E-Liquid Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

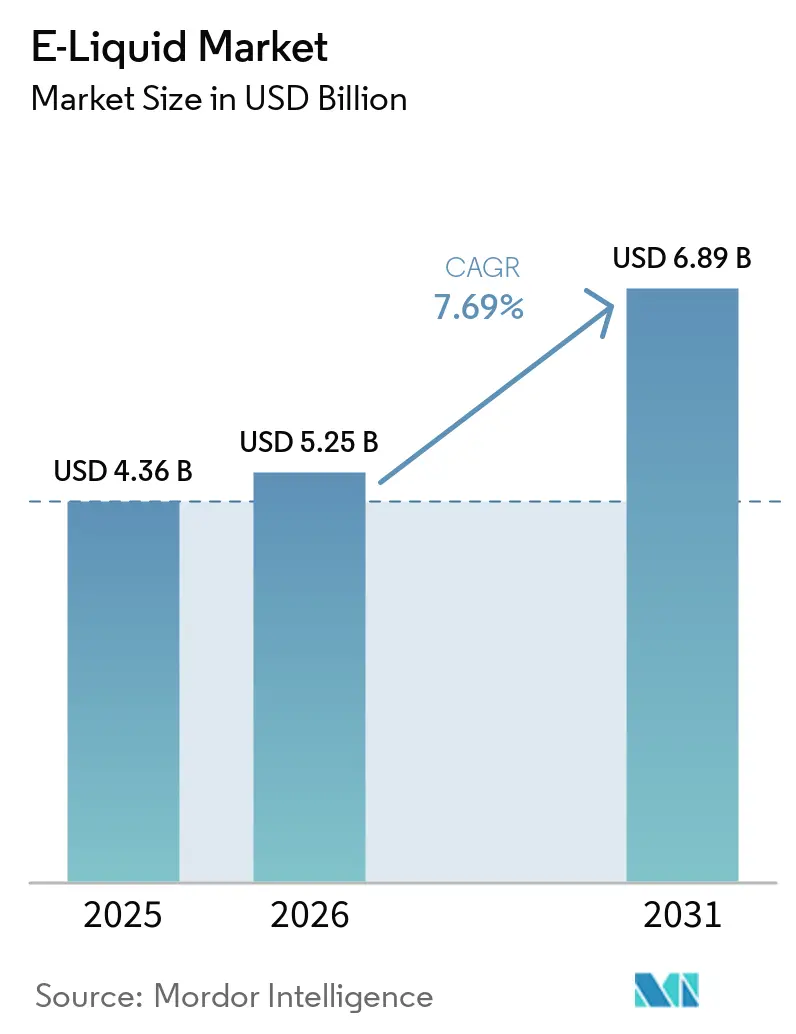

| Market Size (2026) | USD 5.25 Billion |

| Market Size (2031) | USD 6.89 Billion |

| Growth Rate (2026 - 2031) | 7.69% CAGR |

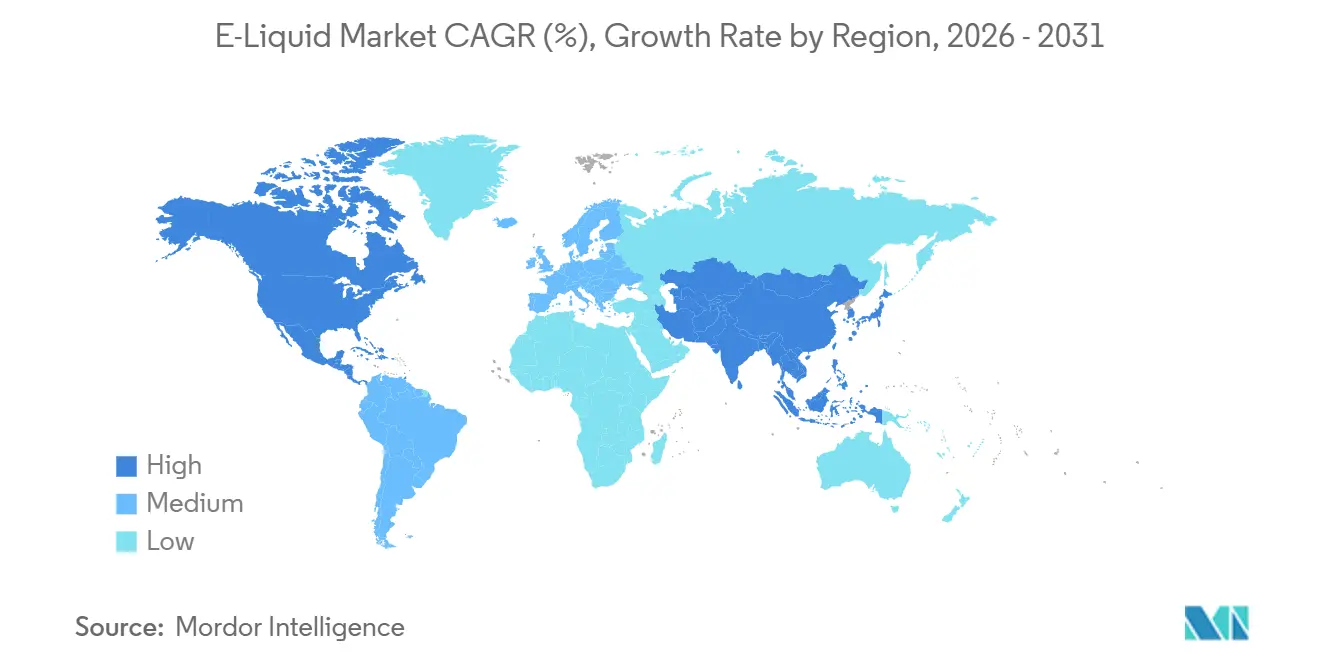

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

E-Liquid Market Analysis by Mordor Intelligence

The e-liquid market size is expected to be USD 4.36 billion in 2025, USD 5.25 billion in 2026, and reach USD 6.89 billion by 2031, growing at a CAGR of 7.69% from 2026 to 2031. Steady demand for reduced-risk nicotine products, the shift from single-use disposables to refillable pod systems, and expanding direct-to-consumer e-commerce are widening the addressable consumer base. Regulatory tightening in North America and Europe is prompting format innovation that limits youth appeal while preserving adult access, a balance that sustains unit growth despite higher compliance costs. Vertically integrated incumbents gain cost advantages by spreading testing, labeling, and logistics expenses across broad portfolios, whereas smaller brands rely on premium positioning and niche flavors to remain competitive. Investments in U.S. smoke-free capacity, Gulf Cooperation Council transparency mandates, and the looming European Union Battery Regulation ban on disposables together define the next five-year strategy playbook for suppliers targeting sustainable share gains in the e-liquid market.

Key Report Takeaways

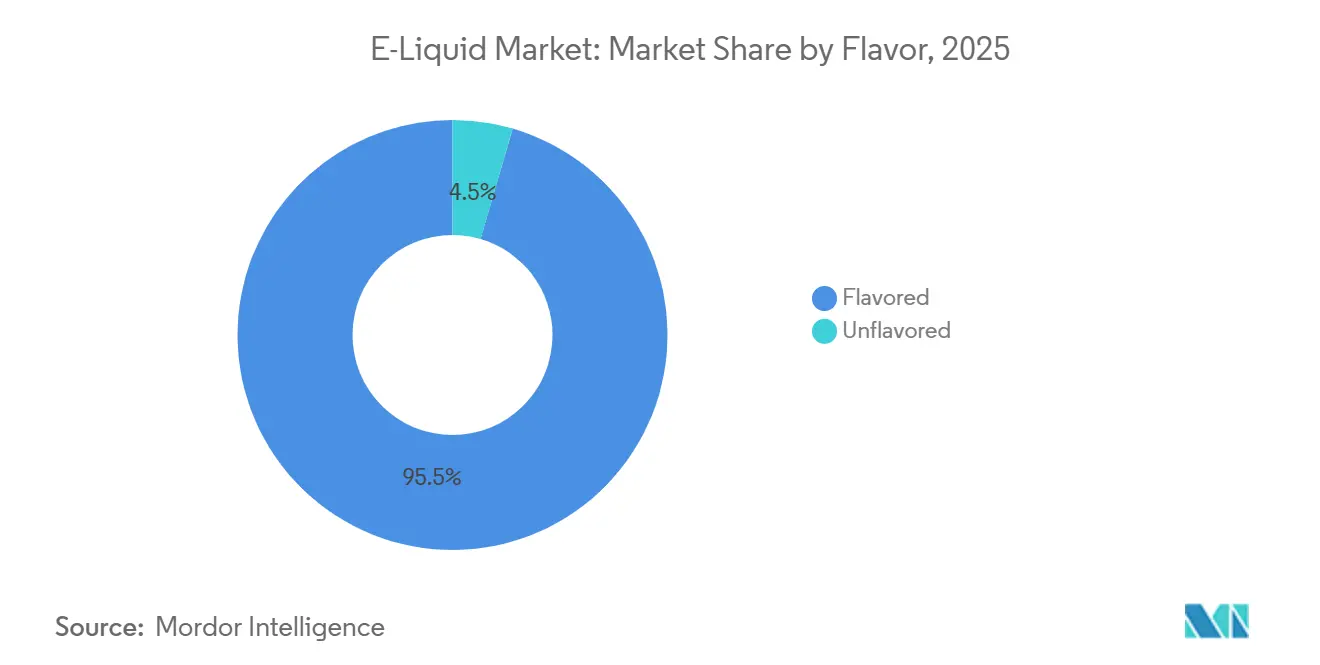

- By flavor, flavored e-liquids led with 95.48% of 2025 revenue; unflavored variants are advancing at a 9.35% CAGR through 2031.

- By bottle size, below-30 ml packs held 65.29% of the e-liquid market share in 2025, while the same segment is projected to expand at a 9.56% CAGR through 2031.

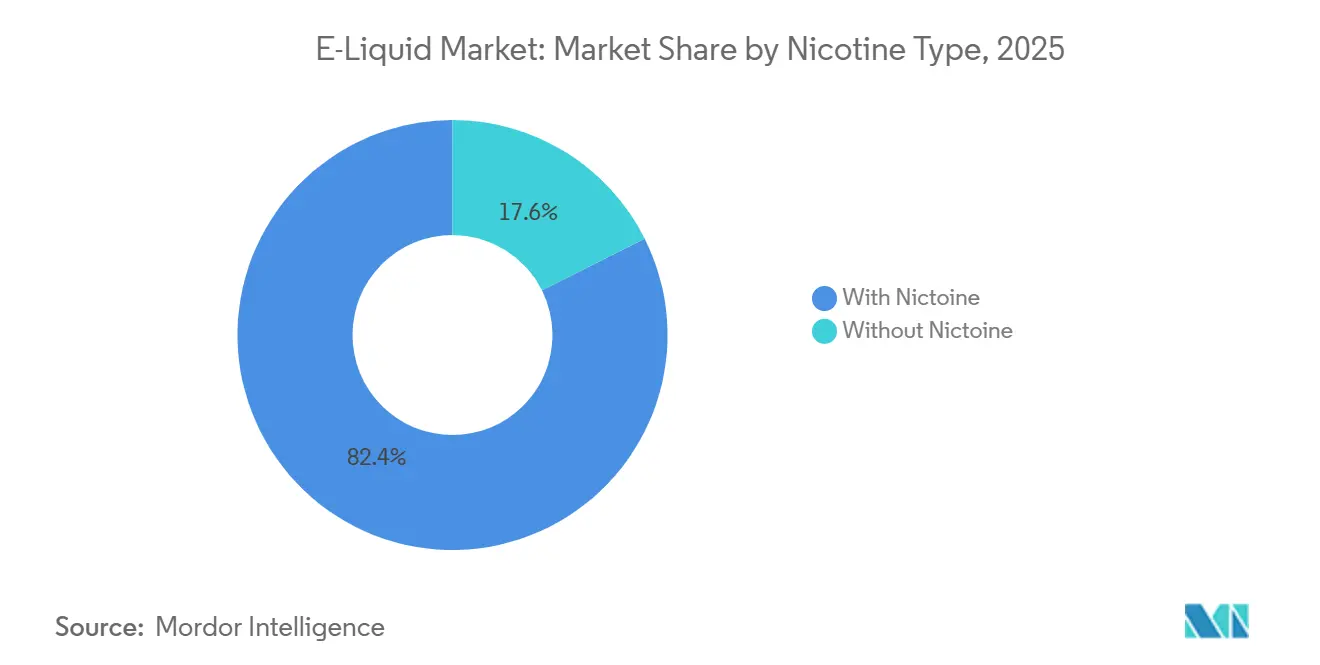

- By nicotine type, formulations containing nicotine commanded 82.38% of 2025 sales; nicotine-free liquids are the fastest mover at a 9.28% CAGR to 2031.

- By distribution, offline stores accounted for 74.32% of the 2025 value, yet online platforms are forecast to post a 9.13% CAGR over the same horizon.

- By geography, North America led with 42.32% 2025 revenue, whereas Asia-Pacific is projected to grow at an 8.65% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global E-Liquid Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Appeal Of Vaping As A Perceived Safer Alternative To Traditional Smoking | +1.8% | Global, with strongest uptake in North America, Western Europe, and developed Asia-Pacific markets | Medium term (2-4 years) |

| Broad Range Of Flavors And Nicotine Strengths Designed To Attract Diverse Consumer Preferences | +1.5% | North America, Europe, and Asia-Pacific; limited in markets with flavor bans (Netherlands, Belgium, Finland, Hungary, Estonia, Latvia, Lithuania) | Short term (≤ 2 years) |

| Convenience And User‑Friendly Nature Of Pre‑Filled Vaping Devices | +1.3% | Global, with accelerated adoption in Europe post-disposable bans (UK, EU Battery Regulation markets) | Short term (≤ 2 years) |

| Expansion Of Online Retail Channels Enhancing Product Availability And Accessibility | +1.2% | North America, Europe, and Asia-Pacific; constrained in China (domestic online sales banned except unified platform) | Medium term (2-4 years) |

| Ongoing Product Innovation In Devices And E‑Liquids | +1.0% | Global, led by Chinese manufacturers (Shenzhen) and multinational tobacco companies | Long term (≥ 4 years) |

| Greater Emphasis On Product Transparency Through Clear Ingredient And Nicotine Labeling | +0.9% | Europe (TPD3 framework), North America (FDA PMTA requirements), UAE (ESMA regulations) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Appeal of Vaping as a Perceived Safer Alternative to Traditional Smoking

Harm-reduction positioning continues to anchor market expansion, yet the narrative is bifurcating between jurisdictions that embrace tobacco-harm-reduction frameworks and those imposing precautionary bans. Philip Morris International's smoke-free portfolio, which now generates 41.5% of net revenues, demonstrates how incumbents are pivoting capital toward reduced-risk products, with VEEV e-vapor unit shipments surging 102% to 3.3 billion in 2025. The company's over USD 20 billion investment since 2022 includes a USD 600 million ZYN nicotine-pouch facility in Colorado that opened in September 2025, signaling a broader shift toward oral nicotine as a complementary category. However, this growth trajectory faces headwinds from markets like India, where the Prohibition of Electronic Cigarettes Act 2019 imposes penalties of up to INR 500,000 (approximately USD 6,000) and 3 years' imprisonment for repeat offenses, yet sustains an estimated annual illicit market of USD 100 million. The regulatory divergence creates a dual-track industry where multinational firms pursue premium, compliant channels in regulated markets while gray-market operators exploit prohibition-driven demand in ban jurisdictions.

Broad Range of Flavors and Nicotine Strengths Designed to Attract Diverse Consumer Preferences

Flavor diversity remains the primary differentiation lever, with flavored formulations holding 95.48% share in 2025, yet regulatory momentum is shifting toward tobacco-only mandates that could reshape product portfolios. Seven European Union member states have enacted flavor bans, and 19 countries now tax vaping products, compressing margins and limiting SKU proliferation. The Fraunhofer Institute projects the EU illicit vape market will expand from EUR 6.6 billion currently to EUR 10.8 billion by 2030, driven largely by flavor bans that push consumers toward unregulated suppliers. This unintended consequence reveals a strategic blind spot: overly restrictive flavor policies erode tax revenue and public-health oversight without curbing demand. Conversely, markets like Chile, which implemented Law 21,642 in January 2024 with a 45mg/mL nicotine cap and mandatory health warnings but preserved flavor availability, demonstrate a middle path that balances youth-access controls with adult consumer choice.

Convenience and User-Friendly Nature of Pre-Filled Vaping Devices

Pre-filled pod systems are capturing share from both disposables and open-tank refillables, driven by regulatory bans on single-use formats and consumer demand for hassle-free operation. The United Kingdom's disposable vape ban, effective June 1, 2025, catalyzed a market pivot toward pre-filled pods that offer plug-and-vape simplicity with 2ml capacities and 7-14 day pod lifespans, reducing annual costs to USD 160-189 compared to USD 720-1,200 for disposables. This 74% cost differential is reshaping purchasing behavior, particularly among price-sensitive demographics. The European Union Battery Regulation, which bans disposable vapes from February 2027, will extend this dynamic across 27 member states, forcing manufacturers to retool production lines and retailers to reconfigure inventory. Elfbar's ELFX Ultra, launched in August 2025 with a child-lock mechanism and InnoGate app integration, exemplifies the format evolution, combining convenience with compliance features like age verification and usage tracking. The shift also benefits e-liquid suppliers, as pre-filled pods require standardized formulations and higher-volume contracts compared to the fragmented demand from open-system users.

Expansion of Online Retail Channels Enhancing Product Availability and Accessibility

Digital distribution is advancing at 9.13% CAGR, outpacing offline's 7.69% baseline, as brands leverage direct-to-consumer models to bypass retailer margins and capture first-party data. However, regulatory constraints fragment the opportunity: China banned domestic online e-cigarette sales except through a unified government platform, while the FDA's March 2026 draft guidance on flavored ENDS imposes premarket tobacco application requirements that raise compliance costs for online sellers[1]Source: U.S. Food and Drug Administration, “Premarket Tobacco Product Applications for Electronic Nicotine Delivery Systems,” fda.gov. The UK's Tobacco and Vapes Bill 2024 introduces age-verification mandates and advertising restrictions that require online platforms to implement robust identity-checking systems, adding friction to the purchase funnel. Despite these hurdles, subscription models are gaining traction, offering consumers automated replenishment and brands predictable revenue streams. Dinner Lady's partnerships with EG Group (402 stores) and ASDA (500 stores) demonstrate a hybrid approach, securing physical shelf space while maintaining a direct online presence that serves 115+ countries. The channel's growth hinges on balancing convenience with compliance, as jurisdictions tighten cross-border sales and age-verification protocols.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict Regulations Governing Nicotine Levels And Advertising Restrictions | -1.4% | Global, with most stringent enforcement in Europe (TPD3), North America (FDA PMTA), UAE (ESMA), and China (STMA) | Medium term (2-4 years) |

| Consumer Health Worries About The Long‑Term Effects Of Regular Vaping | -0.8% | North America and Europe, where public-health campaigns and media coverage are most active | Long term (≥ 4 years) |

| Challenges In Securing Stable Supplies And Raw Materials For E‑Liquid Production | -0.6% | Global, with acute impact in Asia-Pacific (propylene glycol supply) and regions dependent on Southeast Asian vegetable glycerin | Short term (≤ 2 years) |

| Complex And Frequently Changing Compliance Requirements Across Markets | -0.5% | Global, with highest friction in multi-jurisdiction operators navigating EU member-state divergence, US state-level patchwork, and Asia-Pacific regulatory experimentation | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strict Regulations Governing Nicotine Levels and Advertising Restrictions

Regulatory fragmentation is compressing addressable markets and elevating compliance costs, with divergent nicotine caps and advertising bans creating operational complexity for multinational operators. The UAE's 20mg/mL nicotine limit and 10ml container cap align with European Union Tobacco Products Directive standards, yet markets like Chile permit 45mg/mL concentrations, forcing brands to maintain parallel SKU portfolios, according to the Emirates Authority for Standardization and Metrology[2]Source: Emirates Authority for Standardization and Metrology, “Technical Regulation EVAS/TR 01:2023,” esma.gov.ae. China's State Tobacco Monopoly Administration enforcement intensified in 2025, with 19,896 administrative cases and 5,539 criminal cases resulting in over 63.145 million illegal products seized and case values exceeding CNY 15 billion (approximately USD 2.1 billion) Vaping360. The UK's Vaping Products Duty, set at EUR 2.20 per 10ml effective October 2026, will add approximately 15-20% to retail prices, potentially dampening volume growth and incentivizing down-trading to lower-nicotine formulations. The FDA's March 2026 draft guidance on flavored ENDS introduces premarket tobacco application pathways that require clinical evidence of reduced youth appeal, a standard that smaller brands lack the resources to meet. This regulatory ratcheting favors vertically integrated tobacco companies like Philip Morris International, which deployed over USD 20 billion in US smoke-free infrastructure and can amortize compliance costs across broader portfolios.

Consumer Health Worries About the Long-Term Effects of Regular Vaping

Persistent uncertainty around long-term health outcomes is constraining market penetration among risk-averse demographics, despite harm-reduction claims relative to combustible tobacco. Public-health agencies in North America and Europe have issued cautionary guidance, creating a perception gap between industry messaging and official recommendations. This ambiguity is most pronounced in markets like Australia, which adopted a prescription-based model that treats nicotine vaping as a therapeutic intervention rather than a consumer product, limiting the market to USD 492 million in 2024. The lack of longitudinal clinical data on e-liquid inhalation effects, particularly for flavored formulations containing aldehydes and other thermal-degradation byproducts, leaves brands vulnerable to adverse study findings that could trigger regulatory backlash. Japan's classification of nicotine e-liquids as pharmaceutical products under the Pharmaceutical Affairs Law reflects this precautionary stance, requiring licenses to sell and constraining distribution to pharmacy channels.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Flavor: Tobacco-Only Mandates Accelerate Unflavored Growth

In 2025, flavored products accounted for a significant 95.48% of the turnover. However, these products are under increasing scrutiny from policymakers. At the same time, the e-liquid market is experiencing a shift, with unflavored lines projected to grow at an impressive 9.35% CAGR, surpassing the overall market growth. This trend is primarily driven by the alignment of risk-averse consumers and regulators who prefer simpler ingredient profiles. Premium brands are strategically emphasizing dessert and beverage notes, which not only help sustain profit margins but also position these flavors as alternatives for adult smokers, avoiding appeal to younger audiences. Nevertheless, a major challenge persists: seven EU nations have already prohibited non-tobacco flavors, disrupting supply chains and pushing price-sensitive consumers toward illicit imports.

The rise in unflavored product demand is also associated with the gradual reduction in nicotine strength. Many former smokers transitioning to zero-nicotine options prefer neutral flavors to avoid reminders of cigarettes. In North America, transparent bottle labeling and ISO-certified purity enhance consumer trust, enabling brands to justify slight price premiums. Flavor houses are responding by developing heat-stable compounds that reduce carbonyl formation, serving as a precaution against potential widespread flavor bans. As the e-liquid market continues to evolve, portfolio planners face the challenge of balancing flavor innovation with the preparation of contingency SKUs for markets with flavor restrictions.

By Bottle Size: Sub-30 ml Packs Align With Policy Caps

By 2025, formats under 30 ml contributed 65.29% of the revenue and are expected to grow at a strong 9.56% CAGR through 2031. The EU's 10 ml restriction on nicotine liquids, along with the UAE's 10 ml container regulation, is driving demand for smaller bottles, ensuring both portability and compliance with regulations. At the same time, the market share for 30-to-60 ml e-liquids is shrinking. This reduction is primarily due to excise taxes linked to volume, which erode their cost advantage, a trend likely to accelerate with the upcoming U.K. duty.

Small packs are becoming increasingly popular, particularly with pod-based devices that use 2 ml cartridges. Consumers often opt for multiple smaller flavor shots instead of a single large bottle, increasing overall liquid sales. Packaging suppliers are differentiating themselves with features such as child-resistant caps and laser-etched batch codes, which simplify retail audits. While bottles over 60 ml still appeal to hobbyists using open-tank systems, this segment is declining. Mainstream users are shifting towards convenience, and the adoption of higher-efficiency coils has significantly reduced refill frequency.

By Nicotine Type: Zero-Nicotine Liquids Gain New Followers

Nicotine-free liquids represented only 17.62% of 2025 sales but are growing at a strong 9.28% CAGR, the fastest within the category. In regions where nicotine e-liquids face pharmaceutical or excise restrictions, zero-nic variants effectively bypass these regulatory barriers, expanding their retail availability. While the market for nicotine-containing e-liquids remains much larger than that of zero-nic products, the latter's market share is steadily increasing as health-conscious consumers shift their focus to flavor over nicotine's pharmacological effects.

Japan exemplifies this divide: nicotine e-liquids are limited to pharmacies, whereas zero-nic variants are widely available in convenience stores. This accessibility drives greater brand visibility without the need for prescriptions. Additionally, ingredient suppliers are innovating synthetic cooling agents that replicate the throat hit of nicotine, reducing the perceived satisfaction gap for zero-nic products. In response, multinationals are introducing dual product launches, enabling them to quickly adapt to any future tightening of nicotine regulations.

By Distribution Channel: Digital Sales Outpace Storefront Growth

Offline Stores represented 74.32% of the 2025 turnover. Meanwhile, online stores are expected to grow at a 9.13% CAGR, surpassing the growth rate of physical outlets. Subscription clubs provide consistent volume and offer loyalty rewards that rival traditional discounts, such as those on cigarette cartons. If regulatory frameworks focus on secure ID verification instead of outright web bans, the online segment of the e-liquid market could double in size by 2031.

Offline outlets remain essential for first-time buyers seeking device demonstrations and immediate purchases. Leading brands are implementing hybrid strategies: they showcase primary SKUs in grocery chains while promoting flavor extensions exclusively online, simplifying planogram management. Direct sales data analytics drive rapid flavor rotations, keeping physical store assortments fresh and minimizing markdown risks.

Geography Analysis

In 2025, North America contributed 42.32% of global revenues, with the U.S. leading due to its extensive distribution networks, established hardware ecosystems, and a large smoker population. Since 2022, Philip Morris International has invested over USD 20 billion in U.S. smoke-free infrastructure, including a USD 600 million nicotine-pouch facility launched in Colorado in 2025. While FDA's pre-market pathways increase entry barriers, they also enhance consumer trust, supporting premium-brand pricing. Europe presents a varied landscape. The U.K.'s disposable ban, effective June 2025, has driven a shift to refillable pods, reducing annual consumer spending by approximately 74%, according to the Government of the United Kingdom [3]Source: GOV UK, “Excise Duty: Vaping Products Duty,” gov.uk. The upcoming EU Battery Regulation will eliminate single-use devices across 27 countries by February 2027, requiring manufacturers to quickly adapt their portfolios. Furthermore, a EUR 2.20 per 10 ml duty, starting October 2026, is expected to raise price floors, potentially reducing volume but increasing tax revenues.

Asia-Pacific is the key growth region, with a projected CAGR of 8.65% through 2031E. China’s capacity caps and mandatory plant registrations are limiting unchecked expansions while protecting established players from oversupply risks. Japan’s pharmacy-only rule for nicotine liquids supports a thriving zero-nicotine market, while Australia’s prescription model demonstrates how medical frameworks can coexist with commercial supply chains. Latin America features a mix of restrictive and liberal policies. Chile’s 2024 Law 21 642 maintained the legality of flavors but introduced a 45 mg/ml nicotine cap and enforced 18+ age verification. Although Brazil continues to ban sales, cross-border e-commerce sustains a significant gray market, highlighting how outright bans often redirect demand rather than eliminate it.

The Middle East and Africa exhibit diverse dynamics. The UAE’s ESMA code enforces some of the world’s strictest labeling requirements while allowing compliant products to succeed. Saudi Arabia’s ongoing ban has resulted in spillover purchases in Bahrain and the UAE. In sub-Saharan Africa, Nigeria and South Africa, two of the region’s fastest-growing economies, currently lack comprehensive regulations, creating opportunities for early entrants focused on quality assurance and youth protection.

Competitive Landscape

Competitive intensity holds a moderate rank. While no single entity dominates, with none surpassing a tenth of the global retail value, the top five suppliers collectively command around 40%. This concentration earns the e-liquid market a label of 5. In 2025, Philip Morris International (PMI) reported a remarkable 102% year-on-year surge in VEEV e-vapor shipments, totaling 3.3 billion units. Notably, PMI's smoke-free revenue share reached 41.5%, highlighting the company's strategic shift towards multi-format nicotine offerings, thereby reducing its dependence on traditional cigarettes.

Elfbar stands at the forefront of innovation, boasting over 900 granted patents and an impressive 2,200 pending. Their devices, including the ELFX Ultra, JoinOne15, and 4-in-1 Ultra 50, incorporate child-lock features and app-based usage logs. These enhancements not only align with emerging safety standards but also prioritize user convenience. Meanwhile, Dinner Lady, riding on a wave of premium perception, clinched the “E-Liquid of the Decade” title in 2025. Their strategic shelf placements with EG Group and ASDA underscore that boutique branding can thrive, even in a landscape dominated by larger players.

In March 2026, Japan Tobacco International unveiled plans for a EUR 300 million facility in Romania. This move aims to localize heated-tobacco and vaping production for the European market, effectively mitigating supply-chain risks and tariff challenges. On the other hand, smaller Chinese Original Design Manufacturers (ODMs) grapple with a state-imposed cap on new capacity, effective February 2026. This constraint nudges them towards exploring joint ventures or product licensing, steering clear of traditional brick-and-mortar expansions. Technology emerges as both a distinguishing factor and a compliance shield. Features like QR-coded bottles, variable-wattage smart chips, and ISO-20714 certifications bolster trust. Such enhancements empower companies to command premium shelf prices, even amidst excise challenges. As EU and U.K. duties tighten the margin space for smaller brands, the industry braces for intensified consolidation. Those adept at spreading testing and logistics costs over larger volumes stand to gain the most.

E-Liquid Industry Leaders

HALOCIGS

FLAVOUR WAREHOUSE LTD

Elf Bar

Doozy Vape Co.

VGOD INC.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Solobar has officially expanded its UK product presence by launching a new range of bottled e-liquids, marking a strategic shift toward offering standalone refillable products alongside its established device ecosystem.

- July 2025: Riot Labs introduced six new “supercharged” flavours to its Riot X e-liquid range. The updated lineup boasts maximum intensity flavours: Cherry Colada, Blue Razz Sour Watermelon, Mango and Blackcurrant Gelato, Pink Lemon and Lime, Strawberry and Banana Marshmallow, and Sour Grape Chew. These flavours come in nicotine strengths of 5mg, 10mg, and 20mg, with a starting RRP of GBP 3.99.

- June 2024: Vaping trendsetter URBAN TALE made its mark in the US, introducing a nicotine salt e-liquid lineup featuring 12 distinct flavors. Through a co-brand partnership with LOST MARY, this e-liquid collection was crafted specifically for American adult vapers, showcasing a curated selection drawn from the bestselling flavors of the globally acclaimed LOST MARY brand.

Global E-Liquid Market Report Scope

| Flavored |

| Unflavored |

| Below 30 ml |

| 30 ml To 60 ml |

| Above 60 ml |

| With Nicotine |

| Without Nicotine |

| Offline Stores |

| Online Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Vietnam | |

| Indonesia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Flavor | Flavored | |

| Unflavored | ||

| By Bottle Size/E‑Liquid Capacity | Below 30 ml | |

| 30 ml To 60 ml | ||

| Above 60 ml | ||

| By Nicotine Type | With Nicotine | |

| Without Nicotine | ||

| By Distribution Channel | Offline Stores | |

| Online Stores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Vietnam | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current e-liquid market size and how fast is it growing?

The e-liquid market size stands at USD 5.25 billion in 2026 and is projected to reach USD 6.89 billion by 2031 at a 7.69% CAGR.

Which region leads sales of e-liquids?

North America accounts for 42.32% of global revenue, driven mainly by the United States.

Where is the fastest growth expected?

Asia-Pacific is forecast to post an 8.65% CAGR through 2031 due to manufacturing scale and regulatory evolution.

What share do flavored e-liquids hold?

Flavored variants held 95.48% of 2025 sales, underscoring their dominance despite flavor‐ban debates

Page last updated on: