Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

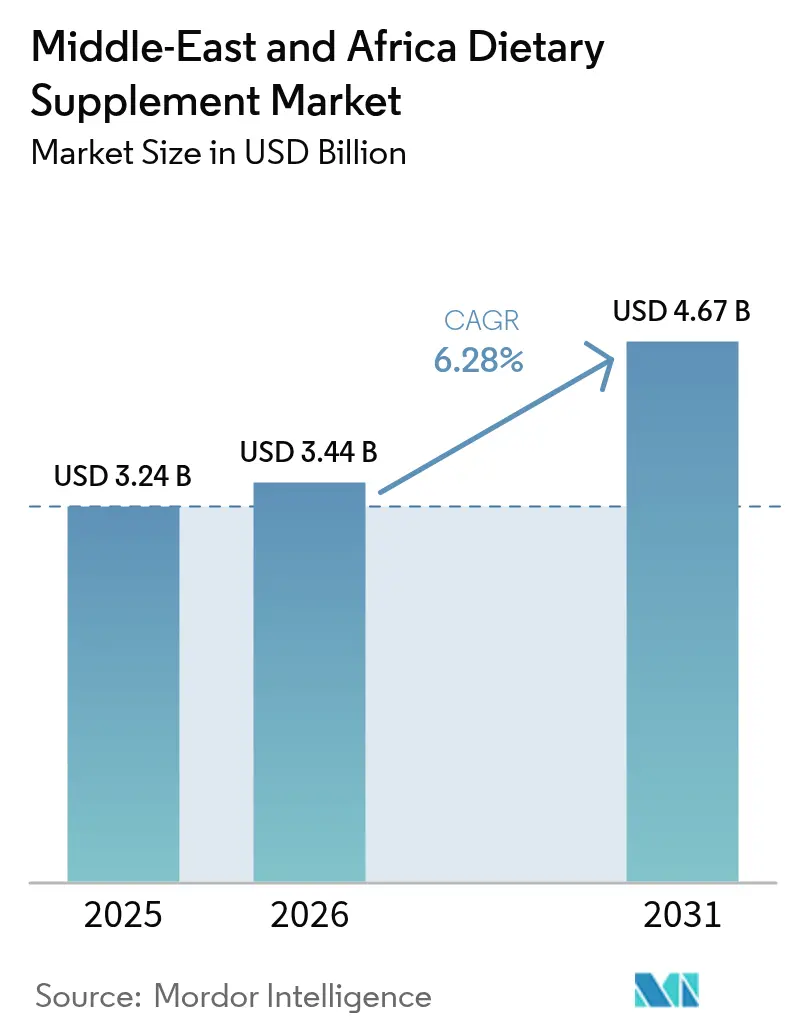

| Base Year Market Size (2025) | USD 3.24 Billion |

| Market Size (2026) | USD 3.44 Billion |

| Market Size (2031) | USD 4.67 Billion |

| Growth Rate (2026 - 2031) | 6.28% CAGR |

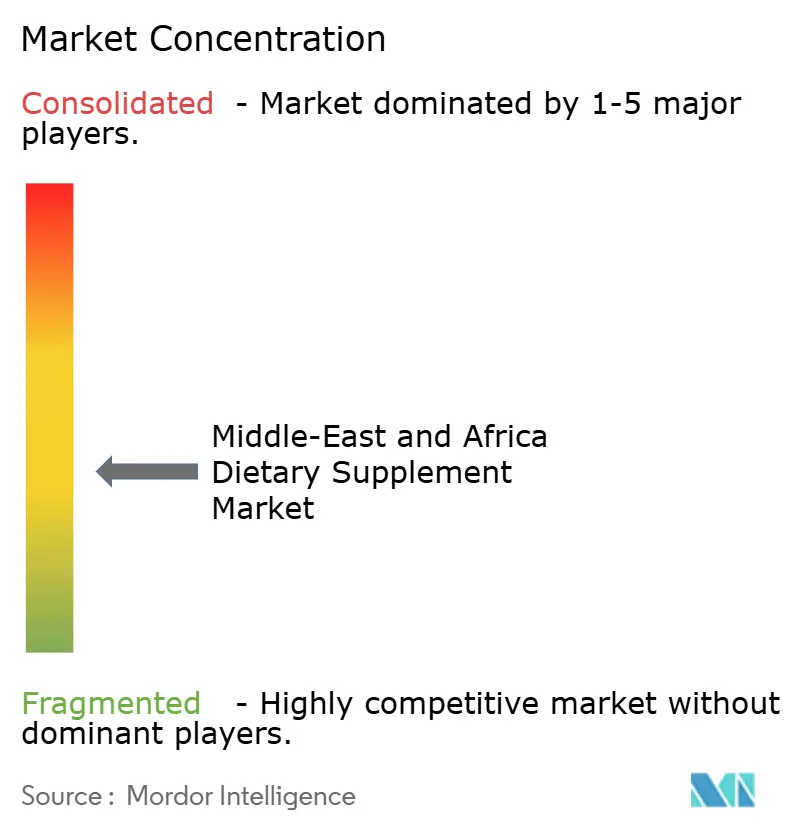

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle-East And Africa Dietary Supplement Market Analysis by Mordor Intelligence

The Middle East and Africa dietary supplement market size was valued at USD 3.24 billion in 2025 and estimated to grow from USD 3.44 billion in 2026 to reach USD 4.67 billion by 2031, at a CAGR of 6.28% during the forecast period (2026-2031). The Middle East and Africa region has been witnessing a significant rise in chronic diseases, particularly diabetes, which has prompted governments to adopt comprehensive preventive healthcare initiatives. These initiatives aim to encourage regular supplement consumption among the population to address health concerns effectively. Additionally, the market's growth is supported by increasing disposable incomes across GCC countries, which has enhanced consumer purchasing power. The ongoing liberalization of retail sectors and the rapid expansion of e-commerce platforms have further improved product accessibility, making dietary supplements more readily available to consumers. To cater to the growing demand and align with consumer preferences, manufacturers have strategically established local production facilities within the region. Moreover, the integration of botanical ingredients in supplements resonates strongly with the cultural values and traditional medicine practices prevalent in the Middle East and Africa region. The market dynamics are further shaped by continuous product innovation, particularly in the development of capsules and functional beverages. This has created a competitive environment where established international companies and dynamic regional manufacturers actively compete to strengthen their market positions.

Key Report Takeaways

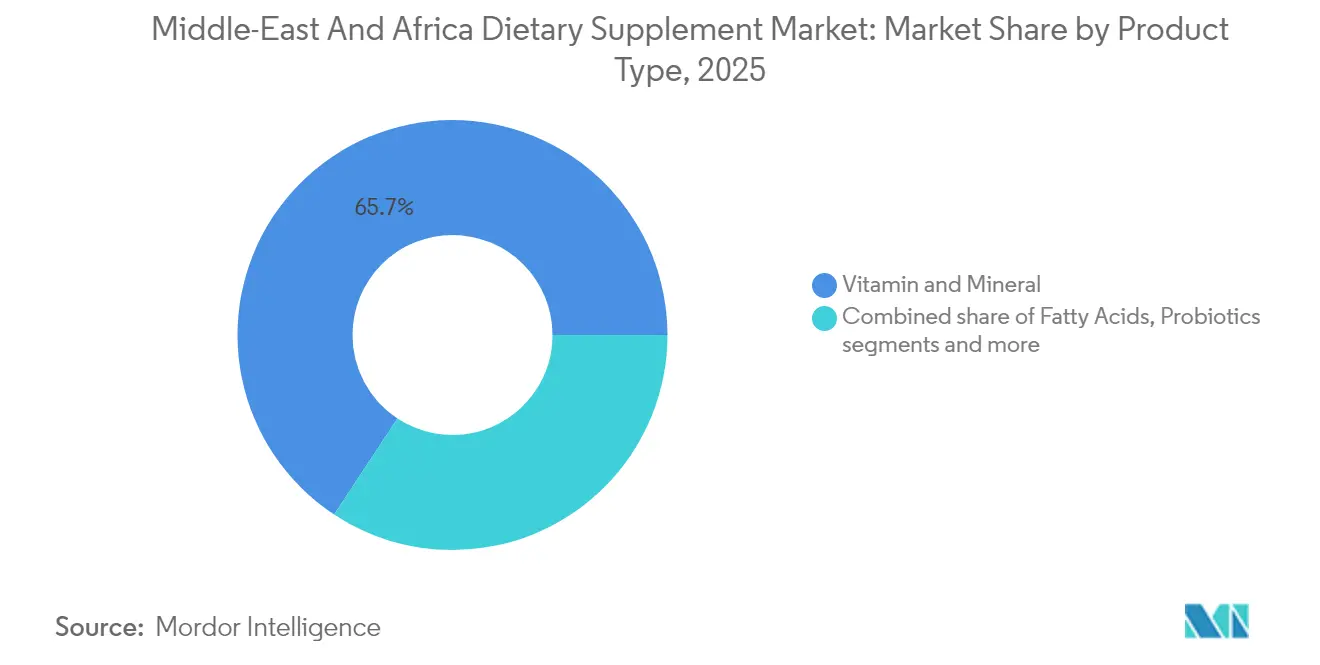

- By product type, Vitamins and Minerals led with 65.72% of the Middle East and Africa dietary supplement market share in 2025, while Herbal Supplements are projected to register the fastest 7.85% CAGR through 2031.

- By form, Tablets captured 31.12% revenue share of the Middle East and Africa dietary supplement market in 2025; Capsules are advancing at a 7.31% CAGR to 2031.

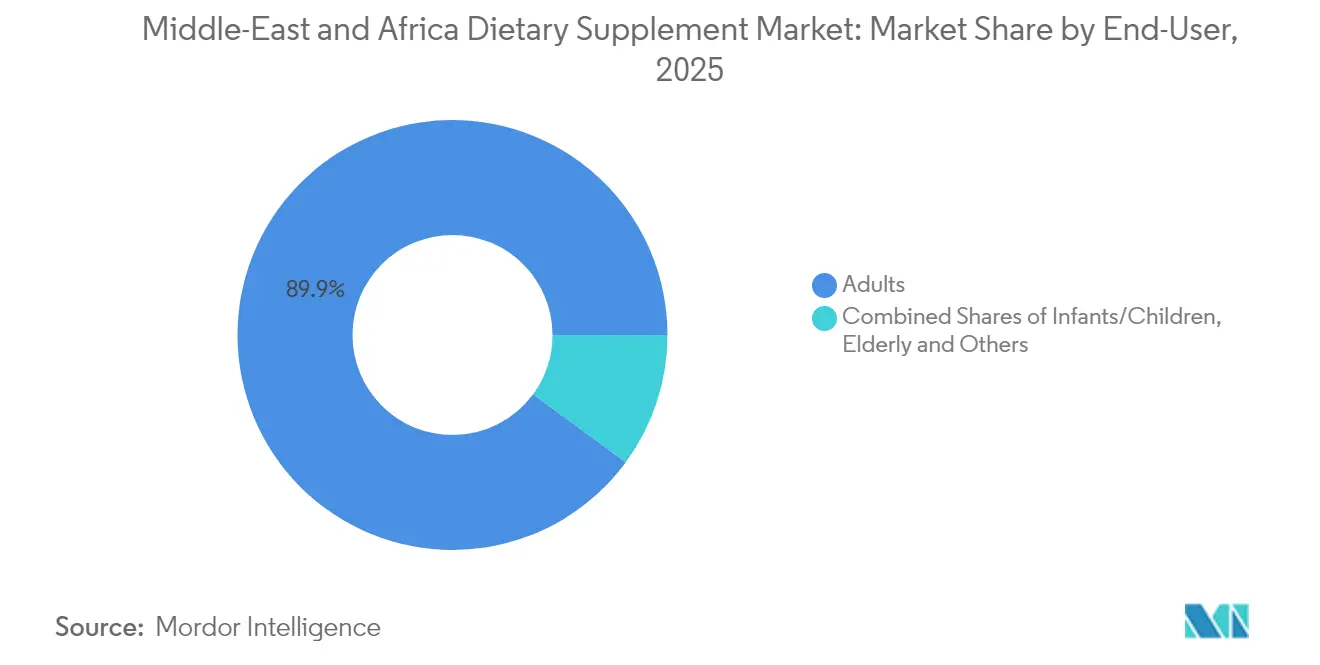

- By end-user, Adults accounted for 89.92% share of the Middle East and Africa dietary supplement market size in 2025 and remain dominant, whereas Infants/Children segment is set to expand at an 7.88% CAGR over 2026-2031.

- By health benefits, General Health retained 32.11% share in 2025, yet Bone andJoint Health is forecast to grow at an 7.76% CAGR, the highest within the Middle East and Africa dietary supplement market.

- By distribution channel, Pharmacies andDrug Stores held 64.10% share in 2025, while Supermarkets/Hypermarkets are poised for the quickest 7.22% CAGR to 2031.

- By geography, Saudi Arabia commanded 16.98% of the Middle East and Africa dietary supplement market size in 2025; Egypt is expected to log the fastest 7.51% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle-East And Africa Dietary Supplement Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Burden of Chronic Diseases Drives Market Growth | +1.8% | Global, with highest impact in GCC countries and Egypt | Long term (≥ 4 years) |

| Expanding Market for Plant-Based and Clean-Label Supplements | +1.2% | United Arab Emirates, Saudi Arabia, with spillover to North Africa | Medium term (2-4 years) |

| Growing Focus on Preventive Healthcare and Lifestyle Management | +1.0% | GCC core, expanding to Egypt and Nigeria | Medium term (2-4 years) |

| Accelerating Development of New Products and Ingredients | +0.8% | Saudi Arabia, United Arab Emirates, with regional distribution | Short term (≤ 2 years) |

| Increasing Demand for Personalized Dietary Solutions | +0.6% | United Arab Emirates, Saudi Arabia, limited to urban centers | Medium term (2-4 years) |

| Consumer Preference for Easy-to-Use Supplement Formats | +0.4% | Global across Middle East and Africa region | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Chronic Diseases Drives Market Growth

The Middle East and Africa region grapples with a significant chronic disease burden that continues to influence supplement consumption patterns. The prevalence of diabetes, affecting 17% of adults in Arab nations compared to the global average of 11.1%, represents a substantial health challenge, with patient numbers expected to reach 80 million by 2050 [1]Source: Advances in Biomedical and Health Sciences, “Diabetes in the Arab world,” journals.lww.com. This ongoing health crisis generates consistent demand for metabolic health supplements, particularly products that help manage blood glucose levels and support cardiovascular function. The financial implications extend beyond healthcare expenses, with productivity losses amounting to USD 72 billion across the Arab region, prompting businesses and individuals to invest in preventive supplements [2]Source: International Journal of Diabetology & Vascular Disease Research, “Indirect Cost of Diabetes In The Arab Region,” scidoc.org. The widespread occurrence of cardiovascular conditions, specifically ischemic heart disease and hypertension, significantly impacts quality of life metrics across the region, creating sustained opportunities for manufacturers of heart health supplements.

Expanding Market for Plant-Based and Clean-Label Supplements

Consumer preferences are evolving toward plant-based formulations, reflecting a broader shift in health consciousness and the enduring influence of traditional medicine practices. A notable portion of supplement consumers in the United States actively choose plant-based products, with this trend expanding significantly in Middle East and Africa markets where herbal remedies remain deeply rooted in cultural practices. The clean-label movement continues to gain momentum as consumers become increasingly mindful of ingredient transparency, actively seeking products free from artificial additives and synthetic compounds [3]Source: Brazilian Journal of Food Technology, “Emerging ingredients for clean label products and food safety,” scielo.br. This market evolution creates substantial opportunities for manufacturers to leverage regional botanical resources, particularly African legumes that provide substantial protein content and beneficial bioactive compounds for supplement development. Recent regulatory advancements, as demonstrated by China's incorporation of Cistanche deserticola into the 'List of Substances Traditionally Used as Both Food and TCM,' establish promising pathways for Middle East and Africa botanical ingredients in the global marketplace. The convergence of environmental sustainability concerns and documented health benefits positions plant-based supplements as a significant growth segment, particularly resonating with younger consumers who prioritize both personal wellness and environmental stewardship in their purchasing decisions.

Growing Focus on Preventive Healthcare and Lifestyle Management

The healthcare landscape in the Middle East and Africa is undergoing significant transformation, shifting from traditional treatment-focused methods to prevention-oriented healthcare. This shift is influencing supplement consumption patterns across the region. Government initiatives are playing a key role in this transition, such as Saudi Arabia's Healthy Food Strategy implemented by the SFDA. This strategy aims to combat non-communicable diseases through dietary improvements and nutritional awareness programs. Consumers are increasingly prioritizing products designed for specific functional needs, particularly those addressing relaxation and energy enhancement. The integration of lifestyle management practices with supplement use has fostered the development of robust wellness ecosystems in the region. This holistic approach to preventive healthcare has emerged as a sustainable driver of market growth, evolving from temporary health trends into a long-term component of consumer health management strategies.

Accelerating Development of New Products and Ingredients

Product development innovation continues to accelerate as manufacturers adapt to changing consumer preferences and regulatory frameworks. The personalized nutrition segment demonstrates significant expansion, highlighted by Herbalife's substantial acquisition of Pro2col Health and Pruvit Ventures, marking a strategic investment in customized supplement solutions. The functional ingredient market shows notable advancement with new developments, including Nexira's GLP-1 Collection featuring Carolean for natural weight management, addressing obesity concerns through appetite control mechanisms. Probiotic formulations have progressed beyond basic digestive health, with a majority of Middle East OTC probiotics now incorporating multistrain compositions and enhanced CFU counts, demonstrating the application of sophisticated microbiome research. The beauty supplement category exhibits strong growth momentum, evidenced by Gold Collagen's regional expansion across multiple Middle Eastern countries, offering comprehensive formulations that combine collagen with antioxidants and vitamins for skin health benefits. The integration of traditional medicine knowledge with modern extraction technologies has unlocked new ingredient opportunities, particularly in South African medicinal plants, which have demonstrated valuable bioactive properties.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Allergen Risks and Cross-Contamination Issues Limit Market Growth | -0.8% | Global, particularly affecting imported products | Medium term (2-4 years) |

| Supply Chain Challenges Due to Environmental and Sustainability Requirements | -0.6% | Import-dependent countries: United Arab Emirates, Saudi Arabia, Egypt | Long term (≥ 4 years) |

| Limited Support from Healthcare Practitioners Impacts Market Adoption | -0.5% | Regional, with highest impact in traditional healthcare systems | Long term (≥ 4 years) |

| Market Share Constraints from Traditional Medicine | -0.4% | North and Sub-Saharan Africa, rural areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Allergen Risks and Cross-Contamination Issues Limit Market Growth

Manufacturing quality issues pose significant challenges to market growth due to increased regulatory oversight and consumer awareness. A Saudi Arabian study found widespread quality deficiencies in probiotic products, with a minimal number of products verifying bacterial strains through genotypic methods, while others used less accurate phenotypic testing. Manufacturing facilities producing multiple supplement types face cross-contamination risks, particularly affecting consumers with allergies or dietary restrictions. The United Arab Emirates Department of Health Abu Dhabi has highlighted that consumers often incorrectly assume dietary supplements are safe, despite potential health risks, especially when taken with medications [4]Source: Department of Health, “Medications & Supplements Awareness Material,” doh.gov.ae. In Egypt, market studies have identified adulteration in herbal weight loss supplements, where manufacturers add undisclosed harmful ingredients to enhance product effectiveness, creating safety concerns. The lack of standardized safety assessment protocols across Middle East and Africa countries compounds these issues, resulting in cautious consumer behavior and potential regulatory restrictions on product availability.

Limited Support from Healthcare Practitioners Impacts Market Adoption

Healthcare professional skepticism toward dietary supplements creates substantial adoption barriers across Middle East and Africa markets, particularly in countries with established medical hierarchies. Healthcare professionals in Qatar demonstrate limited understanding of gut microbiota's role in health, while acknowledging that microbes should be considered in treatment plans. This disconnect highlights a significant knowledge-practice gap that restricts supplement recommendations. Traditional medicine practitioners often view modern supplements as threats rather than complementary solutions, hindering integrated treatment approaches. In Ghana, patients demonstrate substantial knowledge of traditional medicine practices, yet healthcare integration faces challenges due to inadequate processing and certification of traditional products, along with resistance from medical doctors. The absence of standardized dietary supplement education in medical curricula leaves practitioners unprepared to provide informed guidance to patients. This professional knowledge gap reduces consumer confidence and slows market penetration, especially among educated demographics who rely on healthcare provider recommendations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Herbal Supplements Drive Innovation

The Middle East and Africa dietary supplements market demonstrates a clear consumer preference for essential nutrients, with Vitamins and Minerals capturing 65.72% of the market share in 2025. This substantial market dominance reflects the fundamental nutritional requirements across diverse population segments in the region. In parallel, the Herbal Supplements category exhibits remarkable growth potential, projecting an 7.85% CAGR from 2026 to 2031. This growth trajectory represents a significant shift in consumer behavior toward traditional remedies, supported by both cultural heritage preservation and mounting scientific evidence validating botanical effectiveness. Companies like Baidyanath are capitalizing on this trend by expanding their international presence with evidence-based Ayurvedic formulations specifically designed for men's and women's health needs.

The market landscape reveals robust performance across various supplement categories, with Protein and Amino Acids experiencing increased demand driven by heightened fitness consciousness and broader adoption of sports nutrition products. The Fatty Acids segment continues to expand its market presence through targeted omega-3 education initiatives that emphasize cardiovascular health benefits. Additionally, the Probiotics category demonstrates accelerated growth, primarily attributed to advancing research in gut-brain axis connections and microbiome science developments. The Middle East market, in particular, shows increasing sophistication in consumer preferences, with strong adoption of advanced multistrain probiotic formulations that address specific health concerns.

By Form: Capsules Gain Consumer Preference

The dietary supplement market continues to evolve, with tablets maintaining a significant 31.12% market share in 2025. This dominance stems from their cost-effectiveness and consumers' familiarity with tablet consumption. Meanwhile, capsules are showing strong growth potential with a projected 7.31% CAGR from 2026 to 2031, as consumers recognize their improved bioavailability and easier swallowing benefits. The powder segment is expanding through its incorporation into functional beverages and flexible dosing options, particularly appealing to younger consumers who value personalized nutrition solutions. Despite regulatory concerns about sugar content in regions with high diabetes prevalence, gummies remain a preferred choice for children and elderly consumers who prioritize taste.

The liquid supplement segment is experiencing notable developments, particularly in ready-to-drink formats and enhanced absorption claims. For instance, iPRO's expansion of functional hydration products across Saudi Arabia addresses specific regional dehydration challenges. The market's gradual shift toward capsules reflects consumers' deeper understanding of supplement effectiveness and delivery methods. This trend creates opportunities for manufacturers to distinguish their products through advanced encapsulation technologies and targeted-release formulations, focusing on optimizing nutrient absorption while minimizing digestive side effects.

By End-User: Pediatric Segment Shows Promise

The adult demographic continues to be the cornerstone of the supplement market, maintaining a commanding 89.92% market share in 2025. This substantial market dominance is evident across all supplement categories, from vitamins and minerals to specialty formulations, reflecting deeply ingrained health consciousness and established purchasing behaviors among adult consumers. The market's stability in this segment underscores the sustained demand for supplements among working professionals, health enthusiasts, and aging populations seeking to maintain their wellbeing.

In contrast, the infants/children segment is emerging as a dynamic growth opportunity, projecting an impressive CAGR of 7.88% from 2026 to 2031. This remarkable growth trajectory is primarily driven by evolving parental perspectives on preventive healthcare and increasing awareness of childhood nutrition requirements. Modern parents are actively incorporating supplements into their children's daily routines, moving beyond traditional reactive healthcare approaches. This shift represents a broader transformation in parenting practices, where early nutritional intervention through supplementation is increasingly viewed as a fundamental component of children's overall development and long-term health outcomes.

By Health Benefits: Bone Health Accelerates

General Health maintains a significant 32.11% market share in 2025, establishing itself as the primary segment for fundamental nutritional supplementation. The Bone and Joint Health category demonstrates remarkable momentum, achieving the highest growth rate at an 7.76% CAGR from 2026 to 2031. This growth trajectory is primarily attributed to the expanding aging population and heightened consumer awareness regarding osteoporosis prevention measures.

The ongoing transition toward sedentary lifestyles and reduced outdoor activities in the region has resulted in decreased sun exposure, directly impacting natural vitamin D synthesis. This shift has created a sustained market demand for combination supplements, particularly those containing calcium and vitamin D. The Gut Health segment continues to evolve through substantial advancements in microbiome research and probiotic innovations. Kerry's comprehensive market research indicates a growing consumer understanding of the intricate relationships between gut health, brain function, and metabolic wellness across Middle East and Africa markets, further driving segment growth.

By Distribution Channel: Retail Democratization Accelerates

Pharmacies and drug stores are projected to maintain a significant market share of 64.10% in 2025. This dominance is attributed to their established reputation as reliable healthcare providers and their capacity to offer professional guidance on supplement selection. These outlets are often the first point of contact for consumers seeking trusted advice on health-related products, ensuring they remain a preferred choice. Traditional pharmacy channels continue to serve as the primary destination for consumers looking for health and wellness products, particularly those requiring expert recommendations and personalized care.

Meanwhile, the retail landscape is undergoing notable changes. Supermarkets and hypermarkets are expected to grow at a robust CAGR of 7.22% during 2026-2031, driven by the increasing integration of supplements into everyday wellness routines. These retail formats are becoming more popular due to their convenience, wide product availability, and competitive pricing, making them an attractive option for consumers. Additionally, the online retail segment is expanding rapidly, particularly in the Middle East. Online grocery sales are growing at a CAGR of 27% in the United Arab Emirates and 25% in Saudi Arabia, highlighting the rising prominence of e-commerce in the region. The convenience of online shopping, coupled with the growing penetration of digital platforms, is reshaping consumer purchasing behavior and driving significant growth in this segment.

Geography Analysis

Saudi Arabia maintains its position as the regional market leader with a substantial 16.98% market share in 2025. This dominance stems from the country's ambitious Vision 2030 initiatives, which have set clear targets to boost local pharmaceutical production to 40% of the market. The strategic focus on healthcare sector diversification demonstrates Saudi Arabia's commitment to reducing import dependence and developing a robust domestic pharmaceutical industry.

Egypt has emerged as the region's most promising market, projecting an impressive CAGR of 7.51% from 2026 to 2031. This growth trajectory is underpinned by the country's young and growing population, steady increases in consumer purchasing power, and continuous expansion of pharmaceutical retail networks across urban and rural areas. The Egyptian market presents significant opportunities for both local and international pharmaceutical companies looking to expand their presence in the region.

The United Arab Emirates has taken significant steps to enhance its pharmaceutical regulatory framework by establishing the Emirates Drug Corporation as the federal regulator for medical products, replacing Ministry of Health and Prevention (MOHAP). This regulatory evolution is expected to improve market access procedures and create a more streamlined environment for pharmaceutical companies. Meanwhile, Nigeria and South Africa continue to attract attention due to their large population bases and increasing health awareness among consumers. The GCC markets, encompassing Qatar, Bahrain, Kuwait, and Oman, maintain their attractive market status, supported by strong economic fundamentals, high per capita income levels, and well-developed healthcare infrastructure that meets international standards.

Regulatory Landscape

Dietary supplements across the Middle East and Africa operate under a mix of GCC-aligned technical standards and country-specific pre-market controls. In the Gulf, the GCC Standardization Organization (GSO) technical regulation GSO 2571:2021 sets common expectations for supplement categories such as vitamins and minerals, fatty acids, amino acids, enzymes, prebiotics/probiotics, collagen, and herbal extracts, while national authorities determine classification and enforcement. Saudi Arabia applies SFDA classification and registration requirements, including specific triggers that can shift a product into a pharmaceutical pathway when ingredients, concentrations, or label claims imply diagnosis, treatment, or prevention of disease.

In the United Arab Emirates, Federal Decree-Law No. 38 of 2024 provides a more detailed legal framework for medical products and related establishments, shaping how supplements are classified and registered under federal oversight alongside emirate-level food systems. Dubai Municipality continues to influence food-grade products through its Montaji portal and technical guidelines for health supplements, which affect labeling and dossier expectations. In Africa, South Africa regulates many health supplements under SAHPRA as Category D complementary medicines, focusing on permitted substances and evidence thresholds, while other national agencies apply their own registration, labeling, and claim-substantiation requirements. This makes country-by-country compliance planning a practical necessity.

Value Chain Analysis

The regional value chain starts with ingredient sourcing that is often import-led, especially for standardized vitamins, minerals, amino acids, and many botanical extracts. This leaves manufacturers and brand owners exposed to global price movements and lead-time variability. Companies then translate formulas into locally compliant dossiers, where classification checks, label localization, and submission packages (often including certificates of free sale, GMP/ISO credentials, and accredited laboratory analysis) can determine launch timing, particularly in tightly regulated GCC markets.

Finished products move through a distribution system dominated by pharmacies and drug stores across the region, supported by modern retail and expanding e-commerce. Regional logistics and market-access specialists support temperature-controlled handling where needed, which is relevant for hot-climate routes affecting stability for probiotics, liquids, and certain botanicals. Cross-border scaling commonly uses hub-and-spoke fulfillment through Gulf trading infrastructure, while in-market registration differences and claim restrictions continue to shape SKU strategy and channel prioritization.

Competitive Landscape

The Middle-East and Africa dietary supplement market exhibits moderate fragmentation, fostering an environment where both market consolidation and niche specialization thrive simultaneously. This balanced market structure provides established companies the stability to maintain their market positions while creating entry points for new businesses to develop specialized product offerings. Multinational corporations currently command a substantial 59.4% market share across the Middle East and Africa pharmaceutical sector, with industry leaders Sanofi, Novartis, and GSK steering market direction. Regional companies have shown remarkable business acumen, achieving impressive growth rates of 10.2%, which underscores their growing influence in shaping the market's trajectory.

In their pursuit of market expansion, companies are implementing robust growth strategies through calculated acquisitions. A significant example is Herbalife's strategic investment of USD 25-30 million in March 2025, directed towards Pro2col Health and Pruvit Ventures, with the objective of strengthening their personalized nutrition capabilities. Technology integration has emerged as a fundamental market differentiator, with businesses actively incorporating AI-driven personalization systems, establishing partnerships for microbiome testing, and developing comprehensive digital health platforms. These technological advancements enable companies to build integrated wellness ecosystems that comprehensively address consumer health needs, moving beyond conventional product-focused approaches. The market continues to present substantial opportunities in underserved segments, particularly in specialized areas such as pediatric nutrition, elderly care formulations, and culturally-adapted traditional medicine integrations. E-commerce platforms like iHerb have successfully expanded their operational reach to more than 180 countries, while regional businesses focus on meeting local consumer preferences through halal-certified products and locally-sourced ingredients.

The regulatory landscape plays an instrumental role in defining competitive dynamics within the market. The United Arab Emirates's implementation of the Medical Products Law (Federal Decree-Law No. 38 of 2024) has established clearer pathways for innovative dietary supplements while maintaining rigorous safety standards, demonstrating the government's commitment to market development and consumer protection[5]Source: Ministry of Cabinet Affairs, “Federal Decree-Law Governing Medical Products, Pharmacists and Pharmaceutical Establishments,” uaelegislation.gov.ae.

Middle-East And Africa Dietary Supplement Industry Leaders

Bayer AG

Amway Corporation

Herbalife Nutrition

Vitabiotics Ltd

GlaxoSmithKline PLC

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key opportunity is compliance-led portfolio design that reduces rework across jurisdictions while maintaining local fit. Regulatory direction toward pre-market registration, GMP documentation, and tighter claim substantiation across bodies such as the SFDA (Saudi Arabia), Dubai Municipality (UAE), the Egyptian Drug Authority, SAHPRA (South Africa), and national agencies like NAFDAC (Nigeria) supports companies that can industrialize dossier preparation, stability and lab testing, and label governance for multi-country launches. Products with higher claim intensity, novel botanicals, or higher-dose actives face a higher risk of classification outside the food-supplement route. That dynamic creates room for brands that keep formulations within food-grade boundaries while still targeting needs like general health, bone and joint health, and gut health.

Channel evolution is also creating room for faster commercialization cycles and broader assortment. Pharmacies stay an anchor channel for trust-led purchasing, while online grocery growth in the United Arab Emirates and Saudi Arabia is widening access for mainstream vitamins and minerals and convenient formats such as capsules, gummies, and ready-to-drink supplements. Evidence of active innovation and retailer-facing commercialization includes Herbalife launching MultiBurn in July 2025 with a botanical blend targeting weight management, and Revive Collagen entering more than 100 Supercare stores in the UAE in February 2025. These launches indicate that retailers are willing to scale beauty and functional propositions when local registration and labeling requirements are met.

Recent Industry Developments

- February 2026: Bayer Consumer Health launched Priorin Extra, a dietary supplement positioned to support hair and reduce hair loss, across Saudi Arabia, the United Arab Emirates, and Egypt. The rollout strengthens Bayer's consumer health presence in key MEA markets and raises competitive pressure in the beauty and hair-nutrition segment through a multinational brand play.

- July 2025: Herbalife introduced MultiBurn, a dietary supplement featuring botanical extracts including Morosil, Metabolaid, and Capsifen. The launch broadens Herbalife's weight management portfolio with a gluten-free and vegan positioning, aligning with rising demand for metabolic health solutions in the region.

- July 2024: Dubai Municipality published an updated set of technical guidelines for health supplements, reinforcing product and labeling expectations for supplements registered through Dubai's food control processes. The update tightens execution requirements for brands targeting retail distribution in Dubai, making dossier readiness and label compliance more central to time-to-shelf performance.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers dietary supplements sold across the Middle East and Africa for consumer use, measured as the value of finished supplement products across retail and online channels in the region.

Scope exclusions: It excludes conventional foods and beverages that are not positioned and sold as supplements, and it excludes prescription drug therapies even if they address similar health needs.

Segmentation Overview

- By Product Type

- Vitamins and Minerals

- Herbal Supplements

- Protein and Amino Acids

- Fatty Acids

- Probiotics

- Enzymes

- Other Product Types

- By Form

- Tablets

- Capsules

- Powders

- Gummies

- Liquids

- Others

- By End-User

- Infants/Children

- Adults

- Pregnant Women

- Elderly

- By Health Benefits

- General Health

- Bone and Joint Health

- Gut Health

- Immune Health

- Heart Health

- Beauty Supplements

- Others

- By Distribution Channel

- Supermarkets/Hypermarkets

- Pharmacies and Drug Stores

- Online Retail Stores

- Other Distribution Channels

- By Geography

- United Arab Emirates

- Saudi Arabia

- Oman

- Qatar

- Bahrain

- Kuwait

- South Africa

- Egypt

- Nigeria

- Iraq

- Rest of Middle East and Africa

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by building a clean fact base on population, income, and health focus across the Middle East and Africa, then linking it to how supplements are bought and used. We rely on public sources such as World Bank indicators, UN population data, World Health Organization health statistics, and trade data published by UN Comtrade to capture demand signals and cross-border supply movement.

Sizing inputs are then tightened using company annual reports, investor presentations, product catalogs, major retailer and pharmacy chain disclosures, and reputable press coverage that captures launches and price positioning. Where helpful, paid subscriptions for company financials and intelligence, patent databases, and shipment-level import and export records are used to confirm product mix, brand activity, and pricing direction. The examples listed here are illustrative only, and other public sources were also used for data collection, cross-checks, and clarification.

Primary Interviews and Surveys

Primary work focused on interviews and short surveys with supplement brands, distributors, pharmacists, online sellers, and nutrition and regulatory experts across key Middle East and Africa markets, and then the same assumptions were checked again with demand-side voices. We used these discussions to confirm price bands by form and category, typical discounting, channel margins, and how quickly online mix shifts, which helps close gaps that desk sources cannot fully explain.

Children:

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 20% | |

| Mid tier: 51% | Functional/Unit leaders: 30% | |

| Smaller Players: 22% | Managers: 50% |

Market-Sizing & Forecasting

The core model uses a top-down approach. We reconstruct the demand pool for supplements from population, category usage rates, and the observed channel structure across the Middle East and Africa, then roll it into value using realistic pricing. To keep the totals practical, we corroborate with selective bottom-up checks, such as sampled price points multiplied by estimated volumes for fast-moving categories and channel checks on typical sell-through.

Key inputs include supplement adoption by age group, share of sales by pharmacies versus online, mix shifts across vitamins, minerals, herbal, probiotics, and proteins, average selling price movement by pack size and form, and country currency moves against the US dollar. Forecasts are built using scenario analysis supported by regression checks, where growth is tied to variables such as urbanization, income, health awareness, and channel expansion, then refined using what interviewees expect for pricing and category momentum. When bottom-up evidence is thin in smaller markets, we use conservative penetration and price bands and then re-check outputs against regional import signals and channel realities.

Data Validation & Update Cycle

Model outputs are checked against independent signals such as trade flows, category growth cues from major retailers and pharmacy networks, and the direction of reported company revenues, and then large variances are investigated before sign-off. If pricing, currency, or channel mix shifts create an unusual jump, we re-contact sources to confirm whether it is a real change or a data timing issue.

Each report is refreshed annually, and interim updates are triggered when material events occur, such as sharp currency movements, major regulatory changes, or a step-change in online penetration. Before delivery, a final review is completed so the output reflects the latest available information.

Mordor Intelligence's Middle East and Africa Dietary Supplement Market Size Versus Other Published Estimates

Published market sizes for dietary supplements in the Middle East and Africa can look far apart because currency conversion timing, how average selling prices are stepped up, and how each source defines a supplement are handled differently. Differences also show up when some sources rely on a single-year snapshot, while others build a longer history and adjust for channel mix changes.

In our checks, the largest gap drivers are usually tied to whether the estimate uses constant USD conversion or a current-year rate, whether online discounting and pharmacy margins are modeled explicitly, and how quickly price inflation is pushed into the forecast. By refreshing FX timing and price bands during validation calls and then tying the market value to category-level mix and channel shares, Mordor Intelligence avoids overstating growth that is mostly coming from currency and nominal price drift.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.24 B (2025) | |

| Global Consultancy A | USD 4.10 B (2024) | Uses a different base year and tends to lift regional value faster by applying a higher growth trajectory and broader country coverage, which can amplify pricing and currency effects when converted to USD. |

| Industry Publisher B | USD 4.02 B (2024) | Long forecast horizon with aggressive compounding can widen the spread if ASP escalation and channel shift assumptions are not revalidated frequently, and if currency timing is treated uniformly across countries. |

The comparison shows that much of the spread comes from base-year choice, how currency is translated into USD, and whether price and channel dynamics are revisited during updates. By tying value to a repeatable set of demand, mix, and pricing checks, the final number remains traceable to clear inputs rather than being driven mainly by a single assumption.

Key Questions Answered in the Report

How large is the Middle East and Africa dietary supplement market in 2026?

The Middle East and Africa dietary supplement market size stands at USD 3.44 billion in 2026 and is projected to reach USD 4.67 billion by 2031 at a 6.28% CAGR.

Which product category leads sales?

Vitamins and Minerals lead, accounting for 65.72% of 2025 revenue in the Middle East and Africa dietary supplement market.

What segment is growing the fastest?

Herbal Supplements are forecast to post the quickest 7.85% CAGR from 2026-2031.

Which country dominates regional demand?

Saudi Arabia holds 16.98% of the Middle East and Africa dietary supplement market size, the highest country share recorded in 2025.

How are supplements mainly sold across Middle East and Africa ?

Pharmacies and Drug Stores remain the primary channel with 64.10% share, though Supermarkets/Hypermarkets and online platforms are gaining at faster rates.

Page last updated on: