing Western contract wins. South Korean majors, Samsung Biologics and Celltrion, expand perfusion suites, compounding nutrient-rich media requirements. Southeast Asian manufacturers, incentivized by halal certification opportunities, are emerging, while Australia’s Moderna plant cements Oceania’s relevance. The Middle East and Africa experience gradual adoption, tied to diversification programs in the Gulf Cooperation Council and rising pathogen-testing capabilities across North Africa. Latin America, led by Brazil, scales biosimilar capacity yet faces currency volatility that tempers purchasing cycles.

Regulatory Landscape

Regulatory requirements for biologics and advanced therapies are pushing culture media toward greater traceability and tighter control of animal- and human-derived materials. In April 2024, the US FDA issued draft CGT-focused CMC recommendations addressing the use and qualification of human and animal-derived materials in submissions, reinforcing expectations around sourcing transparency and risk control that cascade to media and ancillary-material suppliers.

In Europe, the EMA updated Q&A guidance in October 2024 around microbial control information for cell culture reagents under GMP, clarifying documentation expectations while keeping the underlying requirement for appropriate microbial purity. ISO 20399:2022 for ancillary materials in cell and gene therapy provides a structured risk-management framework that shapes supplier quality systems, including change notification agreements and qualitative composition disclosure needed for marketing authorization holders to maintain current regulatory dossiers.

Competitive Landscape

The culture media market shows moderate fragmentation: Thermo Fisher Scientific, Merck KGaA, Sartorius, Lonza, and Danaher’s Cytiva together command a significant but not overwhelming share, leaving regional players meaningful headroom. Incumbents fortify positions through vertical raw-material integration—Merck’s 2025 amino-acid acquisition in South Korea improves security of supply—and by embedding process-development teams within client sites to create switching costs.

Regional challengers such as HiMedia Laboratories, KOHJIN Bio, and PAN-Biotech undercut on price and delivery speed, especially where localized certifications—halal, kosher, ISO 13485—provide immediate tender advantages. Meanwhile, AI-driven formulation start-ups partner with CDMOs to compress media-optimization cycles from a year to a quarter, threatening to unseat legacy R&D timelines. Patent activity remains vigorous: Thermo Fisher surpasses 150 active filings related to chemically-defined components, while Sartorius’s Ambr upgrades secure digital twins that fine-tune nutrient feeds in perfusion reactors[3]U.S. Patent and Trademark Office, “Patent Database Search,” uspto.gov.

Automation capabilities now anchor competitive bids. Vendors bundling single-use mixers, inline analytics, and validated software sell holistic GMP solutions rather than commodity powders, enabling price premiums and multi-site lock-ins that crystallize long-term revenue. Niche prospects—organoid, halal, and continuous-perfusion media—offer greenfield expansion zones for agile entrants, assuring ongoing churn and dynamic pricing within the global culture media market.

Culture Media Industry Leaders

Merck KGaA (MilliporeSigma)

Sartorius AG

Thermo Fisher Scientific Inc.

Danaher Corp. (Cytiva)

Lonza Group Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

One opportunity is building more regionalized, GMP-grade inputs and distribution networks that reduce exposure to pharmaceutical-grade amino acid and recombinant component constraints. In Europe, Brenntag Pharma and Evonik REXIM signed a strategic distribution partnership for REXIM GMP-grade amino acids effective July 1, 2026, supporting raw-material availability for chemically-defined media and helping media manufacturers and biopharma buyers simplify qualification of key inputs.

Capacity additions and higher-value services around formulation are also moving beyond commodity powders toward liquid, ready-to-use formats and development support for regulated manufacturing. Cytiva completed an expansion at its Logan, Utah site in June 2026 that doubled liquid media production capacity, while Sartorius Stedim Biotech opened a 140 million euro competence center in Freiburg, Germany in May 2026 for quality-critical cell and gene therapy components such as cytokines and growth factors.

Recent Industry Developments

- June 2026: Cytiva completed an expansion of its Logan, Utah facility, increasing the footprint to more than 240,000 square feet and doubling its liquid cell culture media production capacity. The project, supported by BARDA, strengthens domestic supply resilience for high-volume GMP liquid media and supports customers scaling biologics and vaccine manufacturing.

- December 2025: Thermo Fisher Scientific expanded its Gibco Bacto portfolio with next-generation chemically-defined media aimed at improving E. coli biomanufacturing productivity. The launch supports process consistency and documentation needs for regulated production by reducing variability associated with complex or animal-derived inputs.

- July 2024: Merck announced an expansion move in China tied to cell culture media and related bioprocessing supply, reinforcing its local manufacturing and service footprint for biopharma customers. Greater in-region availability supports faster lead times and qualification cycles for GMP media and raw materials as domestic sourcing requirements grow in parts of Asia-Pacific.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the culture media market covers ready-to-use or prepared media and related formulations used to grow, maintain, and test microorganisms and cells in laboratory, clinical, and industrial settings, measured in value terms (USD).

Scope exclusions: We exclude laboratory instruments, incubators, and general lab consumables that do not form part of the culture media product itself.

Segmentation Overview

- By Media Type

- Chromogenic Culture Media

- Dehydrated Culture Media

- Prepared / Ready-to-use Culture Media

- By Formulation

- Serum-based Media

- Serum-free Media

- Chemically-defined Media

- Stem-cell Culture Media

- Specialty / Custom Media

- By Physical State

- Liquid Media

- Powdered Media

- Semi-solid / Gel Media

- By End User

- Pharmaceutical & Biotechnology Companies

- Contract Development & Manufacturing Organisations (CDMOs)

- Academic & Research Institutes

- Clinical & Diagnostic Laboratories

- Other End Users

- By Preparation Automation

- Manual Media Preparation

- Automated Media-Preparation Systems

- By Bioprocess Application

- Monoclonal Antibodies

- Vaccines (mRNA, viral-vector, sub-unit)

- Cell & Gene Therapy

- Recombinant Proteins & Enzymes

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with public datasets that help set the outer boundaries of demand and supply. We typically use source types such as the World Health Organization (WHO), the US CDC, and the US FDA for testing and clinical-use context, and we cross-check trade and production signals using UN Comtrade and national statistics portals.

To make the model practical, we also review peer reviewed journals for shifts in cell culture practices and media formulations, and we use company filings and investor presentations to understand revenue exposure by life science consumables. Patent databases and an import-export shipment-level database are used selectively to confirm activity in specialized media categories and validate country-level movement in key inputs. These sources are not exhaustive, and we also incorporate other public and paid references during the data collection, validation, and clarification stages.

Primary Interviews and Surveys

Primary work focuses on checking what is actually being purchased and used across biopharma production, clinical and diagnostic labs, and academic research, then reconciling that with what is visible in public data. We speak with manufacturers, distributors, and end users across major regions so assumptions like pricing, mix shift, and adoption of serum-free or chemically-defined media can be tested and adjusted.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 14% | APAC: 46% |

| Mid tier: 50% | Functional/Unit leaders: 36% | EMEA: 34% |

| Smaller Players: 14% | Managers: 50% | Americas: 20% |

Market-Sizing & Forecasting

Market sizing is built using a top-down and bottom-up approach. The top-down path reconstructs demand by linking lab testing intensity and bioprocess activity to culture media consumption, then mapping that spend using observed price bands and mix. Once the demand pool is shaped, we use selective bottom-up checks, such as rolling up sampled supplier revenues, distributor channel splits, and ASP multiplied by volume for key media formats.

Key inputs in the model include the production scale-up of biologics and vaccines, the expansion pace of cell and gene therapy pipelines, the penetration of serum-free and chemically-defined formulations, and the share shift toward prepared or ready-to-use media versus dehydrated formats. We also track the relative weight of end users such as pharma and biotech, CDMOs, and diagnostic labs, since their usage patterns and replenishment cycles differ. For forecasting, we run scenario analysis and then anchor it to expert consensus on capacity additions, testing volumes, and pricing progression, which helps keep growth assumptions realistic when country-level data points are thin. Where bottom-up checks are incomplete, the missing pieces are handled through conservative interpolation and then re-tested with interview feedback before the final totals are set.

Data Validation & Update Cycle

Validation is done through repeated cross-checks so the final market number does not depend on one dataset or one interview stream. Analysts compare outputs against independent signals such as trade movement, public manufacturing expansion announcements, and reported segment revenues, and then investigate any large variance before it is approved.

A second review step tests calculation logic, unit consistency, and currency treatment across countries, followed by targeted re-contact when a parameter moves outside the expected range. Reports are refreshed annually, and interim updates are triggered when material events occur that can change pricing, supply availability, or demand patterns. Before delivery, the model is re-run with the latest available inputs so clients receive a current view.

Mordor Intelligence's Culture Media Market Size Measured Against Other Published Estimates

Published market sizes for culture media often do not match because the boundaries are drawn differently and the time settings are not always the same. The biggest drivers tend to be what gets counted as culture media versus adjacent lab consumables, which end users are included, and whether the stated year is a base year, an estimate year, or a forecast start.

By tracking pricing bands and end-user mix shifts, and then checking them through interview re-contacts, Mordor Intelligence keeps the culture media estimate tied to defined media formats (prepared, dehydrated, and specialty formulations) instead of letting it expand into broader lab reagent baskets or narrow to cell-only definitions.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 7.77 B (2026) | |

| Industry Publisher A | USD 5.01 B (2024) | Uses an earlier base year and a slower growth arc, and the scope description appears broader in segmentation labels but lighter on validation of pricing progression and prepared versus dehydrated mix, which can pull the market size down when volumes are rising. |

| Global Publisher B | USD 9.60 B (2025) | Likely includes a wider laboratory culture set (microbial plus broader cell and tissue use) and applies a different starting point and price logic across applications, which can inflate the estimate if adjacent reagents and premium defined media are grouped together. |

The spread across the table mostly comes from year choice and scope edges, especially how prepared media, specialty formulations, and clinical use are treated. Our approach stays traceable because each major step is tied to a measurable driver such as bioprocess scale, lab testing intensity, and realistic ASP movement, and then rechecked before the final value is signed off.

Key Questions Answered in the Report

How large will global demand for culture media become by 2031?

The culture media market size is forecast to reach USD 15.05 billion by 2031 on a 14.12% CAGR from 2026-2031.

Which region is growing fastest in culture media consumption?

Asia-Pacific posts the quickest uptake at 15.42% CAGR, powered by Chinese self-sufficiency policies and India's CDMO build-out.

What formulation trend is most favored by regulators?

Chemically-defined, animal-component-free media are preferred because they provide full traceability and reduce adventitious-agent risk.

Why are automated preparation systems gaining share?

Closed-system automation curbs contamination, slashes technician hours, and provides electronic batch records that satisfy GMP audits.

Which application segment will see the sharpest increase in media usage?

Cell and gene therapy exhibits a 17.82% CAGR as CAR-T and allogeneic pipelines expand globally.

What raw-material issue is limiting near-term growth?

Price spikes and shortages in pharmaceutical-grade amino acids and recombinant proteins are squeezing supplier margins and delaying expansions.

Page last updated on: