Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 5.13 Billion |

| Market Size (2026) | USD 5.43 Billion |

| Market Size (2031) | USD 7.22 Billion |

| Growth Rate (2026 - 2031) | 5.85% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Saudi Arabian Poultry Market Analysis by Mordor Intelligence

The Saudi Arabian Poultry Market size was valued at USD 5.13 billion in 2025 and estimated to grow from USD 5.43 billion in 2026 to reach USD 7.22 billion by 2031, at a CAGR of 5.85% during the forecast period (2026-2031). The Saudi Arabian poultry market is experiencing substantial growth driven by high poultry meat consumption among the country's predominantly Islamic population. In December 2024, Saudi Arabia's General Authority for Statistics (GASTAT) reported an annual poultry meat consumption of 43.40 kg per capita in the country. The market's expansion is further supported by increasing tourism, growth in the food service industry, evolving consumer preferences, and improved retail distribution networks. Furthermore, fast food chains like Al Baik, KFC, and Herfy are major contributors to this trend, as they rely heavily on processed poultry. Additionally, the growing influence of Western and international cuisines has led to an increased preference for processed chicken products like nuggets, and sausages are commonly found in supermarkets such as Danube and Carrefour. The rising demand for animal protein and consumer preference for low-fat, high-protein diets have significantly increased poultry meat consumption in Saudi Arabia. Market expansion is evidenced by recent developments, such as the February 2024 announcement by Meats & Cuts, a UAE-based artisan butcher shop and deli, to open 14 new branches across the GCC region. These developments have created new opportunities for both domestic and international players to enhance their market presence through innovative retail concepts and improved customer experiences.

Key Report Takeaways

- By form, Fresh/Chilled products accounted for 55.08% of the Saudi Arabian poultry market size in 2025, while Canned products are advancing at a 7.21% CAGR.

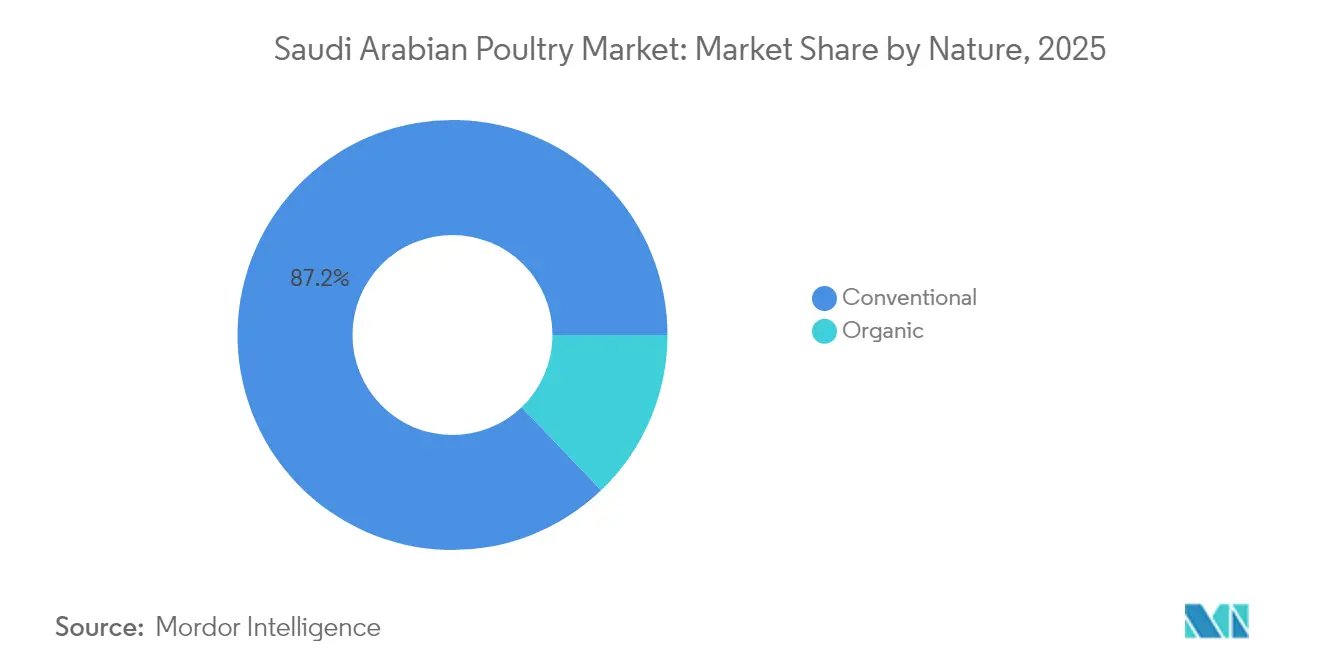

- By nature, the Conventional segment captured 87.15% share in 2025, whereas Organic offerings are on track for a 7.08% CAGR through 2031.

- By distribution channel, Off-Trade retained a 63.72% share in 2025; however, On-Trade is projected to register a 6.27% CAGR to 2031.

- By region, the Western Region held a 50.10% Saudi Arabian poultry market share in 2025 and is forecast to grow at an 7.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabian Poultry Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift Toward Processed and Value-Added Products | +1.2% | Western Region core, expanding to Central Region | Medium term (2-4 years) |

| Expansion of Foodservice and QSR Chains | +1.0% | Western and Central Regions, spillover to Northern Region | Short term (≤ 2 years) |

| Government Support for Local Production | +0.8% | National, with concentrated benefits in Central and Western Regions | Long term (≥ 4 years) |

| Cultural Preference | +0.6% | National, strongest in traditional regions | Long term (≥ 4 years) |

| Consumer Health Awareness | +0.5% | Urban centers in Western and Central Regions | Medium term (2-4 years) |

| Innovation in Product Formats and Packaging | +0.4% | Western Region initially, national rollout planned | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shift Toward Processed and Value-Added Products

The Kingdom's processed poultry segment is experiencing unprecedented transformation as manufacturers pivot from commodity production to value-engineered offerings. JBS's November 2024 launch of its USD 50 million Jeddah nugget facility exemplifies this shift, targeting the growing convenience food market while creating 500 specialized jobs. This strategic repositioning addresses the 25% annual growth in online grocery sales, where processed products command premium pricing and extended shelf life advantages. The Tyson-Tanmiah partnership's focus on doubling processed product capacity through advanced marination and tenderization technologies signals industry-wide recognition that value-addition drives margin expansion in an increasingly competitive landscape. Government incentives through the Agricultural Development Fund specifically target processing infrastructure, with Balady's SAR 1.14 billion expansion plan allocating 40% of investment toward processed product lines. The sector's evolution toward ready-to-cook and ready-to-eat formats aligns with demographic shifts, as 70% of the population under 35 prioritizes convenience over traditional preparation methods.

Expansion of Foodservice and QSR Chains

The foodservice sector's explosive growth creates structural demand shifts that fundamentally alter poultry consumption patterns across the Kingdom. Al Tazaj's expansion to 125 outlets across the MENA region, supported by Fakieh Poultry Farms' strategic 30% stake sale in December 2024, demonstrates how vertical integration between producers and QSR operators drives volume growth. The foodservice market's projected 10% annual growth through 2030 creates predictable demand streams that enable producers to optimize supply chain efficiency and product standardization. The sector benefits from tourism initiatives under Vision 2030, where international visitor growth drives demand for standardized, halal-certified poultry products across hotel and restaurant chains. QSR operators increasingly demand specialized cuts and portion sizes, pushing producers toward flexible manufacturing systems that can accommodate both retail and foodservice specifications.

Government Support for Local Production

The Kingdom's USD 2 billion agricultural funding boost for 2025 represents a strategic acceleration of domestic poultry capacity, targeting critical infrastructure gaps that have historically constrained self-sufficiency. The Agricultural Development Fund's subsidized lending program has enabled major expansions, including Balady's 200 million bird capacity increase, while the USD 2 billion livestock city project in the Eastern Province will create the Middle East's largest integrated poultry complex. Vision 2030's food security mandate drives targeted investments in breeding stock, processing technology, and cold chain infrastructure, with the Saudi Export Development Authority providing specialized support for poultry exporters seeking regional market access [1]Source: Saudi Press Agency, "Package of Services and Programs to Increase Contribution of Non-Oil Exports to GDP", spa.gov.sa. The government's strategic partnership with China, formalized through USD 3.7 billion in agricultural agreements in May 2025, introduces advanced breeding technologies and sustainable farming practices that enhance productivity while reducing environmental impact. Regulatory streamlining through the Saudi Food and Drug Authority's updated import procedures reduces compliance costs for domestic producers while maintaining stringent quality standards that protect market positioning against imports.

Cultural Preference

Saudi consumers' deep-rooted preference for fresh, locally-produced poultry creates sustainable competitive advantages for domestic producers that transcend price competition. Research indicates 69% of Saudi consumers actively choose local food products over imports, with this preference particularly pronounced in poultry where freshness and halal certification intersect with cultural values. Halal certification requirements create natural barriers to entry for international competitors, while local producers benefit from established relationships with Islamic certification bodies and understanding of religious requirements. The Kingdom's food priority matrix, developed to support the National Strategy for Agriculture 2030, identifies poultry as a high-priority protein source due to consumption frequency and cultural acceptance. Regional preferences vary significantly, with Western Region consumers showing higher acceptance of processed formats while Central Region markets maintain stronger traditional preferences for whole bird purchases.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Disease/Avian Influenza Risks | -0.7% | National, with heightened risk in Eastern Province | Short term (≤ 2 years) |

| Consumer Shifts Toward Alternatives | -0.5% | Urban centers in Western and Central Regions | Long term (≥ 4 years) |

| Environmental and Sustainability Concerns | -0.4% | National, acute in water-scarce regions | Long term (≥ 4 years) |

| Feed Cost Volatility | -0.3% | National, impacting all production regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Disease/Avian Influenza Risks

The Kingdom's poultry sector faces persistent biosecurity challenges, with avian encephalomyelitis virus outbreaks documented in the Eastern Province highlighting the ongoing disease management complexities. The global highly pathogenic avian influenza strategy for 2024-2033 emphasizes the critical need for enhanced surveillance and prevention measures, particularly relevant given Saudi Arabia's position as a major poultry importer from regions with documented HPAI cases[2]Source: Food and Agriculture Organization of the United Nations, "Enhanced surveillance and prevention measures", openknowledge.fao.org. Biosecurity investments have intensified following international outbreaks, with producers implementing advanced monitoring systems and vaccination protocols that add 3-5% to production costs but provide essential protection against catastrophic losses. The sector's concentration among major producers creates systemic risks, where disease outbreaks at large facilities could significantly impact national supply chains and consumer confidence. Regulatory frameworks require continuous updates to address emerging pathogen threats, with the Saudi Food and Drug Authority implementing stringent import controls and domestic surveillance programs to maintain the Kingdom's disease-free status in key poultry segments.

Environmental and Sustainability Concerns

Water scarcity poses the most significant long-term constraint to poultry sector expansion, with agriculture consuming 88% of the Kingdom's freshwater resources and only 1% of land suitable for agricultural use. The livestock sector's substantial water footprint conflicts with national water conservation priorities, driving investments in closed-loop systems and alternative water sources that increase capital requirements by 15-20%. Climate change impacts on agricultural productivity, with temperature and precipitation changes negatively affecting feed crop yields, create additional cost pressures for producers dependent on imported grain. The government's commitment to plant 600 million trees by 2030 and establish a Global Water Organization reflects recognition of environmental constraints that will increasingly influence agricultural policy and investment decisions. Sustainable farming practices, including precision agriculture and waste management innovations, require significant upfront investments but offer long-term operational advantages and regulatory compliance benefits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Fresh Products Drive Premium Positioning

Fresh/Chilled products command 55.08% market share in 2025, reflecting Saudi consumers' cultural preference for perceived quality and freshness over convenience Al Rajhi Capital. However, Canned products are experiencing the fastest growth at 7.21% CAGR through 2031, driven by expanding foodservice demand and shelf-life advantages in the Kingdom's challenging climate conditions. In Saudi Arabia, consumers are increasingly purchasing pre-seasoned and marinated frozen poultry products. For instance, in February 2022, Seara introduced its 'Shawaya' Chicken at Gulfood 2022, representing a notable development in the frozen foods market. This marinated frozen chicken was designed for direct cooking from ‘freezer to oven,'. The product range includes frozen marinated whole chicken in three regional flavors, along with a pre-marinated tender whole chicken option. Fresh/chilled poultry meat offers greater culinary flexibility compared to frozen products. Consumers can easily marinate, season, and cook fresh/chilled poultry meat, resulting in enhanced flavors and textures. Market players continue to enhance their market presence through vertical integration, sustainable practices, and advanced production methods. For instancem, in July 2024, Tanmiah, a prominent fresh chicken producer in Saudi Arabia, achieved the AA+ Rating from BRCGS, representing a significant milestone in food safety certification.

Canned poultry products are widely utilized due to their convenience and ready-to-use characteristics. These products, typically pre-cooked, eliminate the need for processes such as thawing, marinating, or cooking from raw. They can be directly incorporated into various dishes, including sandwiches, salads, soups, or stews, offering significant time and effort savings. Suppliers are introducing high-quality products, such as organic and free-range options, to meet the demand for premium ingredients. Examples include organic canned chicken breast, free-range canned duck legs, gourmet canned turkey breast, premium canned quail, and organic canned Cornish hen, which provide opportunities for enhanced culinary applications. For instance, Swanson White Premium Chunk Canned Chicken, manufactured by Campbell Soup Company, is 98% fat-free, gluten-free, contains 18 grams of protein per 4.5-ounce can and is produced without antibiotics or added MSG, is available through both physical retail outlets and online platforms across the market.

By Nature: Organic Growth Accelerates Premium Trends

The Conventional segment maintains 87.15% market share in 2025, supported by established supply chains and cost competitiveness that align with mainstream consumer purchasing patterns. Organic products, while representing a smaller base, are expanding at 7.08% CAGR through 2031, driven by health-conscious consumers and premium positioning strategies among urban demographics. The organic segment's growth trajectory reflects broader dietary shifts among high-income consumers who prioritize perceived health benefits and are willing to pay premium pricing for certified products. Government support for sustainable farming practices, including organic certification programs, creates regulatory tailwinds that facilitate market expansion while ensuring quality standards.

Conventional producers are responding to organic growth through integrated strategies that include transitioning portions of their operations to organic standards while maintaining cost-effective conventional production for price-sensitive segments. The sector benefits from increasing availability of organic feed ingredients and improved certification processes that reduce compliance costs and time-to-market for organic products. Consumer education initiatives, supported by health awareness campaigns, continue to drive organic adoption rates, particularly among younger demographics who demonstrate stronger environmental consciousness and health prioritization in purchasing decisions.

By Distribution Channel: On-Trade Acceleration Reshapes Access

Off-Trade channels command 63.72% market share in 2025, dominated by supermarkets and hypermarkets that benefit from scale economies and consumer preference for one-stop shopping experiences. Within Off-Trade, supermarkets and hypermarkets lead market share, followed by convenience stores that serve immediate consumption needs, while online retail stores experience rapid growth driven by digital adoption and delivery infrastructure improvements. On-trade channels, despite smaller current share, are growing at 6.27% CAGR through 2031, propelled by foodservice sector expansion and tourism growth under Vision 2030 initiatives. The channel evolution reflects structural changes in Saudi consumption patterns, where dining out and food delivery services gain prominence among urban consumers.

BinDawood's USD 390 million investment in delivery hubs exemplifies the infrastructure development required to support omnichannel distribution strategies that bridge traditional retail and emerging digital channels. Online retail penetration creates new opportunities for direct-to-consumer sales and specialized product offerings that bypass traditional distribution constraints. The integration of cold chain logistics with digital platforms enables fresh poultry distribution through online channels, previously limited by temperature control and delivery time constraints.

Geography Analysis

The Western Region's market dominance at 50.10% share in 2025, combined with the fastest growth rate of 7.62% CAGR through 2031, reflects strategic advantages that extend beyond traditional market metrics. Jeddah's transformation into a processing hub, exemplified by JBS's USD 50 million nugget facility launch in November 2024, leverages port infrastructure for efficient feed imports while serving both domestic and export markets. The region benefits from proximity to Mecca's religious tourism, creating consistent demand for halal-certified products from international visitors and pilgrims. Government investment in food processing infrastructure, including specialized economic zones, provides regulatory advantages and infrastructure support that attract international partnerships and technology transfer agreements. The Western Region's coastal location enables efficient cold chain logistics for both imports and exports, positioning local producers to capture regional market opportunities across the Red Sea corridor. Advanced retail infrastructure, including modern hypermarkets and emerging e-commerce fulfillment centers, creates distribution efficiencies that support premium product positioning and margin expansion.

The Central Region, anchored by Riyadh's administrative and financial center status, maintains substantial market presence through institutional demand and corporate purchasing power. Government procurement policies favor local producers, creating predictable demand streams that enable capacity planning and investment decisions. The region's role as a transportation hub facilitates distribution to other geographic segments while supporting the concentration of major poultry companies' headquarters and administrative functions. Riyadh's growing expatriate population drives demand for diverse product formats and international cuisine ingredients, creating opportunities for specialized poultry products and value-added offerings. The Central Region's investment in logistics infrastructure, including automated distribution centers and cold storage facilities, enhances supply chain efficiency while reducing product loss and quality degradation during transportation.

The Northern and Southern Regions represent emerging growth opportunities, with the planned USD 2 billion livestock city project in the Eastern Province expected to create the Middle East's largest integrated poultry complex. These regions benefit from lower land costs and government incentives for agricultural development, attracting investment in large-scale production facilities that leverage economies of scale. The geographic diversification strategy reduces concentration risks while capturing local market demand and supporting regional economic development objectives under Vision 2030. Water resource availability varies significantly across regions, with Northern areas facing greater constraints that drive adoption of water-efficient production technologies and alternative water sources. The regions' proximity to international borders creates opportunities for cross-border trade and export market development, particularly for producers seeking to diversify revenue sources beyond domestic consumption.

Competitive Landscape

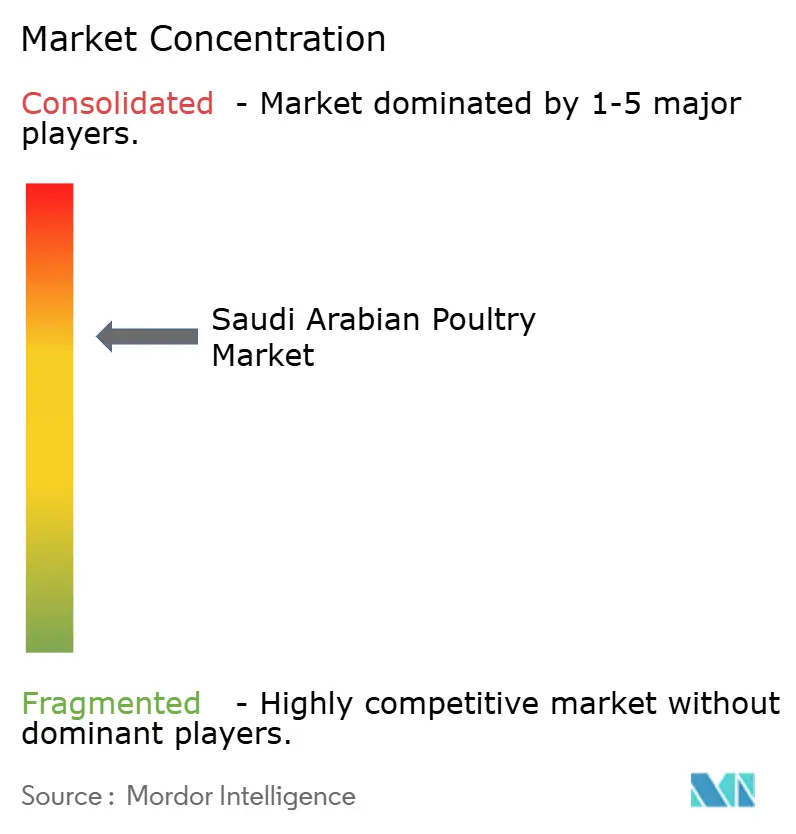

The Saudi Arabian Poultry Market exhibits slightly high concentration, characterized by intense competition among established players and emerging consolidation opportunities. The ongoing SAR 2 billion (USD 533 million) acquisition battle for Al Watania Poultry between Almarai and Tanmiah exemplifies the sector's strategic value and consolidation dynamics. Market Players include Al-Watania Poultry, Fakieh Group, Almarai, Tanmiah Food Company, and Sunbulah Group, among others.

Market leaders employ vertical integration strategies, controlling feed production, breeding, processing, and distribution to capture value chain margins and ensure quality consistency. Technology adoption serves as a key differentiator, with AI-based monitoring systems achieving 93.1% precision in flock management and IoT integration enabling real-time optimization of feed conversion ratios and environmental controls. Strategic partnerships with international players drive technology transfer and market access, as demonstrated by the Tyson-Tanmiah collaboration that doubles processed product capacity while introducing advanced manufacturing techniques.

Opportunities emerge in organic products, specialty processed formats, and regional market penetration, where smaller players can leverage niche positioning and agility advantages. The sector's regulatory framework, including halal certification requirements and Saudi Food and Drug Authority standards, creates natural barriers to entry while protecting domestic producers from international competition. Emerging disruptors focus on sustainable production methods, alternative protein integration, and direct-to-consumer distribution models that bypass traditional wholesale channels and capture premium pricing for differentiated products.

Saudi Arabian Poultry Industry Leaders

-

Al-Watania Poultry

-

Fakieh Group

-

Tanmiah Food Company

-

Sunbulah Group.

-

Almarai Company Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Tanmiah Food Company, in collaboration with McDonald's Saudi Arabia, defied expectations and set new industry benchmarks through a strategic partnership. This alliance, centered on promoting locally sourced poultry, underscored both companies' commitment to quality and the development of local agriculture.

- July 2025: Brazilian meat processor BRF launched its inaugural line of chilled chicken products in Saudi Arabia. This launch underscored BRF's ongoing efforts to bolster its foothold in Saudi Arabia, aiming to lessen its reliance on export sales to the kingdom by amplifying domestic supplies in this pivotal market.

- April 2025: Brazilian meatpacker BRF SA unveiled plans to construct a new processing facility in Jeddah, Saudi Arabia, marking a USD 160-million investment. This project emerged from a collaboration between BRF SA and the Halal Products Development Co. (HPDC), a subsidiary of Saudi Arabia's Public Investment Fund (PIF).

Saudi Arabian Poultry Market Report Scope

Poultry refers to domesticated avian species that can be raised for eggs, meat, and feathers. It covers a wide range of birds, from indigenous and commercial breeds of chickens to Muscovy ducks, mallard ducks, turkeys, guinea fowl, geese, quail, pigeons, ostriches, and pheasants.

The Saudi Arabia poultry market is segmented by product type and distribution channel. By product type, the market is segmented into eggs, broiler meat, and processed meat. Processed meat is further segmented into nuggets and popcorn; burgers; mortadella; franks, sausages, hot dogs; marinated poultry products; and other processed meat products. By distribution channel, the market is segmented into on-trade and off-trade. Off-trade was further segmented into hypermarkets/supermarkets, convenience stores, online retail, and other distribution channel.

The report offers the market size in value terms in USD for all the abovementioned segments.

By Form

| Canned | |

| Fresh/Chilled | |

| Frozen | |

| Processed | Deli Meats |

| Marinated/Tenders | |

| Meatballs | |

| Nuggets | |

| Sausages | |

| Other Processed Poultry |

By Nature

| Organic |

| Conventional |

By Distribution Channel

| Off-trade | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Others | |

| On-trade |

By Region

| Western Region |

| Northern Region |

| Southern Region |

| Central Region |

| By Form | Canned | |

| Fresh/Chilled | ||

| Frozen | ||

| Processed | Deli Meats | |

| Marinated/Tenders | ||

| Meatballs | ||

| Nuggets | ||

| Sausages | ||

| Other Processed Poultry | ||

| By Nature | Organic | |

| Conventional | ||

| By Distribution Channel | Off-trade | Supermarkets/Hypermarkets |

| Convenience Stores | ||

| Online Retail Stores | ||

| Others | ||

| On-trade | ||

| By Region | Western Region | |

| Northern Region | ||

| Southern Region | ||

| Central Region | ||

Key Questions Answered in the Report

What is the current Saudi Arabia Poultry Market size?

The Saudi Arabia Poultry Market size is estimated at USD 5.43 billion in 2026 and is projected to register a CAGR of 5.85% during the forecast period (2026-2031).

Which Saudi region currently leads poultry consumption and production?

The Western Region holds 50.10% share and is on track for an 7.62% CAGR, strengthened by Jeddah’s expanding processing hub.

What pace are processed and canned poultry formats registering?

Canned lines are expanding at a 7.21% CAGR as convenience demand rises, while broader processed offerings gain volume from new nugget and marinated-cut capacity.

Page last updated on: