Self-Sovereign Identity (SSI) Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 3.25 Billion |

| Market Size (2030) | USD 65.55 Billion |

| Growth Rate (2025 - 2030) | 82.40% CAGR |

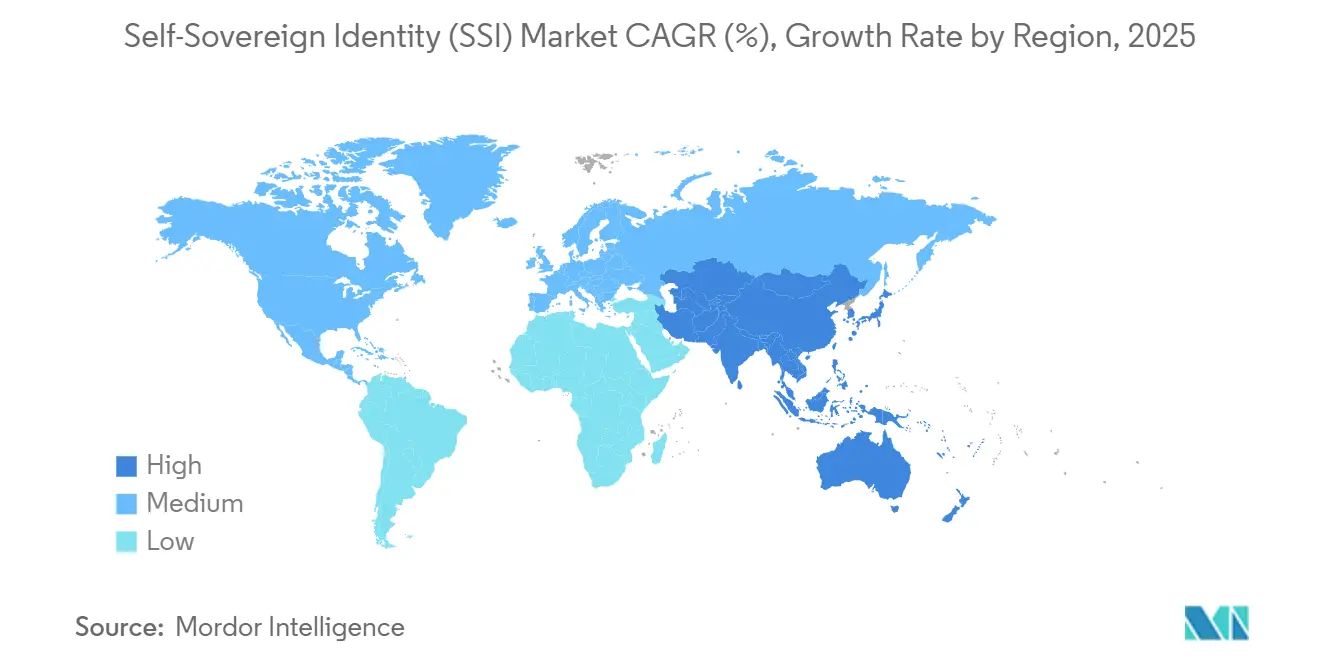

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

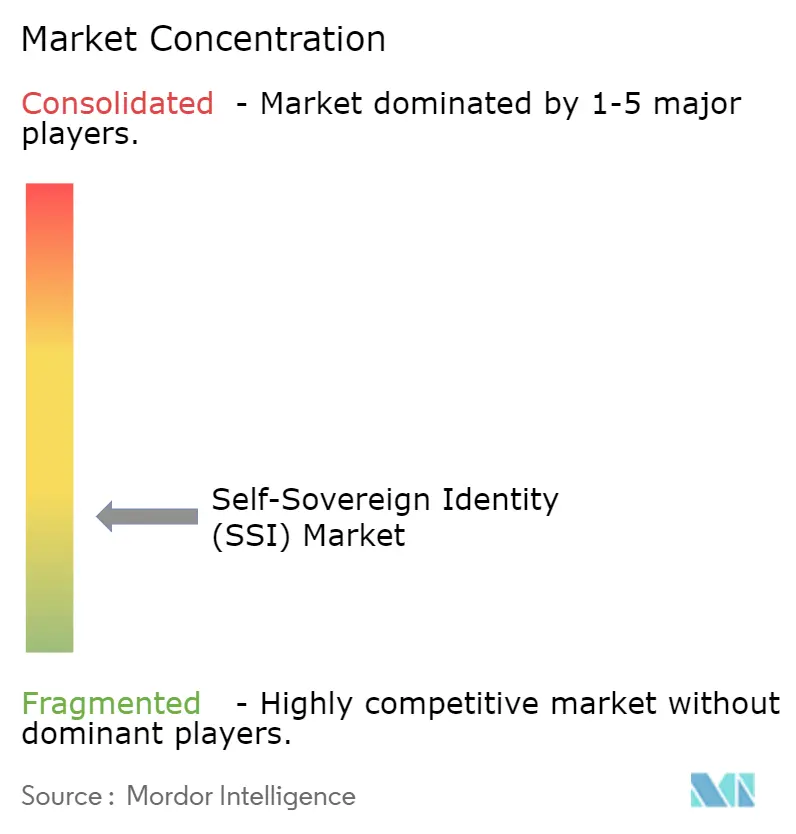

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Self-Sovereign Identity (SSI) Market Analysis by Mordor Intelligence

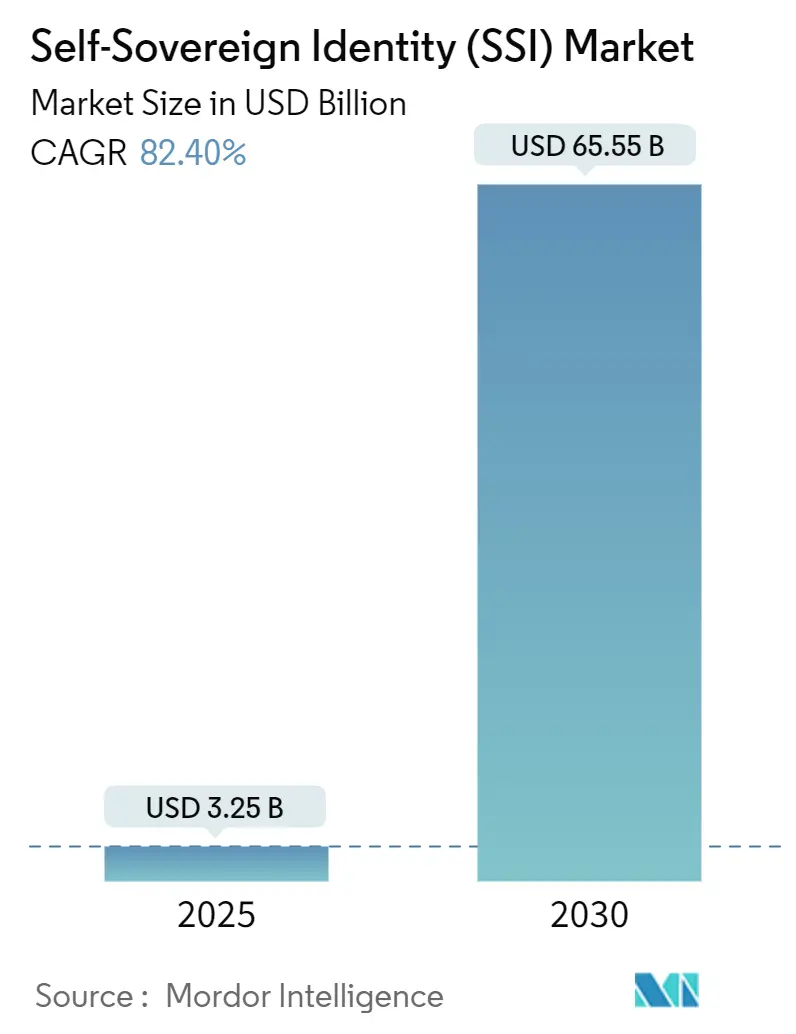

The self-sovereign identity (SSI) market size reached USD 3.25 billion in 2025 and is projected to climb to USD 65.55 billion by 2030, delivering an exceptional 82.40% CAGR. Heightened regulatory pressure, widening Web3 wallet use, and the proliferation of verifiable-credential toolkits are reshaping how organizations manage digital trust. Government mandates in the European Union and the United States are turning decentralized identity from a technological option into a compliance necessity, while large cloud providers embed zero-knowledge proof tooling for mainstream adoption. Intensifying cyber-fraud threats, combined with mounting customer demand for privacy control, are further accelerating the shift from centralized logins to portable credentials across financial services, travel, and healthcare. At the same time, early infrastructure purchases are giving way to large-scale implementation projects that convert proofs-of-concept into production rollouts, underpinning robust service-sector growth.

Key Report Takeaways

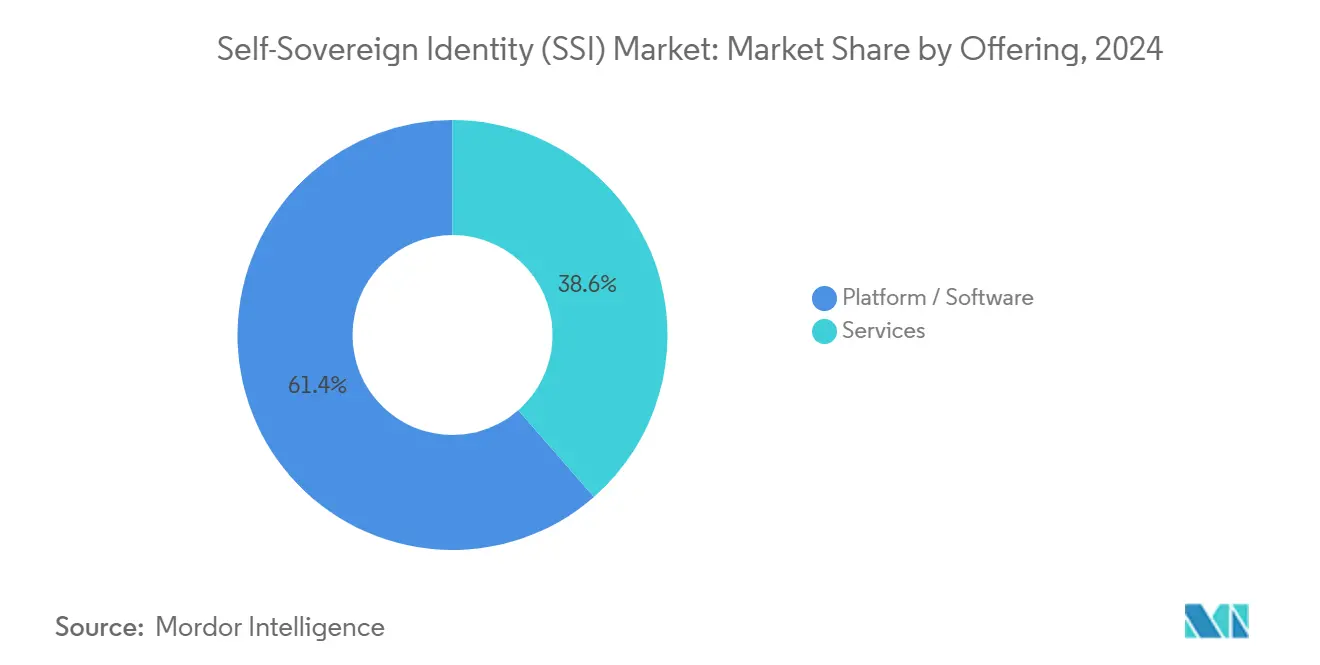

- By offering, platform and software solutions, led with 61.43% of self-sovereign identity market share in 2024, while services advanced at an 83.14% CAGR through 2030.

- By identity type, Individual Identity led with 66.68%% of self-sovereign identity market share in 2024, while IoT / Device Identity advanced at an 82.87% CAGR through 2030.

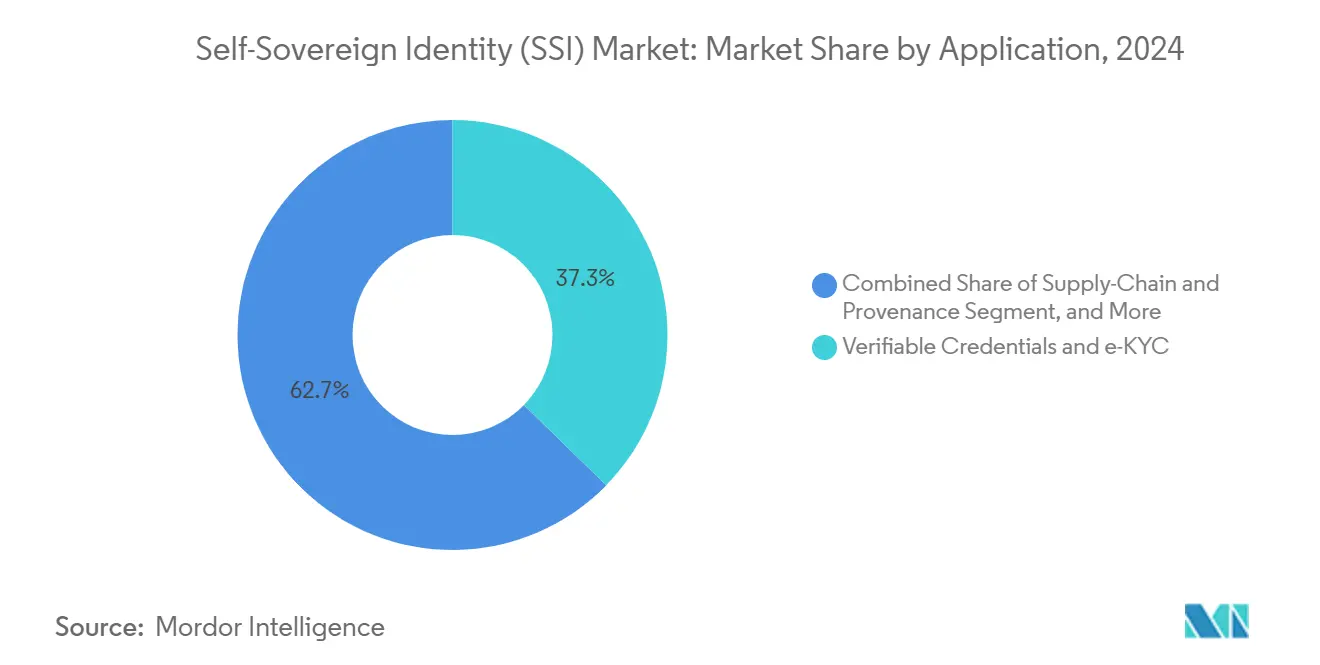

- By application, verifiable credentials and e-KYC commanded a 37.32% share of the self-sovereign identity market size in 2024, whereas supply-chain and provenance solutions are projected to expand at an 82.36% CAGR to 2030.

- By end-user industry, the BFSI segment held 28.73% of the self-sovereign identity market share in 2024, while mobility and transportation are forecast to record the fastest 82.51% CAGR through 2030.

- By geography, North America represented 44.87% of the self-sovereign identity market size in 2024, and Asia-Pacific is positioned for an 82.47% CAGR between 2025 and 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Self-Sovereign Identity (SSI) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand surge for decentralized government IDs | +12.5% | Global, early EU and North America | Medium term (2-4 years) |

| National eID and travel-credential integration | +11.8% | EU core, expanding Asia-Pacific and Americas | Medium term (2-4 years) |

| Rapid rise of Web3 wallets as identity hubs | +15.2% | Global, tech-forward markets | Short term (≤2 years) |

| Compliance push from eIDAS 2.0 and NIST 800-63-4 | +13.7% | North America and EU | Short term (≤2 years) |

| Gen-AI identity proofing lowers onboarding friction | +9.3% | Global BFSI and healthcare | Short term (≤2 years) |

| Reusable KYC networks cut banking costs | +8.1% | Global financial centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing demand for decentralized digital IDs among governments

National and state agencies are scaling SSI pilots into full production as privacy regulation tightens and cost-to-serve pressures mount. The U.S. federal modernization program anchors its architecture on NIST 800-63-4, letting agencies issue high-assurance credentials without central data silos. In parallel, eIDAS 2.0 compels every EU member state to distribute interoperable digital wallets by 2026, providing citizens with one credential for cross-border services. Japan’s My Number card now loads directly into Apple Wallet, illustrating how legacy ID schemes can migrate to citizen-controlled storage while meeting regulatory criteria.[1]Apple Inc., “Use Your My Number Card in Apple Wallet,” apple.com Government adoption establishes critical mass for private-sector uptake, spurring network effects that attract fintechs, airlines, and healthcare providers. As more jurisdictions declare wallet deadlines, SSI transitions from exploratory technology to default identity infrastructure.

Integration of SSI with national eID and travel credential programs

The International Air Transport Association’s Digital Travel Credentials initiative stores passports inside user wallets, permitting document verification in seconds and lowering airport congestion.[2]International Air Transport Association, “Digital Travel Credentials,” iata.org European Digital Identity wallets are built for Schengen-wide acceptance, enabling citizens to open bank accounts in Germany, receive healthcare in France, and board aircraft across the region using the same credential. Transportation Security Administration pilots of mobile driver’s licenses show domestic IDs can fit global aviation requirements, paving the way for frictionless corridor-to-gate experiences. Interoperability mandates from international civil aviation standards bodies now shape wallet specifications, accelerating standard alignment among border agencies.

Rapid rise of Web3 wallets as universal identity managers

Cryptocurrency wallets have evolved into multi-purpose identity containers, bundling payment keys with employment, education, and social proofs. Google Cloud’s integration of Self Protocol merges AI and zero-knowledge proof tooling, allowing developers to embed private credential checks into cloud workloads without exposing data. Hardware maker OneKey fused cold-storage devices with MetaMask, letting users present verifiable credentials while keeping signing keys offline. As wallets consolidate identity, finance, and messaging, network effects accumulate: the more services relying on a single credential, the lower user churn and the higher security. Regulatory conversations are shifting to treat wallet providers as critical trust anchors rather than ancillary crypto tools.

Compliance push from EU eIDAS 2.0 and U.S. NIST 800-63-4

Two cornerstone frameworks are dictating technical guardrails that effectively mandate SSI adoption. eIDAS 2.0 standardizes wallet configuration, issuance, and assurance levels, ensuring every EU resident receives at least one compliant credential. NIST 800-63-4 explicitly recognizes decentralized architectures for federal authentication, providing conformity assessment criteria for private contractors. U.S. states such as California already align mobile driver’s license pilots to these guidelines, creating a pathway for nationwide rollout. The two regulations influence multinational enterprises that must comply simultaneously with EU and U.S. standards, prompting accelerated global wallet deployments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Undefined interoperability beyond W3C VC/DID | -8.4% | Global, fragmented regions | Long term (≥4 years) |

| Reliance on smartphone penetration for custody | -6.2% | Emerging markets | Medium term (2-4 years) |

| Token-economics sustainability risk for SSI ledgers | -4.7% | Blockchain-dependent projects | Medium term (2-4 years) |

| High issuer liability in revocation disputes | -5.1% | Strict data-protection regimes | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Undefined global interoperability standards beyond W3C VC/DID

W3C finalized Verifiable Credential Data Model 2.0 in 2024, yet specifications for revocation, cross-chain proofs, and trust-framework discovery remain unfinished.[3]World Wide Web Consortium, “Verifiable Credentials Working Group Charter,” w3.org Vendors are filling gaps with proprietary extensions, creating silos that undermine the universal portability vision of SSI. Enterprises wary of lock-in postpone multi-vendor rollout until additional standards stabilize. Fragmentation also increases implementation costs because integrators must build bridges between incompatible stacks. The Decentralized Identity Foundation is drafting supplemental guidance, but slow consensus risks delaying enterprise procurement cycles beyond the forecast window.

Reliance on smartphone penetration for credential custody

Most production wallets rely on biometric-enabled smartphones with secure enclaves, assuming continuous connectivity and user familiarity with private-key management. Regions with lower device penetration or reliance on basic handsets face exclusion, jeopardizing government goals for universal service access. Hardware tokens and card-based alternatives exist, yet ecosystem tooling for issuance, recovery, and revocation remains immature. A lost or damaged device can lock users out of critical services, raising social-inclusion concerns. Until low-cost custody formats mature, large deployments in emerging markets may encounter slower uptake.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Surge Despite Platform Dominance

Platform and software products captured 61.43% of the self-sovereign identity market share in 2024, confirming that early adopters prioritized core infrastructure. Services, however, are projected to post an 83.14% CAGR because enterprises now need integration, customization, and governance expertise to operationalize wallets across complex, multi-jurisdiction networks. The services layer includes credential issuance orchestration, zero-knowledge proof configuration, and ongoing compliance audits, yielding recurring revenue streams that outstrip one-time license fees. Alliances such as Dock Labs partnering with cheqd fuse product stacks with consulting depth to accelerate large-scale rollouts. As more regulated sectors adopt SSI, the professional-services pool widens across system integrators, cybersecurity firms, and specialty advisory boutiques.

The shift to services alters budget allocations in procurement cycles. Decision-makers increasingly seek outcome-based contracts that tie vendor remuneration to onboarding-cost reductions or fraud-loss avoidance. Cloud-native delivery models make upgrades seamless, meaning managed services vendors must demonstrate continuous compliance tracking as regulations evolve. Consequently, price competition in the platform tier intensifies while service margins remain resilient. This dynamic supports sustained profitability for consulting-led providers even as software commoditizes.

By Identity Type: Individual Foundation Enables IoT Expansion

Individual identity use cases established the commercial baseline in 2024 because most wallet programs target citizens and retail banking clients. The self-sovereign identity market size for individual credentials underpins subsequent extensions into enterprise and device realms. IoT and device identity applications are poised for an 82.87% CAGR to 2030, driven by connected-car security, smart-grid management, and industrial sensor authentication. Automotive manufacturers now embed verifiable device credentials that authorize over-the-air updates while protecting owner privacy. Manufacturers of smart meters, routers, and drones are likewise adopting decentralized onboarding to neutralize certificate-authority single points of failure, signaling that device identity will broaden revenue diversity.

Interplay between personal and device credentials unlocks novel experiences. Drivers can authenticate to shared vehicles with a face scan that resolves to a verifiable credential, while household members delegate limited-time access rights to delivery robots. These cross-domain workflows push vendors to build delegation protocols and multi-signature schemes that were unnecessary in early consumer wallets. In turn, identity-platform roadmaps increasingly include hierarchical key management and secure-element integration across automotive, industrial, and consumer electronics supply chains.

By Application: Verifiable Credentials Lead While Supply Chain Accelerates

Verifiable credentials and e-KYC workloads accounted for 37.32% of the self-sovereign identity market size in 2024 as banks, fintechs, and telecom operators sought frictionless onboarding. Banks reduce repetitive KYC checks by referencing portable credentials previously validated by peer institutions, shrinking onboarding spend and boosting conversion rates. Authentication and access-management systems anchor these higher-level workflows by supplying proof-presentation APIs that integrate with existing IAM stacks. Payments, insurance, and healthcare providers then layer context-specific attestations on top of the common wallet substrate.

Supply-chain provenance solutions hold the highest growth outlook, tracking an 82.36% CAGR, due to incoming product-passport regulations. The EU Battery Passport mandate compels manufacturers to embed immutable life-cycle data in every cell shipped after 2027. Projects such as Spherity’s credential platform show how SSI makes regulatory compliance and circular-economy reporting financially viable. Across fashion, food, and pharmaceuticals, brand owners leverage tamper-proof identifiers to document sourcing and carbon footprints, turning compliance duties into consumer-trust differentiators. Government agencies also explore SSI to digitize trade paperwork, slashing customs clearance time and fraud risk.

By End-User Industry: BFSI Leadership Amid Mobility Transformation

Banks, insurers, and capital markets firms held 28.73% of the self-sovereign identity market share in 2024 because reusable KYC networks immediately translate to cost savings and fraud-loss mitigation. Large financial institutions deploy credential overlays atop existing core-banking systems to shorten account-opening times and align with stringent anti-money-laundering statutes. Government agencies supply authoritative ID proofs, letting lenders lean on higher-assurance attestations rather than redundant document scans. As wallet adoption scales, cross-border remittance corridors gain efficiency because both sender and receiver organizations rely on shared credential schemas.

Mobility and transportation stand out with an 82.51% CAGR to 2030, reflecting the convergence of travel, automotive, and urban-mobility ecosystems. IATA’s Digital Travel Credentials let passengers move through security and boarding by presenting wallet-stored passports and visas, cutting checkpoint dwell time. Car-sharing and micromobility platforms rely on verifiable driver credentials to automate rental approvals and insurance coverage. As autonomous-vehicle fleets proliferate, each robotaxi needs a device credential, while passengers supply personal assertions that satisfy safety and insurance rules. This dual-credential paradigm accelerates SSI penetration throughout transport value chains.

Geography Analysis

North America retained 44.87% of the self-sovereign identity market size in 2024 because federal and state agencies embraced wallet pilots under NIST 800-63-4. Programs such as the Transportation Security Administration’s mobile driver’s license verification modernize airport security checkpoints while feeding domestic wallet ecosystems. Fintech hubs in New York and San Francisco integrate verifiable credentials into neobank onboarding, creating a virtuous loop that drives platform utilization across retail investors, gig-economy platforms, and healthcare portals. Canada’s public-private Digital Identity and Authentication Council cultivates cross-province credential frameworks that dovetail with U.S. specifications, and Mexico’s fintech law spurs wallet deployment among challenger banks. High smartphone penetration and developer talent density further sustain the region’s leadership.

Europe ranks second in value terms thanks to eIDAS 2.0, which establishes a binding obligation for every member state to issue at least one digital wallet by 2026. Germany invests in blockchain-backed identity registries for public-administration services, France integrates health-insurance cards into citizen wallets, and the United Kingdom advances post-Brexit trust-framework certifications. The European Blockchain Services Infrastructure underpins cross-border verification, letting residents open bank accounts, sign property deeds, or claim social benefits abroad without re-presenting paper ID. EU data-sovereignty norms such as GDPR favor user-centric wallets that store minimal personal data on servers, reinforcing SSI design principles.

Asia-Pacific posts the fastest regional trajectory with an 82.47% CAGR. Japan leads with My Number card integration into major smartphone wallets, providing consumers instant proof of age, address, and tax identification within a privacy-preserving container. India explores SSI overlays on its Aadhaar infrastructure to enable selective-disclosure proofs in credit scoring and gig-worker insurance. South Korea’s digital-driver-license pilot couples with major bank apps, while Australia’s Trusted Digital Identity Framework expands wallet-acceptance in healthcare and education. China focuses on state-controlled digital ID, but pilot zones in Hong Kong test decentralized proofs for cross-border e-KYC within fintech sandboxes. Regional consortiums craft interoperability profiles to support cross-border trade in the Association of Southeast Asian Nations, further intensifying adoption.

The Middle East and Africa, and South America form emerging hot spots. Brazil committed to blockchain-based citizen ID by 2032, aiming to simplify public-service access and reduce document forgery. South Africa expands smart-ID cards into mobile credentials and pilots SSI for welfare disbursement. Gulf Cooperation Council countries experiment with blockchain passports to streamline expatriate labor onboarding. Limited smartphone reach and patchy internet coverage act as near-term brakes, yet rising investment in 4G and 5G networks points toward rapid leapfrog adoption once device costs decline.

Competitive Landscape

The market remains fragmented as dozens of pure-play SSI specialists, blockchain foundations, and traditional IAM vendors vie for traction. Consolidation has begun: SelfKey, SingularityDAO, and Cogito Finance merged to build an EVM Layer-2 network specializing in AI-enhanced digital-identity workflows, illustrating how firms combine liquidity, R&D, and community governance to amplify reach. Platform vendors increasingly pursue ecosystem alliances; Dock Labs joined forces with cheqd to couple credential-management APIs with privacy-preserving tokenomics, easing integration complexity for enterprises. Established IAM leaders such as Ping Identity accelerated capability expansion by merging with ForgeRock to deliver end-to-end customer identity and decentralized wallet orchestration.

Competitive strategies split along vertical-integration lines. Some players bundle issuance, wallet SDKs, and verification gateways, courting regulated sectors that demand single-vendor accountability. Others concentrate on ledger infrastructure, inviting third-party developers to layer services above. Industry-specific entrants target healthcare research consents, academic transcript attestation, or automotive telematics, leveraging domain know-how to outmaneuver horizontal platforms. Regulatory fluency becomes a decisive differentiator as cross-border banks and airlines require suppliers versed in both GDPR and NIST. Forward-looking vendors invest in privacy-tech R&D, including zero-knowledge machine-learning and post-quantum cryptography, to future-proof deployments against evolving compliance mandates.

M&A momentum is expected to continue as investors recognize overlapping codebases and customer pools that can be synthesized for scale. Private-equity interest has grown, particularly in services firms with certified SSI practitioners. Meanwhile, open-source foundations strengthen governance procedures to attract government contracts that often stipulate transparent code. Network-effects logic suggests the field will tilt toward a handful of credential schemas and verification APIs, with niche specialists orbiting around dominant ledger networks and wallet frameworks. However, regional sovereignty policies may still safeguard local champions in critical infrastructure sectors.

Self-Sovereign Identity (SSI) Industry Leaders

Civic Technologies, Inc.

Validated ID, S.L.

Trinsic, Inc.

Jolocom GmbH

Ontology Foundation Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Google Cloud integrated with Self Protocol to embed zero-knowledge proof APIs and AI tooling that streamline Web3 credential checks across cloud workloads.

- January 2025: Dock Labs and cheqd formed a strategic alliance, merging credential SDKs with ledger utility tokens to promote global wallet interoperability.

- January 2025: Prove acquired Portabl to extend reusable digital-identity services inside its authentication suite.

- November 2024: Token-holders of SelfKey, SingularityDAO, and Cogito Finance approved a merger creating Singularity Finance focused on AI-driven decentralized identity.

Global Self-Sovereign Identity (SSI) Market Report Scope

| Platform / Software |

| Services |

| Individual Identity |

| Organizational / Enterprise Identity |

| IoT / Device Identity |

| Authentication / Access Management |

| Payments and Financial Services |

| Verifiable Credentials and e-KYC |

| Supply-Chain and Provenance |

| Other Applications |

| Banking, Financial Services and Insurance (BFSI) |

| Government and Public Sector |

| Healthcare and Life Sciences |

| IT and Telecom |

| Retail and e-Commerce |

| Mobility and Transportation |

| Other End-User Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Offering | Platform / Software | ||

| Services | |||

| By Identity Type | Individual Identity | ||

| Organizational / Enterprise Identity | |||

| IoT / Device Identity | |||

| By Application | Authentication / Access Management | ||

| Payments and Financial Services | |||

| Verifiable Credentials and e-KYC | |||

| Supply-Chain and Provenance | |||

| Other Applications | |||

| By End-User Industry | Banking, Financial Services and Insurance (BFSI) | ||

| Government and Public Sector | |||

| Healthcare and Life Sciences | |||

| IT and Telecom | |||

| Retail and e-Commerce | |||

| Mobility and Transportation | |||

| Other End-User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

How fast is the self-sovereign identity market growing?

The self-sovereign identity market is forecast to expand from USD 3.25 billion in 2025 to USD 65.55 billion by 2030, reflecting an 82.40% CAGR.

Which segment is expanding the quickest?

Services display the sharpest rise with an 83.14% CAGR as enterprises seek integration and compliance support.

What use case dominates adoption today?

Verifiable credentials and e-KYC lead with 37.32% share because banks and telecoms gain immediate onboarding savings.

Which region will add the most new revenue by 2030?

Asia-Pacific is projected to post the largest incremental gains, growing at an 82.47% CAGR on the back of government wallet mandates and high smartphone adoption.

Why are Web3 wallets relevant to corporate identity plans?

Web3 wallets now bundle payment keys with verifiable credentials, letting firms unify customer onboarding, payments, and access control under one cryptographic container.

What main risk could slow enterprise rollouts?

Incomplete interoperability standards beyond W3C specifications create uncertainty about cross-platform credential portability, prompting some firms to delay full production.

Page last updated on: