Brazil Freight Brokerage Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

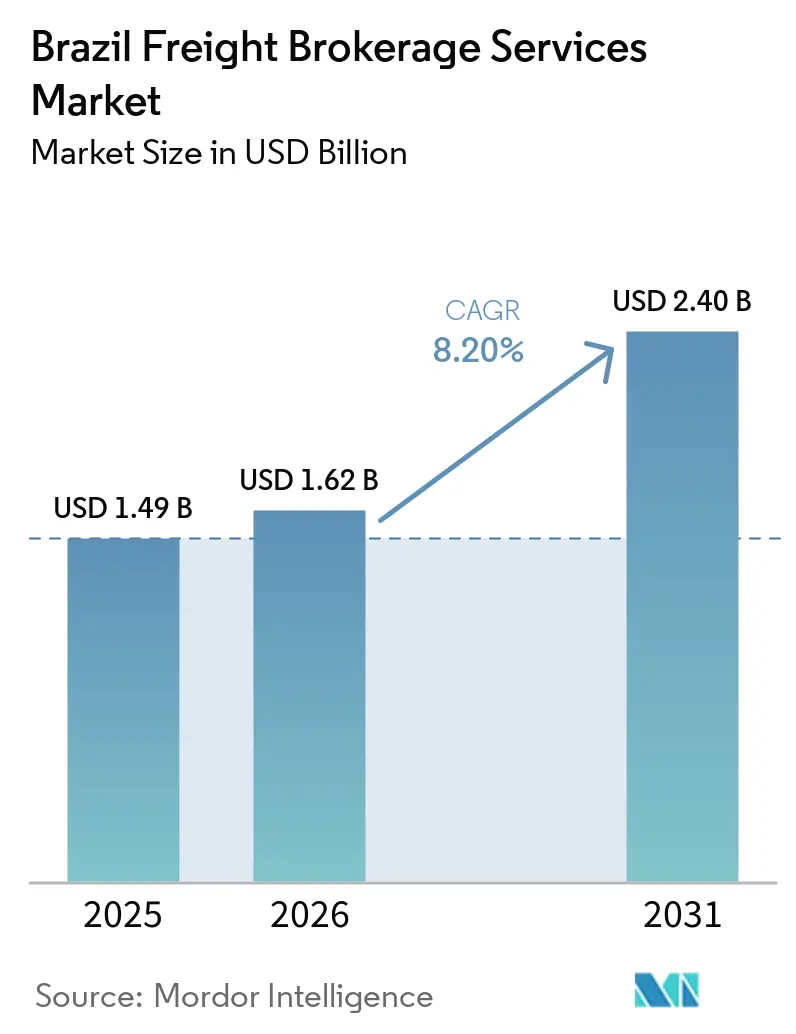

| Base Year Market Size (2025) | USD 1.49 Billion |

| Market Size (2026) | USD 1.62 Billion |

| Market Size (2031) | USD 2.40 Billion |

| Growth Rate (2026 - 2031) | 8.20% CAGR |

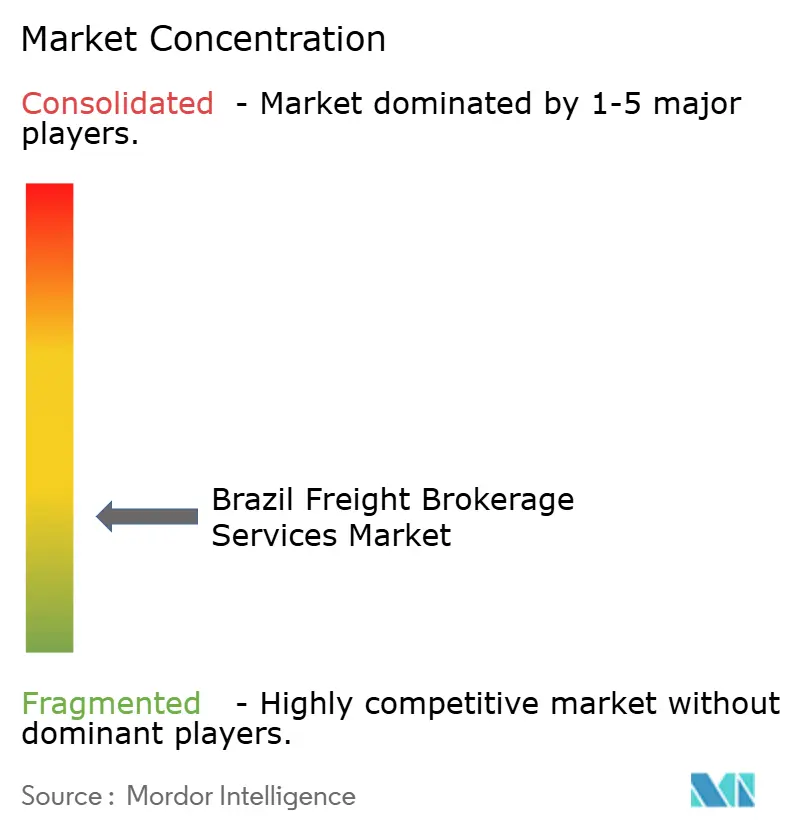

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Freight Brokerage Services Market Analysis by Mordor Intelligence

The Brazil freight brokerage market size is expected to grow from USD 1.49 billion in 2025 to USD 1.62 billion in 2026 and is forecast to reach USD 2.40 billion by 2031 at 8.2% CAGR over 2026-2031. Brazil’s emergence as Latin America’s top destination for nearshoring investment, the nationwide CT-e 4.0 e-documentation mandate, and BRL 161 billion (USD 32.2 billion) in planned toll-road concessions are reshaping competitive dynamics. Digital compliance demands and multimodal corridor build-outs raise the broker value proposition well beyond simple load matching, while embedded fintech and cargo-insurance APIs open new revenue streams. At the same time, port congestion in Santos and Paranagua, surging cyber threats, and exchange-rate volatility tighten operating margins, encouraging specialization in cold-chain, agribulk, and e-commerce lanes. Ongoing consolidation: Scan Global Logistics’ USD 102.35 million acquisition of Blu Logistics Brasil, and Cargo X’s unicorn valuation, signal that scale economics and technology depth now weigh as heavily as long-standing carrier relationships.

Key Report Takeaways

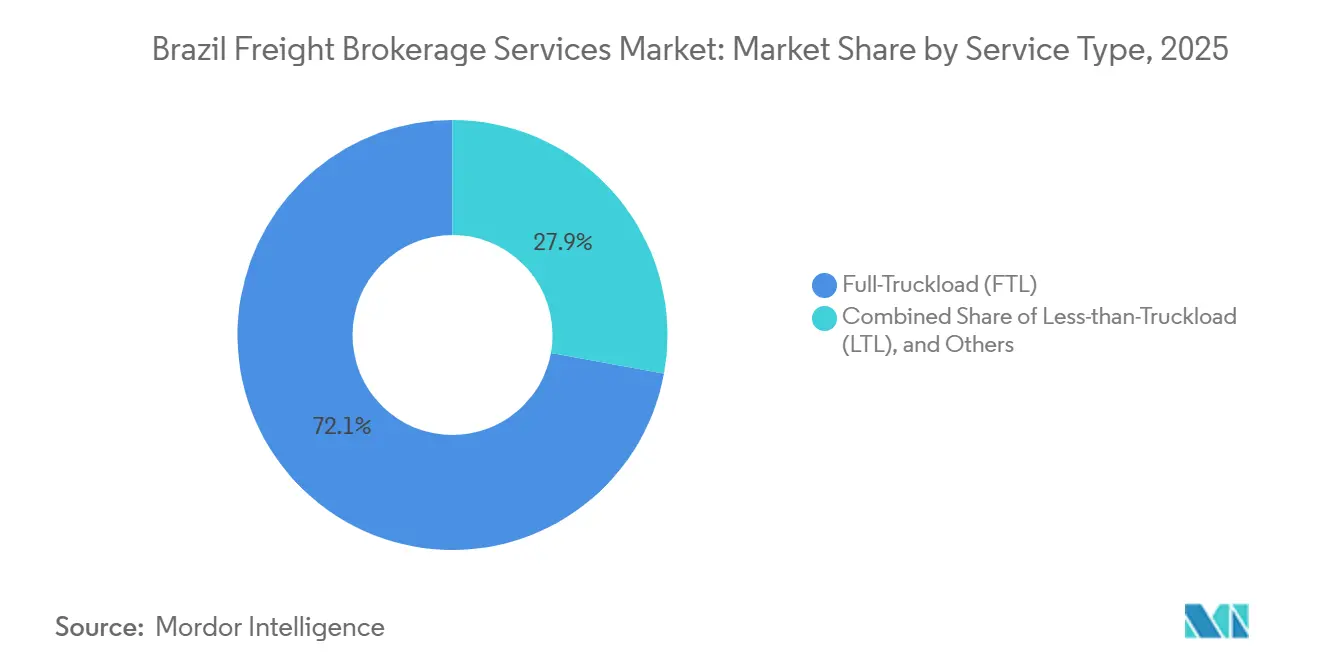

- By service, full-truckload held 72.13% of the Brazil freight brokerage market share in 2025, while less-than-truckload is projected to expand at 10.26% CAGR to 2031.

- By equipment type, dry van commanded 37.87% share of the Brazil freight brokerage market size in 2025, and refrigerated van is advancing at 10.52% CAGR through 2031.

- By haul length, long-haul accounted for 67.98% share, and local haul is forecast to grow at 12.61% CAGR between 2026 and 2031.

- By business model, traditional brokers held 78.30% share in 2025, whereas digital platforms are recording the fastest growth at 28.04% CAGR through 2031.

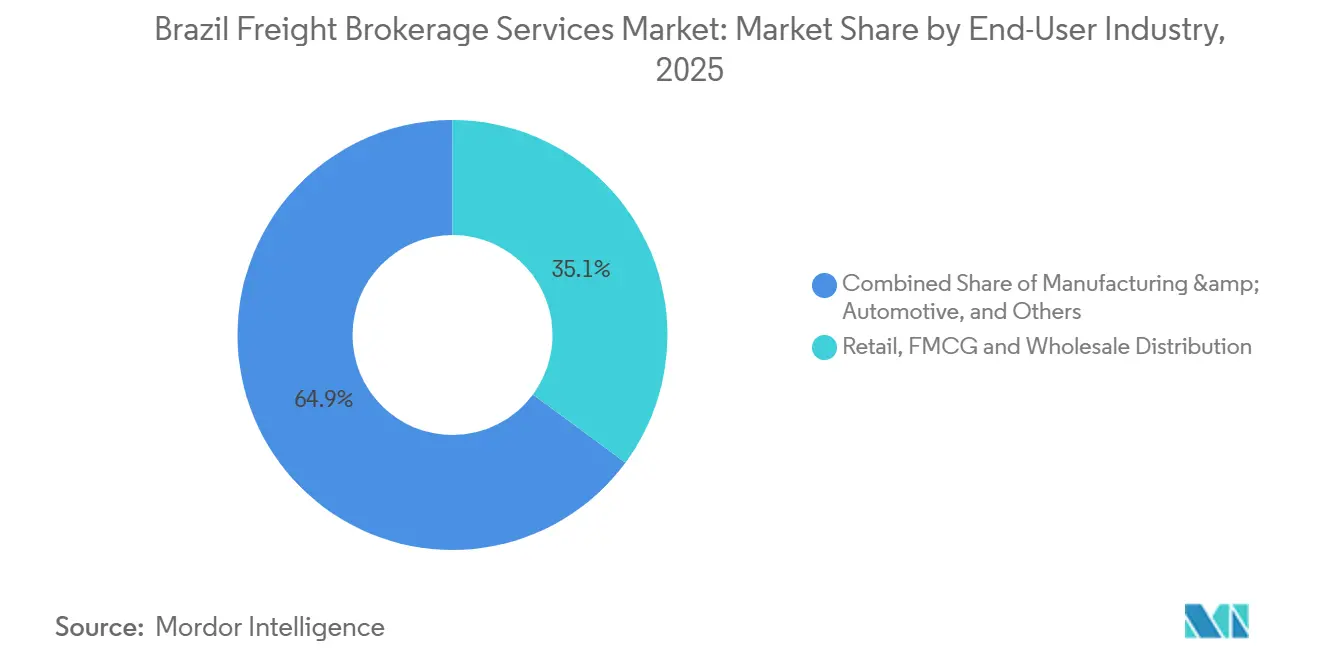

- By end-user, retail & FMCG led with 35.13% share, while e-commerce & 3PL fulfillment is expanding at 21.61% CAGR to 2031.

- By customer size, large enterprises captured 68.13% share in 2025, and small businesses are growing at 15.57% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Brazil participates in a competitive field that extends beyond its own borders. The market landscape in the global freight brokerage services industry outlined by Mordor Intelligence covers that wider structure.

Brazil Freight Brokerage Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Near-Shoring of Manufacturing Driving Domestic Freight Demand | +1.9% | Southeast industrial corridors, expanding to the Northeast | Medium term (2-4 years) |

| Nationwide Roll-Out of CT-e 4.0 E-Documentation Raising Broker Compliance Value | +1.6% | National, with enforcement concentrated in Sao Paulo, Rio | Short term (≤ 2 years) |

| New Rail and Toll-Road Concessions Enabling Integrated Multimodal Brokerage | +1.4% | Center-West to Santos/Paranagua corridors, Northern Arc | Long term (≥ 4 years) |

| Embedded Cargo-Insurance APIs Unlocking Ancillary Broker Revenue | +1.0% | National, led by digital-first brokers in major metros | Medium term (2-4 years) |

| Expansion of Center-West Agribulk Mini-Hubs Boosting First-Mile Brokerage | +1.3% | Mato Grosso, Goias, and Mato Grosso do Sul grain belts | Medium term (2-4 years) |

| Export-Market Carbon Reporting Spurring Route-Optimized Brokerage Solutions | +0.8% | Export-oriented corridors to Santos, Paranagua, Northern Arc | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated Near-Shoring of Manufacturing Driving Domestic Freight Demand

Record announcements of USD 95.5 billion in foreign direct investment during 2024 shifted production of automotive, electronics, and industrial equipment from Asia to Brazil, creating complex multi-leg freight needs. Manufacturing exports rose to USD 181.9 billion, strengthening year-round freight demand. Just-in-time production in the Sao Paulo-Rio-Minas corridors heightens the need for precise inbound component flows and synchronized outbound distribution. State tax incentives in Pernambuco and Bahia further redirect load volumes to emerging Northeast plants. Brokers that combine vendor-managed inventory with cross-docking offset line-stop risks for manufacturers and secure premium margins.

Nationwide Roll-Out of CT-e 4.0 E-Documentation Raising Broker Compliance Value

CT-e 4.0 mandates real-time data transmission and integration with ANTT’s CIOT payment platform, imposing fines of up to 10% of shipment value for errors. Automated validation of transporter credentials under the updated Vale-Pedagio Obrigatorio system intensifies technical hurdles. Digital brokers leveraging API-based tools now anchor pricing power on compliance assurance rather than purely on lane rates. SME shippers lacking logistics IT outsource documentation to brokers, creating ancillary revenue beyond base commissions. Early adopters report 30-40% reductions in manual data rework, translating into lower penalties and faster remittance cycles.

New Rail and Toll-Road Concessions Enabling Integrated Multimodal Brokerage

The 850-kilometer BR-153 contract awarded to Ecorodovias-GLP reduces Center-West grain transit to northern ports by 12 hours. Rail expansions by Rumo create new truck-rail interfaces that favor brokers with terminal expertise. Brokers bundle rail cost savings with guaranteed delivery windows and capture 3-4 percentage-point margins over pure road options. Integrated corridors also mitigate carbon footprints, supporting exporters preparing for EU CBAM tariffs[1]GLP, “Consortium wins Brazil highway concession,” glp.com .

Expansion of Center-West Agribulk Mini-Hubs Boosting First-Mile Brokerage

Mato Grosso’s record 2025 harvest tightened truck supply and pushed spot rates 20-50% above off-season norms. Mini-hub terminals with 50,000-100,000 ton silos consolidate farm-gate pickups into unit-train consignments, improving asset turns. Brokers organize staggered loading windows, align moisture testing, and manage fumigation certificates. Northern Arc ports now capture 30% of grain exports, giving brokers routing alternatives when Santos backlogs escalate. Grain traders prioritize brokers offering harvest-window capacity guarantees, raising switching costs for growers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Highway Toll Rates Compressing Brokerage Margins | -1.2% | National, concentrated on major concession routes | Short term (≤ 2 years) |

| Chronic Congestion at Santos & Paranagua Ports Undermining Delivery Reliability | -1.0% | Southeast export corridors, affecting 70% of containerized freight | Medium term (2-4 years) |

| Surge in Cyber-Attacks on Digital Freight Platforms Increasing Compliance Costs | -0.7% | National, targeting digital-first brokers and platforms | Short term (≤ 2 years) |

| Exchange-Rate Volatility Complicating Long-Term Freight Contract Pricing | -0.9% | National, acute for export-oriented shippers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Highway Toll Rates Compressing Brokerage Margins

Concession contracts permit 15-20% real toll hikes above inflation to fund upgrades, lifting tolls to 8-12% of freight spend on long-haul corridors. Brokers operating on fixed 5-7% commissions absorb margin erosion when shippers resist matching rate increases. Mandatory electronic toll payments under Vale-Pedagio add administrative overhead, while large retailers demand line-item pass-through bills. Cost-plus models gain favor, yet price-sensitive FMCG accounts still benchmark against pre-concession averages, capping broker recovery potential.

Chronic Congestion at Santos & Paranagua Ports Undermining Delivery Reliability

Santos handles 40% of national containers, with peak-season truck queues stretching 30 kilometers and demurrage reaching USD 200 per box per day after free-time expiry. Brokers reroute via Itajai or Suape, adding 200-400 kilometers to inland hauls and 12-18% to landed costs. Exporters shipping during the March-July grain rush pay premiums for guaranteed loading slots, yet still suffer reliability penalties on European retail scorecards[2]APM Terminals, “Consolidation of Hub Ports in Brazil,” apmterminals.com.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Load Fragmentation Raises LTL Velocity

Less-than-truckload captured a 10.26% CAGR through 2031 as online retail parcelization forces shippers to consolidate micro-shipments, while full-truckload retained a dominant 72.13% share of the Brazil freight brokerage market size in 2025. The Brazil freight brokerage market benefits when LTL brokers pool cargo across omnichannel retailers, backfilling empty capacity on return legs and trimming dead-head miles. New urban fulfillment centers inside Sao Paulo’s macro-ring shorten average stage lengths to 41 miles, making LTL tariffs compelling relative to dedicated vans.

E-commerce giants like Mercado Livre and Amazon deploy proprietary networks yet still outsource overflow to brokers during peak events, such as Black Friday, when volumes jump 30-50%. FTL lanes remain anchored by agricultural exports; recurring Mato Grosso-to-Santos grain hauls run 1,000 kilometers and exhibit limited consolidation potential, sustaining FTL’s high Brazil freight brokerage market share. Brokers differentiate through proprietary pricing engines that recompute break-bulk points in real time, optimizing hub sequences to meet next-day delivery promises.

By Equipment Type: Cold-Chain Modernization Outpaces Dry Capacity

Dry vans held 37.87% of Brazil freight brokerage market share in 2025, thanks to their versatility across FMCG and industrial freight, yet refrigerated vans are projected to outstrip overall growth at 10.52% CAGR. The Brazil freight brokerage market size tied to cold-chain is swelling as chicken, beef, and pharmaceutical regulations toughen temperature auditing.

ANVISA’s RDC 430 imposes electronic logging for humidity and temperature, prompting brokers to deploy IoT sensors and cloud dashboards. Cold-chain premiums average 18-22% over dry tariffs, lifting brokerage gross margins even after higher insurance at 0.25-0.30% of cargo value. Flatbed and step-deck equipment ride infrastructure investment cycles; steel girder and cement module moves spike whenever toll-road PPPs break ground. Tanker loads track Brazil’s biodiesel mandates, growing a steady 5-6% but demanding stringent cleaning certificates that only specialized brokers handle.

By Haul Length: Urban Density Fuels Local Acceleration

Long-haul lanes kept 67.98% of Brazil's freight brokerage market share in 2025, yet local hauls under 100 miles are registering 12.61% CAGR on the back of micro-fulfillment and same-day delivery models. The Brazil freight brokerage market size attached to last-mile surged when warehouse vacancy hit 8.3% in Sao Paulo, compelling retailers to scatter stock across multiple nodes.

Local brokers orchestrate 3-4-stop milk-runs, exploit off-peak urban windows, and aggregate returns, techniques that asset-heavy long-haul players find uneconomical. Regional hauls bridge state capitals to tier-two cities and grow at 7-8%, offering midpoint opportunities where brokers balance speed against toll escalation. Infrastructure upgrades on BR-116 and BR-465 shave 25 minutes off the Rio-Belo Horizonte run, letting brokers re-engineer driver hours-of-service and cut dwell.

By Business Model: Technology Platforms Erode Traditional Strongholds

Traditional shops still command 78.30% share through deep shipper relationships and CT-e 4.0 proficiency, but digital platforms are scaling at 28.04% CAGR. The Brazil freight brokerage market size is tilting as algorithmic matching trims dead-head by 12-15%, enabling rate cuts that lure SME shippers.

Cargo X integrates toll, fuel, and insurance APIs into one checkout, shrinking booking to under four minutes. Traditional incumbents retaliate through mergers, such as JSL’s acquisition of Marvel Logistica, layering tech onto branch networks. Asset-based brokers exploit dedicated fleets to lock in automotive and beverage contracts, while agent-model networks expand geographic reach without ballooning SG&A.

By End-User Industry: Digital Retail Outpaces Conventional Verticals

Retail & FMCG owned 35.13% share in 2025 because of high shipment frequency and year-round demand, but e-commerce & 3PL fulfillment posts a blistering 21.61% CAGR. The Brazil freight brokerage market taps API links to order management systems, giving online sellers real-time capacity reservations.

Agriculture and food cargo, valued at USD 164.4 billion in exports, underpins cold-chain growth and seasonal rate spikes. Healthcare freight accelerates under ANVISA compliance, while construction materials ride PPP project pipelines. Oil, gas, and mining keep stable lanes to export terminals, but chemical ADR regulations narrow carrier pools, reinforcing broker gatekeeping roles.

By Customer Size: Fintech Opens the Long-Tail of SMEs

Large enterprises retained 68.13% share owing to scale procurement, yet small businesses below USD 10 million revenue are expanding at 15.57% CAGR on fintech factoring and instant quoting. The Brazil freight brokerage market unlocks trapped demand as platforms drop minimum loads to USD 500 and finance receivables within 48 hours.

goFlux’s USD 6 million raise targets underbanked farmers, marrying freight bids with working-capital advances on confirmed harvest contracts. Mid-market shippers lean on brokers for multimodal architecture yet still prize rate transparency. Currency volatility pushes exporters to seek brokers offering BRL hedging or USD-denominated contracts, adding financial-service overlays to core freight offerings.

Geography Analysis

The Southeast holds around 55% of Brazil freight brokerage market share, anchored by Sao Paulo’s industrial belt and Santos port’s 40% container throughput. Warehouse scarcity in Campinas and Guarulhos tightens last-mile lead times, raising broker premiums for off-peak slotting.

The Center-West delivers the fastest 13% CAGR as Mato Grosso grain production stretches road and rail networks. The 850-kilometer BR-153 concession slashes bottlenecks to northern ports, encouraging brokers to price fixed-date contracts and capture modal shift savings. Record harvests drive surge freight, but limited paved road density elevates first-mile brokerage complexity. Mini-hubs in Sorriso and Rondonopolis aggregate soy and corn, allowing brokers to tender full unit-trains for export elevators.

Northern Brazil remains infrastructure-challenged, with only 15.1% of roads paved and 41% rated poor. Brokers layer river barges with short-haul trucking to reach Belem and Santarém ports, mitigating high diesel costs. The Amazon-LATAM Cargo pact adds two-day air service to 11 states, broadening premium options for electronics and pharma shippers. The Northeast capitalizes on Suape and Pecem expansions, courting European reefers and reducing reliance on congested southern gateways[3]BNamericas, “BNDES supports modernization of EcoRioMinas highway,” bnamericas.com.

Mordor Intelligence provides coverage of the freight brokerage services market across other key regional markets, including North America and Europe, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to Canada, Mexico, Netherlands, Spain, Spain, Poland, and Saudi Arabia incorporating local coverage and market participation, as required.

Competitive Landscape

Brazil hosts more than 500 active brokers, with no single player exceeding 5% share, making the Brazil freight brokerage market low concentrated. JSL Logistica operates 3,600 trucks across 15 states, leveraging asset-based security to court automotive accounts. Cargo X’s AI-driven marketplace manages 1 million monthly searches and lists Heineken and Nestlé among top shippers, underscoring technology’s pull on blue-chip demand[4]Tracxn, “Cargo X – Company profile,” tracxn.com.

Scan Global Logistics’ USD 102.35 million acquisition of Blu Logistics Brazil deepens north-south coverage and signals foreign appetite for beachhead assets. Domestic consolidators focus on vertical expertise: BSoft dominates pharma cold-chain; Flash Courier controls same-day parcels; and AgriTrans specializes in grain drayage from Mato Grosso silos. Digital entrants funnel venture capital into cybersecurity after ransomware incidents rose 38% in 2024, allocating up to 4% of topline to ISO 27001 frameworks.

Competitive scaling hinges on compliance mastery. CT-e 4.0 validation, ICMS rebate automation across 26 states, and minimum freight-floor adherence separate premium brokers from low-service rivals. Sustainability analytics now rank as differentiators; platforms embedded with CO₂ calculators win European exporter bids seeking CBAM readiness. Broker margins cluster at 8-10% on dry lanes and 12-14% on refrigerated loads, with digital cost efficiencies offset by higher tech amortization.

Brazil Freight Brokerage Services Industry Leaders

FreteBras

CargoX

C.H. Robinson Worldwide

DHL Supply Chain

BBM Logistics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Loggi Tecnologia expanded last-mile and middle-mile logistics capacity to support rising e-commerce demand across Brazil.

- May 2025: Truckpad improved digital freight matching platform connecting truck drivers and shippers across Brazil.

- April 2025: DHL expanded contract logistics operations in Brazil, driven by strong e-commerce and healthcare demand.

- March 2025: Maersk expanded end-to-end logistics capabilities in Brazil, integrating inland transport and port services

Brazil Freight Brokerage Services Market Report Scope

| Full-Truckload (FTL) |

| Less-than-Truckload (LTL) |

| Others |

| Dry Van |

| Refrigerated Van |

| Flatbed / Step-Deck |

| Tanker (Bulk Liquid and Chemical) |

| Others |

| Long-Haul (More than 500 miles) |

| Regional (100-500 miles) |

| Local (Less than 100 miles) |

| Traditional Freight Brokerage |

| Asset-Based Freight Brokerage |

| Agent Model Freight Brokerage |

| Digital Freight Brokerage |

| Manufacturing and Automotive |

| Construction and Infrastructure Projects |

| Oil, Gas, Mining and Chemicals |

| Agriculture and Food / Beverage |

| Retail, FMCG and Wholesale Distribution |

| Healthcare and Pharmaceuticals |

| E-commerce and 3PL Fulfilment |

| Other End-User Industry |

| Large Enterprise Shippers (More than USD 100 M) |

| Mid-Market Shippers (USD 10-100 M) |

| Small Businesses (Less than USD 10 M) |

| By Service | Full-Truckload (FTL) |

| Less-than-Truckload (LTL) | |

| Others | |

| By Equipment / Trailer Type | Dry Van |

| Refrigerated Van | |

| Flatbed / Step-Deck | |

| Tanker (Bulk Liquid and Chemical) | |

| Others | |

| By Haul Length | Long-Haul (More than 500 miles) |

| Regional (100-500 miles) | |

| Local (Less than 100 miles) | |

| By Business Model | Traditional Freight Brokerage |

| Asset-Based Freight Brokerage | |

| Agent Model Freight Brokerage | |

| Digital Freight Brokerage | |

| By End-User Industry | Manufacturing and Automotive |

| Construction and Infrastructure Projects | |

| Oil, Gas, Mining and Chemicals | |

| Agriculture and Food / Beverage | |

| Retail, FMCG and Wholesale Distribution | |

| Healthcare and Pharmaceuticals | |

| E-commerce and 3PL Fulfilment | |

| Other End-User Industry | |

| By Customer Size | Large Enterprise Shippers (More than USD 100 M) |

| Mid-Market Shippers (USD 10-100 M) | |

| Small Businesses (Less than USD 10 M) |

Key Questions Answered in the Report

How fast is the Brazil freight brokerage market growing?

The market is projected to grow at a CAGR of 8.2% during 2026–2031, reaching USD 2.40 billion by 2031.

Which service type is expanding the quickest?

Less-than-truckload is the fastest, advancing at 10.26% CAGR as e-commerce parcelization multiplies consolidated shipments.

Why is refrigerated equipment in high demand?

Stricter ANVISA rules and rising agrifood exports are pushing refrigerated van volumes, delivering a 10.52% CAGR through 2031.

What makes the Center-West region attractive to brokers?

Record grain harvests and new BR-153 concessions reduce transit times to northern ports, driving a regional CAGR of 13%.

How are digital platforms changing the competitive landscape?

Algorithmic load matching, embedded fintech, and CT-e 4.0 compliance automation enable digital brokers to grow at 28.04% CAGR, eroding traditional incumbents’ share.

What risks could hinder broker profitability?

Escalating highway tolls, chronic port congestion, higher cybersecurity spending, and BRL/USD volatility can compress margins when not hedged properly.

Page last updated on: