South Korea Freight Brokerage Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

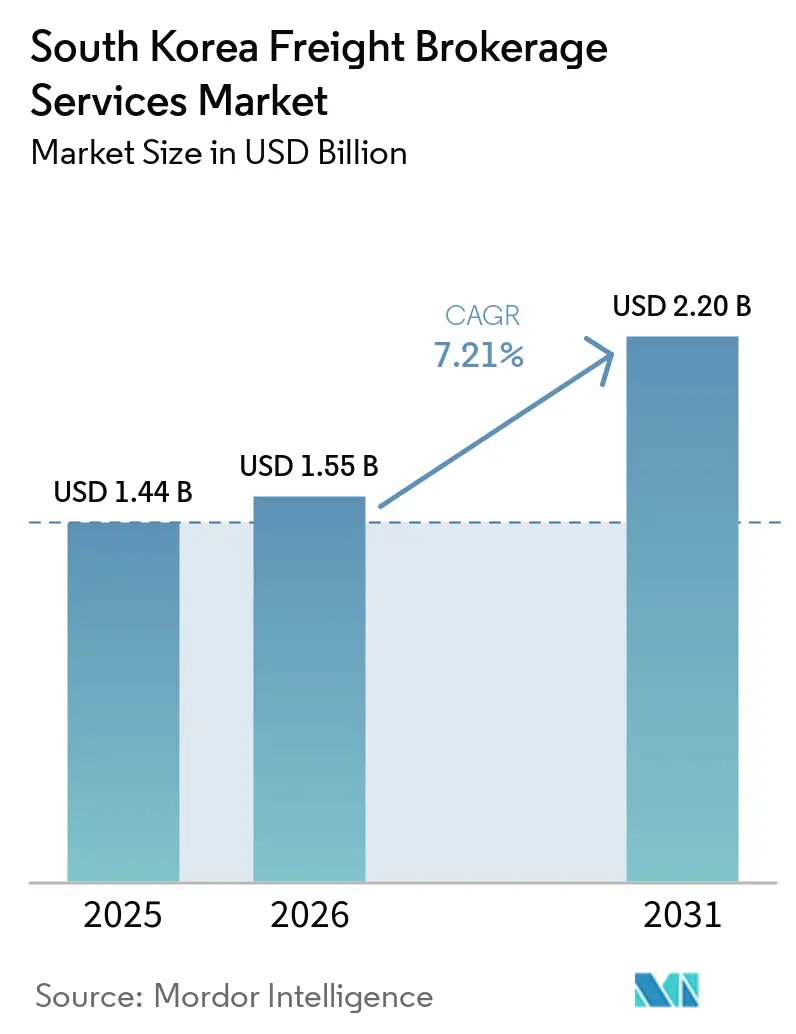

| Base Year Market Size (2025) | USD 1.44 Billion |

| Market Size (2026) | USD 1.55 Billion |

| Market Size (2031) | USD 2.20 Billion |

| Growth Rate (2026 - 2031) | 7.21% CAGR |

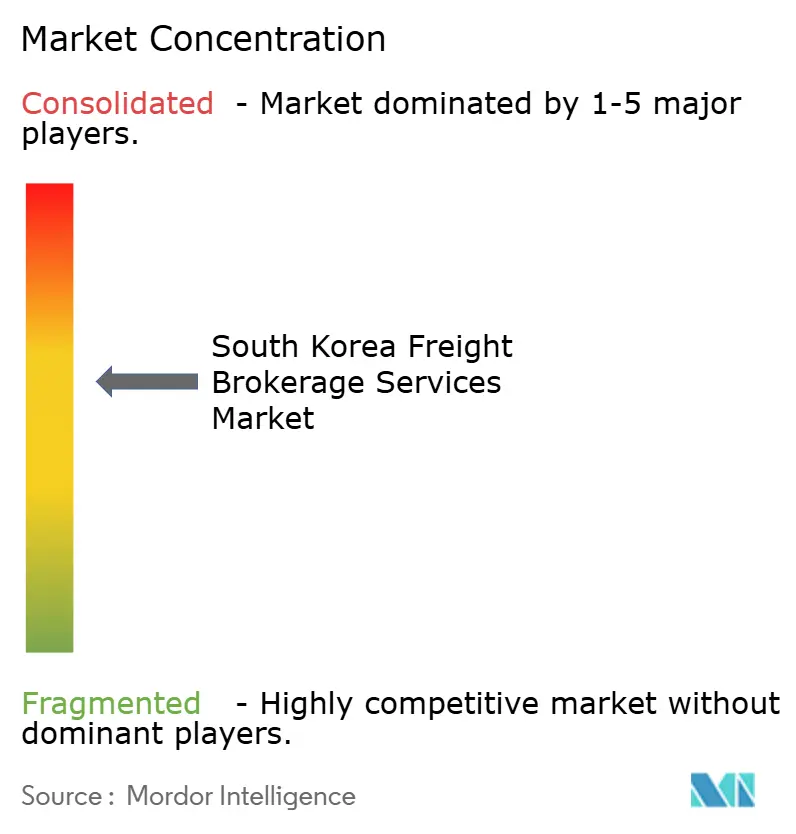

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Freight Brokerage Services Market Analysis by Mordor Intelligence

The South Korea freight brokerage market size is expected to increase from USD 1.44 billion in 2025 to USD 1.55 billion in 2026 and reach USD 2.20 billion by 2031, growing at a CAGR of 7.21% over 2026-2031. Semiconductor export strength, pharmaceutical cold-chain scale-up, and new defense logistics contracts are shifting demand toward time-definite, temperature-controlled, and security-certified shipments that command premium pricing. Brokers able to guarantee capacity during semiconductor peak cycles or provide validated 2-8 °C equipment for biologics win higher margins, while carbon-pricing and fuel-cost pressures threaten rate stability. Digital platforms intensify competition by automating truck–load matching and offering real-time visibility, but regulatory probes into algorithmic pricing are raising compliance costs. Cabotage reforms and Busan’s smart-terminal upgrades expand multimodal routing options, creating opportunities for intermediaries with coastal shipping and drayage expertise.

Key Report Takeaways

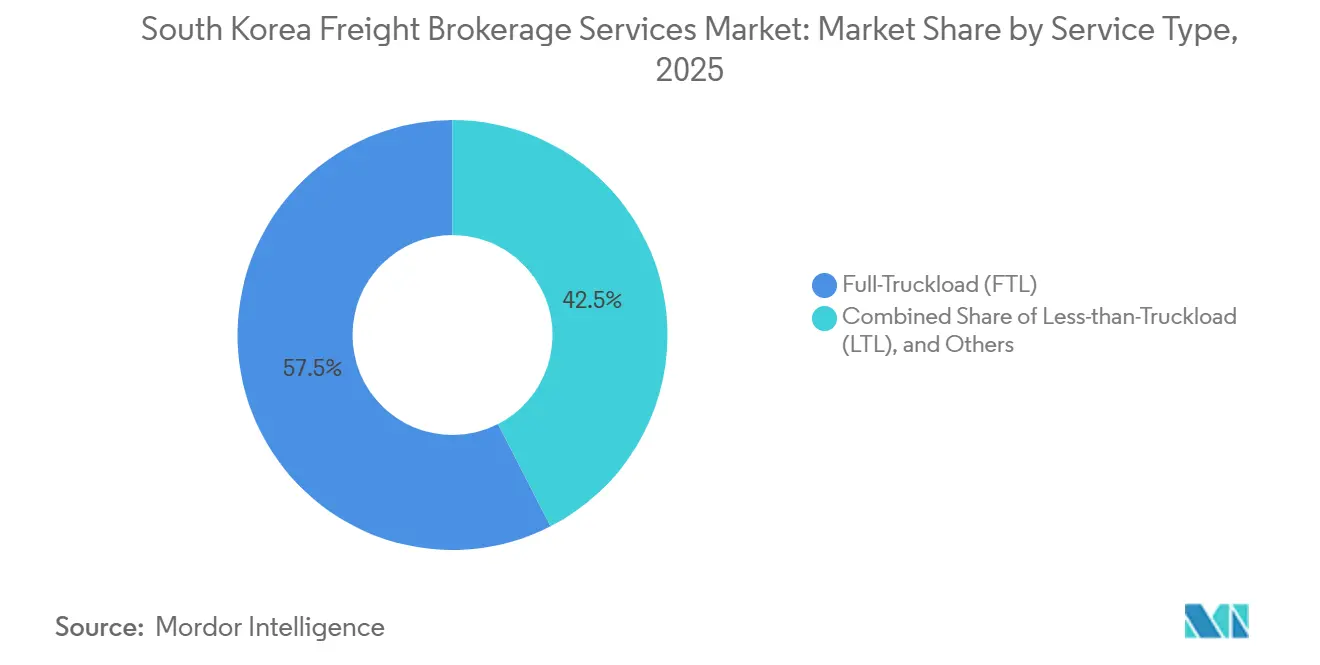

- By service, full-truckload led with 57.54% of South Korea freight brokerage market share in 2025, whereas less-than-truckload is projected to expand at a 9.24% CAGR through 2031.

- By equipment type, dry vans accounted for 51.68% share of the South Korea freight brokerage market size in 2025, while refrigerated vans are forecast to grow at a 10.99% CAGR to 2031.

- By haul length, regional routes captured 47.89% share in 2025; local hauls below 100 miles are advancing at a 12.14% CAGR to 2031.

- By business model, traditional brokerage held 41.98% of the 2025 value, whereas digital platforms record the highest projected CAGR at 17.96% through 2031.

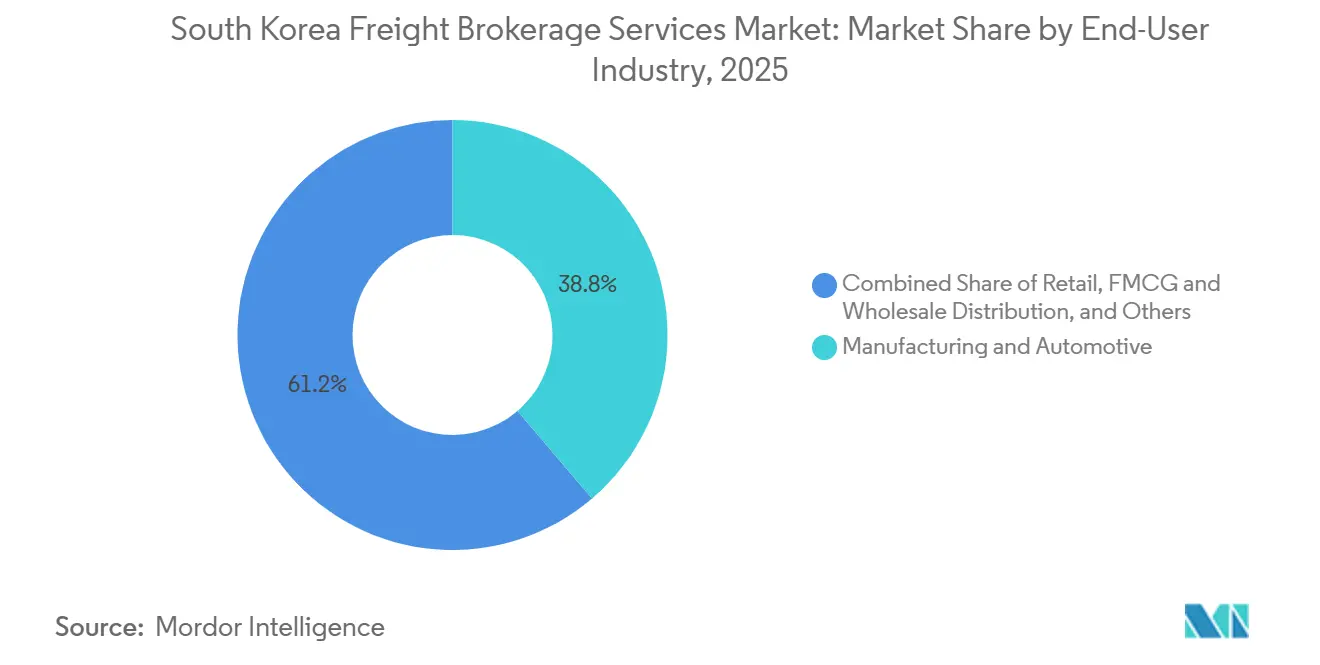

- By end-user industry, manufacturing & automotive comprised 38.76% demand in 2025, but e-commerce & 3PL fulfillment is rising fastest at a 16.37% CAGR to 2031.

- By customer size, large enterprises generated 47.96% revenue in 2025, while small businesses under USD 10 million are expanding at a 13.91% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Dynamics observed within South korea present a country level view when set against the broader international context. The freight brokerage services market analysis by Mordor Intelligence provides that expanded global perspective.

South Korea Freight Brokerage Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Semiconductor export upcycle drives time-definite brokerage loads | +1.6% | Pyeongtaek–Hwaseong–Incheon | Short term (≤ 2 years) |

| Biologics & vaccine cold-chain expansion boosts reefer brokerage demand | +1.3% | Songdo–Incheon biocluster | Medium term (2-4 years) |

| Port of Busan smart-terminal upgrade increases intermodal volumes | +1.0% | Busan–Ulsan–Changwon belt | Medium term (2-4 years) |

| Nationwide blockchain e-B/L rollout slashes administrative lead-time | +0.8% | Major ports & airports | Short term (≤ 2 years) |

| Cabotage law reforms unlock coastal shipping lanes | +0.6% | National coastlines | Long term (≥ 4 years) |

| Defense logistics privatization funnels government freight to brokers | +0.9% | Military bases & ports | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Semiconductor-Export Upcycle Drives Time-Definite Brokerage Loads

Brokers providing real-time visibility and synchronized pickup windows can charge premium rates because any delay risks line shutdowns at global customer fabs. Samsung Electronics’ multibillion-dollar Pyeongtaek expansion amplifies freight volumes requiring security-vetted drivers and expedited customs processing. Dedicated shuttle fleets minimize hand-offs, reduce damage risk, and uphold insurance requirements that semiconductor exporters demand. The concentration of chip plants along the northwestern corridor makes this driver immediately accretive to volumes and margins.

Biologics & Vaccine Cold-Chain Expansion Boosts Reefer Brokerage Demand

Samsung Biologics raised its installed capacity to 784,000 liters after Plant 5 came online in 2025, reinforcing Songdo’s status as the world’s largest contract biomanufacturer. Shipments must stay between 2-8 °C, with continuous IoT monitoring and GDP-compliant documentation. Intermediaries investing in temperature-audit trails, lane-qualification protocols, and certified drivers can protect margins from commoditization. The complexity also raises switching costs, fostering sticky contracts that stabilize revenue even when dry-van rates soften[1]Samsung Biologics, “Plant 5 Completion Announcement,” samsungbiologics.com.

Port of Busan Smart-Terminal Upgrade Increases Intermodal Brokerage Volumes

Automation at Busan New Port enables AI-based berth allocation, unmanned yard cranes, and integrated customs links, cutting vessel dwell time from 31 to 24 hours. Faster turnarounds make inland container drayage more predictable, allowing brokers to pool export-import boxes and reduce empty miles. Manufacturers in Ulsan’s petrochemical cluster can shift from pure trucking to short-sea or rail-plus-truck routings when total transit time shrinks. Brokers who can coordinate chassis supply, depot appointments, and rail slots can capture value by optimizing asset turns for carriers and lowering landed costs for shippers. These intermodal efficiencies support lower carbon footprints, a selling point as K-ETS prices climb.

Nationwide Blockchain e-B/L Rollout Slashes Administrative Lead-Time

Korea Customs Service’s blockchain bill-of-lading platform digitizes endorsement flows, reducing documentation cycles from 3 days to same-day clearance[2]Korea Customs Service, “Blockchain Trade Documentation,” customs.go.kr . Brokers cut clerical headcount and error-correction costs while customers gain visibility into milestones. Data transparency improves carrier score-carding, allowing intermediaries to reward on-time performers and renegotiate poorly performing lanes. System adoption, however, requires API integration and staff retraining, disadvantaging small agencies without IT budgets. Early adopters gain superior analytics that refine truck dispatching and container consolidation decisions, adding a technology moat that resists price competition.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| K-ETS carbon pricing inflates carrier costs passed on to brokers | −1.2% | National | Short term (≤ 2 years) |

| Bunker-fuel price volatility compresses brokerage margins | −0.9% | Coastal trade lanes | Medium term (2-4 years) |

| Shortage of certified reefer-truck drivers constrains capacity | −0.7% | Pharma corridors | Medium term (2-4 years) |

| Fair-Trade probes into algorithmic rate-setting raise burden | −0.5% | Digital platforms | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

K-ETS Carbon Pricing Inflates Carrier Costs Passed On to Brokers

Line-haul carriers running diesel-heavy fleets raise base rates, yet competitive tendering prevents brokers from passing through the full uplift to shippers. Margins narrow most on heavy cargo, where emissions intensity is highest. Intermediaries responding by partnering with LNG-powered or battery-electric fleets differentiate bids, but fleet availability is limited. Carbon-tracking dashboards help shippers benchmark performance and justify green-lane premiums, turning compliance into a service feature rather than an unavoidable cost[3]Carbon Pulse, “South Korea carbon prices surge 50%,” carbon-pulse.com .

Bunker-Fuel Price Volatility Compresses Brokerage Margins

Low-sulfur fuel mandates and geopolitical shocks keep bunker indexes volatile, complicating coastal shipping quotes. When prices spike after a contract is signed, brokers either absorb the delta or invoke fuel-surcharge clauses that customers view unfavorably. Hedging instruments exist but require financial sophistication and minimum volume thresholds that many intermediaries cannot meet. Volatility also discourages shippers from experimenting with newly liberalized cabotage routes, slowing the adoption of potentially cheaper coastal options permitted by the June 2025 amendment. Until pricing mechanisms mature, uncertainty restrains intermodal expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: FTL Dominance Meets Fast-Rising LTL Complexity

Full-truckload accounted for 57.54% of South Korea freight brokerage market share in 2025, anchored by predictable export-bound pallets moving from inland plants to ports or airports. High-value semiconductor shuttles rely on direct routing and sealed trailers for damage control, underpinning repeat lanes that sustain carrier relationships. The South Korea freight brokerage market size for FTL shipments should keep pace with outbound chip capacity, yet incremental growth slows as fabs reach maturity and environmental surcharges push shippers toward rail or sea. Brokers defending FTL positions layer GPS telemetry and delay-predictive analytics to assure shippers of sub-hour arrival variance.

Less-than-truckload volumes climb at a 9.24% CAGR, fueled by e-commerce parcelization and pharmaceutical shipments that ship in pallet lots rather than full trailers. LTL requires hub-and-spoke optimization, cross-docking visibility, and rigorous claim management when temperature excursions occur. Digital platforms bundle fragmented demand from small merchants, enabling them to access national LTL networks that were previously open only to enterprise accounts. This democratization widens the addressable customer pool, but heightens competitive price transparency. The South Korea freight brokerage market still rewards specialists who can design multi-stop milk runs that beat the cost and carbon profile of small FTL moves while meeting next-day delivery expectations.

By Equipment Type: Reefer Upsurge Challenges Dry-Van Incumbency

Dry vans retained 51.68% of the South Korea freight brokerage market size in 2025 on the strength of consumer electronics, auto parts, and apparel loads that need standard 53-foot trailers. Spot rates, however, fluctuate as capacity swings in sync with retail cycles. Brokers hedge by maintaining balanced bid books across verticals.

Refrigerated vans expand at 10.99% CAGR, outpacing every other equipment class as biologics output soars. The South Korea freight brokerage market size for reefer moves will reflect continuous-monitor device rollouts that give shippers lane-temperature audit prints for regulatory filings. Certified carriers remain scarce, pushing load-to-truck ratios above dry-van norms. Brokers pre-qualifying carriers under GDP guidelines can command premium margins. Flatbed, step-deck, and specialized heavy-haul equipment supply defense exports such as K2 tanks, where oversize permits and military escorts raise coordination complexity.

By Haul Length: Local Shuttle Growth Reconfigures Network Design

Regional runs between 100-500 miles held 47.89% share of the South Korea freight brokerage market in 2025, leveraging South Korea’s dense highway grid that lets a single driver complete an out-and-back within daily duty limits. Consolidated regional freight sustains predictable volumes that underpin annual contract tendering.

Local hauls under 100 miles, though a smaller base, grow fastest at 12.14% CAGR as fabs and bio plants push for near-immediate air-cargo transfers. The South Korea freight brokerage market share of local runs improves when intermediaries coordinate multi-trip loops inside congested urban corridors, where asset utilization drops without meticulous planning. Route-optimization software suggesting micro-breaks for driver compliance and electric-truck recharge stops is becoming a critical purchasing criterion for time-critical shippers. Long-haul over 500 miles remains niche, serving project cargo to eastern seaports or cross-border dray to Chinese hubs. Carbon costs and driver shortages cap its growth relative to other haul lengths.

By Business Model: Digital Platforms Scale, Legacy Brokers Adapt

Traditional relationship-based agencies held 41.98% of South Korea freight brokerage market size in 2025 turnover through embedded desks inside manufacturer plants and 24/7 trouble-shooting hotlines that digital rivals struggle to replicate. White-glove incident management keeps them sticky in defense, chemicals, and automotive verticals.

Digital freight intermediaries advance at 17.96% CAGR, automating lane-matching and giving shippers live GPS feeds that reduce check-call labor. The South Korea freight brokerage market now hosts more than 30 app-based platforms linking SME shippers to owner-operators, compressing booking time from hours to minutes. Crackdowns on opaque surcharge algorithms under the December 2025 Shipping Act updates add compliance overhead, but larger platforms budget legal counsel to stay ahead. Asset-based hybrids offering in-house tractors plus brokerage desks hedge against spot volatility, while agent models grant local entrepreneurs’ franchise-like autonomy.

By End-User Industry: E-Commerce Surge Meets Defense Diversification

Manufacturing & automotive still delivers 38.76% of South Korea freight brokerage market share in 2025, anchored by Hyundai-Kia plants feeding export roll-on/roll-off docks. Line-side delivery windows remain unforgiving, incentivizing premium service contracts.

E-commerce & 3PL fulfillment clocks 16.37% CAGR through 2031 as consumers demand next-day delivery nationwide. The South Korea freight brokerage market routes myriad cartons through cross-dock hubs that rely on late-evening pickups and pre-dawn sort runs. Defense logistics privatization injects lumpy but high-margin loads such as the 124 K2 tanks shipped to Poland, requiring heavy-lift cranes, NATO paperwork, and armed escorts. Healthcare, construction, and petrochemical clients round out the portfolio, each attaching unique documentation or haz-mat stipulations that experienced brokers monetize.

By Customer Size: Platforms Democratize Access for SMEs

Large enterprise shippers (more than USD 100 million) accounted for 47.96% of the South Korea freight brokerage market share in 2025. These accounts expect tailored EDI links, quarterly business reviews, and penalty-laden service-level agreements, favoring incumbents with depth.

Small businesses (less than USD 10 million) grow at 13.91% CAGR as app-based booking removes phone-call friction and offers credit terms once inaccessible. The South Korea freight brokerage industry augments SME adoption by pushing self-service portals that quote LTL or parcel moves instantly, while AI chatbots resolve exceptions. Mid-market firms, once poorly served, now toggle between legacy and digital providers, spurring all brokers to unify load-board visibility, carbon calculators, and POD retrieval in a single dashboard.

Geography Analysis

The Pyeongtaek-Hwaseong-Incheon triangle dominates export-oriented freight, funneling high-value chips to Incheon Airport within tight cut-off windows. Semiconductor fabs here rely on guaranteed two-hour driveway-to-dock times, raising demand for vetted drivers and redundant trailers stationed near plant gates. Cabotage reforms may add coastal barge options to relieve highway congestion, but road remains primary until short-sea schedules mature.

Southeastern Busan-Ulsan-Changwon forms the second axis. Busan New Port processes over half of the national container throughput, and its smart-terminal upgrades shorten truck turn-times to under 40 minutes. Brokers able to sync vessel ETAs with inland drays reduce per-box handling cost and carbon output. Ulsan’s petrochemical complexes and Changwon’s machine-tool plants feed heavy and hazardous cargos into this flow, creating specialized brokerage niches that favor safety-certified carriers and escort-permit expertise[4]Port of Busan Authority, “Smart Port Initiative,” busanpa.com .

Songdo-Incheon’s bio cluster emerges as a distinctive cold-chain hub. Fully 784,000 liters of biologics fermenter capacity and rapid vaccine production subjects every pallet to 2-8 °C monitoring protocols. Brokers here orchestrate relay drivers to maintain continuous refrigeration and minimize door-open events. Secondary inland metros such as Daegu and Gwangju develop e-commerce sort centers, spawning last-mile micro-hub volumes that lift local haul growth above national averages. Yet these cities still depend on trunk lines to Incheon and Busan for international hand-offs, reinforcing corridor dominance within the South Korea freight brokerage market.

Coverage of the freight brokerage services market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for North America and Europe, alongside detailed country-level intelligence for Canada, Russia, Spain, Spain, Netherlands, Poland, and Saudi Arabia, each shaped by local operating conditions.

Competitive Landscape

Market structure remains moderately fragmented: the top five intermediaries collectively control a considerable share of the 2025 gross revenue. Incumbents like Hyundai Glovis parlay captive automotive flows into adjacent defense and project-cargo contracts, while CJ Logistics leverages nationwide depots to scale same-day parcel brokerage. Digital challengers such as Trucker Alliance and LinkFlow Logistics are posting triple-digit load growth by onboarding 30,000 owner-operators through smartphone apps, though regulatory scrutiny of pricing algorithms could temper expansion.

Strategic moves center on technology and specialization. Samsung SDS added blockchain B/L modules that automate customs filing, cutting border dwell for electronics exporters. Pantos Logistics opened a GDP-certified cold-store near Incheon, integrating IoT probes that push real-time data to brokers’ TMS dashboards. In defense, Korea Aerospace Industries’ USD 600 million performance-based logistics contract signals a multi-year lift for brokers with security-cleared teams.

Carbon compliance shapes fleet partnerships. Lotte Global aims to deploy 200 LNG tractors by 2028, offering brokers lower-emission lanes that attract ESG-sensitive shippers. Smaller agents pursue niche differentiation; some specialize in coastal steel coil moves unlocked by cabotage relaxation, while others focus on driver recruitment to alleviate reefer-certified labor shortages. Overall, rivalry hinges on technology adoption speed, vertical-specific know-how, and capacity assurance in tight equipment segments.

South Korea Freight Brokerage Services Industry Leaders

CJ Logistics

Hyundai Glovis

LX Pantos

Hanjin Transportation

Cello Square (Subsidiary of Samsung SDS)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: CJ Logistics partnered with Thailand’s CP AXTRA to co-develop advanced logistics IT systems. The agreement supports digital freight solutions and accelerates their expansion across Southeast Asia logistics markets.

- December 2025: CJ Logistics introduced its “CBE One-Stop Package,” integrating cross-border e-commerce logistics with payments and marketing. The solution targets SMEs and strengthens its digital freight forwarding and brokerage capabilities.

- November 2025: Kuehne + Nagel enhanced its logistics solutions for semiconductors and pharmaceuticals in Korea. The firm also invested in digital freight platforms to improve shipment visibility and brokerage efficiency.

- May 2025: Samsung SDS expanded its Cello Square digital logistics platform with AI-based freight visibility and pricing features. The upgrade improves shipment tracking and operational efficiency for global shippers.

South Korea Freight Brokerage Services Market Report Scope

| Full-Truckload (FTL) |

| Less-than-Truckload (LTL) |

| Others |

| Dry Van |

| Refrigerated Van |

| Flatbed / Step-Deck |

| Tanker (Bulk Liquid and Chemical) |

| Others |

| Long-Haul (More than 500 miles) |

| Regional (100-500 miles) |

| Local (Less than 100 miles) |

| Traditional Freight Brokerage |

| Asset-Based Freight Brokerage |

| Agent Model Freight Brokerage |

| Digital Freight Brokerage |

| Manufacturing and Automotive |

| Construction and Infrastructure Projects |

| Oil, Gas, Mining and Chemicals |

| Agriculture and Food / Beverage |

| Retail, FMCG and Wholesale Distribution |

| Healthcare and Pharmaceuticals |

| E-commerce and 3PL Fulfilment |

| Other End-User Industry |

| Large Enterprise Shippers (More than USD 100 M) |

| Mid-Market Shippers (USD 10-100 M) |

| Small Businesses (Less than USD 10 M) |

| By Service | Full-Truckload (FTL) |

| Less-than-Truckload (LTL) | |

| Others | |

| By Equipment / Trailer Type | Dry Van |

| Refrigerated Van | |

| Flatbed / Step-Deck | |

| Tanker (Bulk Liquid and Chemical) | |

| Others | |

| By Haul Length | Long-Haul (More than 500 miles) |

| Regional (100-500 miles) | |

| Local (Less than 100 miles) | |

| By Business Model | Traditional Freight Brokerage |

| Asset-Based Freight Brokerage | |

| Agent Model Freight Brokerage | |

| Digital Freight Brokerage | |

| By End-User Industry | Manufacturing and Automotive |

| Construction and Infrastructure Projects | |

| Oil, Gas, Mining and Chemicals | |

| Agriculture and Food / Beverage | |

| Retail, FMCG and Wholesale Distribution | |

| Healthcare and Pharmaceuticals | |

| E-commerce and 3PL Fulfilment | |

| Other End-User Industry | |

| By Customer Size | Large Enterprise Shippers (More than USD 100 M) |

| Mid-Market Shippers (USD 10-100 M) | |

| Small Businesses (Less than USD 10 M) |

Key Questions Answered in the Report

How fast is the South Korea freight brokerage market expected to grow by 2031?

Value is projected to rise from USD 1.55 billion in 2026 to USD 2.20 billion by 2031, reflecting a 7.21% CAGR.

Which service segment is expanding the quickest?

Less-than-truckload services are forecast to grow at 9.24% CAGR through 2031 due to e-commerce parcelization.

Why are refrigerated vans in higher demand?

Biologics production at Songdo and rising vaccine exports push reefer freight volumes, driving a 10.99% CAGR for the equipment class.

What impact does K-ETS have on freight brokers?

A 50% rise in carbon-allowance prices tightens carrier margins, forcing brokers to renegotiate rates and seek low-emission partners.

How are digital platforms changing brokerage?

Algorithmic matching and real-time visibility cut booking times and attract SMEs, underpinning a 17.96% CAGR for platform-based models.

Which geography offers the largest opportunity for cold-chain specialists?

The Songdo–Incheon biocluster hosts 784,000 liters of biologics capacity, requiring validated 2-8 °C logistics networks.

Page last updated on: