Offshore Drilling Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 32.81 Billion |

| Market Size (2031) | USD 41.68 Billion |

| Growth Rate (2026 - 2031) | 4.90% CAGR |

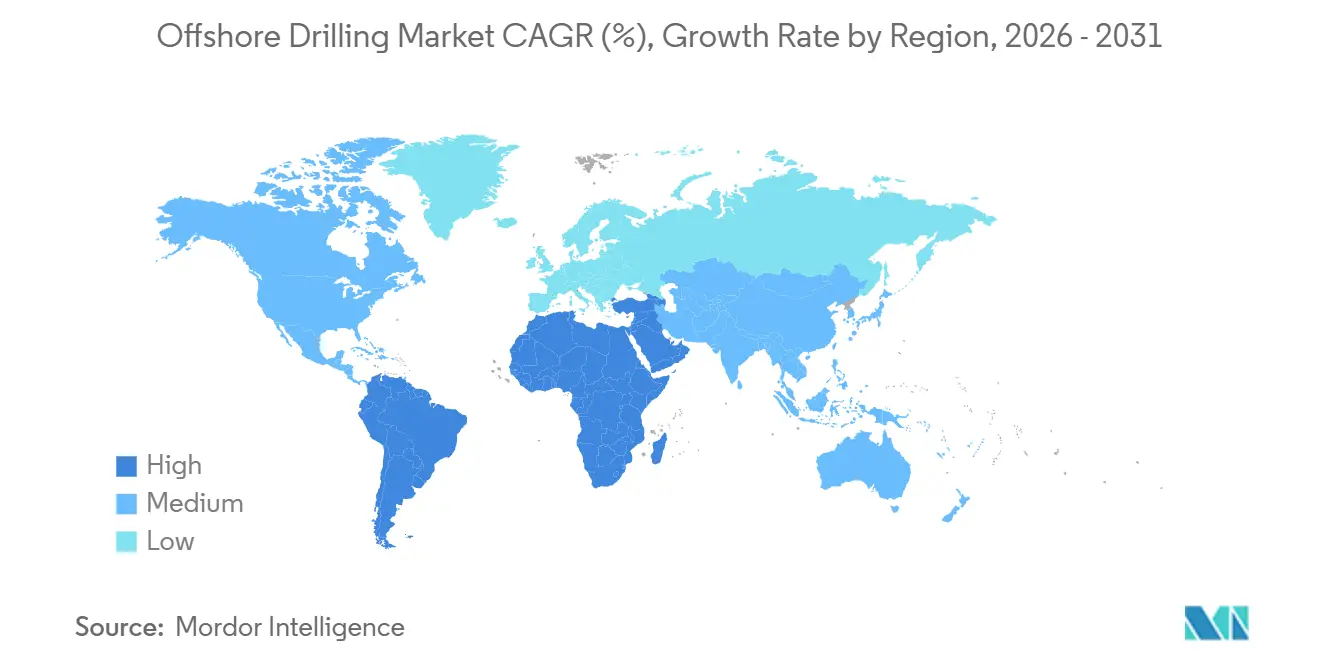

| Fastest Growing Market | Middle-East and Africa |

| Largest Market | Middle East and Africa |

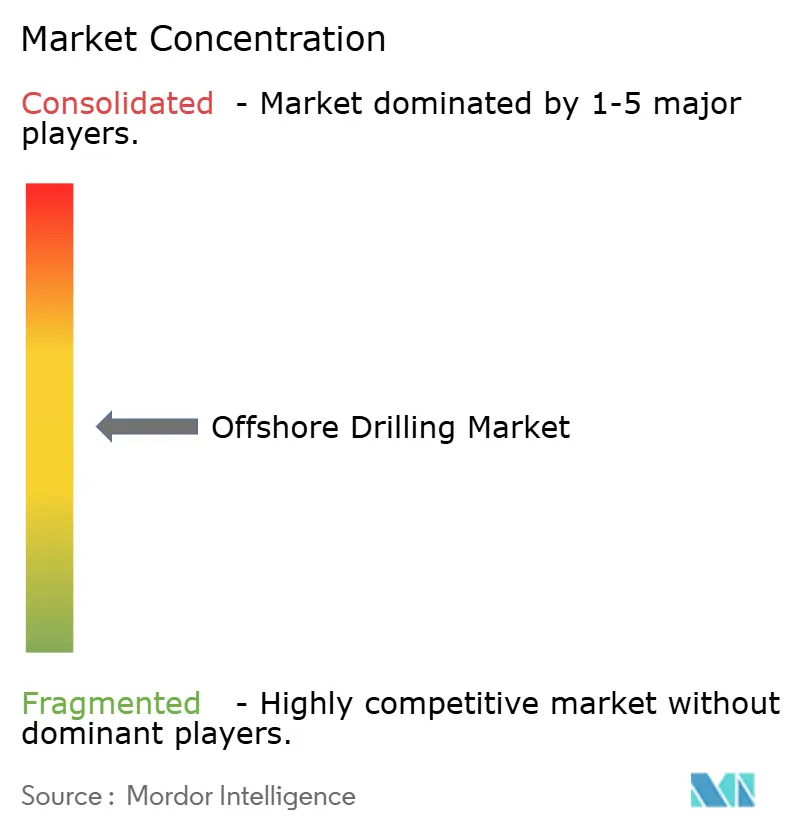

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Offshore Drilling Market Analysis by Mordor Intelligence

The offshore drilling market size reached USD 31.22 billion in 2025 and is projected to climb to USD 32.81 billion in 2026, eventually advancing to USD 41.68 billion by 2031 at a 4.90% CAGR, underscoring a steady upswing in upstream spending on complex wells and longer-life reservoirs. Energy-security mandates in the Middle East and Asia continue to steer capital into multi-decade offshore programs, while deepwater discoveries in Guyana, Brazil, and Namibia shift contractor focus toward high-specification drillships. Tight supply of hybrid-ready rigs, the adoption of autonomous drilling systems, and a structural crew shortage are elevating day rates and stretching backlogs. Simultaneously, national oil companies are crowding out independent explorers, reshaping demand cycles, and reducing the volatility previously caused by short-term shale swings. Competitive positioning now hinges on emissions-reduction technology and digital uptime tools that translate directly into lower fuel burn and higher well counts per rig.

Key Report Takeaways

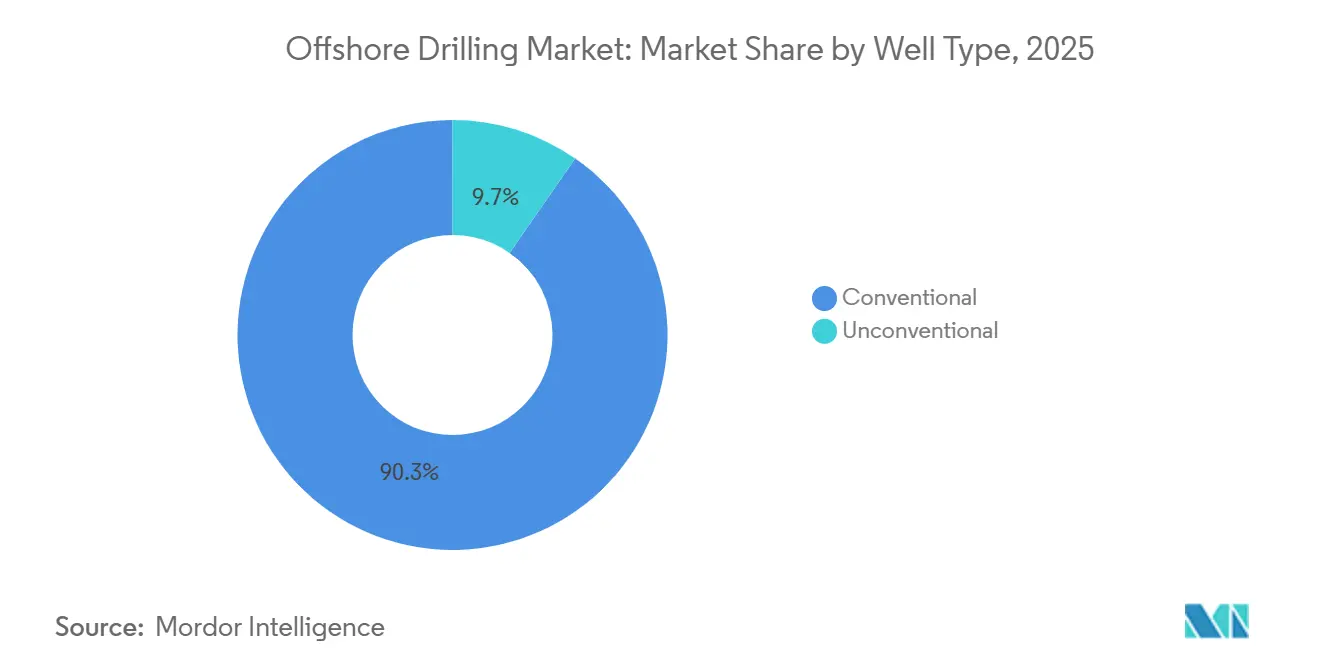

- By well type, conventional wells held 90.33% of the offshore drilling market share in 2025; unconventional wells are poised to expand at a 10.49% CAGR through 2031.

- By water depth, shallow-water projects captured 51.11% of the offshore drilling market size in 2025, while deepwater and ultra-deepwater activity is advancing at a 6.11% CAGR through 2031.

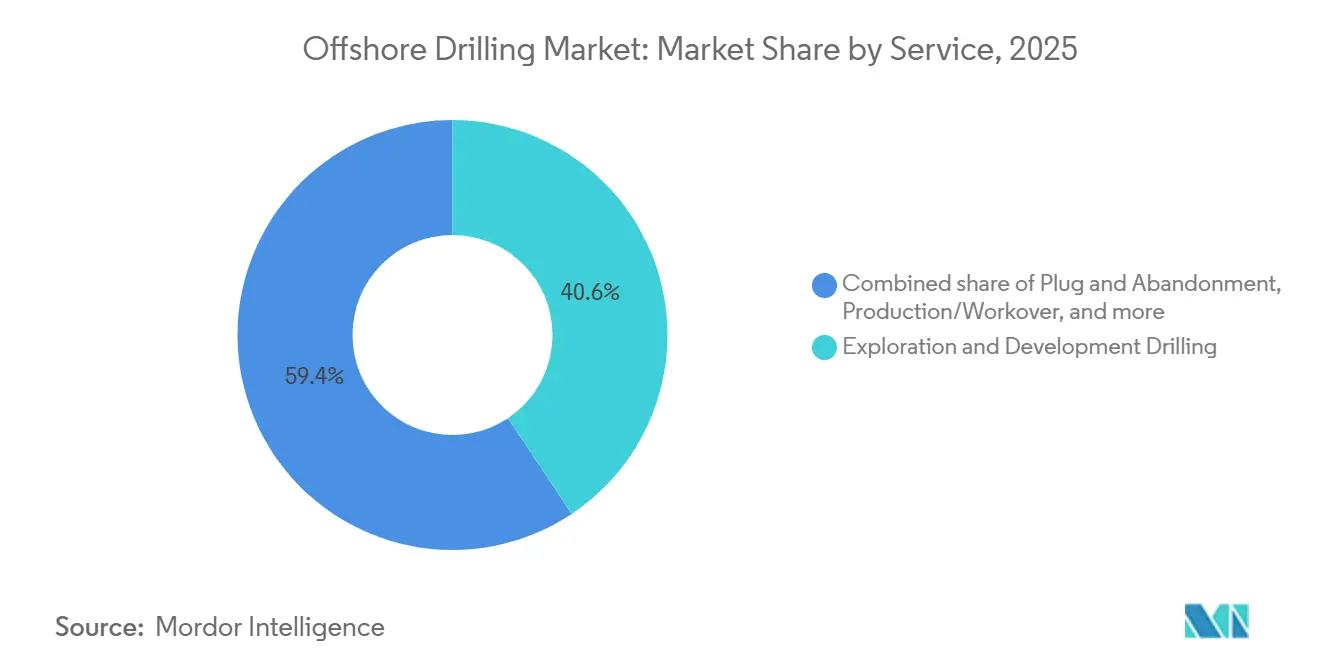

- By service, the exploration and development drilling segment captured a 40.64% share of the market size in 2025; plug and abandonment is projected to grow at a 10.67% CAGR through 2031.

- By geography, the Middle East and Africa commanded 31.09% of 2025 revenue, and the same is projected to grow at 5.50% over the forecast horizon, outpacing North America and Europe.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Offshore Drilling Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing jack-up demand in Middle East mega-programs | 1.2% | Middle East (UAE, Qatar, Kuwait), with spillover to India and Southeast Asia | Medium term (2-4 years) |

| Deepwater discoveries in Brazil, Guyana & Namibia | 1.5% | South America (Brazil, Guyana), Africa (Namibia, Angola) | Long term (≥4 years) |

| E&P CAPEX rebound above 2014 levels | 0.9% | Global, concentrated in Middle East, North America, Asia-Pacific | Short term (≤2 years) |

| Hybrid-powered low-carbon rigs slash fuel burn | 0.6% | Global, early adoption in North Sea, Gulf of Mexico, Brazil | Medium term (2-4 years) |

| Autonomous drilling & digital twins lift uptime | 0.5% | North America, Europe (Norway, UK), Asia-Pacific (Australia) | Medium term (2-4 years) |

| Growing demand for natural gas and developing gas infrastructure | 0.8% | Asia-Pacific (China, India, ASEAN), Middle East (Qatar), Australia | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Growing Jack-up Demand in Middle East Mega-Programs

Multi-year contracts signed by national oil companies in the Arabian Gulf keep jack-up utilization above 90% even as Saudi production cuts introduce spot-rate volatility. ADNOC’s USD 1.15 billion award for two high-specification units in May 2025, locked in fifteen-year charters and expanded the contractor’s fleet past 140 rigs, mirroring QatarEnergy’s requirement for additional capacity tied to a 126 million-tonnes LNG build-out.[1]Abu Dhabi National Oil Company, “Investor Presentation May 2025,” adnoc.ae Shelf Drilling and Borr Drilling benefit from this surge, while India’s ONGC pursues a similar long-term model in the Krishna-Godavari basin. The offshore drilling market, therefore, enjoys improved backlog visibility, though episodic oversupply remains possible whenever OPEC+ quotas constrain Saudi activity.

Deepwater Discoveries in Brazil, Guyana & Namibia

Ultra-deepwater finds exceeding 7,500 feet are redefining commercial breakevens, with Petrobras, ExxonMobil, and TotalEnergies sanctioning multi-billion-barrel fields that favor dynamic-positioning drillships. Atapu-2 and Sépia-2 anchor Transocean and Noble backlogs through the decade, while Equinor’s Bacalhau delivered first oil at sub-USD 35/bbl breakevens in 2025.[2]Petrobras, “Investor Relations Presentation 2025,” petrobras.com.br Namibia’s Orange Basin attracts early-stage capital, indicating that the offshore drilling market will lean increasingly on frontier basins for future growth.

E&P CAPEX Rebound Above 2014 Levels

Global upstream investment exceeded the prior-cycle peak in 2025 as Middle East national oil companies accounted for a record 20% share, redirecting funds from shale toward sustained offshore campaigns. Cost inflation cooled to 3% in 2025, improving project return profiles even as labor expenses rose. Independent North American producers, however, trimmed deepwater budgets in favor of the Permian, consolidating offshore drilling market demand among capital-rich majors and state-owned entities.

Hybrid-Powered “Low-Carbon” Rigs Slash Fuel Burn

Hybrid battery integration reduces fuel use by 15-25%, delivering USD 3–5 million in annual savings per rig. Transocean’s Deepwater Atlas posted a 20% fuel cut and 96% uptime in the Gulf of Mexico, while Seadrill’s Capella achieved similar gains in the North Sea.[3]Transocean Ltd., “Form 10-K 2024,” transocean.com Favorable economics and looming IMO Tier III rules accelerate adoption, giving technologically advanced contractors an edge in negotiating premium day rates.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating switch to offshore wind lease blocks | -0.7% | Europe (UK, Netherlands, Germany), North America (US East Coast), Asia-Pacific (Taiwan, Japan) | Medium term (2-4 years) |

| Volatile Brent breakevens curb FIDs | -0.5% | Global, acute in North America (Gulf of Mexico), Europe (North Sea) | Short term (≤2 years) |

| Offshore-crew shortage inflates OPEX | -0.4% | Global, most severe in North America, Europe, Australia | Medium term (2-4 years) |

| ESG-driven capital drought for newbuild rigs | -0.3% | Europe, North America, with spillover to Asia-Pacific | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Accelerating Switch to Offshore Wind Lease Blocks

Seabed acreage and heavy-lift vessels are being redirected to UK, U.S., and Dutch wind projects, tightening resource pools that once served offshore hydrocarbon campaigns. Labor premiums for crane operators and subsea technicians climbed 25-30% between 2024 and 2025, squeezing operating margins for drilling contractors.

Volatile Brent Breakevens Curb FIDs

Price swings between USD 70–90/bbl delayed marginal deepwater projects in the Gulf of Mexico and the North Sea. Operators now require multi-year price certainty to greenlight billion-dollar developments, trimming near-term rig demand even as low-breakeven South American projects proceed.[4]Chevron Corporation, “Investor Day Transcript 2025,” chevron.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Well Type: Unconventional Offshore Gains Traction

Conventional wells controlled 90.33% of the offshore drilling market share in 2025, reflecting decades of accumulated subsurface data that de-risk projects in the Gulf of Mexico, the North Sea, and offshore. Predictable geology and proven completion techniques let operators convert prospects quickly, keeping development cycles short and cash-flow visibility high. However, unconventional offshore wells are expanding at a 10.49% CAGR through 2031 as horizontal drilling and hydraulic-fracturing methods, refined onshore, migrate to shallow-water settings and unlock tight reservoirs previously viewed as non-commercial. Extended-reach and multilateral designs allow producers to tap new pay zones from existing platforms, trimming upfront capital and stretching field life. The unconventional offshore drilling market size associated with these developments, therefore, represents a growing slice of new-project sanctioning as conventional discovery rates wane and lease inventories mature.

Momentum is sharpest in basins where legacy assets offer infrastructure head starts, letting operators drill long-step-out laterals without building new hubs. BP’s “design one and build many” template for compact facilities exemplifies how simplified topsides, standardized wellhead trees, and factory-style execution lower break-evens and shorten schedules. Contractors that supply precision rotary-steerable systems, high-horsepower frac spreads, and real-time downhole telemetry stand to benefit as operators seek tighter well spacing and higher stimulated reservoir volumes. Because unconventional programs often involve a higher well count per field, service intensity rises, anchoring a durable demand stream that augments traditional exploration and appraisal work. As a result, the offshore drilling market is transitioning toward a dual-track model in which high-spec rigs chase deepwater prospects while adaptable jackups and platform rigs exploit near-field unconventional targets.

By Water Depth: Ultra-deepwater Economics Redefine Value Creation

Shallow-water wells less than 400 ft deep accounted for 51.11% of the offshore drilling market share in 2025, supported by mature infrastructure and short, two-to-three-year lead times that let operators react quickly to price swings. Saudi Aramco’s jack-up program has pushed regional utilization above 84%, preserving a large, low-cost production base even as discovery sizes decline. These projects continue to attract capital because they can be tied back to existing platforms at modest cost, yet rising depletion has forced producers to lean on infill drilling and unconventional targets to sustain output.

Ultra-deepwater campaigns beyond 1,500 m are expanding at a 9.22% CAGR through 2031 as technological advances and multi-billion-barrel finds flip the cost-of-supply curve in their favor. BP’s planned final investment decision on the 6 billion-boe Tiber discovery and TotalEnergies’ Venus success in 2,000-m water prove that breakevens can dip below USD 20 per barrel, redefining the offshore drilling market size that operators target for growth. Drillship utilization is on track to hit 97% in 2025, handing pricing power to contractors equipped with seventh-generation, dual-BOP units that can handle extreme depth and high-pressure wells. Deepwater programs in the 400-1,500 m band maintain steady activity, bridging legacy shelf projects and frontier ultra-deepwater plays while offering mid-cycle economics that diversify portfolio risk. Together, the bifurcated depth mix underscores how shallow water preserves volume leadership through efficiency, whereas ultra-deepwater now captures value leadership by pairing giant resource potential with rapidly improving technology.

By Service: Decommissioning Drives Service Mix Evolution

Exploration and development drilling delivered 40.64% of 2025 spending, buttressed by USD 214 billion of sanctioned offshore projects focused on high-return assets in Brazil, Guyana, and Namibia, where breakevens sit below USD 30 per barrel. Production drilling added steady volumes as operators pursued infill campaigns, while workover and intervention jobs kept mature fields online. Yet plug and abandonment (P&A) is the fastest-growing service line, advancing at a 10.67% CAGR through 2031 as infrastructure installed during the 1970-1990 build-out reaches end-of-life. The United Kingdom alone forecasts GBP 21 billion in decommissioning outlays this decade, prompting grants for AI-enabled planning tools and remote subsea cutting systems that can shrink project time and cost.

Saudi Arabia’s recent award to Subsea7 for well-abandonment work shows that even relatively young provinces are preparing for long-term liabilities. Regulators now demand full-scope removals and verified environmental baselines, cementing P&A as a non-discretionary spend category within the offshore drilling market size earmarked for services. Contractors that develop rigless abandonment spreads, dual-mode vessels, and in-situ pipe-cutting robotics can capture premium margins as operators prioritize risk reduction and stakeholder optics. The rising P&A backlog, therefore, rebalances the service mix, ensuring that cash flows from late-life asset retirement partially offset the cyclicality of front-end exploration drilling.

Geography Analysis

The Middle East and Africa lead the offshore drilling market with a 31.09% share and a 5.50% forecast CAGR. Long-term LNG-linked projects in Qatar, gas development in Saudi Arabia, and deepwater prospects in Nigeria and Angola underpin expansion. South America follows at roughly 22%, driven mainly by Brazil’s pre-salt and Guyana’s Stabroek Block. North America’s 18% share centers on the Gulf of Mexico, where high-pressure technology unlocks new reservoirs but competes with shale capital. Europe’s 15% share is anchored by Norwegian output, but wind-lease priority narrows hydrocarbon acreage. Asia-Pacific’s 14% stake reflects China’s Bohai Bay, India’s KG Basin, and Australia’s Scarborough gas project, each sustaining localized rig demand despite weather and logistics hurdles. These regional dynamics collectively give the offshore drilling market a balanced mix of mature and frontier opportunities.

Competitive Landscape

Transocean, Valaris, Noble, Seadrill, and COSL together control about 55% of marketed rigs, making the sector moderately concentrated. The Noble-Maersk merger created scale economies and triggered cold-stacking of inefficient units, while Transocean’s USD 7.8 billion backlog illustrates pricing power in tight segments. Technology adoption differentiates leaders: hybrid power, automation, and digital-twin systems secure premium contracts with supermajors seeking emissions cuts. Smaller challengers such as Shelf Drilling and Borr Drilling capture spot opportunities in Southeast Asia and the Middle East, but their short-term model heightens exposure to utilization swings. Taken together, competitive intensity pushes the offshore drilling market toward a higher-specification, lower-emission fleet profile.

Offshore Drilling Industry Leaders

Valaris plc

China Oilfield Services Ltd. (COSL)

Transocean Ltd.

Noble Corp.

Seadrill Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: ExxonMobil signed a USD 1.5 billion commitment for new deepwater wells offshore Nigeria, marking its largest African investment since 2019.

- April 2025: BP announced a significant discovery at its Far South prospect in the Gulf of Mexico, finding oil in high-quality Miocene reservoirs.

- March 2025: Valaris secured a two-year, USD 352 million contract for drillship VALARIS DS-10, commencing offshore West Africa in late 2026.

- February 2025: Saipem and Subsea 7 agreed on a USD 4.7 billion merger, creating an offshore services leader with 60 construction vessels.

Global Offshore Drilling Market Report Scope

Offshore drilling extracts oil or natural gas beneath the seabed in oceanic or large lake environments. It involves the exploration, drilling, and production of hydrocarbons from underwater wells located in bodies of water, typically at a considerable distance from the shoreline.

The global offshore drilling market is segmented by rig type, water depth, and geography. By rig type, the market is segmented into jack-ups, semisubmersibles, drillships, platform/barge rigs, and others. By water depth, the market is segmented into shallow water, deepwater, and ultra-deepwater drilling. The report also covers the market sizes and forecasts for the global offshore drilling market across major countries within each region. For each segment, the market sizing and forecasts have been provided on the basis of value (USD).

| Conventional |

| Unconventional |

| Shallow Water (Below 400 ft) |

| Deepwater (400 to 5,000 ft) |

| Ultra-deepwater (Above 5,000 ft) |

| Exploration and Development Drilling |

| Production/Workover |

| Plug and Abandonment |

| Subsea Support |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Norway | |

| Russia | |

| Rest of Europe | |

| Asia-Pacifc | China |

| India | |

| Thailand | |

| Vietnam | |

| Australia | |

| Rest of Asia-Pacifc | |

| South America | Brazil |

| Trinidad and Tobago | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Egypt | |

| Nigeria | |

| Angola | |

| Namibia | |

| Rest of Middle East and Africa |

| By Well Type | Conventional | |

| Unconventional | ||

| By Water Depth | Shallow Water (Below 400 ft) | |

| Deepwater (400 to 5,000 ft) | ||

| Ultra-deepwater (Above 5,000 ft) | ||

| By Service | Exploration and Development Drilling | |

| Production/Workover | ||

| Plug and Abandonment | ||

| Subsea Support | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Norway | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacifc | China | |

| India | ||

| Thailand | ||

| Vietnam | ||

| Australia | ||

| Rest of Asia-Pacifc | ||

| South America | Brazil | |

| Trinidad and Tobago | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Egypt | ||

| Nigeria | ||

| Angola | ||

| Namibia | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the offshore drilling market?

The offshore drilling market size stood at USD 32.81 billion in 2026 and is on track to reach USD 41.68 billion by 2031.

Which rig type is expanding fastest?

Drillships are growing at a 6.95% CAGR thanks to ultra-deepwater commitments in Brazil, Guyana, and Namibia.

Which region leads in offshore drilling activity?

The Middle East and Africa hold the largest share at 31.09% and are forecast to grow at 5.50% through 2031.

How are hybrid power systems affecting rig economics?

Hybrid batteries cut fuel consumption by up to 25%, saving USD 3–5 million per rig each year and meeting IMO Tier III standards.

What is the main restraint facing future offshore drilling projects?

Competition from offshore wind lease blocks is diverting vessels, labor, and seabed acreage, creating a structural supply challenge for oil and gas operators.

Page last updated on: