Market Overview

| Study Period | 2020 - 2031 |

|---|---|

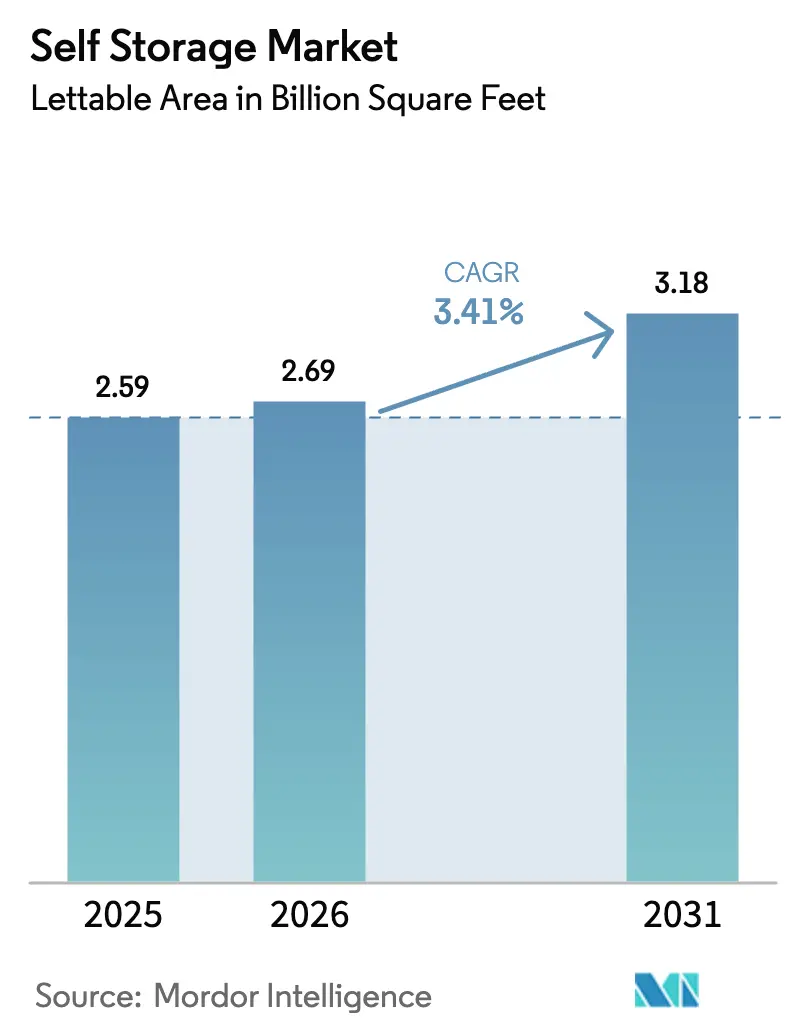

| Market Volume (2026) | 2.69 Billion square feet |

| Market Volume (2031) | 3.18 Billion square feet |

| Growth Rate (2026 - 2031) | 3.41% CAGR |

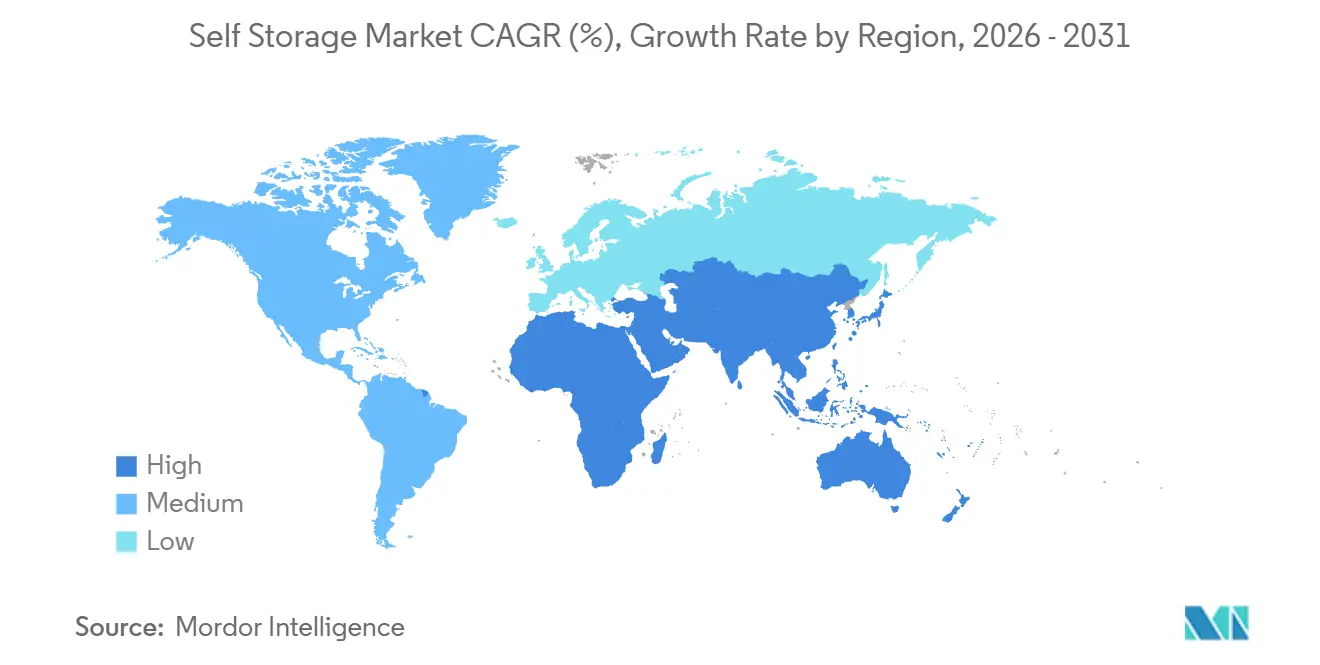

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

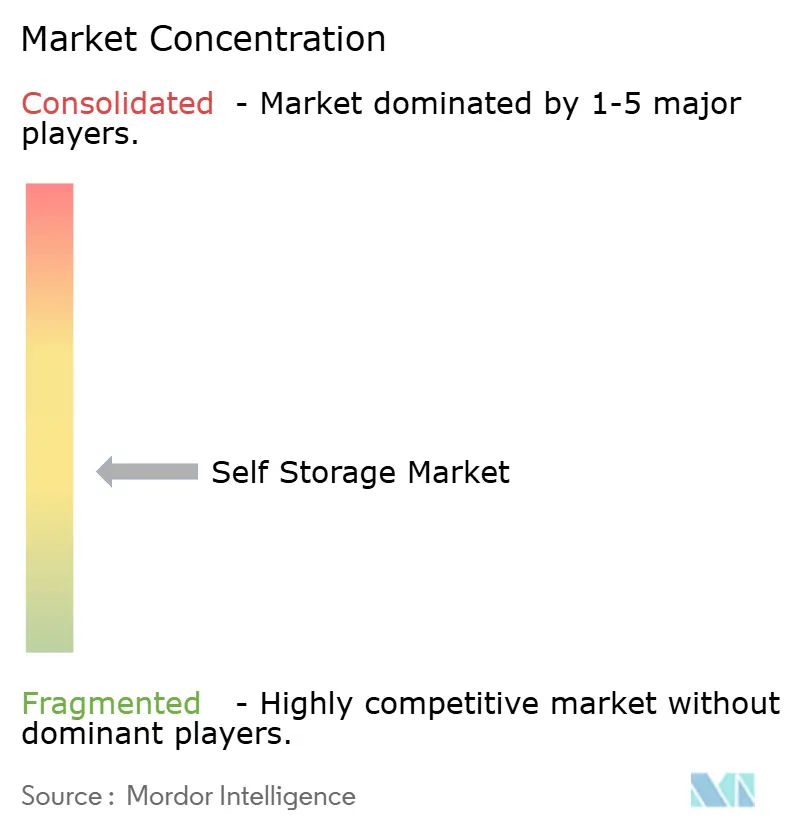

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Self Storage Market Analysis by Mordor Intelligence

The Self Storage Market size in terms of lettable area is expected to increase from 2.59 Billion square feet in 2025 to 2.69 Billion square feet in 2026 and reach 3.18 Billion square feet by 2031, growing at a CAGR of 3.41% over 2026-2031. This moderate expansion conceals a shift toward premium monetization, as climate-controlled facilities, business tenants, and technology-enabled leasing models lift revenue per occupied square foot. Operators retrofit older assets with HVAC systems that double unit revenue and meet corporate cold-chain needs. Contact-free leasing platforms reduce staffing expenses, extend selling hours, and enable algorithmic price adjustments. Geographic momentum shifts to the Asia Pacific, where shrinking urban apartments, rising disposable income, and e-commerce adoption combine to increase paid-storage adoption. Large United States REITs pursue scale advantages, yet fragmentation leaves room for regional specialists who leverage zoning familiarity and micro-market pricing power.

Key Report Takeaways

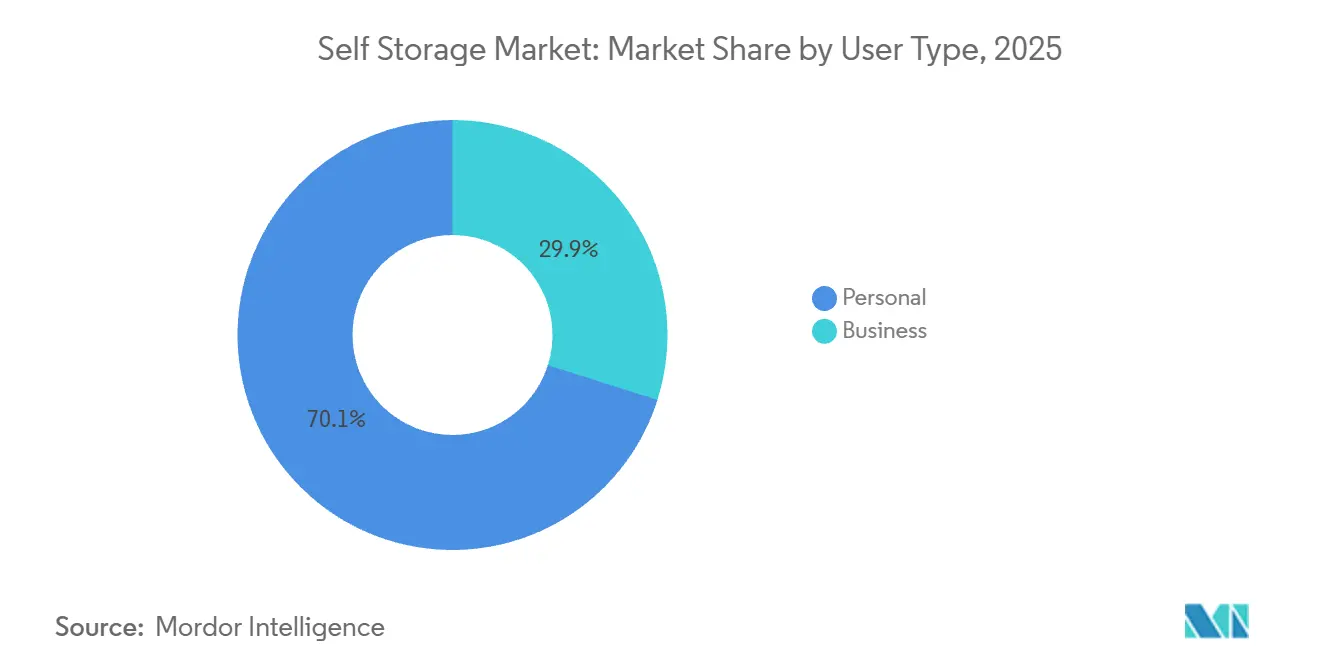

- By user type, personal users held a 70.12% share in 2025, while business tenants are expected to advance at a 5.81% CAGR through 2031.

- By storage type, climate-controlled units captured 54.64% of the self storage market size in 2025 and are expanding at a 6.71% CAGR through 2031.

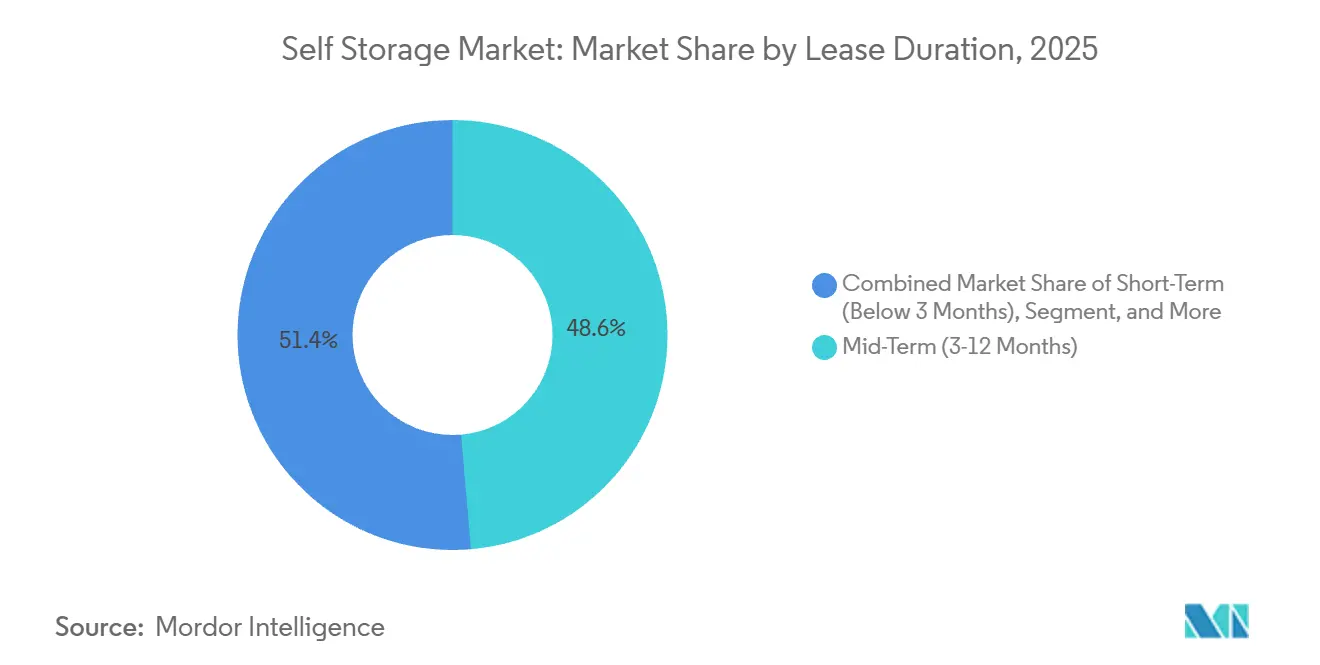

- By lease duration, mid-term contracts held 48.63% of the self storage market share in 2025, whereas short-term leases are growing at a 5.32% CAGR through 2031.

- By unit size, medium (50-100 sq ft) held 40.32% of the self storage market share in 2025, while small units under 50 square feet are expected to grow at a 6.12% CAGR through 2031 and command the highest revenue per square foot.

- By geography, North America retained 52.48% of global capacity in 2025; however, the Asia Pacific is projected to deliver a 5.09% CAGR through 2031.

- By company presence, Public Storage, Extra Space Storage, and CubeSmart together managed roughly 15% of North American capacity in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Self Storage Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urbanization and Shrinking Living Spaces | +1.2% | Global, concentrated in Asia Pacific tier-1 cities, North America urban cores | Long term (≥ 4 years) |

| Proliferation of E-commerce Micro-Merchants | +0.9% | North America and Europe, expanding to Asia Pacific | Medium term (2-4 years) |

| Rising Residential Real-Estate Costs | +0.7% | North America, Europe, Asia Pacific metros | Long term (≥ 4 years) |

| Digitized, Contact-Free Leasing Platforms | +0.5% | Global, early adoption in North America and Europe | Short term (≤ 2 years) |

| Self-Storage as Micro-Fulfillment Hubs | +0.8% | North America and Europe, pilot projects in Asia Pacific | Medium term (2-4 years) |

| Climate-Resilient Asset Preservation Demand | +1.0% | Global, acute in coastal North America, Europe, Asia Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Urbanization and Shrinking Living Spaces

Apartment footprints in Tokyo, Hong Kong, and Shanghai dropped below 500 square feet in 2025, forcing residents to externalize bulky possessions.[1]U.S. Census Bureau, “American Housing Survey 2025,” CENSUS.GOV Penetration climbed to 1.5 square feet per capita in these cities, triple rates in suburban locations with garage space. Developers in Singapore and Mumbai incorporate onsite storage into mixed-use towers that command an 8% rent premium. As Asia Pacific urbanization tops 65%, self storage becomes a structural need rather than a discretionary choice. North American downtowns follow a similar path, sustaining demand even when macro conditions soften.

Proliferation of E-commerce Micro-Merchants

A 2025 survey found 38% of online sellers under USD 500,000 annual revenue stage inventory in self storage rather than warehouses. These tenants stay 40% longer and pay 25%-35% premiums for drive-up loading and parcel acceptance. Climate control is essential for electronics and cosmetics, enabling operators to charge rates 50%-80% above ambient space. Micro-merchants offer counter-cyclical resilience because layoffs prompt side-hustle formation that inflates storage demand during downturns.

Climate-Resilient Asset Preservation Demand

Heat waves topping 110 °F in Phoenix and humid spikes above 80% in Houston damaged goods in conventional units and pushed insurers to raise premiums 15%-25%.[2]Insurance Information Institute, “Commercial Property Insurance Trends 2025,” III.ORG Operators responded by converting ambient buildings to HVAC-equipped facilities that double revenue per square foot. Pharmaceutical distributors and wine collectors now require strict temperature bands, and their willingness to pay sustains investment returns even in slow-growth metros. Regulators increasingly view climate resilience as a public-safety concern, creating a compliance moat for early adopters.

Digitized, Contact-Free Leasing Platforms

Smart-lock and mobile-app leasing captured more than 20% of new rentals at Extra Space Storage in 2025. Automation cut per-facility labor costs 30% and lifted revenue per available square foot by up to 12% through real-time surge pricing. Digital-native renters aged 25-35 adopted app-based contracts at a 60% higher rate than walk-in customers. Cyber-insurance carriers now demand two-factor authentication, adding USD 200-USD 400 per unit in retrofit costs. Operators able to absorb that expense gain a durable acquisition-cost advantage over small independents.

Restraints Impact Analysis of Self Storage Market*

| Restraint | ~ (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Zoning and Land-Use Regulations | -0.6% | North America urban cores, Europe metro areas | Medium term (2-4 years) |

| Oversupply Pockets in Mature Metros | -0.4% | North America Sunbelt cities, select European markets | Short term (≤ 2 years) |

| Escalating Insurance Premiums from Extreme Weather | -0.3% | Coastal North America, flood-prone Europe and Asia Pacific | Medium term (2-4 years) |

| Cyber-Security Risks for Smart Facilities | -0.2% | Global, acute in North America and Europe with high IoT adoption | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Zoning and Land-Use Regulations

Portland, Seattle, and San Francisco reclassified self storage as industrial in 2025, imposing setbacks, parking mandates, and design reviews that delay approvals 18-36 months. European councils in London and Paris cap storage growth below 2% even as demand climbs 5%-7%. Incumbents with grandfathered sites obtain pricing power, but new entrants face steep legal and holding costs that deter capacity additions, shaving roughly 0.6 percentage points from the global CAGR.

Oversupply Pockets in Mature Metros

United States Sunbelt cities added 15%-25% new capacity between 2022 and 2024, resulting in occupancy rates near 82% and forcing 10%-15% rate cuts. Large REITs acquired distressed assets at discounts and shuttered surplus space to stabilize rents, yet recovery in the most saturated submarkets may not arrive before 2027. The divergence creates a two-speed landscape where coastal constraints enable a 4%-6% rate growth while oversupplied interiors lag.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Self Storage Market Segment Analysis

By User Type:

Business Tenants Drive Premium RevenueBusiness tenants occupied 29.88% of capacity in 2025 and were advancing at a 5.81% CAGR through 2031, yet generated more than 40% of total revenue, as their average lease term exceeded two years. These customers pay 25%-35% premiums for 24-hour access, package handling, and reinforced floors, lifting the self storage market size for commercial users faster than the headline rate. E-commerce sellers, contractors, and seasonal retailers prefer month-to-month contracts that avoid multi-year warehouse leases. Personal customers account for 70.12% of the share, but their churn raises cleaning and remarketing costs, which dilute margins.

Operators now design mixed-use layouts where ground-floor commercial units cross-subsidize upper-floor personal lockers. In logistics hubs such as New Jersey and Southern California, business tenants already control 50%-60% of climate-controlled inventory, underscoring the profitability gap with personal users. As more REITs court corporate accounts, competitive emphasis shifts from price to workflow integration, deepening the value pool inside the self storage market.

By Storage Type:

Climate Control Commands Premium GrowthClimate-controlled facilities, which represented 54.64% of the total capacity, captured an outsized share of revenue in 2025 and are expected to expand at a 6.71% CAGR through 2031. Extreme weather losses and rising insurer requirements accelerate conversions, expanding the self storage market share for conditioned space each year. Operators charge premiums of 50%-80% over ambient units, and business tenants willingly pay to protect their high-value inventory.

Conversely, non-climate stock thrives in temperate or rural settings where upgrade costs would not be recouped. Portable container services remain a niche due to logistical complexity, and vehicle storage experiences regional strength in states with strict homeowner association rules against driveway parking. Execution focus, therefore, revolves around matching micro-climate risk to asset mix in order to maximize the self-storage market size captured per location.

By Lease Duration:

Short-Term Flexibility Gains TractionMid-term agreements between 3-12 months still hold 48.63% of contracts, but month-to-month rentals are the fastest climber as gig-economy workers and project-based companies avoid commitment. Each new short-term lease generates ancillary move-in fees and insurance sales, resulting in monthly revenue 20%-30% higher than that of long-term tenants. Short-term leases are growing at a 5.32% CAGR through 2031. Operators respond by eliminating annual-contract discounts and applying 8%-12% rate escalators, lifting the self storage market size attributed to short-stay users.

Long-duration customers provide occupancy stability but constrain the ability to implement dynamic pricing. As digital channels reduce acquisition costs, operators willingly trade vacancy risk for higher effective rates, a pivot expected to keep reshaping the self storage market through 2031.

By Unit Size:

Small Units Capture Urban DensityUnits under 50 square feet achieve 95% occupancy in New York, San Francisco, and London, and earn 40%-60% more revenue per square foot than larger units. Micro-entrepreneurs and urban minimalists value central locations over size, and operators monetize scarcity by charging USD 1.50-USD 2.50 per square foot on compact lockers. Small units under 50 square feet accounted for a 6.12% CAGR through 2031.

Medium sizes between 50-100 square feet serve mainstream residential moves but face margin pressure from both ends of the spectrum. Medium (50-100 sq ft) unit size held 40.32% of the self storage market share in 2025. Large units above 100 square feet attract contractors and downsizers in suburban corridors, while mega units double as low-cost warehouses for e-commerce sellers. Optimal development strategy now skews toward bifurcation, dense-city infill sites favor micro-lockers, whereas suburban parcels emphasize drive-up bays, balancing the self storage market share across formats.

Geography Analysis

North America Self Storage Market

North America held 52.48% of the global capacity in 2025, with a per-capita penetration of 9.5 square feet.[3]Self Storage Association, “Industry Data Report 2025,” SELFSTORAGE.ORG Occupancy gaps emerged between saturated Sunbelt metros, such as Phoenix and Dallas, which hovered near 82%, and coastal cities, where zoning barriers keep facilities full at 95% and allow for 4%-6% annual rent increases. Canada mirrors the United States profile, while Mexico advances quickly as middle-class consumers embrace external storage.

APAC Self Storage Market

The Asia Pacific region posts the fastest growth rate of 5.09%, driven by Chinese and Indian cities where apartment sizes typically fall below 500 square feet, and urbanization surpasses 60%. Japan continues to expand steadily amid an aging population and a climate-controlled demand for humidity protection. Australia and New Zealand focus on consolidating existing facilities rather than undertaking greenfield builds, resulting in a moderate 2.8% growth.

EMEA and LATAM Self Storage Market

Europe growth rate is 3.6%, although disparities persist. The United Kingdom resembles a mid-maturity North American market, with 4.5 square feet per capita, whereas Germany, France, and Spain have lower figures, offering a runway for Shurgard and Safestore. Central Europe, highlighted by recent Polish acquisitions, unlocks incremental demand among e-commerce merchants. Beyond the core regions, Latin America, the Middle East, and Africa together account for less than 8% of supply but expand 6%-8% as expatriate populations and e-commerce adoption scale in cities such as São Paulo and Dubai.

Competitive Landscape

The three largest United States REITs controlled roughly 15% of North American square footage in 2025, leaving a fragmented tail of regional chains and independents. North America retained 52.48% of global capacity in 2025. Consolidation accelerated when Extra Space Storage acquired Life Storage in November 2025, creating a leader with 3,800 facilities across the country. Technology is the chief battleground; smart-lock systems and pricing algorithms cut labor costs 30% and raise revenue 8%-12%.

Door-to-door startups, such as Clutter and MakeSpace, pursue logistics-bundled models that circumvent facility visits; however, fleet and labor costs require high density to break even. Established operators can counter by adding last-mile delivery partnerships or purchasing portable container firms. In Europe, Shurgard and Safestore invest in Central European roll-ups while Big Yellow targets London infill sites with ESG-rated new builds. The Asia Pacific features a mix of domestic champions and REIT entrants. Storefriendly leverages brand localization in tier-1 Chinese cities, whereas National Storage REIT consolidates Australia and New Zealand through discounted buyouts. Asia Pacific posts a 5.09% CAGR through 2031.

Competitive intensity hinges on technology adoption rather than price wars. Operators owning the data advantage maximize yield management and cross-sell insurance. Smaller independents rely on neighborhood knowledge but risk margin squeeze without capital to digitize. The market’s middle tier is likely to shrink through takeovers by scale players or capital exits by 2028.

Self Storage Industry Leaders

Public Storage

Extra Space Storage Inc.

U-Haul International Inc.

CubeSmart LP

National Storage Affiliates Trust

- *Disclaimer: Major Players sorted in no particular order

Self Storage Market Companies Covered in this Report

- Public Storage

- Extra Space Storage Inc.

- U-Haul International Inc.

- CubeSmart LP

- National Storage Affiliates Trust

- Life Storage Inc.

- Safestore Holdings PLC

- StorageMart

- Shurgard Self-Storage SA

- Big Yellow Group PLC

- Prime Storage Group

- Metro Storage LLC

- SmartStop Asset Management LLC

- Clutter Inc.

- MakeSpace Inc.

- Kennards Self Storage

- Access Self Storage Ltd.

- Urban Self Storage Inc.

- Global Self Storage Inc.

- World Class Capital Group LLC (Great Value Storage)

- Amsdell Cos./Compass Self Storage

- All Storage

- Storage King Pty Ltd.

- Storefriendly Self Storage Group

Recent Industry Developments in Self Storage Market

- December 2025: Extra Space Storage closed its USD 12.7 billion acquisition of Life Storage, adding 1,300 facilities across 36 states and projecting USD 70 million annual cost synergies.

- September 2025: Public Storage unveiled a USD 450 million retrofit program to add HVAC and smart locks to 200 properties in California, Texas, and Florida.

- July 2025: Shurgard Self-Storage entered Poland with a USD 71 million acquisition of eight locations in Warsaw and Krakow.

- May 2025: CubeSmart formed a USD 800 million joint venture with Brookfield Asset Management to build 50 facilities in supply-constrained United States metros over three years.

Self Storage Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the global self-storage market as purpose-built facilities that rent enclosed units, containers, or secure outdoor bays to individuals and businesses on flexible terms, tracking lettable square footage and the corresponding rental revenue. According to Mordor Intelligence, this scope captures climate-controlled and conventional units across all size brackets while ignoring informal garage rentals or warehousing that is not separately let.

Scope Exclusion: We exclude third-party "mini-warehouse" services where goods are collected, inventoried, and returned on demand rather than stored under the tenant's lock and key.

Segments Covered in This Report

- By User Type

- Personal

- Business

- By Storage Type

- Climate-Controlled

- Non-Climate-Controlled

- Portable / Container-Based

- Vehicle and Specialty (RV, Boat, Wine)

- By Lease Duration

- Short-Term (Below 3 Months)

- Mid-Term (3-12 Months)

- Long-Term (Above 12 Months)

- By Unit Size

- Small (Below 50 sq ft)

- Medium (50-100 sq ft)

- Large (100-200 sq ft)

- Mega (Above 200 sq ft)

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Rest of Asia Pacific

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Kenya

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Primary Research

We interviewed self-storage REIT executives, independent facility owners in Asia and Europe, and commercial real-estate brokers. Their feedback on achievable rent escalations, churn rates, and cap-rate expectations helped us fine-tune average price and utilization assumptions, fill regional data gaps, and validate demand inflection points suggested by secondary sources.

Desk Research

We started by mapping unit inventories, occupancy rates, average rents, and pipeline projects from open records such as US SEC 10-Ks, UK Companies House filings, and stock-exchange presentations. Trade associations, notably the Self Storage Association USA and FEDESSA, supplied annual facility counts, while official datasets from the U.S. Census, Eurostat building permits, and Australia's ABS clarified urban housing density trends that trigger storage demand. Customs import codes for prefabricated containers, patent logs on portable unit locks, and news archives on facility transactions from Dow Jones Factiva further ground the volume baseline. Marklines or other paid datasets were unnecessary, yet D&B Hoovers supported private-operator revenue ranges. This list is illustrative, not exhaustive, and many additional sources were tapped for cross-checks.

Market-Sizing & Forecasting

A top-down model converts national facility counts and average square-footage into a demand pool, which is then valued with region-specific rent per square foot. Supplier roll-ups and sampled unit-size × price checks act as a light bottom-up sense test before figures are reconciled. Key drivers inside the model include urban population ratio, household move frequency, e-commerce parcel volumes, average residential floor area, occupancy rate cycles, and new facility completions. Forecasts rely on multivariate regression blended with scenario analysis; occupancy and rent trends are regressed against GDP per capita, housing starts, and mobility indicators, while scenario bands capture macro shocks. Where bottom-up samples are thin, gap-filled values are benchmarked to historical spreads and peer clusters.

Data Validation & Update Cycle

Outputs pass three tiers of analyst review; variance thresholds trigger re-runs, and we reconnect with key respondents when anomalies persist. The model is refreshed annually; interim updates occur when material events, large portfolio sales or zoning reforms, shift fundamentals.

How Mordor Intelligence's Self Storage Market Size Compares to Other Published Estimates

Published market values often diverge because firms choose different facility definitions, price baskets, and refresh cadences.

Our disciplined scope, variable selection, and annual re-benchmarking give decision-makers a stable, transparent anchor.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 58.26 B (2023) | Mordor Intelligence | - |

| USD 59.08 B (2024) | Global Consultancy A | Includes portable relocation warehousing and assumes uniform 6% rent growth across regions |

| USD 60.41 B (2024) | Industry Source B | Lacks facility-count audit; applies fixed 92% occupancy for all markets |

| USD 56.81 B (2024) | Trade Journal C | Omits vehicle and specialty units, leading to lower revenue pool |

The comparison shows that numbers swing when scope or core assumptions shift. By anchoring values to auditable facility inventories, observed rent bands, and a living update cycle, Mordor delivers a balanced baseline that clients can trace, replicate, and trust.

Key Questions Answered in the Report

How large is the self storage market in 2026?

The market encompasses 2.69 billion square feet in 2026 and is projected to reach 3.18 billion square feet by 2031.

Which segment is growing fastest within self storage?

Climate-controlled units lead with a 6.71% CAGR because tenants pay premiums to protect temperature-sensitive goods.

Why are business tenants important for operators?

Business users stay longer and pay 25%-35% premiums for features like 24-hour access, lifting revenue density.

Which region shows the highest growth momentum?

Asia Pacific posts a 5.09% CAGR through 2031 as urbanization and small apartment sizes boost paid-storage adoption.

How are technology platforms changing the sector?

Contact-free leasing and smart-lock systems cut labor costs 30% and enable dynamic pricing that raises yield per square foot.

What risks could slow industry growth?

Zoning restrictions in dense cities and oversupply pockets in Sunbelt metros can suppress new construction and pricing power.

Page last updated on: