SDHI Fungicide Market Size and Share

Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Market Size (2026) | USD 4.23 Billion |

| Market Size (2031) | USD 6.14 Billion |

| Growth Rate (2026 - 2031) | 7.72% CAGR |

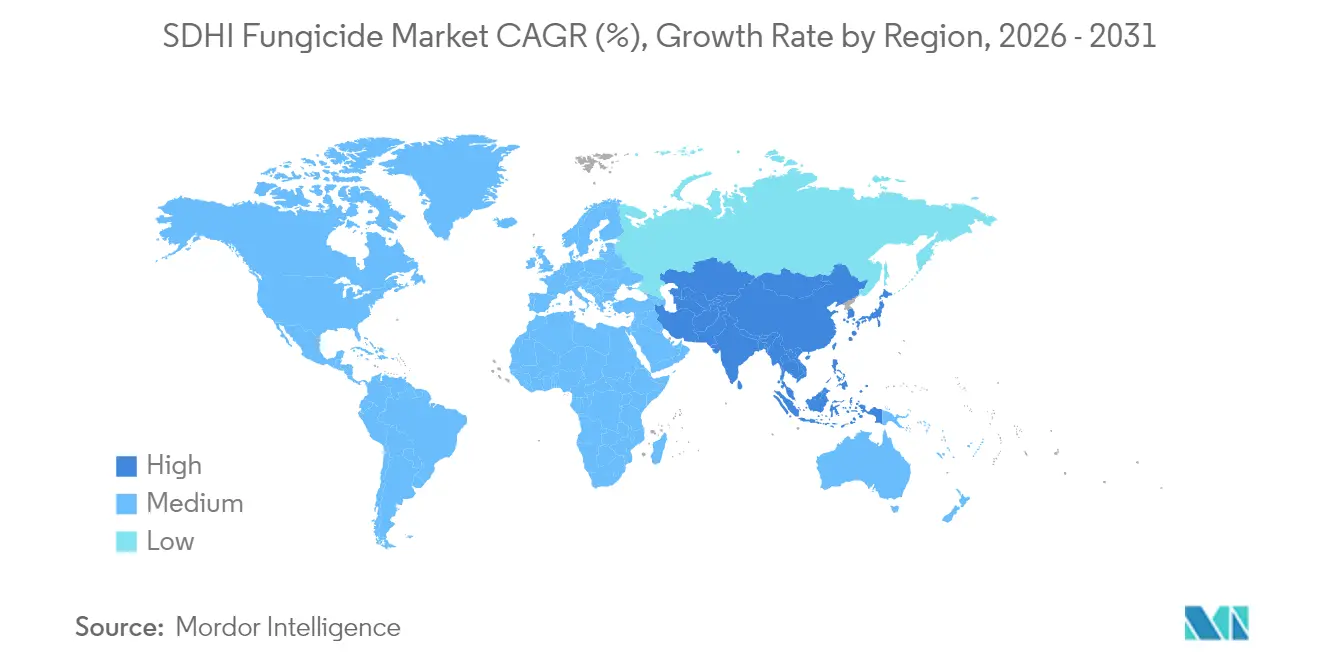

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

SDHI Fungicide Market Analysis by Mordor Intelligence

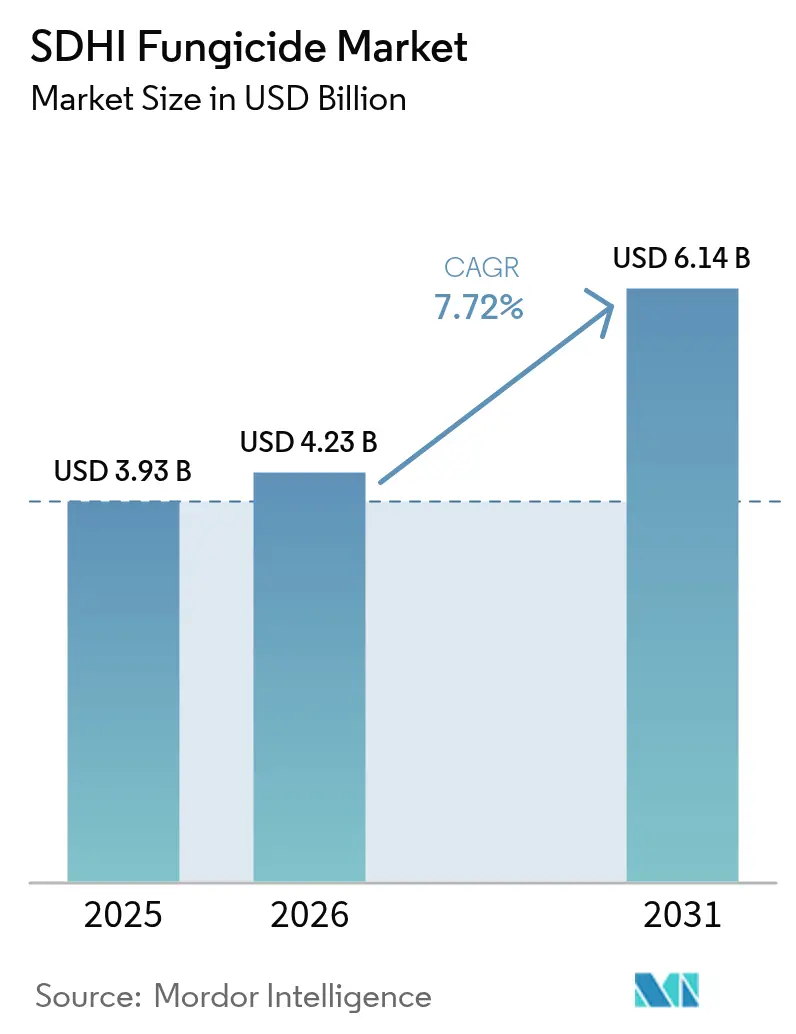

The SDHI fungicide market size is expected to grow from USD 3.93 billion in 2025 to USD 4.23 billion in 2026 and is forecast to reach USD 6.14 billion by 2031 at 7.72% CAGR over 2026-2031. The Succinate Dehydrogenase Inhibitor (SDHI) fungicide market growth is driven by the increasing global demand for high-yield crops, agricultural technology improvements, and rising fungal disease incidence in major food and cash crops. The need for enhanced agricultural productivity stems from growing global food requirements. According to United Nations projections, the global population will reach 9.7 billion by 2050, necessitating a 70% increase in food production[1]Source: United Nations Department of Economic and Social Affairs, "World population projected to reach 9.8 billion in 2050, and 11.2 billion in 2100", un.org. Climate-related disease pressures, accelerated label approvals in emerging markets, and integration with digital decision-making tools further support the market expansion. Market competition focuses on enhanced formulations, data-driven application guidance, and combination products that minimize resistance development. While supply chain disruptions for essential intermediates and stricter residue regulations present cost challenges, farmers continue to use SDHIs to maintain crop yields in grains, cereals, and high-value specialty crops, supporting sustained market growth.

Key Report Takeaways

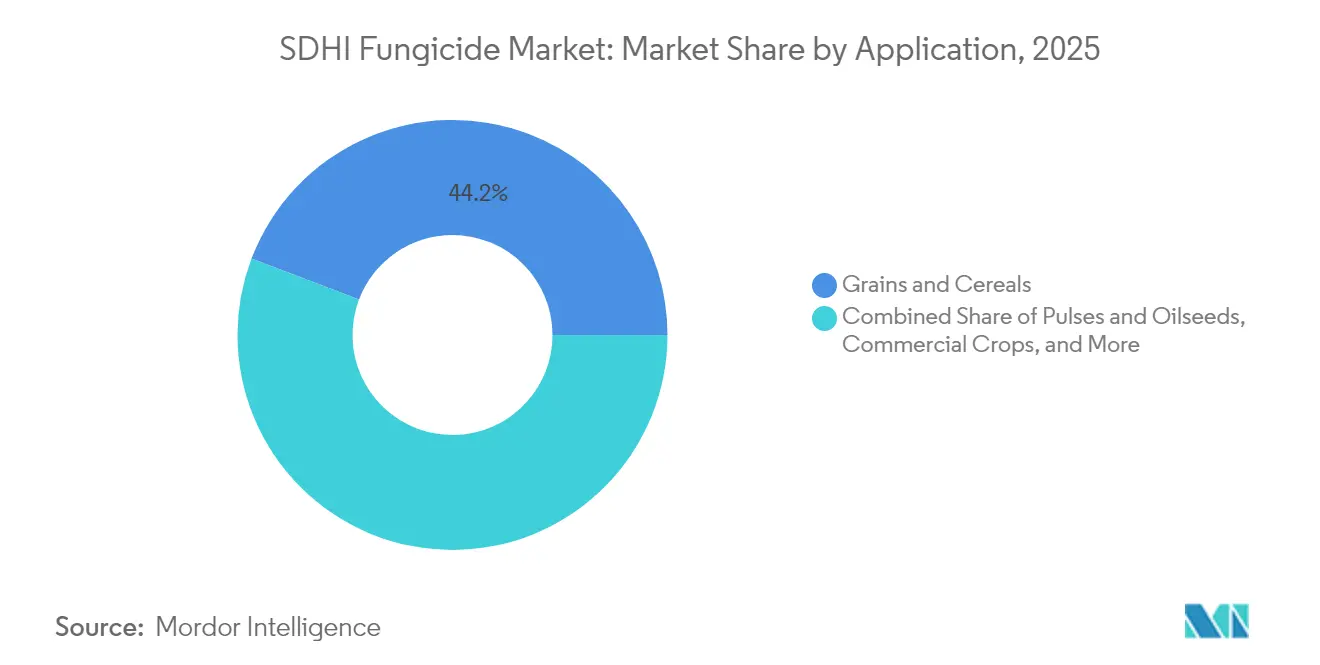

- By application, grains and cereals led with 44.22% of the SDHI fungicide market share in 2025, while turf and ornamentals are projected to expand at a 9.55% CAGR through 2031.

- By mode of application, foliar sprays held 66.35% of the SDHI fungicide market size in 2025, and seed treatment is advancing at a 9.78% CAGR through 2031.

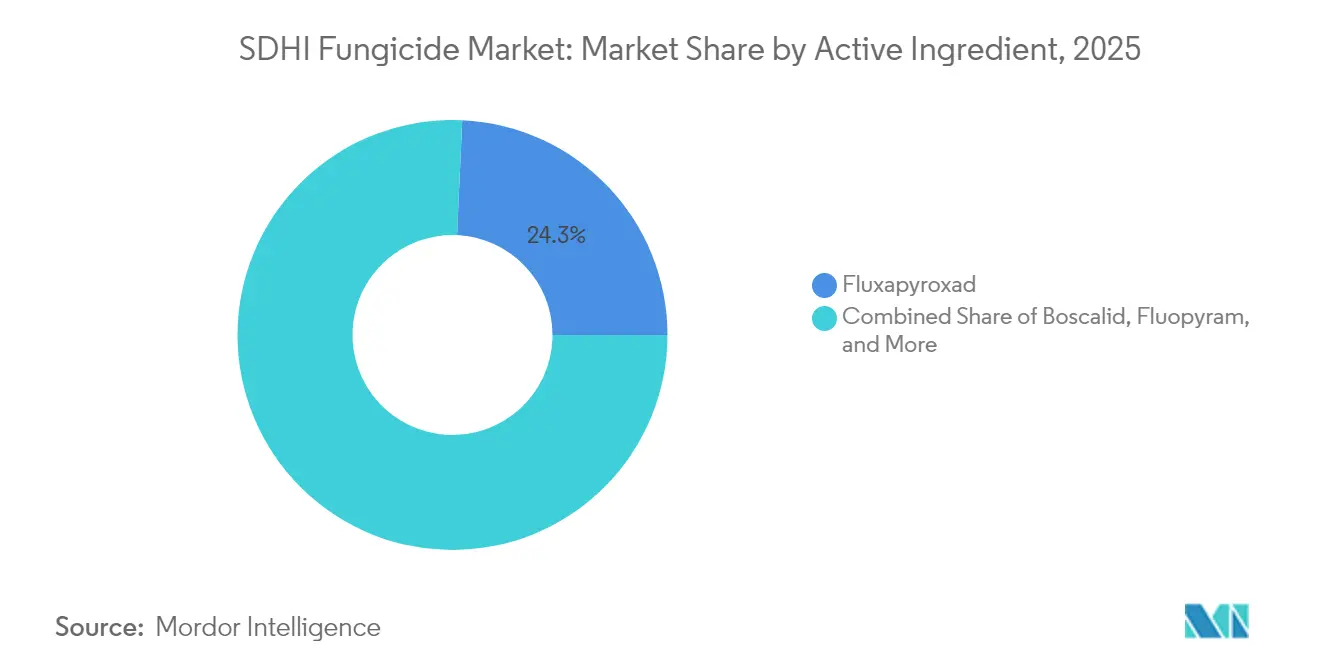

- By active ingredient, fluxapyroxad captured 24.28% of the market share in 2025, whereas isoflucypram is forecast to grow at an 10.85% CAGR between 2026 and 2031.

- By formulation type, liquid suspension concentrates dominated the market with a 57.25% share in 2025, and the water-dispersible granules segment is anticipated to grow at a CAGR of 8.74% during the forecast period.

- By geography, Europe accounted for 33.74% of global revenue in 2025, while the Asia-Pacific is poised for a 9.52% CAGR through 2031.

- BASF SE, Syngenta Group, Bayer AG, Corteva Agriscience, and FMC Corporation collectively hold the majority of the market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global SDHI Fungicide Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Climate-change-driven disease pressure | +1.6% | Global with acute effects in North America and Europe | Medium term (2-4 years) |

| Rapid expansion of SDHI label approvals in emerging markets | +1.4% | Asia Pacific core with spill-over to South America and Africa | Short term (≤ 2 years) |

| Integration with digital-farming decision tools | +1.1% | North America and Europe expanding to Asia Pacific | Medium term (2-4 years) |

| Rising multi-fungicide resistance in fungal pathogens | +1.0% | Europe and North America with emergence in Asia Pacific | Long term (≥ 4 years) |

| Yield-boost imperatives for low-margin row crops | +0.8% | Global grain-producing regions | Short term (≤ 2 years) |

| Investor focus on low-carbon crop-protection portfolios | +0.7% | Europe and North America with global expansion | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Climate-Change-Driven Disease Pressure

The evolution and geographic expansion of pathogens are altering the demand patterns for SDHI fungicides in global agriculture. Wheat blast (Magnaporthe oryzae) has established permanent populations in Bangladesh and Brazil, necessitating growers to implement SDHI rotation programs. Changes in temperature and rainfall patterns have extended infection periods for Fusarium, Septoria, and wheat blast diseases. These longer disease cycles necessitate additional fungicide applications, increasing SDHI usage. The climate-induced disease pressure generates sustained demand growth, unlike historical fungicide adoption patterns. New SDHI molecules, including isoflucypram and benzovindiflupyr, exhibit superior efficacy under varying environmental conditions compared to traditional triazole and strobilurin fungicides.

Rapid Expansion of SDHI Label Approvals in Emerging Markets

Recent regulatory changes in the Asia-Pacific and South American markets have created growth opportunities for SDHI fungicide manufacturers. In China, Interstate Compact on Adoption and Medical Assistance (ICAMA approved several SDHI registrations in 2024, including domestic production licenses for boscalid and fluopyram formulations. Brazil streamlined registrations for soybean and corn applications, providing growers with alternatives to address resistance issues. In 2024, India's Food Safety Standards Authority (FSSAI) increased the Maximum Residue Limit (MRL) of pesticides in herbs and spices from 0.01 mg/kg to 0.1 mg/kg, enabling wider adoption across India's agricultural sector[2]Source: Food Safety Standards Authority of India (FSSAI), " Maximum Residue Limits (MRLs) for Spices and Culinary Herbs", fssai.gov.in . These regulatory developments benefit companies with established registration documentation and local production facilities. The expanded approvals particularly support combination products that integrate SDHI chemistry with other modes of action, aligning with regulatory preferences for comprehensive resistance management strategies.

Integration with Digital-Farming Decision Tools

Digital platforms, such as Syngenta's Xarvio, integrate weather data, crop growth stages, and pathogen risk assessments to optimize SDHI fungicide applications for specific fields. BASF's digital farming solutions have achieved a 30% reduction in fungicide usage through improved application timing and variable-rate technology, addressing both cost and environmental concerns in agriculture. The integration of drone technology and variable-rate applications enables precise dosing and timing, increasing demand for premium, data-connected formulations. SDHI manufacturers that invest in decision support systems and data analytics gain competitive advantages. This digital transformation particularly benefits premium SDHI products that demonstrate enhanced performance and reduced application frequency to justify their higher costs.

Rising Multi-Fungicide Resistance in Fungal Pathogens

Septoria tritici blotch populations in European wheat regions exhibit resistance to triazole and strobilurin fungicides, making SDHI applications necessary for disease control[3]Source: French Agency for Food, Environmental and Occupational Health and Safety, “SDHI Fungicides Risk Assessment,” anses.fr. Fusarium graminearum isolates with reduced sensitivity to multiple modes of action are present across North American cereal regions, increasing the need for SDHI-based rotation programs. The resistance development patterns indicate higher efficacy of newer SDHI molecules with different binding sites and cross-resistance profiles compared to older chemistry. The presence of multi-resistance particularly benefits combination products that contain SDHI chemistry with complementary modes of action, as these formulations provide better resistance management compared to sequential applications of single-active products.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pipeline competition from next-generation biologic fungicides | -1.20% | Global with early adoption in North America and Europe | Medium term (2-4 years) |

| Growing maximum-residue-limit (MRL) scrutiny | -0.90% | Europe and North America expanding to Asia Pacific | Short term (≤ 2 years) |

| High discovery and registration costs | -0.70% | Global with disproportionate effect on small firms | Long term (≥ 4 years) |

| Supply-chain volatility for key SDHI intermediates | -0.60% | Global with concentration in Asia Pacific manufacturing | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Pipeline Competition From Next-Gen Biologic Fungicides

Biological fungicides are gaining acceptance as alternatives to SDHI chemistry in specific crop protection scenarios, which may limit market growth in premium segments. Major agrochemical companies are acquiring biocontrol capabilities to develop synthetic-biological product combinations. Certis Biologicals' acquisition of Howler and Theia in 2024 demonstrates comparable efficacy in certain crops. BASF's Serifel biofungicide offers broad-spectrum disease control through multiple modes of action, enabling reduced SDHI usage in integrated pest management programs. In premium fruit and vegetable markets, growers are transitioning to biological alternatives where buyers prioritize chemical-free produce.

Growing Maximum-Residue-Limit (MRL) Scrutiny

The European Food Safety Authority increased monitoring and documented excess levels in imported agricultural products, leading to enhanced inspections and potential trade restrictions[4]Source: European Food Safety Authority, “Pesticide Residue Monitoring,” efsa.europa.eu. French agricultural regions focused on exports face challenges due to varying Maximum Residue Level (MRL) standards in destination markets, which affect fungicide selection and usage protocols. These regulations particularly impact new Succinate Dehydrogenase Inhibitor (SDHI) compounds that have limited toxicological data and established MRL guidelines. The costs of compliance and restrictions on application may increase the adoption of biological alternatives and integrated pest management methods that reduce reliance on synthetic fungicides, potentially limiting SDHI market growth in regulated areas.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Cereals Drive Volume While Turf and Ornamentals Command Premium

Grains and cereals account for 44.22% of the SDHI fungicide market share in 2025. This dominance stems from extensive acreage and intensive disease management needs across global wheat, corn, and barley production systems. The prevalence of Fusarium head blight in wheat regions and gray leaf spot in corn drives consistent SDHI demand, particularly for products combining SDHI chemistry with other modes of action.

Turf and ornamentals represent the fastest-growing application segment with a 9.55% CAGR through 2031. This growth is driven by high pricing tolerance and intensive maintenance needs in golf courses, sports facilities, and landscape applications. The fruits and vegetables segment expands through new SDHI label approvals for specialty crops, while commercial crops such as cotton and sugarcane implement SDHI programs in high-value production systems. Pulses and oilseeds applications continue to grow as soybean and canola producers adopt SDHI-based solutions for white mold and sclerotinia management, particularly in North American regions with increased disease pressure. This application diversity enables the development of specialized formulations targeting specific crop diseases while meeting regulatory requirements.

By Mode of Application: Foliar Dominance Challenged by Seed Treatment Growth

Foliar spray applications hold 66.35% of the SDHI fungicide market size in 2025, supported by established grower practices and demonstrated effectiveness against foliar pathogens across crop systems. Seed treatment applications are growing at a 9.78% CAGR through 2031, driven by new SDHI formulation approvals and increasing demand for early-season disease protection. Post-harvest treatments occupy specific market segments, including grain storage protection and fruit preservation, creating opportunities for companies with specialized formulation capabilities and required regulatory clearances.

The transition toward seed treatments offers multiple advantages, including minimized environmental impact, precise pathogen control, and compatibility with other seed-applied products like insecticides and plant growth regulators. BASF's ILeVO fluopyram seed treatment exemplifies SDHI chemistry's effectiveness in protecting corn and soybean seedlings from soilborne diseases. Regulatory bodies prefer seed treatments over foliar applications due to reduced drift and lower environmental risks. This trend benefits companies that possess seed treatment formulation expertise and maintain strong connections with seed producers and commercial treatment facilities.

By Active Ingredient: Fluxapyroxad Face Emerging Competition

Fluxapyroxad holds 24.28% of the SDHI fungicide market share in 2025, due to its broad-spectrum effectiveness, regulatory compliance, and established use across multiple crops. Boscalid retains substantial market presence through generic availability and cost-effective formulations, while fluopyram shows strong results in seed treatment applications. Isoflucypram emerges as the fastest-growing compound with an 10.85% CAGR through 2031, driven by its recent market entry and enhanced control of resistant pathogens compared to older SDHI compounds.

Benzovindiflupyr and bixafen occupy distinct market segments based on their performance attributes and regulatory status, while penthiopyrad and sedaxane target specific crop diseases. The market reflects continuous development and patent expirations, creating opportunities for both research-based and generic companies. The 2024 approval for domestic penflufen production by Zhongshan Chemical Group in China illustrates the potential for emerging market manufacturers to gain share in established SDHI segments. Patent expiration schedules and regulatory protection periods shape the competitive environment and pricing strategies across SDHI compounds.

By Formulation Type: Liquid Suspension Concentrates Lead Innovation

Liquid suspension concentrates hold 57.25% of the SDHI fungicide market share in 2025, due to their superior handling characteristics, tank-mix compatibility, and application flexibility. Water-dispersible granules are growing at a 8.74% CAGR through 2031, supported by lower packaging costs, better storage stability, and grower preference for solid formulations in specific applications. Emulsifiable concentrates and wettable powders maintain their presence in specialized applications and regional markets, while dustable powders and soluble powders serve niche market segments.

The formulation sector emphasizes improving biological efficacy, minimizing environmental impact, and enhancing user safety through delivery systems and adjuvant technologies. Regulatory requirements for specific formulation types provide competitive advantages to companies with established manufacturing capabilities and registration expertise. Regional preferences, application equipment requirements, and regulatory standards shape product development and market strategies across different territories.

Geography Analysis

Europe held 33.74% of the SDHI fungicide market share in 2025. The region's extensive cereal production, robust agricultural advisory services, and strict stewardship requirements have established SDHIs as an essential component in resistance management strategies. The region's subsidy systems, which support integrated pest management practices, maintain the demand for premium fungicides despite regulatory challenges. Germany, France, and the United Kingdom serve as primary markets due to their intensive cereal production and established SDHI usage. Spain and Italy focus on specialty crop applications, particularly in fruits and vegetables. Ongoing regulatory reviews by the French Agency for Food, Environmental and Occupational Health & Safety (ANSES) and European Food Safety Authority (EFSA) may affect future market growth in specific European regions.

Asia-Pacific exhibits the highest growth rate at 9.52% CAGR through 2031. This growth stems from agricultural modernization in China and India, new SDHI product approvals, and increasing disease pressures across various crop systems. China's domestic SDHI manufacturing capabilities and regulatory framework for key active ingredients support regional growth. India's expansion in specialty crops and improved Maximum Residue Level (MRL) standards facilitate market development. Japan and Australia represent established markets with consistent SDHI usage and acceptance of premium pricing.

North America maintains consistent growth through extensive grain production and comprehensive disease management programs, particularly in corn and soybean cultivation, where SDHI chemistry provides key resistance management solutions. South America, the Middle East, and Africa present growth opportunities through expanding agricultural production and increasing fungicide adoption. Brazil's agricultural expansion and SDHI approvals for soybeans and corn applications offer significant market potential, while Argentina and other regional markets develop SDHI programs for cereals and specialty crops.

Regulatory Landscape

Residue compliance and risk-mitigation requirements continue to shape the regulatory environment for SDHI fungicides across major agricultural markets. In China, GB 2763-2026 (National Food Safety Standard for pesticide maximum residue limits) was published by the National Health Commission together with the Ministry of Agriculture and Rural Affairs and the State Administration for Market Regulation, and it became effective on March 1, 2026. The update expanded the MRL framework across a wide set of pesticides and added new indicators that affect crop-export compliance planning.

In the United States, the U.S. EPA released a Draft Fungicide Strategy in May 2026 to reduce exposure of federally listed endangered and threatened species, aligning fungicide use with Endangered Species Act implementation through application-focused mitigation measures (for example, spray drift management). Finalization is targeted by fall 2026. In Europe, EFSA continues periodic scientific assessments and monitoring related to pesticide residues and SDHI mode-of-action questions, keeping stewardship, documentation, and residue monitoring central to registrations and market access for SDHI-based products and mixtures.

Competitive Landscape

BASF SE, Syngenta Group, Bayer AG, Corteva Agriscience, and FMC Corporation control the majority of the SDHI fungicide market share in 2024, indicating moderate market concentration. BASF SE maintains market leadership through its broad portfolio of fluxapyroxad, isoflucypram, and fluopyram products. Syngenta Group holds the second position with its benzovindiflupyr formulations and digital agronomy integration. Bayer AG focuses on life-cycle extensions through combination products and seed-treatment variants. Corteva Agriscience and FMC Corporation maintain specialized positions through targeted crop segments and novel active ingredients.

Market dynamics are evolving as patent expirations create opportunities for generic manufacturers and regional specialists, particularly in Asia-Pacific markets where domestic production capabilities continue to expand. BASF integrates carbon-credit verification with SDHI programs, while Syngenta incorporates real-time disease modeling into its Xarvio recommendations. While patent expirations provide opportunities for generic manufacturers, stewardship requirements and digital integration requirements provide competitive advantages to established companies. Supply chain resilience and environmental chemistry alignment have become strategic priorities.

Mergers and cross-licensing agreements reflect industry efforts to expand capabilities. Corteva's soybean collaboration with BASF combines herbicide tolerance with fungicide seed treatments, focusing on SDHIs. Regulatory compliance requirements and stewardship program investments create entry barriers for smaller competitors while allowing established companies to maintain premium positioning and pricing advantages in regulated markets.

SDHI Fungicide Industry Leaders

-

BASF SE

-

Syngenta Group

-

Bayer AG

-

Corteva Agriscience

-

FMC Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: BASF launched Balaya fungicide (Revysol + F500) in Australia for cereals, pulses, and canola. The launch expands BASF's fungicide portfolio in a major cereals market where resistance management and performance under variable disease pressure influence product selection.

- October 2025: BASF received U.S. EPA registration for Zorina fungicide (containing Revysol) for use on soybeans, canola, and dry beans. The registration increases addressable acreage in key row crops and supports portfolio life-cycle management through new labels and mixtures used in rotation programs.

- May 2024: Syngenta reinforced its fungicide portfolio around ADEPIDYN technology (active ingredient: pydiflumetofen). This development supports Syngenta's differentiation in higher-efficacy fungicides and integrated resistance-management programs across multiple crops.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the SDHI fungicide market is the value of succinate dehydrogenase inhibitor fungicide products sold for controlling fungal diseases across major crop and non-crop uses, counted at the point of sale in each geography.

Scope exclusions: We exclude non-SDHI fungicide chemistries and the value of downstream crop output, along with farm service labor and spraying equipment.

Segmentation Overview

-

By Application

- Grains and Cereals

- Pulses and Oilseeds

- Commercial Crops

- Fruits and Vegetables

- Turf and Ornamentals

- Other Applications (Forage and Fodders, Flowers, etc.)

-

By Mode of Application

- Foliar Spray

- Seed Treatment

- Post-Harvest Treatment

-

By Active Ingredient

- Boscalid

- Fluopyram

- Fluxapyroxad

- Bixafen

- Benzovindiflupyr

- Isoflucypram

- Others (Penthiopyrad, Sedaxane, Isaflumet, etc.)

-

By Formulation Type

- Liquid Suspension Concentrates

- Water-Dispersible Granules

- Emulsifiable Concentrates

- Wettable Powders

- Other Formulations (Dustable Powder, Soluble Powder, etc.)

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Spain

- United Kingdom

- France

- Germany

- Russia

- Italy

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Australia

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Rest of South America

-

Middle East

- Saudi Arabia

- Turkey

- Rest of Middle East

-

Africa

- South Africa

- Nigeria

- Rest of Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started by mapping where SDHI actives are registered and how they are used in the field, since product labels and allowed crops shape real demand. We referred to public sources such as pesticide regulatory portals, food residue and maximum residue limit publications, national agriculture statistics, and FAO-style crop area and yield series, which help set the demand pool by crop and region.

To convert agronomic demand into market value, we also reviewed sources such as customs and trade statistics for agrochemical shipments, patent databases for active ingredient and formulation activity, and publicly available company filings and investor presentations for product-mix clues. In a few places, a paid subscription focused on company financials and a shipment-level trade database were used to sanity-check volumes and pricing direction. These examples are illustrative only, and many other public sources and references were used to fill gaps and confirm assumptions.

Primary Interviews and Surveys

Primary conversations were used to confirm how SDHI products are purchased and applied, and which crops and regions show stronger adoption based on disease pressure and resistance management practices. We spoke with stakeholders across the value chain, including formulators, distributors, agronomists, and large farm operators, and then used follow-up checks to align pricing ranges, the split between single active and premix products, and seasonality by crop calendar across regions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 14% | APAC: 48% |

| Mid tier: 56% | Functional/Unit leaders: 29% | EMEA: 34% |

| Smaller Players: 15% | Managers: 57% | Americas: 18% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where crop area and production patterns, together with typical treatment intensity for key fungal diseases, were translated into a demand pool for SDHI applications by region. Once that structure was in place, the totals were cross-checked using selective bottom-up approximations, such as sampled price per hectare by crop, channel markups, and supplier mix checks, so the final value stayed realistic.

Key inputs in the model included planted area and harvested area for major crops, fungicide spray frequency by crop and season, SDHI share within fungicide programs (including rotation practices), average selling price movement by formulation and premix penetration, and changes in registrations and residue limits that affect usable dose rates. Where data was thin for smaller crops or emerging regions, proxy assumptions were taken from comparable crops, and then corrected using interview-based adoption and pricing feedback.

Forecasts were developed using scenario analysis supported by simple trend fitting on planted area and intensity indicators, and then adjusted with expert views on resistance management, new product launches, and regulatory tightening. As the main clause in our outlook arrives at the end, it stays tied to field reality: treated hectares, dose, and price direction determine the growth path.

Data Validation & Update Cycle

Results were validated by checking internal consistency across regions, crop calendars, and implied usage intensity, and by testing for sharp jumps that did not match regulatory or agronomic signals. Where a variance appeared, we reworked the underlying drivers first, then recalculated market totals before review.

A multi-step analyst review was followed so assumptions, conversions, and unit handling were verified, and sensitive inputs such as pricing and adoption were rechecked through follow-up outreach when needed. Reports are refreshed annually, with interim updates captured when material events occur, and a final pre-release pass is completed so the latest information is reflected in the delivered numbers.

Mordor Intelligence's Sdhi Fungicide Market Size Compared With Other Published Estimates

Published SDHI fungicide market values often differ because each publisher selects its own year, scope, and pricing logic, and those choices can move the total up or down quickly. In practice, the largest gaps usually come from how premix products are counted, how currency timing is handled, and whether the study is tied back to treated-area reality or left as a high-level revenue trend.

Some sources lean toward broader crop-protection counting or use earlier base years and then carry forward growth with limited checks on treated hectares and dose rates. For Mordor Intelligence, the market is counted as SDHI fungicide sales only, and the totals are reconciled against crop-wise treatment intensity, adoption by region, and realistic price progression before the forecast is extended.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.23 B (2026) | |

| Industry Publisher A | USD 4.42 B (2025) | Uses a different base year and appears to apply a smoother long-range CAGR, which can miss near-term shifts from residue rule changes and premix mix-shift that affect realized revenue. |

| Industry Publisher B | USD 2.70 B (2023) | Anchored to an earlier year and can understate later adoption and price normalization in high-use crops, especially when treated-area expansion and higher intensity seasons are not explicitly rebuilt. |

The spread in the table is mainly explained by base-year selection and what is included in the counted sales value, and those two items drive most of the math. By rebuilding demand from crop area, spray intensity, and SDHI share, then stress-testing prices through channel feedback, the estimate stays traceable to practical variables that can be reviewed and repeated.

Key Questions Answered in the Report

What is the current value of the SDHI fungicide market?

The market is valued at USD 4.23 billion in 2026.

How fast is the SDHI fungicide market projected to grow?

The market is projected to post a 7.72% CAGR between 2026 and 2031.

Which application segment holds the largest revenue share?

Grains and cereals led with 44.22% of 2025 sales.

Which region is forecast to grow the fastest?

Asia-Pacific is projected to expand at a 9.52% CAGR through 2031.

What factors are driving SDHI adoption in cereals?

Rising multi-fungicide resistance, climate-driven disease pressure, and the need for yield protection underpin demand.

Who are the leading companies in the SDHI space?

BASF SE, Syngenta Group, Bayer AG, Corteva Agriscience, and FMC Corporation collectively control the majority of global revenue.

Page last updated on: