Cell-free Protein Expression Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

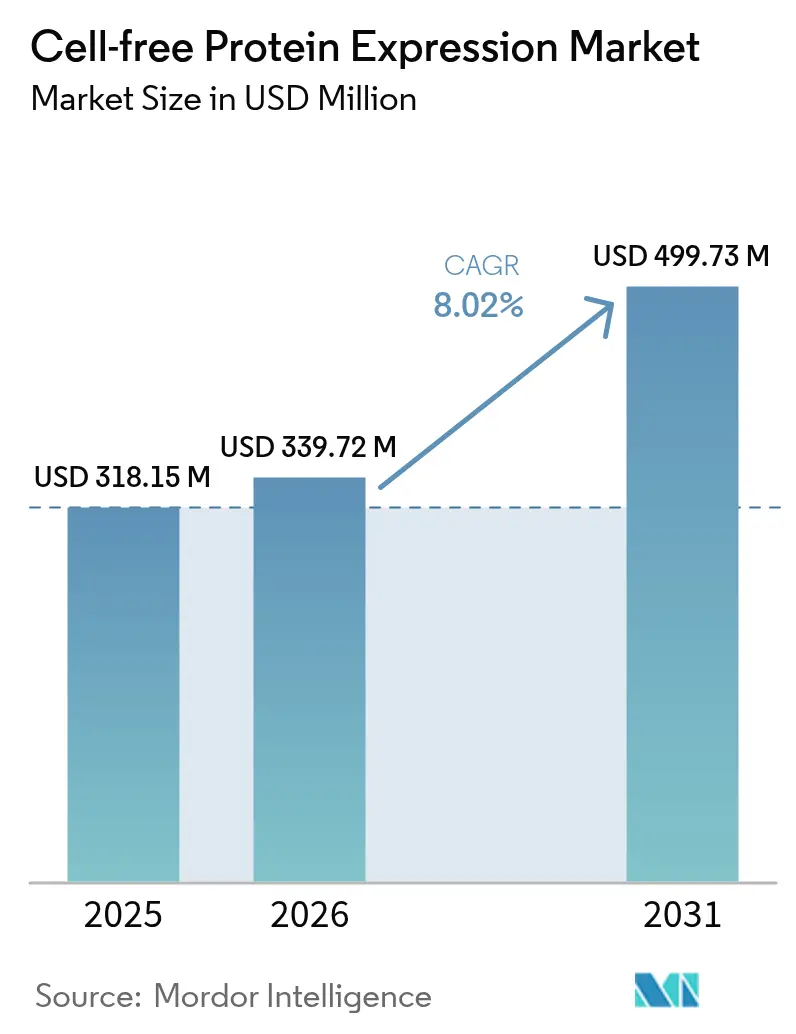

| Market Size (2026) | USD 339.72 Million |

| Market Size (2031) | USD 499.73 Million |

| Growth Rate (2026 - 2031) | 8.02% CAGR |

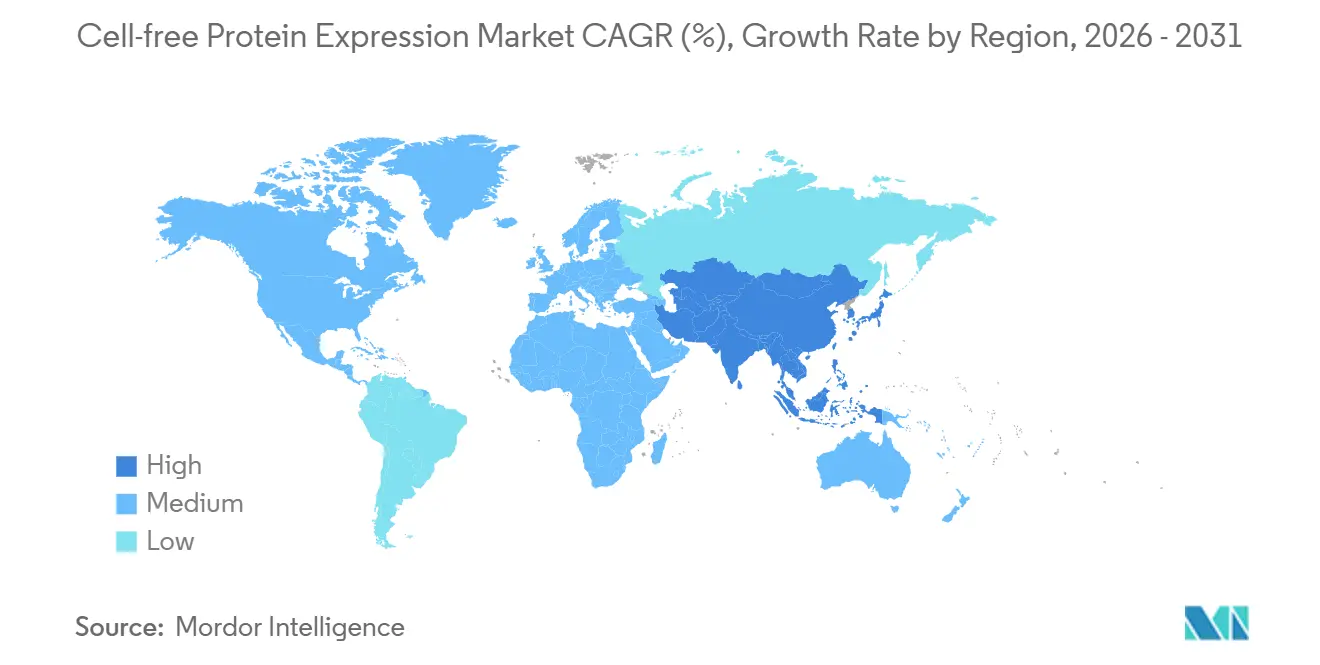

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cell-free Protein Expression Market Analysis by Mordor Intelligence

The Cell-free Protein Expression Market size is expected to increase from USD 318.15 million in 2025 to USD 339.72 million in 2026 and reach USD 499.73 million by 2031, growing at a CAGR of 8.02% over 2026-2031.

Funding for distributed biomanufacturing, especially in the United States and Japan, is reshaping procurement priorities toward portable kits that shorten design–build–test loops for synthetic-biology projects. Government preparedness mandates after pandemic-era supply shocks, together with new FDA guidance clarifying existing biologics rules for cell-free therapeutics, have reduced regulatory risk and attracted pharmaceutical investment.[1]U.S. Food and Drug Administration, “Chemistry, Manufacturing, and Controls Information for Biological Products,” fda.gov Continuous-exchange cell-free (CECF) systems are now scaling beyond multi-gram runs, allowing niche biologics to be produced economically without fermentation start-up delays.[2]Zachary A. Sun, “Continuous-Exchange Cell-Free Systems,” Nature Chemical Biology, nature.com At the same time, freeze-dried reaction kits remain the fastest-growing product type because they remove cold-chain dependence and enable point-of-care protein printing in remote settings.

Key Report Takeaways

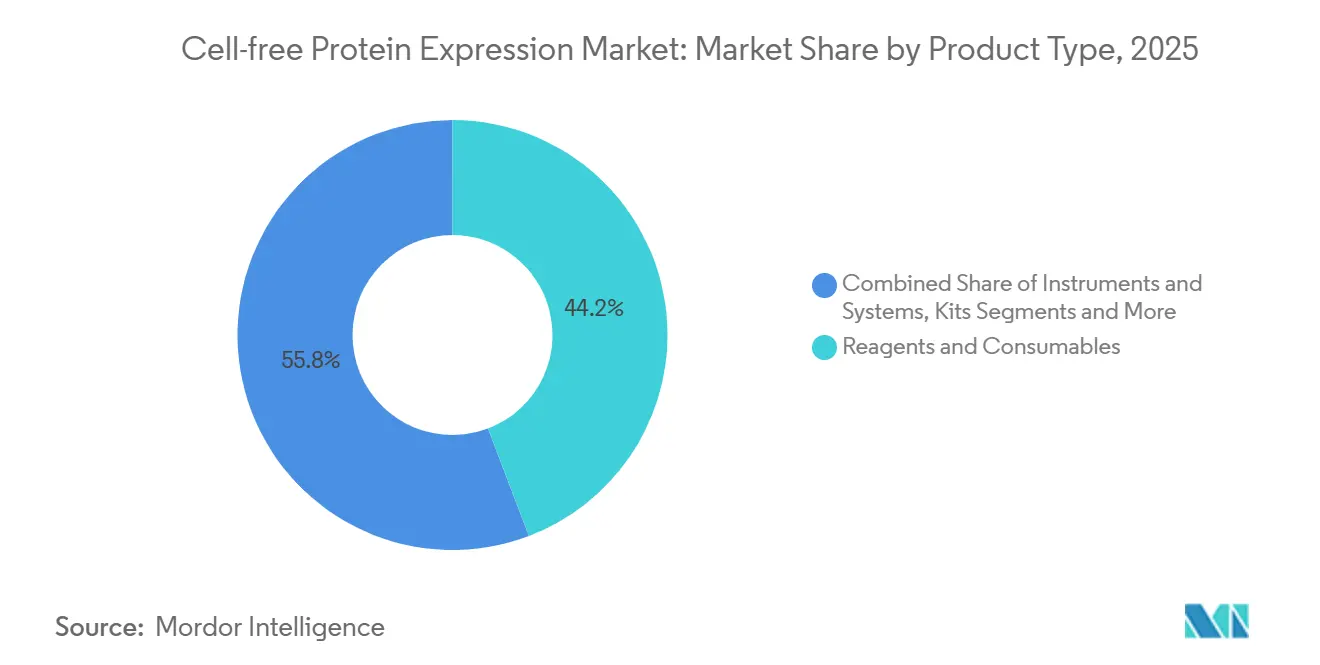

- Reagents and consumables led with 44.22% of cell-free protein expression market share in 2025, while kits are forecast to expand at an 11.52% CAGR through 2031.

- E. coli lysates commanded 51.75% share of the cell-free protein expression market size in 2025, yet insect-cell extracts are projected to post a 10.74% CAGR to 2031.

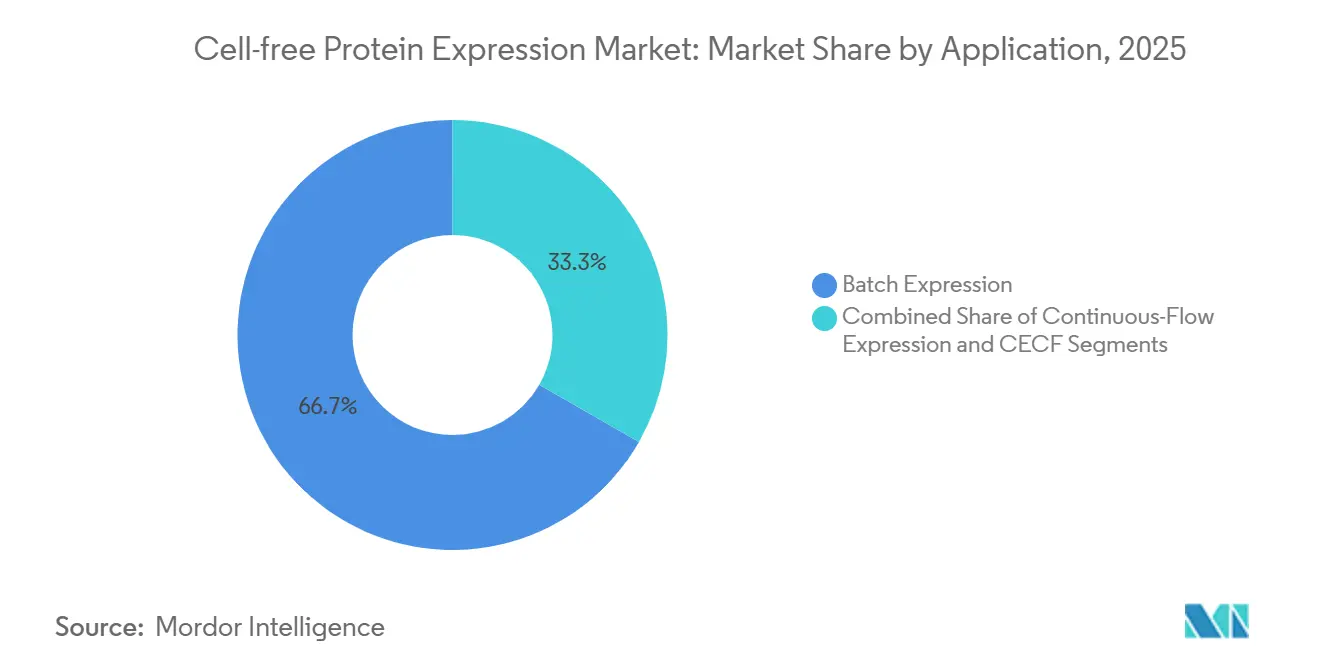

- Batch expression accounted for 66.72% revenue in 2025; CECF is the fastest-growing mode at 10.89% CAGR through 2031.

- Liquid formats held 78.21% of 2025 volume, but lyophilized variants are set to grow 11.48% CAGR, widening access to portable biomanufacturing.

- High-throughput production captured 29.73% share in 2025 and is projected to register an 11.39% CAGR between 2026 and 2031.

- Contract research organizations recorded the highest projected CAGR among end users at 10.24% over 2026-2031.

- North America led with 39.54% revenue in 2025, whereas Asia-Pacific is forecast to expand at 10.28% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cell-free Protein Expression Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Adoption for High-Throughput Protein Engineering & Synthetic Biology | +1.8% | Global, led by North America & Europe | Short term (≤ 2 years) |

| Rising Demand for Biologics & Personalized Therapeutics | +1.5% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Advantages Over Cell-Based Systems (Speed, Toxic Protein Handling) | +1.3% | Global | Short term (≤ 2 years) |

| Government On-Demand Biomanufacturing Preparedness Initiatives | +1.1% | North America, Europe | Medium term (2-4 years) |

| Freeze-Dried Kits Enabling Decentralized Protein Printing | +1.0% | Global, early adoption in North America & Asia-Pacific | Long term (≥ 4 years) |

| AI/ML-Driven Yield Optimization & Automation Integration | +0.9% | North America, Europe, China, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption for High-Throughput Protein Engineering & Synthetic Biology

Cell-free workflows collapse cloning, colony picking, and scale-up into a same-day process, letting researchers screen hundreds of variants in 96- or 384-well plates while living-cell systems would require weeks.[3]Christopher A. Voigt, “Design-Build-Test Cycles in Synthetic Biology,” Proceedings of the National Academy of Sciences, pnas.org DARPA’s USD 87 million BioMaDE awards in 2024 funded modular lysate platforms that prototype enzymes and biosensors for defense applications. Commercial kits bundling lysate and energy mixes standardize performance across labs and lower entry barriers. Seamless integration with Golden Gate and Gibson assembly now transforms a digital DNA design into functional protein inside 24 hours, fundamentally shortening discovery cycles in academia and start-ups.

Rising Demand for Biologics & Personalized Therapeutics

More than 3,800 biologics were in clinical development in 2025, creating urgency for flexible platforms that crank out patient-specific proteins within days. Cell-free systems meet turn-around targets for personalized cancer vaccines, something CHO cells cannot achieve at clinical scale. Sutro Biopharma’s XpressCF, built on E. coli lysates, advanced to Phase II trials in 2025, proving regulators will review cell-free-produced therapeutics when process controls comply with cGMP. FDA guidance in 2024 cemented that host-free manufacturing falls under existing biologic rules so long as analytical characterization is robust. Hospitals in low-resource regions now explore freeze-dried kits to print therapeutic enzymes on site, sidestepping cold-chain dependencies.

Advantages Over Cell-Based Systems (Speed, Toxic Protein Handling)

Membrane and toxic proteins that cripple living hosts express efficiently in open lysates, unlocking drug-target classes previously off-limits. Wheat-germ and insect-cell extracts replicate native lipid environments, enabling structural biologists to elucidate GPCR and ion-channel structures. Non-canonical amino acids can be inserted directly because no cell wall filters substrates, supporting site-specific conjugation strategies used in antibody–drug conjugates. Thermo Fisher’s PURExpress kit, which uses purified translation components, boosted yields 40% in 2025 by removing endogenous nucleases. Batch reactions deliver usable protein within four hours, and continuous-flow reactors sustain synthesis days longer, shrinking early discovery timelines.

Government On-Demand Biomanufacturing Preparedness Initiatives

The U.S. DoD awarded USD 23 million in 2024 to develop backpack-size reactors for field vaccine and antitoxin synthesis. NIST followed with standards to quantify lysate potency, a prerequisite for regulatory acceptance. Japan earmarked JPY 3.2 billion in 2025 to stand up regional hubs able to formulate influenza vaccines inside 72 hours. These projects create a captive market segment that values portability and shelf life more than cost per milligram, favoring freeze-dried kits over stainless-steel bioreactors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Reagent Costs & Scalability Challenges | −1.2% | Global | Short term (≤ 2 years) |

| Limited Post-Translational Modification Capability | −0.9% | Global, acute for mammalian therapeutics | Medium term (2-4 years) |

| Fragmented IP Landscape & Patent Thickets | −0.7% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Regulatory Pathway Uncertainty for Therapeutic Proteins | −0.6% | Global, most acute in emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Reagent Costs & Scalability Challenges

Energy cocktails, nucleotides, and lysate prep account for up to 70% of production cost, often topping USD 500 per milligram for mammalian extracts, dwarfing fermentation economics. Continuous-exchange reactors improve yields five-fold but still trail fed-batch titers by two orders of magnitude. Merck KGaA shaved 30% off reagent expense in 2024 with its ReadyToProcess CFPS line, yet management admits 10-liter scale remains uneconomical for mainstream antibodies. Absence of scale economies in lysate production confines adoption to high-value or time-critical proteins.

Limited Post-Translational Modification Capability

E. coli systems lack glycosylation enzymes, preventing authentic antibody Fc modifications that govern serum half-life. Insect-cell and mammalian extracts offer partial solutions but at yields 5-10x lower than prokaryotic counterparts. Hybrid approaches that bolt glycosyltransferases onto E. coli lysates can restore N-glycans yet add USD 150 per milligram extra cost. Disulfide-bond formation requires redox-balanced buffers that complicate automation, limiting throughput.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Kits Accelerate Democratization

Kits captured growing mindshare as lyophilized formats removed the cold-chain barrier and bundled protocols eliminated troubleshooting. Kits are on track to expand at an 11.52% CAGR between 2026 and 2031, outpacing reagents despite the latter’s 44.22% revenue lead in 2025. This trajectory illustrates how pre-optimized mixes shorten learning curves for small biotechs and academic labs. Instruments that automate pipetting and purification complement kit adoption, as seen with Nuclera’s eProtein platform rollout to 12 pharma labs in 2025. Reagents will remain indispensable for experienced users customizing buffer chemistries, yet kit convenience drives the incremental user base. Accessories and service bundles, including contract lysate prep, grow in tandem because newcomers often outsource complex targets.

By Expression System: Insect-Cell Momentum Builds

The cell-free protein expression market size for insect-cell lysates is expected to climb at 10.74% CAGR, nibbling share from E. coli’s 51.75% dominance in 2025. Demand for eukaryotic glycosylation propels hybrid and insect solutions for vaccine antigens and antibody fragments. Wheat-germ extracts sit in the middle ground, favored for membrane proteins that aggregate in bacteria. Start-ups such as LenioBio combine E. coli yield advantages with exogenous enzymes to approximate mammalian quality at lower cost. Rabbit reticulocyte and mammalian systems persist in niche roles where post-translational fidelity trumps cost.

By Expression Mode: CECF Unlocks Multi-Gram Runs

Batch systems still delivered 66.72% of 2025 revenue because they need only a heat block and microtube, making them the default for quick screens. Yet CECF platforms are forecast to post 10.89% CAGR as pharmaceutical users chase yields above 5 mg/mL, bridging the pre-clinical manufacturing gap. Sutro Biopharma’s CECF-based XpressCF produced antibody–drug conjugates now in Phase II trials, underscoring regulatory viability. Continuous-flow formats serve mid-range needs where extended runs are beneficial but dialysis hardware is acceptable.

By Reaction Format: Lyophilized Leads Portability Wave

Liquid lysates owned 78.21% share in 2025 because freezer capacity is ubiquitous in core labs. However, lyophilized variants are set to expand 11.48% CAGR, supplying defense agencies and rural clinics with shelf-stable “protein printers”. Microfluidic chips integrate synthesis and purification in credit-card footprints, targeting diagnostic OEMs that value automation more than cost per microgram. The cell-free protein expression market share of lyophilized kits will therefore widen as ambient shipping becomes standard for global distribution.

By Application: High-Throughput Workflows Surge

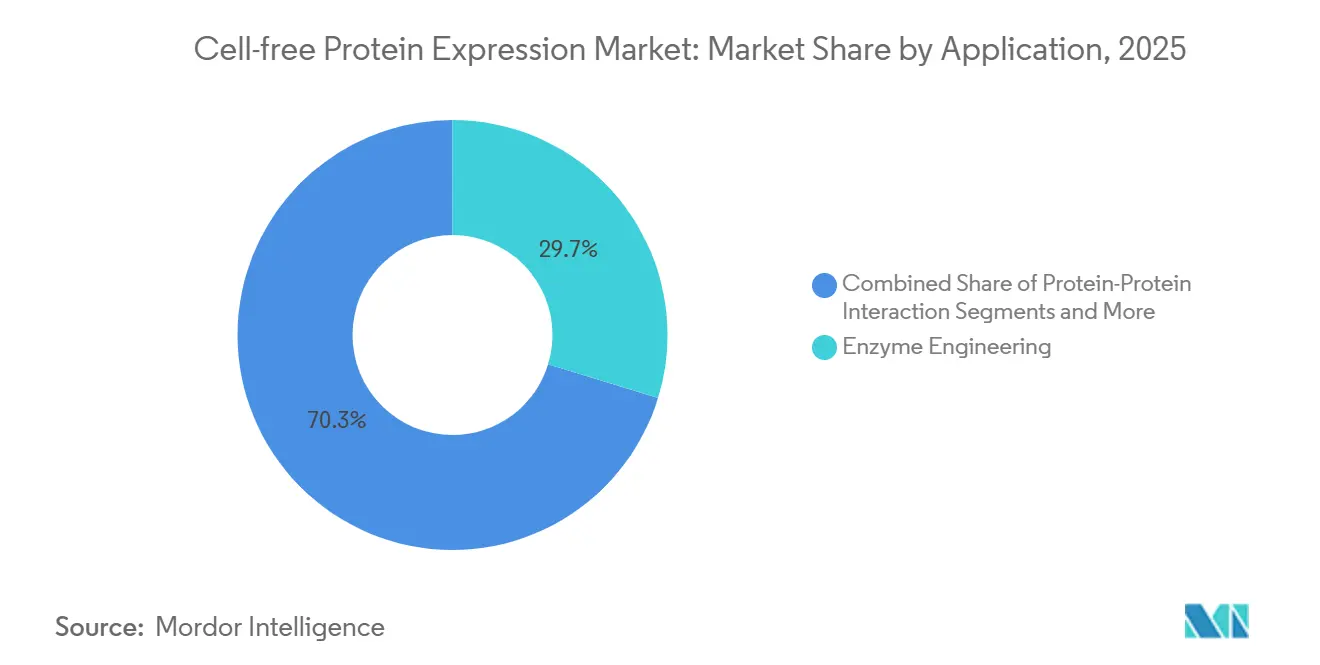

Enzyme engineering retained 29.73% of 2025 revenue, yet high-throughput production is projected to climb at 11.39% CAGR as robotics and AI converge for 96-protein overnight runs. Protein-protein interaction mapping and protein labeling also benefit from open lysate architecture that tolerates co-expression and non-canonical amino acids. Therapeutic protein output, though smaller today, gains legitimacy from clinical-stage programs like Sutro Biopharma, suggesting future expansion once regulatory precedents mature.

By End User: CRO Growth Outpaces In-House Efforts

Pharmaceutical and biotech firms generated 41.27% of 2025 turnover, yet CRO revenue is predicted to grow 10.24% CAGR as outsourcing becomes cheaper than maintaining fermenters for early screens. Academic labs adopt commercial kits thanks to NIH grants covering capital purchases. Diagnostic developers leverage cell-free speed to refresh antigen panels for multiplex tests without large-scale cultures. Other users, including ag-biotech firms, remain exploratory but recognize value where transgenic hosts are impractical.

Geography Analysis

North America commanded 39.54% of 2025 revenue, reflecting NIH and DoD spending on rapid-response platforms. The region also hosts leading kit suppliers and most FDA-regulated clinical programs. Europe follows, buoyed by Horizon Europe’s EUR 200 million grants that subsidize personalized-medicine pilots, particularly in Germany and the United Kingdom.

Asia-Pacific posts the fastest regional growth at 10.28% CAGR, underwritten by China’s RMB 1.2 billion stimulus for domestic lysate production and automation tools. Japan’s Osaka and Fukuoka hubs target 72-hour vaccine turnaround to bolster pandemic preparedness. India funds centers of excellence building low-cost kits for crop-protection enzymes and point-of-care diagnostics.

South America and the Middle East & Africa remain small today, though Brazil explores veterinary vaccines and South Africa pilots rural diagnostic antigen production. Adoption hinges on lowering kit prices and clarifying local biologics regulations.

Regulatory Landscape

Cell-free protein expression (CFPS) products are generally assessed under established biologics expectations for quality and control, with emphasis on Chemistry, Manufacturing, and Controls (CMC) for recombinant and other biotechnology-derived proteins rather than a dedicated CFPS-specific pathway. FDA guidance clarifying CMC information expectations for biological products, along with updated FDA CMC flexibilities (January 2026) for advanced modalities, keeps regulator focus on validated control strategies, analytical characterization, and documented process understanding that CFPS developers can map to open-lysate manufacturing.

In Europe, EMA scientific guidelines used in biotechnology-derived active substance submissions (including process validation and immunogenicity assessment guidance) shape expectations for comparability, impurity control, and lot consistency when CFPS is used for investigational or commercial supplies. Cross-cutting standards also feed into platform quality systems, including ISO 20399:2022 for ancillary materials used in production and ISO 24190:2023 for risk-based rapid microbial detection approaches, which align with CFPS' reagent-heavy profiles and the release-testing and traceability needs of decentralized, rapid-turnaround manufacturing.

Value Chain Analysis

The CFPS value chain starts with high-specification inputs, including enzymes and translation factors, nucleotides, amino acids, energy-regeneration substrates, and DNA templates. It then moves into extract or component production (E. coli, wheat germ, insect, mammalian, or purified systems), formulation into liquid or lyophilized reaction mixes, and packaging as standardized kits or configurable reagents. Platform owners and kit suppliers (for example, New England Biolabs and Promega) sell upstream to end users such as biopharma, CROs, academic institutes, and diagnostic developers, while a parallel branch supports scale-up services, including CDMO-style production for longer-run continuous or continuous-exchange cell-free (CECF) workflows.

Key bottlenecks remain extract consistency, the cost of energy and nucleotide cocktails, and the added complexity of achieving eukaryotic post-translational modifications (notably glycosylation) with acceptable yield. These constraints drive a split supply-chain model: portable, freeze-dried kits that prioritize shelf life and ease of use for decentralized settings, and more controlled reactor-based manufacturing where process monitoring, specialized hardware, and quality systems dominate cost. Recent academic advances in 2026 on modular reconstitution and optimized reagent formulations target upstream cost and reproducibility levers, with the goal of reducing dependency on proprietary inputs and shifting value toward standardized, automatable workflows.

Competitive Landscape

The market is moderately concentrated. Thermo Fisher Scientific differentiates with PURExpress kits that eliminate background nucleases, while Merck KGaA invests in large-scale CECF reactors for CDMO services. Promega extends shelf life via freeze-drying innovations, capturing military and field-diagnostics contracts. Takara Bio and New England Biolabs emphasize modularity, embedding AI into protocol designers and expanding non-canonical amino-acid compatibility.

Disruptors include Nuclera, which bundles hardware, consumables, and software in subscription form, shifting revenue to recurring reagents. LenioBio’s EcoProX hybrid lysate adds eukaryotic folding enzymes to E. coli background, cutting costs relative to mammalian extracts. Synthelis focuses on membrane proteins with insect-cell lysates, serving vaccine and structural-biology niches.

Patent thickets on energy-regeneration chemistries constrain new entrants, but first-generation patents started to lapse, enabling biosimilar lysates. Vendors that pair AI optimization with robotic execution stand to gain, as pharmaceutical clients favor turnkey platforms over commodity reagents.

Cell-free Protein Expression Industry Leaders

Thermo Fisher Scientific Inc.

Promega Corporation

Merck KGaA (Sigma-Aldrich)

Takara Bio Inc.

New England Biolabs

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A major whitespace sits at the intersection of AI-driven protein design and high-throughput expression, where cell-free platforms can provide rapid physical validation for sequences generated by computational pipelines. Sino Biologicals May 2026 launch of its XPressMAX Cell-Free Protein Synthesis Kit, positioned for AI-powered, high-throughput antibody drug discovery and reflected in public research narratives, shows active commercialization around rapid expression of antibody formats and miniproteins in short cycle times. This creates room for vendors that bundle cell-free reagents with automation, data capture, and assay-ready purification workflows, particularly for CROs and pharma groups running 96- to 384-well campaigns.

Another opportunity area is cost and scalability improvement that extends CFPS beyond screening into preclinical and niche manufacturing, supported by 2026 academic results on low-cost reagent formulations and modular assembly approaches that report reductions in preparation costs and improved yields at bench scale. In parallel, the government on-demand biomanufacturing initiatives cited in the market context (for example, US defense programs funding portable reactors and Japans 72-hour regional vaccine hub agenda) support demand for lyophilized, cold-chain-independent kits and standardized potency measurement. Buyers in these settings reward suppliers that can provide long-shelf-life formats, quality documentation, and lot-to-lot consistency for decentralized procurement.

Recent Industry Developments

- May 2026: Sino Biological launched the XPressMAX Cell-Free Protein Synthesis Kit positioned for AI-powered high-throughput antibody drug discovery, using an E. coli lysate system. The kit is marketed around rapid expression of antibody-derived formats and other complex binders within hours, reinforcing the role of CFPS as a fast experimental layer between in silico design and downstream development.

- September 2025: LenioBio partnered with AffinityAI to connect AI-guided protein design workflows with its ALiCE cell-free expression platform. The collaboration links sequence generation with rapid expression and screening, tightening iteration loops for antibody and complex-protein discovery programs.

- October 2024: LenioBio collaborated with ReciBioPharm to establish 10-liter scale ALiCE protein production capability at a facility in Oeiras, Portugal, targeting vaccine-relevant proteins. The expansion increases CFPS availability beyond benchtop research use toward scalable production runs and strengthens the supply-side infrastructure for higher-volume applications.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenues generated from cell-free protein expression systems and related consumables and services used to produce proteins in vitro using cell extracts, without growing living cells, across research and commercial workflows.

Scope exclusions: It excludes conventional in vivo protein expression, upstream cell culture media and bioreactors used for live cells, and downstream purification equipment when sold as standalone products.

Segmentation Overview

- By Product Type

- Kits

- Reagents & Consumables

- Instruments and Systems

- Accessories & Services

- By Expression System

- E. coli

- Wheat Germ

- Rabbit Reticulocyte

- Insect Cell

- Mammalian

- Hybrid / Others

- By Expression Mode

- Batch Expression

- Continuous-Flow Expression

- Continuous-Exchange Cell-Free (CECF)

- By Reaction Format

- Liquid (Fresh Lysate)

- Lyophilized (Freeze-Dried)

- Microfluidic / Chip-Based

- By Application

- Enzyme Engineering

- Protein-Protein Interaction

- Protein Labelling

- High-Throughput Production

- Therapeutic Protein Production

- Others

- By End User

- Pharmaceutical & Biotechnology Companies

- Academic & Research Institutes

- Contract Research Organisations (CROs)

- Diagnostic Developers

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with building a clear view of what is sold in cell-free protein expression and who buys it, since product labeling varies across suppliers. We used public sources such as the US FDA databases for biologics activity signals, the NIH and NSF funding databases for research intensity, and the World Intellectual Property Organization for patent filing patterns around lysates, enzymes, and kits.

To anchor market direction, we also reviewed sources such as OECD science indicators, UN Comtrade trade statistics for lab reagents and instruments as a proxy check, and peer-reviewed journals that discuss yields, throughput, and format shifts, including lyophilized and microfluidic formats. Company annual reports, investor decks, and reputable press releases helped confirm portfolio scope and regional focus, and selective paid subscriptions supported company financials and patent landscaping where public data was thin. These desk research inputs are illustrative, and other public sources were used for cross-checking and clarification as needed.

Primary Interviews and Surveys

Primary discussions were used to confirm which products are typically counted as cell-free expression revenue, and how purchasing behavior differs between pharma and biotech users, academics, and outsourced research groups. We spoke with manufacturers, distributors, and end users across major regions so assumptions such as price ranges, replacement cycles, and adoption drivers could be checked and adjusted before finalizing totals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 17% | APAC: 47% |

| Mid tier: 45% | Functional/Unit leaders: 25% | EMEA: 34% |

| Smaller Players: 22% | Managers: 58% | Americas: 19% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where the demand pool was reconstructed from life science R and D activity, protein engineering workload signals, and the practical substitution of cell-based expression in time-sensitive workflows. After that demand picture was formed, we validated it using selective bottom-up approximations such as sampled average selling prices for kits and reagents multiplied by inferred run volumes, plus channel checks on system placements and usage rates.

Key inputs that shaped the model included funding intensity for synthetic biology and protein research, patent activity around lysate systems, observed shifts toward high-throughput screening, the mix of reaction formats (liquid versus lyophilized), and the adoption curve of continuous-exchange and continuous-flow modes. For forecasts, scenario analysis was used around adoption and pricing, then smoothed with trend-based time series checks so short-term spikes did not distort the forward view. Where supplier disclosures were incomplete, gaps were handled by using peer averages by product category and then re-tested with interview feedback until the totals remained realistic across regions.

Data Validation & Update Cycle

Outputs were checked against independent signals such as research funding direction, patent momentum, and reported lab workflow shifts, then the model was reviewed for outliers at the category and regional levels. When a major variance appeared, assumptions were revisited and follow-up questions were sent to relevant experts so the source of the difference was clearly understood.

Before sign-off, at least one additional analyst review was completed to ensure the math, units, and scope were consistent throughout the model. The report is refreshed annually, and interim updates are done when material events occur, including large product launches, regulatory changes affecting biotech research, or clear pricing resets. Right before delivery, a fresh data pass is completed so clients receive the most current view available at that time.

Mordor Intelligence's Cell Free Protein Expression Market Size Compared Against Other Published Estimates

Published market numbers for cell-free protein expression often do not match because the scope is not always consistent, and the timing of the base year can shift the reported value. Differences also come from how studies treat services versus product-only revenue and whether adjacent protein expression tools are blended in.

The table shows a spread mainly driven by what is counted as cell-free expression revenue and which year is used as the anchor. In Mordor Intelligence's model, the total reflects a broad in-scope basket that includes kits, reagents and consumables, instruments and systems, and accessories and services, which can lift the number versus product-only views, while it stays focused on in vitro expression rather than folding in wider protein expression toolchains.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 339.72 M (2026) | |

| Industry Publisher A | USD 283.50 M (2024) | Uses an earlier base year and may apply a narrower revenue lens that leans more toward systems and core reagents, which can understate newer service and accessory spending as adoption expands. |

| Industry Publisher B | USD 288.90 M (2024) | Anchors the estimate to 2024 with a different forecast window, and the definition emphasizes rapid protein synthesis workflows, which can lead to different inclusion rules for accessories and service revenues. |

Looking across the three figures, most of the difference is explained by year selection and the exact revenue basket included under cell-free expression. When the scope is kept explicit and the assumptions are tested against adoption, pricing, and workflow signals, the resulting market value becomes easier to trace and repeat for updates.

Key Questions Answered in the Report

How large will the cell-free protein expression market be by 2031?

It is forecast to reach USD 499.73 million, rising from USD 339.72 million in 2026 at an 8.02% CAGR.

Which product type is growing fastest?

Lyophilized and other kit-based offerings, projected at 11.52% CAGR through 2031.

Why are insect-cell lysates gaining popularity?

They supply eukaryotic post-translational modifications absent in E. coli systems, meeting vaccine and antibody requirements.

What limits wider adoption today?

High reagent costs and incomplete post-translational modification capability slow large-scale manufacturing uptake.

Which region will see the quickest growth?

Asia-Pacific is forecast to expand at 10.28% CAGR thanks to sizable public funding in China, Japan, and India.

Page last updated on: