Saudi Arabia Food And Beverage Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

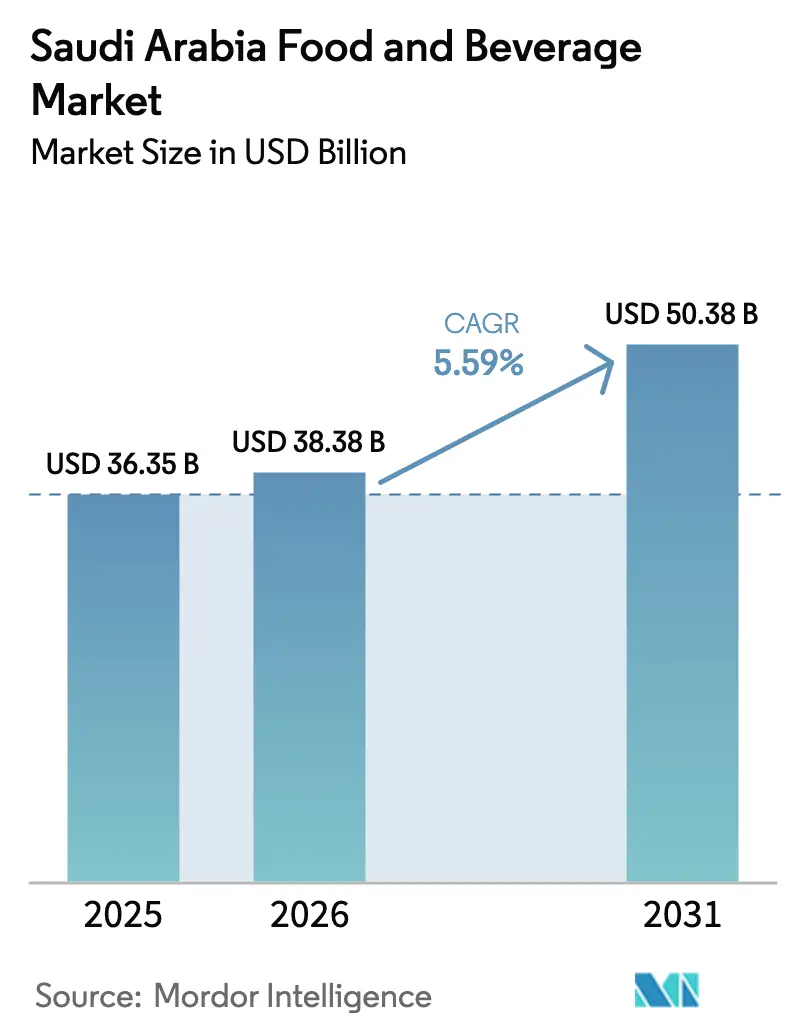

| Base Year Market Size (2025) | USD 36.35 Billion |

| Market Size (2026) | USD 38.38 Billion |

| Market Size (2031) | USD 50.38 Billion |

| Growth Rate (2026 - 2031) | 5.59% CAGR |

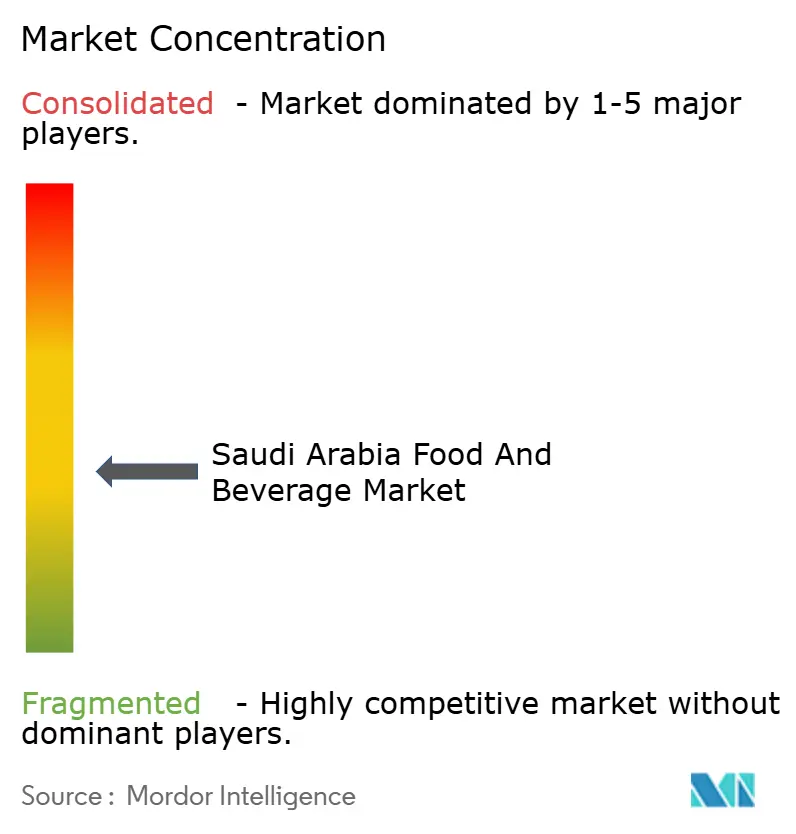

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Saudi Arabia Food And Beverage Market Analysis by Mordor Intelligence

The Saudi Arabia food and beverages market size was valued at USD 36.35 billion in 2025 and estimated to grow from USD 38.38 billion in 2026 to reach USD 50.38 billion by 2031, at a CAGR of 5.59% during the forecast period (2026-2031). Vision 2030 policies are steering oil revenues into bolstering domestic agri-food capabilities. These policies aim to reduce reliance on imports and enhance food security by strengthening local production. A significant government investment of USD 70 billion is being funneled into processing plants to support this initiative. With the population expected to hit 40 million by 2030, these moves are timely and critical for meeting the growing domestic demand[1]Source: USDA FAS," Saudi Arabia: Food Processing Ingredients", fas.usda.gov. Projects aimed at achieving livestock self-sufficiency, coupled with clean-label reformulations that cater to evolving consumer preferences for transparency and healthier options, are driving volume increases. Additionally, a surge in pilgrimage traffic, particularly during peak seasons, is boosting seasonal spending on packaged foods, further contributing to market growth. To protect their margins from utility-price reforms, retailers are tightening their supply chains through vertical integration, which enhances operational efficiency, and developing private labels to offer cost-effective alternatives. While tax surcharges on sugary beverages pose challenges for certain product categories, they simultaneously carve out opportunities for healthier snacks, dairy products, and date-based drinks, aligning with the growing consumer shift toward health-conscious choices.

Key Report Takeaways

- By product type, meat, poultry, seafood, and meat Substitutes led with 27.62% of the Saudi Arabian food and beverages market share in 2025 and are expected to grow at a 3.02% CAGR to 2031.

- By product type, savory snacks are projected to record the fastest 8.31% CAGR during 2026-2031 after holding 3.88% revenue share in 2025, reflecting urban demand for convenience formats.

- By distribution channel, supermarkets/hypermarkets commanded 57.10% share of the Saudi Arabia food and beverages market size in 2025; Online Retail Stores are anticipated to expand at an 7.82% CAGR through 2031, buoyed by nationwide 5G roll-out and last-mile cold-chain hubs.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple countries and regions, with Saudi arabia representing one among them. The global report on food and beverage market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

Saudi Arabia Food And Beverage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for clean-label food and beverages | +0.8% | National, with concentration in urban centers | Medium term (2-4 years) |

| Growth in dairy consumption per capita | +0.6% | National, strongest in Central and Eastern provinces | Long term (≥ 4 years) |

| Hajj and Umrah pilgrimage foodservice spill-over boosting retail packs | +0.4% | Makkah and Madinah regions, spillover to national retail | Short term (≤ 2 years) |

| Rise of government-backed "Made-in-Saudi" localization program | +0.7% | National, with manufacturing hubs in Riyadh and Eastern Province | Long term (≥ 4 years) |

| Expansion of modern grocery retail formats | +0.5% | National, accelerated in secondary cities | Medium term (2-4 years) |

| Surge in cold-chain logistics infrastructure outside Tier-1 cities | +0.3% | Secondary cities and rural distribution networks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand for clean-label food and beverages

Saudi shoppers are increasingly turning away from artificial additives, prompting the SFDA's trans-fat ban to drive reformulations in carbonated drinks, baked goods, and ready-to-eat meals. Local innovators, like Thurath Al-Madina, have introduced Milaf Cola, a soda sweetened with dates and made from indigenous crops, highlighting the advantage of local sourcing[2]Source: Saudi Food and Drug Authority," Eliminating Trans Fats In Saudi Arabia", sfda.gov.sa. This shift reflects a broader consumer preference for products that align with cultural heritage and health-conscious values. With excise taxes set at 50% for soft drinks and a staggering 100% for energy drinks, brands are pivoting towards natural ingredients, motivated by both health considerations and financial incentives. These taxes not only discourage the consumption of sugary and artificially flavored beverages but also create opportunities for healthier alternatives to gain market share. Retailers are capitalizing on this trend, establishing dedicated "healthy shelf" zones that have notably increased sales for low-sugar yogurts and air-fried snacks. These zones cater to the growing demand for functional and better-for-you products, further reinforcing the shift in consumer behavior. Looking ahead, medium-term transparency regulations, in line with Codex labels, are set to solidify this trend, directing premium pricing towards producers who adhere to these standards. These regulations are expected to enhance consumer trust and encourage manufacturers to prioritize compliance, ultimately fostering a more health-oriented market landscape.

Growth in dairy consumption per capita

Saudi Arabia's dairy sector has surpassed 121% self-sufficiency, contributing 46% to the nation's agricultural GDP. Almarai, the sector's flagship player, operates fully integrated farms, ensuring price stability even amidst global feed fluctuations. These farms integrate advanced technologies and sustainable practices, enabling efficient production and cost management. Meanwhile, NADEC reported a net income of SAR 213.2 million in H1 2024, buoyed by a 7.3% rise in revenue, driven by strategic investments in product innovation and market expansion. Domestic loyalty runs deep, with 69% of households favoring local milk due to its perceived freshness and quality. Additionally, government-backed loans are fueling capacity expansions, including the introduction of automated barns in Al-Kharj, which enhance operational efficiency and production scalability. The segment's sustained growth is bolstered by a youthful demographic, increasingly leaning towards fortified, single-serve products that cater to their on-the-go lifestyles, reflecting a shift in consumer preferences toward convenience and health-conscious choices.

Hajj and Umrah pilgrimage foodservice spill-over

By 2030, the government aims to welcome 30 million Umrah visitors, significantly boosting demand for shelf-stable halal packs, portioned dairy desserts, and bottled water. This ambitious target is expected to create a ripple effect across the supply chain, driving growth in production, packaging, and distribution sectors. Each Ramadan, retailers in Jeddah and Taif set up pop-up satellite warehouses to meet the surge in demand, ensuring the timely availability of essential products for pilgrims. These warehouses play a critical role in managing the seasonal spike, enabling retailers to stockpile and distribute goods efficiently. After the rush, they channel any leftover stock through discount channels, maintaining efficient nationwide distribution and minimizing wastage. This annual rhythm benefits nimble manufacturers who adeptly manage inventory, implement flexible production schedules, and prioritize safety protocols, ensuring readiness for any pandemic-related challenges or unforeseen disruptions. Additionally, manufacturers with robust supply chain strategies and adaptive logistics are better positioned to capitalize on this growing market opportunity.

Rise of “made-in-Saudi” localization program

More than 4,800 SKUs now proudly display the certification label, which not only enhances their visibility on shelves but also gives them an edge in public tenders by meeting specific compliance and quality standards. Food processors are reaping the rewards of subsidized industrial land, which reduces operational costs, and a 30% cash-back incentive on capital equipment, effectively bridging the cost gap with imports and encouraging local production. With aquaculture targets set at 300,000 tonnes and significant biotech milestones achieved, there's a clear pivot towards soy analogs and precision-fermented proteins, which are gaining traction as sustainable and innovative food solutions[3]Source: Kingdom of Saudi Arabia, "National Industrial Development and Logistics Program", vision2030.gov.sa. Meanwhile, harmonized SASO regulations guarantee export-grade standards throughout the GCC, ensuring consistency and quality for regional trade. Consumer surveys reveal a growing domestic preference, with 33% of respondents favoring local snacks and bottled water, highlighting the policy's success in fostering demand for domestically produced goods and strengthening consumer trust in local brands.

Restraint Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High salt/sugar preservatives in ready-meals | -0.3% | National, with regulatory pressure in urban markets | Medium term (2-4 years) |

| Price sensitivity amid subsidy rationalization | -0.5% | National, most acute in lower-income segments | Short term (≤ 2 years) |

| Strict shelf-life compliance for summer road freight | -0.2% | National, particularly affecting inter-city distribution | Long term (≥ 4 years) |

| Packaging-waste regulations driving cost inflation | -0.4% | National, with compliance costs affecting all manufacturers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price sensitivity amid subsidy rationalization

As fuel and power tariffs rise, households face increased expenses, leading to a squeeze on disposable incomes and a subsequent reduction in spending on premium food and beverages. This shift in spending patterns has prompted manufacturers to adopt a dual strategy to cater to diverse consumer segments. They are introducing value packs tailored for budget-conscious families, ensuring affordability, while simultaneously rolling out premium SKUs designed to appeal to wealthier consumers seeking high-quality options. To regain sales momentum and drive consumer engagement, promotions are strategically timed around key occasions such as Eid and National Day, which are periods of heightened consumer activity. These promotional efforts often include discounts, bundled offers, and targeted marketing campaigns to attract a wide range of consumers. However, staples like vegetable oil and poultry exhibit significant price sensitivity, making it essential for manufacturers to implement meticulous margin management strategies. This involves closely monitoring input costs, optimizing supply chain efficiencies, and adjusting pricing strategies to maintain profitability while addressing consumer demand effectively.

Packaging-waste regulations driving cost inflation

Under the General Environmental Regulations, the phased plastic ban mandates a shift towards biodegradable films, corrugated shippers, and aluminum caps. This compliance not only incurs machinery retrofit costs but also necessitates new SFDA testing cycles, thereby squeezing margins in the carbonated beverage and confectionery sectors. Companies are required to invest in upgrading their production processes to meet these regulations, which often involves significant capital expenditure. In response, companies are turning to lightweight PET and digital-ink date coding to reduce material intensity. These solutions help minimize environmental impact but come with challenges, as the capital payback period for mid-sized processors extends beyond three years, making it a long-term investment. On the upside, eco-labels offer premium shelf placement, enhancing product visibility and appeal to environmentally conscious consumers. Additionally, they align with the ESG mandates of institutional investors, which are increasingly influencing corporate strategies and market positioning.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Protein Dominance Meets Snacking Revolution

As of 2025, the meat, poultry, seafood, and meat Substitutes segment commands a dominant 27.62% share of Saudi Arabia's food and beverages market. This stronghold is bolstered by substantial infrastructure investments, notably the USD 2 billion livestock city project. This ambitious initiative aims to elevate broiler output by an impressive 250 million birds annually, thereby fortifying the domestic protein supply. Local operators, such as Tanmiah, are capitalizing on this momentum, expanding their capacity with approximately 100 state-of-the-art automated poultry houses. The protein category, driven by a deep-rooted consumer preference for red meat and fish, is poised for steady growth, projecting a 3.02% CAGR through 2031. While the market remains anchored in traditional protein choices, there's a gradual embrace of plant-based alternatives. Items like soy kebabs and jackfruit shawarma, primarily featured on quick-service restaurant menus, cater to the expatriate vegan demographic. The segment's robust domestic production capabilities ensure consistent availability and competitive pricing. Furthermore, strategic expansions and modernization efforts bolster Saudi Arabia's leadership in the regional protein landscape.

On the other hand, the snack segment is emerging as the fastest-growing category in Saudi Arabia's food and beverages market, boasting an impressive 8.31% CAGR. This surge is largely driven by impulse buying and a heightened health consciousness, especially in light of regulatory sodium restrictions. Popular snack choices, including chips, baked nuts, and date bars, owe their rising fame to effective brand positioning and a strong "Made-in-Saudi" identity that resonates with local consumers. By emphasizing authenticity and regional roots, domestic snack producers have elevated brand preference to 33%, carving a niche in a competitive landscape. Their alignment with esports sponsorships and the youth culture further amplifies their reach, especially among Gen Z, leading to both trial and repeat purchases. Moreover, initiatives like reformulating products with sea salt and adopting air-frying technologies underscore the industry's dedication to clean-label standards and regulatory adherence, catering to urban consumers seeking healthier snack options. This robust growth trajectory underscores a significant shift in consumer habits and lifestyle choices, positioning snacks as a dynamic and rapidly expanding segment in Saudi Arabia's food market.

By Distribution Channel: Digital Transformation Accelerates Modern Retail

In 2025, supermarkets and hypermarkets claimed a dominant 57.10% share of Saudi Arabia's food and beverages market, establishing themselves as the primary touchpoint for consumers. These large-format retailers are not just enhancing shopper convenience but are also boosting basket sizes. By integrating features like click-and-collect lockers and in-aisle QR codes, they streamline the shopping experience and promote cross-selling. The organized retail space is on a steady growth trajectory, with a projected CAGR of 3.98%, bolstered by the addition of around 1 million square meters of new mall gross leasable area (GLA). Their vast product assortments and robust physical presence continue to draw a diverse consumer base, seamlessly blending traditional retail strengths with digital innovations. In a strategic pivot, convenience stores are now clustering franchises near industrial zones, operating 24/7 to cater to night-shift workers. Specialty health outlets, emphasizing gluten-free and organic products, are carving a niche in upscale areas like Riyadh’s Diplomatic Quarter and Jeddah’s Corniche. Meanwhile, traditional local shops, or bakalas, thrive on immediacy but grapple with challenges from new payment terminal mandates. These requirements limit their cash transaction flexibility, pushing them to forge partnerships with distributors for competitive pricing.

Online retail stores are emerging as the fastest-growing segment in Saudi Arabia's food and beverages market, boasting a robust 7.82% CAGR. This growth is largely attributed to the expansion of 5G coverage and the rise of advanced fintech payment solutions. Notably, this channel has adeptly transformed Ramadan's bulk buyers into loyal subscribers throughout the year, especially for staples like dairy and rice. While the e-grocery market share currently lingers in the single digits, it's witnessing a doubling approximately every two years. This surge is powered by enhancements in cold-chain infrastructure, ensuring superior product quality and reliable delivery. The allure of digital platforms, coupled with swifter internet speeds and smooth payment methods, is gradually reshaping consumer preferences towards online shopping. Furthermore, the integration of omnichannel strategies allows retailers to merge the benefits of virtual and physical shopping, aligning with the evolving demands for flexibility and efficiency. As digital adoption accelerates, online retail is set to play a pivotal role in the future of Saudi Arabia’s food and beverages distribution landscape.

Geography Analysis

Riyadh, home to 8 million residents, and its integrated logistics parks, anchor one-third of Saudi Arabia's food and beverages market in the Central Province. With robust purchasing power and a modern retail density above the national average, it's no surprise that 45% of new openings from retail giants Lulu and Danube are concentrated here. Meanwhile, the Eastern Province, capitalizing on King Abdulaziz Port and SABIC’s agri-nutrient complexes, plays a pivotal role in supplying animal feed and packaging resin to national processors. The Western Province, benefiting from pilgrimage flows, sees Jeddah’s annual port throughput of 67 million tons significantly expedite import substitution initiatives by reducing inbound freight times.

As part of the Vision 2030 regional programs promoting agricultural diversification, Al-Jouf and Tabuk have made headlines by shipping their first tomato consignment to Europe in 2024, underscoring their export potential. NEOM is making strides in the alternative protein sector, investing in precision fermentation plants with a target of producing 20,000 MT by 2030, setting a benchmark for tech-driven production. Additionally, secondary cities like Hail, Abha, and Najran are capitalizing on new cold-chain corridors, which significantly reduce spoilage and seamlessly integrate local farms into the national retail landscape.

Due to customs union agreements, neighboring GCC countries are eliminating import tariffs on Saudi dairy and poultry products, resulting in a surge in cross-border trade. Rail initiatives, such as the Landbridge, have slashed the transit time from Jeddah to Dammam to a mere 18 hours, bolstering the movement of perishables across the east-west corridor. On another front, the National Water Strategy is making a significant move by designating 2.5 billion m³ of treated wastewater for agrifood use by 2030. This initiative not only alleviates stress on aquifers but also ensures sustained yields in date orchards and forage crops.

Competitive Landscape

Saudi Arabia's food and beverage market is moderately fragmented. To counter competition from both international newcomers and rising local contenders, established domestic players are increasingly turning to vertical integration strategies. Almarai, a key player, oversees everything from fodder farms to processing, boasting a fleet of 1,400 trucks that ensure a swift 24-hour milk-to-shelf cycle. Meanwhile, Savola Group's recent February 2024 decision to spin off its 34.52% stake in Almarai reshuffles equity distribution without disrupting existing operational synergies. NADEC, tapping into Agricultural Development Fund loans, is automating its cheese production, resulting in a notable 310-basis-point increase in profit margins. The race for poultry dominance heats up, with Almarai, Tanmiah, and JBS all vying for a stake in Al Watania, highlighting the strategic importance of protein supply.

Investment in technology is on the rise. In a significant move, Liberation Labs has teamed up with NEOM to establish a precision-fermentation facility, aiming to produce animal-free whey by 2027. This joint venture positions Saudi Arabia as a frontrunner in the regional novel protein market. On another front, Saudi Dairy & Foodstuff Co. is pioneering blockchain technology for yogurt traceability, not only meeting the SFDA’s mandates but also bolstering its export reputation.

Retailers are increasingly turning to private labels to boost margins. Danube's private label, with 380 SKUs, commands a notable 12% of shelf space, while Othaim's budget line offers a 15% discount compared to multinational brands. The e-grocery sector is buzzing with activity; BinDawood's investment in IATC ensures a promise of same-day delivery across 27 cities. Foreign players are making their mark with specialty products, like Nestlé's USD 1.9 billion coffee mix factory extension in 2024, but face a hurdle: a 40% local-content requirement to access public contracts.

Saudi Arabia Food And Beverage Industry Leaders

-

Almarai Co. Ltd.

-

National Agricultural Development Company (NADEC)

-

PepsiCo Inc.

-

Nestle SA

-

Al Rabie Saudi Foods Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Yole, a brand operating in Saudi Arabia, opened a new store, marking its expanded presence in the market. This expansion aligns with the brand's strategy to strengthen its footprint in the region and cater to the growing consumer demand for its products.

- March 2025: Feastables, a brand owned by popular YouTuber MrBeast, launched its snack bar products across Saudi Arabia. These products are available in both online and offline retail stores throughout the country. The launch reflects the brand's efforts to tap into the Saudi Arabian market, leveraging the increasing popularity of healthier snack options among consumers.

- December 2024: Almarai invested approximately USD 4.8 billion in seafood and red meat production in Saudi Arabia. This move aims to lessen the country's reliance on meat imports and aligns with Saudi Arabia's Vision 2030 initiative to boost local food production and achieve greater self-sufficiency in the agricultural sector.

- December 2024: Thurath Al-Madina, a brand under the Saudi Arabian Public Investment Fund, introduced its new Milaf Cola, crafted from dates. The company touts it as a healthier, sugar-free alternative to traditional fizzy drinks. This product launch is part of the brand's commitment to promoting innovative, locally sourced beverages that align with the growing consumer preference for health-conscious options.

Saudi Arabia Food And Beverage Market Report Scope

Food is any nutrient-rich material consumed to sustain life and growth, whereas beverage is any potable liquid, especially one other than water, such as tea, coffee, or any dairy products like milk.

The market scope encompasses product types and distribution channels. Regarding product types, the market is divided into dairy & dairy alternatives products, confectionery, beverages, bakery, snacks, meat, poultry, seafood & meat substitutes, breakfast cereals, and ready meals. The dairy and dairy alternative segment is further categorized into dairy products and dairy alternatives. Confectionery includes chocolate confectionery, sugar confectionery, and snack bars (cereal bars, protein/energy bars, and fruit & nut bars), while beverage consists of alcoholic beverages and non-alcoholic beverages. The bakery segment comprises cakes and pastries, biscuits, bread, morning goods, and other product types (frozen baked products).

The market sizing has been done in value terms in USD for all the abovementioned segments.

| Dairy and Dairy Alternatives | Dairy Products | Butter |

| Cheese | ||

| Cream | ||

| Dairy Desserts | ||

| Milk | ||

| Sour-Milk Drinks | ||

| Yogurt | ||

| Dairy Alternatives | ||

| Confectionery | Chocolate Confectionery | |

| Sugar Confectionery | ||

| Snack Bars | Cereal Bars | |

| Protein/Energy Bars | ||

| Fruit and Nut Bars | ||

| Non-Alcoholic Beverages | ||

| Bakery | Cakes and Pastries | |

| Biscuits | ||

| Bread | ||

| Morning Goods | ||

| Other Bakery Products | ||

| Savory Snacks | ||

| Meat, Poultry, Seafood and Meat Substitutes | Meat | |

| Poultry | ||

| Seafood | ||

| Meat Substitutes | ||

| Breakfast Cereals | ||

| Ready Meals | ||

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Specialty Stores |

| Online Retail Stores |

| Other Distribution Channels |

| By Product Type | Dairy and Dairy Alternatives | Dairy Products | Butter |

| Cheese | |||

| Cream | |||

| Dairy Desserts | |||

| Milk | |||

| Sour-Milk Drinks | |||

| Yogurt | |||

| Dairy Alternatives | |||

| Confectionery | Chocolate Confectionery | ||

| Sugar Confectionery | |||

| Snack Bars | Cereal Bars | ||

| Protein/Energy Bars | |||

| Fruit and Nut Bars | |||

| Non-Alcoholic Beverages | |||

| Bakery | Cakes and Pastries | ||

| Biscuits | |||

| Bread | |||

| Morning Goods | |||

| Other Bakery Products | |||

| Savory Snacks | |||

| Meat, Poultry, Seafood and Meat Substitutes | Meat | ||

| Poultry | |||

| Seafood | |||

| Meat Substitutes | |||

| Breakfast Cereals | |||

| Ready Meals | |||

| By Distribution Channel | Supermarkets/Hypermarkets | ||

| Convenience Stores | |||

| Specialty Stores | |||

| Online Retail Stores | |||

| Other Distribution Channels | |||

Key Questions Answered in the Report

How big is the Saudi Arabia food and beverages market in 2026?

The Saudi Arabia food and beverages market size is USD 38.38 billion in 2026.

What is the forecast CAGR for food and beverage sales in Saudi Arabia?

Aggregate revenue is projected to grow at a 5.59% CAGR between 2026 and 2031.

Which product category leads current sales?

Meat, Poultry, Seafood and Meat Substitutes hold 27.62 % share, the largest among all categories.

Which distribution channel is expanding fastest?

Online Retail Stores are expected to post a 7.82 % CAGR through 2031.

Page last updated on: