Qatar Agriculture Market Analysis by Mordor Intelligence

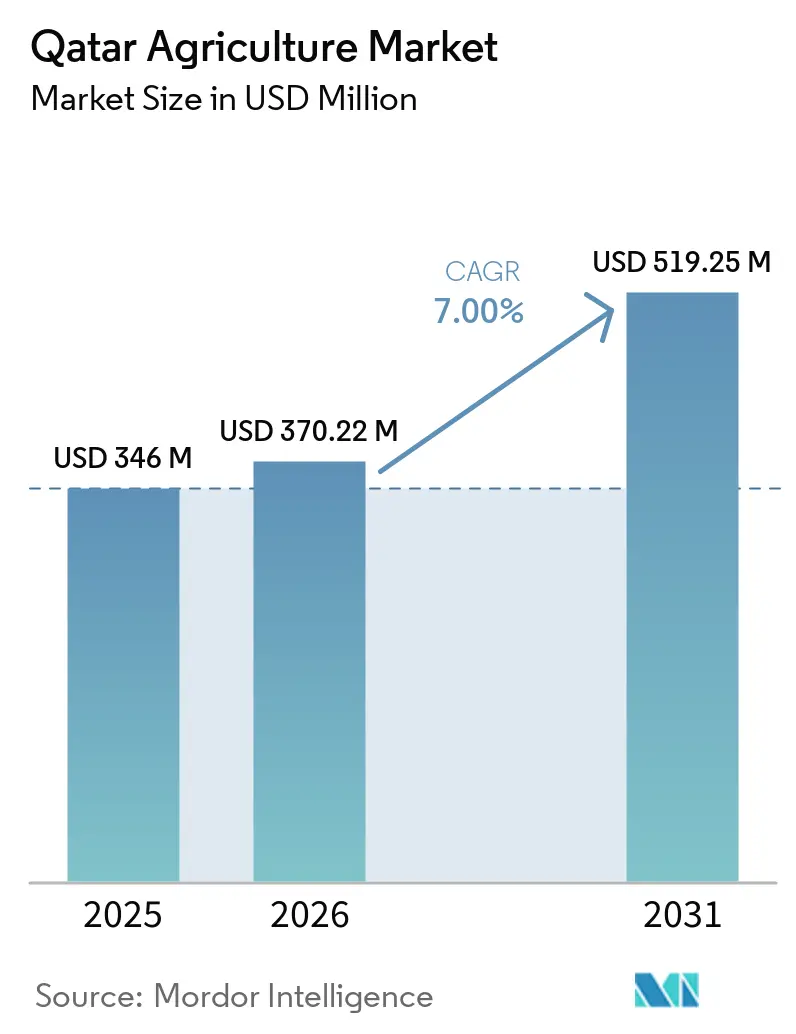

The Qatar agriculture market size was valued at USD 346 million in 2025 and is estimated to grow from USD 370.2 million in 2026 to USD 519.2 million by 2031, at a CAGR of 7% during the forecast period (2026-2031). Robust policy support, greenhouse modernization, and rising venture investment have converted the Qatar agriculture market from an import-heavy system into one that increasingly favors domestic output. A decisive pivot toward food sovereignty spurred record spending on climate-controlled agriculture, water-efficient irrigation, and solar power integration. Consumers now demand fresher produce, traceable quality, and year-round availability, encouraging operators to adopt vertical and container farming. Sovereign-wealth funding and low-interest loans from Qatar Development Bank continue to lower the cost of advanced greenhouses, creating a virtuous cycle of technology adoption and productivity improvement.

Key Report Takeaways

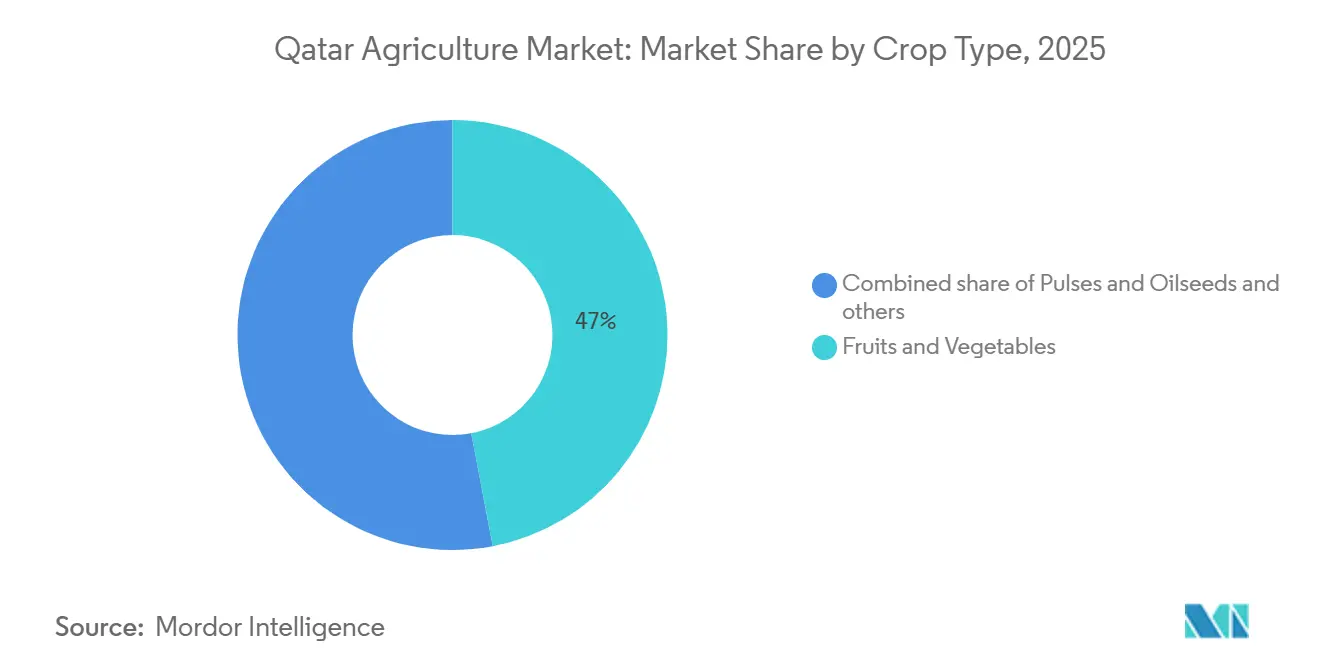

- By crop type, fruits and vegetables captured 47% of the Qatar agriculture market share in 2025, while pulses and oilseeds post the fastest growth at a 9% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Qatar Agriculture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Population Growth Intensifying Food Demand | +1.5% | Doha, Al Rayyan, Al Wakrah | Short term (≤ 2 years) |

| Extensive Government Land-Lease Incentives for Greenhouses | +1.2% | Al Khor, Al Shamal | Medium term (2-4 years) |

| Water-Efficient Hydroponics and Aquaponics Adoption | +1.8% | National, led by Doha | Medium term (2-4 years) |

| Subsidized Photovoltaic Irrigation Systems | +0.9% | Northern agricultural zones | Long term (≥ 4 years) |

| Food-Security Clauses in Sovereign-Wealth Investment Strategy | +0.7% | Domestic and offshore | Long term (≥ 4 years) |

| Blockchain-Enabled Wholesale Market Digitization Platform | +0.5% | Doha wholesale hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Population Growth Intensifying Food Demand

Qatar’s resident count continues to climb, placing persistent strain on food supply chains. Doha and Al Rayyan already house well over half of total consumption, so growers prioritize leafy greens, tomatoes, and cucumbers that deliver quick harvest cycles. The National Food Security Strategy 2030 sets ambitious vegetable self-sufficiency goals, implicitly mandating year-round greenhouse production. Diverse expatriate diets widen the product mix to include rice, lentils, berries, and organic lines, broadening the Qatar agriculture market. Businesses that align crop portfolios with this shifting demand profile gain a first-mover advantage in high-turnover urban outlets.

Extensive Government Land-Lease Incentives for Greenhouses

Long-term, zero-rent land leases lower one of the largest barriers to greenhouse investment. Operators in Al Khor and Al Shamal can secure multi-decade plots, trim upfront expenses, and allocate more capital to hydroponic hardware and climate control. The 2025 agricultural census recorded a step-change in the number of active greenhouses, proving that land policy is translating into real facilities. GLOBALG.A.P. certification by Al Sulaiteen Agricultural and Industrial Complex shows that lease incentives can yield export-grade quality. Even so, smallholders still face sizeable setup costs, keeping total greenhouse penetration below potential.

Water-Efficient Hydroponics and Aquaponics Adoption

Hydroponic systems cut water use by up to 90% versus soil farming, a decisive benefit in a nation dependent on desalination. Agrico’s aquaponics facilities recycle fish effluent as crop nutrients, creating dual revenue streams and eliminating chemical fertilizer. In September 2024, The Qatar Foundation Green Island hub validates vertical farming prototypes powered by reclaimed water and solar energy. Yields per square meter now outpace open fields by double digits, confirming technology viability. These water-light models accelerate the Qatar agriculture market toward higher productivity without depleting scarce groundwater.

Subsidized Photovoltaic Irrigation Systems

Kahramaa's BeSolar program launched in 2024 enables Qatari farms to install distributed solar systems and export surplus energy to the national grid. Instead of cash payments, the program uses a net-billing system, crediting the value of exported electricity against future Kahramaa bills, reducing operational costs[1]Source: Kahramaa Qatar General Electricity and Water Corporation, “BeSolar Program and Renewable Energy,” km.com.qa. Research from Hamad Bin Khalifa University shows agrivoltaic systems with batteries can exceed farms' energy needs, positioning agriculture as a net energy supplier. The Qatar Development Bank supports this with 1% profit-rate loans of up to QAR 2 million (USD 549,000), making photovoltaic irrigation financially attractive[2]Source: Qatar Development Bank, “Agricultural Financing Programs,” qdb.qa. Additionally, municipal tree-planting initiatives using off-grid solar pumps highlight the public sector's commitment to clean energy in agriculture.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hyper-Arid Climate and Limited Arable Land | -0.8% | Northern and western Qatar | Long term (≥ 4 years) |

| Dependency on Expatriate Agri-Labor | -0.6% | Greenhouse and livestock hubs | Medium term (2-4 years) |

| Fragmented Cold-Chain Infrastructure | -0.5% | National last-mile routes | Short term (≤ 2 years) |

| Limited Crop-Insurance Penetration | -0.4% | Small and medium farms | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Hyper-Arid Climate and Limited Arable Land

As per the Food and Agriculture Organization, only about 3% of Qatar’s land is arable, and annual rainfall rarely tops 75 millimeters[3]Source: Food and Agriculture Organization of the United Nations, “Qatar Country Profile,” Food and Agriculture Organization, fao.org. Open fields require heavy irrigation that strains desalination capacity and spikes energy use. Soil salinity has risen after decades of over-watering, leaving growers to choose between costly remediation and conversion to soilless systems. Even where land is available, high summer temperatures above 45 degrees Celsius can wilt high-value crops in hours without intensive shading and cooling. These constraints cap the speed at which the Qatar agriculture market can scale traditional acreage.

Dependency on Expatriate Agri-Labor

Foreign workers make up the bulk of farm labor and remain essential for planting, pruning, and harvesting tasks. Wage reforms in 2020 lifted minimum pay and improved mobility, raising payroll costs for farm owners. Visa policy shifts or transport disruptions, such as the March 2026 Strait of Hormuz closure, can suddenly choke recruitment pipelines. High-tech greenhouses lessen but do not eliminate manual needs because delicate crops still require human handling. Labor uncertainty therefore continues to depress investor confidence in the Qatar agriculture market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Crop Type: Vegetables Lead, Pulses Accelerate

Fruits and vegetables commanded 47% of the Qatar agriculture market in 2025, reflecting strong consumer preference for fresh items and greenhouse-enabled year-round supply. Pulses and oilseeds, are expanding at a 9% CAGR to 2031 as dietary patterns diversify among expatriate populations. Grain and cereal cultivation remains commercially infeasible domestically, so imports continue to bridge a significant value gap despite food-sovereignty ambitions. Forage and fodder crops account for a significant share, sustaining growing dairy and poultry herds, lowering dependence on expensive imported feed. Niche trials in controlled environments have begun testing chickpeas and lentils, hinting at future import substitution potential.

The Qatar agriculture market size for pulses is forecast to climb rapidly as hydroponic experiments prove viable, unlocking incremental revenue streams. Vegetables still enjoy priority greenhouse allocation because of higher turnover and stronger retail margins. Hassad Food’s offshore Kazakhstan pea facility underscores that certain staples will remain externally sourced for the foreseeable future. The organic fruit acreage share is small in absolute terms but is anticipated to show rapid growth through 2026 - 2031, signaling rising premium demand. Over the outlook period, crop diversification is poised to reduce concentration risk and strengthen national nutrition security.

Geography Analysis

Doha and Al Rayyan formed the market’s epicenter with majority of 2025 Qatar agriculture market share, lifted by the country’s highest population density and the tightest cold-chain links to Hamad International Airport. Retailers in this corridor demand frequent, small-batch deliveries that greenhouses can supply within hours, securing premium shelf space. Al Wakrah is the fastest-growing municipality, expanding at an rapid CAGR through 2026-2031 on the back of venture-funded specialty-crop projects and supportive zoning for vertical farms. Combined, these three municipalities set the commercial pace for the national market by pairing high purchasing power with streamlined logistics.

Al Khor and Al Shamal together delivered about significant share of 2025 production value, aided by multi-decade zero-rent land leases that lower fixed costs for large greenhouses. New cold-store depots near Ras Laffan port are shortening haul times to urban supermarkets, improving freshness and trimming waste. Solar irrigation pilots in the north reduce utility bills and support the national renewable-energy roadmap. These infrastructure upgrades position the northern belt as a cost-competitive supplier of bulk staples.

Region-specific initiatives are converging to lift overall output and diversify crop portfolios. Capital districts concentrate high-margin vertical farms, while coastal north zones specialize in scale greenhouse production, creating complementary supply streams. Ongoing road expansions, blockchain-based trading platforms, and additional BeSolar allocations will narrow the distance between farms and retailers, encouraging faster turnover. As each municipality executes its tailored strategy, the combined effect is anticipated to push the national market toward the significant growth by 2031.

Competitive Landscape

In 2025, the top five players dominated Qatar's agricultural commodity market, highlighting its concentrated structure. Hassad Food, backed by sovereign support, integrates domestic greenhouses with a high-capacity wheat and pea mill in Kazakhstan, ensuring steady grain inflows. Meanwhile, Baladna Food Industries, which has achieved 99% dairy self-sufficiency in Qatar, is spearheading a USD 3.5 billion initiative in Algeria. Set to be operational by late 2027, the Adrar facility will accommodate 270,000 cows and produce 200,000 metric tons of milk powder annually. This output will satisfy 50% of Algeria's milk demand, significantly curbing imports. Together, these industry frontrunners establish technological and scale benchmarks, compelling smaller firms to adapt or risk obsolescence.

Agrico Agriculture Development has proven commercial aquaponics viable by integrating fish and vegetable production under one roof, while Al Sulaiteen Agricultural and Industrial Complex won GLOBALG.A.P. certification that opens premium supermarket channels in the Gulf. Widam Food Company focuses on ISO 22000:2018 compliance to safeguard institutional contracts with hotels and hospitals. Flow Farms differentiates through pesticide-free vertical systems that cut water use by nearly 90% compared with open fields. Collectively, these firms widen product variety and raise quality standards across the sector.

Investment pipelines and technology adoption plans point to sustained capacity additions through 2031. Hassad Food is evaluating new offshore acreage, and Baladna intends to double herd size in Algeria once phase-one milestones are met. Second-tier players are scaling solar-powered greenhouses and piloting blockchain traceability to win retailer trust. With capital costs falling and policy support intact, corporate expansions are anticipated to help lift the market growth.

Recent Industry Developments

- August 2025: The Qatar Ministry of Commerce and Industry (MoCI) issued a tender for 2.4 million bags of barley to support the livestock sector and enhance the country's agricultural economy.

- March 2025: Cultivatix announced the successful installation of its first Fodder Capsule System with an integrated algae bioreactor was launched in Qatar, targeting domestic livestock feed security through hydroponic fodder combined with algae-derived biomass to enhance nutrient content and reduce import dependencies.

- December 2024: Qatar's Ministry of Municipality launched the National Food Security Strategy 2030, which aims to achieve 55% self-sufficiency in vegetable production by 2030. To meet these self-sufficiency targets, Qatar has promoted advanced farming techniques among farmers.

- October 2024: Agrico expanded a new indoor farming facility at Qatar Foundation's Green Island. This expansion increased its controlled-environment agriculture production capacity and aims to promote sustainable farming practices among Qatar's students and youth.

Qatar Agriculture Market Report Scope

Agriculture is the art and science of the cultivation of crops. For the study, all the major crops grown in the country using open fields and protected cultivation are also considered. The scope includes only fresh produce. The Qatari agriculture market is segmented by food crops/cereals, fruits, and vegetables. The report includes the production analysis by volume, consumption analysis by value and volume, export analysis by value and volume, import analysis by value and volume, and wholesale price trend analysis. The report offers market sizing in terms of both value (USD) and volume (metric tons).

Grains and Cereals

| Production Analysis (Volume) | Overview | |

| Area Harvested and Yield | ||

| Consumption Analysis (Value and Volume) | ||

| Trade Analysis (Value and Volume) | Import Market Analysis | Overview |

| Key Supplying Markets | ||

| Export Market Analysis | Overview | |

| Key Destinations Markets | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Seasonality Analysis | ||

Fruits and Vegetables

| Production Analysis (Volume) | Overview | |

| Area Harvested and Yield | ||

| Consumption Analysis (Value and Volume) | ||

| Overview | ||

| Key Supplying Markets | ||

| Overview | ||

| Key Destinations Markets | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Seasonality Analysis |

Pulses and Oilseeds

| Production Analysis (Volume) | Overview | |

| Area Harvested and Yield | ||

| Consumption Analysis (Value and Volume) | ||

| Overview | ||

| Key Supplying Markets | ||

| Overview | ||

| Key Destinations Markets | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Seasonality Analysis |

Forage and Fodder Crops

| Production Analysis (Volume) | Overview | |

| Area Harvested and Yield | ||

| Consumption Analysis (Value and Volume) | ||

| Overview | ||

| Key Supplying Markets | ||

| Overview | ||

| Key Destinations Markets | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Seasonality Analysis |

| Grains and Cereals | Production Analysis (Volume) | Overview | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Trade Analysis (Value and Volume) | Import Market Analysis | Overview | |

| Key Supplying Markets | |||

| Export Market Analysis | Overview | ||

| Key Destinations Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Seasonality Analysis | |||

| Fruits and Vegetables | Production Analysis (Volume) | Overview | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Overview | |||

| Key Supplying Markets | |||

| Overview | |||

| Key Destinations Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Seasonality Analysis | |||

| Pulses and Oilseeds | Production Analysis (Volume) | Overview | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Overview | |||

| Key Supplying Markets | |||

| Overview | |||

| Key Destinations Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Seasonality Analysis | |||

| Forage and Fodder Crops | Production Analysis (Volume) | Overview | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Overview | |||

| Key Supplying Markets | |||

| Overview | |||

| Key Destinations Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Seasonality Analysis | |||

Key Questions Answered in the Report

What is the 2026 revenue outlook for the Qatar agriculture market?

The Qatar agriculture market is forecast at about USD 370.22 million during 2026, on its way to USD 519.25 million by 2031.

Which crop category leads domestic output?

Fruits and vegetables lead with a 47% share in 2025, driven by greenhouse expansion and high consumer demand.

How big is the opportunity for pulses production?

Pulses is set to grow at 9% CAGR, signaling room for import substitution as hydroponic trials succeed.

Why are aquaponic systems gaining traction?

They recycle fish effluent into plant nutrients, cut water use sharply, and add fish revenue, boosting overall farm returns.

Page last updated on: