India Fungicide Market Size and Share

Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

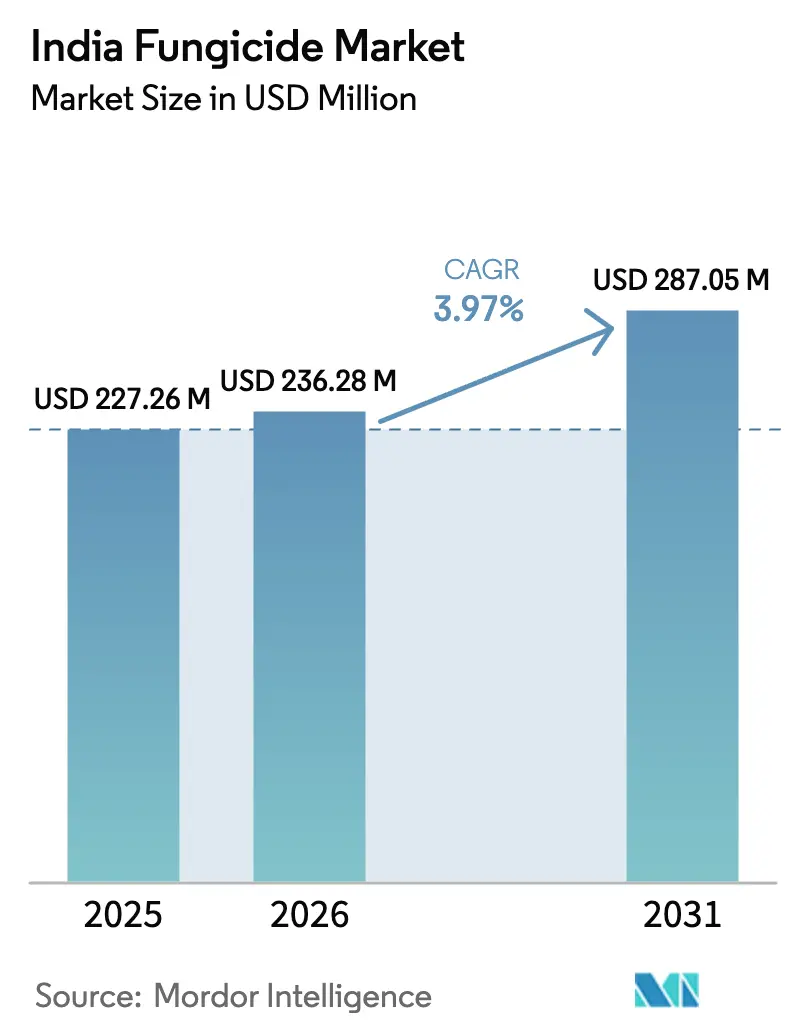

| Base Year Market Size (2025) | USD 227.26 Million |

| Market Size (2026) | USD 236.28 Million |

| Market Size (2031) | USD 287.05 Million |

| Growth Rate (2026 - 2031) | 3.97% CAGR |

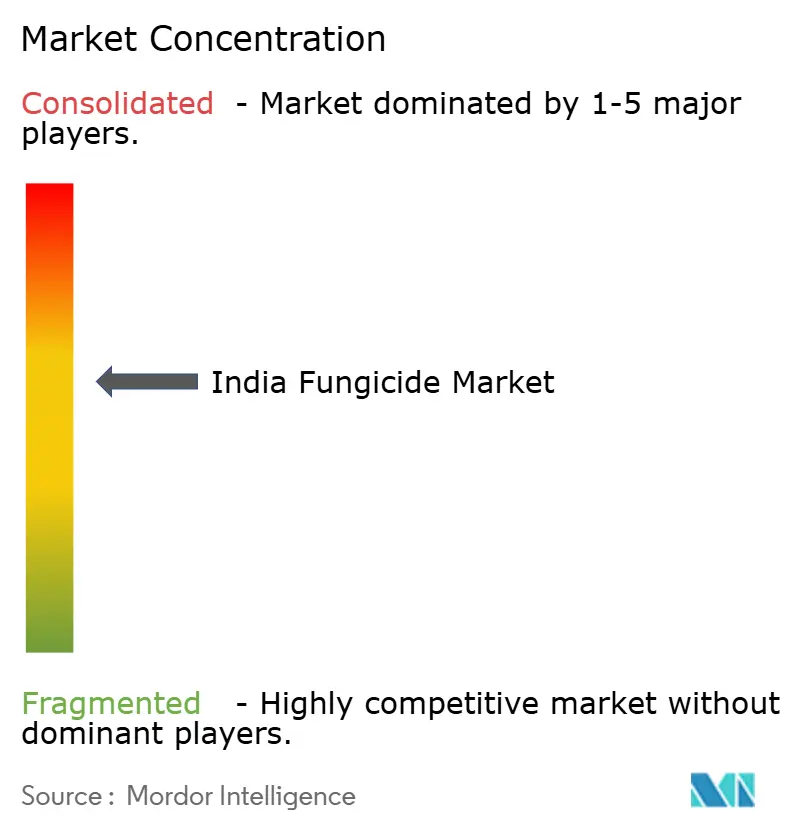

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Fungicide Market Analysis by Mordor Intelligence

India fungicide market size in 2026 is estimated at USD 236.28 million, growing from 2025 value of USD 227.26 million with 2031 projections showing USD 287.05 million, growing at 3.97% CAGR over 2026-2031. Demand reflects the country’s shift toward precision crop protection, wider agro-climatic risks, and growing compliance with residue limits that favor modern chemistries. Larger exports of crop protection actives strengthen local manufacturing economics, while policy incentives for drone spraying shorten application windows and reduce labor exposure. Competition intensifies as multinational innovators defend technology premiums and domestic manufacturers leverage cost efficiency, extensive rural distribution, and close farmer relationships. Regional uptake remains strongest in Punjab, Haryana, Maharashtra, Gujarat, and Karnataka where commercial cropping systems and organized procurement create steady fungicide pull; eastern and north-eastern regions provide long-run upside as subsidy schemes improve access.

Key Report Takeaways

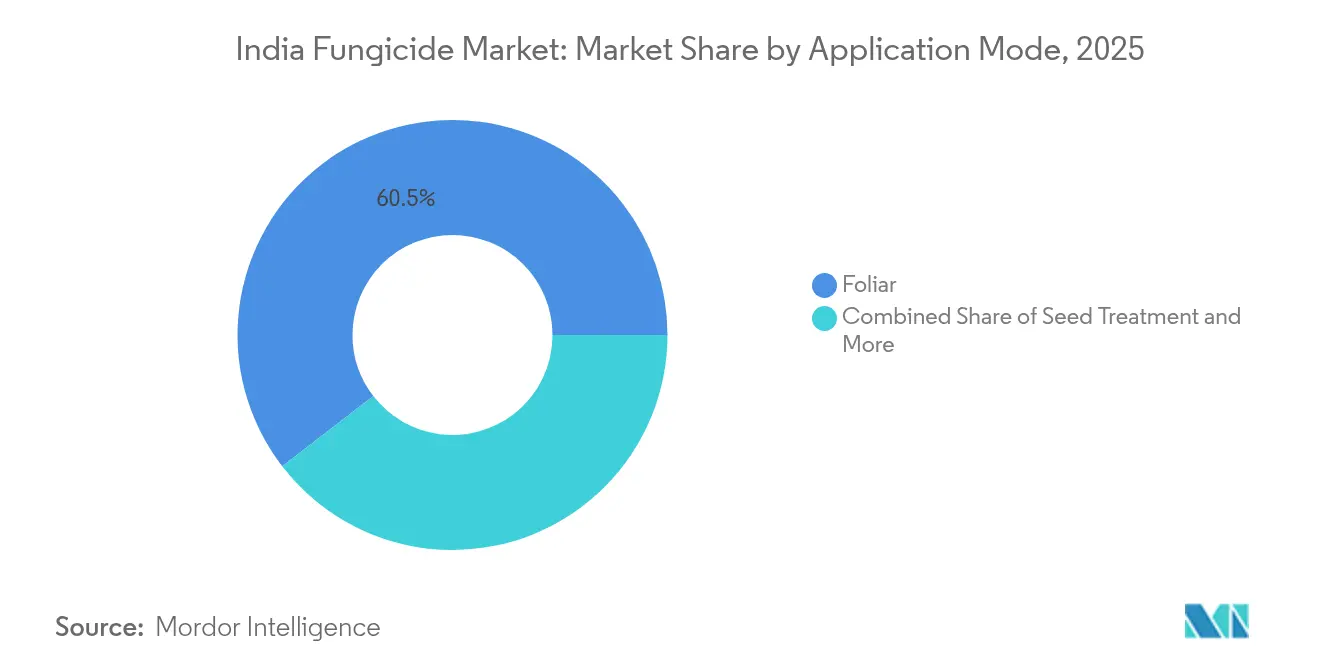

- By application mode, foliar treatments held 60.45% of the India fungicide market size in 2025 and are projected to advance at a 4.12% CAGR to 2031.

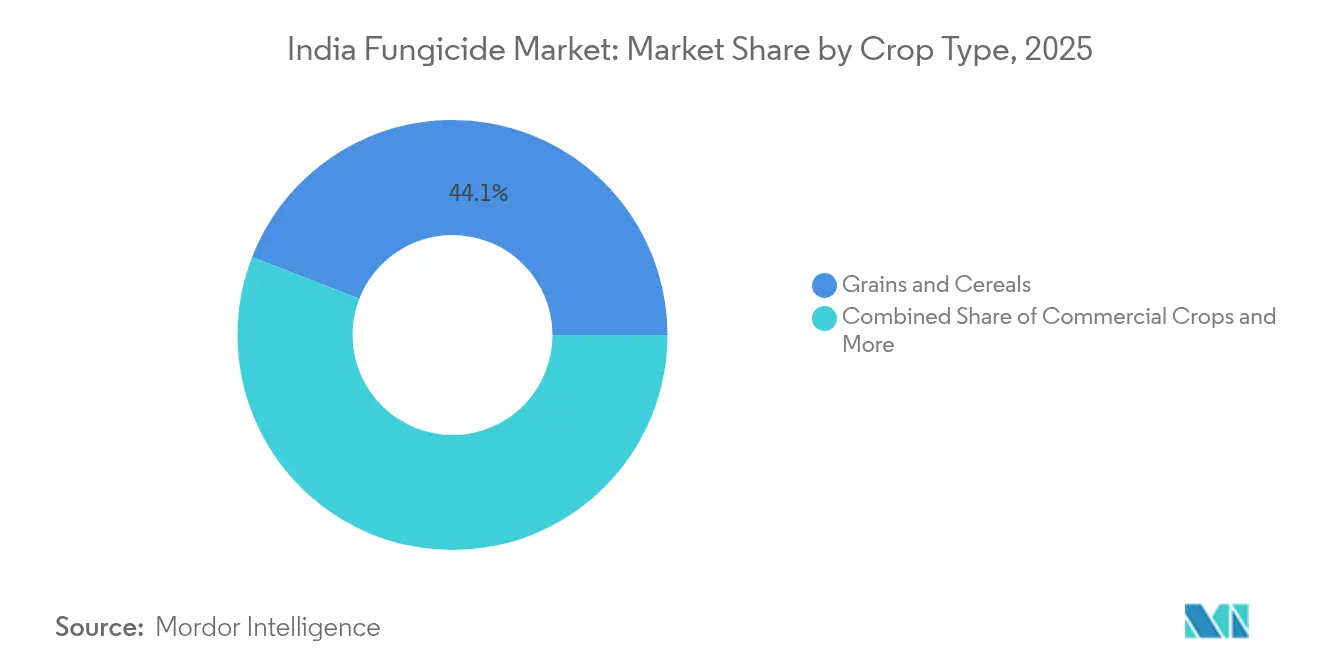

- By crop type, grains and cereals commanded 44.10% of the India fungicide market share in 2025, while commercial crops recorded the fastest growth at a 4.19% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Fungicide Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Widespread herbicide resistance in weeds | +0.8% | Pan-India, concentrated in Punjab, Haryana, Maharashtra | Medium term (2-4 years) |

| Government subsidy reforms favoring post-emergence actives | +0.6% | National, with early gains in Uttar Pradesh, Madhya Pradesh, and Karnataka | Short term (≤ 2 years) |

| Expansion of herbicide-tolerant cotton acreage | +0.5% | Gujarat, Maharashtra, Telangana, and Andhra Pradesh | Long term (≥ 4 years) |

| Surge in farm-labor costs pushing chemical weed control | +0.7% | National, particularly acute in Punjab, Haryana, and Western Maharashtra | Medium term (2-4 years) |

| Climate-induced weed-pressure spikes | +0.4% | Pan-India, variable intensity across agro-climatic zones | Long term (≥ 4 years) |

| Drone-enabled precision spraying adoption | +0.3% | Progressive states: Punjab, Haryana, Karnataka, and Maharashtra | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Widespread herbicide resistance in weeds

Escalating herbicide resistance across India's major cropping systems creates substantial demand for fungicide rotation strategies and integrated pest management approaches. Multiple weed species, including Phalaris minor in wheat and Echinochloa species in rice, demonstrate resistance to commonly used herbicides, forcing farmers to adopt fungicide-based disease management programs that reduce overall chemical pressure on weed populations. The Central Insecticides Board and Registration Committee has documented resistance cases across 15 states, with Punjab and Haryana reporting the highest incidence rates due to intensive monoculture practices[1]Source: Central Insecticides Board, “Minutes of the 441st Registration Committee Meeting,” agricoop.nic.in.

Government subsidy reforms favoring post-emergence actives

Recent policy modifications in agricultural input subsidies prioritize post-emergence fungicide applications over prophylactic treatments, aligning with sustainable agriculture initiatives and integrated pest management protocols. The Ministry of Agriculture and Farmers Welfare's revised subsidy structure provides enhanced support for targeted fungicide applications based on disease surveillance and economic threshold principles, reducing blanket spraying practices while maintaining crop protection efficacy. State governments in Uttar Pradesh and Madhya Pradesh have implemented pilot programs offering 60% subsidies for precision fungicide applications, compared to 40% for conventional broad-spectrum treatments.

Expansion of herbicide-tolerant cotton acreage

Growing cultivation of herbicide-tolerant cotton varieties necessitates complementary fungicide programs to manage disease pressure in simplified weed management systems. These varieties require specialized fungicide regimens to address bollworm resistance and secondary pest complexes that emerge under altered chemical selection pressure. The Central Institute for Cotton Research reports increased fungal disease incidence in herbicide-tolerant systems, particularly Alternaria leaf spot and Fusarium wilt, driving demand for systemic fungicides with extended residual activity. Integration of herbicide tolerance traits with disease resistance remains incomplete, creating sustained fungicide demand growth in cotton-producing regions.

Surge in farm-labor costs pushing chemical weed control

Escalating agricultural labor costs across India's major farming regions accelerate the adoption of chemical crop protection solutions, including fungicides, as cost-effective alternatives to manual field operations. Average farm labor wages increased 12-15% annually between 2022-2024, with peak season rates reaching ₹400-500 (USD 4.8-6.0) per day in Punjab and Haryana, compared to ₹250-300 (USD 3.0-3.6) in 2020. This cost inflation drives mechanization and chemical intensification trends that favor fungicide applications over labor-intensive cultural practices for disease management.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter registration norms for legacy actives | -0.4% | National, affecting all manufacturers | Short term (≤ 2 years) |

| Growing counterfeit product circulation | -0.3% | Pan-India, concentrated in Uttar Pradesh, Bihar, and West Bengal | Medium term (2-4 years) |

| Small-holder fragmentation limiting large-pack sales | -0.2% | National, particularly acute in eastern and southern states | Long term (≥ 4 years) |

| Cultural preference for manual weeding | -0.2% | Rural areas, traditional farming communities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stricter registration norms for legacy actives

Enhanced regulatory scrutiny by the Central Insecticides Board and Registration Committee creates compliance challenges for older fungicide formulations, potentially restricting market availability and increasing development costs for manufacturers. The registration process now requires extensive residue data, bee toxicity studies, and groundwater contamination assessments that can cost ₹50-80 lakh (USD 60,000-96,000) per active ingredient. Several legacy fungicides face deregistration risks, including certain copper-based formulations and older triazole compounds that lack modern safety data packages Ministry of Agriculture & Farmers Welfare. Compliance requirements favor multinational corporations and larger domestic players with robust regulatory affairs capabilities over smaller manufacturers lacking technical resources.

Growing counterfeit product circulation

Proliferation of fake fungicide products undermines market growth by eroding farmer confidence and creating price competition from substandard alternatives that compromise crop protection efficacy. Enforcement agencies conducted major seizures in 2024, including fake pesticides worth ₹2.5 crore (USD 300,000) in Delhi and similar operations across Telangana, Maharashtra, and Uttar Pradesh that revealed sophisticated counterfeiting networks[2]Source: Pesticides Manufacturers and Formulators Association of India, “Counterfeit Agrochemicals Study 2024,” pmfai.org. These products typically contain 20-40% of labeled active ingredient concentrations, leading to control failures and resistance development that damage legitimate product reputations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application Mode: Sustained Foliar Dominance amid Tech Adoption

Foliar applications account for 60.45% of the India fungicide market and are paced to grow at 4.12% through 2031, supported by rapid systemic uptake and the spread of drone spraying that lowers water use. Chemigation serves specialty vineyards and orchards, while fumigation tackles soil-borne pathogens in protected cultivation. Seed treatment advances on hybrid seed adoption, and soil treatment retains niche relevance in intensive vegetable clusters. Precision weather-linked advisory apps further raise foliar efficiency and position the India fungicide market for incremental gains.

Complementary methods expand smaller bases: chemigation benefits drip-irrigated pomegranate blocks in Maharashtra; fumigation protects mushroom and nursery operations; seed treatment lowers early-season losses in pulses. Regulatory emphasis on operator safety and residue compliance sustains foliar and seed treatment share. The India fungicide industry also sees pilot projects blending biologicals with systemic foliar sprays to delay resistance onset.

By Crop Type: Commercial Crops Set the Growth Pace

Grains and cereals maintain a 44.10% share of the India fungicide market, anchored by the wheat-rice rotation across the Indo-Gangetic plains and coarse grains in semi-arid belts. Commercial crops cotton, sugarcane, and high-value horticulture post the fastest 4.19% CAGR, propelled by export ambitions and price premiums that justify intensive fungicide programs. The India fungicide market size for commercial crops is projected to expand as Bt cotton hybrids amplify fungal disease susceptibility under herbicide tolerance regimes.

Fruits and vegetables draw premium import standards, lifting per-acre fungicide spend; grapes and onions typify high-frequency spraying patterns. Pulses and oilseeds require targeted late-season applications against rust and blight; turf and ornamentals remain a niche yet lucrative outlet in urban landscaping and golf greens. Rising residue scrutiny in export channels drives growers toward modern actives with shorter pre-harvest intervals, reinforcing the India fungicide market’s upgrade cycle.

Geography Analysis

India's fungicide market demonstrates regional concentration patterns aligned with intensive agricultural zones and high-value crop production areas, with northern and western states leading consumption due to their advanced farming practices and commercial agriculture focus. Punjab, Haryana, and western Uttar Pradesh account for approximately 35% of national fungicide consumption, driven by intensive wheat-rice cropping systems and high-input agriculture that prioritizes yield maximization over cost considerations.

Eastern states, including West Bengal, Bihar, and Odisha, present growth opportunities through rice intensification programs and vegetable cultivation expansion, though adoption rates remain constrained by small farm sizes and limited purchasing power. The region's high humidity and intensive rice cultivation create favorable conditions for blast disease and bacterial blight that require consistent fungicide protection, yet cultural preferences for traditional practices and limited technical knowledge slow market penetration.

Southern states post balanced year-round demand across rice, cotton, and high-value fruit crops; Karnataka’s maize-plus-horticulture matrix and Tamil Nadu’s precision drip infrastructure bolster ready uptake of foliar and chemigation solutions. Eastern India offers long-term upside: West Bengal’s vegetable belts and Odisha’s rice intensification projects receive higher subsidy allocation for integrated fungicide programs, though small holdings and lower cash flow temper immediate volumes. Humid north-eastern states face chronic blast pressure but require focused extension to scale the India fungicide market.

Competitive Landscape

The India fungicide market exhibits moderate fragmentation, with multinational corporations maintaining technology leadership while domestic players leverage cost advantages and local market knowledge to capture significant market shares. Market concentration reflects a mix of global agrochemical giants, including BASF SE, Bayer AG, PI Industries, and Syngenta, alongside established Indian companies such as UPL, Rallis India, and PI Industries that combine manufacturing capabilities with extensive distribution networks.

Recent consolidation activities reshape competitive dynamics, exemplified by Dhanuka Agritech's ₹165 crore (USD 19.8 million) acquisition of global rights to Bayer's Iprovalicarb and Triadimenol fungicides, granting access to specialized oomycete disease management solutions and international market expansion opportunities. Strategic partnerships between Indian manufacturers and global technology providers create hybrid business models that combine innovation capabilities with cost-effective production and local market access.

Technology adoption emerges as a key competitive differentiator, with companies investing in precision agriculture platforms, drone application services, and digital farmer engagement tools that enhance product efficacy and customer loyalty. UPL's integrated approach, combining seeds, crop protection, and biologicals, creates comprehensive solutions that address farmers' needs beyond individual fungicide products, while Rallis India leverages Tata Group resources to develop sustainable agriculture initiatives and farmer education programs.

India Fungicide Industry Leaders

Bayer AG

PI Industries

Rallis India Ltd

Syngenta Group

UPL Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Dhanuka Agritech completed acquisition of global marketing and distribution rights for two Bayer fungicides, Iprovalicarb and Triadimenol, in a ₹165 crore (USD 19.8 million) transaction covering 20+ countries across Latin America, Europe, Middle East, Africa, and Asia.

- August 2024: Syngenta introduced Miravis Duo and Reflect Top fungicides in the Indian market, offering broad-spectrum disease control for cotton and vegetable crops with improved resistance management profiles.

India Fungicide Market Report Scope

Chemigation, Foliar, Fumigation, Seed Treatment, Soil Treatment are covered as segments by Application Mode. Commercial Crops, Fruits & Vegetables, Grains & Cereals, Pulses & Oilseeds, Turf & Ornamental are covered as segments by Crop Type.| Chemigation |

| Foliar |

| Fumigation |

| Seed Treatment |

| Soil Treatment |

| Commercial Crops |

| Fruits and Vegetables |

| Grains and Cereals |

| Pulses and Oilseeds |

| Turf and Ornamental |

| Application Mode | Chemigation |

| Foliar | |

| Fumigation | |

| Seed Treatment | |

| Soil Treatment | |

| Crop Type | Commercial Crops |

| Fruits and Vegetables | |

| Grains and Cereals | |

| Pulses and Oilseeds | |

| Turf and Ornamental |

Market Definition

- Function - Fungicides are chemicals used to control or prevent fungi from damaging the crop and prevent yield loss.

- Application Mode - Foliar, Seed Treatment, Soil Treatment, Chemigation, and Fumigation are the different type of application modes through which crop protection chemicals are applied to the crops.

- Crop Type - This represents the consumption of crop protection chemicals by Cereals, Pulses, Oilseeds, Fruits, Vegetables, Turf, and Ornamental crops.

| Keyword | Definition |

|---|---|

| IWM | Integrated weed management (IWM) is an approach to incorporate multiple weed control techniques throughout the growing season to give producers the best opportunity to control problematic weeds. |

| Host | Hosts are the plants that form relationships with beneficial microorganisms and help them colonize. |

| Pathogen | A disease-causing organism. |

| Herbigation | Herbigation is an effective method of applying herbicides through irrigation systems. |

| Maximum residue levels (MRL) | Maximum Residue Limit (MRL) is the maximum allowed limit of pesticide residue in food or feed obtained from plants and animals. |

| IoT | The Internet of Things (IoT) is a network of interconnected devices that connect and exchange data with other IoT devices and the cloud. |

| Herbicide-tolerant varieties (HTVs) | Herbicide-tolerant varieties are plant species that have been genetically engineered to be resistant to herbicides used on crops. |

| Chemigation | Chemigation is a method of applying pesticides to crops through an irrigation system. |

| Crop Protection | Crop protection is a method of protecting crop yields from different pests, including insects, weeds, plant diseases, and others that cause damage to agricultural crops. |

| Seed Treatment | Seed treatment helps to disinfect seeds or seedlings from seed-borne or soil-borne pests. Crop protection chemicals, such as fungicides, insecticides, or nematicides, are commonly used for seed treatment. |

| Fumigation | Fumigation is the application of crop protection chemicals in gaseous form to control pests. |

| Bait | A bait is a food or other material used to lure a pest and kill it through various methods, including poisoning. |

| Contact Fungicide | Contact pesticides prevent crop contamination and combat fungal pathogens. They act on pests (fungi) only when they come in contact with the pests. |

| Systemic Fungicide | A systemic fungicide is a compound taken up by a plant and then translocated within the plant, thus protecting the plant from attack by pathogens. |

| Mass Drug Administration (MDA) | Mass drug administration is the strategy to control or eliminate many neglected tropical diseases. |

| Mollusks | Mollusks are pests that feed on crops, causing crop damage and yield loss. Mollusks include octopi, squid, snails, and slugs. |

| Pre-emergence Herbicide | Preemergence herbicides are a form of chemical weed control that prevents germinated weed seedlings from becoming established. |

| Post-emergence Herbicide | Postemergence herbicides are applied to the agricultural field to control weeds after emergence (germination) of seeds or seedlings. |

| Active Ingredients | Active ingredients are the chemicals in pesticide products that kill, control, or repel pests. |

| United States Department of Agriculture (USDA) | The Department of Agriculture provides leadership on food, agriculture, natural resources, and related issues. |

| Weed Science Society of America (WSSA) | The WSSA, a non-profit professional society, promotes research, education, and extension outreach activities related to weeds. |

| Suspension concentrate | Suspension concentrate (SC) is one of the formulations of crop protection chemicals with solid active ingredients dispersed in water. |

| Wettable powder | A wettable powder (WP) is a powder formulation that forms a suspension when mixed with water prior to spraying. |

| Emulsifiable concentrate | Emulsifiable concentrate (EC) is a concentrated liquid formulation of pesticide that needs to be diluted with water to create a spray solution. |

| Plant-parasitic nematodes | Parasitic Nematodes feed on the roots of crops, causing damage to the roots. These damages allow for easy plant infestation by soil-borne pathogens, which results in crop or yield loss. |

| Australian Weeds Strategy (AWS) | The Australian Weeds Strategy, owned by the Environment and Invasives Committee, provides national guidance on weed management. |

| Weed Science Society of Japan (WSSJ) | WSSJ aims to contribute to the prevention of weed damage and the utilization of weed value by providing the chance for research presentation and information exchange. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms