Schistosomiasis Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

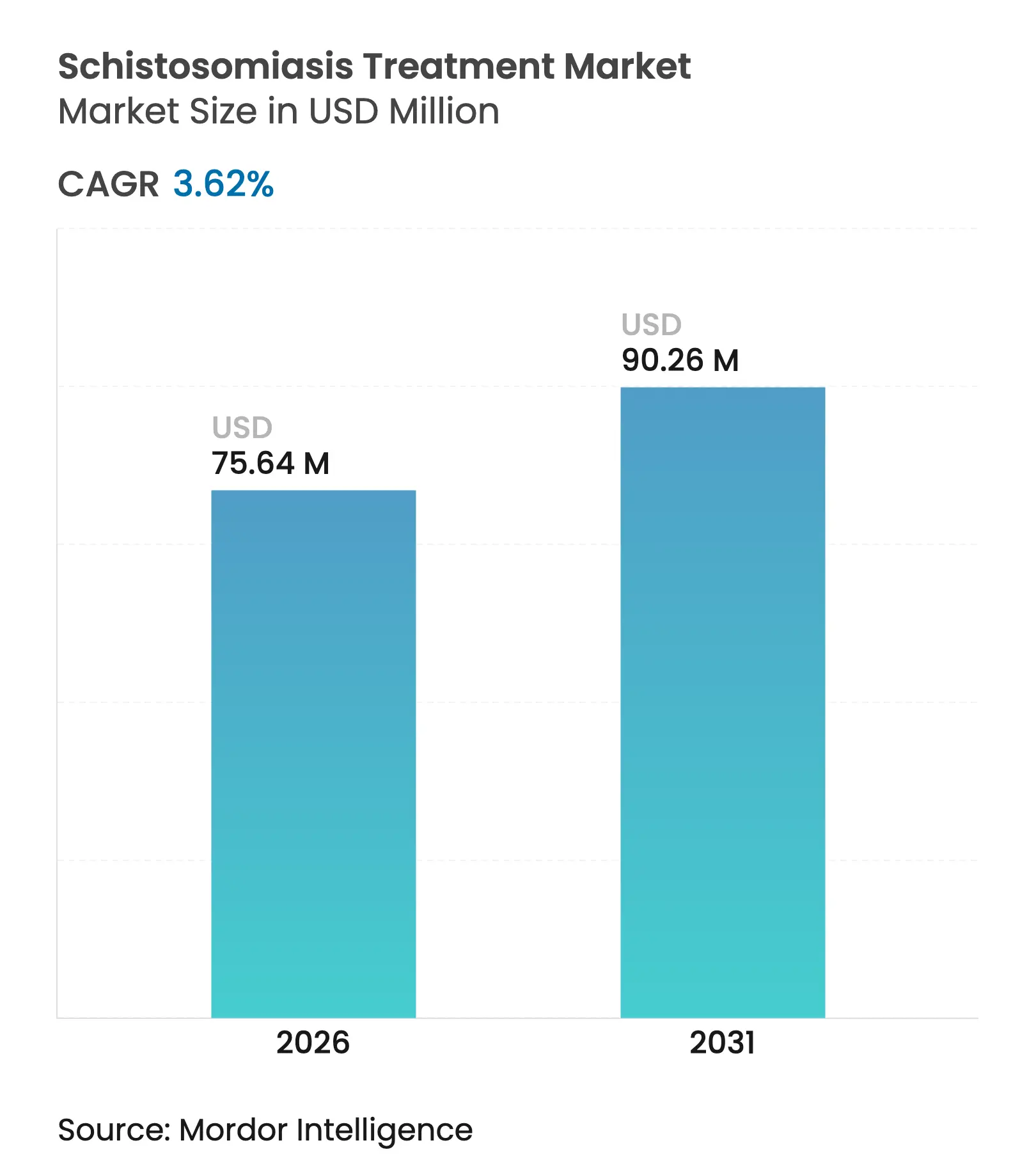

| Market Size (2026) | USD 75.64 Million |

| Market Size (2031) | USD 90.26 Million |

| Growth Rate (2026 - 2031) | 3.62 % CAGR |

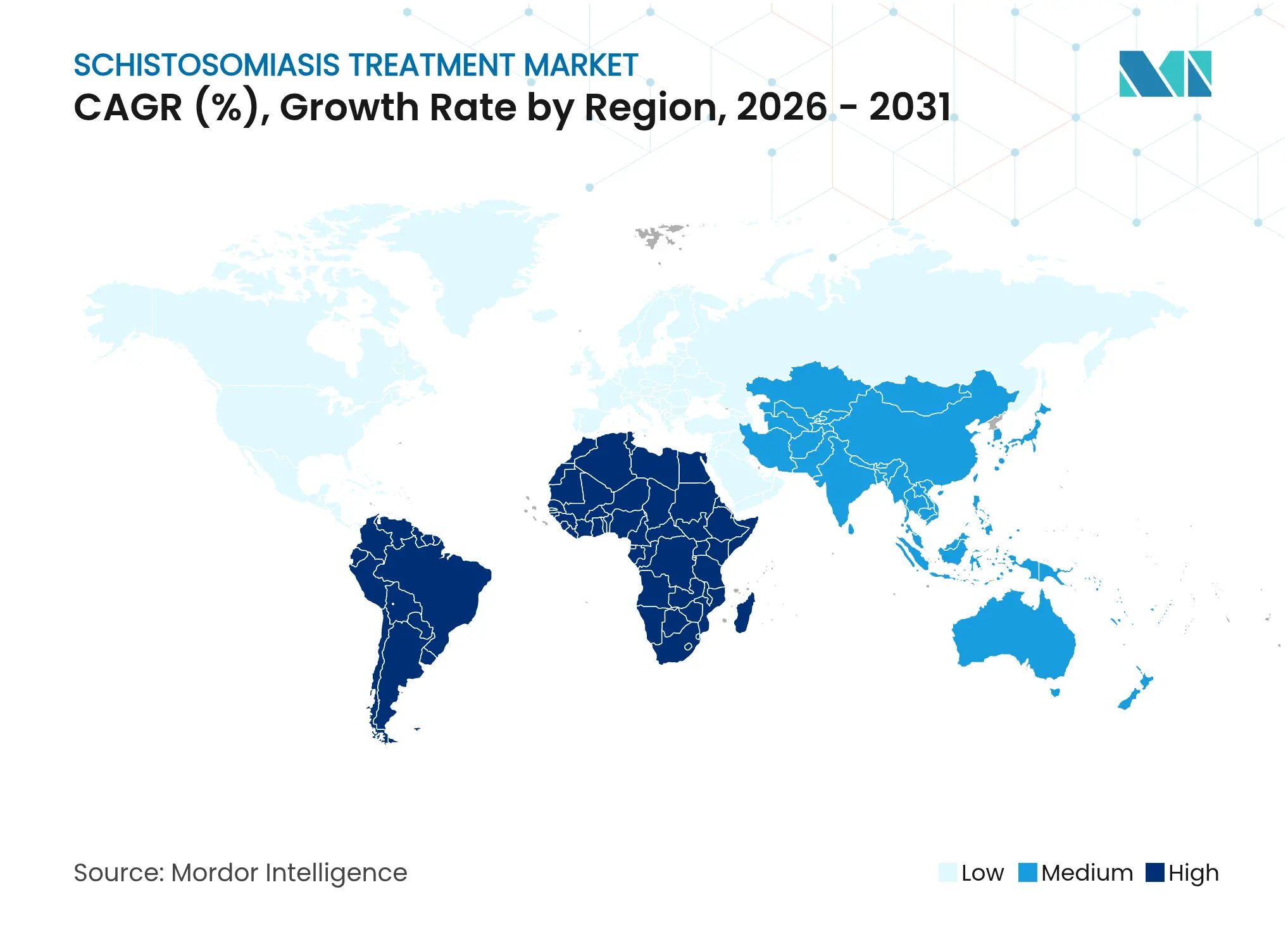

| Fastest Growing Market | Middle East and Africa |

| Largest Market | South America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Schistosomiasis Treatment Market Analysis by Mordor Intelligence

The schistosomiasis treatment market size was valued at USD 73 million in 2025 and estimated to grow from USD 75.64 million in 2026 to reach USD 90.26 million by 2031, at a CAGR of 3.62% during the forecast period (2026-2031). This steady climb is tied to World Health Organization (WHO) elimination targets, broader access to child-friendly medicines and sustained donation programs that keep product volumes high despite narrow commercial margins. Intensified community-wide mass-drug-administration (MDA) campaigns are increasing annual consumption volumes, while arpraziquantel’s pediatric orodispersible tablet (ODT) is opening an untapped preschool segment that once lacked age-appropriate therapy. Alongside this demand uplift, supply shocks from active pharmaceutical ingredient (API) shortages are prompting multisource procurement strategies, and digital platforms are improving stock visibility at sub-national level. Competitive differentiation is shifting away from sheer tablet counts toward formulation innovation, local manufacturing footprints and end-to-end pharmacovigilance capabilities.

Key Report Takeaways

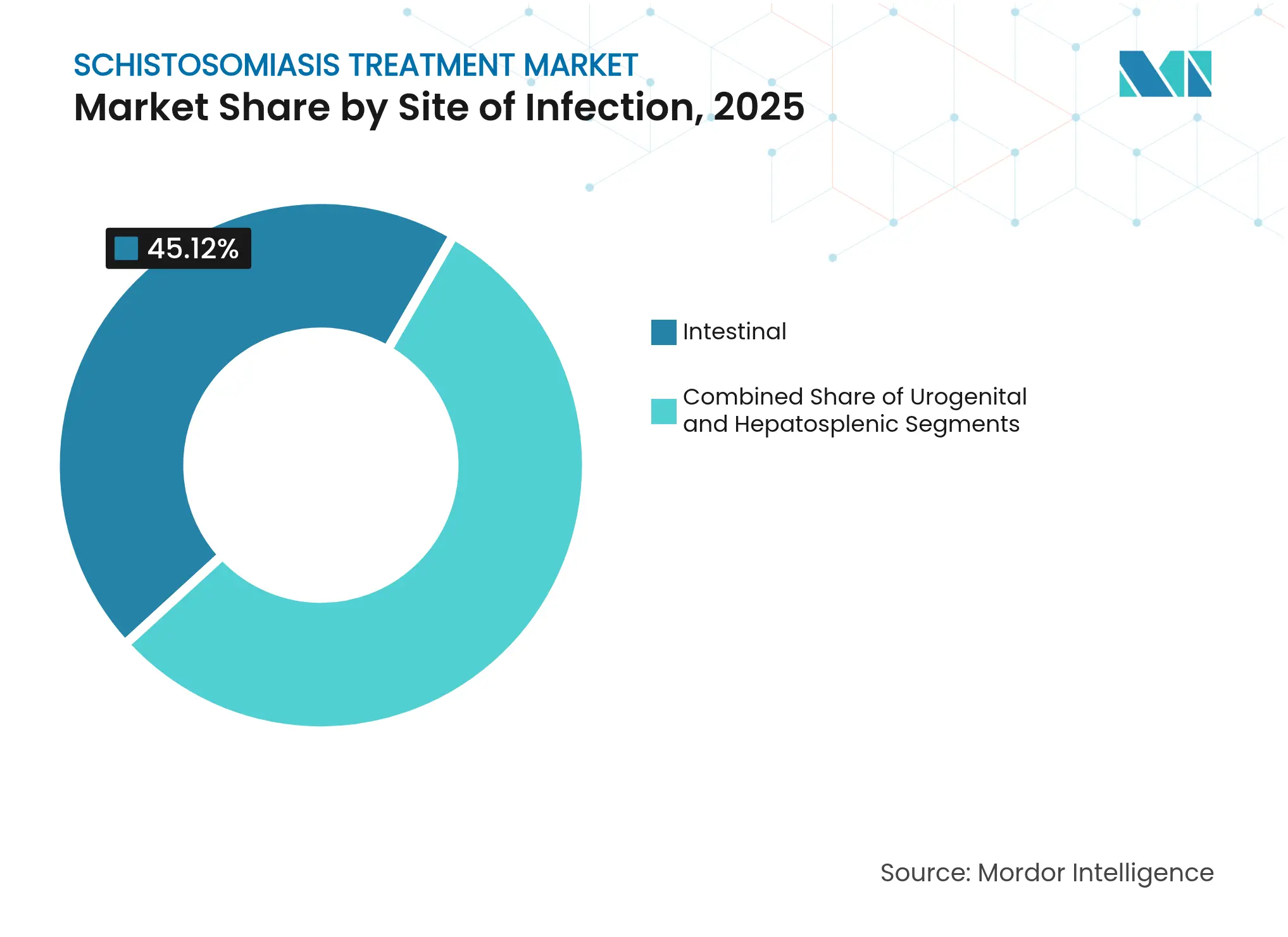

- By site of infection, intestinal presentations led with 45.12% revenue share in 2025; hepatosplenic complications are projected to expand at a 7.22% CAGR to 2031.

- By species, Schistosoma mansoni accounted for 43.07% of the schistosomiasis treatment market share in 2025, while S. japonicum therapies are set to grow at 7.43% CAGR on the back of China’s precision elimination drive.

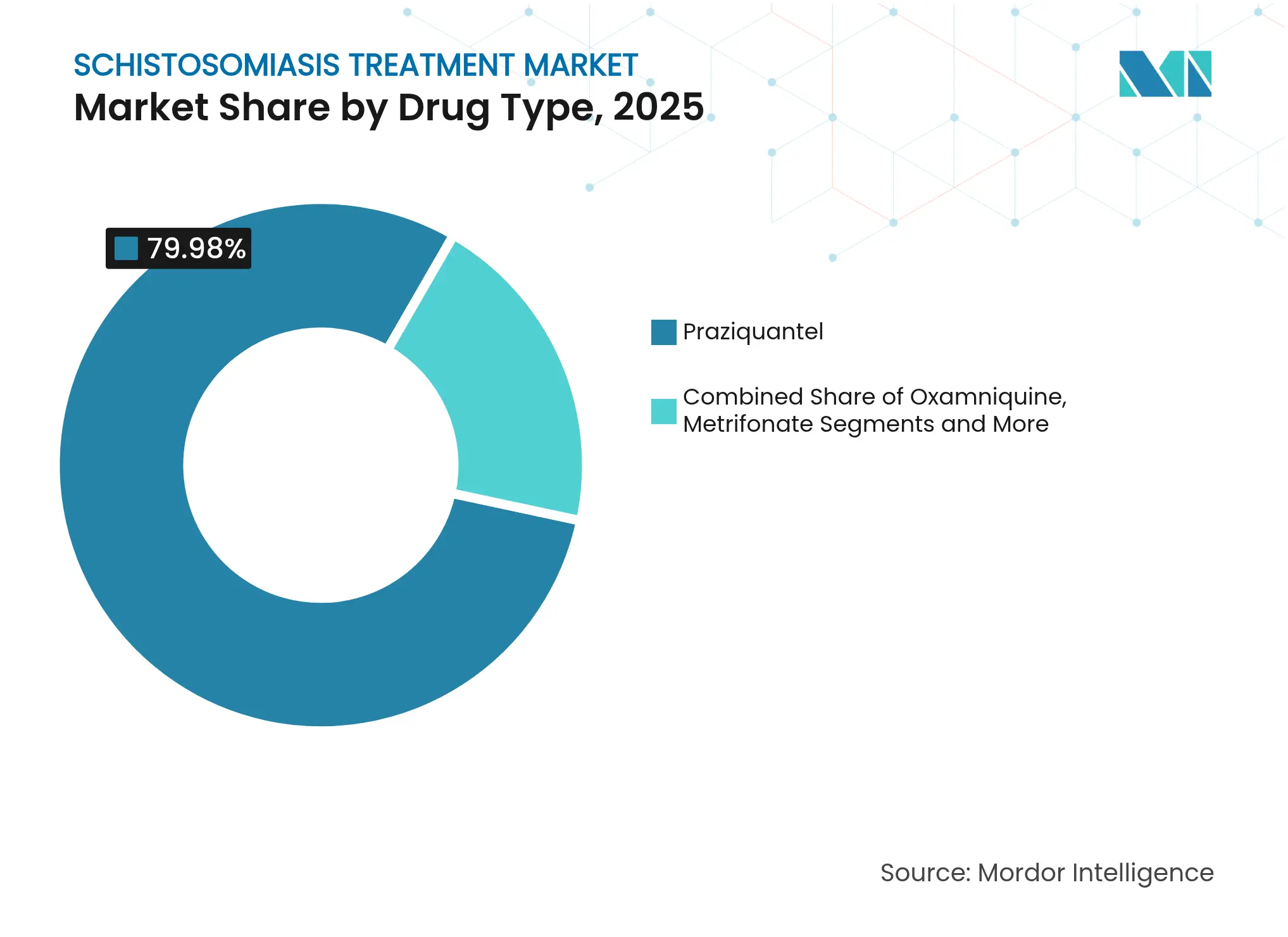

- By drug type, praziquantel held 79.98% of the schistosomiasis treatment market size in 2025; the arpraziquantel ODT is advancing at 12.09% CAGR to 2031 following WHO prequalification.

- By end user, hospitals captured 56.62% share of the schistosomiasis treatment market in 2025, yet community health-worker channels are forecast to post an 8.12% CAGR as decentralized delivery gains ground.

- By geography, the Middle East and Africa commanded 59.55% of 2025 revenue; South America is on track for the fastest 6.07% CAGR through 2031 thanks to Brazil’s expanded surveillance network.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Schistosomiasis Treatment Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Intensified Mass-Drug-Administration (MDA) Targets By WHO

For 2025-30

Intensified Mass-Drug-Administration (MDA) Targets By WHO

For 2025-30

| +1.2% | Global, with primary focus on Sub-Saharan Africa and endemic regions | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

+1.2%

| Geographic Relevance:

Global, with primary focus on Sub-Saharan Africa and

endemic regions

| Impact Timeline:

Medium term (2-4 years)

|

Growing Pipeline Of Arpraziquantel & Paediatric ODT

Formulations

Growing Pipeline Of Arpraziquantel & Paediatric ODT

Formulations

| +0.8% | Global, with early adoption in Côte d'Ivoire, Kenya, Uganda | Short term (≤ 2 years) | |||

Government-Backed Praziquantel Donation Programmes

Expanding To Adults

Government-Backed Praziquantel Donation Programmes

Expanding To Adults

| +0.6% | Sub-Saharan Africa, Middle East, South America | Medium term (2-4 years) | |||

AI-Enabled Repurposing Of Nifuroxazide & Other

Antibiotics

AI-Enabled Repurposing Of Nifuroxazide & Other

Antibiotics

| +0.4% | Global, with research centers in developed markets | Long term (≥ 4 years) | |||

Nanoparticle-Based Combination Therapies Showing >90%

Cure In Vitro

Nanoparticle-Based Combination Therapies Showing >90%

Cure In Vitro

| +0.3% | Global, with clinical trials in endemic regions | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Intensified Community-Wide MDA Targets

WHO’s 2025-30 roadmap calls for treating every person aged 2 years and above when community prevalence exceeds 10%. This change broadens the eligible cohort beyond schoolchildren and addresses adults who sustain transmission reservoirs[1]Pediatric Praziquantel Consortium, “New WHO Guidelines for Schistosomiasis,” pediatricpraziquantelconsortium.org. Tanzania’s three-round campaign cut prevalence from 30.4% to 9.5% in under three years, underscoring the efficacy of high-coverage regimens. Wider coverage immediately boosts praziquantel demand and stresses supply logistics. National programs must now track migrant workers, fishermen and other mobile groups, requiring flexible delivery windows and mobile health teams. Implementation success hinges on reliable tablet forecasting, robust community engagement and adherence monitoring technologies.

Arpraziquantel and Other Pediatric ODT Launches

The EMA’s 2024 positive scientific opinion and WHO prequalification of arpraziquantel allows procurement for children aged 3 months to 6 years, closing a long-standing therapeutic gap for about 24 million preschoolers in Africa[2]European Medicines Agency, “Arpraziquantel Opinion,” ema.europa.eu. Clinical trials posted cure rates of 88% for S. mansoni and 86% for S. haematobium, matching adult therapy outcomes while improving palatability. The not-for-profit consortium behind the product has negotiated technology transfer to Brazil’s Farmanguinhos, ensuring regional supply security and cost-plus pricing. Pilot ADOPT deployments in Côte d’Ivoire, Kenya and Uganda are demonstrating integration with routine immunization visits, a model likely to accelerate elimination timelines once scaled.

Expansion of Praziquantel Donations to Adults

Merck now supplies 250 million tablets annually for free, and national programs such as Ethiopia’s 2030 elimination plan have formally added adults to treatment schedules. Adult inclusion raises per-round volume needs by up to 40% in some districts and demands workplace distribution to reach farmers and fishermen. Storytelling campaigns that highlight occupational risks help drive uptake, while Johnson & Johnson’s extension of the VERMOX donation for soil-transmitted helminths supports integrated community deworming. Sustainability depends on proving transmission interruption and maintaining donor enthusiasm despite plateauing prevalence.

Nanoparticle-Based Combination Therapies

Chitosan-based nanoparticles loaded with praziquantel plus plant-derived compounds have shown >90% cure rates in cultured parasites, suggesting lower dosing and possibly less resistance selection pressure. Early-phase studies also report improved bioavailability and reduced dosing frequency, addressing compliance barriers in adults. While clinical translation remains several years away, national control programs are watching closely as combination regimens could offer fallback options should resistance expand.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Emerging Regional Pockets Of Praziquantel

Tolerance/Resistance

Emerging Regional Pockets Of Praziquantel

Tolerance/Resistance

| -0.9% | Sub-Saharan Africa, particularly high-transmission areas | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

-0.9%

| Geographic Relevance:

Sub-Saharan Africa, particularly high-transmission areas

| Impact Timeline:

Medium term (2-4 years)

|

Supply Bottlenecks For GMP-Grade Praziquantel API

Supply Bottlenecks For GMP-Grade Praziquantel API

| -0.7% | Global, with acute impact in Sub-Saharan Africa | Short term (≤ 2 years) | |||

Low Compliance Of At-Risk Adults In Community MDA

Campaigns

Low Compliance Of At-Risk Adults In Community MDA

Campaigns

| -0.5% | Rural endemic areas globally, especially agricultural communities | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Emerging Pockets of Praziquantel Tolerance

Meta-analysis covering East Africa reported cure-rate variability from 97.9% in Rwanda down to 68.4% in Uganda, flagging possible tolerance clusters. Laboratory studies have induced resistant parasite strains, and molecular surveillance is rolling out to detect field mutations. Resistance, if unchecked, could derail elimination objectives because praziquantel is the single widely available anti-schistosomal agent. Control programs are adopting sentinel efficacy monitoring and exploring rotational therapy models with oxamniquine, though cost and supply hurdles remain.

Supply Bottlenecks for GMP-Grade Praziquantel API

The National Institute for Communicable Diseases signaled shortages through April 2025 after a key supplier halted output for upgrades[3]National Institute for Communicable Diseases, “Praziquantel Supply Update,” nicd.ac.za. Fewer than five manufacturers account for most global API production, concentrating risk. China’s national drug shortage report identified essential parasitic medicines among the 0.41% of compounds in deficit, amplifying pressure on importers. Donor initiatives now require dual-sourcing strategies, and Western governments are co-funding advanced flow-chemistry plants to reshore critical API.

Segment Analysis

By Site of Infection: Chronic Liver Damage Lifts Revenue

The hepatosplenic sub-segment contributes lower patient counts yet higher per-case value because therapy often involves extended monitoring, ultrasound follow-up and repeat dosing. It is forecast to expand at 7.22% CAGR through 2031, outpacing the overall schistosomiasis treatment market. The schistosomiasis treatment market size for hepatosplenic cases is projected to reach USD 22.18 million by 2031, reflecting the cumulative burden of untreated chronic infections.

Advanced ultrasound staging and environmental DNA mapping reveal more hidden fibrosis than once thought, especially in long-standing endemic zones of Brazil and Egypt. These insights drive targeted treatment campaigns that blend praziquantel and anti-inflammatory care. Longer hospitalization periods and follow-up scans boost hospital revenue despite donors covering drug costs. Demand for portable point-of-care diagnostics is also growing as field teams screen lakeside communities for early portal hypertension signs.

Note: Segment shares of all individual segments available upon report purchase

By Species Type: Zoonotic Cycle Complicates Control

Schistosoma mansoni remains the largest contributor with 43.07% of schistosomiasis treatment market share in 2025. Yet Schistosoma japonicum therapies are expanding at 7.43% CAGR as China finishes transmission-interruption activities and shifts to precision surveillance of residual foci. The schistosomiasis treatment market size for japonicum infections is expected to reach USD 12.72 million in 2031.

Precision detection hinges on loop-mediated isothermal amplification assays that track infections in cattle, dogs and rodents. One-Health coordination raises program costs but promises definitive elimination, which in turn lowers long-term drug volume. Cross-border spillover from the Philippines and Indonesia remains a threat, keeping demand for treatment stockpiles alive. Hybrid schistosome forms emerging in West Africa also require species-specific dosing algorithms, pushing research into combination therapies.

By Drug Type: Pediatric ODT Reshapes Formulation Mix

Praziquantel dominated 2025 with 79.98% share, driven by high-volume donations. The arpraziquantel ODT is the fastest-growing line at 12.09% CAGR thanks to child-focused formulation and temperature-stable packaging. The schistosomiasis treatment market size for arpraziquantel alone is set to surpass USD 6.36 million by 2031, still small yet strategically vital because it unlocks a previously untreatable cohort.

Oxamniquine and metrifonate retain niche roles for S. mansoni and S. haematobium resistance cases. Nanoparticle carriers are moving through pre-clinical pipelines, aiming to combine praziquantel with antioxidant extracts and reduce dose frequency. AI-guided repurposing of nifuroxazide derivatives offers another fallback as resistance risk escalates. Successful commercial launch will depend on simplified regulatory pathways for neglected tropical disease (NTD) drugs that WHO is now piloting.

Note: Segment shares of all individual segments available upon report purchase

By End User: Community Channels Drive Last-Mile Reach

Hospitals held 56.62% of 2025 revenue because severe hepatosplenic complications still require inpatient care and imaging. However, community health-worker programs are on an 8.12% CAGR trajectory, supported by digital stock-tracking tools and integration with water, sanitation and hygiene (WASH) education. The schistosomiasis treatment market size handled by community channels could approach USD 19.05 million by 2031.

Mobile phone-based supervision models allow district pharmacists to audit treatment logs remotely, increasing accountability. Coupled with local storytelling campaigns, these platforms boost adult compliance above 70% in pilot zones, compared with 55% under hospital-centric delivery. Donors now earmark funds for solar-powered cold boxes that safeguard pediatric ODT stability during outreach.

Geography Analysis

The Middle East and Africa remain the epicenter, generating 59.55% of sales in 2025 through vast donation-funded volumes. Nigeria, Tanzania and Ethiopia continue to absorb most tablets due to high prevalence pockets. Yet operating conditions are challenging where insecurity hampers field access.

South America is the fastest climber, with a 6.07% CAGR expected through 2031 as Brazil scales precision surveillance using environmental DNA traps along the São Francisco River. Brazil’s model blends livestock treatment and snail habitat modification, lowering reinfection rates below 2% in pilot municipalities. Neighbouring Bolivia and Venezuela are adopting similar protocols, lifting regional demand for combination therapy trials.

Asia-Pacific shows mixed dynamics. China recorded zero indigenous cases in 2023 but still budgets for contingency stockpiles and livestock programs. Meanwhile, India is mapping water bodies for snail clusters and could emerge as a significant buyer of pediatric ODT once regulatory alignment is achieved. Import markets in North America and Europe stay niche, supplying hospitals that treat migrant or travel-related cases and that conduct early-phase drug trials.

Competitive Landscape

Market Concentration

The arena is moderately fragmented. Merck KGaA remains the anchor producer through its 250 million-tablet annual donation, securing preferential WHO procurement slots and regional warehouse networks. Farmanguinhos has gained prominence as it manufactures arpraziquantel for South America under technology transfer.

New entrants focus on formulation differentiation. Start-ups partner with universities to engineer nanoparticle carriers or fixed-dose combinations that tackle early resistance signals. AI-driven repurposing companies license in-silico hits to bigger pharma for clinical validation, compressing discovery timelines from a decade to under five years.

Strategic moves lean on trilateral partnerships among donors, NGOs and manufacturers. Merck’s 2024 storytelling initiative engages local media to raise adult compliance. Johnson & Johnson extended its VERMOX helminth donation, signalling appetite for integrated NTD portfolios. Western API producers are leveraging government incentives to reshore production and undercut supply-risk premiums once borne by African health ministries.

Schistosomiasis Treatment Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2024: WHO added arpraziquantel ODT to its Prequalified Medicines list, paving the way for large-scale UNICEF procurement.

- February 2024: EMA issued a positive scientific opinion on arpraziquantel for children aged 3 months to 6 years.

Table of Contents for Schistosomiasis Treatment Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Intensified Mass-Drug-Administration (MDA) Targets By WHO For 2025-30

- 4.2.2Growing Pipeline Of Arpraziquantel & Paediatric ODT Formulations

- 4.2.3Government-Backed Praziquantel Donation Programmes Expanding To Adults

- 4.2.4AI-Enabled Repurposing Of Nifuroxazide & Other Antibiotics

- 4.2.5Nanoparticle-Based Combination Therapies Showing >90 % Cure In Vitro

- 4.3Market Restraints

- 4.3.1Emerging Regional Pockets Of Praziquantel Tolerance/Resistance

- 4.3.2Supply Bottlenecks For GMP-Grade Praziquantel API

- 4.3.3Low Compliance Of At-Risk Adults In Community MDA Campaigns

- 4.4Porter's Five Forces

- 4.4.1Threat of New Entrants

- 4.4.2Bargaining Power of Buyers

- 4.4.3Bargaining Power of Suppliers

- 4.4.4Threat of Substitutes

- 4.4.5Competitive Rivalry

5. Market Size & Growth Forecasts (Value, USD)

- 5.1By Site of Infection

- 5.1.1Intestinal

- 5.1.2Urogenital

- 5.1.3Hepatosplenic

- 5.2By Species Type

- 5.2.1Schistosoma mansoni

- 5.2.2Schistosoma japonicum

- 5.2.3Others

- 5.3By Drug Type

- 5.3.1Praziquantel

- 5.3.2Arpraziquantel (ODT)

- 5.3.3Oxamniquine

- 5.3.4Metrifonate

- 5.3.5Emerging Repurposed Drugs

- 5.4By End User

- 5.4.1Hospitals

- 5.4.2Specialty & Tropical-disease Centres

- 5.4.3Home-care & Community Health Workers

- 5.4.4Others

- 5.5Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Rest of Europe

- 5.5.3Asia-Pacific

- 5.5.3.1China

- 5.5.3.2Japan

- 5.5.3.3India

- 5.5.3.4South Korea

- 5.5.3.5Australia

- 5.5.3.6Rest of Asia-Pacific

- 5.5.4Middle East and Africa

- 5.5.4.1GCC

- 5.5.4.2South Africa

- 5.5.4.3Rest of Middle East and Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Merck KGaA

- 6.3.2Bayer AG

- 6.3.3Shin Poong Pharmaceutical Co.

- 6.3.4Egyptian International Pharmaceutical Industries Co. (EIPICO)

- 6.3.5GSK plc

- 6.3.6Taj Pharmaceuticals Ltd

- 6.3.7Endo International plc (Par)

- 6.3.8Salvensis Ltd

- 6.3.9Wellona Pharma

- 6.3.10Cipla Ltd

- 6.3.11Lupin Ltd

- 6.3.12Ipca Laboratories Ltd

- 6.3.13Daiichi Sankyo Co.

- 6.3.14Johnson & Johnson (Janssen)

- 6.3.15Pfizer Inc.

- 6.3.16Novartis AG

- 6.3.17Sanofi SA

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Global Schistosomiasis Treatment Market Report Scope

Schistosomiasis treatment involves the use of medications, like praziquantel, to kill the parasitic worms (schistosomes) that cause the disease. The treatment aims to eliminate or reduce the number of schistosomes in the body, to relieve symptoms, to prevent complications, and to reduce transmission.

The schistosomiasis treatment market is segmented by site of infection, species type, drug type, end user, and geography. By site of infection, the market is further segmented into the intestinal, urogenital, and hepatosplenic. The species type segment is further segmented into Schistosoma mansoni, Schistosoma japonicum, and others. The drug type segment is further segmented into praziquantel, metrifonate, biltricide, oxamniquine, and others. The end-user segment is segmented into hospitals, home care, and specialty centers. The geography segment is further segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (USD) for all the above segments.