Saudi Arabia Agriculture Market Analysis by Mordor Intelligence

The Saudi Arabia Agriculture Market size is estimated at USD 15.20 billion in 2026 and is anticipated to reach USD 20.30 billion by 2031, at a CAGR of 5.96% during the forecast period (2026-2031). Continued investment in desalination-fed irrigation, controlled-environment agriculture, and salt-tolerant crop genetics is reshaping production economics, supporting steady gains in domestic fruit, vegetable, dairy, and poultry output. Vision 2030 subsidies covering up to 60% of capital costs have triggered rapid greenhouse expansion, while agrivoltaic pilots deliver dual revenue streams that improve farm cash flow and water-use efficiency. Import costs for cereals and off-season produce still create exposure to Red Sea and Black Sea disruptions, yet treated-wastewater mandates and feed-in tariffs for on-farm solar power strengthen resilience. Private and sovereign capital is shifting toward vertically integrated agritech parks in Tabuk and Al-Jouf, giving the Saudi Arabian agricultural commodity market clear momentum toward food-sovereignty targets.

Key Report Takeaways

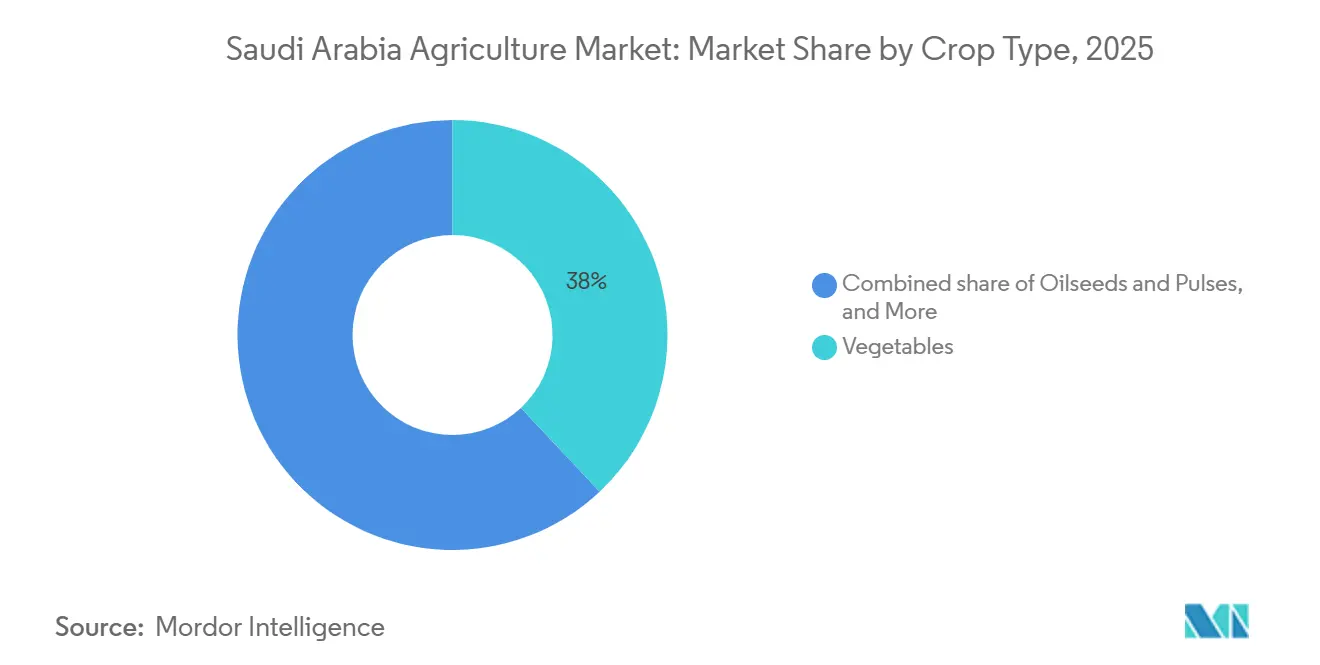

- By crop type, vegetables led with 38% of Saudi Arabia's agriculture market share in 2025, while oilseeds and pulses segment emerges as the fastest-growing crop category with a 10.2% CAGR forecast through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Saudi Arabia Agriculture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Vision-2030 subsidies and grants | +1.8% | National, with concentration in Al-Jouf, Tabuk, Hail provinces | Medium term (2-4 years) |

| Food-security imperative amid import dependence | +1.5% | National, with strategic focus on major consumption centers | Long term (≥ 4 years) |

| Precision and greenhouse tech adoption | +1.2% | National, with early adoption in Northern provinces | Medium term (2-4 years) |

| National water-efficiency programs | +0.9% | National, with priority in water-stressed regions | Long term (≥ 4 years) |

| Solar-powered agrivoltaics in desert farms | +0.4% | Regional, focused on high solar irradiance areas | Long term (≥ 4 years) |

| Salt-tolerant date-palm breeding success | +0.2% | Regional, concentrated in traditional date-growing oases | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Vision-2030 Subsidies and Grants

Vision 2030's agricultural financing programs are reshaping capital allocation patterns across the Kingdom's farming sector through unprecedented government support mechanisms. The Agricultural Development Fund provides up to 75% financing for greenhouse projects and modern irrigation systems, with tax holidays extending up to 10 years for qualifying agritech investments [1]Source: Saudi Vision 2030, “Vision 2030 Programs,” Vision2030.gov.sa . This financial backing has catalyzed a surge in controlled-environment agriculture, with companies like Topian (NEOM subsidiary) opening a 4-hectare climate-resilient greenhouse facility in Oxagon during 2025, marking the Kingdom's largest single investment in precision horticulture to date. The subsidy structure particularly favors water-efficient technologies, creating market incentives that align private sector returns with national water conservation objectives.

Food-Security Imperative Amid Import Dependence

Saudi Arabia's strategic push to reduce food import dependency has intensified following supply chain disruptions during the COVID-19 pandemic and geopolitical tensions affecting global trade routes. The Kingdom currently imports approximately 90-95% of its edible oil requirements and significant portions of its fresh produce, creating vulnerability to external price shocks and supply disruptions. Government mandates now require major food companies to demonstrate domestic sourcing capabilities, with SALIC launching National Grain Supply Company (SABIL) in April 2025 to manage strategic grain storage and procurement operations across 14 silo branches with combined capacity exceeding 2.7 million metric tons. This policy framework is driving vertical integration strategies among agricultural companies, as domestic production capacity becomes a competitive differentiator in government contract bidding processes.

Precision and Greenhouse Tech Adoption

Internet of Things sensors and automated climate control systems are transforming agricultural productivity metrics across Saudi Arabia's controlled-environment facilities. Research partnerships between domestic companies and South Korean technology providers have resulted in smart agriculture systems that integrate soil moisture sensors, weather monitoring, and automated irrigation controls to optimize resource utilization. Companies like FarmERP expanded into Saudi Arabia through partnerships with local technology integrator Seiyaj Tech in August 2024, providing cloud-based farm management platforms that enable real-time monitoring of crop health, irrigation schedules, and harvest timing across multiple cultivation sites.

National Water-Efficiency Programs

The National Water Strategy's emphasis on agricultural water conservation is driving systematic adoption of drip irrigation and micro-sprinkler systems that reduce water consumption by up to 40% compared to traditional flood irrigation methods. Government-funded infrastructure projects include the construction of advanced desalination facilities specifically designed for agricultural use, with King Abdullah University of Science and Technology (KAUST) researchers developing custom desalination technologies that produce irrigation-quality water at lower energy costs than conventional seawater treatment plants. The program's impact extends beyond water savings to soil health improvement, as precision irrigation reduces salt accumulation in agricultural soils and enables cultivation in previously marginal lands.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Extreme aridity and groundwater depletion | -1.1% | National, with severe impact in central and eastern regions | Long term (≥ 4 years) |

| High capex for modern farming systems | -0.8% | National, with disproportionate impact on SME (Saudi Small and Medium-sized Enterprises) farmers | Medium term (2-4 years) |

| Soil-salinity spikes from brine return flows | -0.5% | Regional, concentrated near desalination facilities | Medium term (2-4 years) |

| Cold-chain and remote-logistics gaps | -0.4% | National, with acute challenges in rural production areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Extreme Aridity and Groundwater Depletion

Saudi Arabia's agricultural expansion faces fundamental water resource constraints as fossil aquifers decline at accelerating rates across major production regions. The Kingdom's non-renewable groundwater reserves are dropping by an average of 0.6 meters annually, with some agricultural areas experiencing depletion rates exceeding 1 meter per year [2]Source: World Bank, “Saudi Arabia Water Data,” worldbank.org. This hydrological challenge forces agricultural operators to invest in increasingly expensive water extraction equipment and deeper well drilling, driving up operational costs and threatening the economic viability of water-intensive crops. The situation is particularly acute in the Eastern Province and central regions, where traditional agricultural areas are experiencing well failures and declining water quality as aquifer levels drop below economically extractable depths.

High Capex for Modern Farming Systems

Greenhouse construction costs in Saudi Arabia exceed USD 1.2 million per hectare for advanced climate-controlled facilities, creating significant barriers to entry for small and medium-scale agricultural enterprises. The capital intensity of modern farming systems reflects the specialized equipment requirements for desert agriculture, including advanced cooling systems, automated irrigation networks, and soil-less growing media that can withstand extreme temperature variations. The high upfront investment requirements are concentrating market participation among well-capitalized corporate entities and government-backed development companies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Crop Type: Oilseeds Drive Import Substitution Strategy

Vegetables maintain the largest market share at 38% in 2025, driven by controlled-environment agriculture that enables year-round production of tomatoes, cucumbers, and peppers despite extreme seasonal temperature variations. Growing vegetable output shortens import lines, trimming freight-driven carbon footprints in the Saudi Arabia agriculture market. Controlled environments stabilize supply in Ramadan and Hajj seasons when demand spikes.

The oilseeds and pulses segment emerges as the fastest-growing crop category with a 10.2% CAGR forecast through 2031, reflecting Saudi Arabia's strategic imperative to reduce import dependency for protein-rich crops and cooking oils that currently account for over 90% of domestic consumption. Government incentives specifically target oilseed cultivation through subsidized land allocation and water access programs, with the Ministry of Environment, Water, and Agriculture prioritizing sunflower and soybean production in northern provinces where climate conditions support these temperate crops.

Geography Analysis

Saudi Arabia's agricultural market concentrates in the northern provinces of Al-Jouf, Tabuk, and Hail, which collectively account for the majority of the Kingdom's fresh produce output due to their relatively moderate climate conditions and groundwater availability. Al-Jouf Province has emerged as the primary agricultural hub, hosting major processing facilities, including Al-Jouf Agricultural Development Company's French-fries processing plant that opened in May 2024 with the capacity to serve both domestic and export markets.

The Eastern Province plays a strategic role in agricultural logistics and processing, with major companies like ARASCO (Arabian Agricultural Services Company) operating feed production facilities and Almarai maintaining large-scale dairy operations that support the livestock sector. The NEOM region in the northwest is developing into a showcase for advanced agricultural technologies, with Topian's 4-hectare climate-resilient greenhouse facility representing the largest single investment in precision horticulture within the Kingdom.

Central and southern regions face greater agricultural challenges due to extreme aridity and limited groundwater resources, though specialized crops like dates continue to thrive in traditional oasis systems. The government's National Water Strategy prioritizes these regions for advanced desalination infrastructure and water-efficient irrigation technologies that could unlock additional agricultural potential. Recent investments in cold-chain logistics infrastructure, including the development of 59 logistics centers by 2030 under the Saudi logistics master plan, are improving market access for producers in remote areas and reducing post-harvest losses that previously constrained profitability in marginal production zones.

Regulatory Landscape

Saudi Arabia's agriculture regulatory framework is administered primarily by the Ministry of Environment, Water and Agriculture (MEWA), which sets sector policy and oversees implementation under the Agriculture Law, including registration and licensing requirements across production and trade activities. Compliance requirements intersect with the Saudi Food and Drug Authority (SFDA) on food safety and import clearance, including technical regulations, maximum pesticide residue limits, and documentation such as phytosanitary certificates for relevant crop consignments.

Water and environmental rules also shape farm economics alongside crop rules. The National Water Strategy 2030 anchors water allocation and conservation priorities that push adoption of drip irrigation and other efficiency measures, while the Environmental Law establishes requirements around land management and environmental impact considerations. In June 2026, MEWA scheduled the inaugural Saudi Water Week in Jeddah (June 28 to July 2, 2026), reinforcing the policy focus on water sustainability and its implications for agricultural water-use practices.

Value Chain Analysis

The Saudi Arabia agriculture value chain starts with regulated inputs (seed, fertilizers, crop protection) and farm enablement services that increasingly include digital platforms and on-farm automation. Production is concentrated in open-field systems for selected crops and in controlled-environment agriculture for vegetables and other higher-value crops, supported by government-backed finance such as the Agricultural Development Fund's programs for modern irrigation and greenhouse investments. Research and commercialization linkages with universities and applied research bodies (including KAUST and King Abdulaziz City for Science and Technology) support salt-tolerant genetics and resource-efficient production systems for arid conditions.

Post-harvest handling and distribution rely on packing, cold chain, and logistics connectivity to major consumption centers, with recognized gaps in remote logistics and temperature-controlled storage still creating loss and quality risks. Strategic grain and staple supply resilience depends on state-backed entities and storage networks, with SALIC and its platforms supporting procurement and capacity planning (for example, SABIL managing strategic grain storage across 14 silo branches with over 2.7 million metric tons of capacity). On the domestic fresh-produce side, large-scale corporate farms and project developers are expanding greenhouse footprints (for example, Dava Agricultural's Taif mega-project announcement), while processors and integrated players in provinces such as Al-Jouf anchor offtake through facilities that connect primary production to retail and export channels.

Competitive Landscape

The Saudi Arabian agricultural commodity market is moderately fragmented, and the top five firms held a significant share of 2025 revenue. Almarai leads dairy and poultry through full vertical integration that spans fodder farms in Argentina and 58,000 retail outlets across the Gulf, driving scale efficiencies and brand reach. Nadec follows with diversified dairy and produce lines supplied by thousands of head of cattle and several hectares of crops. Tabuk Agricultural Development Company leverages 22,000 hectares of irrigated land to export potatoes, onions, and greenhouse vegetables, maintaining stable cash flow even after the wheat ban.

Disruptive entrants include Pure Harvest Smart Farms, which deployed AI-driven climate algorithms that cut energy 19% and achieved 95% delivery accuracy. Red Sea Farms introduced seawater-cooled greenhouses that slash freshwater use 90%, broadening technology options for arid-zone horticulture. Patent filings in gene editing surged to 142 in 2024, with King Abdulaziz City for Science and Technology and King Abdullah University of Science and Technology leading breakthroughs in salt tolerance. These innovations pressure incumbents to accelerate R&D or partner with startups.

Investment momentum favors large-scale, desert-adjacent greenhouse estates that pair solar power with desalination. Public Investment Fund backing lowers cost of capital and unlocks globally competitive produce pricing. Smallholders gain by joining cooperatives that aggregate demand for inputs and market output, but high technology entry costs keep them reliant on subsidies. Overall, the Saudi Arabian agricultural commodity market exhibits a blend of state intervention and private entrepreneurship that promotes consolidation and modernization simultaneously.

Market Opportunities and Future Outlook

Controlled-environment agriculture and water-smart production systems are the clearest whitespace within the Kingdom's farm-gate crop value chain, supported by capital programs and announced projects that move policy into build-out. In May 2026, Dava Agricultural announced a Taif expansion plan featuring 350 hectares of glass greenhouses and a stated target of 1,000 tons of daily fresh-produce output by 2030. In July 2026, KUBO and Amtar Al Khair Agricultural Crops Company signed contracts for a 45-hectare greenhouse project in Jazan using an Ultra-Clima concept, with a reported USD 160 million investment. These projects point to sustained demand for greenhouse structures, climate-control systems, substrates, crop genetics for heat and salinity conditions, and specialized agronomy services.

Upstream and enabling services also present opportunity as the country formalizes compliance and scales advisory support. MEWA signed a USD 5 million cooperation agreement with CGIAR in January 2026 to advance agricultural technology and sustainable practices, linking public R&D with field adoption. Digital advisory and farm-management platforms offer an operational lever as scale increases across dispersed production zones, as shown by the Murshiduk platform supporting over 312,000 registered farmers through guidance and remote consultations. On supply security, SALIC's expanding role in global sourcing and coordination increases incentives for integrated procurement, storage, and logistics solutions that connect imported staples with local distribution while domestic production rises in vegetables and targeted import-substitution crops such as oilseeds and pulses.

Recent Industry Developments

- July 2026: KUBO and Amtar Al Khair Agricultural Crops Company signed contracts for a 45-hectare greenhouse project in Jazan province using the Ultra-Clima concept, representing a reported USD 160 million investment. The project reinforces the shift toward large-scale controlled-environment agriculture outside the traditional northern hubs, expanding demand for turnkey greenhouse engineering, climate control, and technical services.

- May 2026: Saudi Agricultural and Livestock Investment Company (SALIC) completed a USD 1.88 billion transaction to raise its stake in Olam Agri Holdings to 80.01 percent. This strengthens SALIC's position across global agri-supply chains, supporting Saudi Arabia's broader food-security strategy and upstream access to grains and other agricultural commodities.

- August 2024: FarmERP expanded into Saudi Arabia through a partnership with local technology integrator Seiyaj Tech to deploy cloud-based farm management tools. The collaboration supports traceability, irrigation and harvest planning, and multi-site monitoring, which are increasingly relevant as greenhouse and precision farming projects scale across the Kingdom.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as the annual farm-gate value of crops produced inside Saudi Arabia, covering field-grown and protected cultivation. Values are expressed in constant 2024 USD to keep year-to-year comparisons consistent.

Scope exclusions: Livestock, aquaculture, forestry products, agro-inputs, and any post-farm processing are not counted in this market value.

Segmentation Overview

- By Crop Type

- Cereals and Grains

- Production Analysis (Volume)

- Overview

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Overview

- Key Supplying Markets

- Export Market Analysis

- Overview

- Key Destination Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis (Volume)

- Fruits

- Production Analysis (Volume)

- Overview

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Overview

- Key Supplying Markets

- Export Market Analysis

- Overview

- Key Destination Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis (Volume)

- Vegetables

- Production Analysis (Volume)

- Overview

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Overview

- Key Supplying Markets

- Export Market Analysis

- Overview

- Key Destination Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis (Volume)

- Oilseeds and Pulses

- Production Analysis (Volume)

- Overview

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Overview

- Key Supplying Markets

- Export Market Analysis

- Overview

- Key Destination Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis (Volume)

- Cereals and Grains

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts with crop output and price signals that can be checked and repeated, then it is aligned to a farm-gate value viewpoint. For Saudi Arabia, we lean on public statistics such as FAOSTAT, Saudi Central Bank exchange-rate tables, and official releases from the Ministry of Environment, Water and Agriculture. Where trade linkages help explain availability and seasonality, customs statistics and UN Comtrade-style datasets are used as supporting context rather than as a direct substitute for domestic production.

We also review company annual reports, investor presentations, and credible press coverage to understand crop focus, protected cultivation expansion, and procurement practices. For cross-checking financial consistency, we selectively use paid subscriptions that provide company financials and intelligence, along with general news and financials screening, and then reconcile those signals to the same constant-dollar basis. The sources listed here are illustrative only, and many other public references were also used for data collection, validation, and clarification during the work.

Primary Interviews and Surveys

Primary work is used to pressure-test the crop mix, yield changes, and realized farm-gate pricing, especially where public data is delayed or reported in different units. We spoke with growers, aggregators, input and equipment participants, and downstream buyers, and feedback was gathered across the main farming areas of the Kingdom to confirm what is actually sold and at typical price points. These discussions also helped validate assumptions on protected cultivation adoption and how water constraints are shaping planting decisions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 17% | |

| Mid tier: 52% | Functional/Unit leaders: 30% | |

| Smaller Players: 17% | Managers: 53% |

Market-Sizing & Forecasting

Sizing is built from a top-down crop economics view where production by crop and cultivation type is reconstructed, then farm-gate value is formed using price and yield realities discussed by market participants. To keep the model practical, we track a short set of market fingerprints, including harvested area and yield shifts, the mix between protected and open-field cultivation, typical farm-gate price ranges by crop, irrigation and water-availability constraints, and seasonality that impacts volumes sold.

Once the headline total is created, it is corroborated with selective bottom-up approximations, such as sampled farm-gate price times volume checks for key crops, plus supplier and buyer channel checks to confirm that implied value movements match what participants are seeing. Where data is patchy for smaller crop groups, we apply transparent gap handling by using proxy crop pricing and conservative yield assumptions, followed by interview-led adjustments. Forecasts are built using scenario analysis, with variables like policy support, water management direction, and protected cultivation penetration guided by expert consensus so the final curve stays realistic for the Kingdom.

Data Validation & Update Cycle

Validation is done in layers so the final number is not driven by one dataset or one assumption. We compare outputs against independent signals like crop production trends, price direction, and consistency with constant-dollar conversion, then investigate large swings before sign-off. If a variance cannot be explained with a clear market event, we re-check inputs and re-contact selected respondents to confirm whether the change is real or caused by timing and unit differences.

The report is refreshed annually, and interim updates are made when material events affect crop output or pricing expectations. Before delivery, an analyst completes a fresh review pass so the client receives the latest updated view rather than an older snapshot.

Mordor Intelligence's the Kingdom of Saudi Arabia Agriculture Market Sizing Compared With Other Published Estimates

Published market values for Saudi agriculture can look far apart, even when they appear to cover the same topic. The main reasons are usually tied to what is counted as agriculture value, which year is used for constant-dollar conversion, and whether the number reflects farm-gate crops only or a wider food system view.

The biggest gap driver is scope expansion into livestock, aquaculture, or downstream processing, and in Mordor Intelligence's case the market is kept at farm-gate crop value only (field-grown plus protected crops) with values converted to constant 2024 USD using average central-bank rates. Other differences come from whether pricing is assumed from retail proxies instead of farm-gate realization, and whether the refresh cadence captures recent shifts in yields and protected cultivation economics.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 15.20 B (2026) | |

| Global Consultancy A | USD 14.80 B (2024) | Uses a different base year and forecast window, and the scope description is broader and may mix revenue and volume lenses, which can shift what is treated as agriculture value versus farm-gate crop receipts. |

| Industry Publisher B | USD 14.70 B (2026) | Often presented as an overall agriculture sector view, which can fold horticulture, livestock, and policy-driven procurement effects into one total, and it may not clearly separate farm-gate crop pricing from downstream value creation. |

The table shows that most of the spread is explained by scope choices and base-year handling, rather than a disagreement on the direction of growth. By sticking to a repeatable crop value build, checking farm-gate price realism through interviews, and holding currency conversion constant, the estimate remains easy to trace back to clear variables and simple steps.

Key Questions Answered in the Report

How large will Saudi Arabia agriculture sector be by 2031?

The Saudi Arabia agriculture market size is forecast to hit USD 20.30 billion by 2031, up from USD 15.20 billion in 2026.

Which crop dominates fresh-produce output?

Vegetables hold the largest share at 38% of 2025 value owing to high-yield greenhouse tomatoes and expanding leafy-green production.

How is Vision 2030 influencing farm investment?

Vision 2030 provides up to 75% project financing and 10-year tax holidays for water-efficient greenhouses, accelerating tech adoption.

Which regions produce most of Saudi Arabia fresh produce?

Al-Jouf, Tabuk, and Hail provinces supply about 65% of national output due to favorable microclimates and targeted infrastructure upgrades.

Page last updated on: