Breast Cancer Liquid Biopsy Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

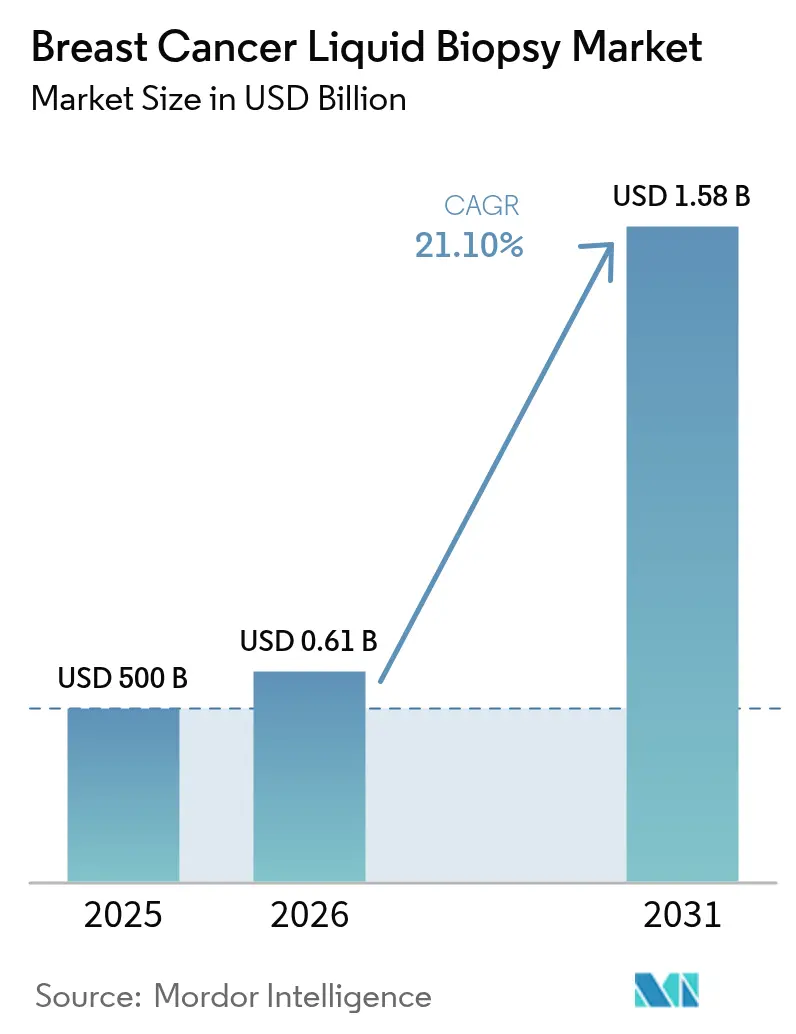

| Market Size (2026) | USD 0.61 Billion |

| Market Size (2031) | USD 1.58 Billion |

| Growth Rate (2026 - 2031) | 21.10% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Breast Cancer Liquid Biopsy Market Analysis by Mordor Intelligence

Breast cancer liquid biopsy market size in 2026 is estimated at USD 605.5 million, growing from 2025 value of USD 500 million with 2031 projections showing USD 1.58 billion, growing at 21.10% CAGR over 2026-2031. Adoption accelerates as physicians switch from tissue sampling to blood-based molecular profiling, helped by FDA guidance that recognizes circulating tumor DNA (ctDNA) as an aid for early-stage drug development. Liquid biopsy-guided treatment now delivers clear survival gains, and reimbursement expansions in the United States have lifted per-test payment to USD 1,495, improving commercial viability. Asia-Pacific laboratories are scaling multi-omics workflows that pool genomic, epigenomic and protein data, setting a precedent for population-level screening. Competitive positioning centers on assay sensitivity: precision-scaled ctDNA tests and AI-driven data analytics cut false-negative rates, which broadens use in minimal residual disease (MRD) management and augments the attractiveness of the breast cancer liquid biopsy market for investors.

Key Report Takeaways

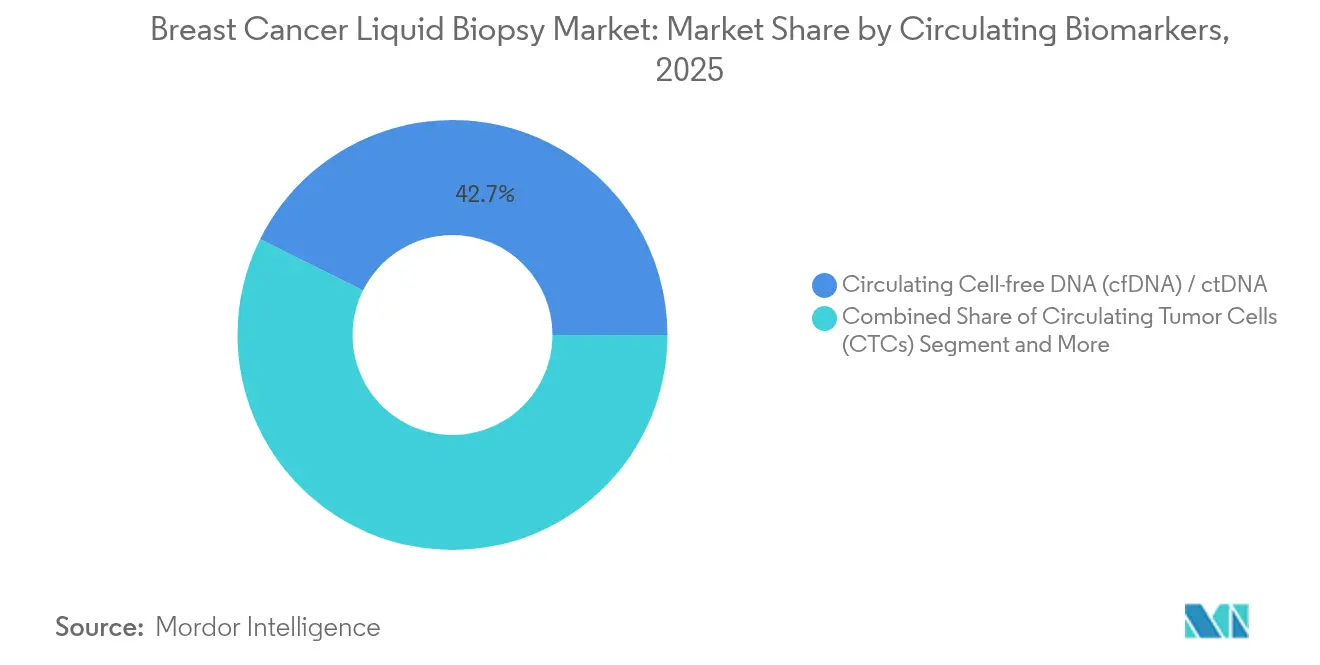

- By circulating biomarker, cfDNA/ctDNA held 42.65% of the breast cancer liquid biopsy market share in 2025, while extracellular vesicles and exosomes are projected to grow at a 22.79% CAGR through 2031.

- By product & service, reagent kits and consumables commanded 44.85% share of the breast cancer liquid biopsy market size in 2025; service offerings are forecast to expand at a 22.88% CAGR to 2031.

- By technology, next-generation sequencing led with 64.10% revenue share in 2025; digital droplet PCR is advancing at a 24.18% CAGR through 2031.

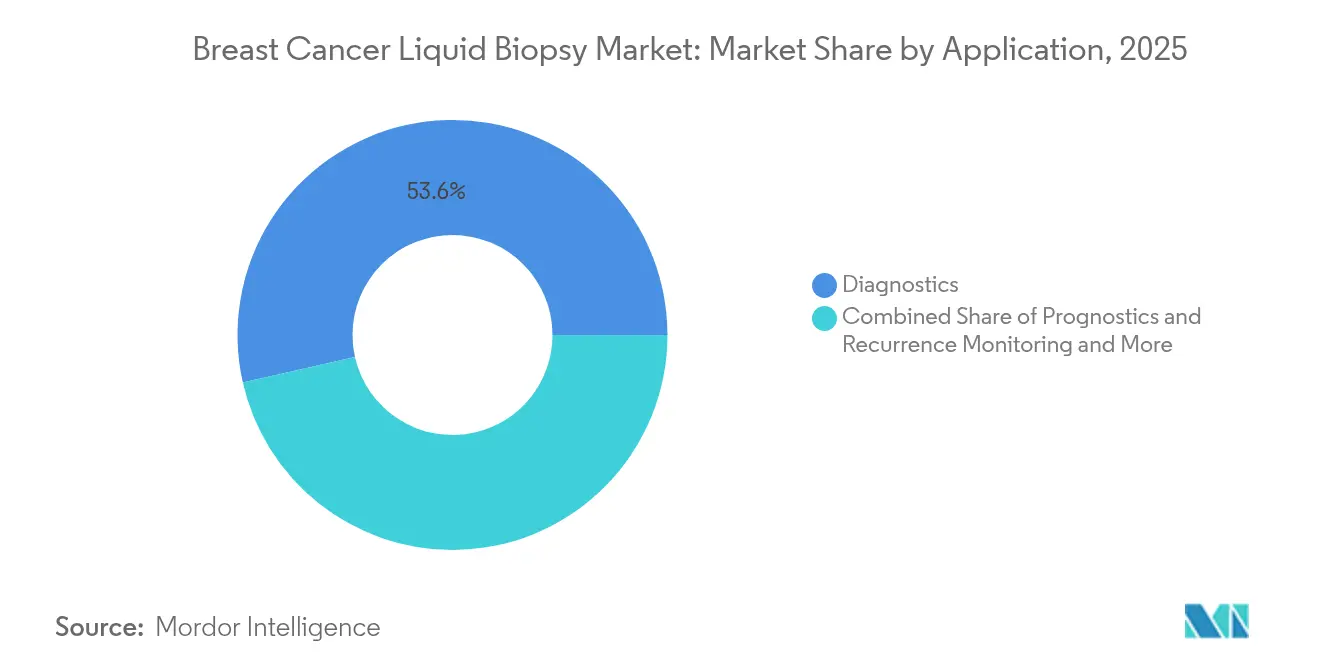

- By application, diagnostics generated 53.55% revenue in 2025, whereas MRD monitoring is expected to record a 22.19% CAGR from 2026-2031.

- By end user, hospital and physician laboratories held 34.70% share in 2025, but reference laboratories will rise fastest at a 22.95% CAGR to 2031.

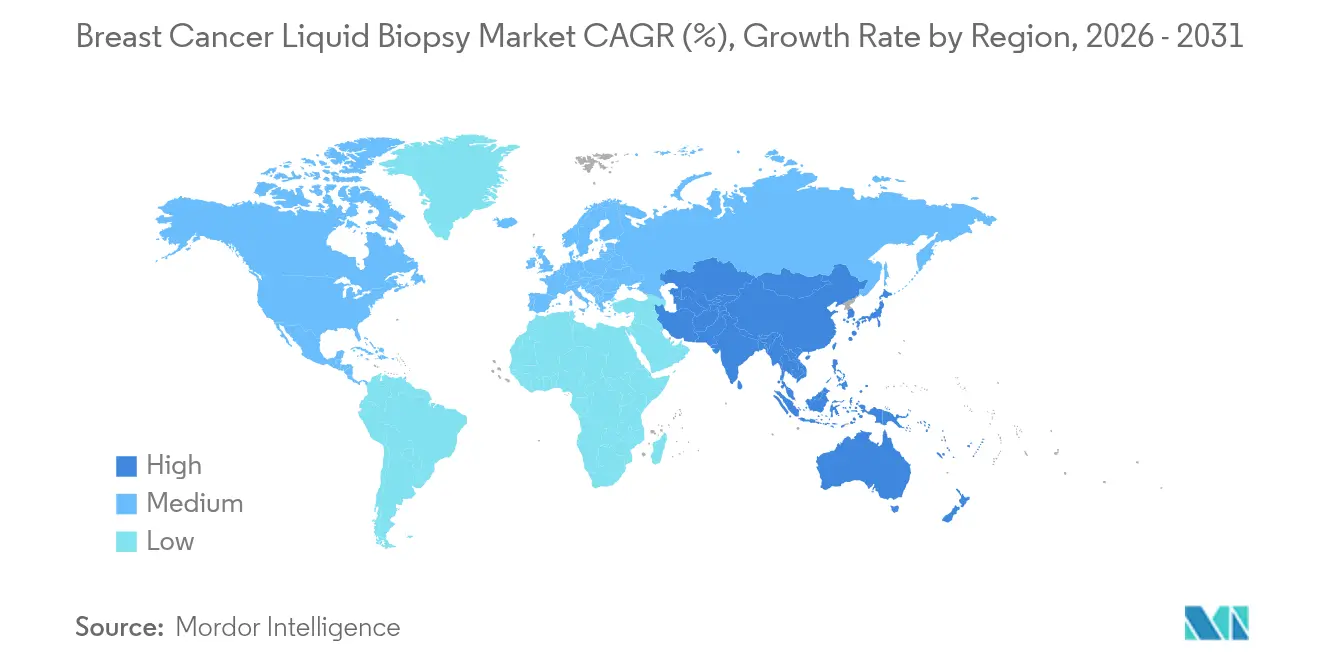

- By geography, North America captured 37.95% revenue in 2025; Asia-Pacific shows the quickest uptick, expanding at a 22.75% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Breast Cancer Liquid Biopsy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Precision-Scaled cfDNA Assays Slash False-Negatives | +4.2% | Global, with early adoption in North America & EU | Medium term (2-4 years) |

| AI-Guided Multi-Omics Panels Enter Routine Screening | +3.8% | North America & EU core, spill-over to APAC | Long term (≥ 4 years) |

| Rising Prevalence Of Breast Cancer | +2.1% | Global | Long term (≥ 4 years) |

| Demand For Minimally Invasive Diagnostics | +3.5% | Global | Short term (≤ 2 years) |

| Rapid Reimbursement Expansion In OECD Economies | +4.1% | North America & EU, selective OECD markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

AI-guided multi-omics panels enter routine screening

AI brings together genomic, epigenomic and RNA information in a single blood draw, allowing laboratories to classify ER, PR and HER2 status without tissue. Smart liquid biopsy applications already subtype breast tumors with 99.5% specificity, which reduces reliance on surgical sampling. Algorithms also flag structural variants and methylation patterns, helping clinicians identify resistance pathways months before standard imaging picks them up. Clinical datasets show that recurring disease can be signaled 10.81 months ahead of radiology, giving oncologists time to adjust therapy. As payers see the value of earlier intervention, reimbursement frameworks increasingly support multi-omics panels, accelerating growth of the breast cancer liquid biopsy market.

Precision-scaled cfDNA assays slash false negatives

High-volume blood draws and ultrasensitive workflows detect ctDNA almost universally in pre-treatment samples, overcoming historical sensitivity gaps[1]Alba E., “Increased blood draws for ultrasensitive ctDNA and CTCs detection in early breast cancer patients,” nature.com. Digital droplet PCR spots ESR1 mutations at very low allele frequencies, guiding endocrine therapy selection. FDA guidance released in 2024 sets uniform standards for assay validation, which narrows inter-laboratory variability. Tumor-informed methods compare new blood samples to a patient’s baseline genomic profile, pushing detection thresholds even lower. When ctDNA changes trigger therapy adjustments—as shown in the SERENA-6 trial—progression risk falls by 56%, underscoring clinical value and strengthening the business case for the breast cancer liquid biopsy market.

Rising prevalence of breast cancer

Incidence continues to climb worldwide, particularly in middle-income countries that lack dense imaging infrastructure. Aging populations in high-income regions further enlarge the at-risk cohort. Liquid biopsy sidesteps the skilled-labor bottlenecks of mammography and surgical biopsy, making large-scale programs feasible. Screening programs in urban China now weave plasma tests into routine checkups, while Japan’s genome initiative banks samples for longitudinal study. The sheer number of potential beneficiaries underpins sustained expansion of the breast cancer liquid biopsy market.

Demand for minimally invasive diagnostics

Blood-based tests cut risk, discomfort and recovery time compared with surgical sampling, lifting patient willingness to undergo repeat monitoring. Turnaround from collection to result averages 3 days in community hospitals, which supports timely treatment decisions. Higher acceptance rates improve trial enrollment and follow-up compliance. For elderly patients or those with co-morbidities, a simple venous draw broadens access to precision oncology. These advantages keep the breast cancer liquid biopsy market on a strong growth trajectory.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Patchy Reimbursement In Emerging Economies | -2.8% | Latin America, Africa, Middle East, selective APAC | Long term (≥ 4 years) |

| High Per-Test Cost Vs. Tissue Biopsy | -3.2% | Global, acute in price-sensitive markets | Medium term (2-4 years) |

| Limited Clinical Evidence For Early-Stage Benefit | -1.9% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High per-test cost versus tissue biopsy

List prices ranging from USD 949 to more than USD 3,000 create budget pressure, especially where payers reimburse tissue assays at USD 500-1,000. Cost-effectiveness studies show value in earlier recurrence detection, yet many emerging markets need sharply lower pricing to meet health-economic thresholds. Sequential tissue-plasma strategies are sometimes preferred to curb overall expense, delaying wide adoption of stand-alone liquid biopsy in cost-sensitive geographies and tempering growth of the breast cancer liquid biopsy market.

Limited clinical evidence for early-stage benefit

Sensitivity drops when ctDNA levels are extremely low, and randomized trials that tie early intervention to better survival are still underway. Regulators and payers want proof that ctDNA-guided changes improve outcomes without exposing patients to unnecessary treatment. Until large-scale studies close this evidence gap, some clinicians reserve liquid biopsy for advanced disease or MRD monitoring, slowing uptake in broad screening and limiting immediate upside for the breast cancer liquid biopsy market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Circulating Biomarkers: cfDNA leadership and exosome momentum

cfDNA and ctDNA accounted for 42.65% of the breast cancer liquid biopsy market share in 2025, cementing their role as the anchor biomarkers for clinical decision making. Companion diagnostic approvals that target PIK3CA mutations have validated their therapeutic relevance, encouraging wider insurer coverage. Extracellular vesicles and exosomes post the fastest growth at a 22.79% CAGR, as their cargo of proteins and nucleic acids captures tumor heterogeneity unseen in cfDNA alone. Investigators now use four-miRNA panels in HER2-positive vesicles to achieve 88% classification accuracy. This multi-marker versatility underlines why the breast cancer liquid biopsy market values novel vesicle assays and predicts sustained double-digit expansion.

A multi-analyte future looms. Circulating tumor cells still provide prognostic power through enumeration metrics, and automated microfluidic systems raise capture efficiency toward 92%. miRNA and protein signatures complement nucleic acid tests, improving early detection where cfDNA copies are sparse. Combining these readouts in a single report improves diagnostic certainty, positioning full-spectrum platforms as favored options for oncologists looking to limit follow-up procedures. Hybrid strategies therefore deepen penetration of the breast cancer liquid biopsy market and widen the addressable clinical scenarios.

By Product & Service: Consumables dominance but services surge

Reagent kits and consumables represented 44.85% of the breast cancer liquid biopsy market size in 2025, mirroring the routine need for plasma stabilization tubes and extraction reagents each time blood is collected. Yet complex analytics push healthcare providers to outsource, making services the quickest riser at a 22.88% CAGR through 2031. Central laboratories promise 14-day MRD turnaround and can handle 700-plus gene panels, a workload most hospitals cannot support in-house. This outsourcing trend places service providers at the heart of the breast cancer liquid biopsy market.

Instrument demand holds steady as laboratories modernize. Next-generation sequencers with higher throughput reduce per-sample cost, while cloud software packages enable AI-assisted variant calling. Point-of-care devices gain traction in community centers for single-mutation tracking, but large-scale profiling still migrates to centralized hubs. Data-as-a-service offerings bundle test results with longitudinal analytics, giving oncologists actionable dashboards without database management tasks, reinforcing the gravitation of revenue to service players within the breast cancer liquid biopsy market.

By Technology: NGS strength challenged by digital PCR

Next-generation sequencing controlled 64.10% of revenue in 2025, offering simultaneous analysis of hundreds of genes and structural variants. Panel updates now include RNA fusion detection and methylation readouts, broadening utility. Digital droplet PCR grows at 24.18% CAGR as it excels in pinpointing single mutations at allele fractions below 0.1%, which is ideal for monitoring resistance drivers like ESR1. Hospitals often use PCR for high-frequency surveillance between periodic NGS assessments, a complementary approach that intensifies overall testing volume inside the breast cancer liquid biopsy market.

Hybrid technology strategies emerge. Oxford Nanopore long-read sequencing improves structural variant mapping, and microarrays simplify gene-expression profiling at lower cost. Instrument makers integrate AI modules that filter sequencing noise, trimming false-positive rates and boosting clinician confidence. As test performance rises, competitive differentiation shifts toward workflow efficiency and reimbursement support, sustaining broad growth prospects for the breast cancer liquid biopsy market.

By Application: Diagnostics lead, MRD monitoring accelerates

Diagnostics functions, including first-line mutation profiling and subtyping, generated 53.55% of revenue in 2025. Hospitals rely on cfDNA to determine PIK3CA status when tissue is scarce or quality is poor. MRD monitoring climbs fastest at a 22.19% CAGR as studies show that ctDNA positivity predicts recurrence well before imaging. The breast cancer liquid biopsy market size for MRD testing is projected to rise sharply as payers authorize serial monitoring protocols for high-risk patients.

Companion diagnostics benefit as the FDA expands liquid biopsy labels attached to targeted therapies. Prognostics and recurrence surveillance become routine through longitudinal ctDNA tracking, allowing oncologists to escalate or de-escalate treatment quickly. The combination of earlier detection and tailored therapy cements liquid biopsy as a core precision-oncology tool, driving steady share gains across multiple application layers inside the breast cancer liquid biopsy market.

By End User: Reference laboratories leverage specialization

Hospital and physician labs retained 34.70% revenue in 2025, but reference laboratories show the highest momentum at 22.95% CAGR. Sophisticated bioinformatics pipelines and quality systems set stringent resource barriers that regional labs solve by partnering with centralized facilities. When reference groups place technicians inside partner hospitals, they combine on-site phlebotomy with remote analytics, ensuring sample integrity while keeping turnaround short. This hybrid model strengthens their stake in the breast cancer liquid biopsy market.

Academic centers conduct pivotal trials and often pilot new biomarkers before commercial release, influencing guideline changes that reshape ordering practices. Community clinics adopt point-of-care assays for follow-up mutation checks, proving particularly useful in rural settings. As stakeholders coordinate across networks, data interoperability standards become a competitive requirement, cementing a service-centric architecture for the breast cancer liquid biopsy market.

Geography Analysis

North America commanded 37.95% of revenue in 2025, propelled by Medicare policies that reimburse multi-cancer detection at USD 1,495 and extend coverage to MRD monitoring in colorectal cancer, paving the way for breast indications. FDA guidance endorses ctDNA for early-stage drug development, and companion diagnostic approvals for PIK3CA mutations foster clinician trust. Over 12,000 oncologists have integrated liquid biopsy into decision making, underlining clinical mainstreaming in the region and anchoring the breast cancer liquid biopsy market.

Europe ranks second, benefiting from In Vitro Diagnostic Regulation certification that allows Guardant360 CDx to report 74-gene profiles across the bloc with 7-day turnaround. Harmonization efforts by the European Liquid Biopsy Society are writing standardized protocols, while national payers explore value-based purchasing linked to outcome data. Cross-border research consortia boost sample volumes for early detection studies, bolstering evidence needed for coverage expansion. This supportive environment advances the breast cancer liquid biopsy market across Europe.

Asia-Pacific posts the fastest projected growth at 22.75% CAGR. Japan’s national genome initiative will analyze 100,000 cancer genomes, and clinical societies have published MRD testing guidelines that encourage routine ctDNA monitoring. China incorporates plasma assays into provincial precision-medicine programs, backed by state quotas for genomic sequencing. Sequential tissue-plasma strategies are cost-effective in many Asian payers’ analyses, opening reimbursement pathways. High population density and rising disposable income amplify the revenue outlook for the breast cancer liquid biopsy market.

Middle East face slower uptake owing to patchy insurance and limited molecular lab capacity. Yet Gulf Cooperation Council states invest in BRCA and HER2 testing hubs, and select private systems in Brazil have adopted multi-cancer detection to differentiate oncology service lines. Partnerships with established North American vendors provide technology transfers and training, gradually extending reach of the breast cancer liquid biopsy market into these regions.

Competitive Landscape

Competition bases on assay breadth, analytical sensitivity and clinical evidence rather than price alone. Guardant Health leads with FDA-approved cfDNA tests covering 80-plus genes and holds extensive survival data from the GOZILA study. Foundation Medicine leverages Roche distribution to bundle tissue and blood profiling, appealing to centers wanting a single vendor. Illumina, Thermo Fisher Scientific and QIAGEN add liquid biopsy panels to complement sequencing hardware, underscoring convergence of instrumentation and clinical testing in the breast cancer liquid biopsy market.

Startups deploy AI to reinterpret raw sequencing output, pitching higher specificity in early-stage disease. Exact Sciences entered MRD with Oncodetect and plans a multi-cancer Cancerguard panel, signaling that scale players are aligning behind longitudinal monitoring[3]Exact Sciences, “Exact Sciences Launches the Oncodetect Molecular Residual Disease Test,” exactsciences.com. Strategic partnerships multiply: Guardant and ConcertAI integrate clinical data streams, while reference labs forge co-development deals to accelerate regulatory filings. Mergers and licensing transactions focus on exosome isolation kits and methylation sequencing know-how, enriching technology pipelines across the breast cancer liquid biopsy market.

Competitive narratives also center on payer engagement. Companies with robust health-economic dossiers gain faster formulary placement. Those able to negotiate ADLT status or country-wide tariff codes enjoy durable pricing power. The result is a moderately concentrated landscape where top firms combine double-digit R&D intensity with commercialization networks that span academic, hospital and reference-lab channels, supporting sustainable growth of the breast cancer liquid biopsy market.

Breast Cancer Liquid Biopsy Industry Leaders

F. Hoffmann-La Roche Ltd

Bio-Rad Laboratories

QIAGEN N.V.

Illumina Inc.

Guardant Health Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Guardant Health reported SERENA-6 Phase III results showing a 56% reduction in disease progression when camizestrant was initiated following ESR1 mutation detection by Guardant360 CDx.

- April 2025: Guardant Health launched Guardant360 Tissue, delivering multi-omic profiling of 742 DNA and 367 RNA genes using fewer slides than standard tissue assays.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the breast cancer liquid biopsy market as every analytical service or kit that detects, enumerates, or characterizes circulating tumor-derived material originating from breast malignancies in easily accessible biofluids (chiefly blood and plasma) for screening, diagnosis, therapy selection, minimal residual disease tracking, and recurrence surveillance. The universe covers reagents, instruments, and outsourced test services that rely on biomarkers such as cfDNA/ctDNA, circulating tumor cells, and extracellular vesicles.

Scope exclusion: Tissue-based core, fine-needle, or surgical biopsies and liquid assays intended solely for non-breast cancers remain outside our numbers.

Segmentation Overview

- By Circulating Biomarkers

- Circulating Tumor Cells (CTCs)

- Circulating Cell-free DNA (cfDNA) / ctDNA

- Extracellular Vesicles (EVs) / Exosomes

- Other Biomarkers (miRNA, proteins)

- By Product & Service

- Reagent Kits & Consumables

- Instruments & Software

- Services (Testing, Data)

- By Technology

- Next-Generation Sequencing (NGS)

- Digital / Droplet PCR

- Other Technologies (Microarrays, Nanopore)

- By Application

- Diagnostics

- Prognostics & Recurrence Monitoring

- Therapy Selection / Companion Dx

- Minimal Residual Disease (MRD)

- By End-User

- Reference Laboratories

- Hospital & Physician Labs

- Academic & Research Centers

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed molecular pathologists, oncology clinicians, reference-lab managers, and reimbursement specialists across North America, Europe, and Asia-Pacific. Conversations validated adoption curves, kit utilization per patient pathway, and price erosion assumptions, while surveys with procurement officers clarified purchasing splits between consumables and service outsourcing.

Desk Research

We began with public datasets that quantify disease burden and testing volumes, such as WHO's Globocan incidence files, CDC and NCI-SEER registries, and Eurostat health accounts. Trade associations like the College of American Pathologists, the American Clinical Laboratory Association, and the European Federation of Clinical Chemistry provided laboratory throughput ratios and reagent consumption rates. Patent intelligence from Questel and company 10-Ks in D&B Hoovers helped us benchmark average selling prices. Select peer-reviewed articles on cfDNA assay sensitivity from PubMed filled technology efficacy gaps. This list is illustrative; many other open sources informed data gathering, cross-checks, and context setting.

Market-Sizing & Forecasting

We applied a top-down build starting with incident and prevalent breast cancer pools, overlaying liquid-biopsy test penetration by line of care, and multiplying by region-specific average price points that we corroborated through selective bottom-up roll-ups of leading-supplier revenues. Key variables include new case incidence, screening guideline shifts, reimbursement coverage breadth, kit price trajectories, and turnaround-time linked usage rates. Multivariate regression aligned historic adoption with shifts in these drivers and feeds our ARIMA forecast that projects values from 2025 to 2030, with gap filling through benchmark price-volume proxies where discrete data were sparse.

Data Validation & Update Cycle

Outputs pass three layers of internal review, anomaly checks against external market signals, and reconciliation with fresh expert feedback before sign-off. Updates occur annually, and an interim refresh is triggered when regulatory approvals, large clinical-guideline changes, or M&A events materially affect baselines.

Why Our Breast Cancer Liquid Biopsy Baseline Commands Reliability

Published figures differ because firms choose dissimilar biomarker baskets, assume varied test-penetration ramps, or refresh models at uneven intervals.

Key gap drivers include divergent inclusion of laboratory-developed tests, alternate currency conversion cut-offs, and optimistic versus conservative reimbursement uptake curves. Mordor's disciplined cycle, transparent scope, and dual-path validation temper both over- and under-estimation.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.50 B (2025) | Mordor Intelligence | - |

| USD 1.26 B (2025) | Global Consultancy A | Includes non-invasive tests for multiple solid tumors, assumes uniform global pricing |

| USD 1.34 B (2024) | Industry Portal B | Uses only revenue reported by listed companies, excludes in-house hospital labs |

| USD 0.23 B (2025) | Regional Consultancy C | Counts blood-based screening kits only, omits service revenues and ctDNA companion diagnostics |

Taken together, the comparison shows that when scope breadth, price normalization, and refresh cadence are harmonized, our baseline sits midway between aggressive and narrow estimates, giving decision-makers a balanced, reproducible starting point.

Key Questions Answered in the Report

What is a breast cancer liquid biopsy and how fast is the market growing?

A breast cancer liquid biopsy is a blood-based test that tracks circulating tumor DNA, tumor cells or exosome biomarkers to guide diagnosis and treatment; the global market is expected to expand from USD 500 million in 2025 to USD 1.58 billion by 2031, reflecting a 21.10% CAGR.

Which circulating biomarker platform currently dominates routine clinical use?

Circulating cell-free DNA and ctDNA assays hold the lead, accounting for 42.65% of global revenue in 2025 thanks to multiple FDA-approved companion diagnostics and strong analytical validity.

How are healthcare payers influencing adoption of liquid biopsy in breast cancer care?

North American payers reimburse multi-cancer detection tests at USD 1,495 per sample and have started covering minimal residual disease monitoring, accelerating physician uptake and commercial traction.

Why are reference laboratories growing faster than hospital-based testing sites?

Sophisticated multi-omics workflows and AI analytics exceed most hospital capabilities, prompting providers to outsource; reference labs are projected to rise at a 22.95% CAGR through 2031.

What technology trends should executives watch between now and 2031?

Next-generation sequencing remains the workhorse, but digital droplet PCR is advancing at a 24.18% CAGR for ultra-sensitive mutation detection, while AI-powered multi-omics panels promise earlier relapse identification.

Page last updated on: