Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

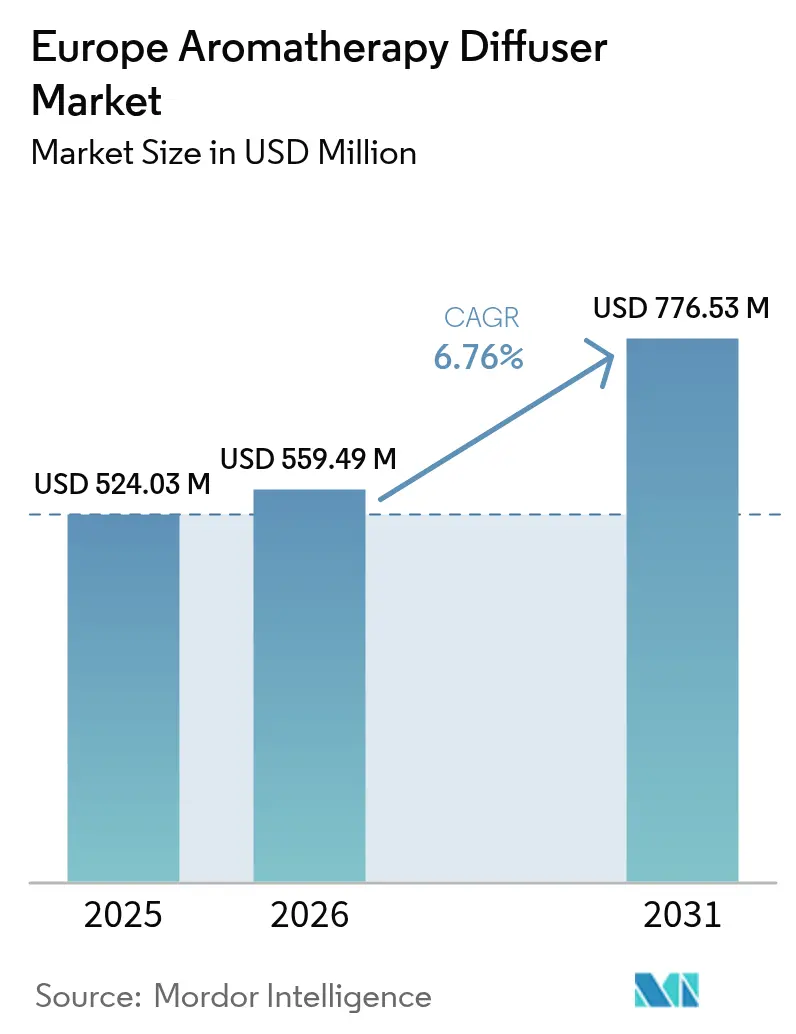

| Base Year Market Size (2025) | USD 524.03 Million |

| Market Size (2026) | USD 559.49 Million |

| Market Size (2031) | USD 776.53 Million |

| Growth Rate (2026 - 2031) | 6.76% CAGR |

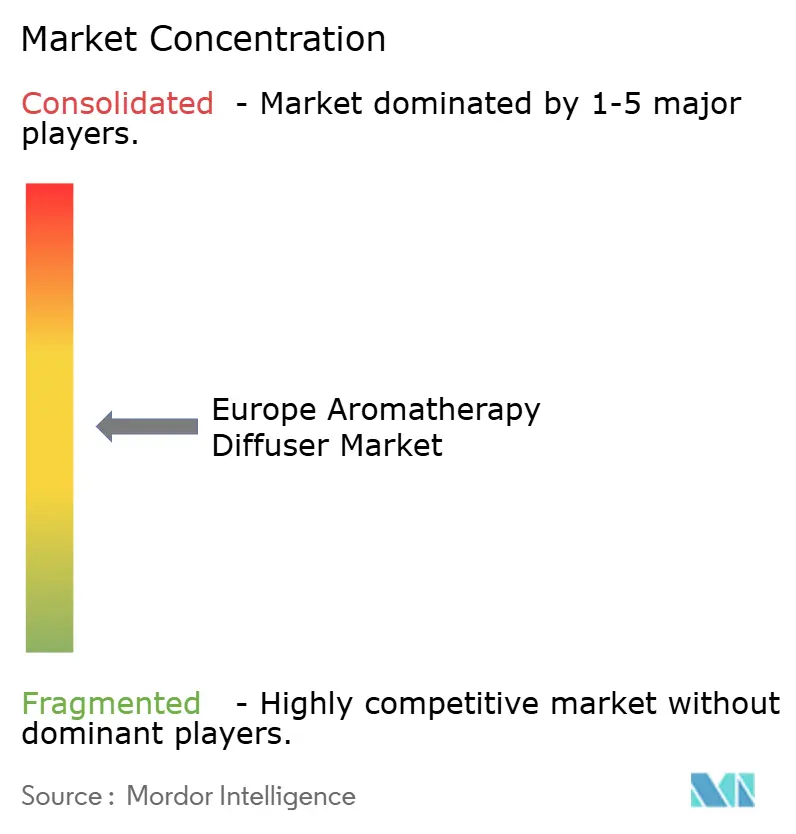

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Aromatherapy Diffuser Market Analysis by Mordor Intelligence

The European aromatherapy diffuser market size was valued at USD 524.03 million in 2025 and estimated to grow from USD 559.49 million in 2026 to reach USD 776.53 million by 2031, at a CAGR of 6.76% during the forecast period (2026-2031). As consumers increasingly prioritize air quality and regulations on indoor environments tighten, the demand for diffusers is surging in both residential and light-commercial spaces. This momentum is further fueled by device manufacturers integrating humidity and volatile organic compound sensors with building management systems. Such advancements empower homeowners and facility managers to not only meet EN 16798 benchmarks but also enhance occupant comfort. The European aromatherapy diffuser market is also reaping rewards from rising disposable incomes, a trend towards premium wellness gifts, and a growing acceptance of subscription oil bundles, which facilitate repeat purchases. While challenges like counterfeiting, fluctuations in raw material costs, and compliance with electronic waste regulations persist, they predominantly impact low-margin players. This dynamic offers better-capitalized brands an opportunity to expand their market share through a focus on product quality, traceable sourcing, and initiatives centered around circular design.

Key Report Takeaways

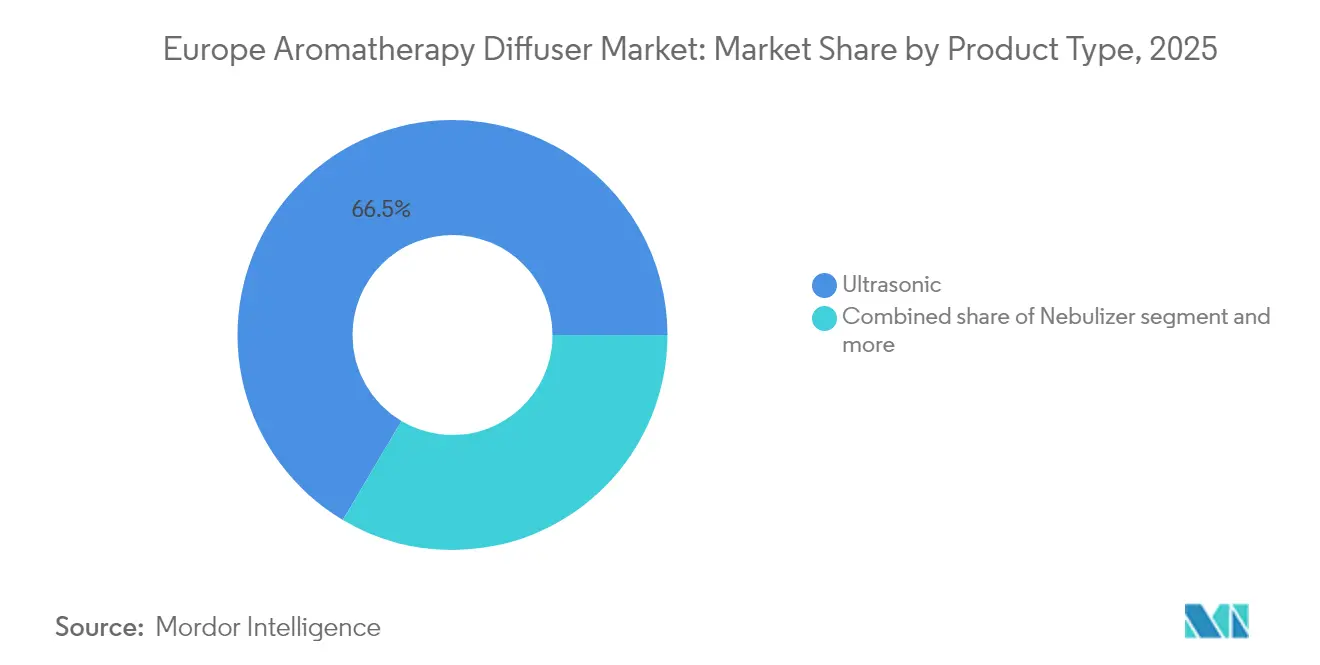

- By type, ultrasonic diffusers led with 66.48% of the Europe aromatherapy diffuser market share in 2025, while nebuliser units are forecast to grow at a 7.13% CAGR between 2026 and 2031.

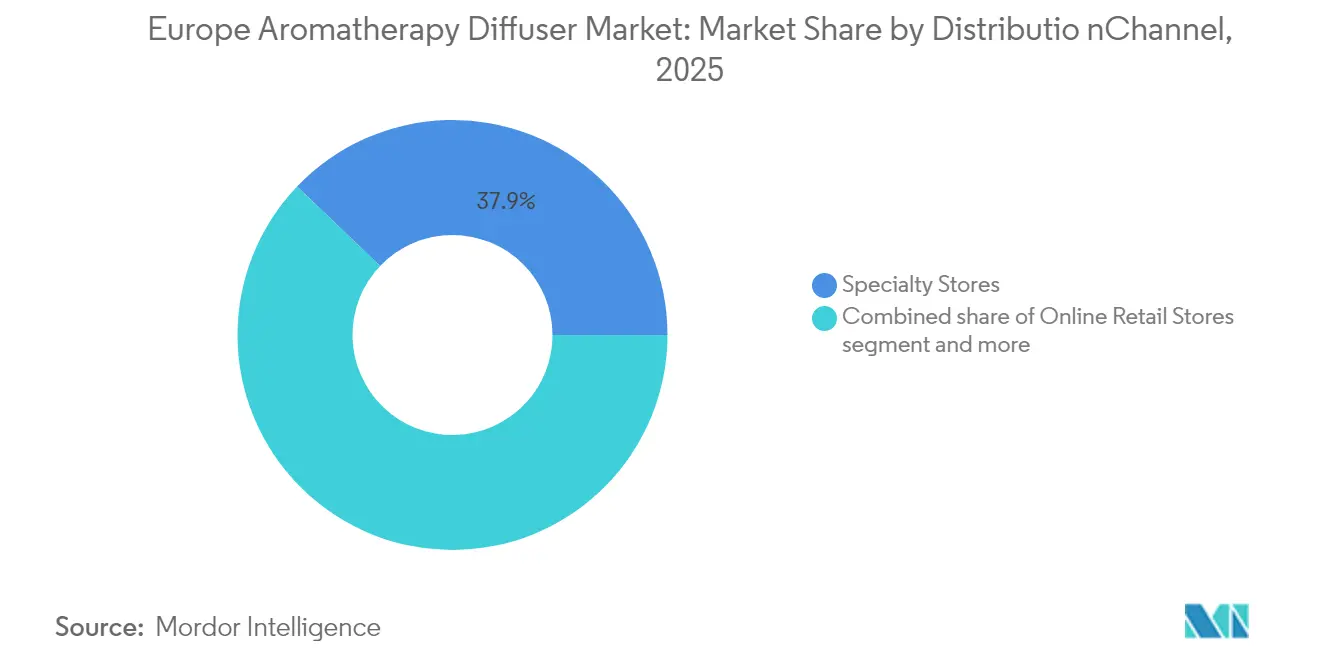

- By distribution channel, specialty retail held 37.86% of 2025 revenue; online platforms are projected to expand at an 8.52% CAGR through 2031.

- By geography, France accounted for 21.54% of regional revenue in 2025, whereas Italy is set to advance at a 7.25% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Aromatherapy Diffuser Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising popularity of home-wellness rituals | +1.2% | Germany, France, UK, Netherlands, Nordics | Medium term (2-4 years) |

| Growing penetration of smart/IoT-enabled diffusers | +1.4% | Urban hubs in Germany, UK, France, Netherlands, Sweden | Short term (≤ 2 years) |

| Premiumisation and gifting trends in Europe | +0.9% | France, Germany, UK, Italy | Medium term (2-4 years) |

| Mandatory indoor-air-quality directives (EN 16798) | +0.8% | EU-wide, led by Germany, Netherlands, Belgium | Long term (≥ 4 years) |

| Retailer private-label expansion | +0.7% | Germany, Netherlands, Poland | Short term (≤ 2 years) |

| Subscription-based essential-oil bundles | +0.6% | UK, France, Germany, Netherlands | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising popularity of home-wellness rituals

In Western Europe, consumers are now integrating in-home recovery, productivity, and relaxation into their daily routines. Diffusers have emerged as essential devices, joining the ranks of yoga mats and sound machines. This transition from mere decorative items to essential wellness tools has led to increased repeat purchases of oils. As a result, brands that curate blends targeting sleep, focus, and stress relief are witnessing a boost in their lifetime value. Users in the Nordics, facing prolonged winters, exhibit heightened engagement with these products. Meanwhile, urban residents are opting for compact ultrasonic units, which produce a silent mist, perfectly suited for their smaller apartments. Brands emphasizing scientifically-backed mood enhancements and promoting low-maintenance operations are resonating more with first-time buyers. Specialty retailers are capitalizing on this trend, offering in-store trials and bundled starter kits to alleviate any purchase hesitations.

Growing penetration of smart/iot-enabled diffusers

Tech-savvy households are increasingly turning to voice-controlled diffusers that seamlessly integrate with platforms like Alexa, Google Home, and Apple HomeKit. These diffusers come equipped with app dashboards, allowing users to adjust mist intensity, set schedules, and receive low-oil alerts. Moreover, they can integrate sensor data into broader home-automation routines. A 2024 peer-reviewed study highlighted the efficacy of these smart diffusers, noting an 18% reduction in indoor particulate matter when activated during peak traffic hours. Manufacturers are capitalizing on anonymized usage metrics, using them to refine designs and enhance predictive maintenance features. Adoption is strongest in Germany and the Netherlands, driven by robust broadband infrastructure and enticing smart-device subsidies from energy utilities. This shift, merging air-quality monitoring with aromatherapy, positions diffusers as essential health-tech appliances rather than mere lifestyle luxuries.

Premiumization and gifting trends in Europe

Consumers are increasingly gravitating towards diffusers priced above EUR 100 (USD 110), drawn by artisanal glass, ceramic finishes, and low-EMF certifications, which align with the growing demand for premium and health-conscious products. Brands are enticed to introduce holiday lines and limited collaborations, as seasonal gift packs pairing designer hardware with themed oil assortments boast margins 40-50% higher than standalone units, making them a lucrative segment. French and Italian shoppers, with their cultural appreciation for craftsmanship and fragrance heritage, exhibit the highest willingness to pay, further driving premiumization in these markets. Retailers, recognizing this trend, structure displays around gift-ready packaging, streamlining purchasing decisions and curbing return rates by offering convenience and aesthetic appeal. Moreover, the predictable demand spikes from the European gifting calendar aid producers in refining their production planning and inventory turnover, ensuring a steady supply chain and optimized resource allocation.

Mandatory indoor-air-quality directives (EN 16798)

Under the revised Energy Performance of Buildings Directive, new and renovated structures are mandated to continuously monitor CO₂, humidity, and volatile organics.. The revised EPBD, effective from 2024, extends these requirements to a broader range of building types, including multi-family residential units and small commercial spaces, expanding the addressable market for IoT-enabled diffusers[1]Source: European Commission, "Energy Performance of Buildings Directive", energy.ec.europa.eu. This directive aims to improve energy efficiency and indoor air quality, aligning with broader sustainability goals across the European Union. As a result, building managers are increasingly viewing sensor-enabled diffusers not just as tools for regulatory compliance, but also as enhancements to occupant experience by ensuring healthier and more comfortable indoor environments. In Germany, the Netherlands, and Belgium, municipal codes mandate digital logbooks to track and report building performance metrics. This regulation positions compliant diffusers as a cost-effective alternative to traditional monitoring stations, reducing the need for separate, dedicated monitoring systems. Brands that provide third-party certifications and ensure seamless integration with building-management software are establishing a strong competitive edge against cheaper imports, which often lack the necessary compliance and interoperability. Looking ahead, as indoor-air regulations tighten and awareness of air quality's impact on health grows, these diffusers are set to transition from being mere accessories to essential fixtures in multifamily housing and small commercial suites, driving demand in the market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Safety concerns over synthetic fragrance oils | -0.5% | EU-wide, notably France, Germany, Netherlands | Short term (≤ 2 years) |

| Counterfeit and low-quality imports from Asia | -0.6% | Italy, Spain, Poland, Russia | Medium term (2-4 years) |

| EU eco-design and WEEE compliance costs | -0.4% | Germany, Netherlands, Sweden | Long term (≥ 4 years) |

| Volatility in essential-oil raw-material prices | -0.7% | All European markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Safety concerns over synthetic fragrance oils

Under the EU REACH framework, manufacturers are now compelled to disclose fragrance ingredients and undertake toxicity assessments. This regulatory shift aims to enhance consumer safety and environmental protection by ensuring transparency in product formulations. Following this, the French agency ANSES advised that diffuser sessions be capped at thirty minutes in well-ventilated rooms to minimize potential health risks[2]Source: National Agency for Food, Environmental and Occupational Health & Safety, "Essential oils should be used with caution", vigilanses.anses.fr. This recommendation has led retailers to increasingly seek third-party safety certificates to validate product safety and compliance. Budget brands, which often rely on less transparent blends, are grappling with heightened testing costs and diminishing shelf space, as they struggle to meet these stringent requirements. In contrast, premium brands that proudly market their 100% pure oils are reaping the benefits of consumer trust, leveraging their transparency as a competitive advantage. The issue has gained traction on social media, thanks to consumer watchdogs, who are actively raising awareness and influencing purchasing decisions. This has steered shoppers towards products that are both traceable and certified, further pressuring manufacturers to adapt. Consequently, players without in-house toxicology expertise or transparent supply chains are feeling the pinch, as the compliance demands eat into their profit margins and challenge their operational sustainability.

Volatility in essential-oil raw-material prices

In 2024, spot prices for essential oils saw significant fluctuations: neroli prices plummeted by 40%, and geraniums by 30%, while lavender and peppermint prices held steady. Subscription services, which set prices for monthly kits in advance, grapple with these price swings, often needing to renegotiate contracts, a move that risks customer loyalty. To mitigate risks, vertically integrated companies are diversifying their acreage and entering into forward contracts with growers located in North Africa and Eastern Europe. Meanwhile, some innovators are exploring biotech alternatives that can replicate terpene profiles on a larger scale. While these alternatives promise price stability, they still await regulatory approval. The ongoing price volatility is pushing companies to adopt multi-sourcing strategies. However, this approach introduces added logistical complexities, which can elevate costs, particularly for smaller brands with limited procurement capabilities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Ultrasonic Dominance Meets Nebuliser Premiumisation

In 2025, ultrasonic units commanded a dominant 66.48% share of the European aromatherapy diffuser market. Their appeal lies in silent operation, energy efficiency, and versatility with various oil viscosities, making them favorites in bedrooms, offices, and yoga studios. By employing a water-dilution method, these units not only extend their run times but also offer cost savings for commercial wellness spaces. A peer-reviewed trial in 2024 highlighted the efficacy of ultrasonic diffusers equipped with air-quality monitors, showcasing an 18% reduction in particulate matter during urban rush hours. This positions them as compliant tools for indoor air management, aligning with EN 16798 standards. Additionally, the integration of smart sensors has captivated tech-savvy consumers, solidifying the dominance of ultrasonics in the market.

Nebulisers, with their unique water-free and heat-free atomization of pure oils, are set to outpace the European aromatherapy diffuser market, boasting a projected CAGR of 7.13% through 2031, slightly ahead of the market's average of 6.76%. While they operate louder than their counterparts, premium spa operators are drawn to their undiluted efficacy, often justifying the higher prices with hand-blown glass and medical-grade materials. Meanwhile, emerging hybrids are making waves, blending the mist of ultrasonics with the bursts of nebulisers for an optimal balance of endurance and purity. The "others" category, encompassing evaporative and heat-plate models, is carving a niche in travel and decor, though it remains smaller in scale.

By Distribution Channel: Specialty Retail Faces Digital Disruption

In 2025, specialty retail claimed 37.86% of Europe's aromatherapy diffuser market revenue. This surge was fueled by tactile product discovery, guided scent matching, and bundled starter kits, all of which elevated the average basket value. In-store educators played a pivotal role, demonstrating diffuser settings and safe oil dilution ratios. Their efforts not only alleviated buyer hesitation but also curtailed return rates. Such hands-on engagement cultivated trust and loyalty, especially among wellness-centric consumers desiring tailored experiences. Specialty retailers also emphasized creating an immersive shopping environment, where customers could test products and receive personalized advice, further enhancing the overall shopping experience. Meanwhile, mass retailers, including supermarkets and drugstores, introduced private-label diffusers at prices 20-30% lower than branded counterparts, broadening access for budget-conscious shoppers and appealing to a wider demographic.

Online sales are projected to grow at a CAGR of 8.52% through 2031, outstripping the overall market. This growth is attributed to direct-to-consumer tactics, emphasizing influencer reviews, flexible payment options, and auto-replenish subscriptions. E-commerce platforms harness zero-party data on scent preferences, offering personalized recommendations that boost repeat purchases. These platforms also invest in user-friendly interfaces and targeted marketing campaigns to attract and retain customers. Supermarkets' click-and-collect programs merge digital sales with the ease of physical pickup, blurring the lines of traditional channels. Leaders in the market adopt omnichannel strategies, harmonizing inventory, loyalty, and service across various platforms, ensuring they remain at the forefront amidst rising demands for effortless returns and consistent pricing. Additionally, seamless integration of online and offline channels allows companies to cater to diverse consumer preferences, driving sustained growth in the competitive landscape.

Geography Analysis

In 2025, France capitalized on its rich aromatherapy heritage and the trust pharmacists command, accounting for 21.54% of total sales. French consumers, valuing certified organic oils, are drawn to premium diffusers. These diffusers, often crafted from artisanal glass or ceramic, find a willing audience among buyers who appreciate craftsmanship and regional sourcing, even at a higher price. Meanwhile, Italy is set to experience a 7.25% CAGR growth rate until 2031, driven by rising household incomes, deeper e-commerce penetration, and a rapidly expanding smart-home base. Italian producers of citrus and rosemary oils leverage short supply chains, ensuring freshness and weaving in stories of their unique terroir.

Germany, the UK, and Spain collectively represent a substantial portion of the market demand. In Germany, stringent regulations mandate CE markings and WEEE registration, compelling suppliers to embrace eco-design and transparent safety labeling. The UK, benefiting from established logistics, has seen a surge in subscription services that offer curated monthly oil deliveries, ensuring a steady revenue stream. In Spain, a resurgence in tourism has led to increased diffuser use in hotels and vacation rentals. This trend extends to urban residences, where renters increasingly seek wellness amenities. Secondary markets such as the Netherlands, Poland, Belgium, Sweden, and Russia are emerging as diverse opportunities. In the Netherlands, consumers are at the forefront of smart-home diffusion, seamlessly integrating diffusers into routines that control lighting and heating through unified apps. Polish retailers are revamping store layouts, emphasizing wellness sections to entice trial among aspirational shoppers. Despite currency fluctuations, affluent urbanites in Russia are drawn to premium imports. In Sweden, consumers are willing to pay a premium for products made from sustainable, recyclable materials. Meanwhile, smaller economies in Central and Eastern Europe are leaning on cross-border e-commerce. Today, they favor budget-friendly ultrasonic units, but as disposable incomes rise, there's a clear signal towards future premiumization.

Competitive Landscape

In Europe, the aromatherapy diffuser market is moderately fragmented, with no single vendor commanding a double-digit share. Leaders in multi-level marketing, doTERRA and Young Living, utilize vertically integrated farms and proprietary distillation. Their direct-selling networks bundle hardware with exclusive oils, ensuring a steady stream of consumable revenue. Electronics experts Stadler Form and HoMedics market diffusers as essential home upgrades, highlighting features like quiet fans, expansive room coverage, and app-based controls. Meanwhile, lifestyle brands Muji and AromaWorks cater to design aficionados, offering minimalist ceramics and eco-friendly packaging.

Entry-level devices from private labels like DM, Rossmann, Etos, and Hema are priced 20-30% lower than leading brands, squeezing margins for mid-market suppliers without distinct offerings. In response, innovators are introducing subscription bundles, blockchain technology for oil provenance, and extended warranties to foster repeat purchases. A 2024 European Patent filing revealed an adaptive diffuser that adjusts mist output based on biometric data from wearables, hinting at a future link with personalized health monitoring.

Today's vendor differentiation hinges on three main pillars: proven oil quality, advanced smart features, and a commitment to sustainability. Brands that offer repairable designs, trade-in initiatives, and modular parts find it easier to meet WEEE obligations and gain favor with eco-conscious retailers. On another front, legitimate players are countering counterfeit imports, which often lack CE marks, by implementing tamper-evident seals and QR-based authenticity checks, bolstering consumer trust at the point of sale. Looking ahead, collaborations between diffuser manufacturers and sectors like lighting, HVAC, and wellness apps are set to deepen, increasing switching costs and broadening potential use cases.

Europe Aromatherapy Diffuser Industry Leaders

-

Young Living Essential Oils

-

doTERRA International

-

Muji Europe Holdings

-

Puzhen Life

-

Stadler Form

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Evolve Beauty unveiled a new aromatherapy range centered on four functional blends: Energise (Joyful Light), Nurture (Wild Divine), Calm (Zen Whisper), and Detox (Vital Clarity). These vegan, COSMOS-certified blends, offered as essences, pulse-point roll-ons, bath oils, and matching hand/body care, utilize essential oils like neroli, rose, lavender, and citrus to promote mood enhancement, focus, relaxation, and emotional balance.

- April 2025: Ripple⁺ Home introduced REED, its inaugural home scent diffuser collection, featuring six aromas co-created with master perfumers from Grasse, France. The collection's crystal glass, droplet-shaped bottles, equipped with a single reed, blend sculptural design with a slow-release luxury fragrance, offering mood-enhancing aromatherapy for the home.

- December 2024: Aluxury expanded its aromatherapy portfolio, introducing new premium essential oils, an extended collection of diffuser oils, and an upgraded Nebula waterless diffuser. The 100% pure, vegan essential oils, including lavender, peppermint, bergamot, and eucalyptus, are ethically sourced and come with documentation from IFRA, CLP, and MSDS.

- June 2024: Airomé launched a holiday ceramic collection that quickly sold out in just six weeks, highlighting the strong consumer demand for premium, gift-ready designs.

Europe Aromatherapy Diffuser Market Report Scope

Europe Aromatherapy diffuser market is segmented by product type, distribution channel, and geography. based on the product type, the market is segmented into ultrasonic, nebulizer, others. based on the distribution channel, the market is segmented into supermarket/hypermarket, convenience stores, specialist stores, online retailers, others. based on geography, the report provides a detailed analysis, which includes Germany, United Kingdom, France, Italy, Spain, Ireland, and rest of Europe.

By Type

| Ultrasonic |

| Nebuliser |

| Others |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Convenience/Grocery Stores |

| Specialty Stores |

| Online Retail Stores |

| Other Distribution Channels |

Country

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Russia |

| Netherlands |

| Poland |

| Belgium |

| Sweden |

| Rest of Europe |

| By Type | Ultrasonic |

| Nebuliser | |

| Others | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | |

| Specialty Stores | |

| Online Retail Stores | |

| Other Distribution Channels | |

| Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe aromatherapy diffuser market in 2026?

The Europe aromatherapy diffuser market size is valued at USD 559.49 million in 2026.

What is the expected growth rate for aromatherapy diffusers in Europe to 2031?

Regional sales are forecast to advance at a CAGR of 6.76% through 2031.

Which diffuser technology holds the biggest share today?

Ultrasonic models dominate with 66.48% of Europe aromatherapy diffuser market share in 2025.

Which sales channel is growing fastest across Europe?

Online platforms are projected to grow at an 8.52% CAGR as direct-to-consumer brands widen reach and push subscriptions.

Page last updated on: