Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

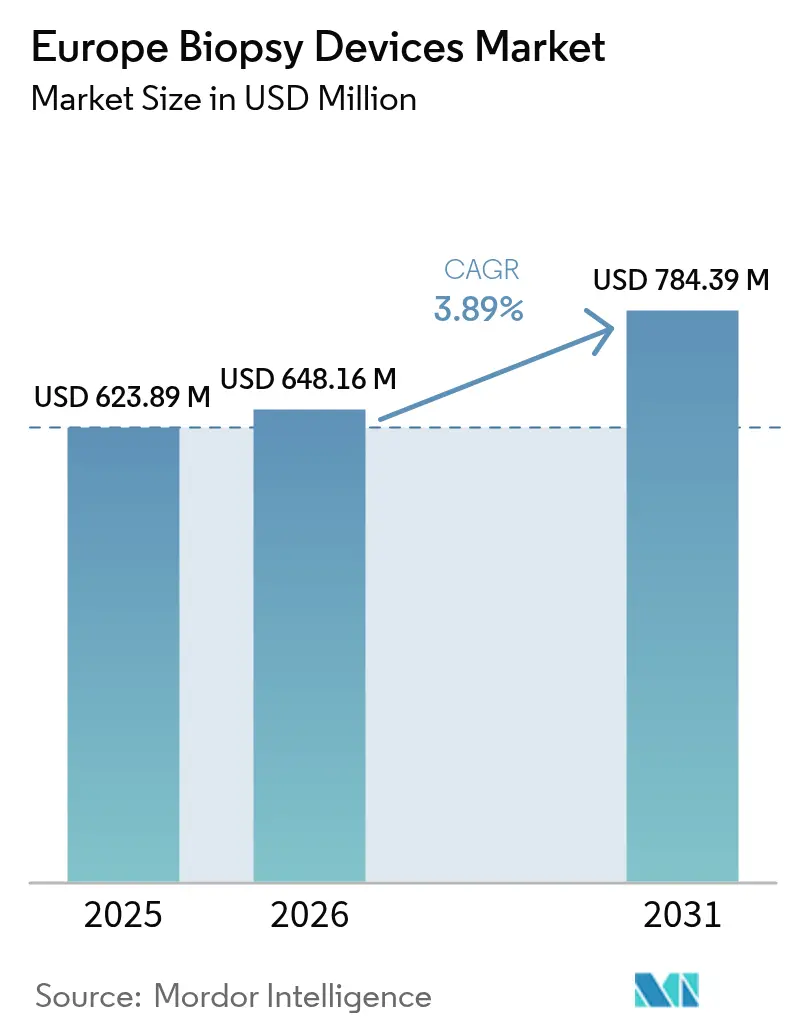

| Base Year Market Size (2025) | USD 623.89 Million |

| Market Size (2026) | USD 648.16 Million |

| Market Size (2031) | USD 784.39 Million |

| Growth Rate (2026 - 2031) | 3.89% CAGR |

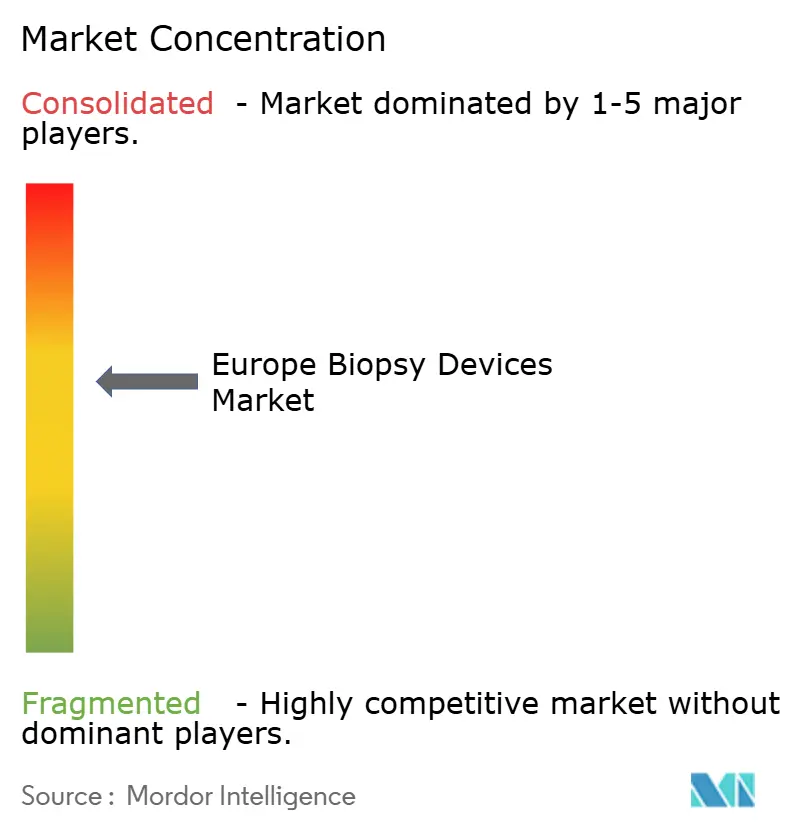

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Biopsy Devices Market Analysis by Mordor Intelligence

Europe biopsy devices market size in 2026 is estimated at USD 648.16 million, growing from 2025 value of USD 623.89 million with 2031 projections showing USD 784.39 million, growing at 3.89% CAGR over 2026-2031. Demand continues to rise as organized cancer-screening programs expand, hospitals upgrade to EU Medical Device Regulation (MDR)-compliant equipment, and physicians shift toward imaging-guided, minimally-invasive techniques. Adoption of vacuum-assisted and core needle systems is accelerating because they reduce sampling errors, shorten procedure time, and integrate easily with MRI or CT guidance. Conversely, supply bottlenecks linked to MDR certification delays keep pricing firm and create procurement gaps, especially for smaller facilities. Safety-related product recalls underscore the need for robust post-market surveillance, prompting hospitals to favor vendors that can demonstrate strong quality systems. Across the region, national reimbursement reforms are steering a growing share of biopsies to ambulatory surgical centers, lowering overall procedure costs while preserving hospital capacity for complex oncology cases.

Key Report Takeaways

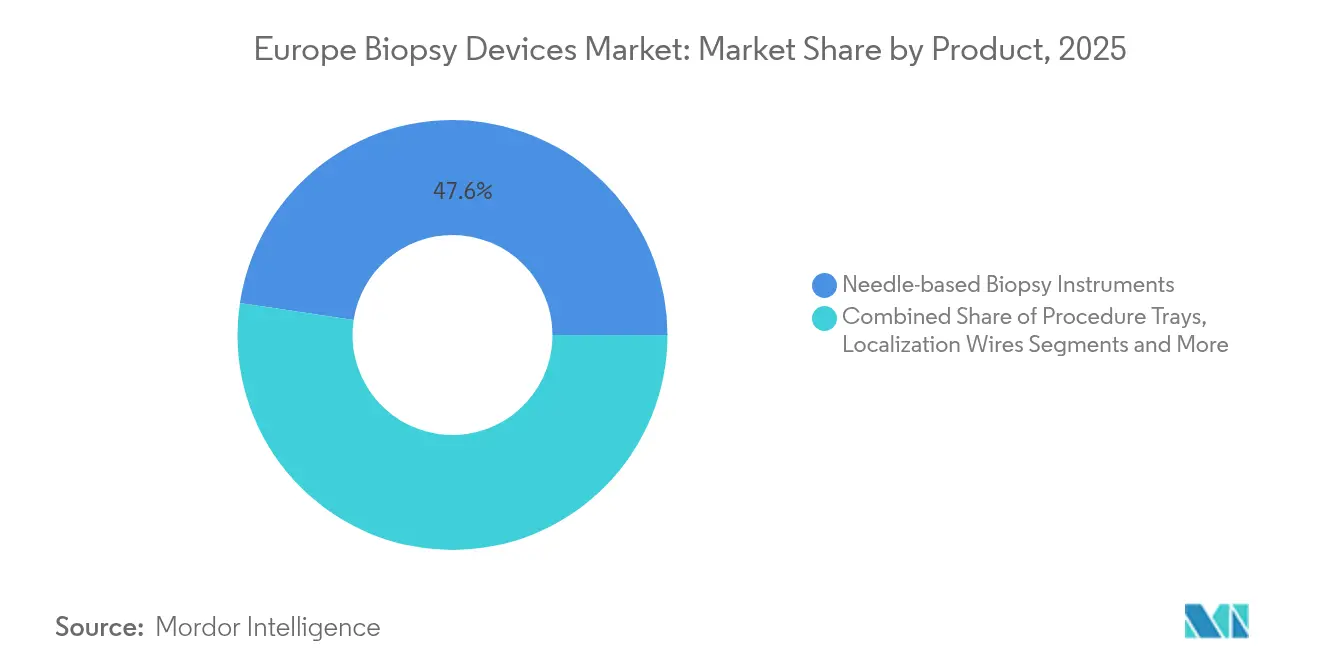

- By product, needle-based instruments led with 47.62% Europe biopsy devices market share in 2025 while also posting the fastest 7.89% CAGR through 2031.

- By application, breast procedures retained a 38.02% revenue share in 2025; lung biopsies are projected to grow the quickest at 8.61% CAGR to 2031.

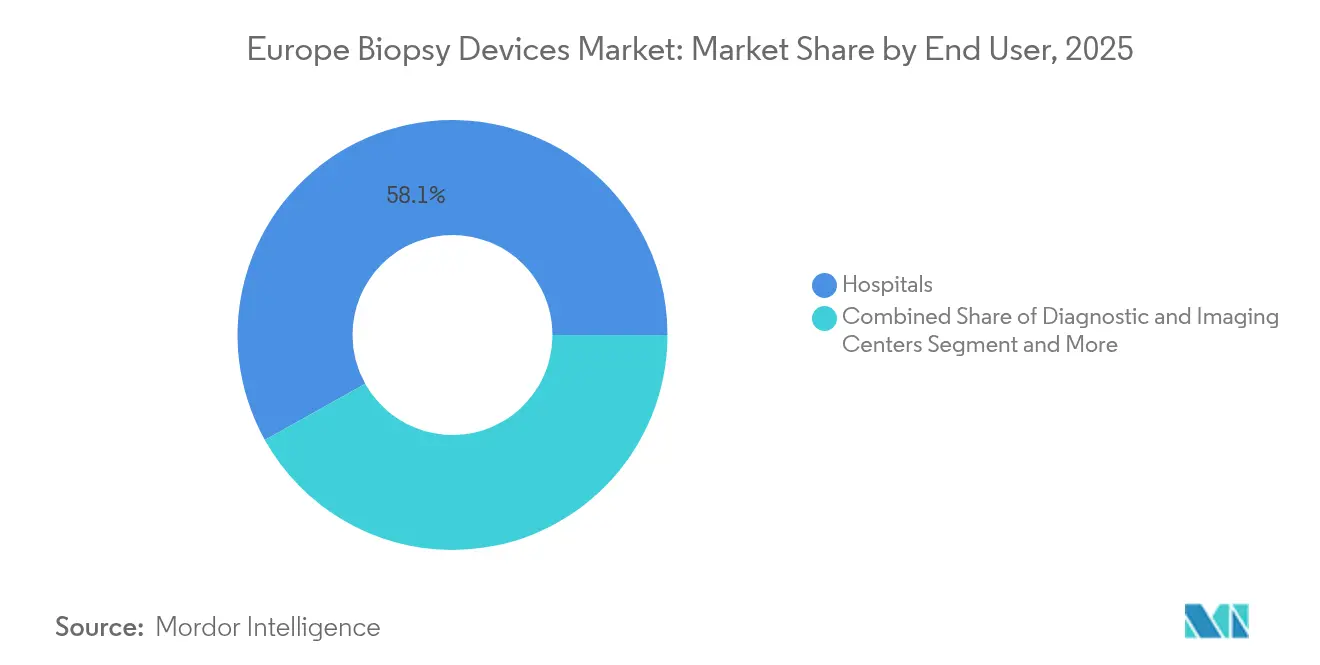

- By end user, hospitals held 58.11% of the Europe biopsy devices market size in 2025, whereas ambulatory surgical centers are expanding at 8.03% CAGR over the same period.

- By geography, Germany accounted for 22.55% of regional revenue in 2025; Spain is set to record the highest 6.24% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Biopsy Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing preference for minimally-invasive procedures | +1.2% | Germany and Nordic markets | Medium term (2-4 years) |

| Rising cancer screening programs across EU-27 | +1.8% | All EU-27 member states | Long term (≥ 4 years) |

| Shift toward ambulatory & outpatient biopsy centers | +0.9% | Western Europe first movers | Medium term (2-4 years) |

| Technological convergence of imaging-guided robotics | +1.1% | Germany, France, UK | Long term (≥ 4 years) |

| EU in-vitro diagnostic regulation driving device upgrades | +0.7% | EU-27 | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Preference for Minimally-Invasive Procedures

Transperineal prostate biopsies now represent standard-of-care across leading urology centers after a multicenter trial showed lower infection rates than the traditional transrectal route, without compromising diagnostic accuracy. MRI-guided freehand techniques for small liver lesions reach 90% clinical success, encouraging their dissemination to oncology units that previously relied on CT guidance. Such patient-friendly modalities shorten recovery time and reduce hospital stays, aligning with payer cost-containment goals. Research groups are now testing nanoneedle patches capable of sampling intracellular biomarkers painlessly, a breakthrough that could reach clinical practice by 2026. These advances should keep the Europe biopsy devices market on a steady adoption curve even as regulatory hurdles rise.

Rising Cancer Screening Programs Across EU-27

The European Commission’s Beating Cancer Plan earmarked EUR 4 billion to achieve 90% screening coverage for breast, cervical, and colorectal cancers by 2025, and has broadened scope to lung and prostate cancers[1]European Commission, “A Cancer Plan for Europe,” commission.europa.eu. Organized programs replace opportunistic screening, compelling health systems to buy standardized biopsy kits, training mannequins, and AI-enabled image-review software. Updated mortality projections for 2025 already show a 9.8% decline in breast-cancer deaths among women aged 50-69, a result that is reinforcing political support for national screening budgets. Central and Eastern European countries, historically under-equipped, are channeling EU cohesion funds into mobile biopsy units to close access gaps. This policy-driven demand supports a predictable, multi-year order pipeline for device suppliers.

Shift Toward Ambulatory & Outpatient Biopsy Centers

European payers are moving routine biopsies out of hospital wards and into specialized day-surgery centers where overheads are lower and scheduling is faster. Reimbursement catalogues in Germany, France, and the UK now provide higher relative value units for outpatient procedures, encouraging private investors to open new facilities that can deliver MRI-guided breast, prostate, and thyroid biopsies on the same visit. COVID-19 disruptions accelerated this migration as hospitals preserved beds for critical care. Patient satisfaction scores have improved due to reduced waiting times, while infection-control protocols are easier to maintain in small, dedicated units. As a result, ambulatory centers will account for a rising share of the Europe biopsy devices market through 2030.

EU In-Vitro Diagnostic Regulation Driving Device Upgrades

Regulation (EU) 2024/1860 grants limited extensions yet still requires fresh clinical evidence and tighter post-market vigilance, driving hospitals to replace legacy tools with MDR-certified models[2]European Parliament and Council, “Regulation (EU) 2024/1860,” eur-lex.europa.eu. Some small manufacturers are exiting low-volume niches, prompting purchasing-group tenders that favor established brands with full conformity dossiers. Although certification costs add short-term price pressure, the wave of equipment refreshes sustains demand in the Europe biopsy devices market over 2025-2027.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Product recalls & safety notices | -0.8% | High-adoption markets across Europe | Short term (≤ 2 years) |

| Stringent MDR certification timelines causing supply gaps | -1.1% | All EU-27 member states | Medium term (2-4 years) |

| Limited reimbursement for novel vacuum-assisted systems | -0.6% | Variable across health systems | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Product Recalls & Safety Notices

Hologic voluntarily withdrew more than 91,000 BioZorb 3D markers after 188 adverse-event reports of pain, infection, and migration, triggering a Class I recall and heightening regulatory scrutiny. The FDA also flagged Stereotactic disposable needle kits that risked stainless-steel debris contamination, prompting EU vigilance notices and procurement freezes. Hospitals now impose stricter supplier audits and require real-time batch traceability, lengthening sales cycles and raising support costs for manufacturers. These episodes dampen near-term volume growth within the Europe biopsy devices market but reinforce the strategic value of robust quality-management systems.

Stringent MDR Certification Timelines Causing Supply Gaps

A MedTech Europe survey shows 50% of companies plan to shrink their EU portfolios and may discontinue one-third of devices due to MDR documentation burdens. Notified-body queues extend to 24 months, leaving order backlogs and spot shortages that delay installations in public hospitals. Small and medium enterprises struggle most, diverting R&D budgets to regulatory affairs. Nevertheless, once certified, larger suppliers enjoy reduced competition and stronger pricing power, an offsetting factor that stabilizes long-term revenue within the Europe biopsy devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Needle-Based Instruments Drive Innovation

Needle-based systems dominated the Europe biopsy devices market with a 47.62% revenue share in 2025, and they will grow at an 7.89% CAGR toward 2031 as physicians upgrade to core and vacuum-assisted platforms that minimize sampling errors. Core devices now feature sharper tip designs, proprietary coatings, and adjustable throw lengths that preserve tissue architecture for genomic assays. Vacuum-assisted handpieces collect multiple contiguous cores through a single incision, reducing repeat procedures; the VACIS trial even positions vacuum excision as a surgery-sparing option for low-grade ductal carcinoma in situ. Steady demand also persists for localization wires and radioactive seed systems that guide breast-conserving surgery, although adoption varies with reimbursement. Digital guidance consoles integrate electromagnetic tracking with real-time ultrasound, easing workflow in busy ambulatory centers. NeoDynamics’ pulse-technology device underscores continuing innovation aimed at shortening procedure time and operator learning curves.

Procedure trays, markers, and ancillary kits deliver recurring consumable sales that insulate vendors from capital-budget cycles. Price competition remains moderate because MDR compliance costs limit new entrants. Hospitals prioritize suppliers that offer comprehensive portfolios—core needles, vacuum systems, localization tools, and AI-ready consoles—along with field-service capabilities that ensure uninterrupted screening workflows.

By Application: Lung Procedures Accelerate Growth

Breast applications accounted for 38.02% of Europe biopsy devices market share in 2025, underpinned by national mammography programs and well-established clinical pathways. Yet lung indications will expand the fastest at 8.61% CAGR through 2031, lifting their contribution to the Europe biopsy devices market size as low-dose CT screening gains acceptance. Advances in minimum-intensity projection imaging now predict pneumothorax risk with 87.2% specificity, shortening observation time after percutaneous procedures. Navigational bronchoscopy and robotic catheters further reduce complication rates and enable sampling of small peripheral nodules detected in screening scans.

Colorectal biopsies rise more gradually as many EU countries still work to boost colonoscopy participation above 60%, while prostate procedures benefit from PRAISE-U efforts to standardize transperineal, MRI-fusion protocols. Liver and kidney biopsies enjoy incremental gains from improved ultrasound elastography and contrast-enhanced MRI. Overall, diversified application uptake mitigates cyclical risk and keeps the Europe biopsy devices market on a balanced growth trajectory.

By End User: Ambulatory Centers Gain Momentum

Hospitals remained the primary buyers with 58.11% revenue in 2025 because they handle complex cases that require multiplanar imaging and multidisciplinary oversight. They invest heavily in hybrid MRI-OR suites and robotic guidance arms that underpin their role as referral hubs. Still, ambulatory surgical centers will post the strongest 8.03% CAGR to 2031 as payers incentivize same-day discharge. These centers embrace compact ultrasound-based vacuum systems and portable 3-Tesla MRI units calibrated for extremity and breast applications, lowering upfront costs. Diagnostic-imaging clinics bridge the gap by offering biopsy services under radiologist supervision, an arrangement that is popular in Southern Europe where private insurers reimburse bundled imaging-plus-biopsy packages. As outpatient volumes rise, vendors re-engineer devices for quick sterilization turnaround and develop cloud dashboards that auto-populate electronic health records, ensuring their relevance across all Europe biopsy devices industry segments.

Geography Analysis

Germany led the Europe biopsy devices market with 22.55% share in 2025, supported by universal statutory insurance, early MDR adoption, and swift reimbursement updates to finance AI-augmented pathology workflows. The market benefits from centralized procurement linked to digital quality registries that track adverse events and resource use. Hospitals in Munich and Berlin piloted 7-Tesla MRI biopsies in 2025, setting a technology benchmark that neighboring countries often follow. Federal health policy prioritizes medical-technology innovation, ensuring capital budgets for device refresh cycles.

The United Kingdom remains a pivotal market despite post-Brexit regulatory divergence. The Medicines and Healthcare products Regulatory Agency (MHRA) fast-tracks innovative diagnostic tools under the Innovative Devices Access Pathway, smoothing adoption of AI-guided biopsy consoles. France maintains steady demand through national cancer-control plans that guarantee screening budgets, although purchasing is centralized under the Union des Hôpitaux pour les Achats. Italy shows regional heterogeneity; northern provinces mirror German adoption curves, whereas southern regions lean on EU cohesion funds for equipment upgrades.

Spain is the fastest-growing market at 6.24% CAGR, propelled by digital-health investments and expanded screening in underserved autonomous communities. The RedETS health-technology assessment framework now evaluates biopsy devices quarterly, shortening time-to-approval and improving transparency. Nordic countries, though smaller in population, command high per-capita spending on MRI-guided systems and thus represent profitable niches for premium-priced platforms. Central and Eastern European nations use EU structural funds to modernize oncology centers, offering vendors a multiyear pipeline of tenders tied to milestone funding tranches. Collectively, these dynamics ensure the Europe biopsy devices market maintains a resilient growth outlook across macro-economic cycles.

Regulatory Landscape

Biopsy devices marketed in Europe fall under the EU Medical Device Regulation (MDR) (EU) 2017/745, with conformity assessment conducted by designated notified bodies and supported by clinical evaluation, quality management system evidence, and UDI-based traceability. Implementation actions in 2026 add further structure to notified-body conformity assessment: Implementing Regulation (EU) 2026/977 introduces uniform quality management and procedural requirements for notified-body conformity assessment activities, applying from 25 February 2027 (with certain provisions from 1 January 2028). These changes reinforce the compliance burden that has contributed to longer certification timelines and portfolio rationalization, particularly among smaller suppliers.

Technical compliance is also influenced by periodic updates to harmonised standards listed in the Official Journal. In June 2026, Implementing Decisions (EU) 2026/1231 and (EU) 2026/1313 updated harmonised standards for MDR and IVDR, including adding EN 60601-1:2006/A13:2024 for basic safety and essential performance of electrically powered medical devices, which is relevant for biopsy systems with powered handpieces, consoles, or accessories. Alongside MDCG guidance and EU borderline/classification references, these updates shape documentation, testing, and post-market expectations that affect procurement decisions, including preferences for MDR-certified, well-supported platforms in hospitals and ambulatory settings.

Competitive Landscape

The Europe biopsy devices market is moderately concentrated. Global players such as BD, Hologic, and B. Braun sustain advantage through broad catalogues and MDR-compliant quality files, while regional specialists focus on vacuum systems or robotic guidance. Recalls have heightened customer focus on supplier reliability; hospitals now reward vendors that can document cycle-time analytics and adverse-event response protocols. Strategic alliances proliferate: BD teamed with Techcyte to deliver AI-powered cervical-cytology platforms to European labs in 2024, and it is co-developing flow-cytometry companion diagnostics with Quest Diagnostics for oncology drugs.

M&A activity intensifies portfolio breadth. Teleflex agreed in February 2025 to buy BIOTRONIK’s vascular-intervention unit, adding drug-coated balloons that complement its biopsy access sheaths. Firms also file more patents at the European Patent Office covering sensor-embedded needles, vacuum-assisted seal mechanisms, and cloud-based procedure-tracking dashboards. Pricing remains stable because MDR barriers restrict new entrants, but buyers use multi-year framework agreements to negotiate bundled service packages. Over 2025-2030, competition will hinge on AI integration, robotics compatibility, and speed of MDR recertification.

Europe Biopsy Devices Industry Leaders

Becton, Dickinson and Company

Boston Scientific Corporation

Argon Medical Devices

Hologic Inc

Cook Medical

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The main opportunities center on workflow standardization, outpatient migration, and precision enablement technologies that can reduce repeat sampling while aligning with MDR-driven procurement preferences. In high-volume markets such as Germany, tenders increasingly specify single-use, vacuum-assisted systems to reduce reprocessing validation workload and liability exposure, which creates whitespace for vendors that can pair disposable platforms with reliable supply and training support for ambulatory surgical centers and imaging clinics. There is also scope for suppliers that can demonstrate traceability and post-market responsiveness after widely publicized safety actions in the broader biopsy ecosystem, which has pushed buyers toward vendors with stronger quality systems and batch-level visibility.

AI-assisted guidance and robotics provide a differentiation track beyond incremental needle design. In May 2026, the EU-funded ROBIOPSY project reported completion of the REGOLUS prototype, a semi-automatic AI-enabled robotic platform for prostate biopsy, highlighting active European R&D aimed at reducing operator variability and improving targeting in MRI-fusion and image-guided workflows. Clinical adoption pathways also benefit from accumulating evidence for newer needle formats, including a March 2026 first-in-human European experience publication for Cook Medicals 22-G EchoTip ClearCore fine-needle biopsy system, which supports broader use cases where clinicians seek improved core acquisition with smaller gauges. At the system level, EU4Health-aligned efforts such as PRAISE-U and related screening protocol deployments support standardizing transperineal and imaging-guided biopsy approaches across member states, underpinning demand for compatible device kits, guidance accessories, and training infrastructure.

Recent Industry Developments

- April 2026: Boston Scientific announced a EUR 75 million investment to expand research and development capabilities in Galway, Ireland. The expansion increases European-based engineering capacity for advanced interventional and imaging-adjacent device development, supporting regional responsiveness for product iteration and lifecycle compliance.

- July 2025: Argon Medical Devices opened a new Distribution and Education Center in Derby, United Kingdom, to serve operations across Europe, Africa, the Middle East, and Asia-Pacific. The facility adds localized logistics and clinical education capacity, improving product availability and procedural training coverage for biopsy and related interventional portfolios.

- September 2024: Argon Medical Devices launched the TLAB Transvenous Liver Biopsy System, enabling liver biopsy sample collection via femoral vein access. The system expands biopsy options for patients who are poor candidates for percutaneous approaches, supporting adoption in tertiary centers managing complex hepatology and oncology caseloads.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the Europe biopsy devices market covers devices used to collect tissue samples for diagnostic examination, including the related single use tools and reusable systems that directly enable tissue acquisition in clinical settings.

Scope exclusions: Liquid biopsy tests and reagents, standalone imaging systems, and lab automation equipment that does not perform tissue acquisition are excluded.

Segmentation Overview

- By Product

- Needle-based Biopsy Instruments

- Core Biopsy Devices

- Aspiration Biopsy Needles

- Vacuum-assisted Biopsy Devices

- Procedure Trays

- Localization Wires

- Other Products

- Needle-based Biopsy Instruments

- By Application

- Breast Biopsy

- Lung Biopsy

- Colorectal Biopsy

- Prostate Biopsy

- Other Applications

- By End User

- Hospitals

- Diagnostic & Imaging Centers

- Ambulatory Surgical Centers

- Others

- Geography

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set market boundaries, build a clean country roll-up for Europe, and form an initial view of procedure demand and pricing logic. We referred to public health statistics and disease burden sources such as WHO Europe, OECD health data, and national ministries of health to capture signals on screening, diagnosis, and oncology service utilization.

To connect that demand view to devices, we also reviewed European Commission medical device regulation updates, customs and trade statistics (where relevant for medical instruments), and peer reviewed clinical journals that describe biopsy technique adoption and changes in practice. Company annual reports, investor presentations, and press releases helped cross-check product coverage and revenue exposure, and a paid subscription database was used for company financials and patent landscape screening to validate product mix trends. This list is not exhaustive, and many other public and paid sources were also reviewed to collect data points, clarify assumptions, and validate findings.

Primary Interviews and Surveys

Primary work focused on speaking with stakeholders who see procedure mix and purchasing decisions closely, such as hospital procurement teams, pathology and radiology department users, distributors, and device specialists. We used these discussions to confirm what gets counted as a biopsy device in practice, how average selling prices change between disposable-led setups and reusable systems, and how demand differs across major European care settings.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 13% | |

| Mid tier: 59% | Functional/Unit leaders: 30% | |

| Smaller Players: 14% | Managers: 57% |

Market-Sizing & Forecasting

Market sizing was first built using a top-down demand pool approach where procedure volumes and care setting mix were reconstructed from public health indicators, and then translated into device value using utilization and pricing assumptions. To keep totals grounded, we corroborated the outputs with selective bottom-up checks, including sampled ASP by device category, distributor channel checks, and supplier revenue exposure to Europe. Where the two views did not line up, we adjusted the model.

Inputs that mattered in the model included the mix of image-guided biopsies versus surgical approaches, the shift toward minimally invasive sampling, disposable attach rates per procedure, typical replacement cycles for reusable systems, and country-level differences in reimbursement and hospital budget timing. Where direct procedure data was patchy, we filled gaps using proxy indicators like oncology diagnostic workloads and population age bands, then rechecked those assumptions with interview feedback.

Forecasting relied mainly on scenario analysis so growth could be tied to practical drivers that experts can validate, such as procedure growth, setting shifts toward outpatient care, and price changes linked to product mix. The scenario outputs were reviewed against recent adoption trends discussed by interviewees, so the forecast stayed realistic rather than aggressive.

Data Validation & Update Cycle

Results were validated by comparing model outputs with independent signals, including country-level health spending patterns, procedure trend direction from public sources, and company commentary on regional performance. Outliers were flagged, assumptions were rechecked, and when a variance could not be explained, respondents were recontacted for clarification before sign off.

Each report is refreshed annually, and interim updates are made when material events occur, such as regulation changes or major pricing shifts. Before delivery, a final review pass is completed so the client receives the latest updated view based on the most recent available information.

Mordor Intelligence's Europe Biopsy Devices Market Market Sizing Compared With Other Published Estimates

Published market sizes for Europe biopsy devices often do not match, and the gap is usually linked to what each publisher counts as a device, the year used as the base, and how prices are converted and carried forward.

The table shows a tight cluster around the mid hundreds of millions. In Mordor Intelligence's model, the value is limited to tissue acquisition devices and their dedicated guidance accessories, so items like liquid biopsy reagents, standalone imaging consoles, and lab automation are not added into the total even when they are used in the same diagnostic pathway.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 623.89 M (2025) | |

| Industry Publisher A | USD 629.60 M (2024) | Uses a different base year and a broader market framing that can bundle guidance systems and procedure scope more widely, which can shift totals even if Europe coverage looks similar. |

| Healthcare Analytics B | USD 594.73 M (2024) | Provides limited visibility on inclusions and exclusions, and the lower value may reflect a narrower product list or a more conservative pricing assumption for disposables versus reusable systems. |

Across the three figures, the main spread comes from scope choices and the practical steps used to convert procedures and product mix into revenue, especially around what is treated as a device versus an adjacent diagnostic input. By keeping the counted items tied to tissue acquisition and validating pricing and utilization through interviews, the estimate stays traceable to clear drivers that can be repeated and rechecked.

Key Questions Answered in the Report

What is the Europe biopsy devices market size and its expected growth?

The market is valued at USD 648.16 million in 2026 and is projected to reach USD 784.39 million by 2031, reflecting a 3.89% CAGR

Which product segment holds the largest share?

Needle-based biopsy instruments commanded 47.62% of revenue in 2025 and are set to grow at an 7.89% CAGR through 2031

What main factors are boosting demand for biopsy devices in Europe?

EU-wide cancer-screening targets, rising preference for minimally-invasive procedures, and the shift toward ambulatory centers are driving steady device uptake

How is the EU Medical Device Regulation (MDR) influencing market dynamics?

Tougher certification requirements and limited notified-body capacity are prompting some firms to trim portfolios, creating short-term supply gaps but raising quality standards

Which country is forecast to grow the fastest?

Spain is expected to post the highest national CAGR at 6.24% between 2026 and 2031, thanks to healthcare digitization and expanded screening programs

Page last updated on: