Scleroderma Therapeutics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

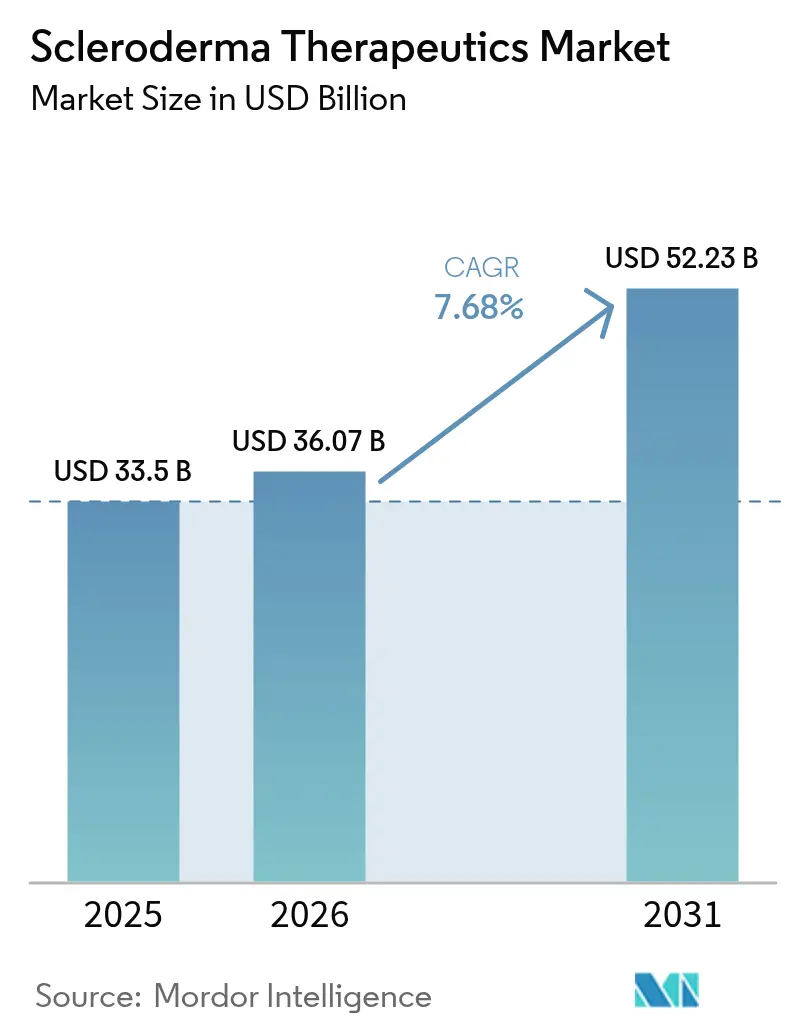

| Market Size (2026) | USD 36.07 Billion |

| Market Size (2031) | USD 52.23 Billion |

| Growth Rate (2026 - 2031) | 7.68% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Scleroderma Therapeutics Market Analysis by Mordor Intelligence

The scleroderma therapeutics market size in 2026 is estimated at USD 36.07 billion, growing from 2025 value of USD 33.50 billion with 2031 projections showing USD 52.23 billion, growing at 7.68% CAGR over 2026-2031. Momentum comes from accelerated regulatory pathways, breakthrough cell and gene therapies, and biomarker-guided treatment algorithms that shift the therapeutic focus from symptom relief toward disease modification[1]U.S. Food & Drug Administration, “Rare Diseases: Orphan Drug Program,” fda.gov. Expanded orphan-drug incentives, earlier diagnosis, and rising specialist awareness further sustain demand, while investment flows into precision medicine platforms deepen pipeline diversity. Manufacturers balance patent-expiry headwinds by advancing next-generation compounds such as nerandomilast, and payers increasingly link reimbursement to quality-adjusted life-year gains. Intensifying competition among traditional immunosuppressants and emerging cell therapies fosters strategic licensing agreements, encouraging global expansion, particularly in Asia-Pacific. Despite high therapy costs and complex trial designs, the market outlook remains positive as stakeholder collaboration improves patient access frameworks.

Key Report Takeaways

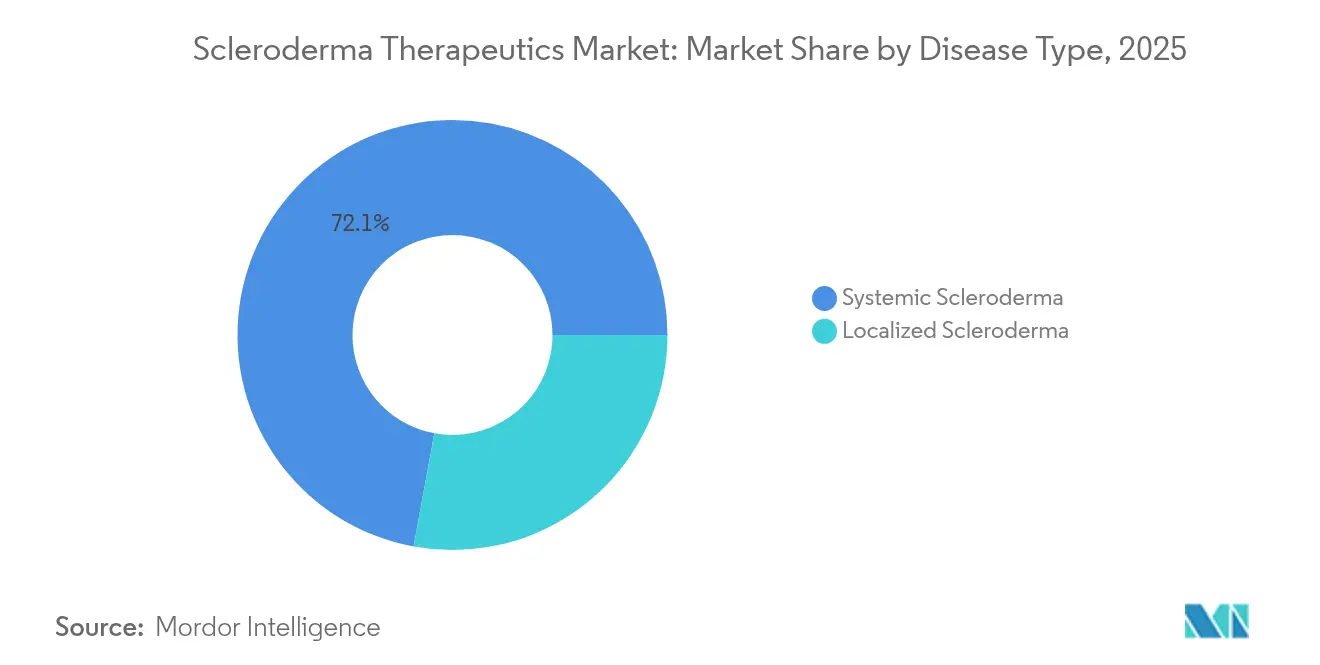

- By disease type, systemic scleroderma held 72.10% of the scleroderma therapeutics market share in 2025; localized scleroderma is forecast to expand at an 8.35% CAGR through 2031.

- By drug class, endothelin receptor antagonists led with 28.10% revenue share in 2025, while cell and gene therapies are projected to grow at 8.78% CAGR to 2031.

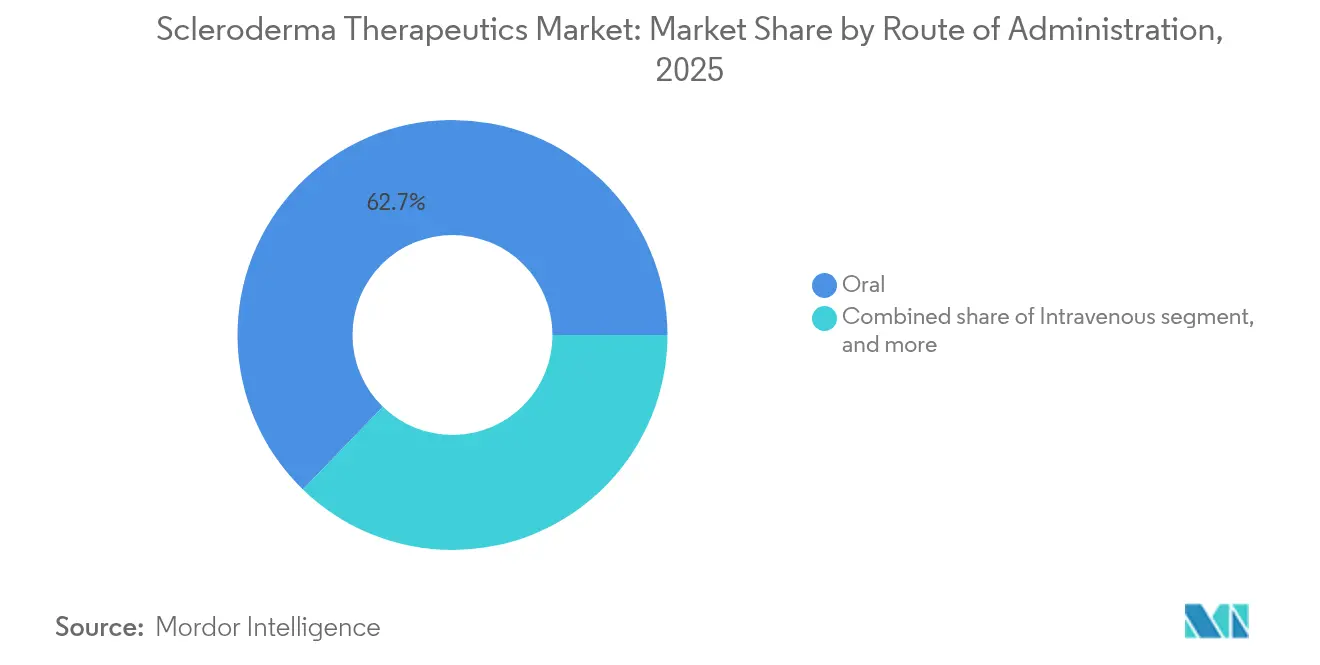

- By route of administration, oral therapies commanded 62.75% share of the scleroderma therapeutics market size in 2025; intravenous delivery is advancing at a 9.95% CAGR through 2031.

- By distribution channel, hospital pharmacies accounted for 45.60% of the scleroderma therapeutics market size in 2025; retail pharmacies record the highest projected CAGR at 10.2% to 2031.

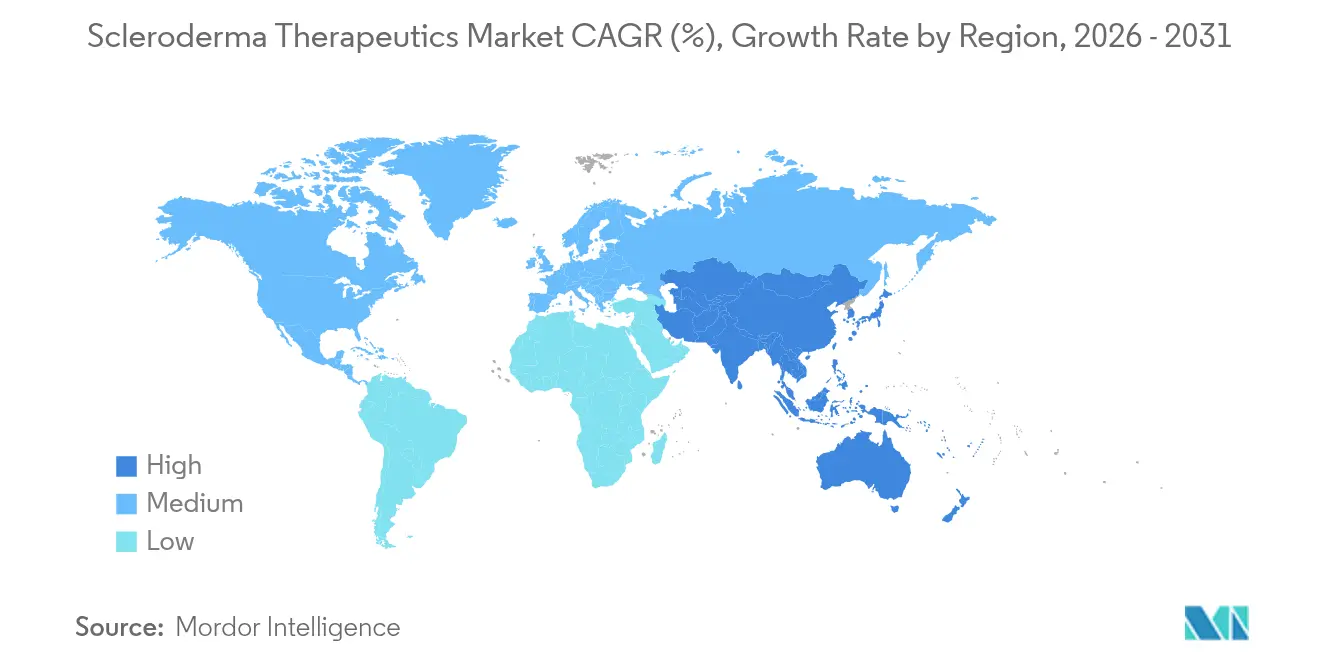

- By geography, North America dominated with 44.20% share in 2025, whereas Asia-Pacific is the fastest-growing region at an 8.45% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Scleroderma Therapeutics Market*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing disease burden and unmet clinical needs | +1.8% | Global, highest in North America and Europe | Long term (≥ 4 years) |

| Expansion of targeted and disease-modifying treatment options | +2.1% | Global; early adoption in North America, EU, Japan | Medium term (2-4 years) |

| Favorable orphan-drug designations and reimbursement frameworks | +1.4% | North America and EU; expanding in Asia-Pacific | Short term (≤ 2 years) |

| Increasing specialist awareness and earlier diagnosis rates | +1.2% | Global, with variation by healthcare access | Medium term (2-4 years) |

| Rising investments in rare-disease R&D | +1.6% | North America and Europe core; spillover to Asia-Pacific | Long term (≥ 4 years) |

| Advances in biomarker-driven precision medicine platforms | +1.3% | Concentrated in advanced healthcare systems worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Disease Burden And Unmet Clinical Needs

Systemic progression remains high, with 65.6% of very-early patients developing significant complications within five years, reinforcing demand for earlier intervention. Interstitial lung disease leads mortality and hematologic malignancy incidence doubles versus healthy cohorts, underscoring multi-organ risk. Only 30.8% of newly diagnosed patients receive immunomodulators within the first year, highlighting therapy gaps. Limited efficacy of legacy agents amplifies the call for disease-modifying solutions that suppress fibrotic pathways rather than mask symptoms, propelling the scleroderma therapeutics market.

Expansion Of Targeted And Disease-Modifying Treatment Options

CD19-targeted CAR-T cells in the RESET-SSc trial achieved deep B-cell depletion, enabling drug-free remission in severe cases. Isoform-selective TGF-β3 inhibition and TAK1 blockade broaden the pipeline, while 2024 EULAR guidance elevated rituximab to top-tier status for systemic disease. FDA Fast Track status for FT011 exemplifies regulator willingness to expedite transformative candidates. Precision platforms align treatment to autoantibody subsets and vascular pathology, shifting practice toward individualized regimens.

Favorable Orphan-Drug Designations And Reimbursement Frameworks

Multiple 2024 orphan designations, including FT011 and CABA-201, unlock tax credits, fee waivers, and seven-year exclusivity, catalyzing capital inflows[2]NIH, “Grants for Rare Disease Clinical Trials,” nih.gov. The FDA Office of Orphan Products earmarked USD 650,000 annually for rare-disease trial innovation. Payers adapt by covering high-cost cell therapies through specialty networks, and assistance programs now offer up to USD 16,500 per year for eligible systemic sclerosis patients. Combined US-EU orphan recognition shortens launch timelines and sustains global expansion of the scleroderma therapeutics market.

Increasing Specialist Awareness And Earlier Diagnosis Rates

The VEDOSS initiative shows Raynaud’s red-flag algorithms predict systemic transition with 70% accuracy, prompting prophylactic treatment. AI-driven dermal imaging quantifies fibrosis progression and guides therapy changes. Telemedicine broadens specialist access, and decentralized trials cut travel burdens, raising enrollment in rare-disease studies.

Restraints Impact Analysis of Scleroderma Therapeutics Market*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High therapy costs and affordability challenges | −1.9% | Global, most acute in emerging markets | Short term (≤ 2 years) |

| Stringent regulatory and clinical trial complexities | −1.1% | Global, varying by regulatory jurisdiction | Medium term (2-4 years) |

| Limited patient pool constraining large-scale studies | −0.9% | Global, especially in ultra-rare disease settings | Medium term (2-4 years) |

| Adverse event profiles impacting long-term adherence | −0.8% | Global, more pronounced in regions with limited specialist follow-up | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Therapy Costs And Affordability Challenges

Annual care for severe multisystem cases can exceed USD 50,000, and CAR-T out-of-pocket liability may top USD 100,000 in markets with limited coverage. Gross-to-net pricing distortions reached USD 334 billion in 2024, complicating patient access. Infrastructure limits, especially in emerging economies, hinder adoption of infusion-dependent therapies, slowing potential uptake within the scleroderma therapeutics market.

Stringent Regulatory And Clinical Trial Complexities

Endpoints such as modified Rodnan skin score correlate poorly with long-term outcomes, forcing sponsors to incorporate biomarker validation and patient-reported metrics that lengthen development timelines. Small patient pools inflate recruitment periods, and combination regimens require extensive safety packages. Manufacturing standards for autologous cell products raise cost and complexity, restricting the number of firms capable of commercial progression.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Scleroderma Therapeutics Market Segment Analysis

By Disease Type:

Systemic Dominance Drives Therapeutic InnovationSystemic disease controlled 72.10% of the scleroderma therapeutics market in 2025, reflecting multi-organ burden and higher drug utilization. Localized forms, though less prevalent, post the fastest 8.35% CAGR on improved recognition and early treatment. Systemic scleroderma patients often receive triple or quadruple therapy, reinforcing revenue concentration. Evidence that early localized intervention can avert systemic progression in 15% of cases widens therapy adoption. Regulatory approvals such as nintedanib for systemic sclerosis-associated interstitial lung disease have strengthened systemic segment lead. Innovations in biomarker-guided regimens now spill into localized disease, boosting segment momentum.

Therapeutic R&D gravitates toward systemic complications, especially lung fibrosis and pulmonary arterial hypertension, which drive 70% of disease mortality. The scleroderma therapeutics market size for systemic manifestations is projected to grow steadily as antifibrotic, vasculoprotective, and immunologic agents enter commercial lines. Localized cases gain from topical-to-systemic treatment escalation models, underscoring convergence of care pathways within the broader scleroderma therapeutics market.

By Drug Class:

Cell Therapies Disrupt Traditional ParadigmsEndothelin receptor antagonists held 28.10% revenue in 2025, anchored by bosentan and newer dual-target agents. Patent expirations and biosimilars threaten this base, while cell and gene therapies register a 8.78% CAGR—the fastest class growth. CD19-CAR-T candidate KYV-101 induced durable drug-free remission in 70% of treated patients, redefining clinical expectations. Nintedanib, a tyrosine kinase inhibitor, expanded beyond pulmonary fibrosis, illustrating class diversification.

Combination regimens integrate immunosuppressants as bridges to cellular therapies, preserving current revenue yet pivoting toward durable solutions. As data mature, the scleroderma therapeutics market size for cell therapies is forecast to climb, challenging incumbents and altering long-term competitive dynamics.

By Route of Administration:

Intravenous Surge Reflects Biologic ComplexityOral products captured 62.75% revenue in 2025 owing to convenience and chronic dosing patterns. Intravenous delivery, however, grows 9.95% annually alongside cell therapies and monoclonal antibodies. Hospital infusion centers scale capacity and digital scheduling to accommodate rising volumes. Sotatercept’s subcutaneous format for pulmonary hypertension shows how alternative delivery can sustain efficacy with lower clinic burden. As next-generation injectables advance, route selection will hinge on balancing patient convenience with pharmacologic requirements across the scleroderma therapeutics market.

Demand for specialized infusion services encourages hospital–retail partnerships, where trained nurses manage community-based administration. These hybrid models improve access and bolster adherence, an essential factor for high-cost biologics that dominate the evolving scleroderma therapeutics market.

By Distribution Channel:

Retail Expansion Driven by Specialty NetworksHospital pharmacies retained 45.60% share in 2025 because complex biologics require controlled storage and on-site administration. Retail pharmacies, powered by specialty divisions, post a 10.2% CAGR as they handle reimbursement coordination and patient education for oral and some injectable therapies. The Assistance Fund’s systemic sclerosis program illustrates how financial support aligns with expanded retail distribution. Online pharmacies increase reach through temperature-controlled logistics, yet cell therapies remain anchored in hospital settings due to manufacturing and safety imperatives. The scleroderma therapeutics market continues shifting toward integrated networks where retail, specialty, and hospital channels collaborate on comprehensive patient journeys.

Geography Analysis

North America Scleroderma Therapeutics Market

North America commanded 44.20% revenue in 2025, leveraging FDA accelerated approval, strong payer coverage, and concentrated cell-therapy R&D. U.S. firms such as Kyverna Therapeutics and Novartis drive trial activity, while Canadian public insurance facilitates orphan-drug uptake. Market maturity tempers growth, but ongoing launches of precision therapies sustain momentum.

Europe Scleroderma Therapeutics Market

Europe secured 38.60% share, supported by EMA centralized approvals and robust academic-industry alliances. Germany leads trial initiation, having cleared Phase 1/2 study of KYV-101 in January 2024. EULAR 2024 guidelines standardize treatment, enhancing cross-border adoption. Post-Brexit regulatory divergence modestly impacts UK timelines yet academic partnerships remain intact.

APAC Scleroderma Therapeutics Market

Asia-Pacific represents the fastest lane at an 8.45% CAGR to 2031. Japan’s advanced reimbursement of orphan drugs speeds cell therapy entry, and China’s reforms widen biologic access though regulatory hurdles persist. Australian sites contribute to global trials, while region-wide medtech venture funding contraction challenges local innovation. Nevertheless, demographic expansion and infrastructure upgrades underpin high regional growth within the scleroderma therapeutics market.

Regulatory Landscape

The regulatory environment for scleroderma (systemic sclerosis) therapeutics continues to be shaped by rare-disease frameworks and expedited review tools. In the United States, the FDA provides a dedicated rare-disease drug-development guidance suite and maintains rare-disease approval resources, which sponsors use to align on endpoints, natural history evidence, and biomarker strategies when conventional measures (eg, skin score) are insufficient.

In Europe, the EMA orphan-designation register shows sustained activity for systemic sclerosis programs. This supports incentives such as protocol assistance and potential market exclusivity upon authorization. Recent EMA orphan designations include upadacitinib (EU/3/26/3220) in April 2026 and resecabtagene autoleucel (EU/3/25/3158) in November 2025, reinforcing regulator engagement across both small molecules and advanced therapies.

Competitive Landscape

Market concentration remains moderate. Established firms defend share through patent portfolios and lifecycle management, yet rising biotech entrants accelerate disruption. Boehringer Ingelheim licensed new fibro-inflammatory compounds from Kyowa Kirin to extend pipeline depth. Johnson & Johnson faces Stelara expiry in 2025, opening a USD 6.72 billion vulnerability and attracting biosimilar challengers. Kyverna’s AI-enabled Verily partnership enhances manufacturing analytics for KYV-101, exemplifying data-driven competitive edges. Firms increasingly explore combination protocols that integrate antifibrotic, vasodilatory, and immunomodulatory actions to meet evolving clinical guidelines. Strategic alliances, regional commercialization agreements, and co-development of precision diagnostics define the next phase of rivalry across the scleroderma therapeutics market.

Scleroderma Therapeutics Industry Leaders

Boehringer Ingelheim International GmbH

F. Hoffmann-La Roche Ltd (Genentech)

Johnson & Johnson Services Inc. (Actelion)

Bayer AG

Novartis AG

- *Disclaimer: Major Players sorted in no particular order

Scleroderma Therapeutics Market Companies Covered in this Report

- Boehringer Ingelheim

- Roche

- Johnson & Johnson Services Inc. (Actelion)

- Bayer

- Novartis

- GlaxoSmithKline

- Bristol Myers Squibb Co. (Celgene)

- Sanofi S.A. (Kadmon)

- Corbus Pharmaceuticals Holdings Inc.

- Emerald Health Pharmaceuticals

- Prometic Life Sciences

- Cytori Therapeutics

- argenx SE

- Mallinckrodt plc

- Eiger BioPharmaceuticals Inc.

- Pfizer

- AstraZeneca

- Bristol Myers Squibb – Nogra Pharma (ETX-01)

- United Therapeutics Corp.

- Galapagos NV

Market Opportunities and Future Outlook

White space remains concentrated in disease-modifying options that can address immune dysregulation, fibrosis, and vasculopathy, particularly in systemic sclerosis across interstitial lung disease and treatment-resistant subsets. One practical opportunity is improving clinical-development efficiency and comparability through platform and master-protocol approaches. The CONQUEST trial infrastructure (NCT06195072) supports testing multiple investigational agents within a shared trial framework.

A second opportunity is scalability for next-generation immune reset strategies that reduce reliance on individualized manufacturing. In July 2026, preliminary Phase 1 data presented for an investigational iPSC-derived CAR-T program (FT819) in treatment-resistant systemic sclerosis pointed to progress on off-the-shelf cellular approaches. In parallel, Boehringer Ingelheim listed a Phase 3 start (NCT07497087) in July 2026 for nerandomilast in systemic sclerosis, signaling continued investment in antifibrotic mechanisms. Execution room also comes from regulatory-pathway clarification efforts, including Aisa Pharma stating plans (March 2026) for an End of Phase 2 FDA meeting for AISA-021 in systemic sclerosis-associated Raynaud's phenomenon to clarify a registration route and evidence requirements.

Recent Industry Developments in Scleroderma Therapeutics Market

- June 2026: Boehringer Ingelheim reported continued pipeline progress focused on its systemic sclerosis program, following completion status updates for avenciguat (BI 685509) in systemic sclerosis. The update kept attention on soluble guanylate cyclase activation as a differentiated mechanism alongside antifibrotic approaches for systemic disease complications.

- February 2025: Boehringer Ingelheim announced that the Phase III FIBRONEER-ILD trial of nerandomilast (BI 1015550) met its primary endpoint for lung function improvement in progressive pulmonary fibrosis, including systemic sclerosis-associated interstitial lung disease. The readout strengthened late-stage confidence in antifibrotic positioning for SSc-ILD and increased competitive pressure on legacy immunosuppression-only strategies.

- July 2024: Actelion Pharmaceuticals (Johnson & Johnson) published real-world evidence from the EXPOSURE study on selexipag use in pulmonary arterial hypertension associated with connective tissue disease, a frequent complication in scleroderma. The findings reinforced the role of registry-grade evidence in supporting prescribing, payer discussions, and treatment persistence for PAH therapies used in scleroderma-linked disease pathways.

Scleroderma Therapeutics Market Report Scope and Research Methodology

Market Definition and Coverage

We define the scleroderma therapeutics market as the value of prescription treatments used to manage localized scleroderma and systemic sclerosis, including drug therapy used across major organ complications that are treated as part of scleroderma care.

Scope exclusions: OTC skin care products, standalone phototherapy devices, and procedure only surgical spending are excluded from this market sizing.

Segments Covered in This Report

- By Disease Type

- Systemic Scleroderma

- Localized Scleroderma

- By Drug Class

- PDE-5 Inhibitors

- Prostacyclin Analogues

- Endothelin Receptor Antagonists

- Immunosuppressants

- Tyrosine-Kinase / Anti-fibrotic Agents

- Cell & Gene Therapies

- Other Drug Class

- By Route of Administration

- Oral

- Intravenous

- Sub-cutaneous

- Transdermal / Topical

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to map the patient pool and the treated share before any revenue math is applied, since scleroderma is a low-prevalence condition where diagnosis and referral patterns affect the addressable population. We reviewed public sources such as CDC and NIH pages, PubMed indexed clinical literature, US FDA drug labels and approvals, and WHO and OECD health statistics to anchor basic epidemiology, treatment pathways, and therapy availability.

In parallel, we screened company filings and investor decks for therapy positioning and broader sales context. We also used reputed press and association websites for guideline changes and real-world access signals. When needed, paid company financials and intelligence subscriptions and a patent database were used to cross-check corporate activity and timing signals around products and pipelines. These examples are not exhaustive, and many other public and paid sources were also referred to for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on stress testing assumptions that are hard to read cleanly from public sources, especially diagnosis rates, treatment sequencing, and how quickly new options get adopted in systemic sclerosis versus localized disease. We spoke with a mix of clinicians, payer or access specialists, and industry participants across major geographies so the model reflects real prescribing patterns and typical coverage constraints, and then we used follow-ups to reconcile conflicting viewpoints.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 13% | APAC: 39% |

| Mid tier: 50% | Functional/Unit leaders: 41% | EMEA: 35% |

| Smaller Players: 22% | Managers: 46% | Americas: 26% |

Market-Sizing & Forecasting

Sizing starts with a top-down treated-patient build where prevalence and incidence are translated into diagnosed patients, and then filtered through specialty referral patterns, organ involvement profiles, and the share that receives prescription therapy in a given year. Revenue is derived by applying therapy class mix and typical annual cost by regimen, then adjusting for persistence, switches, and the split between hospital and retail dispensing where relevant.

To keep totals realistic, we run selective bottom-up checks using supplier revenue signals, sampled regimen cost multiplied by expected patient counts in key countries, and channel checks on adoption timing. Inputs that are actively tracked include diagnosis delay trends, specialty center density, the share of systemic sclerosis within total scleroderma, use of immunosuppressants and antifibrotic related regimens, biologic uptake, and gross-to-net effects driven by access and reimbursement. When country-level data is thin, gaps are filled using comparable market analogs with a similar payer structure and then revalidated through expert feedback.

For forecasting, scenario analysis is used because the market is sensitive to approval timing, guideline adoption, and reimbursement changes. Assumptions on treated share and pricing are carried forward using expert consensus ranges, then stress tested for upside and downside cases before the final view is locked.

Data Validation & Update Cycle

Validation is done through multiple checks so the model does not depend on a single data stream. We compare outputs against independent signals such as therapy uptake commentary, country-level access changes, and whether the implied treated population stays consistent with epidemiology and care pathway realities.

Anomalies are flagged when growth, pricing, or treated share shifts faster than what interviews and public events can explain, and then the underlying inputs are rechecked and, if needed, respondents are re-contacted. The work is reviewed in steps by another analyst before sign-off, and the report is refreshed annually with interim updates when material events occur. Before delivery, a final update pass is completed so clients receive the latest adjusted view.

Mordor Intelligence's Scleroderma Therapeutics Market Size Measured Against Other Published Estimates

Published market sizes for scleroderma therapeutics can differ a lot, even when they are discussing the same disease area, because the counted therapies and the way the patient pool is built are not always consistent. Differences in what gets treated as scleroderma revenue, and how pricing and uptake are carried forward year to year, usually explain most of the spread.

The main gap comes from scope and therapy counting, where Mordor Intelligence treats scleroderma therapeutics as prescription treatment revenues tied to scleroderma use, and does not fold in broad immunology sales that are not attributable to scleroderma patients. Another driver is the patient funnel, since some estimates lean heavily on headline prevalence, while our model filters through diagnosis, referral, and treated share before applying regimen costs. Smaller differences also come from currency timing and whether forecasts assume faster uptake for new options versus a more gradual access driven ramp.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 33.50 B (2025) | |

| Global Consultancy A | USD 2.74 B (2025) | Uses a narrower drug-only view and is more conservative on treated share, which keeps revenues closer to currently addressed patients rather than broader scleroderma care spending. |

| Industry Research Publisher B | USD 2.69 B (2025) | Anchors on a 2024 base and applies a steady CAGR with limited adjustment for diagnosis delay, access step edits, and regimen mix shifts, which can understate pricing and uptake changes in specialty care. |

Across the three figures, most of the difference is explained by what is counted as scleroderma specific revenue and how the treated population is filtered before pricing is applied. By keeping assumptions tied to clear patient funnel steps and a transparent regimen cost build, the estimate stays easier to reproduce and simpler to validate as new clinical and access signals emerge.

Key Questions Answered in the Report

What is the current size of the scleroderma therapeutics market?

The market is valued at USD 36.07 billion in 2026 and is expected to reach USD 52.23 billion by 2031.

Which disease segment holds the largest market share?

Systemic scleroderma accounts for 72.10% of the scleroderma therapeutics market share in 2025.

Which drug class is growing fastest?

Cell and gene therapies are forecast to register a 8.78% CAGR through 2031, the fastest among all classes.

Why is Asia-Pacific the fastest-growing region?

Regulatory modernization, expanding healthcare infrastructure, and rising specialist awareness drive an 8.45% CAGR in the region.

How are high therapy costs being addressed?

Specialty pharmacy networks, orphan-drug incentives, and patient assistance programs offering up to USD 16,500 annually help mitigate affordability barriers.

What is the main driver behind market growth?

The expansion of targeted, disease-modifying treatment options—including CAR-T cells and biomarker-guided therapies—is the most influential growth driver, adding roughly 2.1 percentage points to forecast CAGR.

Page last updated on: