Sentinel Node Biopsy Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

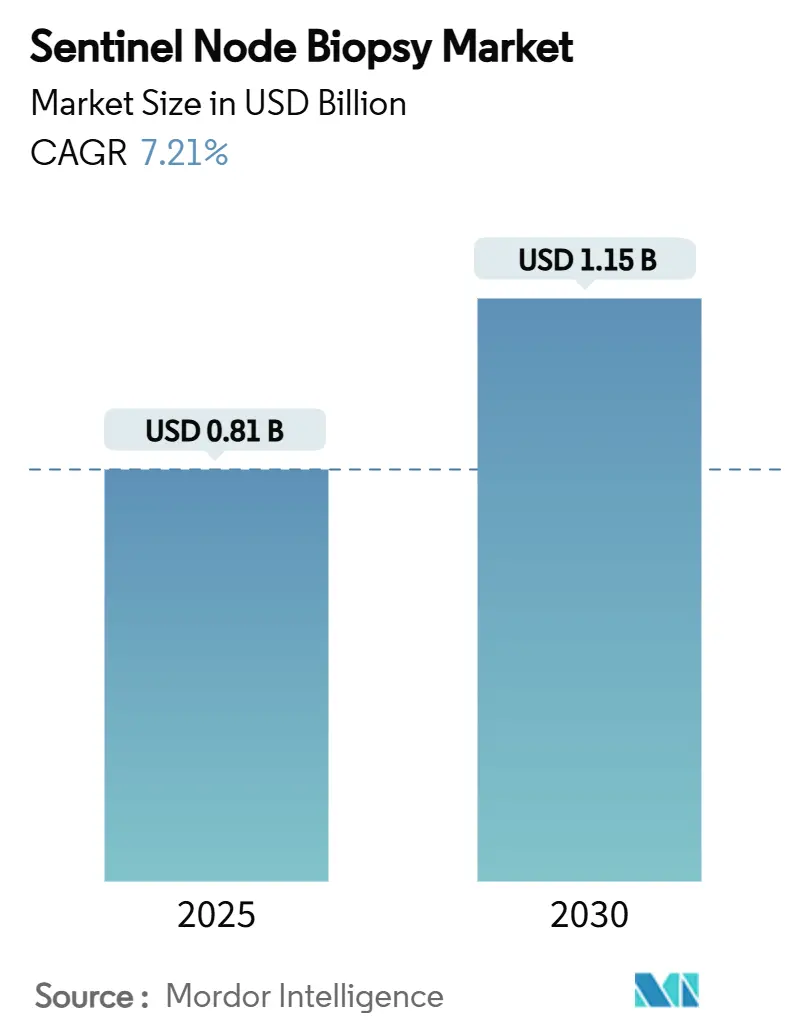

| Market Size (2025) | USD 0.81 Billion |

| Market Size (2030) | USD 1.15 Billion |

| Growth Rate (2025 - 2030) | 7.21% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sentinel Node Biopsy Market Analysis by Mordor Intelligence

The sentinel node biopsy market size stands at USD 814 million in 2025 and is on track to reach USD 1.15 billion by 2030, reflecting a 7.21% CAGR during the forecast period. This steady climb captures the transition from traditional radiotracer protocols toward artificial-intelligence-guided, multi-modal imaging that limits patient morbidity while safeguarding diagnostic rigor. Uptake has been strongest in breast cancer surgery, where evolving guidelines have elevated sentinel node biopsy to standard practice for early-stage disease. AI-enabled gamma detection, the arrival of radioisotope-free magnetic tracers, and more flexible reimbursement rules are shaping a competitive field in which technology differentiation and supply-chain resilience now outrank scale. Intensifying global breast and melanoma incidence, an aging demographic base, and the migration of procedures to outpatient centers together reinforce a supportive demand backdrop. North America remains the largest regional contributor, but Asia-Pacific shows the swiftest acceleration on the back of healthcare infrastructure upgrades and expanding screening programs.

Key Report Takeaways

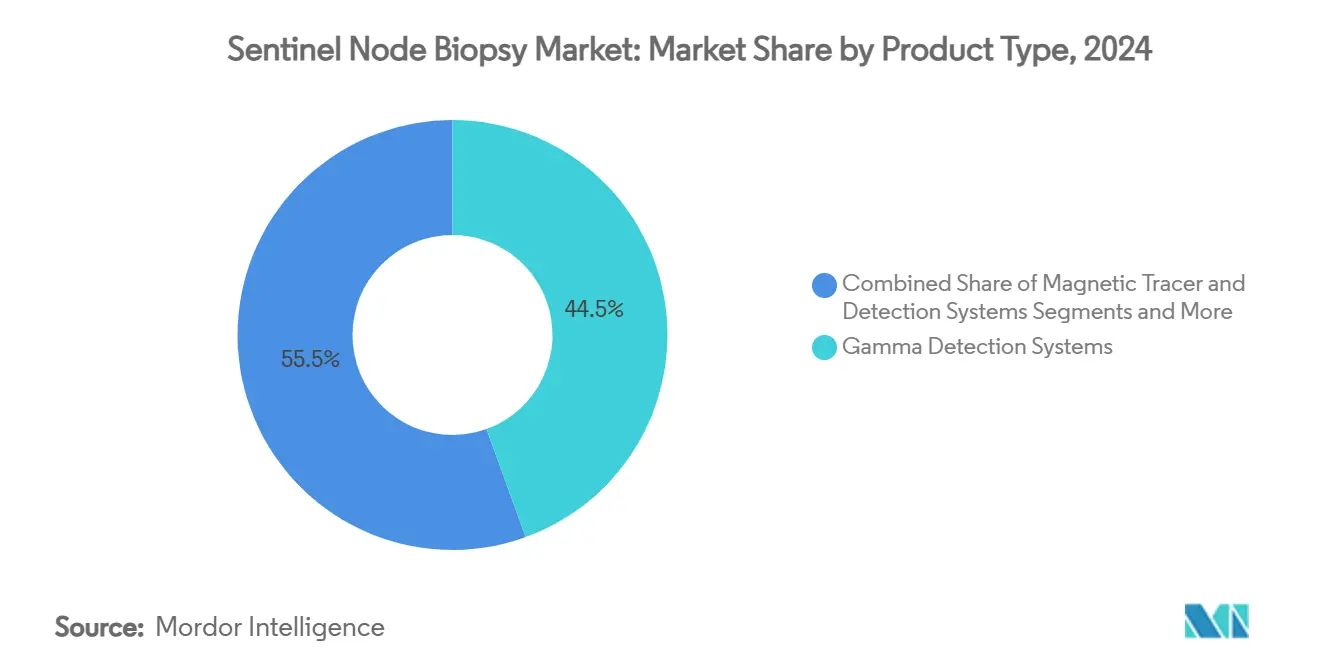

- By product type, gamma detection systems held 44.46% sentinel node biopsy market share in 2024, while magnetic tracer platforms are projected to advance at a 10.34% CAGR through 2030.

- By technology, the radioisotope plus blue dye method accounted for 53.64% of the sentinel node biopsy market size in 2024 and near-infrared fluorescence is forecast to expand at an 11.48% CAGR between 2025 and 2030.

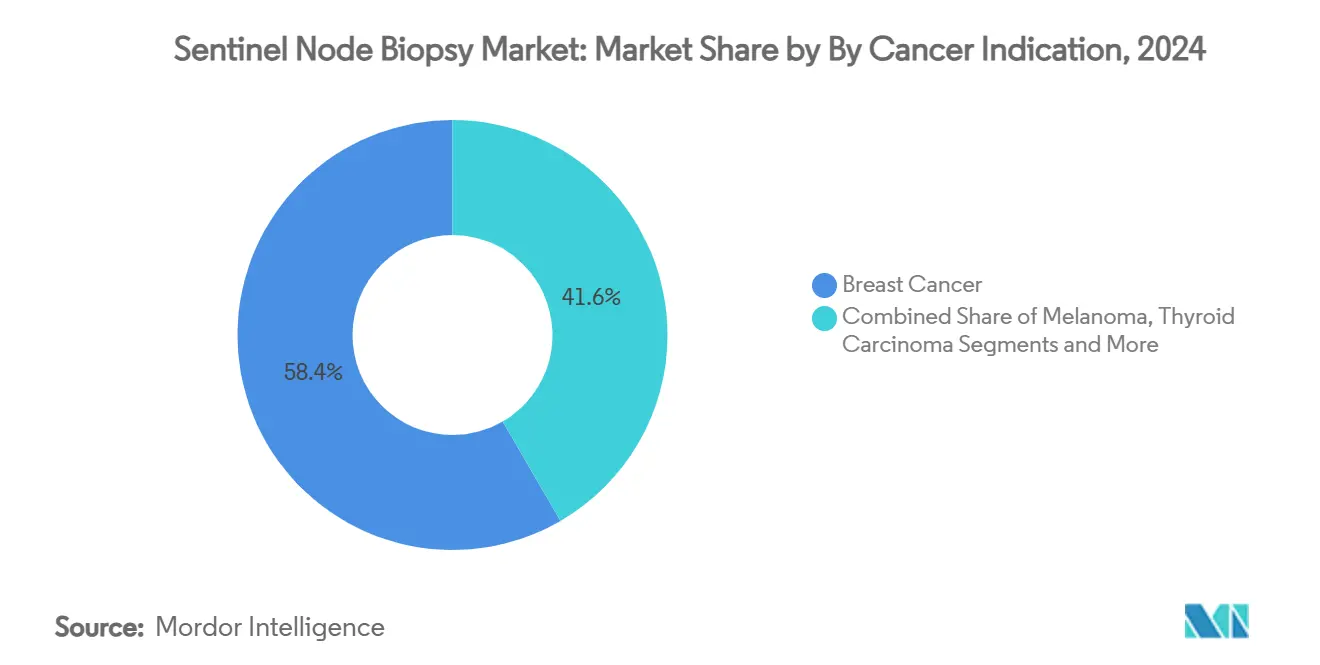

- By indication, breast cancer contributed 58.37% revenue share in 2024; thyroid carcinoma is expected to grow at a 10.76% CAGR to 2030.

- By end user, hospitals and surgical centers commanded 68.73% of the sentinel node biopsy market size in 2024, while ambulatory surgical centers are set to record a 9.37% CAGR through 2030.

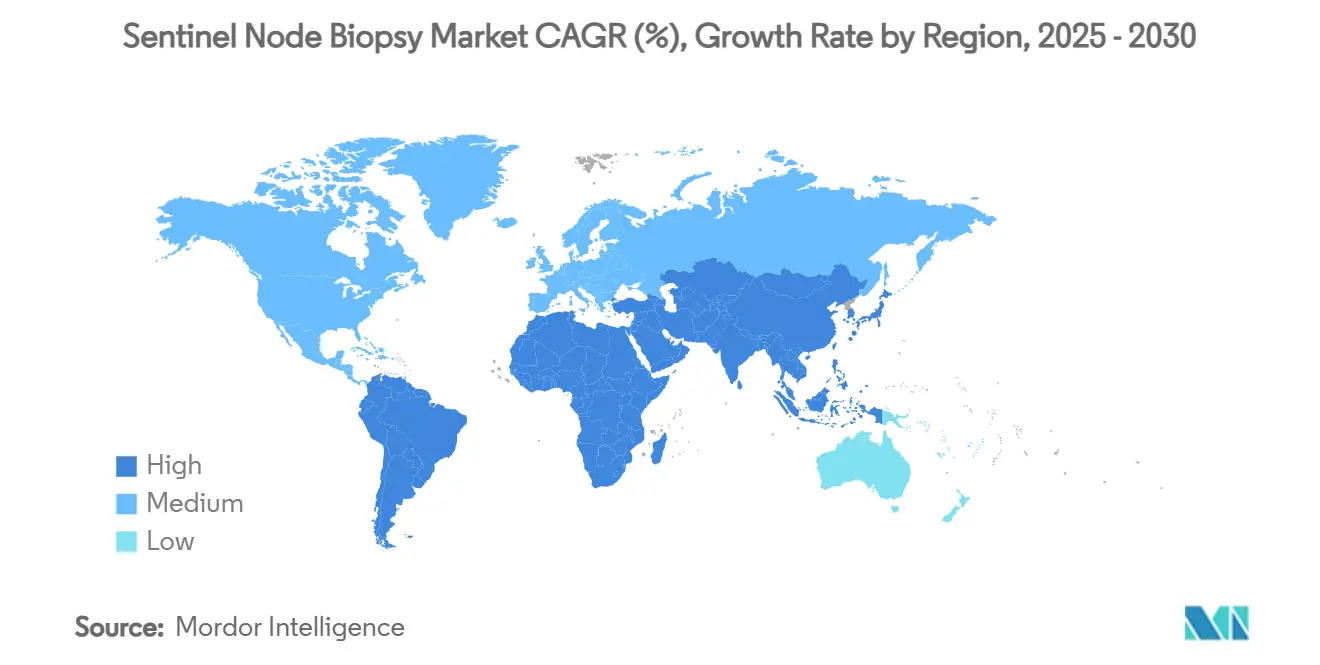

- By geography, North America led with 39.33% of 2024 revenue and Asia-Pacific is anticipated to register a 9.57% CAGR through 2030.

Global Sentinel Node Biopsy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global incidence of breast cancer and melanoma | +1.8% | North America and Europe leading; global relevance | Long term (≥ 4 years) |

| Shift toward minimally invasive staging to reduce morbidity | +1.5% | Developed markets worldwide | Medium term (2-4 years) |

| Technological advances in gamma detection and tracer chemistry | +1.2% | North America and European Union; adoption in Asia-Pacific | Medium term (2-4 years) |

| Favorable reimbursement and expanding guideline adoption | +1.0% | Primarily North America and European Union | Short term (≤ 2 years) |

| FDA approval of magnetic tracers enabling radioisotope-free procedures | +0.8% | Initial impact in North America with global rollout | Short term (≤ 2 years) |

| AI-powered intraoperative imaging improving localization accuracy | +0.9% | Centers of excellence in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Incidence of Breast Cancer and Melanoma

Elevated breast cancer and melanoma caseloads have become a structural catalyst for the sentinel node biopsy market. The American Cancer Society reports 316,950 new breast cancer cases and 42,680 deaths in 2025, underscoring the continuing need for accurate nodal staging.[1]American Cancer Society, “Cancer Facts & Figures 2025,” American Cancer Society, cancer.orgEarly-stage tumors dominate diagnosis profiles, and clinical protocols now favor sentinel node biopsy over axillary dissection to minimize postoperative morbidity without conceding oncologic safety. Melanoma shows comparable momentum, as tumors thicker than 1 mm routinely trigger sentinel node assessment according to AJCC guidance. Demographic aging amplifies demand in developed economies, while rapid oncology service expansion in China and other emerging nations broadens the global procedure base.

Shift Toward Minimally Invasive Staging to Reduce Morbidity

Health systems are championing approaches that shorten recovery times and curb complications. Results from the INSEMA trial revealed axillary recurrence of only 1.0% when sentinel node biopsy was omitted in carefully selected low-risk breast cancer patients versus 0.3% for standard care, highlighting the safety of conservative strategies.[2]Ines Mouuller, “Lessons from the INSEMA Trial,” Frontiers in Oncology, frontiersin.org With Medicare spending USD 6.1 billion on ambulatory surgical center procedures in 2022, outpatient settings have grown into pivotal adoption nodes. National Comprehensive Cancer Network updates now recommend sentinel node biopsy for early-stage vulvar cancer, illustrating the expanding clinical reach of minimally invasive staging.

Technological Advances in Gamma Detection and Tracer Chemistry

Artificial intelligence fused with gamma probes now classifies lymphographic patterns with 97.78% accuracy, surpassing traditional subjective reads.[3]Takashi Kato, “Artificial Intelligence–Based Indocyanine Green Lymphography,” Plastic and Reconstructive Surgery, lww.com Receptor-targeted radiotracers such as technetium Tc 99m tilmanocept achieve 97% node detection by selectively binding macrophage CD206 receptors, a leap toward molecularly precise staging. Near-infrared fluorescence, including indocyanine green, logs double-digit growth thanks to real-time visualization and radiation-free workflows. Hybrid tracers that merge radioactive and fluorescent properties supply surgeons with multi-channel guidance that tightens localization margins.

Favorable Reimbursement and Guideline Adoption

Clarity in billing has strengthened procedure economics. Medicare’s 2025 National Correct Coding Initiative manual expressly lists sentinel node biopsy as separately reportable when performed before breast excision or mastectomy in node-negative patients. The 2025 MIPS Quality Measure 264 rewards compliance, nudging adoption across oncology practices. Although inflation-adjusted Medicare payments for breast surgery declined 20.70% between 2003 and 2023, the distinct line-item recognition of sentinel node biopsy offsets some budget pressure.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost of advanced detection systems and consumables | -1.2% | Cost-sensitive markets worldwide | Medium term (2-4 years) |

| Radiation safety and regulatory hurdles for radioisotopes | -0.8% | Strictest in European Union and North America | Short term (≤ 2 years) |

| Global supply-chain risk for technetium-99m radioisotope | -1.0% | Regions dependent on imports, notably United States | Short term (≤ 2 years) |

| Limited surgical expertise in emerging markets | -0.6% | Asia-Pacific, Middle East and Africa, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Advanced Detection Systems and Consumables

Premium gamma probes that integrate real-time AI analytics can cost more than USD 200,000, placing them out of reach for resource-constrained hospitals. Ongoing spend on specialized tracers further burdens operating budgets, compelling finance departments to benchmark capital outlays against projected procedure volumes and reimbursement yields. Ambulatory centers, built on high-turnover economics, hesitate to invest until unit costs decline. Magnetic systems promise lower long-run expenses by removing regulated radiation spaces, yet current acquisition prices remain elevated.

Global Supply-Chain Risk for Technetium-99m Radioisotope

Production of molybdenum-99, the parent isotope of technetium-99m, still hinges on a handful of aging reactors susceptible to unplanned outages. A 2023 shutdown at a primary European facility delayed thousands of imaging sessions in North America, underscoring the vulnerability. The United States is advancing domestic manufacturing through the Department of Energy’s cooperative programs, yet full commercial capacity is several years away. Persistent supply risk encourages providers to consider magnetic tracers or fluorescence-only workflows.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Magnetic Tracers Drive Innovation

Gamma detection systems generated the largest revenue in 2024, anchored by decades of validation and a 44.46% sentinel node biopsy market share. Magnetic tracer platforms, approved only recently, are accelerating at a 10.34% CAGR as surgeons embrace radiation-free workflows that sidestep regulatory duties and guard against technetium-99m shortages. A pivotal study found Magtrace identified an average of 3.2 sentinel nodes versus 1.9 for standard methods, with patient satisfaction scoring 100% for scheduling flexibility. Consumables such as single-use probes and tracer vials generate stable recurring revenue, encouraging suppliers to bundle hardware with subscription models.

Consumable demand amplifies as hybrid imaging grows popular; combined magnetic and fluorescence injections are gaining traction for simultaneous deep-node localization and surface visualization. Artificial intelligence overlays on gamma detectors achieved 97.78% pattern recognition accuracy, enabling time-pressed surgeons to interpret readings with greater confidence. Together these dynamics reinforce the magnet for premium offerings that enhance throughput without sacrificing performance.

By Technology: Near-Infrared Fluorescence Gains Momentum

The radioisotope plus blue dye technique retained a 53.64% sentinel node biopsy market share in 2024. Near-infrared fluorescence is the fastest-growing, predicted to register an 11.48% CAGR through 2030. Indocyanine green enables real-time lymphatic mapping under either open or robotic platforms, boosting detection rates as high as 100% in select colon cancer series. Dual-tracer protocols that marry technetium-99m with fluorescence reduce empty-pocket incidences to 2.7% in early-stage endometrial cases.

Magnetic tracers complement fluorescence by supplying depth-penetrating signals absent optical tools. The technological arms race now centers on integrated consoles that co-register gamma, magnetic, and optical signatures, with AI engines triaging signal strength to guide resection margins. This multi-modal orientation underpins the sustained premium commanded by advanced platforms.

By Cancer/Indication: Thyroid Carcinoma Shows Rapid Growth

Breast surgery, at 58.37% of 2024 revenue, remains the sentinel node biopsy market anchor, yet thyroid carcinoma is the clear growth outlier. With global incidence projected to top 1.1 million cases by 2050, thyroid sentinel node applications are climbing at a 10.76% CAGR. Melanoma continues to secure policy support as tumors thicker than 1 mm trigger mandatory node mapping. Vulvar cancer guidelines now recommend sentinel node biopsy for stage IB disease, pushing adoption within gynecologic oncology.

Non-melanoma skin cancers, once perceived as low-risk, have shown 24.4% positivity rates on sentinel testing, advocating broader surgical staging. Expanding clinical breadth de-risks the sector by diluting its historical reliance on breast oncology volumes.

By End User: Ambulatory Centers Drive Efficiency

Hospitals and integrated surgical centers still dominate, holding 68.73% of 2024 revenue because of installed nuclear medicine facilities and multidisciplinary teams. Ambulatory surgical centers, however, registered the fastest growth trajectory at a 9.37% CAGR. Medicare’s explicit payment models encourage the shift after validating that outpatient sentinel node procedures can match inpatient safety benchmarks.

Cancer research institutes continue to seed innovation through trials that evaluate AI decision assistants and hybrid tracers. Specialty breast clinics represent an emerging niche equipped to offer one-stop diagnostics, surgery, and reconstruction, supporting further magnetization of outpatient volumes.

Geography Analysis

North America secured 39.33% of 2024 revenue, nurtured by wide insurance coverage, cumulative surgeon proficiency, and a sizable installed base of gamma cameras. The United States benefits from clear procedure coding, though a 20.70% real-term drop in breast surgery payments since 2003 puts pressure on capital budgets. Supply-chain strain for molybdenum-99 remains the region’s key vulnerability, prompting many centers to trial magnetic or fluorescence-only protocols while domestic isotope production ramps under the Department of Energy’s programs.

Europe constitutes a mature yet innovation-friendly environment. Approval of radiopharmaceuticals such as tilmanocept across the 27-member bloc broadens access to 505,000 annual cancer cases, maintaining a solid revenue cushion. The region’s strict radiation stewardship amplifies interest in magnetic tracers, especially in outpatient clinics that cannot justify full nuclear infrastructure.

Asia-Pacific registers the highest regional CAGR at 9.57%. China recorded 4.8 million new cancer cases in 2022, and its fast-scaling tertiary hospitals are adopting sentinel node techniques alongside breast-conserving surgery mandates. Japan’s universal coverage and aging demographic enhance baseline volume, while India and Southeast Asia represent value-conscious markets open to cost-efficient fluorescent tracers. Limited surgical training and capital constraints remain headwinds, though multinational device makers are rolling out education partnerships to bridge gaps.

Latin America and the Middle East and Africa collectively account for a modest share but post above-average growth on rising screening awareness. Public hospital modernization programs in Brazil and Saudi Arabia include nuclear medicine suites, setting the stage for sentinel node biopsy rollouts once staff training milestones are hit.

Competitive Landscape

The sentinel node biopsy industry displays moderate fragmentation. Established device suppliers such as Hologic, Stryker, and BD compete with focused imaging innovators bringing AI software and novel tracers. Hologic’s USD 310 million purchase of a magnetic tracer specialist in 2024 highlighted the value of radiation-free platforms in a market attentive to isotope shortages, while BD’s fiscal 2025 earnings call showcased incremental revenue from consumable probes that drive repeat sales. Cardinal Health strengthened its radiopharmaceutical portfolio by acquiring tilmanocept rights, emphasizing supply-chain control over tracer availability.

Competitive positioning now hinges on integrated offerings that blend hardware, software, and tracer chemistry. Firms able to secure multi-modal patents and forge hospital service contracts are advantaged. Partnerships between device makers and pharmaceutical companies proliferate as targeted tracers move through regulatory pipelines. AI start-ups are entering via algorithm licensing deals, capitalizing on the installed base of gamma cameras that can be software-upgraded without a wholesale equipment swap.

Supply resilience functions as an emerging differentiator. Vendors with alternative tracer lines, such as magnetic nanoparticles or indocyanine green kits, can buffer clients when technetium-99m disruptions strike. Tier-one suppliers leverage global manufacturing footprints to hedge geopolitical shocks, while newcomers often rely on contract assemblers, introducing risk but allowing nimble scaling in niche segments.

Sentinel Node Biopsy Industry Leaders

Mammotome (Devicor Medical Products Inc.)

Hologic Inc.

Stryker Corporation

Dilon Technologies Inc.

Navidea Biopharmaceuticals Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: SkylineDx announced a meta-analysis confirming that its Merlin CP-GEP assay accurately stratifies cutaneous melanoma patients for sentinel node biopsy, enabling more precise patient selection.

- April 2024: Hologic completed its USD 310 million acquisition of Endomagnetics, adding magnetic tracer technology to its breast surgery portfolio.

Global Sentinel Node Biopsy Market Report Scope

| Gamma Detection Systems (Probes & Consoles) |

| Magnetic Tracer & Detection Systems |

| Radiotracers |

| Fluorescent & Dye Tracers |

| Consumables & Accessories |

| Radioisotope + Blue Dye Technique |

| Dual-Tracer Technique (Radioisotope + Fluorescence) |

| Near-Infrared Fluorescence (ICG) Technique |

| Magnetic Tracer Technique |

| Breast Cancer |

| Melanoma |

| Thyroid Carcinoma |

| Vulvar Cancer |

| Non-Melanoma Skin Cancer |

| Other Cancers (Head & Neck, GI, etc.) |

| Hospitals & Surgical Centers |

| Ambulatory Surgical Centers (ASCs) |

| Cancer Research Institutes |

| Specialty Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Gamma Detection Systems (Probes & Consoles) | |

| Magnetic Tracer & Detection Systems | ||

| Radiotracers | ||

| Fluorescent & Dye Tracers | ||

| Consumables & Accessories | ||

| By Technology | Radioisotope + Blue Dye Technique | |

| Dual-Tracer Technique (Radioisotope + Fluorescence) | ||

| Near-Infrared Fluorescence (ICG) Technique | ||

| Magnetic Tracer Technique | ||

| By Cancer/Indication | Breast Cancer | |

| Melanoma | ||

| Thyroid Carcinoma | ||

| Vulvar Cancer | ||

| Non-Melanoma Skin Cancer | ||

| Other Cancers (Head & Neck, GI, etc.) | ||

| By End User | Hospitals & Surgical Centers | |

| Ambulatory Surgical Centers (ASCs) | ||

| Cancer Research Institutes | ||

| Specialty Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

1. What is the current size of the sentinel node biopsy market?

The sentinel node biopsy market size is USD 814 million in 2025 and is projected to reach USD 1.15 billion by 2030 at a 7.21% CAGR.

2. Which product type dominates revenue?

Gamma detection systems lead with 44.46% sentinel node biopsy market share because of their long clinical track record.

3. Why are magnetic tracers gaining attention?

Magnetic tracers remove radiation licensing hurdles and mitigate technetium-99m shortages, supporting a 10.34% CAGR through 2030.

4. Which indication is growing fastest?

Thyroid cancer applications are forecast to grow at a 10.76% CAGR as incidence climbs and surgical protocols evolve.

5. What is the main regional growth engine?

Asia-Pacific posts the highest regional CAGR at 9.57% driven by expanding oncology infrastructure and increasing cancer screening penetration.

Page last updated on: