Electronic Skin Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 13.40 Billion |

| Market Size (2030) | USD 37.10 Billion |

| Growth Rate (2025 - 2030) | 23.60% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electronic Skin Market Analysis by Mordor Intelligence

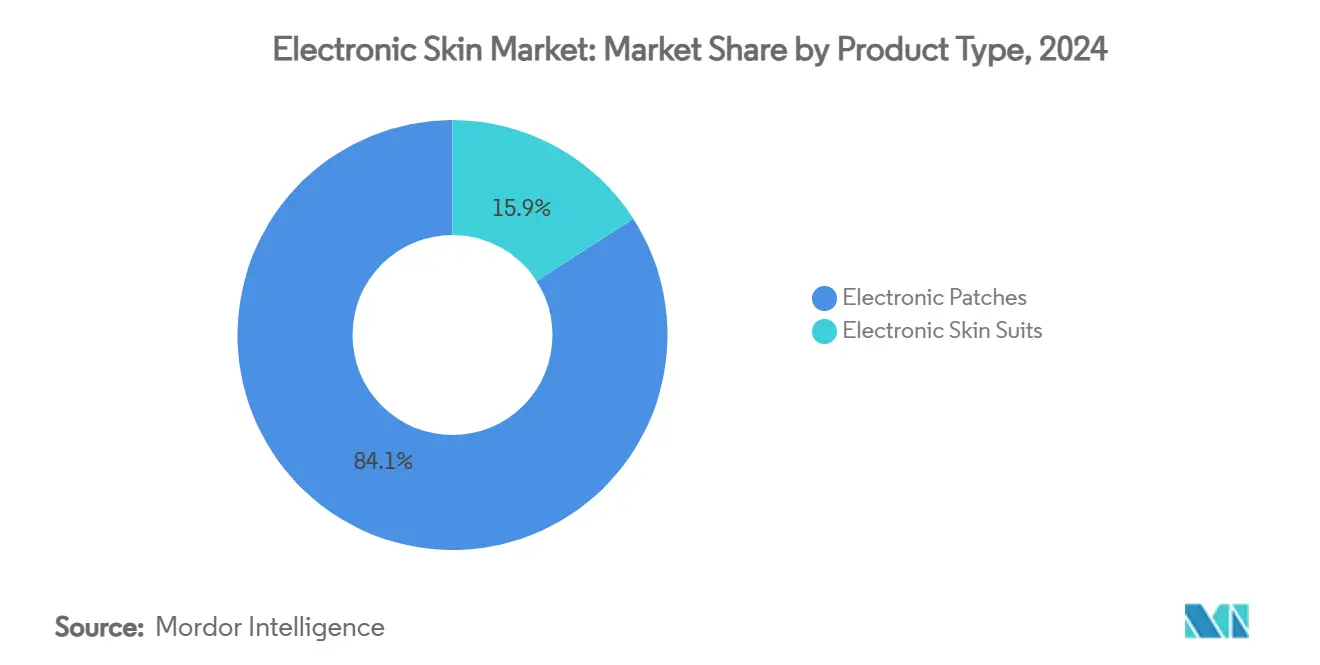

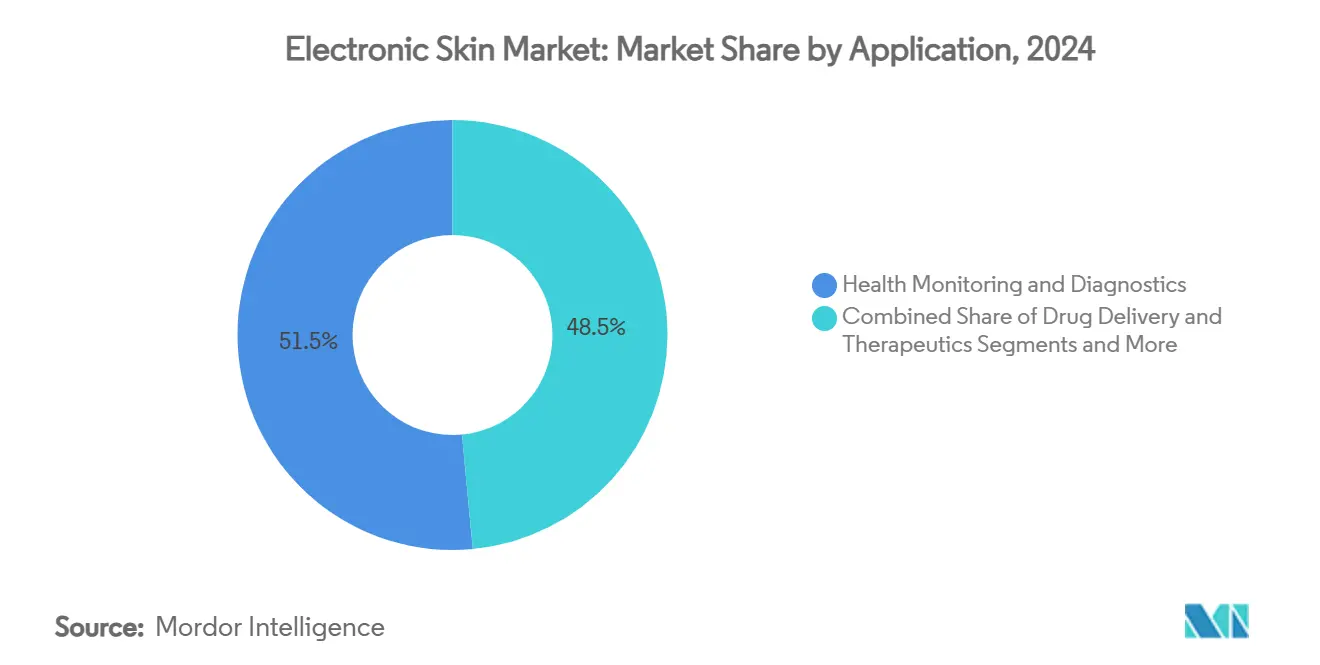

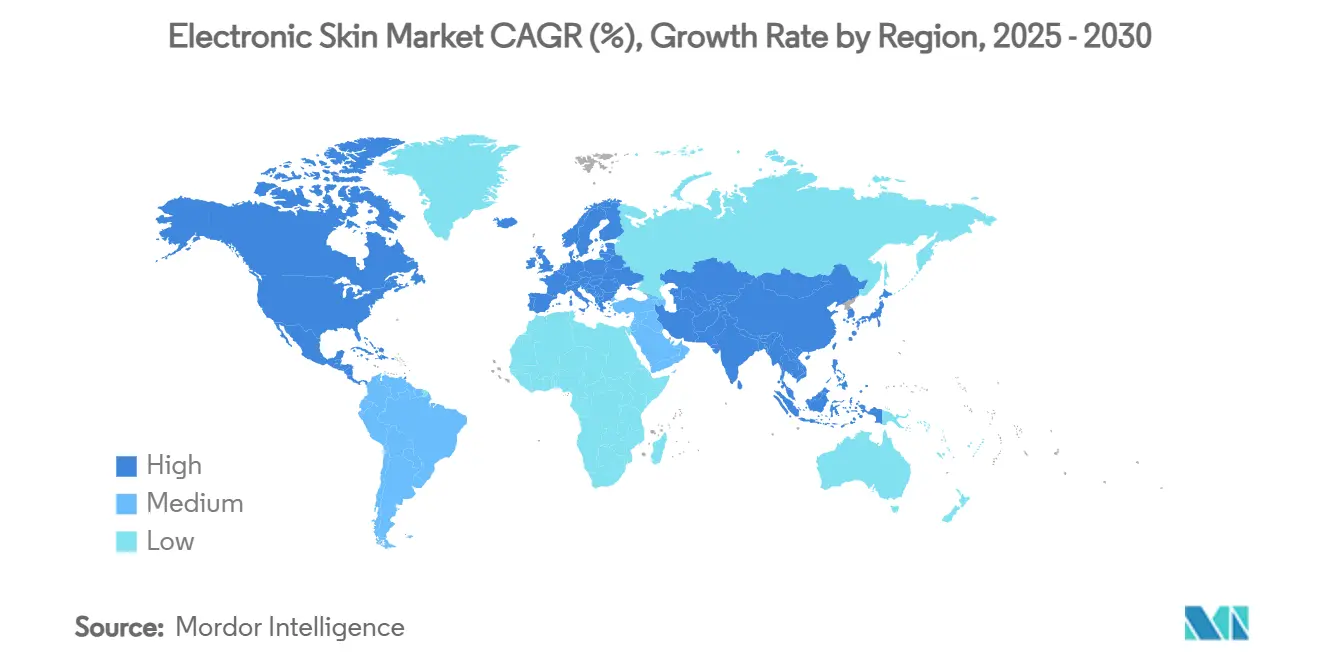

The electronic skin market reached USD 13.4 billion in 2025 and is forecast to attain USD 37.1 billion by 2030, reflecting a 23.6% CAGR. This expansion stems from the convergence of advanced materials science, 5G connectivity, and edge-AI processing that transforms how bioelectronic wearables interface with human physiology. Demand escalates as remote patient-monitoring programs become embedded in value-based care, while self-healing polymers lengthen device lifespans and falling prices of stretchable conductive inks accelerate mass commercialization. North America retains a 43.4% 2024 revenue lead, yet Asia Pacific’s 23.4% CAGR to 2030 signals a geographic pivot toward semiconductor-driven manufacturing hubs. Electronic patches command 84.1% 2024 revenue owing to clinical acceptance, whereas electronic skin suits grow fastest at 22.7% CAGR on defense and sports funding. Stretchable circuits deliver the core functionality with 46.2% share, but photovoltaic subsystems rise at 26.2% CAGR, underscoring the drive for energy-autonomous operation.

Key Report Takeaways

- By product type, electronic patches held 84.1% of the electronic skin market share in 2024; electronic skin suits expand at 22.7% CAGR through 2030.

- By application, healthcare monitoring captured a 51.5% share of the electronic skin market in 2024, while drug-delivery therapeutics grew at a 5.8% CAGR.

- By component, stretchable circuits led with 46.2% revenue share in 2024; photovoltaic systems post the highest 26.2% CAGR to 2030.

- By geography, North America accounted for 43.4% revenue in 2024, whereas Asia Pacific is projected to advance at a 23.4% CAGR.

Global Electronic Skin Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Proliferation Of Remote Patient-Monitoring Programs | +4.20% | Global, with early adoption in North America & EU | Medium term (2-4 years) |

| Integration Of 5G & Edge-AI Enabling Cloud-Connected E-Skins | +3.80% | APAC core, spill-over to North America | Long term (≥ 4 years) |

| Declining Cost Of Stretchable Conductive Inks & Substrates | +3.10% | Global, manufacturing concentrated in APAC | Short term (≤ 2 years) |

| Regulatory Fast-Track Pathways For Digital-Therapeutic Patches | +2.70% | North America & EU regulatory jurisdictions | Medium term (2-4 years) |

| Emergence Of Self-Healing Polymer Platforms Prolonging Device Life | +2.40% | Global, R&D concentrated in North America | Long term (≥ 4 years) |

| Defense Funding For Tactile Sensing Suits In Soldier Programs | +1.90% | North America, with expansion to allied nations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Proliferation of Remote Patient-Monitoring Programs

Healthcare providers integrate electronic skin into chronic-disease protocols for glucose, cardiac, and wound assessments. The FDA’s Digital Health Center of Excellence reduced Class II approval times from 18 to 8 months, accelerating commercialization.[1]U.S. Food & Drug Administration, “Digital Health Center of Excellence,” fda.gov Reimbursement frameworks now cover continuous monitoring for diabetes and cardiac care, creating sustainable revenue streams. Value-based payment models incentivize predictive monitoring that identifies physiological shifts before symptoms emerge. As a result, hospitals adopt electronic skin to cut readmissions and improve outcomes across large patient cohorts.

Integration of 5G & Edge-AI Enabling Cloud-Connected E-Skins

5G networks combined with embedded AI lower response times to 110 milliseconds while cutting data-corruption rates to 0.07% in clinical tests.[2]S. Kim et al., “Edge-AI in 5G Wearable Devices,” arxiv.org On-device analytics detect muscle fatigue and cardiac anomalies without constant cloud access, mitigating privacy risks. Telemedicine platforms benefit from real-time alerts that streamline clinician workflows. APAC telecom operators pilot nationwide low-latency coverage, positioning regional manufacturers for export growth. Longer term, multi-access edge computing will enable population-scale remote diagnostics with seamless software updates.

Declining Cost of Stretchable Conductive Inks & Substrates

Silver-nanowire and graphene ink prices have fallen 35% since 2024 as high-throughput gravure and screen printing gain traction.[3]L. Li, “High-Throughput Printing of Conductive Inks,” sciencedirect.com Material recyclability further lowers the total cost of ownership, with recovered nanowire networks retaining performance across multiple cycles. Affordable substrate polymers expand consumer use cases into sports and cosmetics. Manufacturers leverage APAC supply-chain efficiencies to scale output, narrowing the price gap with conventional wearables and broadening market penetration.

Regulatory Fast-Track Pathways for Digital-Therapeutic Patches

The FDA’s Software Precertification Pilot simplifies compliance for electronic skin-enabled therapeutics, with more than 20 devices cleared for indications from chronic pain to psychiatric disorders. Streamlined cybersecurity and data-integrity requirements reduce time-to-market for software-driven treatments. Successful precedents such as the N-SWEAT patch foster investor confidence and accelerate R&D expenditure. The pathway also harmonizes with EU MDR provisions, supporting transatlantic product launches.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex Multi-Material Manufacturing Raises Yield Losses | -2.80% | Global, particularly affecting APAC manufacturing hubs | Short term (≤ 2 years) |

| Limited Skin-Adhesion Duration Causing Device Failure | -2.10% | Global, with higher impact in humid climates | Medium term (2-4 years) |

| Data-Privacy Concerns Over Continuous Biometric Streaming | -1.90% | North America & EU regulatory jurisdictions | Medium term (2-4 years) |

| Recycling & End-Of-Life Challenges Of Biocomposite Films | -1.40% | Global, with stricter enforcement in EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Complex Multi-Material Manufacturing Raises Yield Losses

Current fabrication combines stretchable circuits, photovoltaic cells, and sensor layers, driving yield losses of 15–25%. High-precision alignment demands clean-room investment that inflates capital costs. Yield variability hits profitability, especially for APAC contract manufacturers operating at thin margins. Process-control advances, including in-line optical inspection and AI-driven defect analytics, aim to curb scrap rates but require additional upfront spending. Until yield stabilizes, scaling remains a bottleneck for high-volume orders.

Limited Skin-Adhesion Duration Causing Device Failure

Current adhesives support 7–14 day wear before signal drift or detachment occurs. Perspiration and motion degrade bonding, limiting suitability for chronic monitoring. Perforated designs modeled on sweat pores improve breathability yet increase production complexity. Biocompatibility standards further constrain adhesive formulations, delaying rollouts in humid markets such as Southeast Asia. Material scientists are exploring hydrogel-mesh hybrids to extend wear time without skin irritation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Patches Dominate, Suits Gain Momentum

Electronic patches accounted for 84.1% revenue in 2024, reflecting broad clinical validation and straightforward integration with telehealth platforms. This maturity anchors the electronic skin market, allowing healthcare providers to monitor glucose, cardiac rhythms, and wound healing with minimal patient training. Demand remains strong in hospital-to-home care transitions where reimbursement frameworks reward continuous data flow. Pharmaceutical partnerships embed patches in clinical trials to track therapeutic efficacy, reinforcing entrenched adoption.

Electronic skin suits, though smaller, register a 22.7% CAGR to 2030, illustrating rapid evolution from research prototypes to defense-grade products. Military funding fuels breakthroughs in strain-resistant wiring, while sports science labs adopt suits for real-time biomechanics assessment. Commercial versions target rehabilitation therapy by mapping pressure distribution to optimize gait training. Manufacturing learning curves cut material waste, narrowing price differentials with traditional compression garments. Cross-sector interest positions suit as the next growth engine once costs drop below USD 1,000 per unit.

By Component: Circuits Lead, Photovoltaics Accelerate

Stretchable circuits secured 46.2% of 2024 revenue, underpinning every device class through conductive networks that endure 600% elongation without signal loss. Their dominance stems from advancements in silver-nanowire meshes and carbon-nanotube composites that maintain sub-1 Ω cm resistivity under repeated deformation. Supply-chain integration with printed-electronics foundries keeps production scalable, supporting aggressive unit-cost targets.

Photovoltaic modules post the swiftest 26.2% CAGR as the sector shifts toward energy-autonomous platforms. Recent organic solar films reach 16% power-conversion efficiency at 200 µm thickness. Eliminating coin-cell batteries extends wear time and simplifies medical approvals that otherwise mandate battery-fire testing. Hybrid designs pair solar harvesters with ultrathin supercapacitors, ensuring peak-power delivery during sensor bursts. Parts standardization encourages OEMs to bundle power and sensing in modular kits for rapid product iteration.

By Application: Healthcare Dominates, Therapeutics Emerge

Health-monitoring applications commanded 51.5% revenue in 2024, cementing their role at the core of electronic skin adoption. Hospitals deploy patches for post-operative vital-sign tracking, while insurers subsidize devices for chronic-disease management to curb readmissions. Clinical data sets amassed from continuous monitoring feed predictive models that enhance triage decision-making and population health stratification.

Therapeutic drug-delivery, advancing at 5.8% CAGR, leverages electro-responsive membranes to release precise drug doses within 30 seconds of command signals. Oncology trials explore electronic skin for chemotherapy micro-infusion to reduce systemic toxicity. Venture investment accelerates development of pain-relief patches dispensing non-opioid analgesics on demand. The segment benefits from patient preference for needle-free treatments and regulatory clarity following early FDA clearances.

By Sensor Type: Tactile Sensors Prevail, Chemical Sensors Rise

Tactile sensors held 39.7% 2024 revenue by delivering sub-kPa pressure sensitivity critical for prosthetics and robotic manipulation. Micropyramid elastomer stacks generate amplified piezoresistive output, surpassing human fingertip acuity. Automotive supply chains examine tactile skins for adaptive interiors that adjust ergonomics by sensing occupant posture changes.

Chemical sensors are growing at a 25.1% CAGR as sweat-based glucose monitoring proves viable for diabetes management. Laser-engraved graphene electrodes detect lactate, cortisol, and electrolytes, enabling holistic fitness insights. Integrating multiplexed chemical arrays with electrophysiological sensors yields comprehensive health dashboards on a single patch. Market feedback favors single-unit solutions that minimize attachment points, streamlining user experience, and reducing medical waste.

Geography Analysis

North America delivered 43.4% 2024 revenue as early regulatory pathways and payer reimbursement catalyzed adoption. Silicon Valley and Boston ecosystems host start-ups that partner with hospital networks to run large-scale pilots. Tech majors, including Apple and Google, invest in non-invasive glucose monitoring that leverages electronic skin modalities, while Samsung pursues optical blood-sugar sensing for consumer devices. Federal research grants sustain foundational material science, fostering a virtuous cycle of academic-industry collaboration.

Asia Pacific leads growth with a 23.4% CAGR through 2030, driven by semiconductor mastery and cost-efficient manufacturing. China scales roll-to-roll electronics lines that reduce per-unit costs by 28%, propelling domestic brands into price-sensitive ASEAN markets. Japan’s industrial conglomerates develop self-healing substrates that withstand humid tropical climates, enhancing device longevity. South Korea leverages foundry capacity to co-fabricate microcontrollers and flexible interconnects, solidifying regional supply resilience.

Europe balances stringent privacy regulations with strong public funding, nurturing research on biodegradable polymers that support circular economy mandates. Government-sponsored pilots integrate electronic skin into national health systems, validating longitudinal benefits for elder care management. Manufacturing clusters in Germany and the Netherlands adopt closed-loop recycling protocols, aiming for EU recyclability targets. High clinical-quality standards build trust among global buyers, reinforcing the region as a benchmark for safety and sustainability.

Competitive Landscape

The electronic skin market remains moderately fragmented, yet consolidation looms as vertical integration becomes vital. Abbott Laboratories and Medtronic leverage long-standing clinician relationships to bundle electronic skin with chronic-disease programs, shortening sales cycles. Samsung and Apple integrate flexible sensors into consumer wearables that sync with broader health ecosystems, positioning hardware as data gateways for subscription services.

Start-ups such as MC10 and VivaLNK focus on platform modularity, licensing reference designs to OEMs that lack in-house flexible-electronics expertise. Patent filings concentrate on self-healing polymers and energy harvesting, signaling future differentiation through durability and autonomy. Component suppliers forge joint ventures with contract manufacturers to secure capacity for conductive-ink deposition, reflecting a race to control upstream bottlenecks.

Strategic partnerships shape go-to-market execution: sensor developers team with adhesives specialists to solve wear-duration challenges, while cloud analytics firms integrate data workflows into electronic health records. Market entry barriers rise due to escalating cybersecurity certification costs, favoring players with dedicated compliance teams.

Electronic Skin Industry Leaders

Abbott Laboratories

Medtronic plc

Koninklijke Philips NV

MC10 Inc.

VivaLNK Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: The Technical University of Denmark introduced a graphene-polymer electronic material that can stretch sixfold while maintaining conductivity. This material is suited for soft robotics and health monitoring.

- April 2025: MIT engineers created 10-nm-thick electronic skin membranes with thermal sensitivity for lightweight night-vision devices.

- March 2025: Helmholtz-Zentrum Dresden-Rossendorf produced magnetoreceptive electronic skin enabling touchless control in VR and underwater settings.

- February 2025: Terasaki Institute for Biomedical Innovation unveiled a self-healing electronic skin that repairs within 10 seconds and retains 80% functionality over 50 cut-and-heal cycles.

Global Electronic Skin Market Report Scope

| Electronic Patches |

| Electronic Skin Suits |

| Stretchable Circuits |

| Photovoltaics Systems |

| Stretchable Conductors |

| Electroactive Polymers |

| Health Monitoring & Diagnostics |

| Drug Delivery & Therapeutics |

| Cosmetic & Personal-Care |

| Others |

| Tactile Sensors |

| Chemical Sensors |

| Electrophysiological Sensors |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Electronic Patches | |

| Electronic Skin Suits | ||

| By Component | Stretchable Circuits | |

| Photovoltaics Systems | ||

| Stretchable Conductors | ||

| Electroactive Polymers | ||

| By Application | Health Monitoring & Diagnostics | |

| Drug Delivery & Therapeutics | ||

| Cosmetic & Personal-Care | ||

| Others | ||

| By Sensor Type | Tactile Sensors | |

| Chemical Sensors | ||

| Electrophysiological Sensors | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the electronic skin market?

The electronic skin market stands at USD 13.4 billion in 2025 and is projected to reach USD 37.1 billion by 2030 at a 23.6% CAGR.

Which product segment leads the electronic skin market?

Electronic patches dominate with 84.1% 2024 revenue due to clinical acceptance in chronic monitoring.

Which component shows the fastest growth?

Photovoltaic subsystems grow at a 26.2% CAGR as manufacturers pursue energy-autonomous electronic skin platforms.

Why is Asia Pacific the fastest-growing region?

Asia Pacific posts a 23.4% CAGR through 2030 because of semiconductor manufacturing hubs, cost-effective production, and supportive digital-health policies.

What major barrier limits wider adoption?

Complex multi-material manufacturing drives 15–25% yield loss, elevating costs and constraining high-volume scalability.

How does self-healing technology benefit electronic skin?

Self-healing polymers restore up to 80% functionality within seconds after damage, reducing maintenance and extending device service life for medical and defense use cases.

Page last updated on: