Market Overview

| Study Period | 2020 - 2031 |

|---|---|

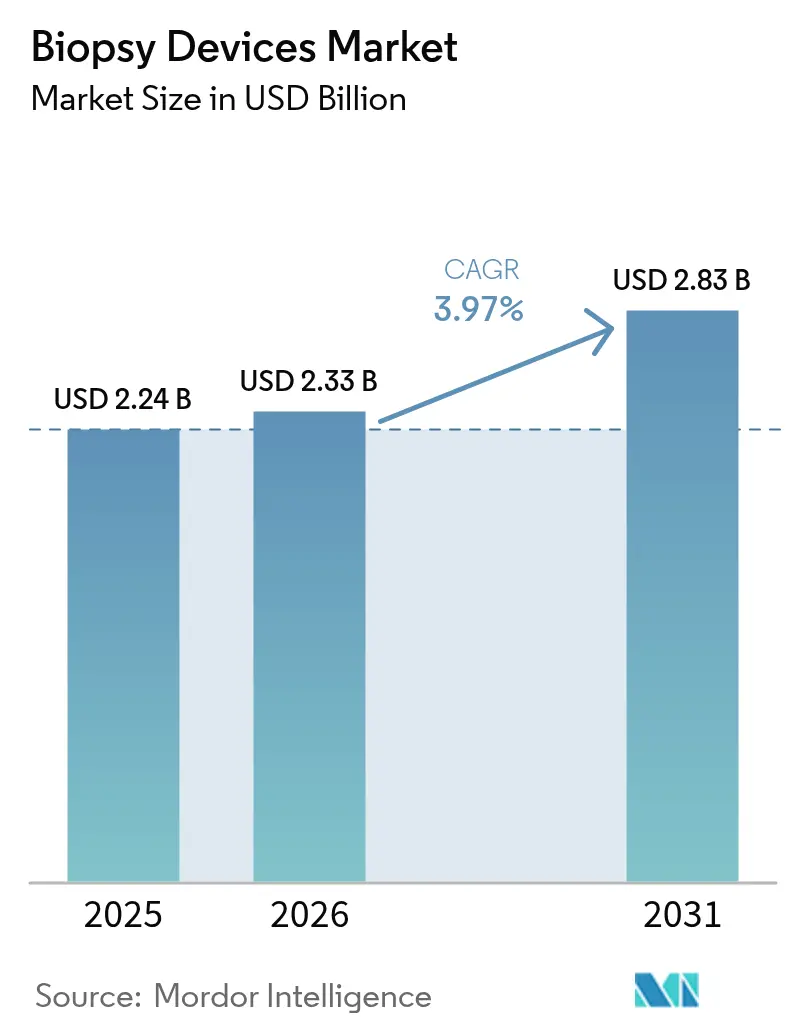

| Market Size (2026) | USD 2.33 Billion |

| Market Size (2031) | USD 2.83 Billion |

| Growth Rate (2026 - 2031) | 3.97% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Biopsy Devices Market Analysis by Mordor Intelligence

Biopsy devices market size in 2026 is estimated at USD 2.33 billion, growing from 2025 value of USD 2.24 billion with 2031 projections showing USD 2.83 billion, growing at 3.97% CAGR over 2026-2031. Demand is advancing steadily as hospitals, ambulatory centers, and diagnostic clinics expand early-cancer programs that hinge on tissue confirmation. Needle-based innovation, especially systems that mate vacuum technology with AI image guidance, is driving procedural efficiency and supporting a shift toward minimally invasive work-flows. Government-funded screening initiatives, such as Australia’s new lung program using bulk-billed low-dose CT, are pushing higher volumes of follow-up biopsies and reducing barriers to access. Meanwhile, the biopsy devices market faces headwinds from sterility-related recalls and the accelerating uptake of liquid-biopsy assays, factors that temper—but do not derail—its growth trajectory.

Key Report Takeaways

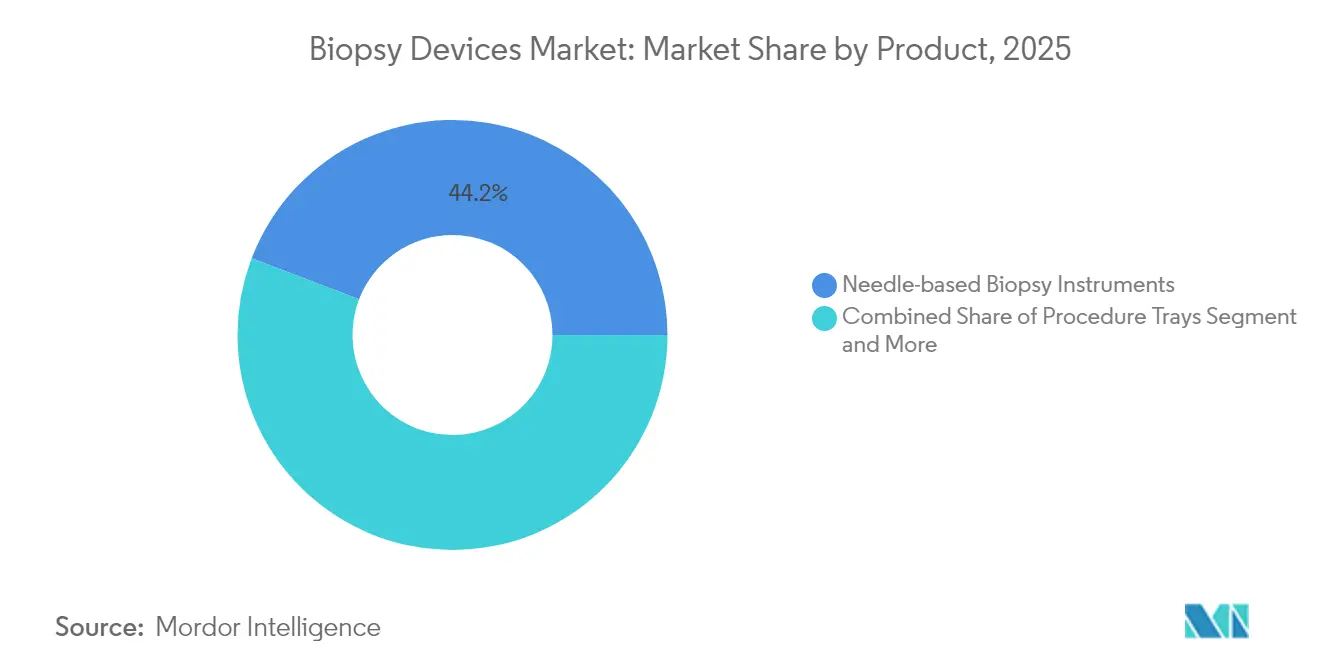

- By product type, needle-based systems led with 44.20% revenue share in 2025 and are projected to expand at an 8.12% CAGR through 2031.

- By application, breast procedures held 31.12% of the biopsy devices market share in 2025, while lung procedures are set to grow at a 9.02% CAGR through 2031.

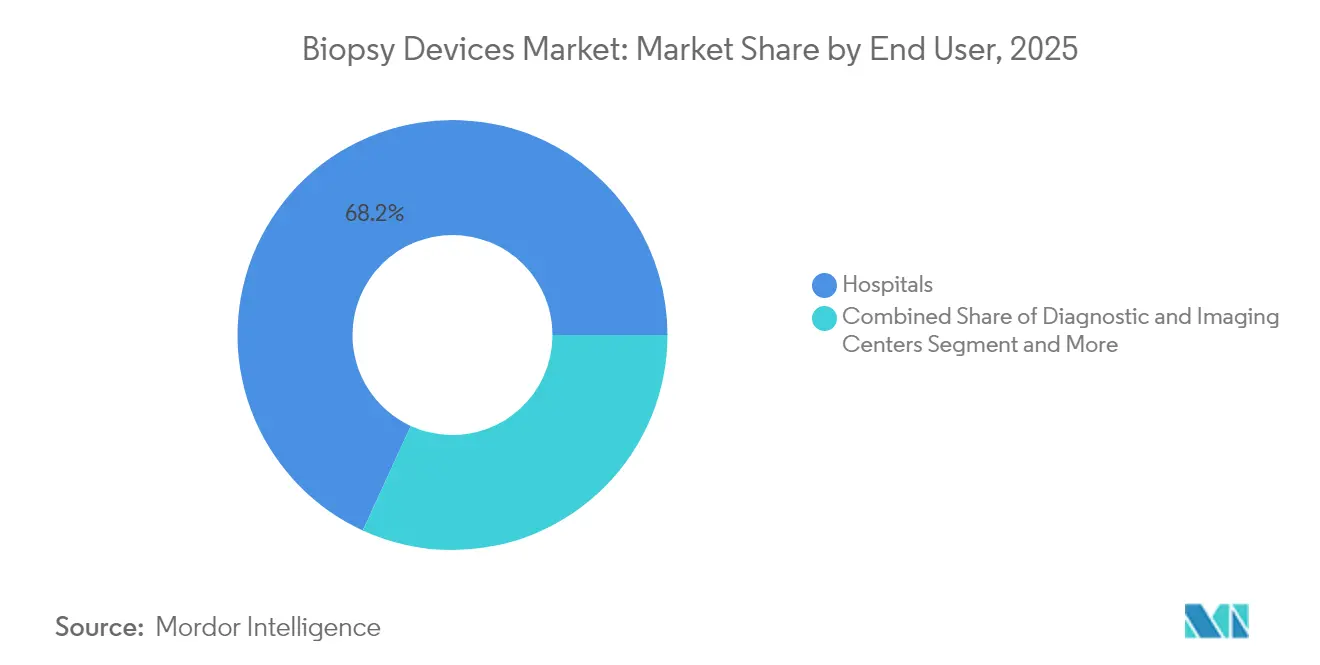

- By end-user, hospitals commanded 68.15% of the biopsy devices market size in 2025; ambulatory surgical centers represent the fastest-growing channel with a 9.18% CAGR to 2031.

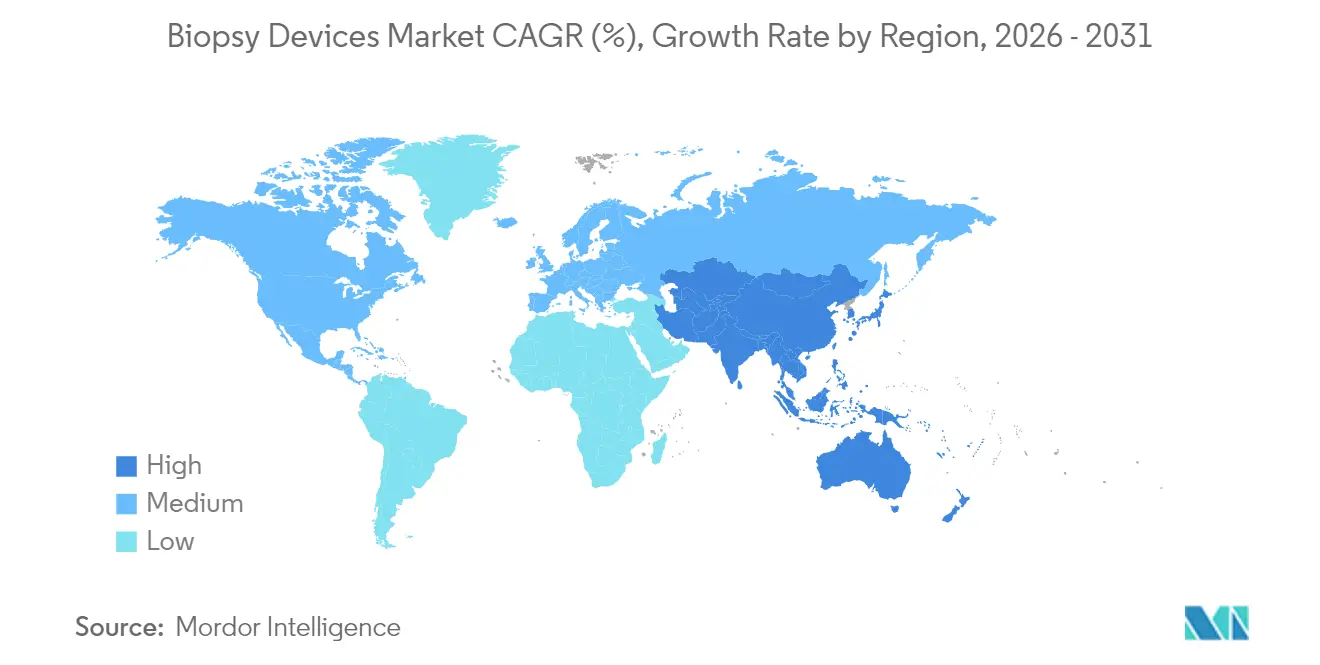

- By geography, North America accounted for 41.25% of 2025 revenue, whereas Asia-Pacific is forecast to post the highest regional CAGR at 8.25% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Biopsy Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for minimally invasive cancer diagnostics | +1.2% | Global | Medium term (2-4 years) |

| Growing incidence of hard-to-reach organ cancers | +0.8% | Global | Long term (≥ 4 years) |

| AI-enabled image guidance improves first-pass yield | +0.9% | North America & EU | Short term (≤ 2 years) |

| Expansion of government-funded screening programs | +0.7% | APAC core, North America | Medium term (2-4 years) |

| Growth of ambulatory surgical centers in emerging markets | +0.6% | APAC core | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand For Minimally Invasive Cancer Diagnostics

Nanoneedle patches developed at King’s College London allow painless tissue sampling by inserting millions of micro-needles that are 1,000 times thinner than human hair, enabling real-time monitoring without tissue damage. Parallel advances in pneumatically driven robotic catheters achieve six-direction sampling inside tortuous luminal organs, cutting procedure time and improving patient comfort. Clinics therefore increasingly favor less invasive hardware that minimizes complications and yields high-quality specimens, a key catalyst for the biopsy devices market worldwide. Health-system purchasers also note lower downstream costs from shorter recovery times and fewer repeat procedures, reinforcing adoption. As these technologies mature, suppliers that integrate robotic actuation and micro-sampling into cohesive platforms are gaining a competitive edge.

Growing Incidence Of Hard-To-Reach Organ Cancers

Lung cancer remains the world’s top cause of cancer mortality, representing 18.7% of global cancer deaths in 2024[1]World Health Organization, “Global cancer burden growing, amidst mounting need for services,” who.int. The anatomical obstacles of accessing lungs, pancreas, and brain heighten demand for precision needles, steerable catheter systems, and advanced imaging accessories. High-income nations report the greatest disease burden, yet emerging markets are witnessing rapid incidence growth without equivalent diagnostic capacity. Hospitals are therefore upgrading to image-guided core and vacuum-assisted devices that improve sampling accuracy and shorten anesthesia time—an investment pattern that sustains the biopsy devices market even as reimbursement regimes tighten.

AI-Enabled Image Guidance Improves First-Pass Yield

Perimeter Medical Imaging AI won FDA review for its B-Series OCT system that reduces re-excision rates in breast-conserving surgery by mapping margins intra-operatively. Clairity’s breast-risk platform and Olympus’s CADDIE colonoscopy software likewise secure U.S. clearances, showing regulators’ willingness to fast-track algorithms that enhance accuracy. In June 2025 the FDA published draft guidance outlining performance-monitoring, bias mitigation, and post-market expectations for AI devices, giving manufacturers clearer routes to approval. Early adopters see measurable gains in first-pass success, procedure time, and staff productivity, accelerating integration across radiology and operating rooms.

Expansion Of Government-Funded Screening Programs

Australia’s National Lung Cancer Screening Program, launched July 2025, offers bulk-billed low-dose CT for high-risk adults aged 50-70 and is expected to lift early-stage detection from 16% to 60%[2]Australian Government Department of Health, “About the National Lung Cancer Screening Program,” health.gov.au. The country also lowered bowel-screening eligibility to 45 years in 2024, widening the pool of positive findings that require tissue confirmation. In the United States, the National Cancer Institute’s new Screening Research Network will enroll up to 24,000 volunteers to test emerging multi-cancer assays. These initiatives funnel large screening cohorts into diagnostic pathways, lifting procedure volumes and ensuring recurring demand for biopsy instruments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Device recalls & sterility-failure events | -0.4% | Global | Short term (≤ 2 years) |

| Competition from liquid-biopsy technologies | -0.6% | North America & EU | Medium term (2-4 years) |

| Reimbursement pressure in high-volume markets | -0.3% | North America, EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Device Recalls & Sterility-Failure Events

Olympus withdrew single-use lung-biopsy sheaths after detachable tips caused 26 serious injuries, compelling hospitals to quarantine stock and reschedule procedures. Hologic’s Class I recall of 53,492 BioZorb markers followed reports of pain, infection, and migration. Cardinal Health likewise pulled biopsy-related procedure kits over sterility concerns. Such events intensify regulatory scrutiny, force costly remediation programs, and can dampen clinician confidence, thereby restraining near-term growth for the biopsy devices market.

Competition From Liquid-Biopsy Technologies

Circulating tumor DNA assays offer painless, repeatable sampling for tumor monitoring and are gaining clinical traction. The National Cancer Institute is funding validation studies, and companies such as Guardant Health and Thermo Fisher are expanding assay menus, putting price and performance pressure on traditional biopsy devices. Device manufacturers must therefore differentiate through accuracy, margin assessment, and integration with molecular-profiling workflows to defend share.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Needle-Based Systems Drive Innovation

Needle-based instruments generated USD 0.99 billion of revenue in 2025, equal to 44.20% of the biopsy devices market size, and they are forecast to clock an 8.12% CAGR through 2031. Core and vacuum-assisted models integrate electromagnetic tracking and AI analytics that highlight suspicious tissue in real time, cutting the learning curve for less-experienced operators. Elucent Medical’s EnVisio X1 earned FDA breakthrough status for combining optical navigation with radiofrequency-guided depth control, underscoring the investment arms race around precision targeting. In parallel, disposable needle cartridges align with infection-control mandates and accelerate turnover in ambulatory theatres, helping the biopsy devices market penetrate lower-acuity settings.

Procedure trays register steady gains because standardized kits streamline set-up and lower costs per case, an advantage prized by outpatient facilities under bundled-payment models. Localization wires remain a breast-care staple, yet newer clip-based markers that dissolve or emit low-energy radar signals are gradually cannibalizing demand by improving patient comfort and eliminating retrieval steps. Supporting accessories such as cannulas, obturators, and vacuum tubing now feature RFID tags that automate lot tracking and simplify recall management, a response to recent sterility failures.

By Application: Lung Procedures Accelerate Growth

Breast applications retained 31.12% of the biopsy devices market share in 2025 on the back of mammography-driven screening pathways and well-rehearsed surgical protocols. Yet lung procedures are projected to register a 9.02% CAGR, outpacing every other use-case through 2031. Australia’s publicly funded lung program and similar pilots in the United States and South Korea are redirecting large cohorts of CT-screen-detected nodules to bronchoscopy suites, lifting demand for steerable needles and electromagnetic navigation catheters. Suppliers that combine radial ultrasound, thin-gauge biopsy, and real-time pathology imaging are capturing early adopters.

Colorectal procedures benefit from expanded screening ages and AI-enabled colonoscope add-ons that flag polyps, increasing tissue-sampling events per colonoscopy. Prostate applications pivot toward MRI-fusion guidance, using transperineal access and vacuum-assisted cores to raise cancer detection and cut infection. Other applications such as pancreatic, liver, and renal biopsies see incremental uptake as hospitals invest in endoscopic ultrasound and intravascular robotics to reach previously inaccessible lesions, strengthening the long-tail of the biopsy devices market.

By End-User: Ambulatory Centers Emerge As Growth Engine

Hospitals handled 68.15% of procedures in 2025 and continue to buy high-throughput biopsy platforms, particularly those that integrate AI decision-support with PACS and electronic health records for immediate multidisciplinary review. However, ambulatory surgical centers are forecast to deliver a 9.18% CAGR, leveraging lower overhead and shorter stay times to backfill elective surgeries that shifted away from hospitals during the pandemic. Developers that supply compact vacuum-assisted consoles, sterile single-use needles, and tray-based component kits gain traction because capital budgets in these centers favor modular, pay-per-use models.

Diagnostic imaging centers keep broadening service lines by adding ultrasound-guided fine-needle aspiration and CT-guided core biopsy, capitalizing on portable scanners that fit within existing floor plans. Specialty clinics and mobile units form a small but rising share as governments fund outreach to rural districts, especially in Asia-Pacific nations where unmet need remains high. Collectively, these trends reinforce the diffusion of the biopsy devices market beyond tertiary campuses into community settings.

Geography Analysis

North America captured 41.25% of 2025 revenue owing to robust insurance coverage, technology-minded clinicians, and well-defined reimbursement pathways, cementing the region’s anchor position in the global biopsy devices market. Continuous innovation—illustrated by AI-assisted OCT, robotic bronchoscopy, and ultrathin flexible needles—ensures a steady refresh cycle for capital equipment. Nevertheless, hospitals face payer scrutiny over procedure bundles, nudging facilities toward cost-effective disposables and predictive analytics that prune unnecessary sampling.

Europe records modest but stable gains as national health systems emphasize value-based purchasing and personalized medicine. Uptake of markers that aid in margin assessment and molecular assays that guide targeted therapy is noticeable, spurring EU demand for high-quality tissue retrieval. Regulatory alignment under the Medical Device Regulation has lengthened approval timelines, but clear clinical-benefit documentation offsets the bureaucratic burden.

Asia-Pacific is projected to log an 8.25% CAGR through 2031, by far the fastest cadence for the biopsy devices market. India’s USD 612 billion health-sector build-out, China’s expansion of tier-2 oncology centers, and Southeast Asia’s private hospital boom enlarge the addressable install base. Governments simultaneously roll out lung, bowel, and cervical screening policies that feed procedure pipelines. Domestic manufacturers are emerging, yet premium U.S., Japanese, and European brands maintain technical leadership in vacuum and image-guided systems.

The Middle East, Africa, and South America account for smaller shares but show selective spikes where public-private partnerships fund cancer hubs. In the Gulf, large specialty hospitals procure top-tier biopsy suites tied to comprehensive oncology campuses. In Brazil and Mexico, reimbursement reforms encourage private insurers to cover advanced biopsy techniques, incrementally widening the patient pool. Supply-chain challenges and variable regulatory oversight temper immediate gains, but multinationals are positioning via local assembly and distribution alliances to unlock future growth.

Competitive Landscape

The competitive tier is moderately concentrated, with the top five manufacturers controlling significant global revenue. Becton Dickinson’s decision to spin off its Biosciences and Diagnostics unit sharpens focus on high-growth interventional technologies; the company is investing USD 2.5 billion to expand U.S. manufacturing capacity over five years. Boston Scientific, buoyed by USD 4.2 billion Q3 2024 sales, is scaling single-use duodenoscopes that eliminate infection-control burdens, aligning with clinician preference for disposable pathways.

Mid-tier companies cultivate niches in AI-guided imaging, robotics, and nano-scale sampling. Perimeter Medical Imaging AI leads optical coherence tomography integration, while start-ups advance nanoneedle patches and capsule robots that harvest tiny tissue fragments from gastrointestinal walls. Established suppliers pursue co-development agreements: Olympus collaborates with cloud-analytics providers for colonoscopy AI, and Argon Medical launches liver-biopsy devices through oncology partnerships.

Quality incidents are reshuffling reputations. Olympus, Hologic, and Cardinal Health face remediation costs after high-profile recalls, prompting all competitors to tighten sterilization validation and post-market surveillance. Simultaneously, the encroachment of liquid-biopsy firms such as Guardant Health motivates hardware vendors to bundle tissue devices with genomic testing services, anchoring relevance in an omics-driven oncology era. White-space prospects in emerging markets reward players able to pair cost-sensitive pricing with training programs that elevate procedural standards.

Biopsy Devices Industry Leaders

Argon Medical Devices

Cook Medical

Hologic Inc.

Becton, Dickinson and Company

Boston Scientific Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: King’s College London unveiled nanoneedle patches that perform painless real-time tissue sampling, signaling a potential shift away from conventional biopsy needles.

- September 2024: Argon Medical Devices introduced the TLAB Transvenous Liver Biopsy System for interventional radiology, expanding options for minimally invasive hepatic sampling.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study from Mordor Intelligence defines the biopsy devices market as all reusable and single-use instruments, core, fine-needle and vacuum-assisted guns, biopsy needles, localization wires, and pre-packed procedure trays, specifically engineered to retrieve solid-tissue samples under manual or image guidance in hospitals, diagnostic centers, and ambulatory settings.

Scope exclusion: liquid-biopsy kits, pathology consumables (slides, stains), and general surgical forceps are outside the present sizing.

Segmentation Overview

- By Product

- Needle-based Biopsy Instruments

- Core Biopsy Devices

- Aspiration Biopsy Needles

- Vacuum-Assisted Biopsy Devices

- Procedure Trays

- Localization Wires

- Other Products

- Needle-based Biopsy Instruments

- By Application

- Breast Biopsy

- Lung Biopsy

- Colorectal Biopsy

- Prostate Biopsy

- Other Applications

- By End-User

- Hospitals

- Diagnostic & Imaging Centers

- Ambulatory Surgical Centers

- Others

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts held structured calls with interventional radiologists, oncology surgeons, procurement heads, and device distributors across North America, Europe, and Asia-Pacific to verify utilization rates, gauge vacuum-assisted penetration, and test price erosion assumptions. Follow-up email surveys with biomedical engineers clarified maintenance cycles and refurbishment trends that rarely surface in documents.

Desk Research

A wide scan of open datasets such as GLOBOCAN cancer incidence tables, the WHO Global Health Observatory, U.S. FDA MAUDE recall logs, and OECD Health Statistics gives baseline epidemiology, device safety alerts, and procedure volumes. Trade bodies including the Medical Device Manufacturers Association and regional radiology societies publish guideline updates and installed-base counts that help us calibrate product adoption curves. Company 10-Ks, device 510(k) summaries, and reputable news streams accessed through Dow Jones Factiva and D&B Hoovers supply revenue splits, ASP commentary, and capacity expansions that ground our price and channel assumptions. The sources listed illustrate our approach; many additional public and paid references were tapped for data cross-checks.

Market-Sizing & Forecasting

A top-down construct begins with cancer incidence and image-guided biopsy procedure rates, which are then multiplied by modality-specific penetration and disposable-per-case factors to derive unit demand. Select bottom-up roll-ups of leading suppliers' biopsy-needle shipments and sampled ASP multiplied by volume checks anchor the totals before reconciliation. Key drivers, screening program coverage, vacuum-assisted share, average selling price drift, day-care procedure mix, and device recall frequency feed a multivariate regression, while an ARIMA overlay captures short-term cyclical swings. Missing datapoints (e.g., private clinic volumes) are gap-filled using regional proxy ratios validated through interviews.

Data Validation & Update Cycle

Outputs pass variance tests versus independent procedure counts and hospital spend trackers; anomalies trigger secondary peer review and, if needed, a fresh expert call. Reports refresh every twelve months, with interim revisions when material recalls, reimbursement shifts, or major M&A events surface.

Why Mordor's Biopsy Devices Baseline Earns Stakeholder Trust

Published figures often diverge because firms select unlike product baskets, price bases, and refresh cadences. Our disciplined scope, annual refresh, and dual-stage validation give decision-makers a stable anchor.

Key gap drivers include: some publishers fold visualization consoles and robotic arms into market value, others uplift 2023 revenues with undisclosed distributor mark-ups, and a few roll historical data forward without re-checking procedure counts, leading to overstated 2024 totals.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.24 B (2025) | Mordor Intelligence | - |

| USD 7.27 B (2024) | Global Consultancy A | Includes visualization systems and robotic platforms |

| USD 2.40 B (2024) | Trade Journal B | Uses 2023 supplier revenues rolled forward without procedure validation |

| USD 2.90 B (2024) | Regional Consultancy C | Adds ancillary disposables and assumes uniform ASP uplift globally |

The comparison shows that when scope is tightened to true tissue-retrieval devices and variables are re-benchmarked yearly, Mordor delivers a balanced, traceable baseline clients can rely on.

Key Questions Answered in the Report

How large is the biopsy devices market today?

The market generated USD 2.33 billion in 2026 and is forecast to rise to USD 2.83 billion by 2031 at a 3.97% CAGR.

Which product category holds the largest share?

Needle-based systems led with 44.20% of 2025 revenue and are also the fastest-growing segment at an 8.12% CAGR.

What application is expanding the quickest?

Lung procedures are projected to grow at a 9.02% CAGR through 2031, propelled by new government-funded screening programs.

Which end-user segment offers the highest growth opportunity?

Ambulatory surgical centers are predicted to post a 9.18% CAGR, outperforming hospitals and imaging centers.

What region will add the most incremental revenue by 2031?

Asia-Pacific is set to provide the greatest incremental gain with an 8.25% CAGR, supported by large-scale healthcare investments and expanded cancer screening policies.

Page last updated on: