Vietnam Fungicide Market Size and Share

Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

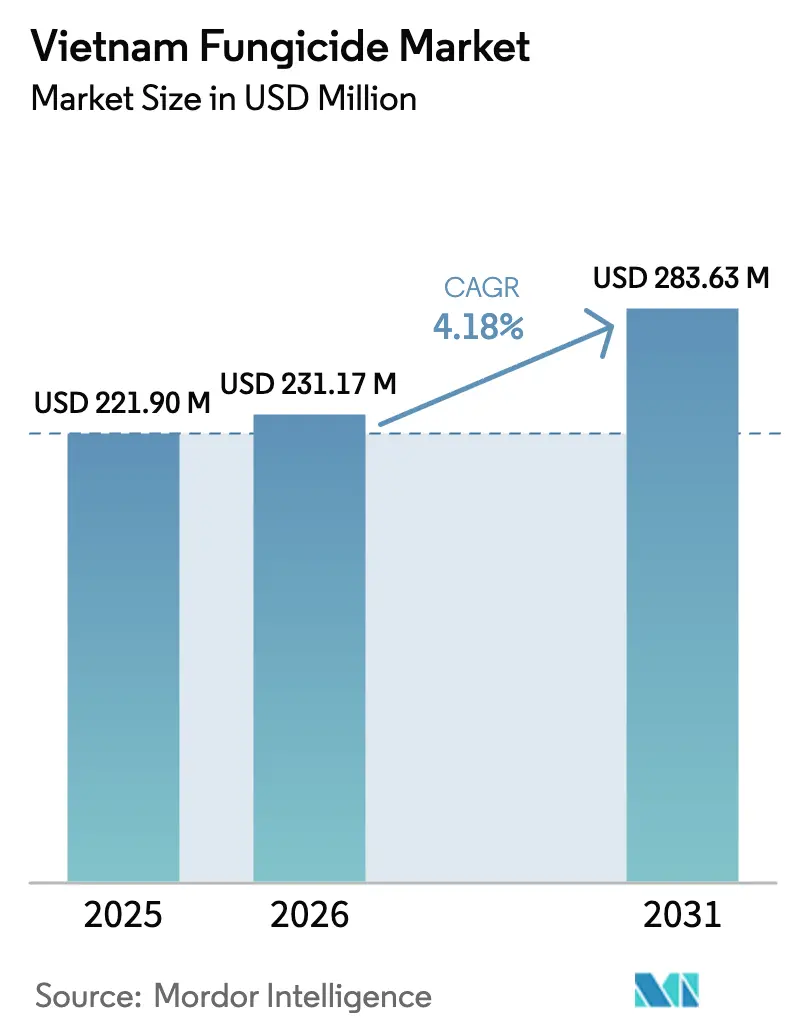

| Base Year Market Size (2025) | USD 221.9 Million |

| Market Size (2026) | USD 231.17 Million |

| Market Size (2031) | USD 283.63 Million |

| Growth Rate (2026 - 2031) | 4.18% CAGR |

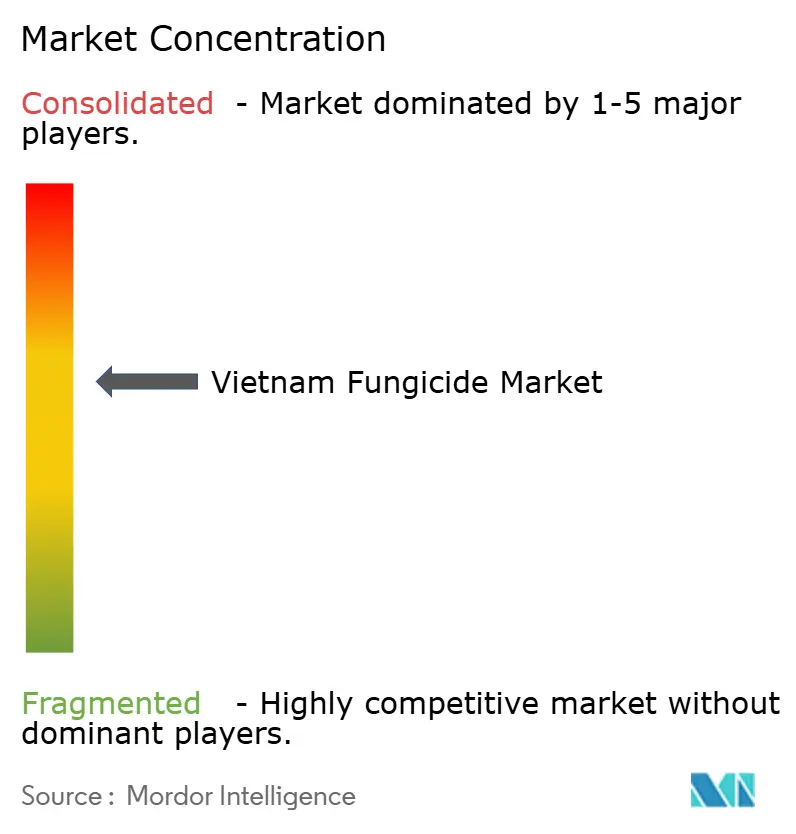

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Fungicide Market Analysis by Mordor Intelligence

The Vietnam fungicide market size in 2026 is estimated at USD 231.17 million, growing from 2025 value of USD 221.9 million with 2031 projections showing USD 283.63 million, growing at 4.18% CAGR over 2026-2031. Current growth reflects an export-oriented agriculture model, widening fungal disease pressure, and strong government incentives for modern chemistry. Climatic volatility is lengthening high-humidity periods, pushing growers to apply preventive and curative foliar sprays more often. Import dependence for nearly all active ingredients keeps supply chains vulnerable, yet it also creates opportunities for local formulation and contract manufacturing. New regulatory approvals allow 112 additional active ingredients, broadening resistance-management options and attracting multinational investments to Vietnam’s evolving crop-protection ecosystem.

Key Report Takeaways

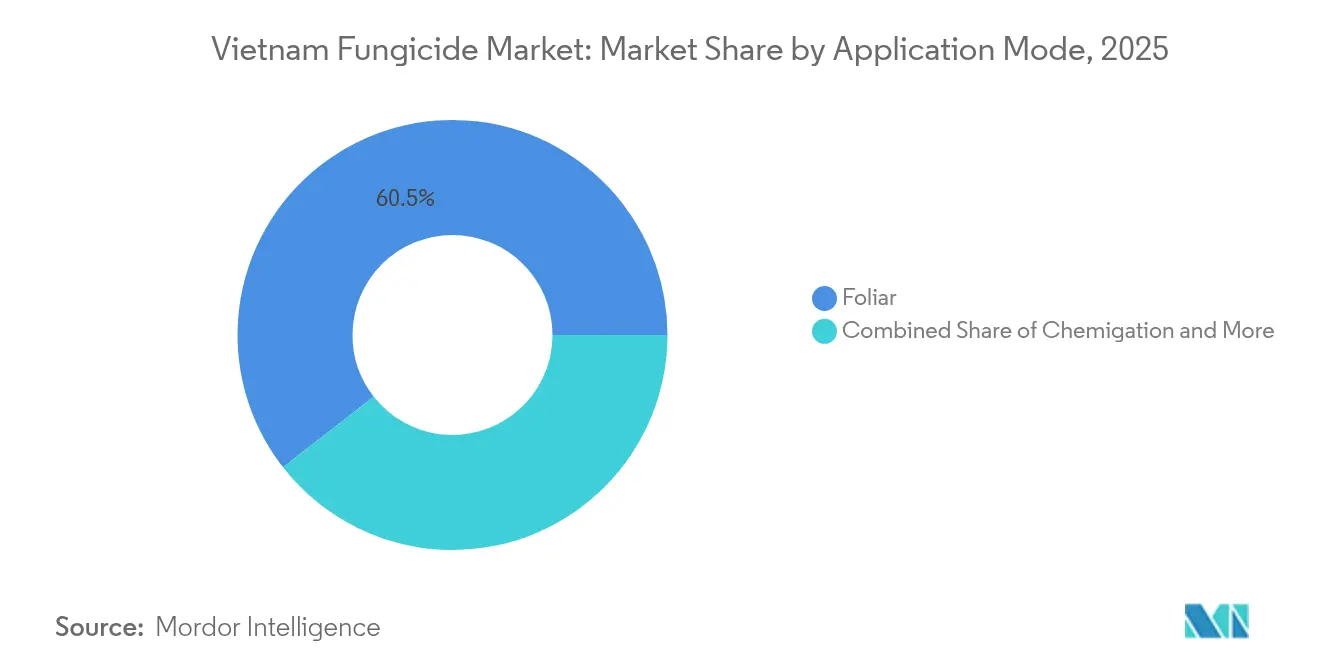

- By application mode, foliar treatments led with 60.55% revenue share in 2025, and are projected to record the fastest 4.30% CAGR through 2031.

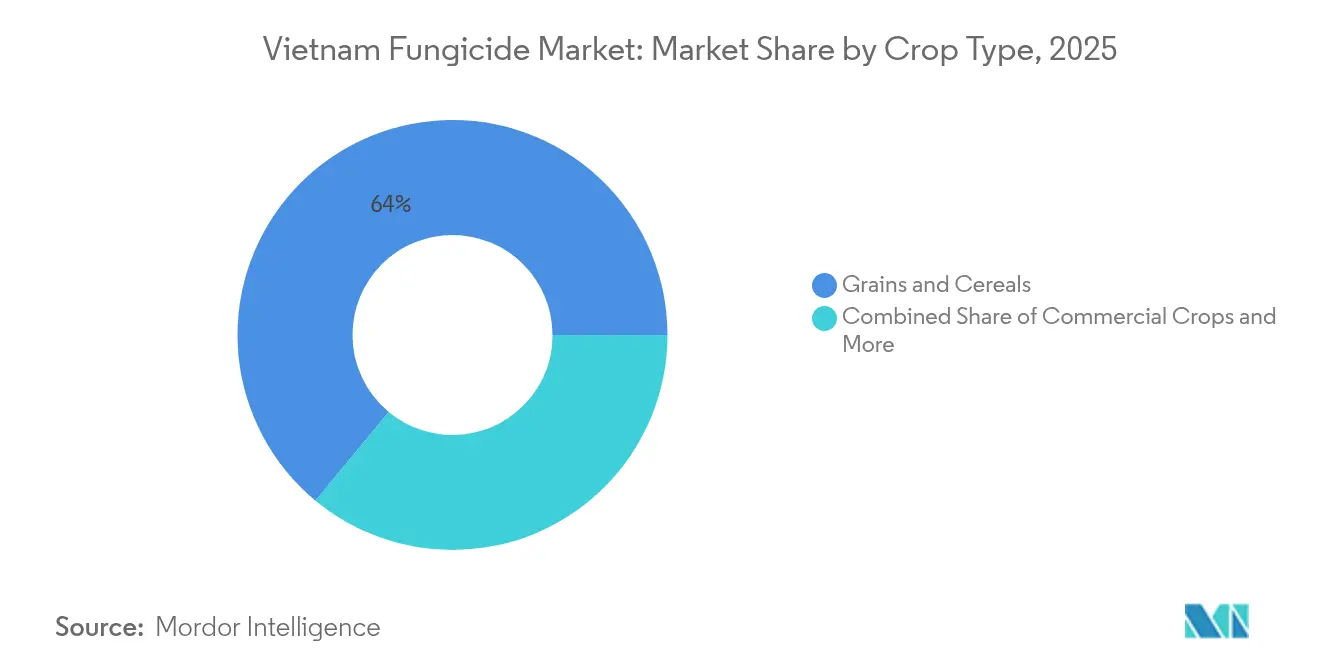

- By crop type, grains and cereals held 64.00% of the Vietnam fungicide market share in 2025; fruits and vegetables are projected to expand at a 4.40% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Vietnam Fungicide Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid expansion of high-value fruit and vegetable exports | +1.2% | Mekong Delta, Central Highlands, Northern provinces | Medium term (2-4 years) |

| Government incentives for modern fungicide formulations | +0.8% | National, with priority in export-focused regions | Short term (≤ 2 years) |

| Rising fungal resistance is driving product rotation | +0.7% | National, concentrated in intensive farming areas | Long term (≥ 4 years) |

| Growth in protected cultivation acreage | +0.6% | Northern provinces, urban periphery areas | Medium term (2-4 years) |

| Climate-change-linked spike in humidity-borne diseases | +0.9% | Mekong Delta, coastal provinces | Long term (≥ 4 years) |

| Cross-border supply chain shifts from China to Vietnam | +0.5% | Northern border provinces, industrial zones | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid expansion of high-value fruit and vegetable exports

Export earnings from fruits and vegetables reached USD 6.2 billion in 2024, with durian alone contributing USD 2.3 billion. International buyers enforce strict shelf-life and residue thresholds, prompting uptake of premium systemic fungicides that extend storage periods without breaching China’s GB 2763 or European Union limits[1]Source: Vietnam Fruit and Vegetable Association, “Export Performance Report 2024,” vinafruit.com. Dragon fruit shipments to China require documented fungicide protocols, pushing many cooperatives to adopt digital traceability. Central Highlands producers of coffee and pepper have begun trial programs using strobilurin and SDHI rotations to preserve specialty-grade status. Export bonuses offered by buyers further encourage compliance with prescribed spray schedules, reinforcing demand for advanced formulations in the Vietnam fungicide market.

Government incentives for modern fungicide formulations

The National Target Program budgeted VND 12.5 trillion (USD 500 million) through 2025, allocating roughly 15% for modern farm inputs, including low-dose, high-efficacy fungicides[2]Source: Ministry of Planning and Investment, “National Target Programs 2021-2025,” mpi.gov.vn. Decree 98/2020 doubles penalties on counterfeit products, encouraging distributors to shift toward reputable labels. Circular 03/2025 widened the approved active list, stimulating competitive launches of premix products that align with integrated pest-management guidance. Provincial subsidies cover up to 30% of certified fungicide costs for farmers adhering to complete field-record systems. These measures accelerate the penetration of next-generation products in the Vietnam fungicide market.

Rising fungal resistance driving product rotation

Surveys show a good share of Mekong Delta rice fields harbor Magnaporthe oryzae strains resistant to single-site triazoles. Adoption of rotation programs that include SDHI and QoI compounds has raised per-hectare spend. Collaboration among the International Rice Research Institute, local universities, and suppliers is producing rotating schedules that switch chemistry every two crop cycles. Retail outlets now stock smaller package sizes of premium actives to lower entry cost while maintaining rotation discipline. Increased laboratory testing capacity supports early detection of resistant biotypes, sustaining momentum in the Vietnam fungicide market.

Growth in protected cultivation acreage

Protected environments create unique disease pressure patterns, particularly for Botrytis cinerea and Sclerotinia sclerotiorum, requiring specialized fungicide application protocols that differ significantly from open-field programs. Enclosed environments foster Botrytis and Sclerotinia outbreaks that differ from open-field patterns. Capital subsidies and interest loans encourage investment in automated chemigation rigs, leading to precise dosing. Protected farms typically schedule fungicide sprays every 7–10 days, double the frequency of open-field vegetables. Advisory programs run by input suppliers provide data-driven application alerts, cementing a loyal customer base within the Vietnam fungicide market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent maximum residue limit compliance for export markets | -0.9% | Export-oriented regions, Mekong Delta | Short term (≤ 2 years) |

| Increasing consumer preference for low-chem residue foods | -0.6% | Urban-adjacent farming areas, premium crop zones | Medium term (2-4 years) |

| Illegal/parallel imports of cheaper generics | -0.4% | Border regions, rural distribution networks | Short term (≤ 2 years) |

| Labor shortage limiting on-field application windows | -0.3% | Rural provinces, labor-intensive crop areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent maximum residue limit compliance for export markets

China’s updated GB 2763 and the European Union’s regulation 396/2005 have lowered residue thresholds for several key actives. Export packers now routinely reject produce that tests above these limits, cascading financial penalties to growers. Compliance pushes farmers toward short-reentry, low-dose products that cost 15–20% more than traditional formulations. Larger exporters invest in on-site residue labs, while smallholders rely on extension centers for pre-harvest sampling. This dynamic elevates cost and complexity in the Vietnam fungicide market.

Increasing consumer preference for low-chem residue foods

Urban supermarkets market “clean and traceable” produce, often carrying certification seals that cap total chemical load. Growers supplying these channels must integrate biological or reduced-risk fungicides, which are priced at premiums. Marketing campaigns highlight residue-free claims, shaping buying behavior and pulling input choices upstream. The trend moderates volume growth but stimulates innovation in the Vietnam fungicide market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application Mode: Foliar applications lead disease management evolution

Foliar spraying accounted for 60.55% of sales in 2025, and the segment is forecast to record a 4.30% CAGR to 2031. High humidity accelerates leaf-surface infections, making contact and systemic foliar mixes indispensable. Remote-sensing drones and predictive models increase timing precision, reducing unnecessary passes and preserving efficacy. Chemigation of protected-crop treatments, with closed systems delivering droplet uniformity that supports residue compliance. Soil treatment holds a good share, largely within rice paddies. The Vietnam fungicide market size for seed treatment is projected to expand annually, steeper than the overall market, reflecting rising professional seed production standards. Meanwhile, foliar deliveries constitute the backbone of the Vietnam fungicide market, reinforcing the critical role of aerial and ground sprayers in disease suppression.

Foliar dominance aligns with the market’s need for swift curative action against outbreaks that materialize within 72 hours. Farmers often integrate preventives seven days before forecasted humidity spikes, then switch to systemic curatives if lesions appear. Precision-ag agriculture helps optimize droplet density, minimizing rebound drift and reducing total active ingredient per hectare by up to 20%. Such efficiency gains sustain the Vietnam fungicide market share of foliar products while opening pathways for premium pricing strategies linked to performance guarantees.

By Crop Type: Grains drive volume while fruits accelerate growth

Grains and cereals commanded a 64.00% share of the Vietnam fungicide market in 2025, mirroring rice’s dominance in planted area. Typical rice programs involve two to three fungicide rounds each cycle, targeting blast, brown spot, and sheath blight. Yield stability and export-grade quality requirements maintain volume demand despite moderate price sensitivity. The Vietnam fungicide market size for grains and cereals is forecast to move in line with flat production growth, resulting in low-single-digit value expansion.

Fruits and vegetables register the fastest 4.40% CAGR through 2031, due to widening export channels and domestic diet shifts toward fresh produce. Strawberry, durian, and dragon fruit farmers adopt low-preharvest interval chemistries to meet importer audits. Specialty arabica commands higher fungicide spend per hectare, supporting product premiumization in the Vietnam fungicide market. Pulses and oilseeds provide rotational diversity that may temper pathogen persistence. Turf and ornamental segments benefit from tourism and real-estate projects that demand visually flawless landscapes. Niche opportunities here include granular slow-release formulations for golf courses, further diversifying the Vietnam fungicide market.

Geography Analysis

Vietnam’s fungicide consumption shows regional concentration. The Mekong Delta represents a high share of national volume, driven by 2.5 million hectares of rice plus expanding tropical fruit acreage. Extended floodplain moisture favors Rhizoctonia and Pyricularia outbreaks, prompting prophylactic sprays at tillering and booting stages. Provincial authorities in Dong Thap and An Giang report average use of 3 kilograms of active ingredient per hectare, well above the national 2.1-kilogram figure. High trade connectivity through river ports enables just-in-time delivery, reinforcing Mekong Delta leadership within the Vietnam fungicide market.

Northern provinces are characterized by diversified crop rotations that include vegetables, tea, and emerging greenhouse clusters. Larger humidity swings and winter cold stress raise disease complexity, requiring both foliar and soil treatments. Hai Duong and Hung Yen show double-digit annual growth as protected cultivation scales up to meet cross-border demand. Collaborative extension services deliver residue-testing support, building trust with Chinese importers and enhancing the Vietnam fungicide market presence in these provinces.

Central regions, including the Central Highlands, account for the remaining share. Coffee and pepper plantations at higher altitudes face unique fungal challenges such as Phytophthora foot rot, necessitating targeted trunk drench and copper-oxychloride sprays. Mountainous transport corridors raise logistics costs, so suppliers offer consolidation centers that bundle fungicides with fertilizers. Coastal provinces integrate post-harvest fungigation to preserve quality during maritime shipping. Climate models indicate longer wet seasons, likely boosting per-hectare spray rounds and underpinning regional demand in the Vietnam fungicide market through 2031.

Competitive Landscape

The top five companies together control a good share of sales, indicating moderate concentration. Syngenta Group, UPL Limited, FMC Corporation, PI Industries, and Bayer AG emphasize science-backed formulations that comply with global residue laws, securing loyalty among export-oriented cooperatives. Corteva teams with local research institutes to embed fungicides into coffee and pepper integrated programs, bolstering foothold in the Central Highlands[3]Source: Corteva Vietnam, “Research Partnerships and Development,” corteva.com.vn. Summit Agro’s USD 12 million stake in Hop Tri extends distribution to 58 provinces, showcasing the importance of last-mile reach in the Vietnam fungicide market.

Competitive focus is shifting from single-product transactions to bundled solutions. Suppliers pair fungicides with biostimulants or micronutrients, offering season-long packages that smooth cash flow for growers. Digital advisory platforms deliver weather-linked spray alerts, creating service ecosystems that lock users into proprietary protocols. Demand for biological alternatives spurs launches such as Nufarm’s Bacillus-based product, appealing to residue-sensitive buyers yet still requiring integration with conventional chemistry. These dynamics foster innovation while preserving premium price corridors in the Vietnam fungicide market.

Regulatory openings under Circular 03/2025 attract mid-tier entrants from India and China, intensifying price competition in the generic azoxystrobin and propiconazole categories. Established players respond with stewardship campaigns that emphasize correct dosage and resistance management. The Ministry of Public Security’s crackdown on counterfeit networks in June 2024 reinforces the value propositions of authentic labels. Overall, strategic alliances, localized manufacturing, and precision-tech partnerships will define competitive advantage in the Vietnam fungicide market over the next five years.

Vietnam Fungicide Industry Leaders

Bayer AG

FMC Corporation

Syngenta Group

UPL Limited

PI Industries

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: PAN Group formed a strategic partnership with a Japanese biostimulant technology company, investing VND 450 billion (USD 18 million) to develop integrated crop protection solutions. The partnership focuses on combining fungicides with plant health enhancers for fruit and vegetable production targeted at export markets.

- January 2025: Syngenta introduced Orande 280SC fungicide in Vietnam, formulated for local crop production systems. The fungicide contains dual active ingredients that provide 85-90% control efficacy against fungal infections.

- November 2024: Summit Agro (Sumitomo Chemical) acquired a 49% stake in Hop Tri Investment Corporation for USD 12 million. This acquisition expanded the company's distribution network to 58 provinces across Vietnam, out of a total of 63 provinces, and strengthened its market position in the northern agricultural regions.

Vietnam Fungicide Market Report Scope

Chemigation, Foliar, Fumigation, Seed Treatment, Soil Treatment are covered as segments by Application Mode. Commercial Crops, Fruits & Vegetables, Grains & Cereals, Pulses & Oilseeds, Turf & Ornamental are covered as segments by Crop Type.| Chemigation |

| Foliar |

| Fumigation |

| Seed Treatment |

| Soil Treatment |

| Commercial Crops |

| Fruits & Vegetables |

| Grains & Cereals |

| Pulses & Oilseeds |

| Turf & Ornamental |

| Application Mode | Chemigation |

| Foliar | |

| Fumigation | |

| Seed Treatment | |

| Soil Treatment | |

| Crop Type | Commercial Crops |

| Fruits & Vegetables | |

| Grains & Cereals | |

| Pulses & Oilseeds | |

| Turf & Ornamental |

Market Definition

- Function - Fungicides are chemicals used to control or prevent fungi from damaging the crop and prevent yield loss.

- Application Mode - Foliar, Seed Treatment, Soil Treatment, Chemigation, and Fumigation are the different type of application modes through which crop protection chemicals are applied to the crops.

- Crop Type - This represents the consumption of crop protection chemicals by Cereals, Pulses, Oilseeds, Fruits, Vegetables, Turf, and Ornamental crops.

| Keyword | Definition |

|---|---|

| IWM | Integrated weed management (IWM) is an approach to incorporate multiple weed control techniques throughout the growing season to give producers the best opportunity to control problematic weeds. |

| Host | Hosts are the plants that form relationships with beneficial microorganisms and help them colonize. |

| Pathogen | A disease-causing organism. |

| Herbigation | Herbigation is an effective method of applying herbicides through irrigation systems. |

| Maximum residue levels (MRL) | Maximum Residue Limit (MRL) is the maximum allowed limit of pesticide residue in food or feed obtained from plants and animals. |

| IoT | The Internet of Things (IoT) is a network of interconnected devices that connect and exchange data with other IoT devices and the cloud. |

| Herbicide-tolerant varieties (HTVs) | Herbicide-tolerant varieties are plant species that have been genetically engineered to be resistant to herbicides used on crops. |

| Chemigation | Chemigation is a method of applying pesticides to crops through an irrigation system. |

| Crop Protection | Crop protection is a method of protecting crop yields from different pests, including insects, weeds, plant diseases, and others that cause damage to agricultural crops. |

| Seed Treatment | Seed treatment helps to disinfect seeds or seedlings from seed-borne or soil-borne pests. Crop protection chemicals, such as fungicides, insecticides, or nematicides, are commonly used for seed treatment. |

| Fumigation | Fumigation is the application of crop protection chemicals in gaseous form to control pests. |

| Bait | A bait is a food or other material used to lure a pest and kill it through various methods, including poisoning. |

| Contact Fungicide | Contact pesticides prevent crop contamination and combat fungal pathogens. They act on pests (fungi) only when they come in contact with the pests. |

| Systemic Fungicide | A systemic fungicide is a compound taken up by a plant and then translocated within the plant, thus protecting the plant from attack by pathogens. |

| Mass Drug Administration (MDA) | Mass drug administration is the strategy to control or eliminate many neglected tropical diseases. |

| Mollusks | Mollusks are pests that feed on crops, causing crop damage and yield loss. Mollusks include octopi, squid, snails, and slugs. |

| Pre-emergence Herbicide | Preemergence herbicides are a form of chemical weed control that prevents germinated weed seedlings from becoming established. |

| Post-emergence Herbicide | Postemergence herbicides are applied to the agricultural field to control weeds after emergence (germination) of seeds or seedlings. |

| Active Ingredients | Active ingredients are the chemicals in pesticide products that kill, control, or repel pests. |

| United States Department of Agriculture (USDA) | The Department of Agriculture provides leadership on food, agriculture, natural resources, and related issues. |

| Weed Science Society of America (WSSA) | The WSSA, a non-profit professional society, promotes research, education, and extension outreach activities related to weeds. |

| Suspension concentrate | Suspension concentrate (SC) is one of the formulations of crop protection chemicals with solid active ingredients dispersed in water. |

| Wettable powder | A wettable powder (WP) is a powder formulation that forms a suspension when mixed with water prior to spraying. |

| Emulsifiable concentrate | Emulsifiable concentrate (EC) is a concentrated liquid formulation of pesticide that needs to be diluted with water to create a spray solution. |

| Plant-parasitic nematodes | Parasitic Nematodes feed on the roots of crops, causing damage to the roots. These damages allow for easy plant infestation by soil-borne pathogens, which results in crop or yield loss. |

| Australian Weeds Strategy (AWS) | The Australian Weeds Strategy, owned by the Environment and Invasives Committee, provides national guidance on weed management. |

| Weed Science Society of Japan (WSSJ) | WSSJ aims to contribute to the prevention of weed damage and the utilization of weed value by providing the chance for research presentation and information exchange. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms