Seasonal Affective Disorder Therapeutics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

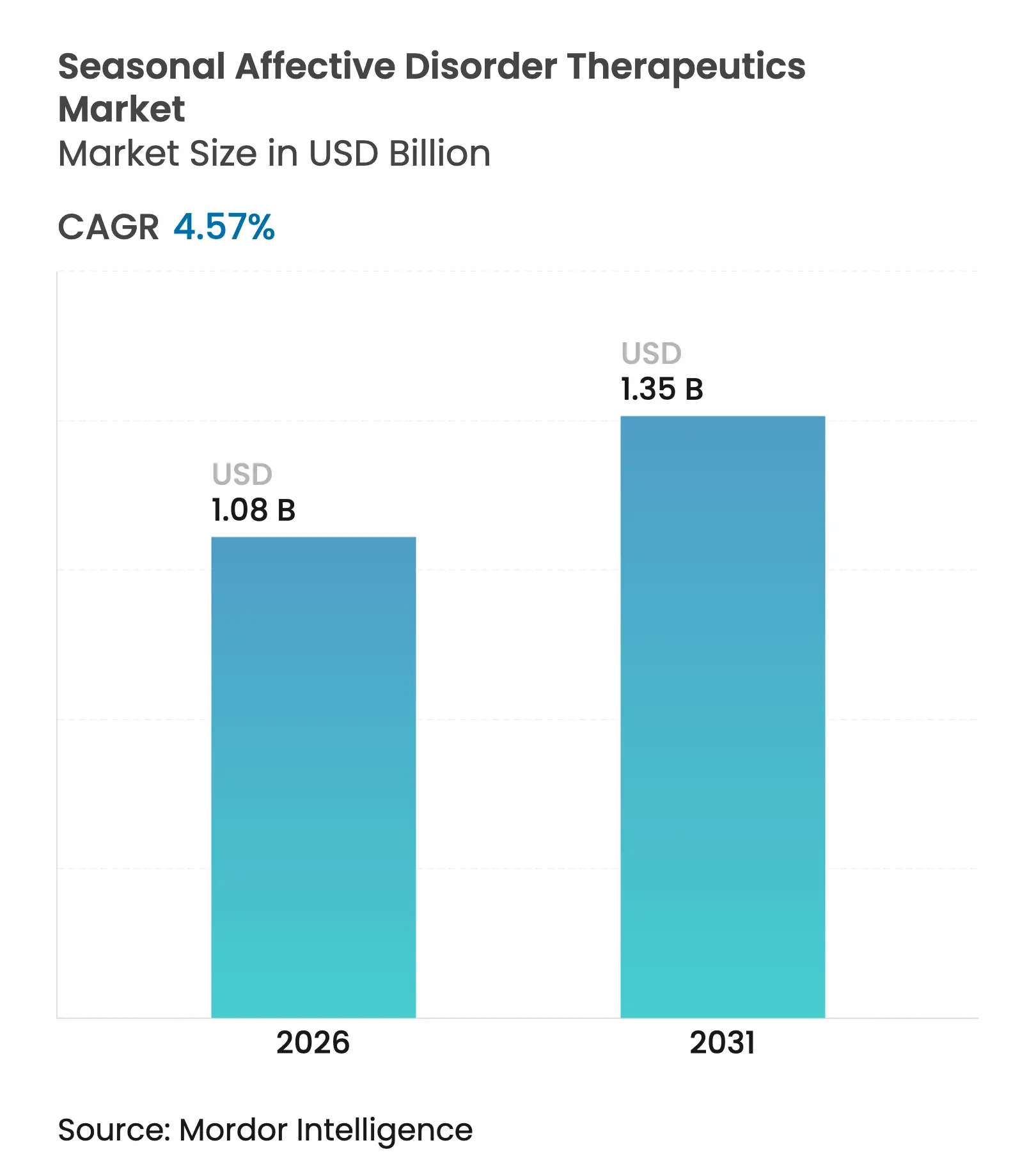

| Market Size (2026) | USD 1.08 Billion |

| Market Size (2031) | USD 1.35 Billion |

| Growth Rate (2026 - 2031) | 4.57 % CAGR |

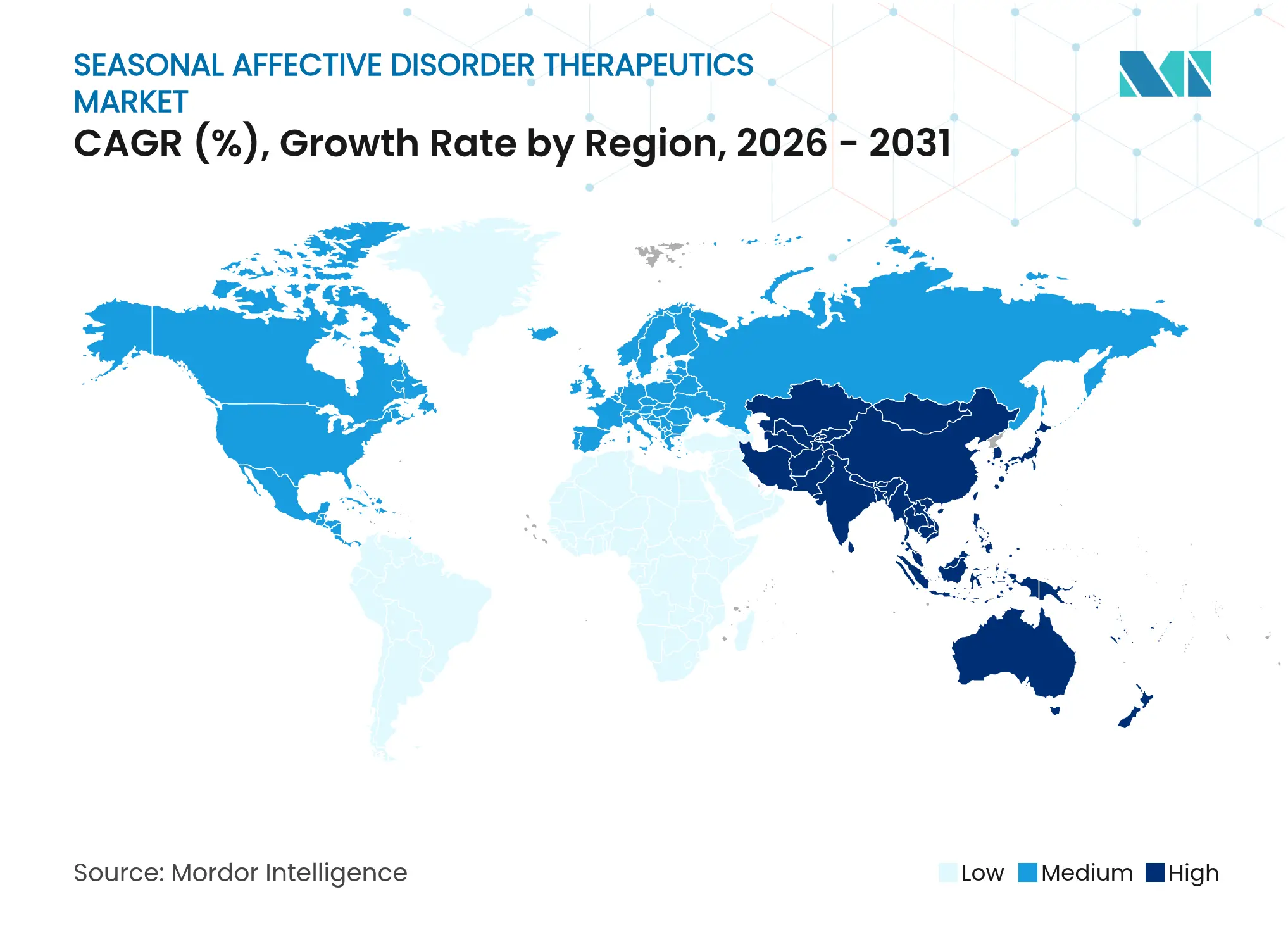

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Seasonal Affective Disorder Therapeutics Market Analysis by Mordor Intelligence

The Seasonal affective disorder therapeutics market size is expected to grow from USD 1.03 billion in 2025 to USD 1.08 billion in 2026 and is forecast to reach USD 1.35 billion by 2031 at 4.57% CAGR over 2026-2031. The trajectory shows a measured transition from reliance on conventional pharmacotherapy toward blended paradigms that unite drugs, neuromodulation and software-based care. Established manufacturers defend their portfolios through lifecycle management, yet the arrival of prescription digital therapeutics such as Rejoyn validates technology-driven models that can accompany or even substitute medication during winter episodes. Acquisition activity—most notably Johnson & Johnson’s USD 14.6 billion purchase of Intra-Cellular Therapies and AbbVie’s USD 2 billion neuroplastogen partnership—signals that large incumbents aim to secure clinical breadth across mood-disorder domains and, by extension, larger slices of the Seasonal affective disorder therapeutics market. Regionally, North America preserves leadership because of favorable reimbursement and mature diagnostic infrastructure, while Asia-Pacific records double-digit expansion as mental-health literacy accelerates in China and India.

Key Report Takeaways

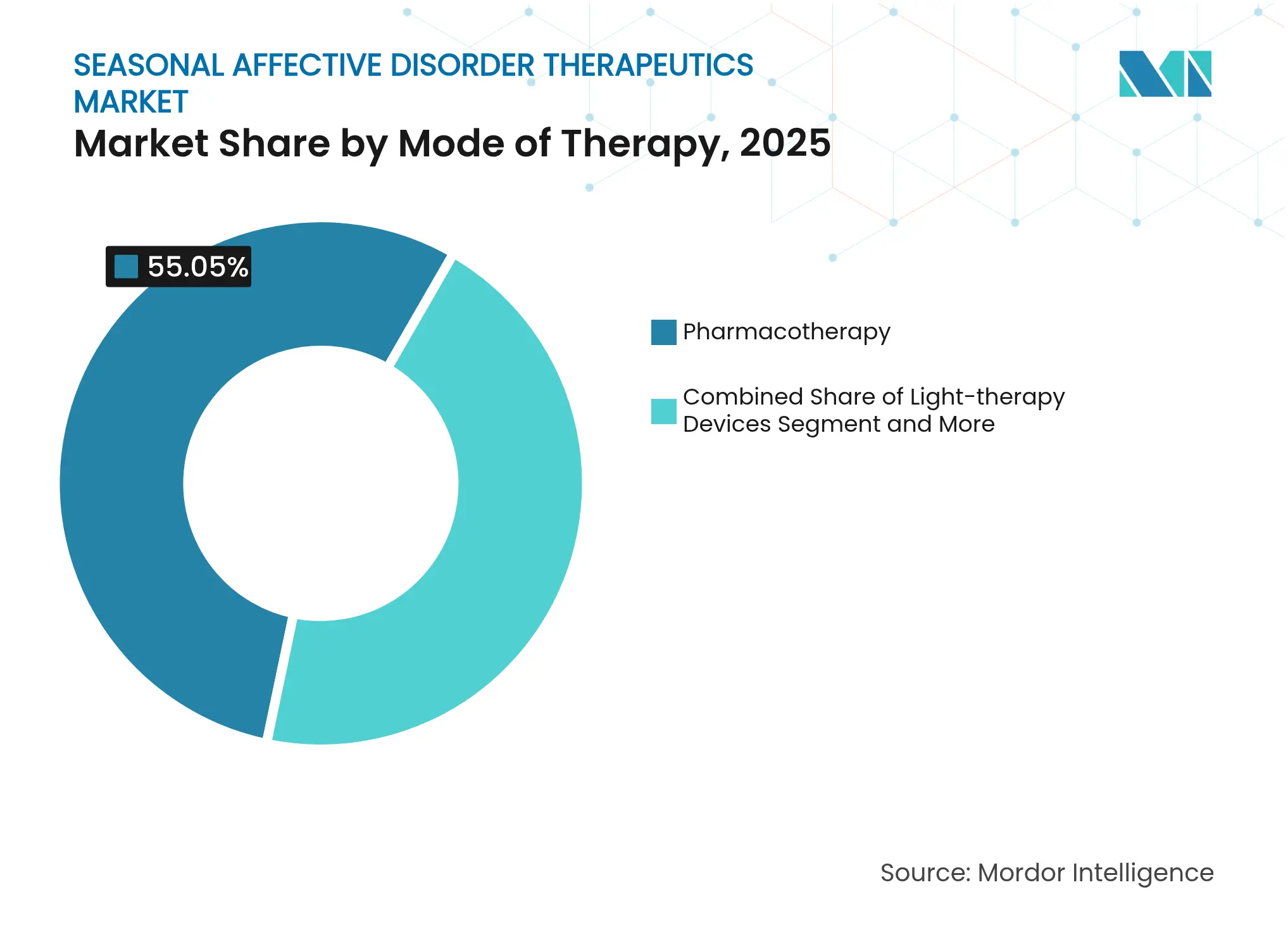

- By mode of therapy, pharmacotherapy led with 55.05% of the Seasonal affective disorder therapeutics market share in 2025, while neuromodulation is projected to post a 12.59% CAGR through 2031.

- By distribution channel, retail pharmacies commanded 58.62% share of the Seasonal affective disorder therapeutics market size in 2025; online pharmacies and telemedicine platforms are on track for 11.45% CAGR between 2026-2031.

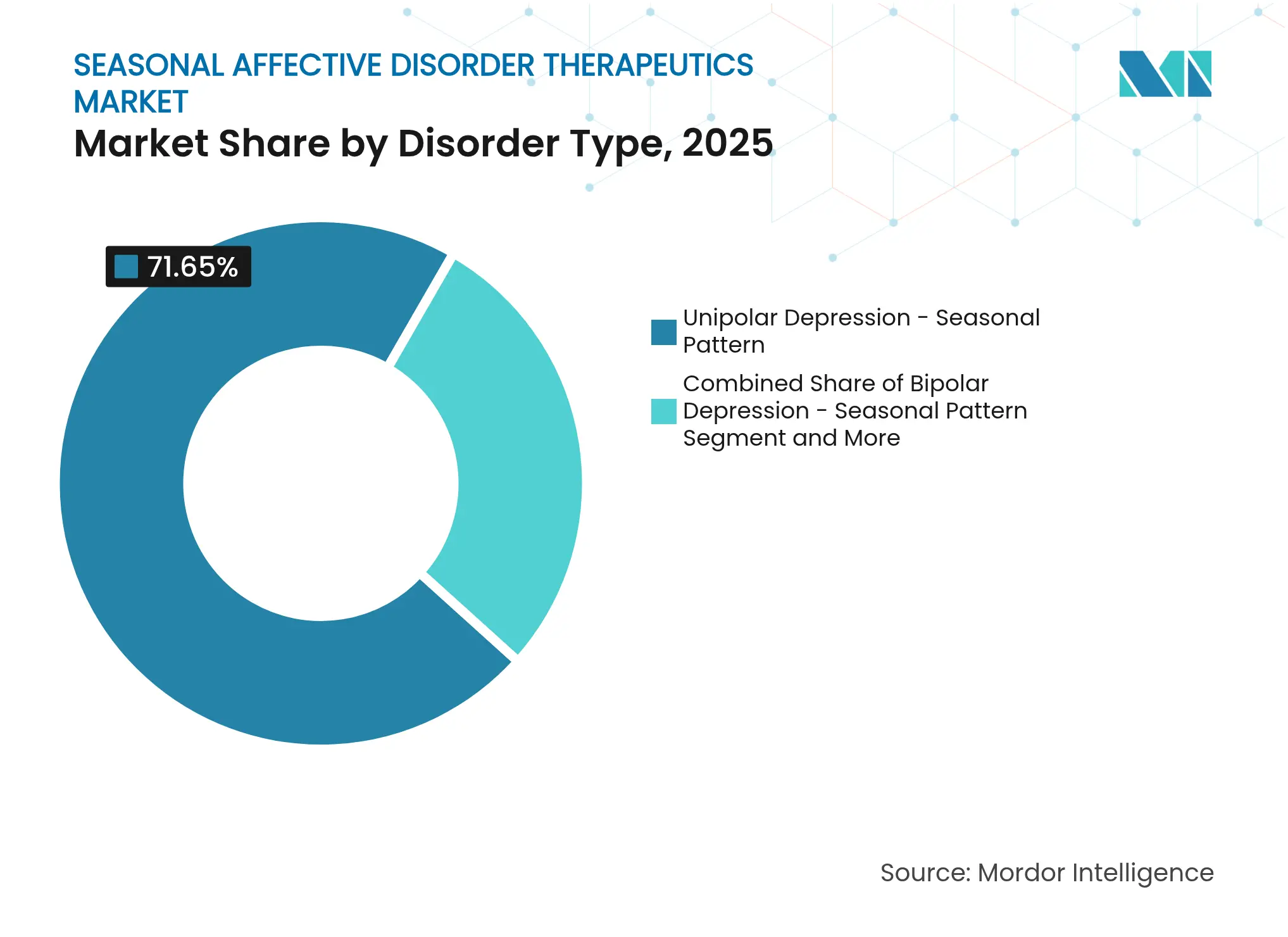

- By disorder type, unipolar depression captured 71.65% of Seasonal affective disorder therapeutics market size in 2025, whereas bipolar depression with seasonal pattern is advancing at 9.43% CAGR through 2031.

- By geography, North America generated 35.78% revenue in 2025, and Asia-Pacific is forecast to expand at 11.37% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Seasonal Affective Disorder Therapeutics Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising prevalence of SAD & MDD

Rising prevalence of SAD & MDD

| +1.2% | Global, with higher impact in Northern latitudes | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

+1.2%

| Geographic Relevance:

Global, with higher impact in Northern latitudes

| Impact Timeline:

Medium term (2-4 years)

|

R&D momentum & new approvals for drugs &

light-therapy devices

R&D momentum & new approvals for drugs &

light-therapy devices

| +0.8% | North America & EU primary, APAC emerging | Short term (≤ 2 years) | |||

Growing awareness & mental-health screening programs

Growing awareness & mental-health screening programs

| +0.7% | Global, accelerated in developed markets | Long term (≥ 4 years) | |||

Tele-medicine & e-prescription adoption

Tele-medicine & e-prescription adoption

| +0.6% | Global, with early gains in North America, Europe | Medium term (2-4 years) | |||

Cortical-targeted home neuromodulation devices

Cortical-targeted home neuromodulation devices

| +0.5% | North America & EU core, spill-over to APAC | Long term (≥ 4 years) | |||

Employer-funded seasonal wellness benefits

Employer-funded seasonal wellness benefits

| +0.4% | North America & Northern Europe primarily | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Prevalence of SAD & Major Depressive Disorder

Clinical recognition of seasonal affective disorder has climbed in parallel with broader depression statistics, driving steady patient inflow to the Seasonal affective disorder therapeutics market. CDC surveys showed a 60% rise in U.S. adult depression prevalence over the past decade, and 40% of respondents reported counseling or therapy use in 2024[1]Centers for Disease Control and Prevention, “New Reports Highlight Depression Prevalence and Medication Use in the U.S.,” cdc.gov. Mobile-health analytics underline wide seasonal variability, reinforcing the need for personalized treatment sequences that software platforms can orchestrate. Employers increasingly quantify winter-linked productivity loss, prompting preventive benefit programs that steer workers toward early therapy initiation. Geographic clustering in higher latitudes supports micro-targeted distribution strategies that pharmaceutical and device firms adopt to maximize uptake during darker months.

R&D Momentum & New Approvals for Drugs & Light-Therapy Devices

Regulators have streamlined review pathways for mood-disorder innovations, encouraging a pipeline that refreshes the Seasonal affective disorder therapeutics market. The FDA’s breakthrough designation for non-invasive brain-stimulation systems and clearance of app-based interventions such as Rejoyn illustrate appetite for diversified modalities. Gepirone’s 2025 approval introduced a selective 5-HT1A agonist that lowers sexual-dysfunction risk, potentially supporting stronger adherence in seasonal regimens. Photobiomodulation meta-analyses identified optimal wavelength bands that can enhance or substitute conventional broad-spectrum light boxes, opening new device niches. Trials of extended-release ketamine tablets reported sustained antidepressant efficacy with moderated dissociation, suggesting expanded access for severe winter depression cases.

Growing Awareness & Mental-Health Screening Programs

Policy and employer initiatives have multiplied screening touchpoints, funneling previously undiagnosed individuals into the Seasonal affective disorder therapeutics market. Medicare’s 2024 expansion of family-therapy benefits cuts cost barriers for older adults, a demographic prone to pronounced winter symptomatology. Social-media-centric campaigns demystify seasonal depression, prompting earlier self-referral. Primary-care settings increasingly embed validated seasonal screening tools within annual check-ups, ensuring uniform referral pathways to pharmacologic, neuromodulation, or digital services. Continuing-education modules for clinicians sharpen diagnostic sensitivity, decreasing historical under-recognition of seasonal patterns.

Tele-medicine & E-Prescription Adoption

Virtual care platforms sustained the pandemic-era surge, widening the Seasonal affective disorder therapeutics market to underserved rural zones. Telepsychiatry demonstrates clinical parity with in-person sessions and alleviates psychiatrist scarcity in many jurisdictions. AI-driven triage tools embedded in these platforms achieved up to 100% accuracy in predicting mental-health disability, including seasonal forms, streamlining clinician workload. Digital prescriptions enable near-real-time dose titration during seasonal transitions, critical for prophylactic regimens that aim to blunt episode onset. Combined with remote monitoring wearables, clinicians can intervene before symptom escalation, curbing emergency-care utilization.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Side-effects & black-box warnings curb adherence

Side-effects & black-box warnings curb adherence

| -0.9% | Global, with higher impact in developed markets | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:

-0.9%

| Geographic Relevance:

Global, with higher impact in developed markets

| Impact Timeline:

Short term (≤ 2 years)

|

Low awareness & under-diagnosis in LMICs

Low awareness & under-diagnosis in LMICs

| -0.7% | APAC, MEA, Latin America primarily | Long term (≥ 4 years) | |||

Payor clamp-down on off-label psychedelic / ketamine

clinics

Payor clamp-down on off-label psychedelic / ketamine

clinics

| -0.5% | North America & EU primarily | Medium term (2-4 years) | |||

LED rare-earth supply risk for light boxes

LED rare-earth supply risk for light boxes

| -0.3% | Global, with manufacturing concentration in Asia | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Side-Effects & Black-Box Warnings Curb Adherence

Mandatory warnings on antidepressants regarding suicidality in young adults continue to temper physician enthusiasm and patient willingness, restraining rapid expansion of the Seasonal affective disorder therapeutics market. Although gepirone mitigates weight-gain and sexual-dysfunction concerns, it still carries the class-label warning. Ketamine-based offerings face regulatory vigilance over dissociative potential; even newer extended-release tablets producing 6.1-point MADRS improvements reported notable headache and dizziness incidence. Digital interventions bypass pharmacologic side effects yet must overcome skepticism about stand-alone efficacy.

Low Awareness & Under-Diagnosis in LMICs

Sparse psychiatric infrastructure and cultural stigma prevent many low- and middle-income countries from integrating seasonal mood screening, limiting downstream demand for the Seasonal affective disorder therapeutics market. Spatial analyses in Thailand revealed urban clustering of care access, highlighting rural gaps[2]C. Rotejanaprasert, “Investigating Mental Health Service Patterns in Thailand,” biomedcentral.com. Integrated Chinese-Western therapy guidelines illustrate culturally attuned pathways, but economic hurdles still restrict entry to branded drugs and light-therapy devices. Without robust diagnostic pipelines, mild seasonal presentations frequently remain untreated until severe, missing the preventive window that yields best outcomes.

Segment Analysis

By Mode of Therapy: Neuromodulation Gains Momentum

Pharmacotherapy secured 55.05% of the Seasonal affective disorder therapeutics market in 2025, anchored by widespread SSRI and SNRI prescribing. The segment remains the volume backbone, yet a gradual shift is visible as clinicians layer medication with device-based options for incomplete responders. Neuromodulation, while only a mid-single-digit share today, is forecast to rise at 12.59% CAGR through 2031, the fastest within the Seasonal affective disorder therapeutics market. FDA clearance for NeuroStar in adolescents broadens the eligible population, and home-based transcranial direct-current stimulation studies that cut Hamilton Depression scores by 9.41 points exemplify convenience-driven uptake.

Home-use photobiomodulation devices address patients who prefer non-pharmacologic care, although LED semiconductor constraints pose cost risks. Cognitive-behavioral therapy tailored to seasonal patterns (CBT-SAD) earns payer interest because of durable relapse prevention, often delivered via telehealth. Emerging psychedelic-assisted protocols remain investigational yet receive media attention, potentially accelerating future demand once safety profiles mature. Collectively, these dynamics reinforce a blended-care future where software scheduling tools optimize the sequence and duration of multiple modalities inside the Seasonal affective disorder therapeutics market.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Digital Access Redefines Supply Lines

Retail outlets preserved 58.62% share of Seasonal affective disorder therapeutics market size in 2025, sustained by medication counseling and existing chronic-care scripts. Nevertheless, online pharmacies and telemedicine prescriptions are projected to grow 11.45% annually, underpinned by regulatory acceptance of e-prescription workflows and rising consumer comfort with home delivery. Integrated platforms allow patients to obtain antidepressants, light boxes and app licenses through a single digital interface, minimizing friction.

Hospital and institutional pharmacies retain relevance for complex cases demanding multi-drug regimens or monitored initiation of ketamine-based therapy. Pharmacy-benefit managers increasingly bundle seasonal depression modules within employer benefit packs, offering fixed-fee programs that bypass insurance co-pays. Auto-refill algorithms and AI-powered adherence tracking help maintain therapeutic continuity over the winter, a critical factor in the Seasonal affective disorder therapeutics industry.

By Disorder Type: Unipolar Dominates but Bipolar Segment Accelerates

Unipolar depression with a seasonal pattern accounted for 71.65% of the Seasonal affective disorder therapeutics market size in 2025, reflecting diagnostic prevalence where depressive episodes occur without mania. Treatment typically centers on SSRIs augmented by light therapy or CBT-SAD, a regimen supported by decades of randomized evidence. Bipolar depression with seasonal manifestation shows 9.43% CAGR through 2031 as clinicians refine diagnostic criteria and deploy mood-stabilizer-adjusted protocols, mitigating manic-switch risk during antidepressant exposure.

Subsyndromal presentations broaden the eligible pool for preventive light therapy, while comorbid anxiety drives prescriptions of agents such as gepirone that treat both symptom clusters. Digital phenotyping via smartphone sensors enhances pattern recognition, enabling earlier prophylactic intervention and thus enlarging the Specialty segment of the Seasonal affective disorder therapeutics market. As payer policies reward preventive care, uptake of such stratified approaches is expected to intensify.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America led the Seasonal affective disorder therapeutics market with a 35.78% share in 2025, underpinned by long winter photoperiods, robust insurance coverage and rapid FDA approvals. U.S. Medicare’s mental-health benefit expansion and workplace wellness mandates reinforce demand momentum. Canada’s high-latitude provinces exhibit concentrated patient clusters that favor specialized seasonal clinics, while Mexico offers a nascent opportunity as urban mental-health infrastructure enlarges.

Europe contributes steady volume through national health services and latitude-driven prevalence, with Germany and the U.K. at the forefront of clinical trials for neuromodulation and digital therapies. Harmonized CE-mark regulation facilitates cross-border device sales, smoothing commercialization timing across member states. Northern Europe’s employer wellness schemes, including subsidized light-box programs, extend preventive uptake during polar-night intervals.

Asia-Pacific is the fastest-growing region, posting an 11.37% CAGR through 2031, and is expected to reshape future rankings within the Seasonal affective disorder therapeutics market. China’s guideline that marries traditional herbal formulations with Western agents illustrates culturally nuanced adoption paths, while Japan’s rapidly aging society drives demand for therapies with favorable tolerability profiles. India’s telehealth proliferation offsets psychiatric workforce shortages and enables remote CBT-SAD delivery. Smaller economies across Southeast Asia still face low diagnostic capture, yet rising mental-health literacy suggests an emerging inflection.

South America and the Middle East & Africa hold modest shares today, but urbanization and private insurance penetration are gradually unlocking new consumer cohorts. Awareness campaigns in Brazil and South Africa leverage social media to counter cultural stigma, providing incremental tailwinds. Overall, regional heterogeneity underscores the importance of tailored omnichannel strategies inside the Seasonal affective disorder therapeutics market.

Competitive Landscape

Market Concentration

The Seasonal affective disorder therapeutics market remains moderately fragmented, lacking a single dominant supplier and thereby encouraging multidimensional competition. Traditional pharmaceutical majors, such as Pfizer, AbbVie and Johnson & Johnson, leverage deep commercial infrastructures yet increasingly complement classic molecules with acquisitions in digital or device domains. Johnson & Johnson’s assimilation of lumateperone via Intra-Cellular Therapies augments its neuroscience arm and fortifies cross-indication positioning.

Digital-health entrants including Otsuka/Click Therapeutics capitalize on lighter regulatory pathways to deliver software-as-medicine, evidenced by the 2024 FDA clearance of Rejoyn for major depression. Device innovators like Neuronetics and Sooma exploit breakthrough designations to accelerate adoption of neuromodulation options that secure double-digit CAGRs. Photobiomodulation specialists exploring precise wavelength protocols may undercut traditional broad-spectrum light boxes on efficacy and energy efficiency.

White-space growth avenues center on combination therapeutics that interlink pharmacologic, device and software components through AI-curated sequencing. Firms developing predictive algorithms for individualized dose timing or light-exposure scheduling may achieve outsized differentiation. Employer-funded wellness contracts provide alternate reimbursement routes outside traditional payer systems, granting first movers early revenue capture across the Seasonal affective disorder therapeutics market.

Seasonal Affective Disorder Therapeutics Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Mount Sinai surgeons became the first in the United States to implant Abbott deep-brain-stimulation hardware within a randomized trial for treatment-resistant depression.

- January 2025: The FDA approved Johnson & Johnson’s nasal spray Spravato (esketamine) as a standalone therapy for treatment-resistant depression.

Table of Contents for Seasonal Affective Disorder Therapeutics Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising Prevalence Of SAD & MDD

- 4.2.2R&D Momentum & New Approvals For Drugs & Light-Therapy Devices

- 4.2.3Growing Awareness & Mental-Health Screening Programs

- 4.2.4Tele-Medicine & E-Prescription Adoption

- 4.2.5Cortical-Targeted Home Neuromodulation Devices

- 4.2.6Employer-Funded Seasonal Wellness Benefits

- 4.3Market Restraints

- 4.3.1Side-Effects & Black-Box Warnings Curb Adherence

- 4.3.2Low Awareness & Under-Diagnosis In LMICs

- 4.3.3Payor Clamp-Down On Off-Label Psychedelic / Ketamine Clinics

- 4.3.4LED Rare-Earth Supply Risk For Light Boxes

- 4.4Porter's Five Forces Analysis

- 4.4.1Threat of New Entrants

- 4.4.2Bargaining Power of Buyers

- 4.4.3Bargaining Power of Suppliers

- 4.4.4Threat of Substitutes

- 4.4.5Competitive Rivalry

5. Market Size & Growth Forecasts (Value, USD)

- 5.1By Mode of Therapy

- 5.1.1Pharmacotherapy

- 5.1.1.1Selective Serotonin Re-uptake Inhibitors (SSRIs)

- 5.1.1.2Serotonin-Norepinephrine Re-uptake Inhibitors (SNRIs)

- 5.1.1.3Norepinephrine-Dopamine Re-uptake Inhibitor

- 5.1.1.4Monoamine Oxidase Inhibitors (MAOIs)

- 5.1.1.5Atypical / Novel Antidepressants

- 5.1.1.6Herbal & OTC Adjuncts

- 5.1.1.7Others

- 5.1.2Light-therapy Devices

- 5.1.3Cognitive-Behavioural Therapy (CBT-SAD)

- 5.1.4Neuromodulation (rTMS, tDCS)

- 5.1.5Emerging Psychedelic-assisted Protocols

- 5.2By Distribution Channel

- 5.2.1Institutional / Hospital Pharmacies

- 5.2.2Retail Pharmacies

- 5.2.3Online Pharmacies & Tele-Rx

- 5.3By Disorder Type

- 5.3.1Unipolar Depression - Seasonal Pattern

- 5.3.2Bipolar Depression - Seasonal Pattern

- 5.3.3Others

- 5.4Geography

- 5.4.1North America

- 5.4.1.1United States

- 5.4.1.2Canada

- 5.4.1.3Mexico

- 5.4.2Europe

- 5.4.2.1Germany

- 5.4.2.2United Kingdom

- 5.4.2.3France

- 5.4.2.4Italy

- 5.4.2.5Spain

- 5.4.2.6Rest of Europe

- 5.4.3Asia-Pacific

- 5.4.3.1China

- 5.4.3.2Japan

- 5.4.3.3India

- 5.4.3.4South Korea

- 5.4.3.5Australia

- 5.4.3.6Rest of Asia-Pacific

- 5.4.4Middle East and Africa

- 5.4.4.1GCC

- 5.4.4.2South Africa

- 5.4.4.3Rest of Middle East and Africa

- 5.4.5South America

- 5.4.5.1Brazil

- 5.4.5.2Argentina

- 5.4.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1AbbVie Inc.

- 6.3.2Eli Lilly and Company

- 6.3.3Pfizer Inc.

- 6.3.4GSK plc

- 6.3.5Viatris Inc.

- 6.3.6Novartis AG

- 6.3.7Teva Pharmaceutical Industries Ltd.

- 6.3.8Otsuka Pharmaceutical Co. Ltd.

- 6.3.9Bausch Health Companies Inc.

- 6.3.10Johnson & Johnson (Janssen)

- 6.3.11Sanofi SA

- 6.3.12Forest Laboratories / Pierre Fabre

- 6.3.13Sunovion Pharmaceuticals

- 6.3.14Lundbeck A/S

- 6.3.15Takeda Pharmaceutical

- 6.3.16Angelini Pharma

- 6.3.17Hikma Pharma

- 6.3.18Alkermes plc

- 6.3.19Lupin Ltd.

- 6.3.20Cipla Ltd.

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-need Assessment

Global Seasonal Affective Disorder Therapeutics Market Report Scope

As per the scope of the report, seasonal affective disorder refers to a mood disorder characterized by depression that occurs at the same time every year. Seasonal affective disorder occurs in climates where there is less sunlight at certain times of the year. Symptoms include fatigue, depression, hopelessness, and social withdrawal. The report covers the several types of drugs used to treat these disorders.

The seasonal affective disorder therapeutics market is segmented by drug type (selective serotonin reuptake inhibitors, norepinephrine-dopamine reuptake inhibitors, monoamine oxidase inhibitors, other drug types), disorder type (unipolar disorder, bipolar disorder), distribution channel (institutional sales, retail sales), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally.

The report offers the market size and forecasts in value (USD) for the above segments.