Bahrain Agriculture Market Analysis by Mordor Intelligence

Bahrain agriculture market size in 2026 is estimated at USD 644.79 million, growing from 2025 value of USD 634.20 million with 2031 projections showing USD 700.43 million, growing at 1.67% CAGR over 2026-2031. Growth derives from state-led greenhouse programs, vertical farm pilots, and procurement guarantees that reduce revenue risk for local producers. Intensifying GCC food-security targets, rising consumer preference for premium produce, and the kingdom’s ambition to double tree coverage to 3.6 million by 2035 all reinforce the transition from volume to value creation. Competitive intensity is increasing as capital-rich agritech entrants partner with state entities such as Edamah on a 50,000 m² facility that integrates solar power with climate-controlled cultivation. While the headline CAGR appears modest, the Bahrain agriculture market is pivoting toward high-margin segments, such as leafy greens, premium dates, pomegranates, and pulses, supported by guaranteed off-take agreements with hospitality chains and public institutions.

Key Report Takeaways

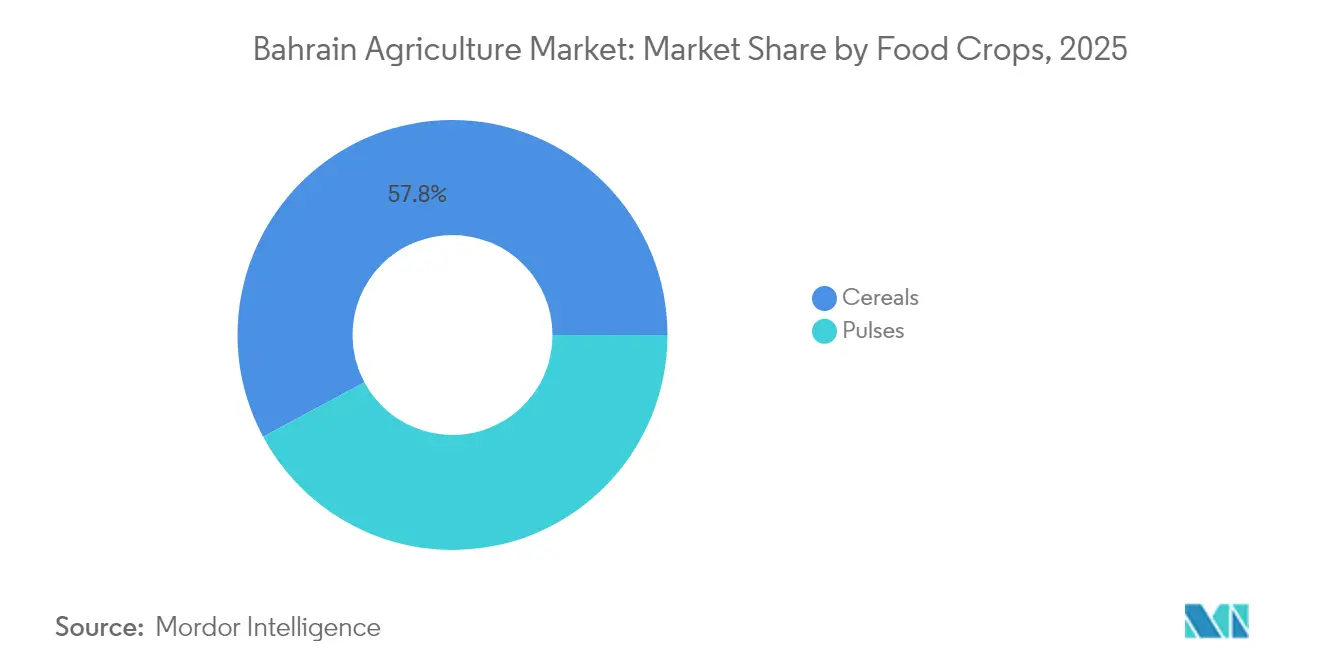

- By food crop type, cereals held 57.84% of the Bahrain agriculture market size in 2025, yet pulses are projected to grow fastest at 5.05% CAGR between 2026 and 2031.

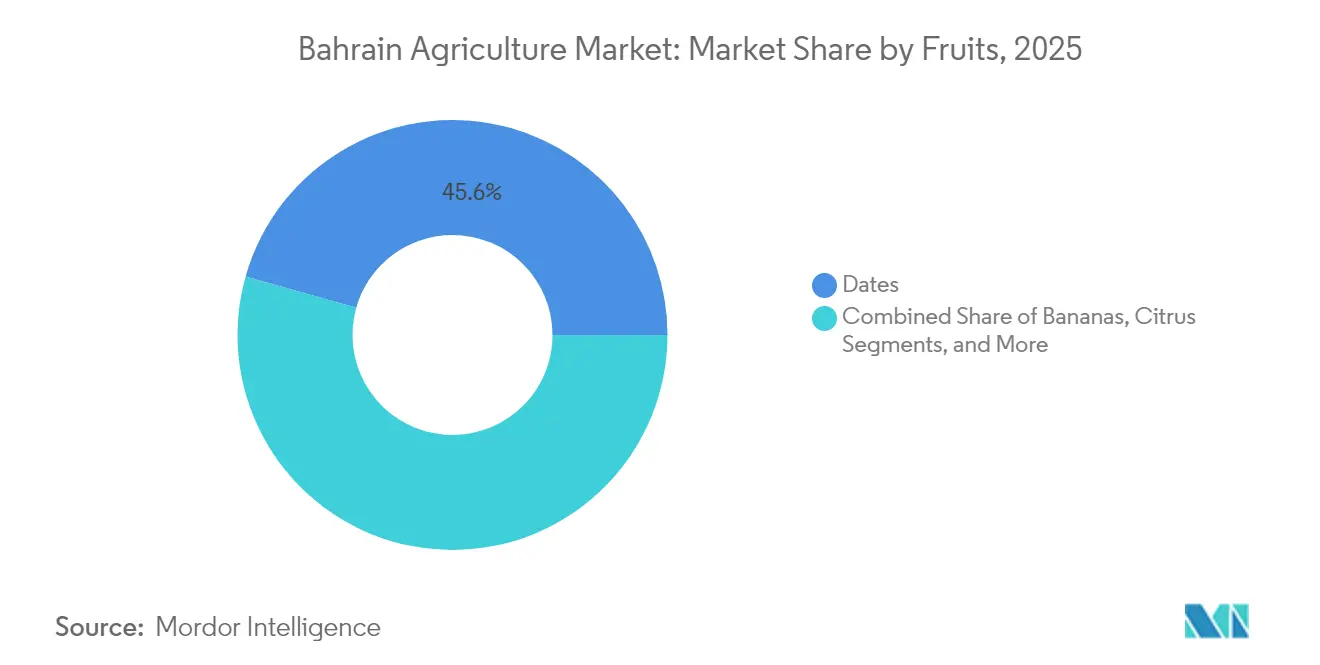

- By fruit type, dates led with 45.62% of the Bahrain agriculture market share in fruit production volume in 2025, and pomegranates are projected to grow at a 6.33% CAGR through 2031.

- By vegetable type, tomatoes commanded 41.23% of the Bahrain agriculture market share in vegetables in 2025, and leafy greens are forecast to expand at a 7.19% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Bahrain Agriculture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-backed water-saving greenhouse projects | +0.4% | National – Northern Governorate | Medium term (2-4 years) |

| National Food Security Initiative procurement guarantees | +0.3% | National – spillover to GCC supply chains | Long term (≥ 4 years) |

| Controlled-environment farms lowering import reliance | +0.5% | National – tech transfer to regional partners | Medium term (2-4 years) |

| Surge in GCC demand for premium dates | +0.2% | Regional – Bahrain date-growing areas | Short term (≤ 2 years) |

| Adoption of solar-powered desalination for irrigation | +0.3% | National – coastal pilot projects | Long term (≥ 4 years) |

| Vertical-farm export contracts with luxury hotel chains | +0.1% | National – hospitality clusters | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government-backed Water-saving Greenhouse Projects

State-funded climate-controlled complexes have become the cornerstone of the Bahrain agriculture market transformation. The 50,000 m² Edamah–Badia Farms facility taps sovereign land, hydroponics, and on-site solar arrays to prove that water use can drop by 90% while output rises threefold. Streamlined licensing and infrastructure support attract global agritech vendors eager for a showcase in hot-arid zones. Success criteria extend beyond tonnage, each unit must verify water-use efficiency and export revenues, aligning with Vision 2030 diversification targets. Demonstration effects spur copycat investments, deepening local expertise in sensors, nutrient dosing, and renewable energy coupling. As more pilot plots reach commercial scale, the Bahrain agriculture market secures a role as a regional testbed for desert farming innovations.

National Food Security Initiative Procurement Guarantees

Under the National Food Security Initiative, the government pledges to purchase vegetables and dairy at pre-set premiums, building on its 96% self-sufficiency in dates and 90% in fish.[1]Ministry of Information, “Agricultural Statistics 2025,” Ministry of Information, moi.gov.bh The guarantees allow farmers to de-risk multimillion-dollar greenhouses, as banks accept guaranteed contracts instead of collateral. Quality premiums tie payouts to traceability and sustainable practice scores, nudging growers toward Integrated Pest Management and digital recordkeeping. Timed tenders even out seasonal gluts, while buffer stocks strengthen emergency readiness. The program must calibrate pricing carefully, overly generous terms could inflate fiscal burdens, whereas thin margins would fail to stimulate investment. Early evidence shows private lenders extending tenors to match the longer payback periods typical of controlled-environment assets.

Controlled-environment Farms Lowering Import Reliance

Facilities using vertical stack or Dutch-style greenhouses deliver 30–35 kg of leafy greens per square meter yearly and recycle up to 95% of nutrient solution, cutting import dependency that exceeded 80% for vegetables in 2023. Hospitality chains, retailers, and airline caterers now advertise “grown in Bahrain” labels that command 20% price premiums. Local technical colleges have launched diplomas in precision horticulture, expanding the talent pipeline and reducing reliance on expatriate agronomists. Technology spillovers reach aquaculture and floriculture start-ups, broadening the Bahrain agriculture market’s diversification base.

Surge in GCC Demand for Premium Dates

Growing affluence and health positioning for potassium-rich dates fuel regional demand for artisanal varieties. Bahrain palms yield award-winning Khalas and Khuneizi cultivars, with saline-tolerant rootstocks proving resilient on reclaimed land.[2]Abdullah Al-Haddad, “Salinity-Tolerant Date Palms,” Frontiers in Sustainable Food Systems, frontiersin.org Exporters leverage Manama port’s cold-chain corridors to reach Dubai and Riyadh within 48 hours, assuring quality retention. Luxury retailers prioritize blockchain-verified provenance, and Bahraini packers are rolling out QR-coded pouches to meet that requirement. The trend supports downstream confectionery, such as date-filled chocolates and energy bars, layering extra value onto the raw fruit trade.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarce arable land and saline soils | -0.3% | National – traditional farming zones | Long term (≥ 4 years) |

| Volatile global feed and fertilizer prices | -0.2% | Global input markets with domestic spillover | Short term (≤ 2 years) |

| High capex for climate-controlled structures | -0.4% | National – all new tech facilities | Medium term (2-4 years) |

| Limited ag-specific credit for SMEs | -0.2% | National – smallholder clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Scarce Arable Land and Saline Soils

Only 6,400 hectares remain under cultivation, and 35% of that area shows salinity levels above 8 dS/m, cutting yields by up to 60% for sensitive crops. Remediation via gypsum and leaching costs USD 4,000/hectare annually, eroding margins. Small plots limit mechanization, keeping unit costs high and hindering rotation schemes that would break pest cycles. Consequently, the Bahrain agriculture market gravitates toward soilless systems that sidestep soil degradation but require substantial capital and technical know-how.

Volatile Global Feed and Fertilizer Prices

Fertilizer quotations jumped 30% in early 2022 and eased 17% in 2024, yet remain higher than pre-pandemic norms, compressing dairy and poultry margins that already rely on imports for 79% of feed inputs. Bahrain’s smallholders lack hedging instruments or storage, forcing spot purchases at peak price points. Input shocks deter borrowing for technology upgrades, slowing the overall pace at which the Bahrain agriculture market can pivot to higher productivity systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Food Crops: Cereals Dominate Despite Import Dependence

Cereals captured 57.84% of 2025 food-crop output, yet Bahrain imports its entire wheat requirement, 50,000 metric tons in 2024, revealing that the Bahrain agriculture market size for cereals hinges on feed, not flour. Barley underpins dairy self-sufficiency and benefits from procurement guarantees that stabilize prices. Pulses, though smaller today, register a 5.05% CAGR to 2031 as consumers lean into plant-protein and greenhouses prove effective at lentil and chickpea cycles. Precision fertigation trims input waste, supporting margins even under elevated global fertilizer prices.

Strategically, cereals will not become export winners; instead, policy steers growers toward specialty barley for local dairies and high-value pulses. Field sensors and AI-based leaf-area mapping improve nutrient timing, raising yields on constrained plots. Blockchain-enabled sourcing bolsters feed traceability, a growing requirement from dairy processors aiming for premium positioning.

By Vegetables: Controlled Environment Systems Enable Leafy Greens Growth

Leafy greens will post the fastest 7.19% CAGR to 2031, yet tomatoes retain a 41.23% share of vegetable output in 2025, underscoring their cultural and culinary importance. Vertical farms achieve 350 harvest cycles of lettuce annually, compared with 10–12 in open fields, slashing import reliance and transit losses. The Bahrain agriculture market size for greenhouse tomatoes is projected to reach USD 89.4 million by 2031, supported by stable off-take from retail chains.

Cucumbers and eggplants receive renewed interest after pilots demonstrate 80% water savings through deep-water culture beds. Energy-efficient LEDs and heat-exchange chillers extend production into the hottest months, smoothing supply peaks and troughs. Combined, these advances lock vegetables into a higher-value stratum of the Bahrain agriculture market.

By Fruits: Premium Dates Drive Export Opportunities

Dates held 45.62% of the 2025 fruit output, equating to the largest Bahrain agriculture market share within horticulture. Khalas, Khuneizi, and Ajwa varieties leverage saline-tolerant rootstocks to thrive in marginal soils while achieving export-grade sugar profiles. Pomegranates outpace all other fruits at a 6.33% CAGR through 2031, driven by controlled-environment orchards that shield blossoms from heat stress and allow off-season fruiting.

Export-oriented pack-houses introduce food-grade stainless steel lines and laser-sorting, lifting unit-value returns. Adjacent opportunities include date syrup and pomegranate-based nutraceuticals. Knowledge partnerships with regional food-research institutes aim to breed varieties optimized for high-salinity and high-temperature conditions, further fortifying this corner of the Bahrain agriculture market.

Geography Analysis

The Capital Governorate played a prominent role in the Bahrain agriculture market, linking dense population, five-star hotels, and high-end grocers to premium produce demand that sustains hydroponic economics. Logistics efficiency prevails: farms within 25 km ferry greens by refrigerated van in under 45 minutes, preserving shelf life and taste.

Northern Governorate hosts the majority of production assets, including the flagship 50,000 m² Edamah–Badia site. Access to desalination plants and the national grid’s highest solar penetration rates cut operating expenses by 18% compared with central regions. Afforestation corridors double as windbreaks, mitigating sand intrusion and stabilizing microclimates. Cluster development accelerates technology diffusion, as spare parts suppliers and agronomic consultants agglomerate within the same zone.

Southern Governorate, though traditionally pastoral, is driven by residential expansion and tourism investments. Start-ups are experimenting with agritourism plots that pair boutique lodgings with pick-your-own experiences, capturing premium margins and bolstering brand recognition for Bahraini produce. Muharraq’s free-trade zone continues to channel outbound shipments, leveraging proximity to Bahrain International Airport to move high-value perishables across GCC capitals within hours.

Regulatory Landscape

The Ministry of Municipalities Affairs and Agriculture (MMAA) oversees agricultural health and quarantine controls, fertilizer-related oversight, and import licensing for plants and plant products in Bahrain. Agricultural imports (including plants, seeds, fertilizers, and plant-origin feed) require prior permits from the Agricultural Health Directorate, must be supported by phytosanitary certification from the exporting country, and are inspected upon arrival at customs ports. Permit fees are set at BD 10, and permits are typically valid for six months.

Bahrain also aligns food and agriculture requirements to Gulf standards as national references, including through Ministerial Order No. 29 for 2025. The National Food Security Strategy 2020-2030, developed with FAO cooperation, frames programs that emphasize local production technologies and resilience measures, including local production expansion, supply-chain diversification, and food reserve management. Import compliance remains detailed in practice, with requirements such as non-GMO declarations for seeds and radiation-free certificates for grains from specified origins that shape sourcing decisions and documentation workflows.

Value Chain Analysis

The Bahrain agriculture value chain begins with imported inputs (seeds, substrates, fertigation components, fertilizers and soil conditioners, and controlled-environment equipment), which move through regulated entry and inspection before production across open-field plots and protected agriculture systems (greenhouses, hydroponics, and vertical setups). Post-harvest handling and aggregation increasingly focus on short-cycle perishables, particularly leafy greens and greenhouse vegetables, where cold-chain movement to retailers, hospitality buyers, and institutional channels supports premium positioning. Year-round output from controlled environments, combined with traceability, helps stabilize supply to these buyers.

Midstream coordination is also shifting through institutional consolidation and shared data infrastructure. Mumtalakat completed the transfer of Bahrain Agriculture Development Company (Gheras) to Bahrain Food Holding Company (BFHC) in November 2024, linking production-oriented initiatives with a wider food ecosystem approach. On the enabling side, the National Initiative for Agricultural Development (NIAD) runs the AgroBH platform to centralize agricultural data (land use, soils, workforce) for investment facilitation, while government support tools, including extension services and farmers markets (the permanent market in Aali and the seasonal market in Budaiya), connect local producers with demand and reduce go-to-market friction for smaller growers.

Market Opportunities and Future Outlook

The clearest opportunities center on scaling controlled-environment horticulture and the enabling capabilities around it, rather than expanding traditional acreage, given Bahrain's binding land and water constraints. The government has operationalized channels for investment and capability building, including NIAD's AgroBH platform to reduce information barriers for site selection and crop planning. Separately, the Ministry of Municipalities Affairs and Agriculture has formalized entrepreneurship upskilling through an MoU with NIAD (May 2026) for specialized training programs on modern scientific and practical techniques, which can support execution readiness for greenhouse and hydroponic projects.

Commercialization pathways are also broadening through downstream integration and logistics-oriented infrastructure. Bahrain Food Holding Company (Ghitha) launched its corporate strategy and announced the Food City project with Edamah (June 2025), positioning an integrated industrial center for food production, manufacturing, and distribution to support faster routing from farms to higher-frequency buyers. In parallel, the June 2026 tender for operation and maintenance of irrigation networks and landscaping at East Sitra points to continued spend on water-management systems, reinforcing demand for irrigation O&M capabilities, monitoring, and efficiency upgrades across agriculture-adjacent green assets.

Recent Industry Developments

- May 2026: The Ministry of Municipalities Affairs and Agriculture and the National Initiative for Agricultural Development (NIAD) signed an MoU to implement specialized training programs for agricultural entrepreneurs. The initiative supports adoption of modern scientific and practical techniques, strengthening the local operating base for greenhouse and hydroponic production and improving bankability of new projects through better execution capability.

- June 2025: Bahrain Mumtalakat Holding Company announced the launch of the Ghitha strategy and a Food City (food park) project in collaboration with Edamah, with the first phase covering around 1 million square meters. The project signals a coordinated push to link production with manufacturing and distribution infrastructure, tightening routes to market for locally produced crops and supporting larger-scale agri-food investment.

- April 2024: Bahrain Agricultural Development Company opened the first phase of a hydroponics production project in Hoorat A'ali, targeting annual output of about 520 tons across Hoorat A'ali and Duraz sites. This expansion adds domestic protected-cultivation capacity and provides a reference point for commercial-scale hydroponics in Bahrain's constrained land and water environment.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is sized as the annual value generated from agricultural output in Bahrain, measured at the farm gate and through first-level aggregation for products that are sold or consumed locally.

Scope exclusions: We exclude aquaculture, livestock, agrochemical sales, farm inputs like seeds and machinery, and downstream food processing.

Segmentation Overview

- By Commodity Type

- Food Crops

- Cereals (Wheat, Barley, Maize)

- Pulses (Lentils, Chickpeas, Beans)

- Fruits

- Dates

- Bananas

- Citrus (Limes, Oranges)

- Pomegranates

- Vegetables

- Tomatoes

- Cucumbers and Gherkins

- Eggplants

- Leafy Greens (Lettuce, Spinach)

- Food Crops

Data Sources, Market Sizing, and Validation

Desk Research

Desk work was used to build the factual backbone for the model, especially around Bahrain farm output, trade flows, and pricing signals that explain value changes over time. For this, we leaned on public sources such as FAOSTAT, UN Comtrade, national statistics releases, agriculture and water-related ministry publications, and customs and port updates where available.

We also reviewed company filings, investor presentations, association websites, and credible local and regional press to understand crop mix changes, protected cultivation expansion, and retail pricing context. When needed, a paid subscription for company financials and a separate paid shipment-level trade database were used to cross-check totals and remove obvious data gaps. The desk research sources listed here are illustrative only, and many other public and paid sources were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what is actually sold, how value is formed, and how fast farm-gate prices and yields are shifting in Bahrain. We spoke with growers, first-level aggregators, importers and distributors, and technical experts tied to protected agriculture, and then we cross-checked the assumptions across the main demand centers.

Because desk sources can lag on small-market shifts, interviews were also used to confirm seasonality patterns, the share of protected production versus open-field supply, and the practical limits created by water and land constraints.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 15% | |

| Mid tier: 55% | Functional/Unit leaders: 29% | |

| Smaller Players: 18% | Managers: 56% |

Market-Sizing & Forecasting

The core sizing logic starts with a top-down reconstruction of Bahrain agriculture value by linking production volumes to farm-gate and first-trade prices, and then adjusting for import reliance and the portion that is traded versus directly consumed. To keep the totals realistic, selective bottom-up checks were run, such as sampling crop-level volumes and prices from channel discussions and rolling them up to a reasonableness range.

Key inputs that were tracked (as indicators, not as a complete list) included crop output volumes, harvested area and yield shifts, protected cultivation adoption, import and export values by relevant agricultural headings, and farm-gate price movement tied to water and energy costs. For forecasting, scenario analysis was used and then narrowed through primary feedback on near-term capacity additions, water availability, and expected price normalization. When a bottom-up input was missing for a niche crop, we filled gaps using proxy yields and price bands from similar crops and then rechecked the result with interview feedback.

Data Validation & Update Cycle

Estimates were triangulated through cross-checks between production, trade, and price signals, and then the model outputs were compared against independent checkpoints shared by market participants. If a variance looked too wide, the assumption was revisited, the arithmetic was rerun, and follow-up calls were triggered to confirm what changed and why.

Before sign-off, the draft model and narrative go through a multi-step analyst review so that outliers and unit conversions are caught early. Reports are refreshed annually, and interim updates are made when material events occur (for example, policy shifts, water restrictions, or major controlled-environment capacity additions). Right before delivery, a final pass is completed so clients receive the most current view available.

Mordor Intelligence's Bahrain Agriculture Market Size Compared Against Other Published Estimates

Published market sizes for Bahrain agriculture can look far apart because the market label is used differently across sources, and the underlying value build-up is not always the same. Differences usually come from what is counted as agriculture value, how imports are treated, and whether prices are taken at the farm gate or further downstream.

Some published figures blend in adjacent areas like livestock or broader agri-tech spending, and they may also mix service and solution revenues into the same number. In contrast, the main split comes from scope, where Mordor Intelligence counts the annual gross value of food crops, fruits, and open-field and protected-vegetable production traded or consumed domestically, and it excludes aquaculture, livestock, inputs, and downstream processing, all kept in constant 2024 US dollars.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 634.20 M (2025) | |

| Industry Research Publisher A | USD 331.00 M (2025) | The estimate appears to emphasize domestic activity and technology-led production expansion, which can undercount total farm-gate value if traditional crop output and first-level trading margins are not fully captured, and if the value basis is not held constant in USD. |

| Industry Research Publisher B | USD 624.65 M (2025) | This estimate discusses a wider agriculture narrative that can include rural activities and livestock modernization themes, so the number can shift depending on whether livestock-linked value and service components are included, and how farm-gate pricing versus retail-linked pricing is handled. |

Overall, the spread is mainly explained by what sits inside the agriculture bucket and where value is measured in the chain. By keeping the scope tied to crop output value and then checking it against trade and price signals, the final number stays traceable to clear drivers that can be revisited as conditions change.

Key Questions Answered in the Report

What is the current size of the Bahrain agriculture market?

The Bahrain agriculture market stands at USD 644.79 million in 2026 and is forecast to reach USD 700.43 million by 2031.

Which crop segment is growing fastest in Bahrain?

Leafy greens lead growth with a projected 7.19% CAGR between 2026 and 2031, thanks to expansion of vertical farms and hydroponic systems.

How significant are dates in Bahrain’s fruit sector?

Dates command 45.62% of 2025 fruit production and position Bahrain as 96% self-sufficient, enabling export opportunities within the GCC.

What key policy supports agriculture investment in Bahrain?

The National Food Security Initiative offers procurement guarantees that lock in demand and pricing for locally produced vegetables and dairy.

Page last updated on: