Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

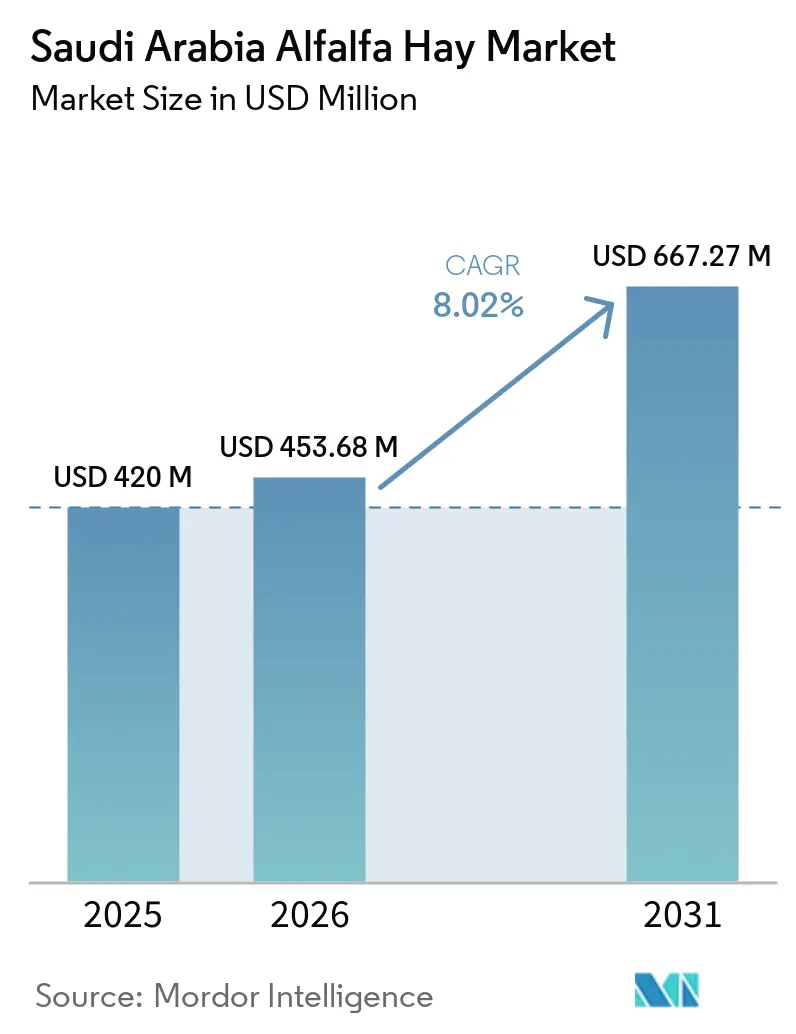

| Base Year Market Size (2025) | USD 420 Million |

| Market Size (2026) | USD 453.68 Million |

| Market Size (2031) | USD 667.27 Million |

| Growth Rate (2026 - 2031) | 8.02% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Alfalfa Hay Market Analysis by Mordor Intelligence

The Saudi Arabia alfalfa hay market size in 2026 is estimated at USD 453.68 million, growing from 2025 value of USD 420 million with 2031 projections showing USD 667.27 million, growing at 8.02% CAGR over 2026-2031. Robust livestock expansion, Vision 2030 policy shifts, and steady capital inflows position the country as a pivotal hub in the global forage trade. The 2018 prohibition on water-intensive green fodder accelerated import dependence, making the Kingdom the second-largest buyer of United States alfalfa in 2024[1]Source: Hay & Forage, “Hay exports tumbled in 2023,” hayandforage.com. Simultaneously, the Agricultural Development Fund’s SAR 1.5 billion (USD 0.40 billion) financing window signals strong state support for modern feed technologies. Shipping investments at Jeddah, Dammam, and King Abdullah ports improve handling efficiency, while hydroponic systems pioneer water-smart production that uses 48 times less water than field cultivation. Volatile global hay prices, however, expose import-heavy buyers to cost swings that fell from USD 288 per metric tons in April 2023 to USD 165 in November 2024.

Key Report Takeaways

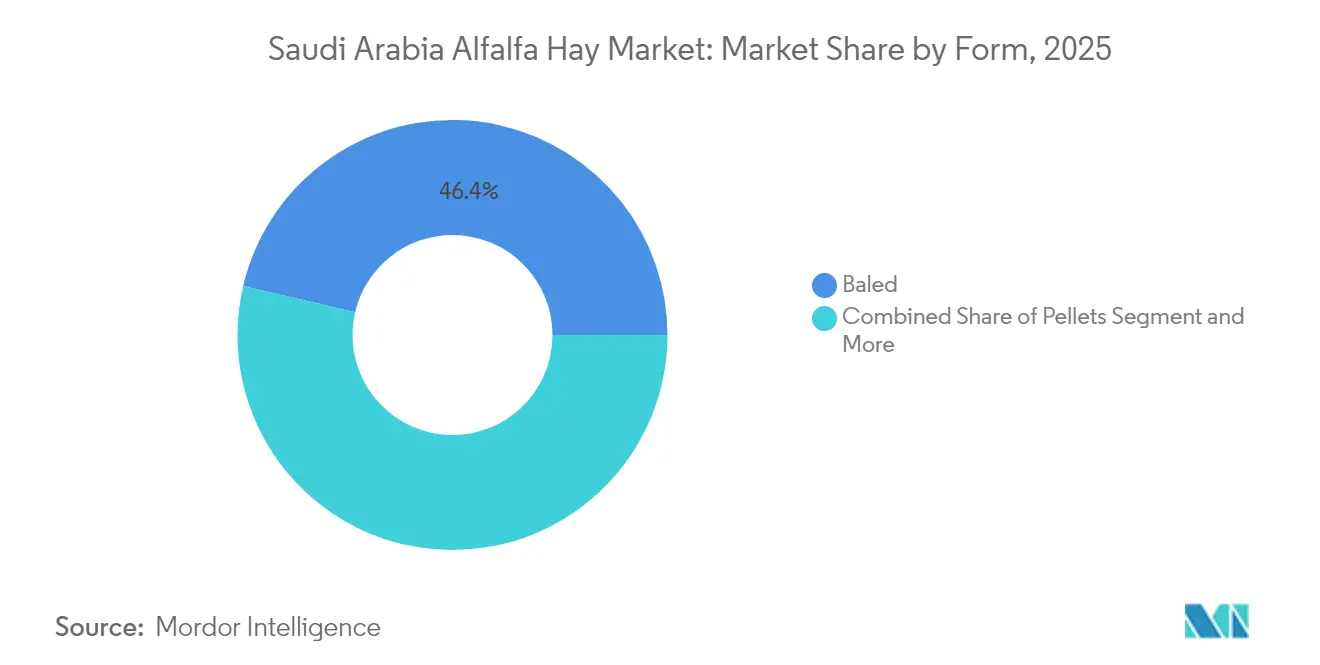

- By form, baled products held 46.35% of Saudi Arabia alfalfa hay market share in 2025, while pellets are advancing at a 10.28% CAGR through 2031.

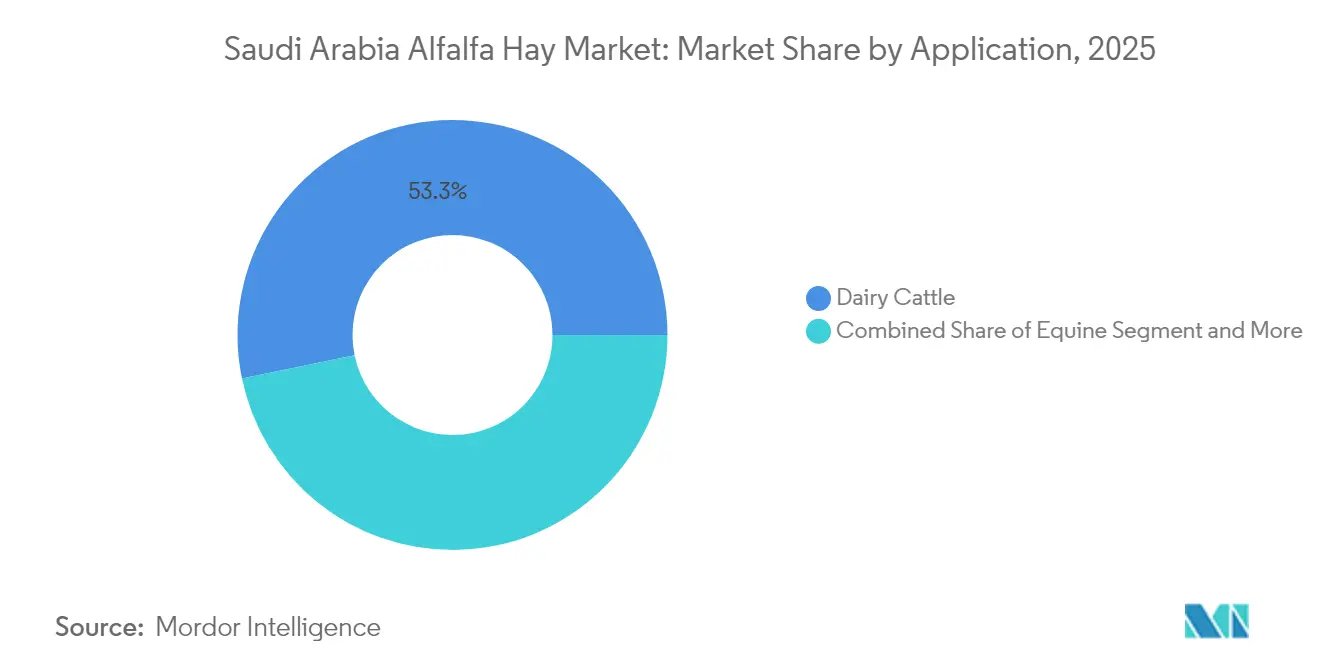

- By application, dairy operations captured 53.25% of the Saudi Arabia alfalfa hay market size in 2025 and camel and equine demand is projected to grow at an 11.63% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Alfalfa Hay Market Trends and Insights

Drivers Impact Analysis*

| Driver | ~ ( %) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing dairy industry feed demand | +2.1% | Al-Kharj and Eastern Province | Medium term (2-4 years) |

| Government initiatives for fodder self-sufficiency | +1.8% | Hail, Qassim, Al-Jawf | Long term (≥ 4 years) |

| Increasing adoption of hydroponic alfalfa cultivation | +1.2% | Coastal and NEOM corridor | Long term (≥ 4 years) |

| Rising imports of high-protein hay | +1.5% | Jeddah, Dammam, King Abdullah Port | Short term (≤ 2 years) |

| Water-footprint regulations shifting crop choices | +0.9% | Riyadh and central zones | Medium term (2-4 years) |

| Expanding camel-racing demand for premium forage | +0.7% | Riyadh and northern racing centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Dairy Industry Feed Demand

Rapid herd expansion has made integrated farms such as Al Safi a 170 million-liter annual producer that keeps 50,000 Holstein-Friesian cows [3]Source: Ruminants, “World’s largest integrated dairy farm: a look at innovation and scale,” ruminants.ceva.pro. Higher-protein rations dictate premium forage procurement and reinforce long-term supply contracts in the Saudi Arabia alfalfa hay market. Almarai’s vertical model secures imports through dedicated United States partnerships, shielding milk producers from price shocks. As milk self-sufficiency was achieved in 2023, additional capacity now targets value-added exports to GCC neighbors. Precision feeding programs that optimize conversion efficiency continue to lock in steady offtake, anchoring the Saudi Arabia alfalfa hay market through 2030.

Government Initiatives for Fodder Self-Sufficiency

SALIC channels sovereign capital into farmland in Canada, Australia, Brazil, and Ukraine, diversifying import routes while boosting domestic hydroponic pilots. The Agricultural Development Fund earmarked SAR 1.5 billion (USD 0.40 billion) for water-efficient projects, lowering entry barriers for small growers. Licensing rules cap individual wheat or alfalfa plots at 50 hectares, creating planned rotation cycles that protect aquifers. Vision 2030 also spawned public-private desalination ventures that pair renewable energy with greenhouse irrigation, reinforcing fodder autonomy. These initiatives are supporting the modernization of Saudi Arabia Agriculture by encouraging water-efficient farming practices, biotechnology adoption, and sustainable forage production. The National Biotechnology Strategy rolled out in March 2024 targets crop optimization that could raise protein yields by 15% [4]Source: Saudi Press Agency, “Unleashing Saudi Arabia’s Potential, HRH the Crown Prince Launches National Biotechnology Strategy,” spa.gov.sa.

Increasing Adoption of Hydroponic Alfalfa Cultivation

Controlled-environment acreage rose 58% in five years to reach 407,000 metric tons by 2024. Hydroponic water use of 2.83 m³ per metric tons compares favorably to 117 m³ in open fields. The NEOM Investment Fund teamed with Liberation Labs to explore precision fermentation feed options that complement hydroponic roughage. Red Sea studies prove saline-adapted crops can thrive at 100% seawater salinity without yield loss. Estidamah’s SAR 100 million (USD 26.7 million) vertical farming program validates the economic case for integrating hydroponics and desalination.

Water-Footprint Regulations Shifting Crop Choices

Agriculture consumes 80% of national water, while aquifer recharge is only 0.17%. The National Water Strategy mandates 90% desalination usage by 2030, raising on-farm pumping costs and favoring low-water crops. Farmers that exceed license quotas face fines and forced shutdowns, pushing many to stop green-fodder planting. Feedlots increasingly purchase imported pellets to avoid compliance hurdles, bolstering processed forage demand in the Saudi Arabia alfalfa hay market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Water scarcity and irrigation restrictions | -1.9% | National, acute in Riyadh | Long term (≥ 4 years) |

| Volatile global alfalfa prices | -1.3% | Import-dependent port zones | Short term (≤ 2 years) |

| Limited local processing infrastructure | -0.8% | Rural production clusters | Medium term (2-4 years) |

| Bio-security risks from imported pests | -0.5% | Border inspection points | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Water Scarcity and Irrigation Restrictions

Groundwater supplies over 90% of farm water, yet aquifers such as Wasia-Biyadh are declining rapidly. The licensing cap of 50 hectares per farmer restrains expansion, and metering systems impose additional operating costs. Desalination investments compete for state funds with agriculture, prolonging reliance on imports within the Saudi Arabia alfalfa hay market. Regulatory enforcement through groundwater licensing, metering systems, and hundreds of observation wells creates compliance costs and operational constraints for alfalfa producers dependent on aquifer extraction.

Limited Local Processing Infrastructure

Only a handful of pelletizing units operate at scale, dominated by ARASCO’s 4.5 million metric tons feed complex. Inland livestock producers incur higher haulage for processed forms, discouraging pellet uptake. Capital needs for high-capacity dehydrators remain a barrier for new entrants in the Saudi Arabia alfalfa hay market. The Agricultural Development Fund's financing programs target processing infrastructure development, but capital requirements for modern dehydration and pelletizing equipment create barriers for smaller regional processors. Limited cold storage and controlled-atmosphere facilities compromise quality preservation during the Kingdom's extreme summer temperatures, reducing shelf life and nutritional value of processed alfalfa products compared to international standards.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Pellets Drive Processing Innovation

Baled forage represented 46.35% of the Saudi Arabia alfalfa hay market share in 2025, underscoring long-standing logistics built around bulk loading. Pellets, however, are forecast to post a 10.28% CAGR, supported by feedlot automation that favors uniform particle size and reduced storage footprints. Pellets also mitigate post-harvest losses that can reach 8% in high-humidity summers, creating quantifiable savings for desert farms. Processing leaders like ARASCO scale pellet output to 4.5 million metric tons, lowering unit costs and ensuring nationwide availability. Importers collaborate with Spanish and United States suppliers on nutrient-dense pellet blends that align with dairy protein targets. Bale usage is anticipated to shrink in remote governorates where transport premiums make dense products more economical. Cubes stay niche, favored by equine owners seeking slow-chew formats that aid digestion.

Operating data indicate that pellet durability maintains 94% of original protein levels after three months of warehouse storage, outperforming baled hay by seven percentage points, an attribute that reinforces pellet momentum in the Saudi Arabia alfalfa hay market.

By Application: Camel Racing Premiumization

Dairy herds captured 53.25% of the Saudi Arabia alfalfa hay market size in 2025 through high-volume offtake, and their share is projected to stay dominant as self-sufficiency programs broaden milk output. Integrated players like Almarai and Al Safi combine forward contracting and freight hedging to guarantee year-round supply. Poultry, sheep, and goat operations contribute steady but smaller demand streams, often relying on lower-grade baled material blended into compound feeds.

Camel and equine use is set to surge at an 11.63% CAGR. The Camel Club’s prize money, now over SAR 200 million (USD 53.3 million), supports commercial ranches that upgrade to pellet diets for performance gains. Veterinary studies report that lucerne raises camel milk protein by 12%, reinforcing preference for premium forage. Equine clubs in Riyadh and Qassim increasingly source low-dust cubes to minimize respiratory issues, a micro-segment that could evolve into a branded feed line over the forecast horizon.

Geography Analysis

The central cluster around Riyadh and Al-Kharj concentrates the highest dairy densities and thus consumes the most imported alfalfa. These areas rely heavily on road freight from Dammam Port, elevating costs and encouraging pellet adoption that optimizes load weight. Eastern Province operators benefit from direct port storage and can bargain for better landed prices, preserving the Saudi Arabia alfalfa hay market’s coastal-inland price gradient.

Western coastal zones leverage Jeddah and King Abdullah ports, where new pallet guidelines streamline discharge times by 18%. NEOM and Red Sea corridor projects introduce large-scale controlled-environment agriculture that promises partial substitution of imports with hydroponic output. Research stations along the coast trial seawater irrigation crops, signaling future supply diversification. Northern governorates such as Hail and Al-Jawf obtain cultivation licenses for up to 50 hectares of alfalfa, yet water limits curb scalability. Processed pellet transport to these interior zones carries a 14% freight premium over baled imports landed at Jeddah, fostering localized pellet plants under consideration by regional investors. As the government offers concessional loans to rural processors, a gradual dispersion of value-added capacity is anticipated, reshaping the geographic pattern of the Saudi Arabia alfalfa hay market.

Competitive Landscape

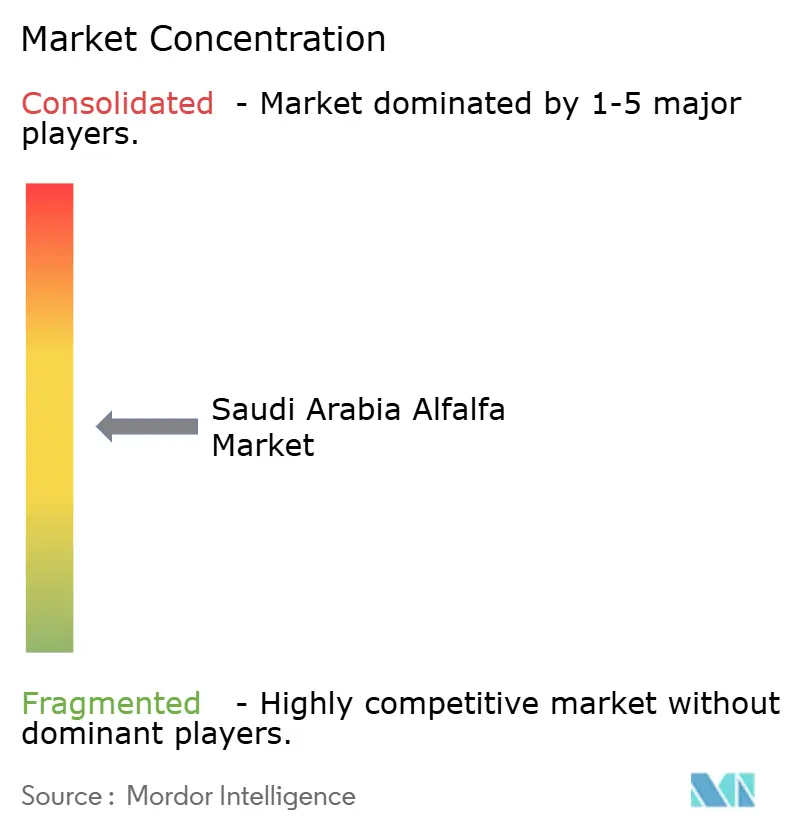

The Saudi Arabia alfalfa hay market is moderately concentrated. Al Dahra, Alfeed, Alfalfa Monegros, TADCO, and Nafosa are some of the key players catering to the Saudi Arabia alfalfa hay market. Al Dahra leads via vertically integrated farms in Saudi Arabia and the United States, ensuring supply continuity despite trade volatility. Almarai leverages captive dairy demand and dedicated shipping charters to safeguard procurement.

Strategic emphasis is shifting toward supply chain resilience. Al Dahra’s partnership with ADQ unlocks fresh capital for pellet plant upgrades. Almarai invests in data-driven nutrition models that predict protein deficits and automatically trigger purchase orders.

Emerging threats include precision fermentation ventures such as Liberation Labs, which could provide amino acid concentrates that replace part of the forage protein. Small regional processors supported by SAR 200 million (USD 53.3 million) in subsidized loans are likely to capture niche segments for cube products. Overall, rivalry is projected to intensify, particularly around processed forms where economies of scale lower the per-metric tons cost.

Saudi Arabia Alfalfa Hay Industry Leaders

Al Dahra ACX, Inc

Alfeed

Alfalfa Monegros

TADCO

Nafosa(Grupo Osés)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Tanmiah Food signed with Chengdu Design and Research Institute to build 100 modern broiler houses across Saudi Arabia in a SAR 165 million project scheduled for completion by December 2026, increasing domestic poultry production and feed demand, ultimately leading to increased demand for alfala feed in the country.

- February 2025: Balady Poultry unveiled a five-year growth plan including USD 304 million investment to build new slaughterhouse, processing facility, and hatcheries, funded through the Saudi Agricultural Development Fund and commercial loans, directly impacting the alfalfa demand in the country.

- May 2024: Almarai completed the acquisition of Etmam Logistics to strengthen supply chain capabilities and reduce distribution costs for dairy operations, indirectly supporting more efficient forage procurement and handling systems. The vertical integration strategy aims to improve margins and service quality across the dairy value chain.

Saudi Arabia Alfalfa Hay Market Report Scope

Alfalfa, popularly known as lucerne, is an important forage crop widely grown for hay, pasturage, and silage. Alfalfa hay is very nutritious and palatable, high in protein, minerals, and vitamins. The Saudi Arabia alfalfa hay market includes production analysis (volume), consumption analysis (value and volume), export analysis (value and volume), import analysis (value and volume), and price trend analysis. The report offers the market size and forecasts in terms of value (USD) and volume (metric tons) for the segments mentioned above.

By Form

| Baled |

| Pellets |

| Cubes |

By Application

| Dairy |

| Camel and Equine |

| Poultry |

| Other Livestock |

| By Form | Baled |

| Pellets | |

| Cubes | |

| By Application | Dairy |

| Camel and Equine | |

| Poultry | |

| Other Livestock |

Key Questions Answered in the Report

How large is the Saudi Arabia alfalfa hay market in 2026?

The market is valued at USD 453.68 million in 2026 and is projected to rise to USD 667.27 million by 2031.

How fast is the market growing?

It is advancing at an 8.02% CAGR over 2026-2031.

Which form of alfalfa is expanding the fastest?

Pellets are forecast to grow at a 10.28% CAGR due to storage and handling efficiencies.

Why is camel feed demand rising?

Government support for camel racing and herd expansion is lifting premium forage requirements at an 11.63% CAGR.

Page last updated on: