Russia Freight Brokerage Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

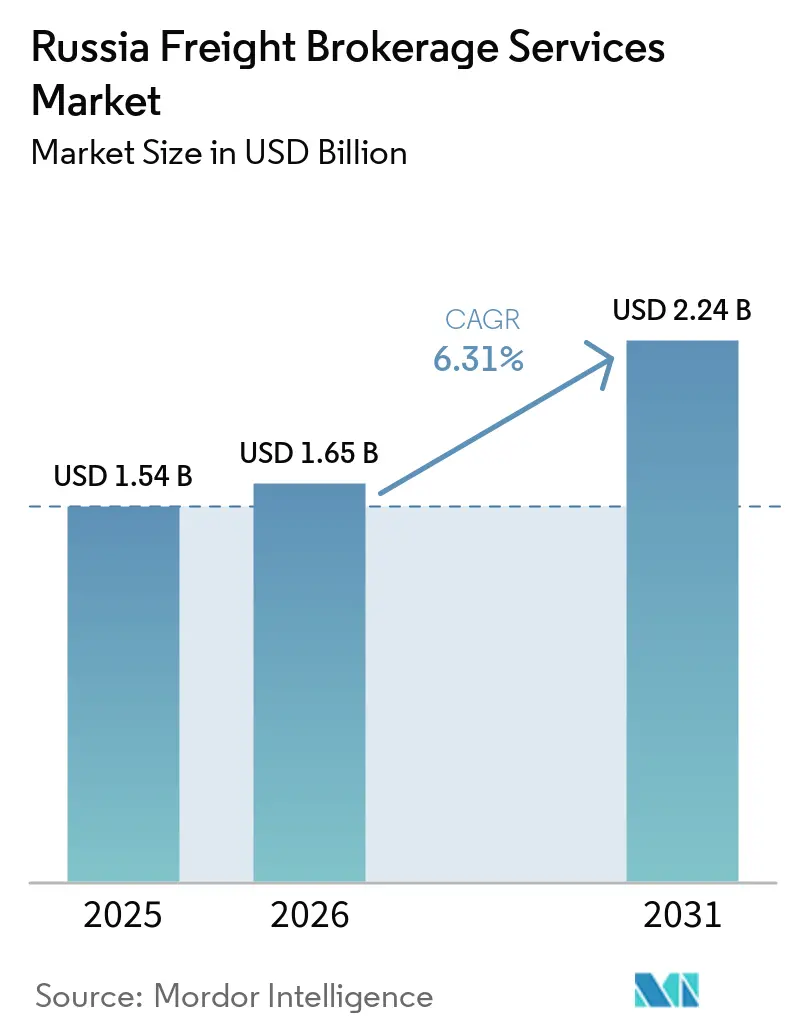

| Base Year Market Size (2025) | USD 1.54 Billion |

| Market Size (2026) | USD 1.65 Billion |

| Market Size (2031) | USD 2.24 Billion |

| Growth Rate (2026 - 2031) | 6.31% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Russia Freight Brokerage Services Market Analysis by Mordor Intelligence

The Russia freight brokerage services market size is projected to expand from USD 1.54 billion in 2025 and USD 1.65 billion in 2026 to USD 2.24 billion by 2031, registering a CAGR of 6.31% between 2026 to 2031.

Intensifying east- and south-bound trade corridors, compulsory electronic waybill adoption, and widening e-commerce fulfilment footprints are reshaping contract structures and rate discovery mechanisms. Digital platforms have moved load-matching cycles from hours to minutes, tightening spread opportunities yet raising transaction velocity. As international trade corridors shift eastward and southward, domestic logistics infrastructure is being modernized. This expansion in the sector is overshadowed by these significant changes. Brokers face a unique challenge: navigating the complexities of sanctions-driven payments while also embracing the rapid rise of digital platforms. Those who can adeptly balance compliance and algorithmic freight matching stand to gain. While government initiatives like electronic waybill systems and digitized border queues aim to streamline transactions, the carrier base is shrinking under financial strain. In 2024, rail freight volumes fell by 3.3% to 1.308 billion tons, contrasting with a surge in road transport. This shift is reshaping the economics of transport modes and altering broker service offerings. Capacity attrition 20% of small carriers are forecast to exit by end-2025 has begun to tilt bargaining power toward brokers that can guarantee equipment availability during peak seasons.

Key Report Takeaways

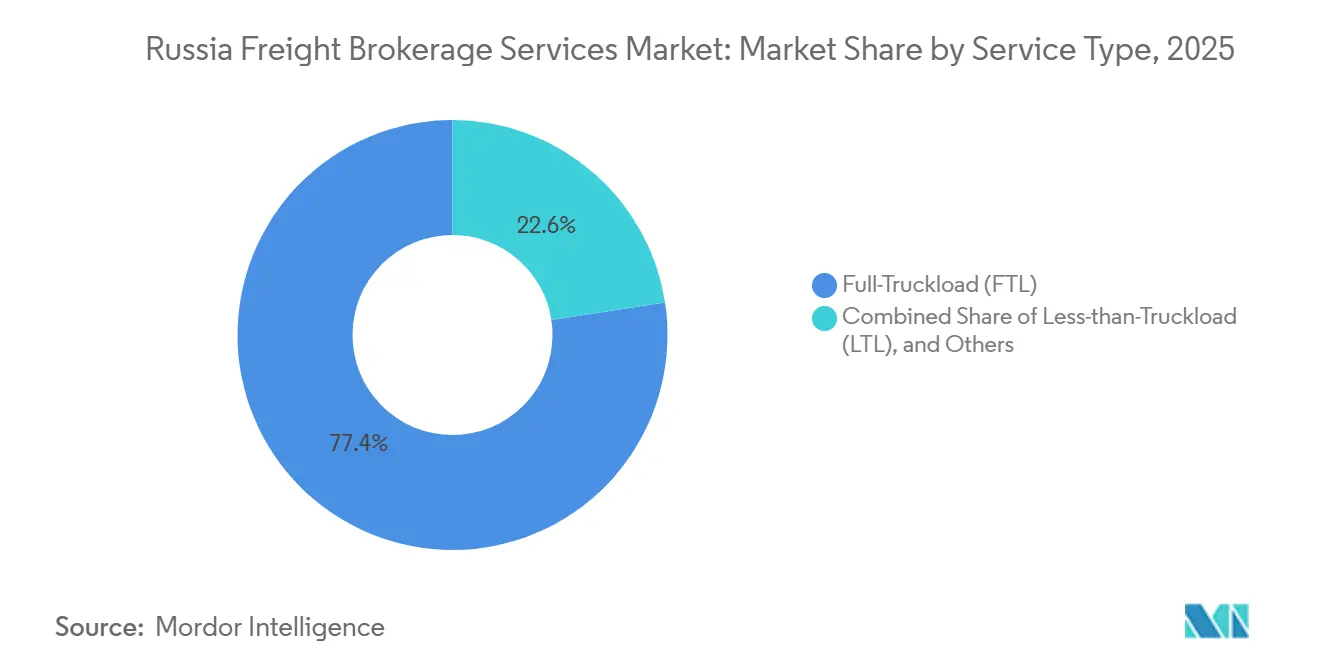

- By service, full-truckload captured 77.41% of the Russia freight brokerage services market share in 2025, while Less-than-Truckload is projected to advance at an 8.79% CAGR through 2031.

- By equipment type, dry van commanded 28.56% share of the Russia freight brokerage services market size in 2025, whereas refrigerated van capacity is forecast to rise at an 8.88% CAGR between 2026 and 2031.

- By haul length, long-haul routes held 71.25% of the Russia freight brokerage services market share in 2025; while local hauls under 100 miles will expand at an 11.24% CAGR to 2031.

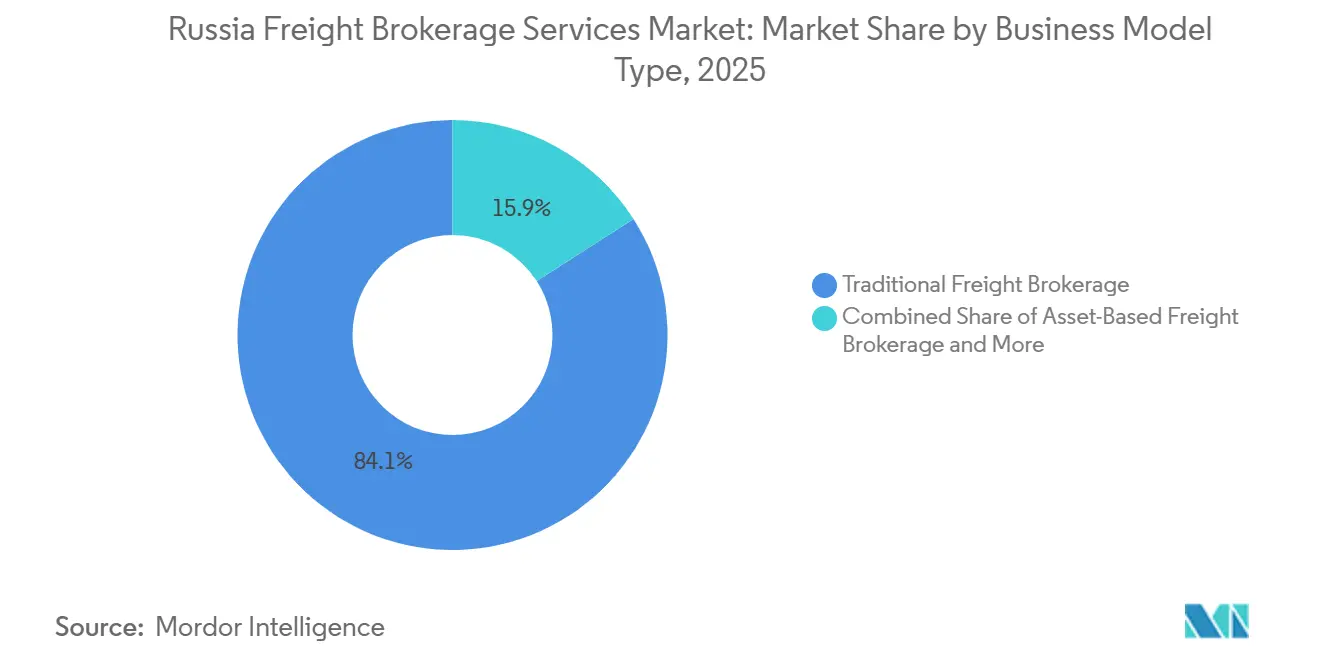

- By business model, traditional brokerage controlled 84.06% market share in 2025, whereas digital brokerage volume is set to grow 24.51% annually through 2031.

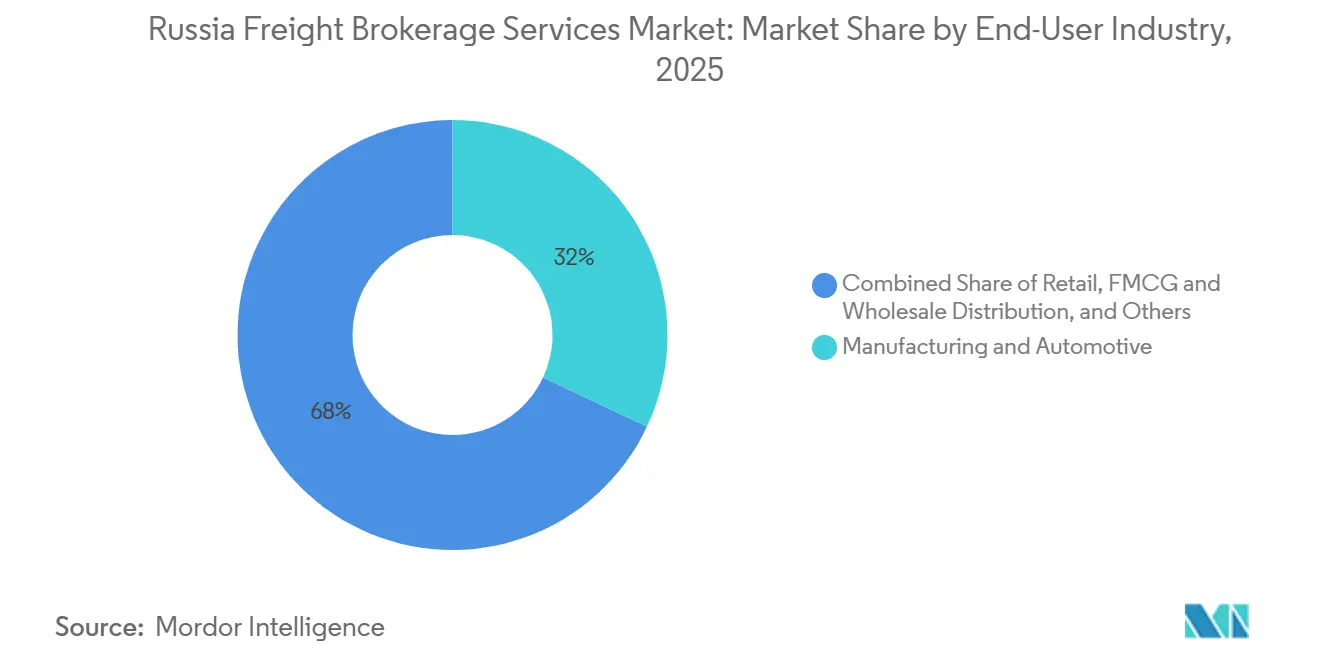

- By end-user, manufacturing and automotive accounted for 32.00% of the 2025 market size, yet the e-commerce and 3PL fulfilment segment is projected to grow at a 17.94% CAGR through 2031.

- By customer size, large enterprise shippers accounted for 75.13% of the Russia freight brokerage services market share in 2025, while small businesses segment is forecast to post the fastest 16.58% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Understanding the full system requires moving beyond Russia boundaries into a wider international view. Mordor Intelligence captures the global freight brokerage services market scope in its worldwide coverage.

Russia Freight Brokerage Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| INSTC-driven multimodal volume surge | +1.3% | Caspian gateways, North Caucasus | Medium term (2-4 years) |

| Far-East bonded terminals accelerating China trade | +1.5% | Primorsky Krai, Zabaikalsk | Short term (≤2 years) |

| Ruble weakness boosting bulk-export freight flows | +0.9% | Commodity-producing regions | Short term (≤2 years) |

| Domestic e-truck fleets & battery-swap depots | +0.6% | Moscow-St Petersburg axis | Long term (≥4 years) |

| Dynamic highway tolling stimulating algorithmic brokerage | +0.8% | Platon-covered network | Medium term (2-4 years) |

| Classified-cargo boom requiring licensed secure brokers | +0.7% | Defense-industrial clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

INSTC-Driven Multimodal Volume Surge

In 2025-2026, the INSTC has become a critical multimodal driver for Russian freight brokers by integrating rail, sea, and road cargo flows, enabling end-to-end packaging, with strong linkages to Russia rail freight transport networks. Corridor throughput highlights this growth, with 2024 traffic at 26.9 million tons and 2025 container volumes projected at 11,000-11,500 TEU, signaling a shift to steady commercial operations. The eastern INSTC route reduces transit times to around 16 days from Moscow to Bandar Abbas, enhancing shipper confidence and repeat bookings. Cost reductions, including a 30-50% drop in route fees and a 56% decrease in eastern-route service costs, have made the corridor more competitive. The corridor has transitioned from a geopolitical option to a commercially viable service, with regular container operations, upgraded ports, and improved reverse-load opportunities [1]“Electronic Waybill Adoption Statistics 2026,” Ministry of Transport of the Russian Federation, mintrans.gov.ru. End-to-end electronic seals trialed in 2025 have cut re-inspection delays by 23%, further amplifying brokerage throughput.

Far-East Bonded Terminals Accelerating China Trade

FESCO’s EUR 40 million (USD 47.05 million) Zabaikalsk logistics hub, inaugurated in April 2025, cut transhipment dwell time to 26 hours and lifted daily truck slots by 38%. Bonded status lets Asian exporters stage inventory inside Russia without immediate duty payment, spiking spot-load listings on Vladivostok exchanges by 31% quarter-on-quarter. Brokers that pre-book electronic border queues via GIS EPD secure predictable lead times and win loyalty from electronics and apparel shippers sensitive to seasonal launches[2]“North-South and East-West Corridor Upgrades,” Rossiyskaya Gazeta, rg.ru.

Ruble Weakness Boosting Bulk-Export Freight Flows

Depreciation of the ruble against major trading currencies widened netbacks for fertilizer, lumber, and metals producers, pushing fertilizer rail carloads up 9.1% in 2024 despite an overall rail slump. Brokers arranging dry-bulk movements through Baltic trans-shipment points report 14% higher volume commitments as exporters chase hard-currency receipts. However, informal settlement channels elevate compliance vetting costs, increasing reliance on brokers versed in sanctions-screened payment flows.

Domestic E-Truck Fleets and Battery-Swap Depots Creating Premium Lanes

Battery-swap depots, alongside zero-emission freight corridors, are enhancing the feasibility of electric Class 8 trucking. By minimizing downtime, these innovations facilitate extended duty cycles. Recent pilot programs and the establishment of new corridors underscore the transition of this model from mere concept to tangible operations. Shippers, including grocers and pharmaceutical companies, are driving demand, placing a premium on certified zero-emission transport. Meanwhile, brokers and freight platforms are capitalizing on this trend, marketing these eco-friendly services as premium "green lane" offerings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Certified driver shortage amid mobilization and ageing workforce | -1.2% | Nation-wide | Short term (≤2 years) |

| Diesel-price volatility squeezing margins | -0.9% | Long-haul corridors | Short term (≤2 years) |

| Escalating ransomware on TMS platforms | -0.7% | Digital hubs | Medium term (2-4 years) |

| Stricter seasonal axle-weight limits | -0.6% | Siberia, Far-East roads | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Certified Driver Shortage amid Mobilization and Ageing Workforce

Cross-border lanes are feeling the pinch of certified driver shortages. The demand for drivers with language skills, specific licensing, and ADR-style qualifications has surged. Coupled with policy shifts and a limited recruitment pipeline, this has led to a constrained supply. Wage pressures are also on the rise. Industry sources indicate significant pay increases in 2025. As a result, brokers find themselves in a tight spot: they either extend tender lead times, pay a premium for the few qualified drivers available, or face penalties for missed slots.

Diesel-Price Volatility Squeezing Brokerage Margins

Brokerage margins are being squeezed by diesel volatility. Fuel costs can surge more rapidly than spot prices, putting fixed-rate contracts at risk and widening the gap between operating costs and revenue. Consequently, numerous brokers and carriers are pivoting to floating fuel surcharges. These are now linked to external benchmarks, like Argus-style indexes, enhancing transparency in cost pass-throughs and mitigating the risk of sudden fuel spikes[3]“Margin Compression in Road Freight 2025,” Trans.ru, trans.ru.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: LTL Granularity Outpaces FTL Scale

The Russia freight brokerage services market share attached to Full-Truckload lanes reached 77.41% in 2025, reflecting entrenched industrial demand. In contrast, Less-than-Truckload revenue stood visibly lower yet expanded 270 basis points faster year-on-year as e-commerce consignments mushroomed. It is growing at 8.79% CAGR through 2031. Russia freight brokerage services market share for FTL is set to slip marginally by 2031 as omnichannel retailers divert replenishment volumes into hub-and-spoke LTL routes.

Hybrid networks now superimpose scheduled milk runs atop ad-hoc spot moves, allowing brokers to double backhaul utilization. GIS EPD’s electronic proof-of-delivery cuts LTL paperwork cycles from 48 hours to five minutes, favouring tech-adept operators[4]“Russian E-Commerce Reaches ₽19.9 Trillion,” TAdviser, tadviser.ru.

By Equipment / Trailer Type: Cold Chain Premium Intensifies

Dry van continues as the workhorse with 28.56% Russia freight brokerage services market share, yet plug-in-ready Reefer Van slots trade at 15-20% rate premiums. Rural agribusiness clusters in Kuban and Stavropol ship berries and deep-frozen meat to Gulf markets, amplifying refrigerated demand that brokers scramble to secure amid import restrictions on EU-built units.

Russia freight brokerage services market share attached to refrigerated lanes is forecast to expand by 8.88% CAGR through 2031, propelled by double-digit growth in pharma cold-chain mandates under Russia’s Chestny ZNAK serialization regime.

By Haul Length: Local Density Challenges Line-Haul Primacy

In 2025, long-haul corridors exceeding 500 km command a dominant 71.25% market share, facilitating inter-regional flows such as Moscow to Novosibirsk and St. Petersburg to Vladivostok. Meanwhile, local movements under 100 km are witnessing a robust expansion at an 11.24% CAGR, projected to continue through 2030.

In Moscow's MKAD ring and the heart of St. Petersburg, local density drives daily vehicle turns: 5-6 for groceries and electronics, compared to just 1.5-2 for line-haul. This disparity results in truck fees that are twice as lucrative. While congestion tolls and last-mile fines in major federal cities chip away 8-12% from profit margins, brokers are increasingly gravitating towards curb-management APIs and real-time pricing solutions, notably on platforms like ATI.SU. The push for 24-hour fulfillment mandates agile carrier matching and the establishment of micro-hub networks in densely populated areas.

By Business Model: Platform Brokers Capture Network Effects

Digital brokerage gross transaction value is projected to grow at 24.51% CAGR by 2031, grabbing incremental Russia freight brokerage services market share as mobile onboarding and instant payment reconciliation become table stakes. Traditional players retain legacy through 84.06% market share and enterprise portfolios, but face talent drain to tech firms offering data-science career paths.

Embedded fuel-card and micro-lending programs on top platforms drive client retention, with ATI.SU logging over 300,000 verified carriers after April 2025’s T-ID rollout ATI.SU.

By End-User Industry: Marketplace Fulfilment Recasts Volume Mix

Manufacturing and automotive still anchors 32.00% of 2025 market share, yet chip import curbs and localized supply loops cap medium-term momentum. In stark contrast, Russia freight brokerage services market size allocated to e-commerce and 3PL fulfilment is tracking a 17.94% CAGR, underpinned by 45% online retail growth in 2024.

Marketplace drop-ship models require inventory touches at four to six regional sort centres, multiplying brokerage invoices per order versus factory-to-dealer moves. Temperature-controlled grocery deliveries and flash-sale electronics campaign peaks further spike ad-hoc lane bidding.

By Customer Size: SMEs Ride Platform Democratization

Large enterprises accounted for 75.13% of market share, but SMEs outpaced them with a remarkable 16.58% CAGR growth through 2030, thanks to digital platforms eliminating minimum-load thresholds. Platforms like ATI.SU, using automatic rating engines, quotes SME loads in under 60 seconds. This innovation skips manual credit checks, allowing regional bakeries and exporters to book shipments alongside major retailers.

While SME shipment values are generally lower, their collection cycles average just 7 days, compared to over 24 days for conglomerates. This quicker turnaround helps stabilize broker cash flow, especially during spot-rate fluctuations. Platforms, seizing LTL volumes in the Far East and North Caucasus, witnessed a growth spurt of 65-68%. Here, features like embedded finance and real-time tracking have become pivotal, especially for smaller shippers.

Geography Analysis

European Russia remains the volume nucleus, yet saturation caps its five-year growth to mid-single digits. The Far East leverages bonded terminals and Chinese origin-demand, booking double-digit gains despite episodic customs seizures of dual-use cargo. Siberia’s timber and mineral streams pivot south toward INSTC depots, diverting flow away from congested Baltic exits.

North-South corridor upgrades around Makhachkala and Derbent slashed transit times by 18% in pilot convoys, resurrecting Caspian Ro-Ro routes neglected since 2010. Meanwhile, 65-68% e-commerce order growth in the North Caucasus is spawning micro-fulfilment depots that feed next-day truck drayage into Dagestan and Chechnya hill towns.

The Russia freight brokerage services market size benefits as brokerage penetration climbs in previously underserved geographies; brokers translate urban platform models to smaller cities such as Vladikavkaz and Khabarovsk, widening the addressable shipper base.

Mordor Intelligence examines the freight brokerage services market across diverse other regional markets as well, including Europe and North America, while also offering granular country-level perspectives for Spain, Spain, Canada, Saudi Arabia, Brazil, South Africa, and South Korea and more.

Competitive Landscape

In 2025-2026, the Russia freight brokerage market is increasingly leaning towards platform dominance. Recent market analyses from 2025 highlight a pronounced concentration in the digital segment. Here, the top five platforms command a staggering 95% of the segment's volume, with digital newcomers outpacing traditional brokers in growth. ATI.SU is bolstering its competitive edge through API connectivity, enhanced GPS milestone visibility, and banking-integrated payment systems. Meanwhile, GIS EPD and the newly introduced GosLog regime are elevating electronic documentation from a mere differentiator to a fundamental requirement.

Fura’s 2024 acquisition of НТК remains highly relevant in 2025. This move not only broadened the verified carrier base to approximately 200,000 but also reinforced scale economics, echoing the consolidation trends currently shaping the market. Traditional players, like Delovye Linii, are pivoting towards a hybrid model. Their 2025 mobile app and LTL tools exemplify how established operators are leveraging self-service booking, tracking, and multimodal features to retain small and medium-sized business (SMB) clientele.

While carrier exits and a shrinking fleet favor asset-light brokers in securing spot capacity, 2026 regulatory changes are inflating costs related to compliance, IT integration, and data storage. This surge in expenses poses challenges for smaller portals lacking the advantage of scale. In the current landscape, cyber-resilience, sanctions screening, and secure digital payment processes have gained prominence in RFP evaluations. This shift underscores the market's tight integration with electronic records, centralized oversight, and cohesive settlement systems.

Russia Freight Brokerage Services Industry Leaders

Delovye Linii

CDEK Logistics

VTN (Vneshtrans)

ATI.SU

Transit LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Delovye Linii launched a new air transportation division in Irkutsk, seizing the opportunity presented by a surge in demand in Siberia and the Far East, where air cargo volumes had skyrocketed over 100% year-over-year.

- January 2026: Delovye Linii unveiled a new express route for consolidated (LTL) cargo originating from China, slashing delivery times to Russia from the previous 35-40 days down to a swift 10-17 days. This service eliminates intermediate transshipment, reducing delays and risks, while handling shipments from 1 kg to 15 tons with end-to-end logistics support.

- April 2025: FESCO and Xi’an Free Trade Port commenced a EUR 40 million (USD 47.05 million) Zabaikalsk bonded hub, adding 80,000 m² of warehousing and a private 3-track rail spur.

- February 2025: ATI.SU opened an integration unit providing plug-and-play 1C modules and bespoke API suites to shippers seeking zero-touch tender automation.

Russia Freight Brokerage Services Market Report Scope

| Full-Truckload (FTL) |

| Less-than-Truckload (LTL) |

| Others |

| Dry Van |

| Refrigerated Van |

| Flatbed / Step-Deck |

| Tanker (Bulk Liquid and Chemical) |

| Others |

| Long-Haul (More than 500 miles) |

| Regional (100-500 miles) |

| Local (Less than 100 miles) |

| Traditional Freight Brokerage |

| Asset-Based Freight Brokerage |

| Agent Model Freight Brokerage |

| Digital Freight Brokerage |

| Manufacturing and Automotive |

| Construction and Infrastructure Projects |

| Oil, Gas, Mining and Chemicals |

| Agriculture and Food / Beverage |

| Retail, FMCG and Wholesale Distribution |

| Healthcare and Pharmaceuticals |

| E-commerce and 3PL Fulfilment |

| Others |

| Large Enterprise Shippers (More than USD 100 M) |

| Mid-Market Shippers (USD 10-100 M) |

| Small Businesses (Less than USD 10 M) |

| By Service | Full-Truckload (FTL) |

| Less-than-Truckload (LTL) | |

| Others | |

| By Equipment / Trailer Type | Dry Van |

| Refrigerated Van | |

| Flatbed / Step-Deck | |

| Tanker (Bulk Liquid and Chemical) | |

| Others | |

| By Haul Length | Long-Haul (More than 500 miles) |

| Regional (100-500 miles) | |

| Local (Less than 100 miles) | |

| By Business Model | Traditional Freight Brokerage |

| Asset-Based Freight Brokerage | |

| Agent Model Freight Brokerage | |

| Digital Freight Brokerage | |

| By End-User Industry | Manufacturing and Automotive |

| Construction and Infrastructure Projects | |

| Oil, Gas, Mining and Chemicals | |

| Agriculture and Food / Beverage | |

| Retail, FMCG and Wholesale Distribution | |

| Healthcare and Pharmaceuticals | |

| E-commerce and 3PL Fulfilment | |

| Others | |

| By Customer Size | Large Enterprise Shippers (More than USD 100 M) |

| Mid-Market Shippers (USD 10-100 M) | |

| Small Businesses (Less than USD 10 M) |

Key Questions Answered in the Report

How big will Russia’s freight brokerage services sector be by 2031?

It is forecast to reach USD 2.24 billion, up from USD 1.65 billion in 2026.

Which segment is growing fastest within Russian freight brokerage?

Digital brokerage is expanding at a 24.51% CAGR because automated pricing and embedded payments attract both carriers and shippers.

Why are Less-than-Truckload lanes gaining share?

Marketplace fulfilment requires frequent, smaller shipments that fit LTL networks better than dedicated truckload service.

What is driving refrigerated trailer demand in Russia?

Growth in agricultural exports and pharma cold-chain rules is pushing reefer capacity needs, growing at 8.88% annually.

How are sanctions influencing payment practices?

Exporters and brokers increasingly rely on domestic banks and alternative settlement channels to bypass restricted foreign systems, adding complexity but sustaining flow.

Page last updated on: