Server Operating System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

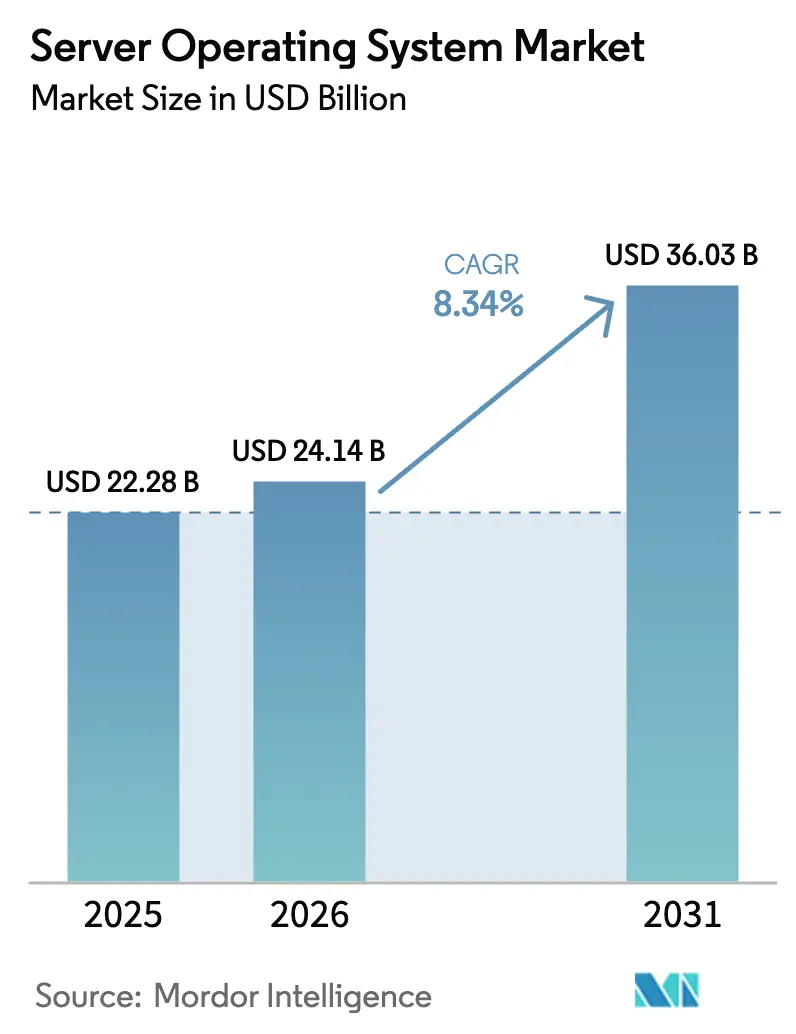

| Market Size (2026) | USD 24.14 Billion |

| Market Size (2031) | USD 36.03 Billion |

| Growth Rate (2026 - 2031) | 8.34% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Server Operating System Market Analysis by Mordor Intelligence

Server Operating System Market size market size in 2026 is estimated at USD 24.14 billion, growing from 2025 value of USD 22.28 billion with 2031 projections showing USD 36.03 billion, growing at 8.34% CAGR over 2026-2031. Demand growth reflects enterprise-wide digital transformation, widespread cloud-first refresh cycles, and artificial intelligence workloads that need purpose-built operating system features. [1]Microsoft Corporation, “Microsoft 2024 Annual Report,” microsoft.com Vendor road maps emphasize hybrid management, container orchestration, and energy-aware scheduling, while buyer priorities center on lower total cost of ownership, hot-patch security, and license model flexibility. Hyperscale data-center expansion, edge build-outs tied to 5G, and cyber-insurance requirements are reinforcing the strategic value of future-ready server platforms. Competition is intensifying as commercial Linux distributions, Windows Server, and emerging ARM-optimized releases vie to shape the next phase of the server operating system market.

Key Report Takeaways

- By deployment mode, cloud installations captured 63.60% revenue in 2025, while hybrid environments expand the quickest at a 10.22% CAGR through 2031.

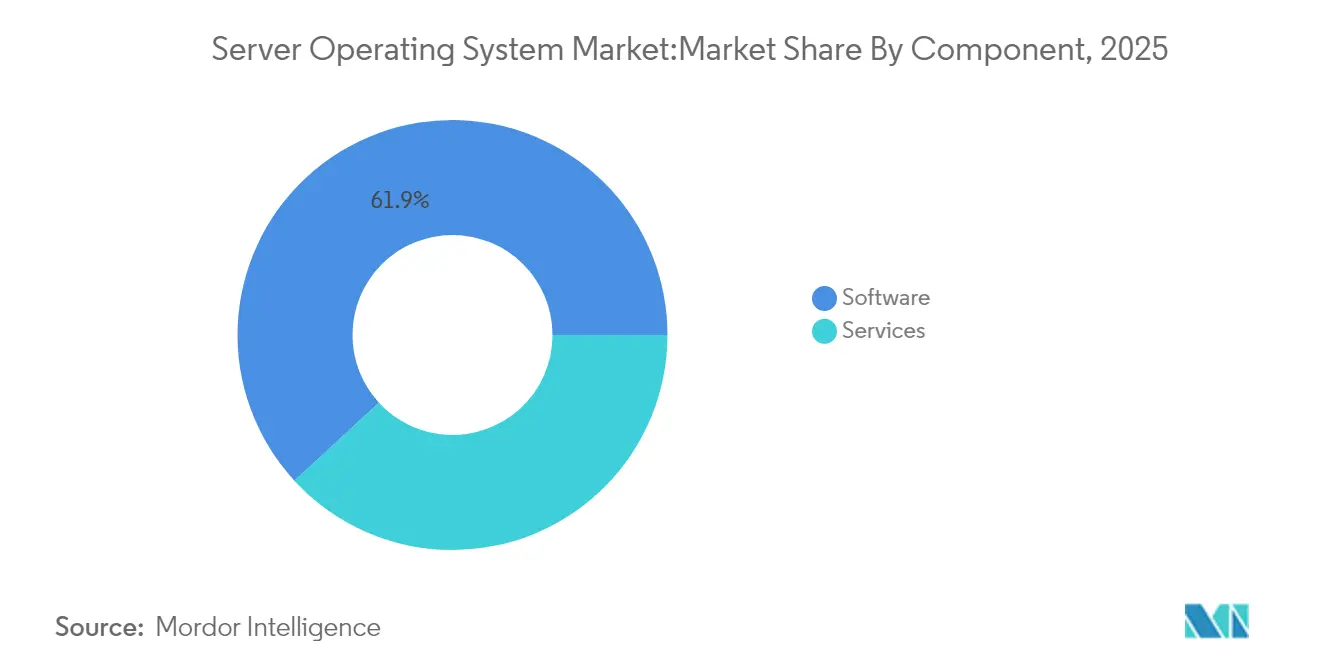

- By component, software held 61.85% of 2025 revenue; services register the fastest 10.58% CAGR as enterprises seek migration and integration support.

- By license model, commercial proprietary offerings commanded 39.10% share in 2025, whereas subscription-based SaaS operating systems grow at a 9.82% CAGR to 2031.

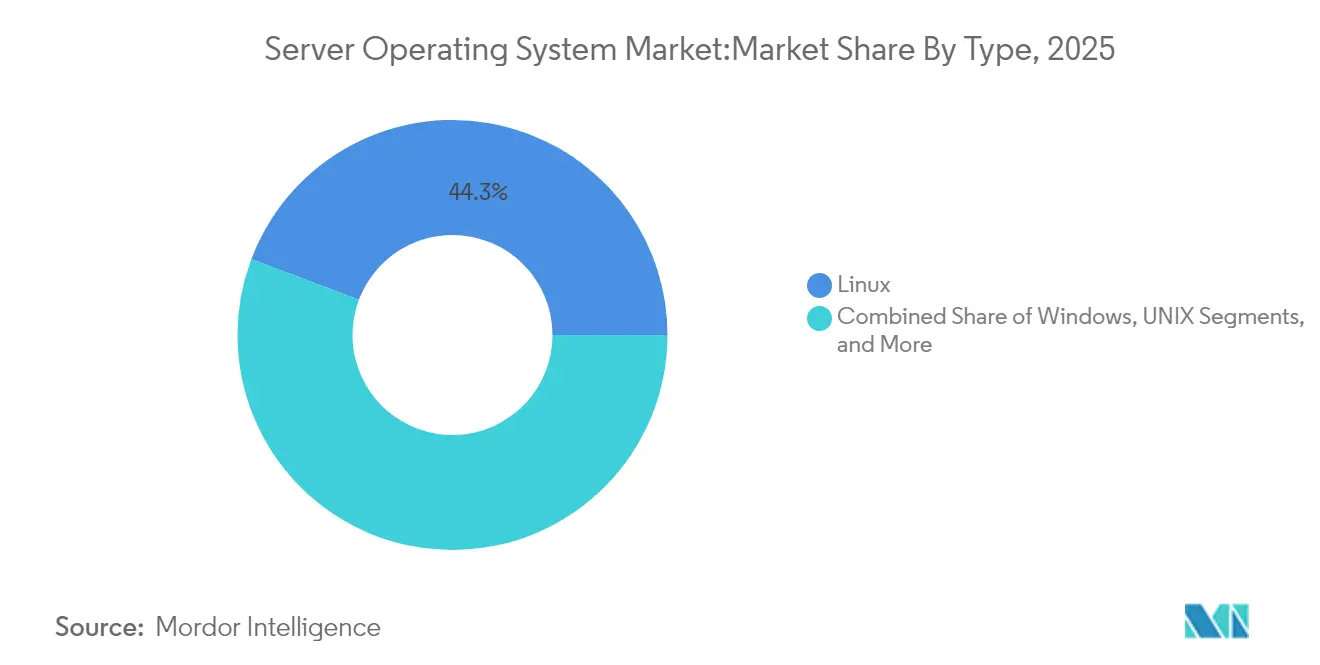

- By type, Linux led with 44.25% share in 2025, and Windows shows the highest 9.62% CAGR on the strength of Windows Server 2025 adoption.

- By server architecture, x86/x64 platforms controlled 56.05% of server operating system market share in 2025; ARM-based servers advance at a 9.47% CAGR to 2031.

- By virtualization status, virtual machines accounted for 59.70% of the server operating system market size in 2025, while containerized deployments rise at a 10.31% CAGR.

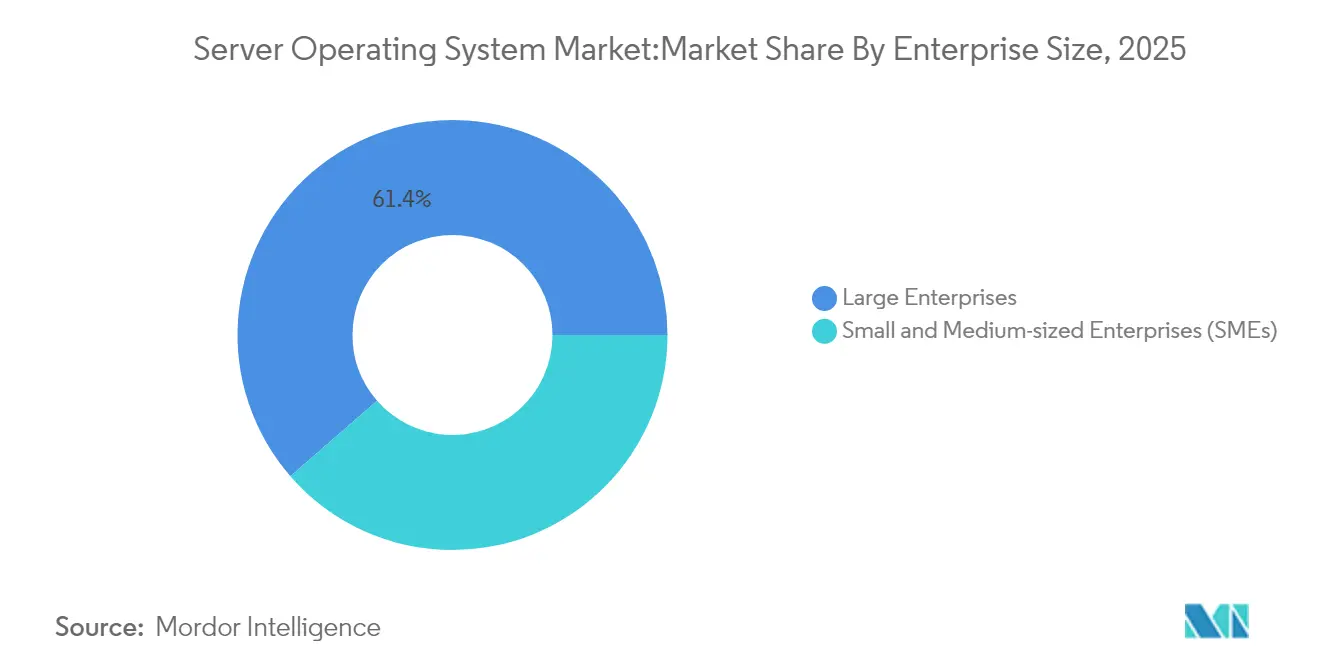

- By enterprise size, large organizations generated 61.40% of 2025 revenue, yet SMEs post the fastest 10.74% CAGR as managed services lower adoption barriers.

- By industry vertical, IT and Telecom supplied 27.55% revenue in 2025, whereas healthcare accelerates the most at a 9.91% CAGR on telemedicine and AI workloads.

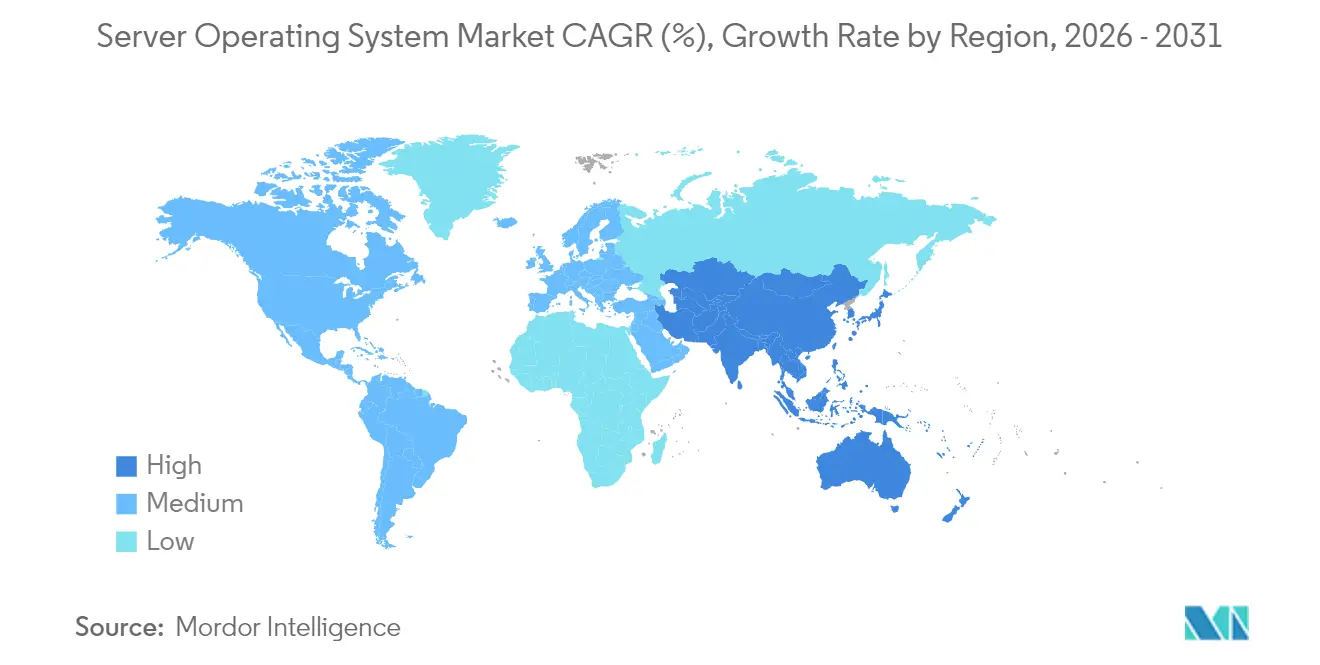

- By geography, North America led with 36.25% revenue in 2025, and Asia-Pacific records the highest 11.02% CAGR thanks to large-scale data-center investment.

- Microsoft, Red Hat, and SUSE jointly represented about 54.70% of 2025 commercial revenue, underscoring moderate concentration in the server operating system market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Server Operating System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-first enterprise refresh cycles | +2.1% | North America and EU with global roll-out | Medium term (2-4 years) |

| Hyperscale data-center build-outs | +1.8% | North America leading, APAC scaling | Long term (≥ 4 years) |

| Edge and 5G micro-data-center rollout | +1.4% | APAC core, spill-over to North America and EU | Medium term (2-4 years) |

| AI/ML workload proliferation | +2.3% | Early adoption in North America and China | Short term (≤ 2 years) |

| RISC-V server OS tool-chains mature | +0.8% | APAC focus, gradual EU and North America uptake | Long term (≥ 4 years) |

| Cyber-insurance compliance hardening | +1.2% | North America and EU, spreading worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cloud-first enterprise refresh cycles

Organizations are modernizing infrastructure beyond hardware replacement, choosing operating systems that deliver cloud parity on-premises. Windows Server 2025 brings native Azure Arc integration and hot-patch updates, cutting downtime and smoothing workload mobility Microsoft Corporation. Healthcare provider Kaleida Health projects USD 5–10 million in annual savings from hypervisor consolidation and software-defined infrastructure. [2]Cisco Systems, “Kaleida Health Case Study,” cisco.com Vendors court these needs; Red Hat now packages Enterprise Linux AI on Azure to simplify hybrid AI deployment Red Hat. Enterprises expect a single control plane, automated lifecycle management, and predictable cost models. The result is sustained demand for solutions that harmonize licensing, telemetry, and security across multi-location estates in the server operating system market.

Hyperscale data-center build-outs

Cloud providers keep raising capital intensity; Microsoft has earmarked USD 80 billion for AI-ready facilities, while Google plans USD 75 billion over the same horizon. Scale drives operating system redesign so that tens of thousands of nodes appear as one logical computer. Power capping, silicon accelerators, and telemetry APIs are embedded at the kernel level to extract every kilowatt. Warehousing compute at this magnitude spurs new distributions tailored to ARM and custom silicon, widening the addressable base of the server operating system market. Nuclear and renewable energy alliances highlight cost pressure, making energy-aware scheduling in the OS a competitive differentiator.

Edge and 5G micro-data-center rollout

Latency-sensitive use cases push compute to retail stores, cell towers, and factory floors. Red Hat’s MicroShift shrinks Kubernetes to fit fanless appliances, while SUSE Linux Enterprise Micro offers an immutable footprint for unattended sites. Hardware such as GIGABYTE E-series pairs with these OS builds to meet low-power, wide-temperature requirements. Operators demand zero-touch provisioning, self-healing, and secure boot. As 5G coverage widens, traffic steering between edge and core will depend on real-time telemetry integrated at the OS layer, expanding addressable opportunities across the server operating system market.

AI/ML workload proliferation

GPU partitioning, PCIe topology awareness, and high-bandwidth memory scheduling now sit inside mainstream server operating systems. Windows Server 2025 supports live GPU partitioning to enable multiple virtual machines per GPU. AMD positions EPYC platforms for everyday AI inference, requiring kernel patches for concurrent NUMA and GPU. Kubernetes adds elastic AI serving primitives. Operating systems that abstract heterogeneous accelerators give enterprises flexibility, pushing AI adoption deeper into verticals and lifting growth across the server operating system market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High migration and downtime costs | -1.6% | Global, large enterprise bias | Short term (≤ 2 years) |

| Rising zero-day vulnerabilities | -1.1% | Worldwide, acute in regulated industries | Medium term (2-4 years) |

| CentOS EOL license uncertainty | -0.9% | Global, most felt by cost-sensitive users | Short term (≤ 2 years) |

| Energy-efficiency regulations | -0.7% | EU lead, North America and APAC follow | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High migration and downtime costs

Moving mission-critical workloads can consume over USD 15,000 per terabyte when testing, staff retraining, and service windows are included, according to Hitachi Data Systems. Legacy application dependencies make direct upgrades risky, pushing some firms to virtualization wrappers. The CentOS sunset underscored exposure: 26% of scanned Linux servers needed replacement within months. Professional services surge as enterprises seek staged cut-overs that limit business disruption. Cost sensitivity slows near-term churn, tempering expansion of the server operating system market.

Rising zero-day vulnerabilities

Threat actors exploit new vectors faster than patch cycles close them. Hot-patch support in Windows Server 2025 shrinks reboot windows, yet many industries lack automated validation. Hardware-assisted isolation frameworks add layers but also complexity. Compliance audits and insurer questionnaires lengthen operations schedules. Security overhead weighs on budgets and can postpone refresh plans, creating friction that moderates the server operating system market trajectory.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Navigate Integration Complexity

Software dominated with 61.85% revenue in 2025, anchored by subscription licensing and continuous update streams, and it remains the economic foundation of the server operating system market. Enterprises favor predictable operating expense profiles and direct tie-ins with cloud consoles, which strengthens vendor lock-in yet simplifies procurement. Vendors integrate telemetry, policy engines, and cost governance features, blurring traditional OS boundaries and expanding wallet share.Services record an 10.58% CAGR to 2031 as hybrid estates multiply. Migration from CentOS, mainframe offload projects, and edge rollouts all call for advisory, design, and managed services. Providers build packaged engagements that bundle licenses, tuning, and regulatory mapping. As operating environments scale to multicloud and edge, specialized managed service offerings become essential, sustaining momentum for the server operating system market.

By License Model: Subscriptions Shift Economics

Commercial proprietary licenses claimed 39.10% share in 2025, reflecting Windows Server’s hold on directory-centric workloads. However, subscription SaaS models top growth at 9.82% CAGR as enterprises trade capital expenditure for pay-as-you-go utility. Vendors like Red Hat refine per-core and per-node tiers that scale linearly with workload peaks.Community distributions lose ground following CentOS 7 end-of-life, steering production users toward supported variants. Enterprises cite compliance attestations and indemnification as justification for paid Linux. The evolution underscores how consumption-based pricing increasingly defines value in the server operating system market.

By Type: Linux Widens Use-Case Breadth

Linux held a 44.25% share in 2025 on strength in container, cloud, and HPC tasks. Windows enjoys a 9.62% CAGR through 2031, bolstered by ARM64 support and deep Azure integration. UNIX continues a secular decline as proprietary RISC hardware ages out, though pockets remain in telecom billing and financial trading.Workload alignment drives choice: Linux dominates cloud-native microservices, while Windows keeps traction in ERP and identity services. Emerging distributions tuned for AI pipelines and edge autonomy diversify options, extending competitive contours within the server operating system market.

By Server Architecture: ARM and RISC-V Broaden Instruction Diversity

x86/x64 led with 56.05% share in 2025. Competitive challenges arise as ARM garners 13.45% revenue share and posts a 9.47% CAGR on the back of cloud custom silicon programs. AMD’s share climb to 27.2% of server CPU shipments illustrates competitive churn. RISC-V pilots in China showcase open-ISA potential, with early workloads focusing on web serving and object storage. Operating systems that abstract multiple ISAs behind common management APIs strengthen relevance, opening new lanes for adoption across the server operating system market.

By Virtualization Status: Containers Accelerate Modernization

Virtual machines accounted for 59.70% of 2025 deployments, yet containers grow 10.31% CAGR as microservices architecture becomes mainstream. Kubernetes sets the default scheduling layer, and operating systems expose namespace, cgroup, and seccomp optimizations to raise density. Physical deployments persist where hardware pass-through or licensed per-socket software dictate bare-metal.Container-optimized OS variants featuring read-only root and OTA updates shrink attack surfaces. These attributes encourage regulated industries to bypass generalized images in favor of minimal footprints, expanding the reachable base of the server operating system market.

By Deployment Mode: Hybrid Links Cloud and Site

Cloud hosted installations form 63.60% of 2025 nodes. Hybrid placements deliver the highest 10.22% CAGR as firms balance latency, autonomy, and compliance. Windows Server 2025, plus Azure Arc and Red Hat Device Edge, show how vendors unify policy and monitoring across locations. On-premises footprints remain for data sovereignty and equipment amortization.Unified control planes, consistent secrets management, and workload-aware placement algorithms rise to checklist status. Vendors delivering these capabilities shape purchasing criteria, boosting their standing in the server operating system market.

By Enterprise Size: SMEs Embrace Managed Platforms

Large enterprises held 61.40% revenue in 2025, leveraging volume discounts and bespoke support. Still, SMEs deliver an 10.74% CAGR as cloud marketplaces and managed service providers package turnkey stacks. Korean MSP revenue jumped from KRW 7 trillion to KRW 12 trillion in 2024, demonstrating local ecosystem momentum.Low-touch licensing, automated patching, and bundled security compliance help SMEs leapfrog traditional IT buildouts. The democratization accelerates the overall penetration of the server operating system market.

By Industry Vertical: Healthcare Accelerates Modernization

IT and Telecom captured 27.55% of 2025 spend, driven by telco cloud initiatives and data-center refreshes. Healthcare posts the top 9.91% CAGR as telemedicine, imaging, and AI diagnostics demand secure, high-throughput platforms. HCA Healthcare’s OpenShift deployment illustrates real-time analytics gains. BFSI maintains steady demand anchored in stringent governance.Industry-specific compliance, such as HIPAA and PCI-DSS, places a premium on audit-ready kernels and long-term support. Accommodating these mandates steers product differentiation within the server operating system market.

Geography Analysis

North America led with 36.25% revenue in 2025, backed by hyperscale investments from Microsoft, Google, and AWS. Microsoft alone budgeted USD 80 billion for next-generation AI facilities. Canada’s forthcoming efficiency rules for computer room air conditioners emphasize sustainable infrastructure. Mexican manufacturing expansion adds industrial server demand, further anchoring regional leadership in the server operating system market.

Asia-Pacific delivers the fastest 11.02% CAGR to 2031. China’s cloud sector is on track to surpass CNY 1 trillion by 2025. South Korean MSP revenue gains and GPU server sales, which touched KRW 5.1 trillion in 2024 for 72.7% growth, underscore AI’s pull-through effect. Japanese audit tooling and security compliance reinforce demand for hardened platforms. Regional policy pushes domestic ISAs, making multiarc OS support a prerequisite, broadening adoption opportunities in the server operating system market.

Europe witnesses steady uptake as the Energy Efficiency Directive obliges operators above 100 kW IT load to publish energy KPIs by September 2024. Operators adopt OS telemetry extensions to meet mandatory reporting. Germany, France, and the United Kingdom drive enterprise refresh cycles, while Eastern members explore sovereign open-source stacks. Regulatory alignment shapes purchasing criteria, sustaining consistent growth for the server operating system market.

Competitive Landscape

Competition remains moderate with Microsoft, Red Hat (IBM), and SUSE capturing an estimated 55% combined commercial revenue in 2024. Microsoft reinforces integration with Azure and introduces ARM64 builds while maintaining Active Directory dominance. Red Hat leverages OpenShift and Device Edge to extend Linux from core to edge. SUSE and Canonical focus on immutable, lightweight variants for container workloads. Oracle retains niche demand through highly tuned distributions for its database estate.

Architectural shifts alter the battlefield. ARM’s rise, AMD’s share gains, and experimental RISC-V pilots nudge vendors to broaden ISA support. Platform convergence emerges as a theme: operating system vendors fold observability, compliance scanning, and AI tool-chains into core subscriptions, blurring lines with adjacent software layers. Edge autonomy, AI scheduling, and energy telemetry form the next set of differentiators, steering share capture across the server operating system market.

Strategic moves show direction. IBM’s LinuxONE Emperor 5 embeds AI acceleration. [4]Tux Machines, “IBM Announces Powerhouse Linux Server,” tuxmachines.org Canonical extends 12-year LTS for Docker images. CoreSite partners with Oxide for hyperscale-grade on-prem cloud. Each action reflects a tilt toward lifecycle longevity, workload specificity, and sustainable operations that resonate with current buying criteria in the server operating system market.

Server Operating System Industry Leaders

Microsoft Corporation

Red Hat Inc. (IBM Corporation)

SUSE Group

Oracle Corporation

Amazon Web Services Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: IBM unveiled LinuxONE Emperor 5 with Telum II CPUs and post-quantum encryption, targeting confidential computing.

- March 2025: AMD introduced EPYC 4005 CPUs for small data centers.

- February 2025: NTT DATA completed a mainframe-to-AWS migration, cutting support costs by 25%.

- January 2025: China set energy-efficiency labeling for servers, effective Dec 2025.

- November 2024: Microsoft made Windows Server 2025 generally available.

- November 2024: Red Hat and Microsoft widened their collaboration to bring Enterprise Linux AI to Azure.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the server operating system market as all revenue generated from licenses, subscriptions, and embedded distributions that run on dedicated server hardware or in virtualized and containerized server instances within enterprise, cloud, and edge data-center environments, regardless of CPU architecture.

Scope exclusion: consumer desktop, mobile, and IoT operating systems temporarily repurposed as servers are out of scope.

Segmentation Overview

- By Component

- Software

- Services

- By License Model

- Commercial Proprietary

- Paid Linux Distribution

- Community Linux Distribution (Free)

- Subscription-based SaaS OS

- By Type

- Windows

- Linux

- UNIX

- Others

- By Server Architecture

- x86/x64

- ARM

- RISC-V

- POWER

- Others

- By Virtualization Status

- Virtual Server

- Physical Server

- Containerised Environment

- By Deployment Mode

- Cloud

- On-premise

- Hybrid

- By Enterprise Size

- Large Enterprises

- Small and Medium-sized Enterprises (SMEs)

- By Industry Vertical

- IT and Telecom

- BFSI

- Manufacturing

- Retail and E-Commerce

- Government

- Healthcare

- Media and Entertainment

- Other Industry Verticals

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Malaysia

- Singapore

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Experienced Mordor interviewers engage server OEM product managers, open-source distribution maintainers, cloud architects, and large-enterprise IT directors across North America, Europe, and fast-growing Asian hubs. These conversations clarify real-world license mix, typical core counts, container conversion rates, and regional price dispersion, thereby filling gaps left by public datasets and strengthening our assumptions.

Desk Research

We first gather macro and technology indicators from freely available tier-1 sources such as the International Telecommunication Union, OECD ICT statistics, Uptime Institute survey results, UN COMTRADE customs codes for HS 847141 servers, and regional trade-association white papers, which map shipments, installed base, and virtualization ratios. Company filings, 10-Ks, investor decks, and reputable press help us track software ASP shifts, support revenues, and cloud OS adoptions. Mordor analysts also pull financial snapshots from D&B Hoovers and headline trends from Dow Jones Factiva to cross-check market momentum. This list is illustrative; many additional sources were reviewed for context and validation.

Market-Sizing & Forecasting

A top-down "IT-capex spend to OS spend" model converts global server shipments and average core densities into an addressable licensing pool, which is then balanced with selective bottom-up supplier roll-ups and channel checks to avoid overstatement. Key variables include installed server stock, virtualization penetration, average license/subscription price per core, share of cloud-hosted workloads, container adoption ratio, and refresh cadence. Multivariate regression anchored on GDP growth, enterprise cloud migration rates, and data-center capacity additions projects the 2025-2030 trajectory, while scenario analysis tests upside from ARM servers and downside from serverless workloads.

Data Validation & Update Cycle

Outputs pass three-layer checks: automated anomaly flags, peer review among regional analysts, and a final sign-off by a senior mentor. We refresh models annually and re-open them immediately when material events (for example, major vendor pricing changes) occur, ensuring clients always receive the latest calibrated view.

Why Mordor's Server Operating System Baseline Stands Up to Scrutiny

Published market values often diverge because firms choose different scope definitions, licensing inclusions, and update cadences.

Key gap drivers include whether services revenue is counted, if cloud provider in-house kernels are treated as external sales, currency conversion timing, and how aggressively free Linux distributions are monetized.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 22.28 B (2025) | Mordor Intelligence | |

| USD 74.73 B (2025) | Global Consultancy A | Broadly counts desktop upgrades and edge micro-servers, with limited primary validation |

| USD 25.70 B (2024) | Industry Association B | Excludes support/services revenue and applies uniform ASPs across regions |

| USD 20.00 B (2025) | Regional Consultancy C | Focuses on four regions only and scales estimates solely from data-center counts |

The comparison shows that when scope is either stretched or narrowed, figures swing widely. Mordor's disciplined variable selection, mixed-method modeling, and yearly refresh cadence together provide a balanced, transparent baseline that decision-makers can trust.

Key Questions Answered in the Report

What is the value of the server operating system market in 2026?

The market is valued at USD 24.14 billion in 2026 and is projected to reach USD 36.03 billion by 2031.

Which deployment mode holds the largest share today?

Cloud installations lead with 63.60% of 2025 revenue, reflecting the dominance of hyperscale and SaaS workloads.

What segment is expanding the fastest through 2031?

Hybrid deployments post the quickest growth at a 10.22% CAGR as enterprises balance cloud scalability with on-premises control.

How quickly is ARM gaining ground in server architectures?

ARM-based servers are advancing at a 9.47% CAGR, buoyed by energy-efficient custom silicon adopted by major cloud providers.

Why are services growing faster than software sales?

Integration and migration complexity-especially post-CentOS EOL and during hybrid rollouts-drives a 10.58% CAGR for professional and managed services.

Which vertical shows the highest growth rate?

Healthcare leads with a 9.91% CAGR through 2031 as telemedicine, imaging, and AI diagnostics fuel demand for secure, high-performance server operating systems.

Page last updated on: