Saudi Arabia Fruits And Vegetables Market Analysis by Mordor Intelligence

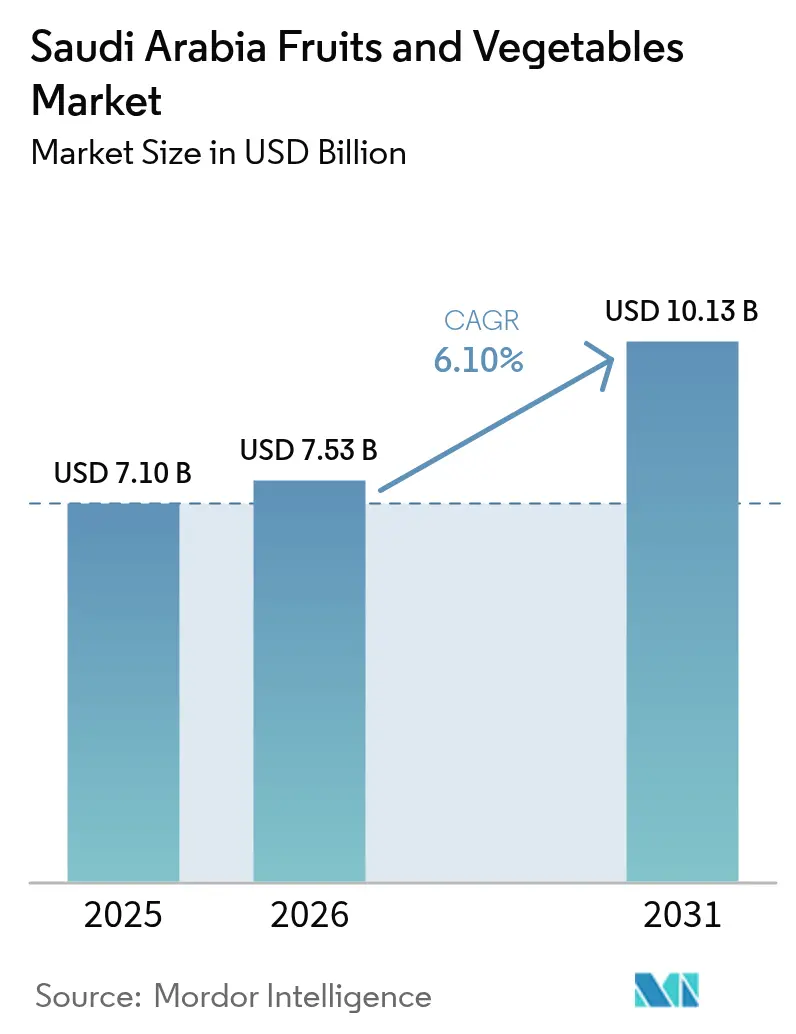

Saudi Arabia fruits and vegetables market size in 2026 is estimated at USD 7.53 billion, growing from 2025 value of USD 7.1 billion with 2031 projections showing USD 10.13 billion, growing at 6.1% CAGR over 2026-2031. With Vision 2030 food-security programs and steady population growth, 70% of residents are younger than thirty-five, driving a rising demand for fruit and vegetables. Although the Kingdom still imports about 80-85% of its fresh supply, yearly investments of SAR 20 billion (USD 5.3 billion) in controlled-environment farming, cold-chain upgrades, and desalinated-water projects are increasing domestic output and reducing post-harvest losses. Online grocery adoption, supported by a ninety-five percent smartphone penetration rate, enlarges access to premium items and accelerates market expansion. The Saudi Food and Drug Authority's enhanced regulatory framework and the Ministry of Environment, Water, and Agriculture's (MEWA's) modernization programs are reshaping supply chain dynamics while supporting food security objectives that reduce import dependency and strengthen domestic fresh produce capabilities.

Key Report Takeaways

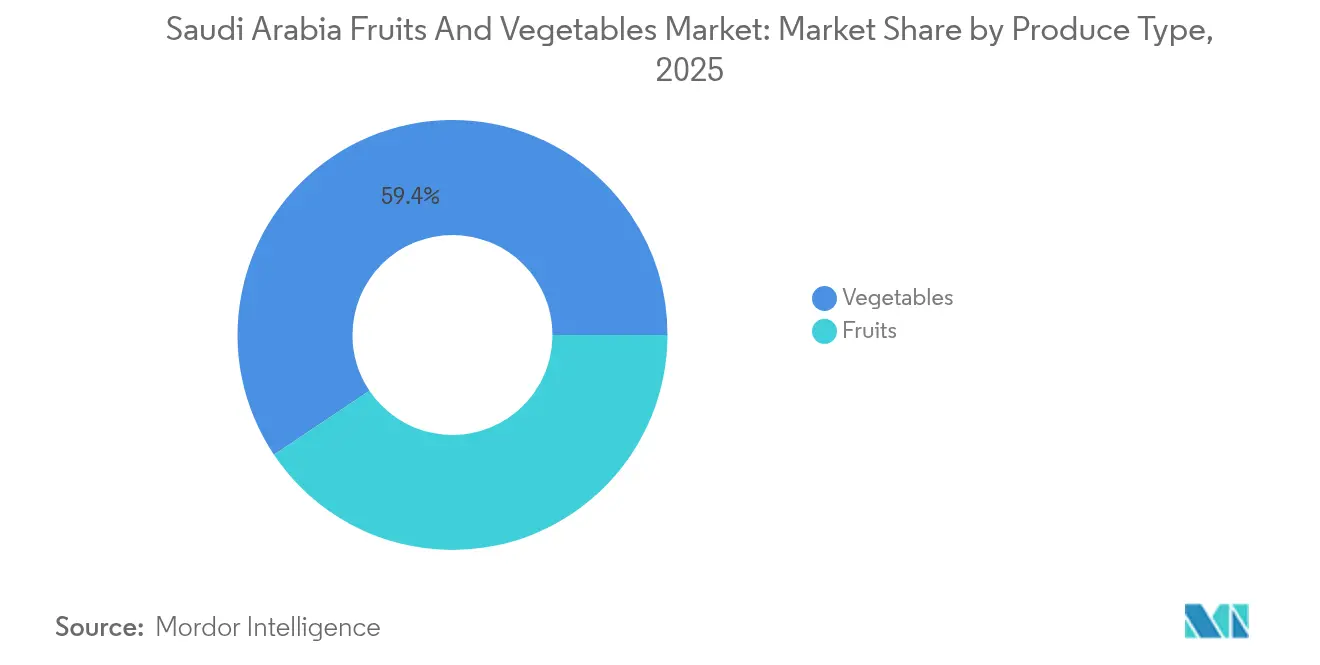

- By produce type, vegetables led with 59.40% of the Saudi Arabia fruits and vegetables market share in 2025, while the fruits segment is projected to register the fastest 6.25% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Fruits And Vegetables Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Focus | Impact Timeline |

|---|---|---|---|

| Government food-security incentives | +1.0% | Central and Eastern regions | Long term (≥ 4 years) |

| Growth of greenhouse/hydroponic farming | +0.8% | NEOM, Central, Eastern | Medium term (2-4 years) |

| Expansion of e-grocery platforms | +1.0% | Major urban centers | Short term (≤ 2 years) |

| Health-driven rise in fresh-produce intake | +0.7% | Nationwide | Medium term (2-4 years) |

| Desalinated-water projects for horticulture | +0.6% | Coastal and Red Sea zones | Long term (≥ 4 years) |

| Foreign direct investment in high-tech farms | +0.5% | Central and Eastern corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Food-Security Incentives

Vision 2030 targets call for 40% vegetable self-sufficiency by 2030. Subsidies nowadays cover half of greenhouse building costs, and low-interest loans at two percent spur technology upgrades, giving growers predictable payback horizons while anchoring raw-material supply for retailers [1]Source: Vision 2030 Council, “National Food Security Roadmap,” vision2030.gov.sa . The National Food Security Strategy prioritizes import substitution through subsidies covering 50% of greenhouse construction costs and 30% of operational expenses for the first three years, creating economic incentives that make controlled-environment agriculture financially viable for commercial fresh produce operations. The Saudi Agricultural Development Fund provides low-interest loans at 2% annually for agricultural technology adoption, compared to commercial rates of 6-8%, enabling smaller producers to access capital for modernization projects that support fresh produce self-sufficiency objectives [2]Source: Saudi Agricultural Development Fund, “Low-Interest Loan Program for Greenhouse Projects,” adf.gov.sa.

Growth of Greenhouse/Hydroponic Farming

Controlled-environment agriculture capacity in Saudi Arabia expanded by 150% during 2024, reaching 12,000 hectares of greenhouse and hydroponic facilities that enable year-round fresh produce cultivation despite extreme desert conditions. The technology delivers water efficiency gains of 90-95% compared to open-field cultivation while achieving yields 8-12 times higher per square meter, making desert agriculture economically viable for high-value fresh crops, including leafy greens, herbs, and specialty vegetables. NEOM's agricultural projects demonstrate commercial scalability, with Phase 1 facilities producing 2,000 tons annually of premium fresh vegetables using seawater-based hydroponic systems that eliminate freshwater consumption [3]Source: NEOM Company, “Seawater Hydroponic Farms Reach Phase 1 Output,” neom.com. The Saudi Standards, Metrology and Quality Organization established certification requirements for controlled-environment fresh produce in 2024, ensuring quality consistency and consumer confidence while supporting premium positioning that justifies higher production costs.

Expansion of E-Grocery Platforms

Digital grocery platforms in Saudi Arabia processed SAR 4.2 billion (USD 1.1 billion) in fresh produce sales during 2024, representing 35% annual growth as consumers embrace convenience and quality consistency that traditional retail struggles to match reliably. Nana, Noon, and Baqala apps collectively serve 8.5 million active users, with fresh produce representing 40-45% of total order value and demonstrating higher customer retention rates compared to packaged goods categories. The Saudi Communications and Information Technology Commission's e-commerce facilitation framework, implemented in 2024, provides regulatory support for digital payment systems and consumer protection measures that build trust in online fresh produce purchasing. Two-hour delivery windows and temperature-verified logistics encourage larger baskets and premium selections, driving online channels deeper into mainstream purchasing.

Health-Driven Rise in Fresh-Produce Intake

Health-conscious consumption patterns are driving 20-25% annual growth in organic and premium fresh produce categories, as Saudi consumers increasingly prioritize nutritional value over price considerations in food purchasing decisions. The Ministry of Health's National Nutrition Strategy, launched in 2024, promotes fresh fruit and vegetable consumption through public awareness campaigns that specifically target diabetes and cardiovascular disease prevention among Saudi nationals. Per capita fresh produce consumption increased from 180 kg annually in 2019 to 220 kg in 2024, with the highest growth in leafy greens, berries, and citrus fruits that align with wellness trends and dietary recommendations from healthcare professionals. Premium supermarket chains report 40-60% growth in organic fresh produce sales, while specialty health food stores are expanding rapidly in urban centers where affluent consumers seek certified organic, locally-grown, and imported specialty varieties.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Focus | Impact Timeline |

|---|---|---|---|

| High capital cost of climate-controlled facilities | -0.8% | Nationwide | Long term (≥ 4 years) |

| Extreme summer temperatures | -0.7% | Central and Northern regions | Short term (≤ 2 years) |

| Dependence on imported seeds and inputs | -0.5% | Nationwide | Medium term (2-4 years) |

| Cold-chain infrastructure gaps | -0.4% | Northern and Southern provinces | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of Climate-Controlled Facilities

Advanced greenhouse and hydroponic systems require initial investments of USD 1-2 million per hectare, creating significant barriers for small and medium-scale producers seeking to adopt controlled-environment fresh produce technologies. The capital intensity particularly affects traditional farmers who lack access to commercial financing or collateral requirements for agricultural development loans, limiting participation in government modernization programs despite available subsidies for fresh produce cultivation. Operational complexity of advanced systems necessitates skilled technicians and ongoing maintenance contracts that add 15-20% to annual operating costs, making return on investment calculations challenging for producers without established market access and premium pricing capabilities for fresh produce.

Extreme Summer Temperatures

Summer temperatures exceeding 45°C for 4-5 months annually increase cooling costs by 40-60% for controlled-environment fresh produce facilities while creating stress conditions that reduce crop yields and extend growing cycles. Open-field cultivation becomes virtually impossible during peak summer months, forcing producers to concentrate production in cooler periods and rely on imports or stored inventory to maintain year-round fresh supply consistency. The extreme climate conditions particularly affect leafy greens and herbs that are sensitive to temperature fluctuations, limiting crop diversity and forcing specialization in heat-tolerant varieties that do not align with consumer preferences or premium market opportunities for fresh produce.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Produce Type: Vegetables Retain Lead While Fruits Accelerate

Vegetables accounted for 59.40% of the Saudi Arabia fruits and vegetables market share in 2025, confirming their role as everyday staples across Saudi meal planning. Fruits held the remaining 40.60% yet are projected to advance at a 6.25% CAGR with imported berries, citrus, and exotic varieties driving premium spending. Domestic growers focus on tomatoes, cucumbers, and peppers for consistent turnover, while controlled-environment farms add leafy greens and herbs that carry a higher margin. Retailers widen assortments during cooler months when outdoor events lift snacking occasions, and they rely on imports during summer heat to protect shelf availability. Government targets that push vegetable self-sufficiency to 40% by 2030 ensure investment momentum for greenhouse acreage.

Fruits benefit from health campaigns that link antioxidant intake to wellness, lifting impulse purchases despite price points that sit three or four times above local apples. This balanced mix underpins the overall fruits and vegetables market size and cushions seasonal volatility. Price sensitivity shapes vegetable promotions, loyalty shifts when consumers encounter convenient prepared packs and recipe-ready mixes. Fruits increasingly appear in gifting boxes for Eid and corporate hospitality, reinforcing status appeal. Domestic raspberry trials inside cooled tunnels point to a future where local fruit supply can chip away at air-freighted imports. Segment players who combine reliable volume vegetables with niche high-value fruits diversify revenue and elevate brand equity within the growing fruits and vegetables market.

Geography Analysis

The central region dominates with a significant market share in 2025, driven by Riyadh's concentration of retail infrastructure, government institutions, and high-income demographics that support premium fresh produce consumption patterns. The region benefits from strategic location advantages for import distribution and domestic production access, while hosting headquarters for major retail chains, including Al-Othaim Markets and Panda, that drive supply chain optimization and market development initiatives. The growth reflects steady urbanization and income growth, supported by Vision 2030 economic diversification projects that create employment opportunities and consumer spending power. The central region's market leadership stems from infrastructure advantages, including King Khalid International Airport's cargo facilities and extensive highway networks that enable efficient distribution to other regions while maintaining product quality and competitive pricing.

The eastern province emerges as a significant fastest-growing region through 2031, benefiting from industrial diversification, port access through Dammam and Jubail, and the petrochemical sector employment that supports higher disposable incomes and premium food consumption. The region's growth acceleration reflects economic transformation beyond oil dependency, with manufacturing and logistics sectors creating employment opportunities that drive consumer spending on fresh produce and specialty food categories. Major retail investments, including LULU Group's distribution center expansion and Tamimi Markets' store network growth, are capturing market share through improved product availability and competitive pricing that appeals to price-sensitive consumers. The eastern province's strategic advantages include proximity to GCC markets for re-export opportunities and established cold-chain infrastructure that supports import distribution and quality maintenance across the Kingdom.

The western region, encompassing Makkah and Madinah, maintains steady growth, driven by religious tourism, port access through Jeddah, and cultural diversity that creates demand for specialty and international produce varieties. The region benefits from year-round tourism flow that supports foodservice demand and premium retail opportunities, while hosting significant expatriate populations who seek imported products from their home countries. Jeddah's position as the Kingdom's commercial capital creates opportunities for premium positioning and specialty retail formats that serve affluent consumers and international business communities with higher quality expectations and willingness to pay premium prices. The western region's market dynamics reflect cultural sophistication and international exposure that drive demand for organic, imported, and specialty produce categories that command higher margins compared to traditional retail formats in other regions.

Regulatory Landscape

Saudi Arabia regulates fresh fruits and vegetables across production and trade through the Ministry of Environment, Water and Agriculture (MEWA) and the Saudi Food and Drug Authority (SFDA). Importers typically use an electronic import license process via MEWA, and consignments must clear SFDA food requirements, including mandatory documentation such as phytosanitary certificates for fresh fruits and vegetables.

On standards and compliance, imported fresh produce must meet GCC technical regulations, including general requirements for fresh fruits and vegetables and labeling rules for prepackaged foodstuffs, along with specific requirements for areas such as irradiation and genetically modified unprocessed agricultural products. Border measures also shape landed costs, with a general 5% import duty applied to food products, while selected agricultural items may carry higher protective duties (up to 40% ad valorem). This policy mix aligns with Vision 2030 food-security programs aimed at expanding domestic production.

Value Chain Analysis

The value chain covers input suppliers (seed, substrates, nutrients, crop protection, greenhouse structures, irrigation and climate-control equipment), primary production (open-field farms and controlled-environment agriculture), aggregation, packing and grading, cold storage, wholesale markets, and distribution to modern retail, traditional trade, foodservice, and e-grocery channels that have expanded access to fresh items. MEWA oversees sector development and market organization, including programs run through its General Department of Marketing and Cooperatives to improve market access and marketing services for farmers.

Domestic supply is increasingly shaped by protected cultivation alongside traditional field production. Government statistics for 2024 point to open-field vegetable production of about 2,745 thousand tons and greenhouse vegetable production of 797 thousand tons, supported by more than 121 thousand greenhouses, reinforcing the scaling role of controlled-environment agriculture. Financing and capability-building remain central to upstream and midstream upgrades, with the Agricultural Development Fund (ADF) providing soft loans for projects such as greenhouses and cold storage, and Reef Saudi supporting fruit cultivation and smallholder integration. Digitization is also entering the chain, as MEWA signed an August 2024 agreement with Al-Riyadh Development Company to launch a digital portal for the vegetable and fruit market to automate entry and improve tracking, along with farmer-to-market connections.

Market Opportunities and Future Outlook

Opportunities center on import substitution and quality consistency in premium, temperature-sensitive categories that fit controlled-environment agriculture. These opportunities are reinforced by ongoing financing and specific initiatives. Large-scale greenhouse investments create demand for turnkey greenhouse systems, climate control, hydroponics, substrates, seeds, and agronomy services, as well as packhouses and cold-chain operators that support year-round availability. The Agricultural Development Fund reported loan approvals reaching about SAR 6.47 billion by end-2025 for agricultural projects linked to national self-sufficiency objectives, indicating continued capital access as producers and logistics players expand.

Commercial projects and government platforms offer near-term entry points across regions. Dava Agricultural announced in May 2026 a Taif mega-project focused on 350 hectares of high-tech glass greenhouses, highlighting the need for engineering, construction, and operational know-how for protected cultivation at scale. MEWA also continues to list integrated agricultural city investment opportunities through the Furas platform, covering vegetables, crops, and fruit trees and widening the pipeline for developers and service providers that can bundle production with packing, labs, and market infrastructure. Downstream, the spread of e-grocery and temperature-verified delivery is creating scope for differentiated offerings such as grading, private label, traceability, and ready-to-eat or recipe-ready packs that can reduce shrink and support premiumization.

Recent Industry Developments

- May 2026: Dava Agricultural announced a Taif mega-project centered on 350 hectares of high-tech glass greenhouses to scale domestic fresh produce production. The plan emphasizes a shift toward protected cultivation in response to climate constraints and water efficiency requirements, creating demand for greenhouse engineering, inputs, and specialized operations across the Kingdom.

- April 2026: The Agricultural Development Fund reported that loan approvals for agricultural projects reached about SAR 6.47 billion by the end of 2025 as part of efforts to bolster national food self-sufficiency. Broader financing availability supports expansion in greenhouses, cold storage, and other post-harvest infrastructure, which affects fresh produce availability and quality.

- August 2024: The Ministry of Environment, Water and Agriculture signed an agreement with Al-Riyadh Development Company to launch a digital portal for the vegetable and fruit market. By automating market entry and improving supply chain tracking, the initiative supports price discovery and traceability while tightening links between farmers and wholesale market demand.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as the value of fresh fruits and fresh vegetables consumed in Saudi Arabia, with sizing supported by domestic production, trade flows, and price signals to reflect the fresh produce economy in the country.

Scope exclusions: Processed forms such as frozen, dried, canned, and juices are excluded from this market sizing.

Segmentation Overview

- By Produce Type (Production Analysis (Volume), Consumption Analysis (Volume and Value), Import Analysis (Volume and Value), Export Analysis (Volume and Value), and Price Trend Analysis)

- Fruits

- Vegetables

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started with getting the hard, public numbers that can anchor fresh produce demand in Saudi Arabia, and then building context around them. For example, we used official agriculture and food-balance style statistics, customs import and export series, and price publications from government portals, along with datasets from organizations such as FAOSTAT and UN Comtrade.

To make the desk inputs practical for a market model, we also reviewed public materials such as company annual reports, investor presentations, association websites, and reputable press coverage on cold chain, retail formats, and food security programs. In parallel, paid database subscriptions for company financials and intelligence, shipment-level trade visibility, and patents were used selectively to cross-check scale, product flows, and technology adoption signals. The desk sources listed are illustrative only, and many other public and paid references were used during data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to pressure-test what the desk numbers implied, especially where official series lag or where product definitions get mixed in day to day trade language. We spoke with a balanced mix of growers, importers, distributors, wholesalers, and modern retail stakeholders across key demand centers, and the discussions helped us confirm price formation, seasonality, and what share is truly sold as fresh.

To keep assumptions grounded, interviews were also used to validate trade dependence, local production ramp-up in protected farming, and the typical wastage and shrink seen along the cold chain, which are hard to infer from public tables alone.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 17% | |

| Mid tier: 55% | Functional/Unit leaders: 28% | |

| Smaller Players: 18% | Managers: 55% |

Market-Sizing & Forecasting

Sizing was built using a top-down structure where production and trade data reconstruct the fresh supply available to the country, which is then translated into market value using observed price bands and mix assumptions. Since fresh fruits and vegetables move through different routes, the model separates domestic output from imports and then adjusts for export outflows, distribution losses, and retail shrink before value is computed.

A selective bottom-up view was used as a check, mainly through sampled price per kilogram by commodity group multiplied by estimated volumes moving through key channels, followed by reasonableness checks using importer and distributor scale. Inputs that mattered most included import volumes by major fresh categories, average unit values from customs declarations, local harvested output trends under protected cultivation, seasonal price swings, and the shift in sales between traditional markets and organized retail.

For forecasting, scenario analysis was used because supply security actions, water constraints, and investment pace can change trajectories quickly. The base case uses expert-agreed assumptions on local production growth, import dependency, and price progression, and then stress tests are run for shocks in logistics costs, yield variability, and consumer demand changes. Where bottom-up inputs were missing for smaller categories, gaps were handled through proxy pricing and mix ratios that were confirmed during interviews and kept consistent with official totals.

Data Validation & Update Cycle

Validation was done in layers so that one data series did not drive the entire outcome. Outputs were checked against independent signals such as per-capita consumption direction, import dependency ranges discussed by trade participants, and whether price trends align with observed seasonal patterns and supply constraints.

Anomaly flags were reviewed by an analyst not involved in the first build, and outliers were either explained with a clear event driver or corrected with refreshed inputs. When large variances showed up between desk indicators and interview feedback, respondents were re-contacted and assumptions were revised before sign-off. Reports are refreshed annually, and material events trigger interim updates, followed by a final pre-delivery pass so clients receive the latest view.

Mordor Intelligence's the Kingdom of Saudi Arabia Fruits and Vegetables Market Size Compared With Other Published Estimates

Published market values for Saudi Arabia fruits and vegetables often do not match because the scope lines are drawn differently and the underlying price and volume logic is not always the same. Differences typically come from whether the estimate is limited to fresh only, whether trade is treated as a core driver or just a side note, and how fast price assumptions are allowed to move year to year.

In this study, the number is kept tied to the fresh demand pool by building from production plus imports minus exports and then applying realistic price bands, while some other sources appear to blend in frozen or dried forms, use a different base year, or rely on high-level revenue splits that are not reconciled to customs and output series. Currency timing and update cadence can also shift the headline value when inflation and retail pricing change quickly.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 7.53 B (2026) | |

| Global Consultancy A | USD 6.50 B (2024) | Uses an earlier base year and appears to present a broader fruits and vegetables revenue view without clearly separating fresh-only scope from adjacent processed forms, which can shift the total when compared on a like-for-like year. |

| Regional Consultancy B | USD 2.20 B (2023) | Reports a much smaller figure that looks closer to a narrower definition or partial channel coverage, and its inclusion of fresh, dried, and frozen as types suggests the value pool is framed differently than a fresh-only market tied to trade and production totals. |

The table shows that the spread is mainly explained by scope and timing rather than one single assumption. When fresh-only is enforced, and when import and export volumes are reconciled to price bands and loss factors, the market value trends stay consistent with observable supply and demand signals, which is the treatment applied here by Mordor Intelligence.

Key Questions Answered in the Report

How large is the Saudi Arabia fruits and vegetables market?

The market was valued at USD 7.53 billion in 2026 and is projected to reach USD 10.13 billion by 2031.

Which produce type category holds the largest share in 2025?

Vegetables lead with 59.40% of the Saudi Arabia fruits and vegetables market share in 2025.

How fast is the fruits segment anticipated to grow?

The fruits are projected to post a 6.25% CAGR through 2031.

How strict are Saudi import rules for fresh produce?

The Saudi Food and Drug Authority mandates full traceability and tight residue limits, raising quality standards for all suppliers.

Page last updated on: