Bipolar Disorder Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

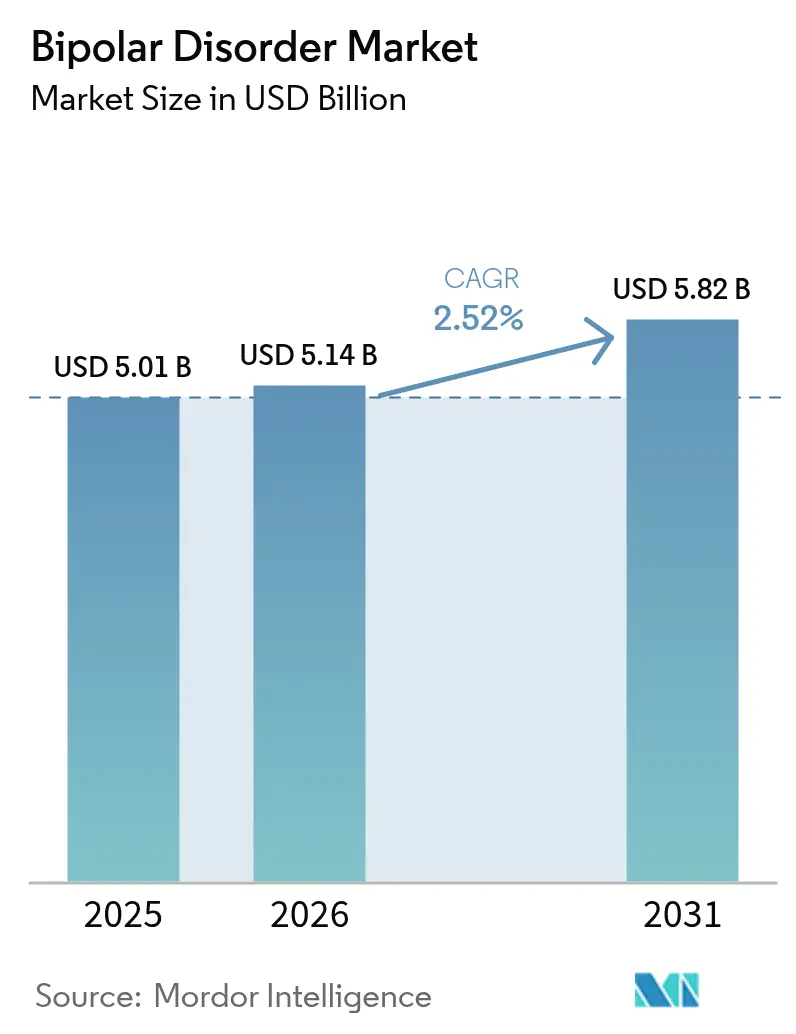

| Market Size (2026) | USD 5.14 Billion |

| Market Size (2031) | USD 5.82 Billion |

| Growth Rate (2026 - 2031) | 2.52% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bipolar Disorder Market Analysis by Mordor Intelligence

The bipolar disorder market size is expected to grow from USD 5.01 billion in 2025 to USD 5.14 billion in 2026 and is forecast to reach USD 5.82 billion by 2031 at 2.52% CAGR over 2026-2031. Prescriber preference for second-generation antipsychotics (SGAs), broader reimbursement under mental-health parity rules, and accelerating uptake of digital therapeutics collectively sustain growth momentum. The 2025 acquisition of Intra-Cellular Therapies by Johnson & Johnson vaults Caplyta into a leading position for bipolar depression and underscores renewed strategic emphasis on neuroscience portfolios. Long-acting injectables (LAIs) are proving cost-effective by curbing relapse-linked hospitalizations, while AI-driven diagnostic tools shrink the historical treatment-initiation gap. Competitive focus is shifting toward metabolic-sparing combinations and precision digital monitoring, signaling a market pivot from volume to value.

Key Report Takeaways

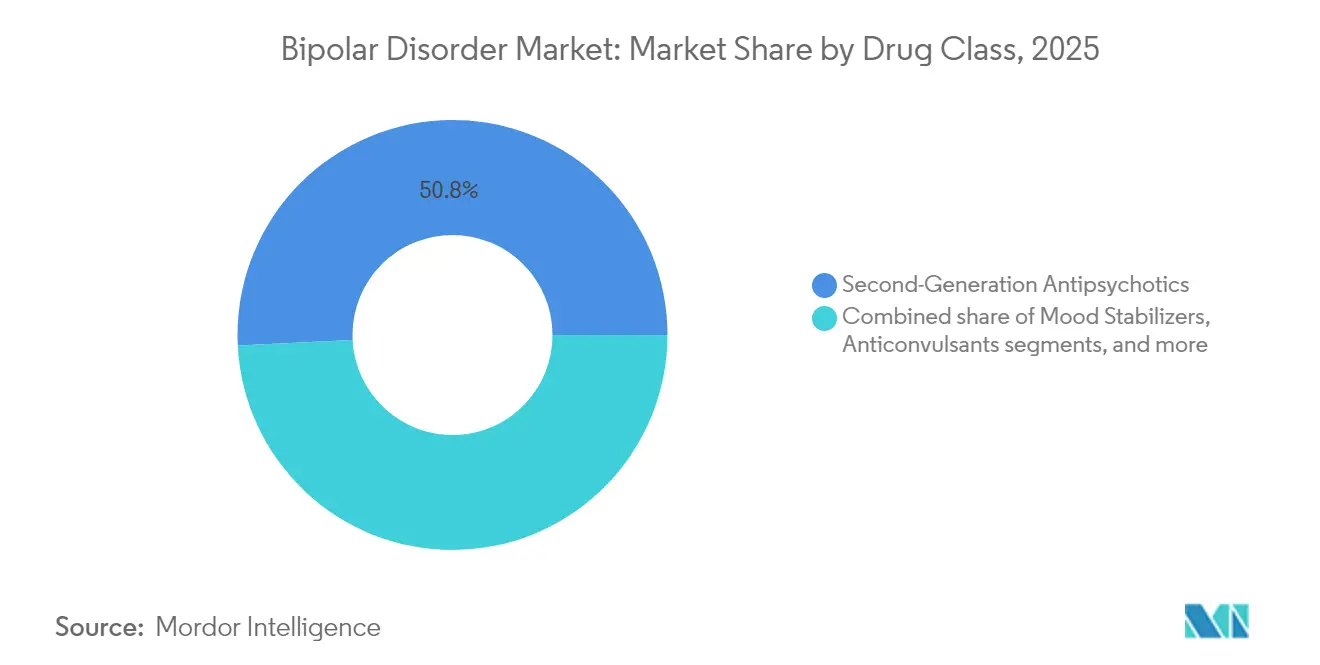

- By drug class, second-generation antipsychotics led with 50.78% of bipolar disorder market share in 2025; antidepressants are projected to expand at a 4.18% CAGR to 2031.

- By mechanism of action, dopamine D₂/D₃ partial agonists held 36.95% of the bipolar disorder market size in 2025, whereas glutamate pathway modulators record the highest forecast CAGR at 4.71% through 2031.

- By disease type, bipolar I disorder accounted for 61.72% of the bipolar disorder market size in 2025, while bipolar II disorder is set to grow at a 4.27% CAGR to 2031.

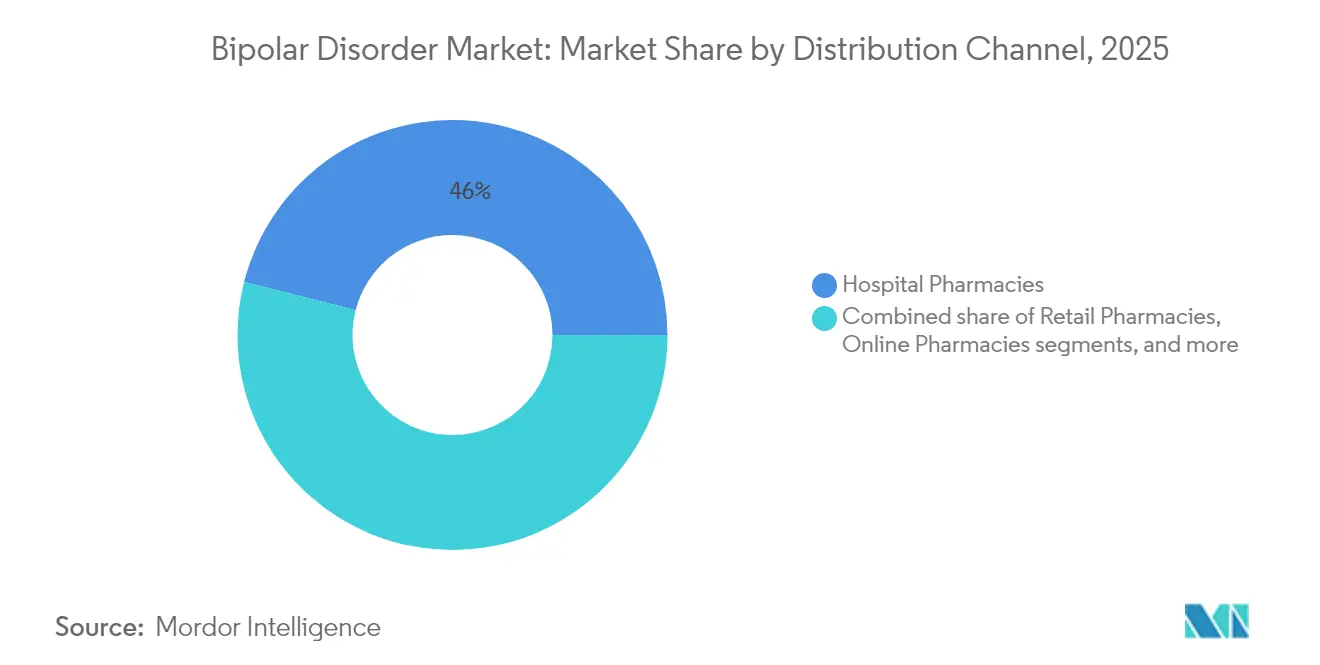

- By distribution channel, hospital pharmacies captured 46.02% revenue share in 2025; online pharmacies show the fastest growth at 5.34% CAGR through 2031.

- By treatment setting, inpatient care represented 52.88% of revenue in 2025, and digital therapeutics are advancing at a 5.63% CAGR to 2031.

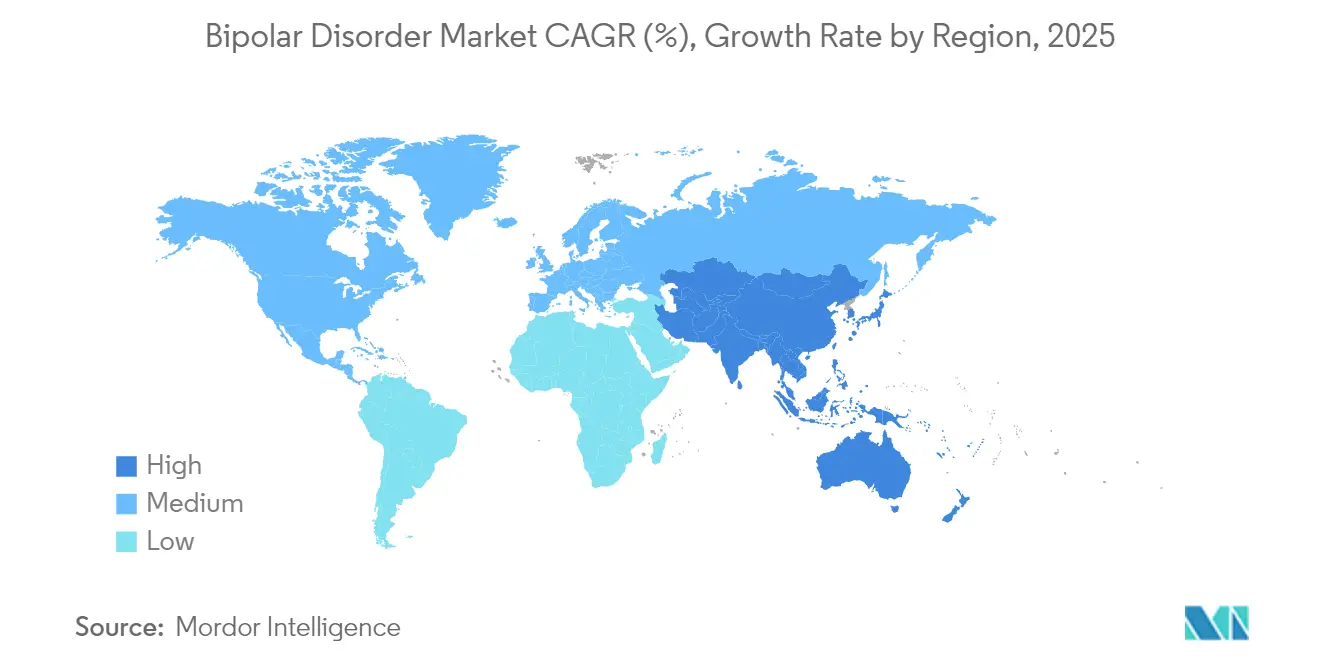

- By geography, North America dominated with 42.11% share in 2025; Asia-Pacific registers the quickest expansion at 3.52% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Bipolar Disorder Market Trends and Insights

Driver Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence & earlier diagnosis of bipolar spectrum disorders | +0.8% | Global, concentrated gains in North America & Europe | Medium term (2-4 years) |

| Government-led mental-health parity laws & reimbursement expansion | +0.6% | North America primary, EU secondary adoption | Short term (≤ 2 years) |

| Rapid uptake of second-generation antipsychotics & long-acting injectables | +0.5% | Global, with acceleration in Asia-Pacific | Medium term (2-4 years) |

| Digital phenotyping & AI-driven screening tools boosting treatment rates | +0.4% | North America & EU core, Asia-Pacific emerging | Long term (≥ 4 years) |

| Real-world evidence (RWE) platforms accelerating label expansions | +0.3% | Primarily United States & Europe, expanding to developed APAC markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence & Earlier Diagnosis of Bipolar Spectrum Disorders

Machine-learning classifiers now distinguish bipolar disorder from major depression with 85% pooled accuracy, cutting historic misdiagnosis lags that averaged 9.5 years[1]Y. Huang et al., “AI-Enabled Differential Diagnosis Between Bipolar Disorder and Major Depression,” nature.com. Blood-based RNA-editing biomarker panels validated with 0.904 AUC make earlier prodromal-phase intervention feasible. Smartphone-based digital phenotyping detects mood-state shifts with 88% sensitivity and 89% specificity relative to clinician assessments, while sustained telemedicine utilization broadens specialty access in underserved communities. Earlier recognition is translating into swifter treatment initiation, lower disability-adjusted life-year burdens, and heightened demand across every stage of the bipolar disorder market.

Government-Led Mental-Health Parity Laws & Reimbursement Expansion

Final rules under the Mental Health Parity and Addiction Equity Act effective January 2025 compel private health plans to prove equivalent access metrics for mental-health and medical benefits[2]“Mental Health Parity Final Rule,” federalregister.gov. New CMS billing codes extend Medicare and Medicaid reimbursement to prescription digital therapeutics, setting a precedent later echoed by several European payers. Region-wide EMA coordination eliminates duplicative trials, shortening time-to-market for novel agents. These policies reduce out-of-pocket costs, improve adherence, and support measurable cost-savings from fewer acute-care episodes—all reinforcing steady demand within the bipolar disorder market.

Rapid Uptake of Second-Generation Antipsychotics & Long-Acting Injectables

Real-world evidence shows LAIs cut annual mood-episode rates by 67% and hospitalizations by 81% versus oral SGAs[3]Springer Nature, S. K. Lin, “Real-World Outcomes With LAI Antipsychotics,” link.springer.com. FDA clearances in 2024 for Rykindo and Erzofri enlarge the LAI toolbox, while six-monthly paliperidone formulations raise patient acceptance. Economic assessments confirm upfront drug costs are offset by fewer emergency visits and reduced inpatient days. Together with SGA receptor-profile refinements, these dynamics sustain the largest revenue block inside the bipolar disorder market.

Digital Phenotyping & AI-Driven Screening Tools Boosting Treatment Rates

Rejoyn secured FDA clearance in April 2024 as the first prescription digital therapeutic for major depressive disorder and is already used off-label for bipolar depression adjunct therapy. DaylightRx posted 70% remission in generalized-anxiety trials, and SleepioRx tackles insomnia comorbidity prevalent in 90% of bipolar patients. Algorithms parsing social-media language patterns identify manic or depressive shifts with 84% accuracy, triggering timely clinician outreach. Wearables that track circadian rhythm irregularities allow dose adjustments weeks before clinical relapse. Collectively, these capabilities propel higher treated prevalence and deepen home-based engagement within the broader bipolar disorder market.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent safety concerns (weight gain, metabolic risk) for SGAs | -0.4% | Global, heightened scrutiny in North America & EU | Medium term (2-4 years) |

| High mis-/under-diagnosis in primary-care settings | -0.3% | Global, with acute challenges in Asia-Pacific & emerging markets | Long term (≥ 4 years) |

| Patent cliffs for leading brands (e.g., Latuda®, Vraylar®) post-2027 | -0.5% | Global, most pronounced in developed markets with high generic uptake | Short term (≤ 2 years) |

| Data-privacy barriers limiting adoption of digital therapeutics | -0.25% | North America & Europe, emerging in data-localization jurisdictions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent Safety Concerns (Weight Gain, Metabolic Risk) for SGAs

Studies indicate 4-13% of SGA-treated patients gain at least 7% body weight, compared with 2-5% on placebo. Clozapine induces metabolic syndrome in about 30% of users, prompting regulators to mandate routine BMI and glycemic monitoring. Metformin remains the most-studied adjunct for psychotropic-related weight gain, while GLP-1 receptor agonists enter phase-3 evaluation as combination partners. These cardiometabolic liabilities temper prescribing enthusiasm, especially for patients with pre-existing risk factors, and could modestly dampen bipolar disorder market growth.

High Mis-/Under-Diagnosis in Primary-Care Settings

Primary-care clinicians accurately identify bipolar disorder in only 34% of initial presentations; bipolar II is misclassified as unipolar depression in 60% of cases. Resulting antidepressant monotherapy may precipitate manic switching and prolong the diagnostic journey beyond nine years. Mood Disorder Questionnaire adoption sits below 30% in many health systems, while rural geographies face specialist shortages. Under-recognition delays mood-stabilizer initiation and depresses overall treatment penetration, constraining upside for the bipolar disorder market, particularly in fast-growing but resource-limited regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Second-Generation Antipsychotics Dominate Despite Antidepressant Surge

Second-generation antipsychotics held 50.78% of bipolar disorder market share in 2025, underscoring their broad efficacy across all mood phases. Quetiapine and lumateperone illustrate dual dopamine-serotonin modulation that stabilizes mania and depression, aligning with 2024 Veterans Affairs treatment algorithms. Lithium prescriptions fell from 31% to 16% of patients due to monitoring burdens, though its neuroprotective value endures. Anticonvulsants such as lamotrigine safeguard cognitive function and remain central to maintenance therapy.

Antidepressants represent the fastest-growing category, expanding at a 4.18% CAGR as Caplyta gains traction for bipolar depression. Regimens increasingly combine antidepressants with mood stabilizers to prevent manic switching, broadening therapeutic flexibility. Pipeline diversity spans glutamate and GABA modulators that seek superior tolerability. Collectively, these trends reinforce sustained revenue generation inside the bipolar disorder market while opening room for differentiated newcomers across the bipolar disorder industry.

By Mechanism of Action: Dopamine Modulation Leads While Glutamate Innovation Accelerates

Dopamine D₂/D₃ partial agonists accounted for 36.95% of the bipolar disorder market size in 2025, reflecting a balance of efficacy and softer side-effect profiles. Aripiprazole’s stabilizing action without full receptor blockade typifies this class’s appeal and spurs similar candidates in mid-stage trials.

Glutamate-pathway agents show the highest forward CAGR at 4.71% as ketamine’s rapid antidepressant response validates NMDA receptor targeting. Serotonin-norepinephrine reuptake inhibitors preserve utility where cognitive activation is a therapeutic goal, although selective serotonin reuptake inhibitors require mood-stabilizer co-administration. GABA modulators and ion-channel stabilizers, led by lithium and lamotrigine, continue as backbone options. Mechanistic diversification reduces clinical inertia and broadens prescriber choice throughout the bipolar disorder market.

By Disease Type: Bipolar I Dominance Reflects Severity While Bipolar II Recognition Grows

Bipolar I disorder captured 61.72% of revenue in 2025, owing to full-blown manic episodes that necessitate urgent pharmacologic and often inpatient intervention. Clear diagnostic criteria and greater hospitalization rates translate into higher drug utilization intensity. Cyclothymia and mixed-feature specifiers further enrich clinical complexity and expand the addressable pool.

Bipolar II prevalence is rising and is predicted to climb at a 4.27% CAGR to 2031 as clinician education improves and digital symptom-tracking identifies hypomanic periods. Rapid-cycling forms affect up to 20% of patients and favor anticonvulsant over lithium therapy. Broader spectrum recognition enlarges the bipolar disorder market while underscoring the need for nuanced treatment algorithms across the wider bipolar disorder industry.

By Distribution Channel: Hospital Pharmacy Strength Versus Online Growth Momentum

Hospital pharmacies held 46.02% revenue in 2025, reflecting acute-care protocols during manic crises and the controlled handling requirements of LAIs. Integrated medication-therapy management supports dosing titrations and side-effect monitoring, crucial during stabilization.

Online pharmacies, projected to expand at 5.34% CAGR, meet rising demand for home delivery and telepharmacy counseling. Digital workflows streamline prior authorization for costly LAIs and prescription apps, reducing start-of-therapy delays. Omnichannel models that blend in-person oversight with digital convenience broaden patient engagement and enlarge the bipolar disorder market size globally.

By Treatment Setting: Inpatient Care Leads While Digital Therapeutics Transform Home-Based Treatment

Inpatient settings accounted for 52.88% of spending in 2025 as hospitalization remains the gold standard for acute mania management and suicidality. Average stays of 7-14 days permit rapid medication titration and safety monitoring, justifying hospital pharmacy dominance.

Digital therapeutics grow fastest at 5.63% CAGR through 2031, complementing outpatient follow-up with CBT modules and wearable-enabled monitoring. FDA-cleared apps, remote vital-sign tracking, and telepsychiatry visits reduce emergency-room use and enhance adherence. Hybrid care models that integrate inpatient stabilization with tech-enabled home support enlarge the bipolar disorder market while lowering per-patient costs.

Geography Analysis

North America dominated the bipolar disorder market with 42.11% share in 2025. Parity-law enforcement effective 2025 obliges health plans to match mental-health benefits with medical coverage. Early uptake of LAIs and rapid pathways for digital therapeutics speed diffusion of innovation. FDA approvals for Uzedy and Fanapt reinforce treatment diversity, while integrated delivery networks negotiate value-based contracts that reward relapse reduction.

Europe maintains robust demand through centralized EMA approvals that streamline cross-border launches. Universal healthcare financing guarantees baseline access, although country-specific health-technology assessments steer price negotiations. Variability in legacy lithium use reflects differing monitoring infrastructures, and post-Brexit divergence may lengthen UK-specific timelines for certain agents.

Asia-Pacific is the fastest-growing region at 3.52% CAGR. China’s regulatory reforms trimmed NDA review times and widened reimbursement for innovative therapies, strengthening commercial cases for novel agents. Japan’s annual drug-price revisions nudge manufacturers to pursue high-value indications, while India’s generic manufacturing base rises as a global supplier. Nonetheless, limited specialist density and diagnostic under-recognition still temper treated-prevalence gains, leaving substantial headroom in the bipolar disorder market.

Competitive Landscape

Johnson & Johnson’s USD 14.6 billion purchase of Intra-Cellular Therapies positions Caplyta for an estimated USD 5 billion peak in annual sales and signals renewed pursuit of neuropsychiatric leadership. AbbVie, now marketing Vraylar, leverages Gilgamesh collaboration to access neuroplastogen assets, committing USD 65 million upfront with milestones worth USD 1.95 billion. Otsuka builds on Abilify’s franchise by pairing prescription drugs with proprietary digital therapeutics, extending engagement beyond pill adherence.

Patent cliffs reshape revenue streams: aripiprazole generics arrive in January 2025, prompting price erosions of up to 70%, while Vraylar remains protected until 2029. Lifecycle management focuses on LAI reformulations and expanded mood-disorder indications. Digital-health convergence creates new battlegrounds; companies integrate AI-powered adherence platforms to differentiate beyond molecule efficacy.

Moderate consolidation defines the field. Top five brands account for about two-thirds of branded revenue, yet over 100 generics supply lithium, valproate, and legacy SGAs. Strategic M&A, pipeline diversification, and payer-linked digital tools are emerging as prime levers to secure durable advantage across the bipolar disorder market.

Bipolar Disorder Industry Leaders

Johnson & Johnson (Janssen)

Otsuka Holdings Co. Ltd.

AbbVie Inc.

Eli Lilly and Company

AstraZeneca plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Johnson & Johnson closed its USD 14.6 billion purchase of Intra-Cellular Therapies, adding Caplyta for bipolar I and II depression and projecting peak annual sales above USD 5 billion.

- February 2025: FDA accepted Teva and Medincell’s sNDA for Uzedy extended-release risperidone for bipolar I maintenance based on RISE and SHINE trials.

- January 2025: Autobahn Therapeutics began a phase-2 trial of ABX-002 as adjunctive therapy for bipolar depression after securing USD 100 million in series-C funding.

- October 2024: AbbVie and Gedeon Richter broadened their partnership to include ABBV-932 for bipolar depression.

- September 2024: U.S. Departments of Labor, Treasury, and Health finalized Mental-Health Parity Act rules extending equivalent coverage to more than 175 million insured Americans.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the bipolar disorder treatment market as every prescription mood stabilizer, atypical or typical antipsychotic, anticonvulsant with a bipolar indication, and combination product sold for acute mania, bipolar depression, or maintenance therapy across all age groups, with spending captured at ex-manufacturer prices in constant 2024 US dollars.

Scope exclusion: We do not count psychotherapy-only services, neuromodulation devices, consumer wellness apps, or revenues from clinical-trial supply.

Segmentation Overview

- By Drug Class

- Mood Stabilizers

- Anticonvulsants

- Second-Generation Antipsychotics

- Antidepressants

- Other Drug Classes

- By Mechanism of Action

- Selective Serotonin Reuptake Inhibitor

- Serotonin Norepinephrine Reuptake Inhibitor

- Dopamine D?/D? Partial Agonists

- GABA Modulators

- Glutamate Pathway Modulators

- Ion-channel Stabilizers

- By Disease Type

- Bipolar I Disorder

- Bipolar II Disorder

- Cyclothymia & Others

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Specialty Clinics

- By Treatment Setting

- In-patient

- Out-patient

- Digital Therapeutics / Home-based Care

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts then interviewed psychiatrists, hospital pharmacy buyers, payor formulary managers, and patient-advocacy leads across North America, Europe, Asia-Pacific, and selected emerging markets. These conversations clarified real-world adherence, average course length, off-label substitution, and upcoming procurement shifts that secondary data alone could not reveal.

Desk Research

We first mapped supply and demand signals from trusted public domains such as World Health Organization mental-health datasets, CDC National Center for Health Statistics, OECD Health Data, and UN Population Prospects, which provided prevalence, treatment-gap, and demographic baselines. Trade bodies such as the International Society for Bipolar Disorders, peer-reviewed journals like Lancet Psychiatry, and national formularies offered clinical adoption rates and typical dose regimens. Company 10-Ks, investor decks, and quarterly calls supplied brand level revenue clues, while D&B Hoovers and Dow Jones Factiva gave cross-checks on corporate financials. This list is illustrative; many other open sources fed our desk analysis.

Market-Sizing & Forecasting

We built a top-down and bottom-up hybrid model. Prevalence-to-treated-cohort estimates anchored the demand pool, and then average daily dose, branded-to-generic mix, and weighted ex-factory price produced 2024 volume and value. Supplier roll-ups of leading molecules plus sample channel checks validated and adjusted totals. Key variables like diagnosed prevalence trends, generic erosion speed, adoption of long-acting injectables, payer reimbursement revisions, and telepsychiatry penetration drive yearly changes. A multivariate regression model, stress-tested through scenario analysis, generates the 2025-2030 outlook; gaps in molecule level data are bridged with regional analogs before final calibration.

Data Validation & Update Cycle

Outputs pass three-step analyst review, variance screening against independent indicators, and anomaly callbacks to experts. Reports refresh each year, with mid-cycle updates triggered by material events such as major drug approvals or guideline shifts, ensuring clients receive the most current baseline.

Why Mordor's Bipolar Disorders Treatment Baseline Commands Reliability

Published figures often diverge because firms pick different geographic baskets, price points, and refresh cadences.

Mordor's disciplined scope, annual refresh, and phone-verified treatment patterns keep our baseline grounded, whereas others may lean on list prices or narrow country sets.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.01 Bn (2025) | Mordor Intelligence | - |

| USD 5.56 Bn (2024) | Global Consultancy A | Adds retail mark-ups and omits uninsured self-pay volumes |

| USD 4.88 Bn (2023) | Analyst House B | Stops at 2023 and excludes long-acting injectable uptake outside the United States |

| USD 3.20 Bn (2024, 7 countries) | Trade Journal C | Covers only seven high-income markets, not the worldwide landscape |

The comparison shows that varying geographies, price bases, and molecule coverage explain the spread, and it underlines why our transparent variables and repeatable steps offer decision-makers a dependable starting point.

Key Questions Answered in the Report

What is the current size of the bipolar disorder market?

The bipolar disorder market stands at USD 5.14 billion in 2026 and is projected to reach USD 5.82 billion by 2031.

Which drug class leads revenue?

Second-generation antipsychotics generate the largest revenue, holding 50.78% market share in 2025.

Which segment is growing fastest?

Digital therapeutics within home-based care display the fastest CAGR at 5.63% through 2031.

Why is North America the largest regional market?

Strong insurance coverage under parity laws, rapid approval pathways, and early adoption of LAIs drive North America’s 42.11% share.

What safety concerns limit SGA use?

Weight gain and metabolic syndrome affect up to 13% of patients, prompting intensive monitoring and exploration of GLP-1 adjuncts.

How will patent expirations affect competition?

Aripiprazole’s January 2025 patent expiry will intensify generic competition and cut branded prices by as much as 70%, reshaping revenue distribution.

Page last updated on: