Seitan Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Market Size (2025) | USD 92.54 Million |

| Market Size (2030) | USD 133.22 Million |

| Growth Rate (2025 - 2030) | 7.56% CAGR |

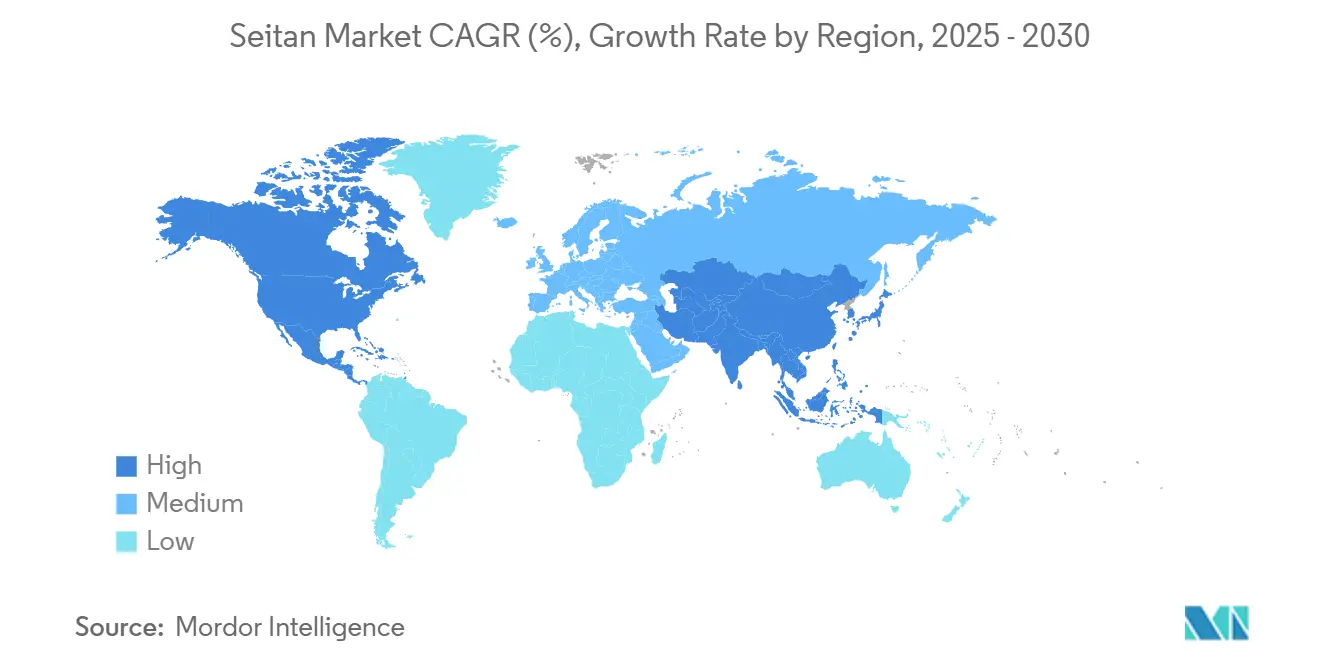

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Seitan Market Analysis by Mordor Intelligence

The seitan market size stands at USD 92.54 million in 2025 and is forecast to reach USD 133.22 million by 2030, advancing at a 7.56% CAGR. This wheat-based meat alternative represents a specialized segment within the broader plant-based protein ecosystem, distinguished by its unique gluten-derived texture that closely mimics animal muscle fibers. Unlike conventional plant proteins that rely on processing aids to achieve meat-like characteristics, seitan's inherent viscoelastic properties stem from vital wheat gluten's natural protein network, positioning it as a premium alternative for consumers seeking authentic meat experiences without compromising dietary preferences. The FDA's June 2025 draft guidance on plant-based alternative labeling provides regulatory clarity that could accelerate mainstream adoption [1]Source: U.S Food and Drug Administration, "Labeling of Plant-Based Alternatives to Animal-Derived Foods", fda.gov. Supply chain vulnerabilities present both challenges and opportunities, as wheat price volatility in Q2 2024 demonstrated the market's exposure to agricultural commodity fluctuations. Geopolitical tensions, particularly the Russia-Ukraine conflict, combined with adverse weather conditions affecting major wheat-producing regions, created supply constraints that elevated input costs. Altogether, the seitan market shows balanced growth opportunities across both heritage Asian users and new Western adopters.

Key Report Takeaways

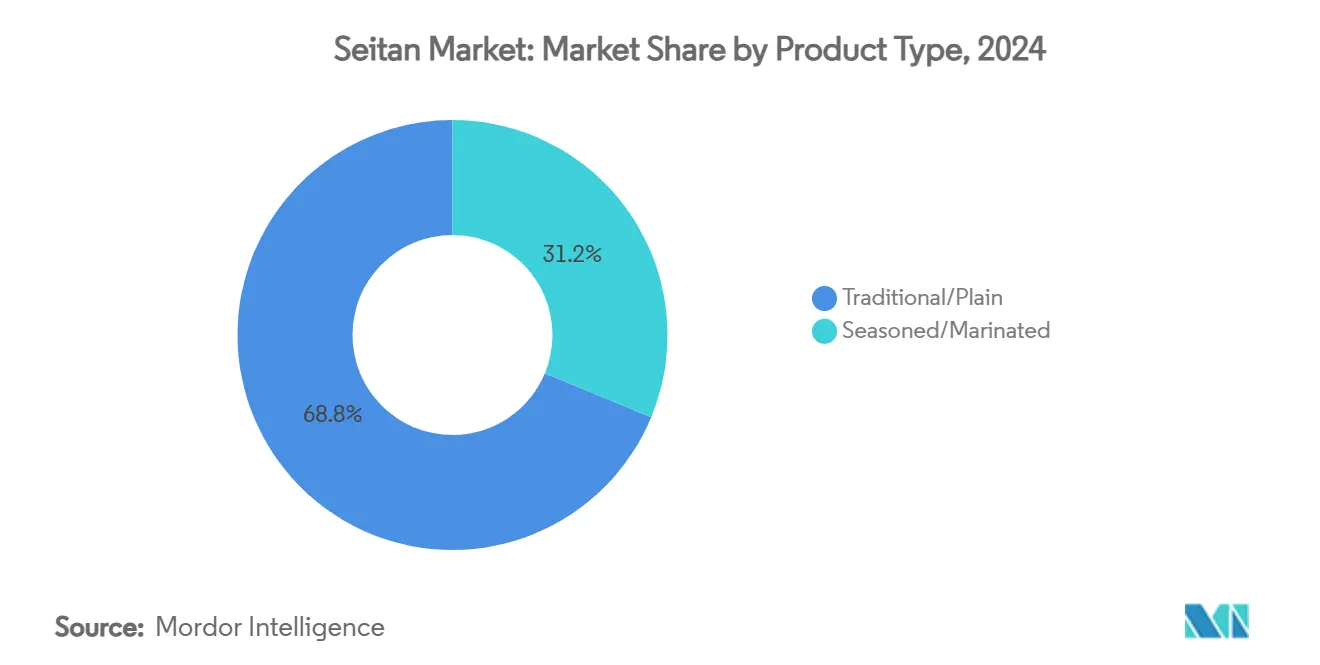

- By product type, Traditional/Plain captured 68.76% of seitan market share in 2024; Seasoned/Marinated is projected to lead growth at an 8.34% CAGR through 2030.

- By category, Conventional products accounted for 85.11% share of the seitan market size in 2024, while Organic is set to expand at a 9.34% CAGR between 2025 and 2030.

- By form, Strips/Steaks held 45.32% of seitan market share in 2024 and Ground/Crumbles is advancing at an 8.63% CAGR through 2030.

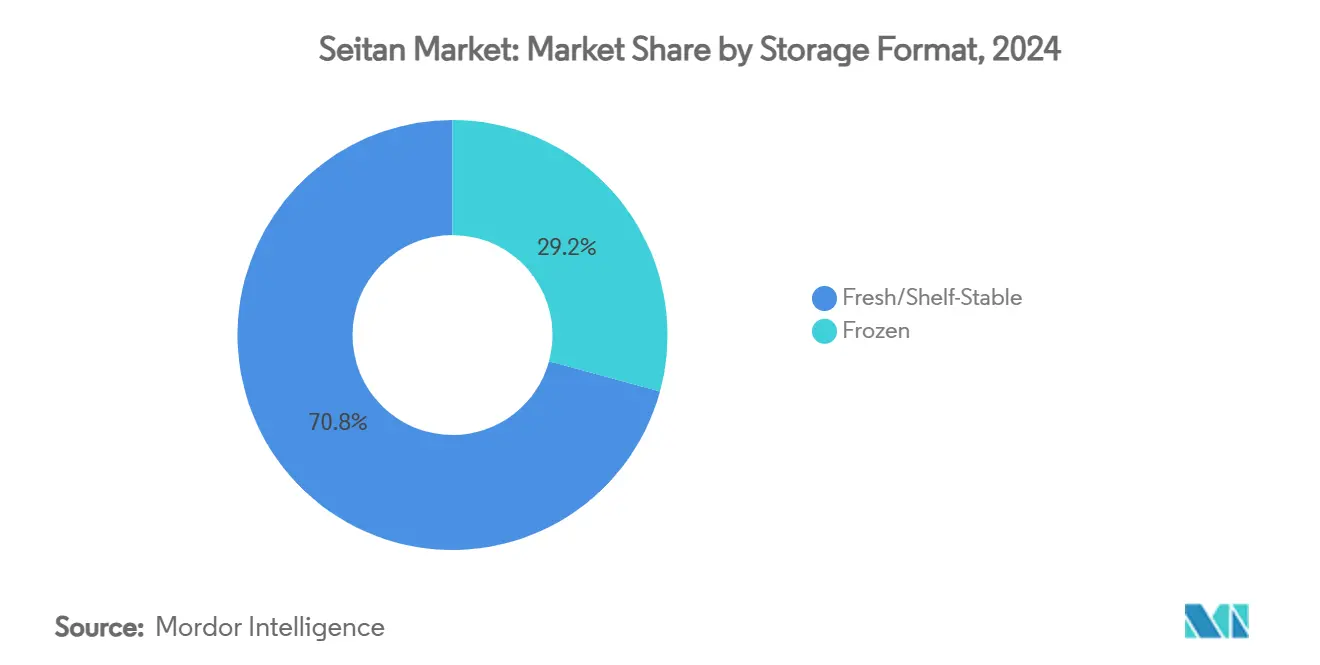

- By storage format, Fresh/Shelf-Stable products commanded 70.76% share of the seitan market size in 2024; Frozen formats are expected to grow at a 9.77% CAGR to 2030.

- By distribution channel, Off-Trade/Retail held 60.75% of seitan market share in 2024, whereas On-Trade/Foodservice is forecast to post an 8.38% CAGR through 2030.

- By geography, North America dominated with 38.05% share of the seitan market size in 2024; Asia-Pacific is on track for a 9.77% CAGR to 2030.

Global Seitan Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vegan And Vegetarian Diets | +1.8% | Global, with concentration in North America & Europe | Long term (≥ 4 years) |

| Foodservice Sector Adoption | +1.5% | North America & Asia-Pacific core, spill-over to Europe | Medium term (2-4 years) |

| Innovations In Product Development | +1.2% | Global, led by North America & Europe | Short term (≤ 2 years) |

| Consumer Health Awareness | +1.0% | Global | Long term (≥ 4 years) |

| Soy-Allergic Consumers | +0.8% | North America & Europe primarily | Medium term (2-4 years) |

| Convenience And Ready-To-Eat (RTE) Plant-Based Meals | +0.9% | Global, with early gains in North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Vegan And Vegetarian Diets

The proliferation of plant-based dietary patterns creates sustained demand momentum for seitan, particularly among consumers seeking protein-dense alternatives that replicate meat's textural complexity. In 2025, according to the World Population Review, countries with the highest share of vegans are India-9%, Mexico-9%, Israel-5%, Canada-4.6%, and Ireleand-4.1% [2]Source: World Population Review, "Countries with the Highest Share of Vegans", worldpopulationreview. Global plant-based sales increased 5% in 2024 despite US market setbacks, indicating resilient international adoption patterns that favor wheat-based proteins over soy alternatives. Seitan's protein density of approximately 19 grams per 100 kilocalories positions it favorably against other plant proteins, though its lysine deficiency necessitates complementary amino acid sources, creating opportunities for fortified product variants. The demographic shift toward flexitarian consumption patterns, rather than strict veganism, expands seitan's addressable market beyond traditional plant-based consumers to mainstream protein seekers. This dietary evolution coincides with growing awareness of environmental impacts, as plant-based proteins demonstrate significantly lower greenhouse gas emissions and water usage compared to animal proteins. The sustained nature of this trend suggests long-term market expansion potential, particularly as younger demographics prioritize sustainability considerations in food choices.

Foodservice Sector Adoption

The demand for seitan in the foodservice sector is primarily driven by the increasing shift toward plant-based and vegan menu options in restaurants, fast-food chains, and catering services. As more consumers embrace plant-based diets for health, ethical, and environmental reasons, foodservice providers are expanding their offerings to include high-protein, versatile meat alternatives like seitan. Seitan’s neutral taste and meat-like texture enable chefs to incorporate it into a wide variety of dishes, from burgers and sandwiches to stir-fries and ethnic cuisines, allowing customization to diverse flavor profiles which align well with current culinary trends. Additionally, the rapid growth of vegan and vegetarian populations, especially among younger and urban demographics, is fueling demand in foodservice. Quick-service restaurants and casual dining chains, in particular, are adopting seitan as a clean-label, minimally processed, and nutritionally appealing protein source to attract health-conscious customers and meet sustainability goals. IFIC (International Food Information Council) reports that in 2023, U.S. consumers regularly purchased food or beverages based on labels: 40% favored "natural," 30% opted for "organic" and "no added hormones," 29% chose "locally sourced" and "clean ingredients," and 28% selected "non-GMO," among other labels[3]Source: IFIC (International Food Information Council)," Consumers who buy food or beverages on a regular basis based on labels", ific.org. The ability to offer affordable, high-protein plant-based menu items addresses customer demands for healthier and more sustainable options without sacrificing taste or texture. This expansion of seitan-based products in foodservice is accelerating the overall market growth.

Soy-Allergic Consumers

Soy protein allergies and sensitivities create dedicated demand for wheat-based alternatives, positioning seitan as a preferred option for consumers unable to consume traditional plant proteins. Allergen contamination studies in wheat flour highlight the importance of clean processing protocols to prevent cross-contamination with soy and other allergenic proteins, ensuring product safety for sensitive populations. The prevalence of soy allergies varies geographically, with higher incidence rates in certain populations creating regional market opportunities for seitan producers. Manufacturing protocols that prevent allergen cross-contamination become competitive advantages, particularly for companies targeting allergen-sensitive demographics. Product labeling and certification programs that verify soy-free status command premium pricing and brand loyalty among affected consumers. The medium-term impact timeline reflects growing awareness of food allergies and increasing diagnosis rates that expand the addressable market for soy-free protein alternatives.

Convenience And Ready-To-Eat (RTE) Plant-Based Meals

The expansion of convenient, shelf-stable seitan products addresses time-constrained consumers seeking quick protein solutions without sacrificing dietary preferences or nutritional goals. Ready-to-eat applications leverage seitan's processing versatility to create products ranging from deli slices to prepared entrees, with companies like Green Wolf Foods achieving triple sales growth since 2022 through innovative applications like seitan salami VegNews. Seitan’s inherent versatility and meat-like texture make it an ideal protein choice for RTE meal formats, which appeal to increasingly busy consumers seeking nutritious, quick, and satisfying food options. Packaged seitan products such as pre-seasoned strips, chunks, slices, and crumbles require minimal preparation—often just heating or light cooking—making them effortless substitutes for meat in wraps, stir-fries, sandwiches, and bowls. This convenience aligns perfectly with the growing consumer preference for healthy, plant-based alternatives that save time without compromising flavor or nutrition. The ready availability of vacuum-packed or frozen seitan ensures freshness and prolonged shelf life, which benefits both retailers and consumers optimizing meal planning. Industry analysis highlights that these convenient, RTE seitan products not only meet the needs of vegetarians and vegans but also attract flexitarians and mainstream consumers increasingly adopting plant-based foods. By addressing the demand for convenience, seitan is becoming a staple in refrigerator aisles and meal kits, expanding its footprint beyond specialty markets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost Volatility in Wheat/Gluten Supply | -0.9% | Global, with acute impact in import-dependent regions | Short term (≤ 2 years) |

| Niche Positioning | -0.7% | North America & Europe primarily | Long term (≥ 4 years) |

| Growing Competition from Other Plant-Based Proteins | -0.6% | Global | Medium term (2-4 years) |

| Stringent Food Safety and Labeling Regulations | -0.4% | North America & Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cost Volatility in Wheat/Gluten Supply

Agricultural commodity price fluctuations create margin pressure for seitan manufacturers, with wheat prices experiencing significant volatility in Q2 2024 due to geopolitical tensions and adverse weather conditions affecting major producing regions. Global wheat production forecasts for 2024-25 indicate tightening supplies amid ongoing conflicts and climate challenges, with ending stocks expected to decline from previous years. Vital wheat gluten, the primary ingredient in seitan production, represents a concentrated form of wheat protein that amplifies commodity price movements, creating operational challenges for manufacturers with limited hedging capabilities. Supply chain disruptions in key wheat-producing regions, particularly Russia and Ukraine, continue to influence global pricing dynamics and availability patterns. Import-dependent regions face acute exposure to currency fluctuations and trade policy changes that compound commodity price volatility. The short-term impact timeline reflects immediate cost pressures that affect production economics and retail pricing strategies, potentially limiting market expansion during periods of elevated input costs.

Stringent Food Safety and Labeling Regulations

Stringent food safety and labeling regulations present a significant challenge to the growth of the seitan market, particularly as producers and distributors strive to comply with complex and evolving standards. Regulatory bodies such as the USDA-FSIS and FDA have intensified oversight on food safety, focusing on preventing contamination from pathogens like Salmonella and Listeria, especially in ready-to-eat and processed protein products. For seitan manufacturers, this means implementing rigorous testing, sanitation, and traceability systems to meet these heightened requirements, often increasing production costs and operational complexity. Labeling regulations also impose strict guidelines on ingredient disclosure, allergen declarations, and truthful marketing claims. As seitan is often positioned as a meat alternative or plant-based protein, regulatory scrutiny over nomenclature, health claims, and source origins can restrict marketing flexibility and require extensive documentation and verification. The emergence of new policies, such as the FDA’s Food Traceability rule under FSMA, compels suppliers to maintain detailed, accurate records along the supply chain, complicating logistics and compliance, especially for small and medium-sized enterprises.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Plain Variants Drive Volume

Traditional/Plain seitan products command 68.76% market share in 2024, reflecting consumer preference for versatile base ingredients that enable customized preparation and flavor development. This dominance stems from foodservice applications where chefs prefer neutral-flavored proteins that accommodate diverse culinary styles and seasoning profiles. Seasoned/Marinated variants achieve 8.34% CAGR growth through 2030, driven by convenience-seeking consumers who value ready-to-cook solutions that reduce preparation time and culinary expertise requirements. The growth differential indicates market bifurcation between professional users who prioritize versatility and retail consumers who seek convenience and flavor innovation.

Advanced processing techniques enable texture differentiation within both segments, with high-moisture extrusion creating more meat-like characteristics that enhance consumer acceptance across applications. Innovation opportunities exist in hybrid products that combine plain bases with separate seasoning packets, enabling customization while maintaining convenience positioning. The segment dynamics suggest premiumization trends in seasoned variants, where unique flavor profiles and artisanal positioning command higher margins compared to commodity-oriented plain products.

By Category: Organic Growth Accelerates

Conventional seitan products maintain 85.11% market share in 2024, supported by established supply chains and cost-competitive positioning that serves price-sensitive consumer segments. However, Organic variants drive category innovation with 9.34% CAGR through 2030, reflecting premiumization trends among health-conscious demographics willing to pay premium prices for certified organic wheat proteins. This growth trajectory aligns with broader organic food market expansion and consumer willingness to invest in perceived health and environmental benefits.

Organic certification requirements create supply chain complexity and cost pressures that limit market participation to larger producers with dedicated sourcing capabilities and certification expertise. Cargill's emphasis on sustainably sourced vital wheat gluten, verified through SAI Platform's Farm Sustainability Assessment, demonstrates industry movement toward traceable and environmentally responsible sourcing practices. The organic segment's growth potential depends on continued consumer education about organic benefits and expanded retail distribution that increases product accessibility beyond specialty channels.

By Form: Ground Products Lead Innovation

Strips/Steaks formats capture 45.32% market share in 2024, leveraging seitan's natural texture advantages that closely replicate muscle meat characteristics without extensive processing modifications. These whole-muscle formats serve premium applications in restaurants and retail where visual meat similarity drives consumer acceptance and willingness to pay higher prices. Ground/Crumbles variants achieve 8.63% CAGR through 2030, driven by versatility in applications ranging from pasta sauces to taco fillings that integrate seamlessly into familiar recipes.

The form segmentation reflects different use cases and preparation methods, with strips/steaks targeting direct meat replacement applications while ground formats enable ingredient substitution in composite dishes. Chunks/Shreds and Sausage/Patty formats serve specific culinary applications, with innovation opportunities in texture modification and flavor enhancement that address remaining gaps in meat replication. Processing technology advances enable form customization that serves both foodservice and retail requirements.

By Storage Format: Frozen Gains Momentum

Fresh/Shelf-Stable products dominate with 70.76% market share in 2024, supported by distribution advantages and consumer preference for immediate consumption without thawing requirements. However, Frozen formats achieve 9.77% CAGR through 2030, driven by extended shelf-life benefits that enable broader geographic distribution and reduced food waste concerns. The frozen segment's growth reflects retail expansion into mainstream grocery channels where frozen plant-based proteins compete directly with conventional frozen meat products.

Temperature-controlled distribution requirements for frozen seitan create logistical complexity and cost pressures that favor larger producers with established cold chain capabilities. Innovation in packaging and preservation technologies enables shelf-stable products with extended shelf life that combine convenience benefits with distribution advantages. The storage format dynamics indicate market maturation, with different formats serving distinct consumer needs and retail channel requirements that drive segmentation and specialization strategies.

By Distribution Channel: Foodservice Momentum Builds

Off-Trade/Retail channels control 60.75% market share in 2024, reflecting established grocery distribution networks and consumer familiarity with retail protein purchasing patterns. However, On-Trade/Foodservice segments demonstrate superior growth at 8.38% CAGR through 2030, driven by restaurant menu diversification and chef adoption of plant-based proteins that showcase culinary creativity. This growth differential indicates foodservice's role as an innovation driver and trial generation channel that influences subsequent retail adoption patterns.

Within retail channels, Supermarkets/Hypermarkets provide volume distribution while Specialty Stores serve niche demographics seeking artisanal or organic variants. Online Retail Stores capture growing e-commerce adoption, particularly among younger consumers comfortable with digital food purchasing and subscription models. The distribution evolution reflects broader retail trends toward omnichannel strategies that serve different consumer preferences and shopping behaviors across demographic segments.

Geography Analysis

North America maintains market leadership with 38.05% share in 2024, supported by established vegan infrastructure, regulatory clarity, and consumer acceptance of wheat-based meat alternatives. The region's dominance reflects early adoption of plant-based diets, sophisticated retail distribution networks, and foodservice integration that normalizes seitan consumption across demographic segments. Recent FDA guidance on plant-based alternative labeling provides regulatory certainty that encourages investment and product development, while USDA oversight frameworks ensure food safety standards that build consumer confidence.

Asia-Pacific emerges as the fastest-growing region with 9.77% CAGR through 2030, driven by traditional familiarity with wheat gluten preparations, expanding middle-class protein consumption, and government support for alternative protein development. The region's growth trajectory benefits from cultural acceptance of plant-based proteins, lower production costs due to proximity to wheat sources, and increasing health consciousness among urban populations. China's plant-based meat market development, supported by favorable demographic trends and environmental awareness, creates substantial opportunities for seitan producers seeking international expansion. Government initiatives across multiple Asia-Pacific countries, including Australia, Japan, Malaysia, Singapore, and South Korea, provide regulatory frameworks and investment incentives that foster alternative protein innovation and market development.

Europe represents a mature market with established organic food channels and sustainability-focused consumers who drive premium product adoption and innovation. The region's projected plant-based protein market growth reflects steady expansion supported by environmental regulations and consumer awareness initiatives. Strategic partnerships, such as Tofoo Co's collaboration with Temple of Seitan in April 2024 for retail product launches, demonstrate market development through brand alliances and distribution expansion. Technology suppliers like Bühler and GEA establish application centers to support plant-based product development, providing infrastructure for innovation and scaling that benefits regional seitan producers.

Competitive Landscape

The global seitan market exhibits moderate fragmentation, indicating balanced competition between established players and emerging specialists without dominant market control by any single entity. This competitive structure reflects the market's evolution from artisanal production to industrial scaling, where traditional Asian manufacturers compete alongside Western plant-based protein companies seeking to diversify their portfolios.

Leading players such as Upton’s Naturals, Nestlé S.A., Ahimsa Companies, etc. dominate the market by offering a wide range of seitan products catering to the growing vegan and vegetarian consumer base. These companies invest heavily in research and development to improve the texture, flavor, and shelf life of seitan, enhancing its acceptance as a meat substitute. The inclusion of organic and seasoned varieties has allowed key players to capture health-conscious and flavor-seeking segments alike. For instance, in April 2024, In a strategic move, The Tofoo Co, a prominent UK tofu brand, rolled out two innovative seitan products. This launch was made possible through a collaboration with Temple of Seitan, a renowned vegan restaurant chain based in London. As a result of this partnership, supermarket shoppers can now find the Original Seitan – a chicken-flavored block previously exclusive to Temple of Seitan's eateries – alongside a new smoky and spicy Pepperoni Seitan. Simultaneously, regional manufacturers in North America, Europe, and Asia are expanding their production capabilities to meet domestic demand, supported by advancements in manufacturing technologies and adherence to stringent food safety regulations.

Competition is also intensifying through product innovation and distribution channel expansion, with many players leveraging e-commerce and direct-to-consumer models alongside traditional supermarkets and specialty stores. Strategic collaborations, acquisitions, and co-branding efforts are common as companies aim to broaden their product portfolios and geographic reach. The market’s competitive dynamics are influenced by fluctuating raw material costs, tariff changes, and regulatory compliance requirements, prompting firms to optimize supply chains and improve operational efficiencies. Overall, the seitan market is evolving with a strong emphasis on sustainability and catering to the increasing preference for plant-based, nutrient-dense foods, positioning innovation and consumer engagement as critical factors for market leadership in the coming years.

Seitan Industry Leaders

-

Upton’s Naturals

-

Nestlé S.A.

-

Ahimsa Companies

-

Wheaty

-

VBites Foods

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Blackbird Foods, a plant-based food company hailing from New York City, rolled out its plant-based wings in Wegmans stores. The brand's Buffalo and Korean BBQ-flavored wings debuted at more than 100 Wegmans locations across the country. Crafted from seitan, a wheat-derived protein, these plant-based wings aim to replicate the texture and flavor of conventional chicken wings.

- May 2023: Dublin-based Thanks Plants rolled out a range of meat alternatives at all 157 ALDI outlets across the Republic of Ireland. These seitan-based products boast natural ingredients, including beans, barley, mustard, vinegar, and spices. Highlighting the lineup, the NoMoooo Burger melds seitan with black beans, pearl barley, fresh carrots, beetroot, and mushrooms.

Global Seitan Market Report Scope

| Seasoned/Marinated |

| Traditional/Plain |

| Organic |

| Conventional |

| Strips/Steaks |

| Chunks/Shreds |

| Ground/Crumbles |

| Sausage/Patty/Other Forms |

| Fresh/Shelf-Stable |

| Frozen |

| On-Trade/Foodservice | |

| Off-Trade/Retail | Supermarkets/Hypermarkets |

| Speciality Stores | |

| Online Retail Stores | |

| Other Retail Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Seasoned/Marinated | |

| Traditional/Plain | ||

| By Category | Organic | |

| Conventional | ||

| By Form | Strips/Steaks | |

| Chunks/Shreds | ||

| Ground/Crumbles | ||

| Sausage/Patty/Other Forms | ||

| By Storage Format | Fresh/Shelf-Stable | |

| Frozen | ||

| By Distribution Channel | On-Trade/Foodservice | |

| Off-Trade/Retail | Supermarkets/Hypermarkets | |

| Speciality Stores | ||

| Online Retail Stores | ||

| Other Retail Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the seitan market?

The seitan market size is USD 92.54 million in 2025.

How fast is the seitan market growing?

Between 2025 and 2030 the market is projected to log a 7.56% CAGR.

Which region shows the highest growth rate?

Asia-Pacific is forecast to grow at a 9.77% CAGR through 2030, the fastest globally.

What product type leads the seitan market?

Traditional/Plain variants hold the largest share at 68.76% of 2024 revenues.

Page last updated on: