Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

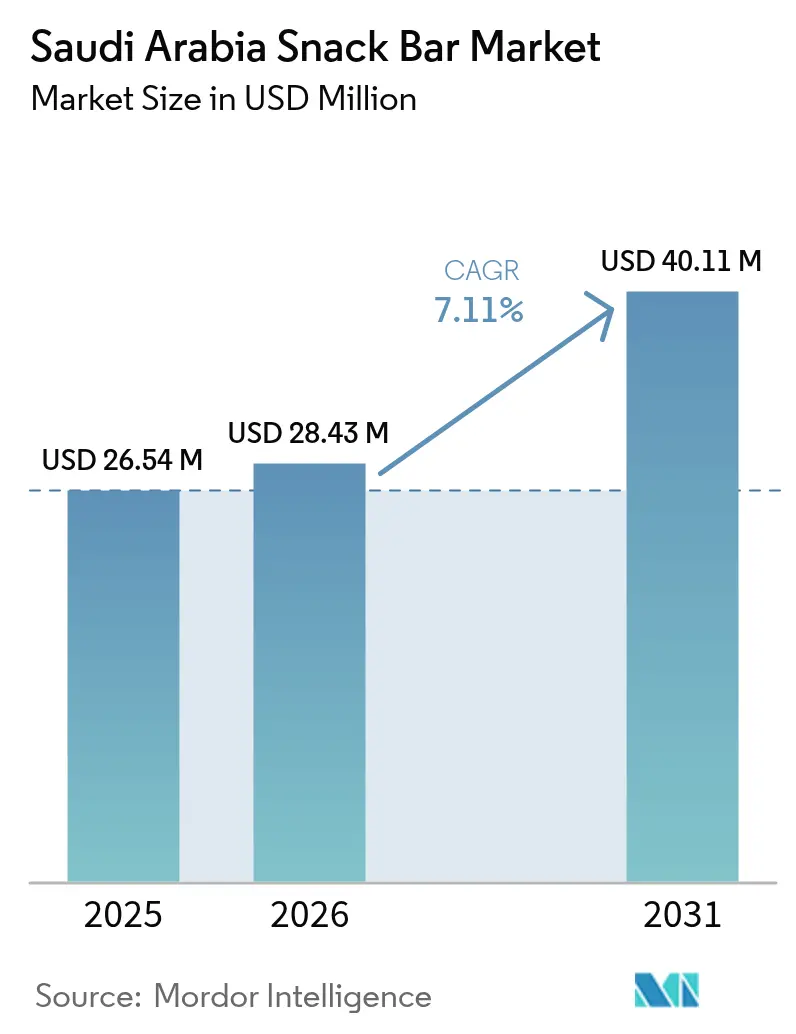

| Base Year Market Size (2025) | USD 26.54 Million |

| Market Size (2026) | USD 28.43 Million |

| Market Size (2031) | USD 40.11 Million |

| Growth Rate (2026 - 2031) | 7.11% CAGR |

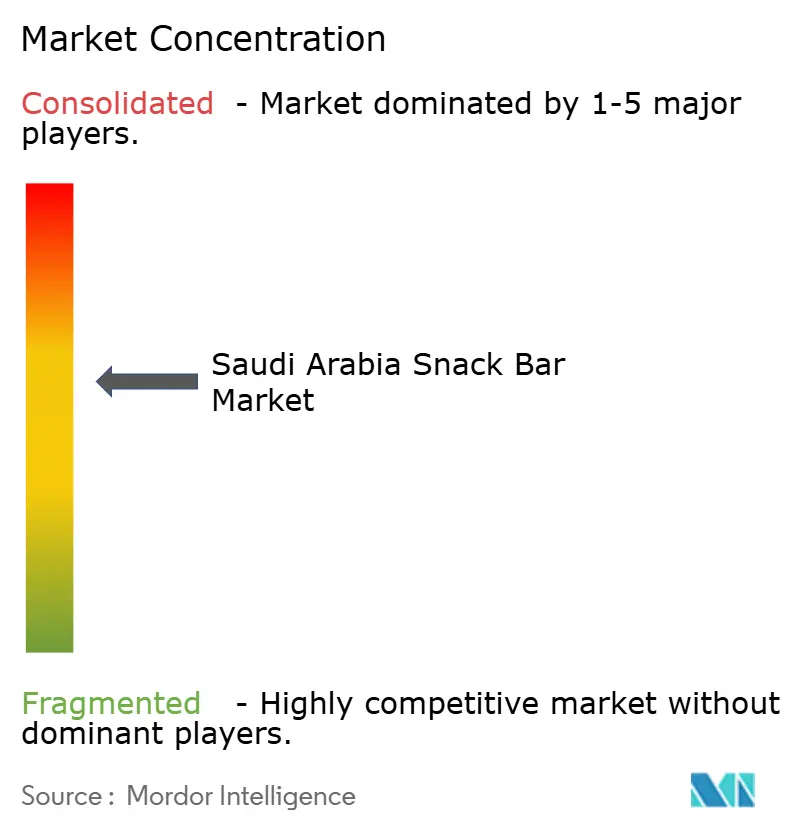

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Saudi Arabia Snack Bar Market Analysis by Mordor Intelligence

The Saudi Arabia snack bar market size was valued at USD 26.54 million in 2025 and estimated to grow from USD 28.43 million in 2026 to reach USD 40.11 million by 2031, at a CAGR of 7.11% during the forecast period (2026-2031). Saudi Arabia's Vision 2030 health initiatives, urban lifestyle shifts, and a USD 10 billion food-security investment program are driving the country's upward trajectory[1]Source: Multidisciplinary Digital Publishing Institute, "Saudi Arabia’s Healthy Food Strategy: Progress & Hurdles in the 2030 Road", mdpi.com. These initiatives not only bolster domestic supply chains but also underscore the Kingdom's commitment to health and wellness. General Authority for Statistics statistics revealed that in 2024, 58.5% of individuals aged 18 and above in the Kingdom engaged in at least 150 minutes of exercise weekly[2]Source: General Authority for Statistics (GASTAT), "General Authority for Statistics Announces Physical Activity Statistics for Saudi Arabia in 2024", mos.gov.sa. This growing fitness culture fuels a consistent demand for protein-rich convenience foods. Market players are reaping rewards from mandatory calorie disclosures and trans-fat bans, which favor transparent and reformulated products. Additionally, regulatory alignments, enhancements in cold-chain logistics, and surging travel retail volumes during the Hajj and Umrah seasons are expanding the market's addressable demand. The ecosystem dynamics are further enriched by multinational consolidations, a shift towards local ingredient sourcing, and a swift acceleration in e-commerce, all pointing towards a robust and sustained growth trajectory for Saudi Arabia's snack bar market.

Key Report Takeaways

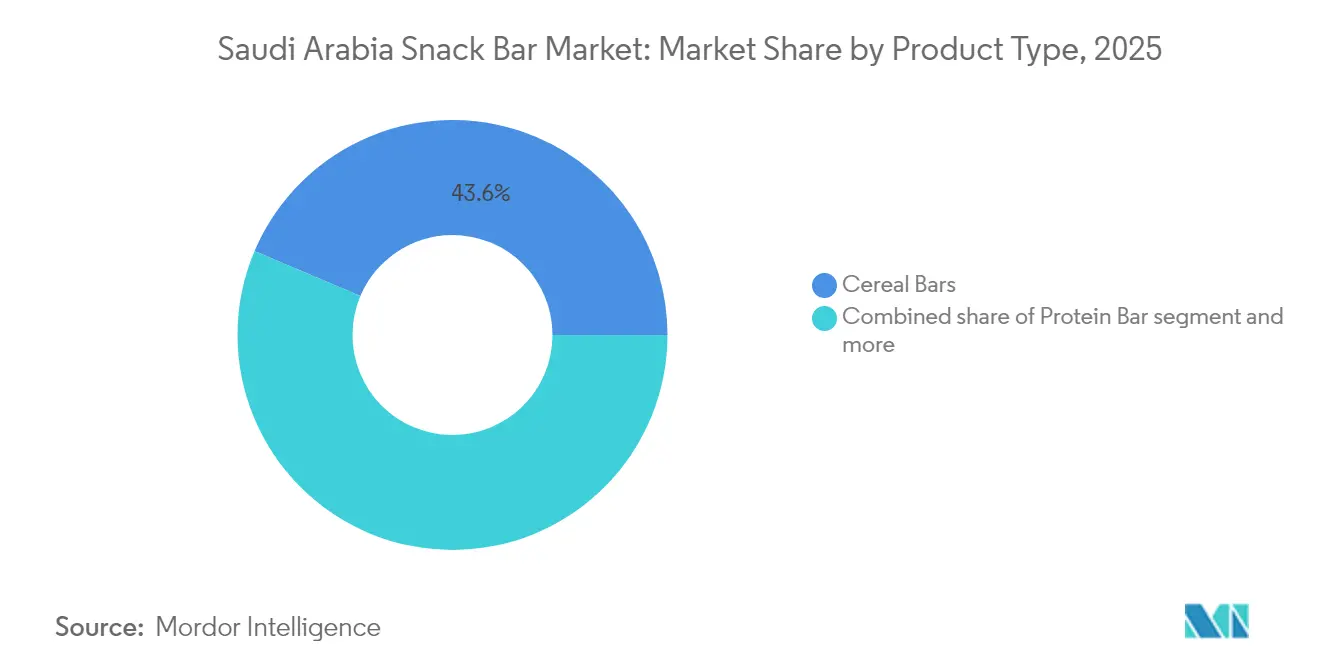

- By product type, cereal bars led with 43.62% of the 2025 Saudi Arabia snack bar market share and energy bars are projected to record the fastest 7.97% CAGR from 2026-2031.

- By flavor profile, chocolate variants commanded 34.21% revenue share in 2025, while nuts and seeds flavors are expected to expand at a 7.62% CAGR through 2031.

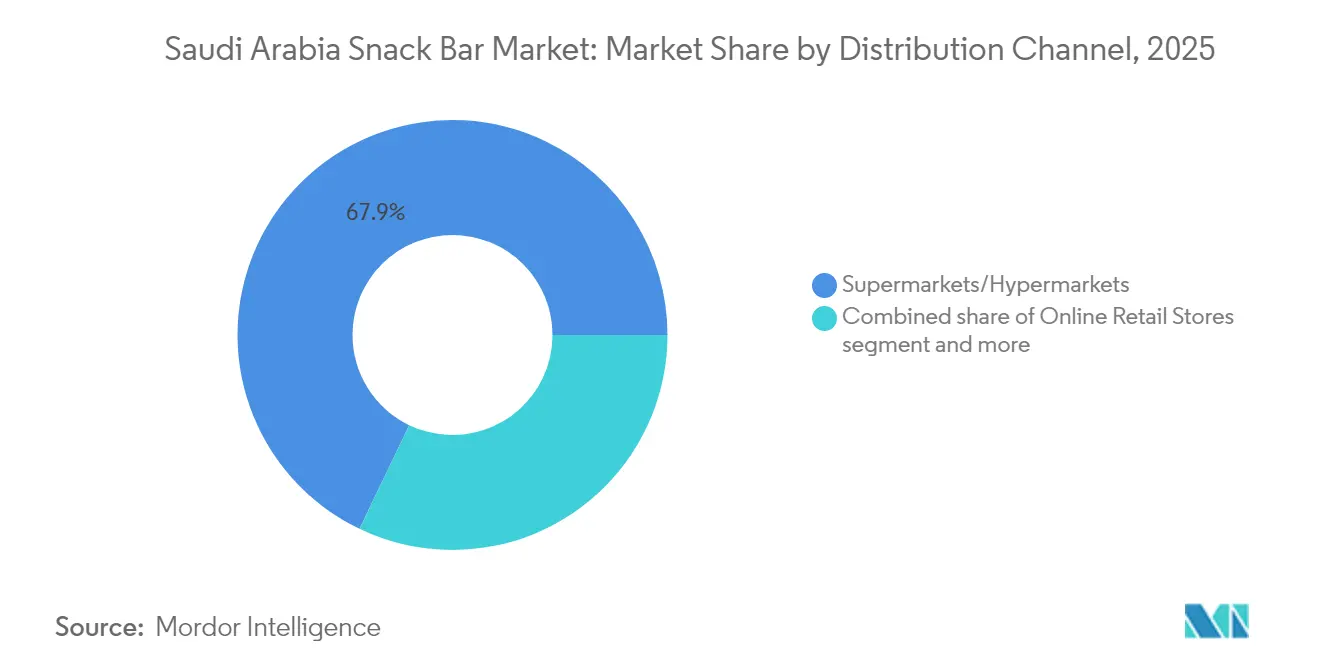

- By distribution channel, supermarkets and hypermarkets held 67.88% of the 2025 market, whereas online retail is poised for the sharpest 7.73% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Snack Bar Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for convenient on-the-go breakfast options | +1.8% | Riyadh, Jeddah, Eastern Province | Medium term (2-4 years) |

| Growth of fitness culture and gym membership | +1.5% | Urban centers, secondary cities | Long term (≥ 4 years) |

| Expanding modern grocery retail footprint | +1.2% | National | Short term (≤ 2 years) |

| Government “Healthy Food Strategy” initiatives | +1.0% | National | Long term (≥ 4 years) |

| Higher disposable income among Saudi millennials | +0.9% | Urban areas | Medium term (2-4 years) |

| Rise of Hajj and Umrah tourism boosting travel retail | +0.7% | Mecca, Medina, major airports | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand for convenient on-the-go breakfast options

As urbanization accelerates, busy professionals increasingly opt for on-the-go breakfast solutions to accommodate compressed morning routines. Extended shifts at Vision 2030 mega-project sites are driving up sales volumes, particularly through construction camps and corporate cafeterias, where demand for convenient and nutritious options is high. With consumer spending on the rise, premium pricing is becoming more feasible, as consumers are willing to pay for quality and convenience. Additionally, the local abundance of dates and dairy not only keeps costs down but also ensures products resonate with cultural flavor preferences, making them more appealing to the target audience. These ingredients allow manufacturers to create cost-efficient formulations that align with both taste expectations and nutritional needs. Meanwhile, government-backed workplace wellness initiatives are further promoting the shift towards healthier packaged options by endorsing products that align with nutritional guidelines and wellness goals. Such programs are fostering greater awareness and acceptance of healthier eating habits among working professionals.

Growth of fitness culture and gym membership

In Saudi Arabia, a growing number of adults are meeting the World Health Organization's activity benchmarks, reflecting an increasing awareness of physical fitness in the region. At the same time, the market for sports-nutrition supplements is expanding, driven by rising consumer demand for health and wellness products. With protein recommendations set at 1.2-2 g/kg of body mass, higher-protein bars are gaining traction as preferred post-workout solutions, catering to the nutritional needs of active individuals. Local start-ups are tapping into influencer marketing to build brand recognition and connect with younger demographics, while global brands are seizing opportunities presented by the country's expanding sports infrastructure, including new gyms and fitness centers. The allure of enhanced performance and stress relief resonates with both athletes striving for better results and corporate professionals seeking to manage work-related stress effectively.

Expanding modern grocery retail footprint

Saudi Arabia is rapidly modernizing its retail landscape, marked by significant chain expansions and a robust push into e-commerce. Notably, the grocery e-commerce sector is expected to witness significant growth in the coming years. In 2023, the Kingdom's food retail market achieved remarkable expansion, supported by consistent annual growth. This growth is largely attributed to the rise of hypermarkets and supermarkets in secondary cities, extending their reach beyond the traditional hubs of Riyadh and Jeddah. As modern retail expands, it establishes standardized distribution channels. These channels increasingly favor packaged snack bars over the traditional loose snacks. Furthermore, advanced cold-chain capabilities play a pivotal role in preserving functional ingredients. The Jeddah Food Cluster, spanning an impressive 11 million square meters and recognized by Guinness World Records as the world's largest food park, boasts 134,000 square meters dedicated to shared cold and dry storage[3]Source: Saudi Food Manufacturing," Saudi Arabia Unveils World’s Largest Food Park in Jeddah, Eyes $5.3B in Investments", saudifoodmanufacturing.com. This facility significantly cuts distribution costs for temperature-sensitive products. Embracing retail technology, from digital inventory management to consumer analytics, has empowered retailers with enhanced demand forecasting and optimized shelf space for snack bar categories. Since 2023, a mandate for local content procurement at government facilities has opened up new distribution avenues, especially through institutional channels.

Government's "healthy food strategy" initiatives

In September 2018, the Saudi Food and Drug Authority (SFDA) launched its "Healthy Food Strategy." This initiative seeks to establish a transparent regulatory framework for snack products, requiring calorie disclosures and setting targets for sodium reduction. SFDA identified gaps in compliance with these voluntary sodium limits, highlighting the need for reformulation a shift that benefits manufacturers of compliant snack bars. The strategy also prohibits partially hydrogenated oils, effectively eliminating trans fats from snacks. Additionally, a significant excise tax on sugar-sweetened beverages enhances the appeal of low-sugar snack alternatives. Food establishments are required to disclose calorie counts on menus, with inspections revealing areas of non-compliance, suggesting a potential crackdown that could favor brands emphasizing transparency. The government's "Balanced Meal" certification provides a marketing advantage to compliant products. However, only a small portion of manufacturers have adopted the voluntary front-of-pack nutrition labeling, positioning early adopters for significant gains. SFDA also mandates allergen declarations across various categories, simplifying labeling for international brands targeting the Saudi market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price sensitivity amid subsidy reforms | -1.4% | National, rural focus | Short term (≤ 2 years) |

| Perception of high sugar content in certain bars | -0.8% | Health-conscious urban consumers | Medium term (2-4 years) |

| Limited cold-chain for functional ingredient bars | -0.6% | Rural and remote areas | Long term (≥ 4 years) |

| Dominance of traditional snacks in rural areas | -0.5% | Rural regions, smaller cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price sensitivity amid subsidy reforms

Saudi Arabia's ongoing subsidy cuts are making consumers more price-sensitive, especially when it comes to discretionary food items like premium snack bars. In March 2025, food inflation hit 2.0% year-over-year. At the same time, the Kingdom's broader economic reforms, which include implementing VAT and adjusting energy subsidies, are straining household budgets. While diesel price hikes in January 2025 had a slight impact on production costs for major food manufacturers, smaller entities grappled with relatively steeper logistics costs. In response, consumers are turning to bulk buying and seeking value, opting for multipacks and promotions instead of premium single servings. Traditional snacks, often much cheaper than their imported or premium local counterparts, continue to exert competitive pressure in price-sensitive markets. Yet, with millennials and urban professionals enjoying rising disposable incomes, there's a noticeable split in the market: one segment remains value-conscious, while the other leans towards premium offerings.

Perception of high sugar content in certain bars

As health consciousness rises among consumers, skepticism is mounting towards certain snack bars. Energy bars and chocolate variants, often high in sugar content, are under particular scrutiny. The Saudi Healthy Food Strategy, which emphasizes reduced sugar intake and levies a significant excise tax on sugary beverages, has intensified the focus on added sugars across various food categories. Surveillance by the Saudi Food and Drug Authority (SFDA) revealed that a majority of food products marketed to children exceeded the sugar limits set by the World Health Organisation (WHO). Such findings could influence perceptions of snack bars, especially given their broader implications. Recent studies show that many young adults have a solid grasp of nutrition, driving a demand for cleaner labels that prioritize natural sweeteners or reduced sugar. In response, the market is shifting towards date-based sweeteners, leveraging Saudi Arabia's rich date production, and spotlighting protein-to-sugar ratios rather than just sugar content. This challenge offers brands a distinct opportunity to set themselves apart by emphasizing functional benefits over mere taste indulgence.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Cereal Bars Lead Despite Energy Bar Momentum

In 2025, cereal bars dominated the Saudi snack bar market, claiming 43.62% of total revenues. This stronghold is largely due to Saudi consumers' deep-rooted affinity for granola and oat-based products, which seamlessly integrate into their traditional grain-centric breakfasts. Valued for their convenience and wholesomeness, cereal bars have found favor among a diverse demographic, from busy professionals to schoolchildren. For local consumers, cereal bars feel like a natural progression of their established eating habits, making them easier to embrace than more specialized formats. Boosted by global brand visibility and the introduction of regionally-inspired formulations, cereal bars have deepened their cultural resonance. Given their adaptability and the trust they've garnered, cereal bars are poised to maintain their leading position, even as they face heightened competition from functional and hybrid snack formats.

Energy bars are the market's fastest-growing segment, with projections indicating a CAGR of 7.97% through 2031. Their surge is closely linked to Saudi Arabia's burgeoning fitness culture, fueled by rising investments in gyms, fitness centers, and sports clubs. As awareness of sports nutrition, especially energy balance and recovery, grows, energy bars have carved a niche among urban youth and active professionals. Unlike their cereal counterparts, energy bars are positioned as performance enhancers, appealing to a younger audience driven by fitness aspirations. Innovations tailored to workout needs, like carbohydrate-rich pre-exercise bars and post-exercise replenishment options, are diversifying consumer choices. With rising disposable incomes and a shift towards health-conscious living, energy bars are set to spearhead the market's premiumization trend, attracting consumers who prioritize nutrition as a cornerstone of their long-term performance and well-being.

By Flavor Profile: Chocolate Dominance Faces Nuts and Seeds Challenge

In 2025, chocolate-based flavors dominated the Saudi snack bar flavor segment, capturing 34.21% of the market share. Their widespread allure is rooted in a global perception of chocolate as a symbol of indulgence and comfort, appealing to diverse age groups and income brackets. This deep-seated emotional bond consumers share with chocolate solidifies its status as a cornerstone flavor, pivotal in both mainstream and premium market strategies. Yet, challenges loom. The Saudi Food and Drug Authority (SFDA) is intensifying its focus on reducing sugar content. Given that chocolate formulations have historically leaned on added sugars for sweetness and texture, this regulatory shift is significant. Manufacturers are now urged to pivot, exploring alternatives like natural sweeteners or amplifying cocoa content to meet these new health benchmarks. Still, in settings driven by impulse purchases, chocolate's familiar allure and the promise of indulgence keep it at the forefront of consumer choices.

Nuts and seeds flavors are emerging as the fastest-growing segment, projected to grow at a CAGR of 7.62% through 2031. Their ascent is largely due to a pivot among health-conscious consumers towards products that are perceived as clean, natural, and nutrient-rich. Packed with protein, fiber, and healthy fats, nuts and seeds resonate with sports nutrition ideals and align with government-endorsed health initiatives promoting balanced diets. The global superfood trend further amplifies this interest, spotlighting ingredients like almonds, chia, and sunflower seeds as valuable additions to daily snacks. There's also potential to weave in culturally significant flavors, using regional nuts and traditional pairings to boost local appeal. Yet, a primary hurdle lies in ensuring texture consistency and shelf stability amidst Saudi Arabia's sweltering climate. Despite this, the category's knack for balancing nutritional benefits with cultural relevance positions it as a vibrant growth engine in the flavor landscape.

By Distribution Channel: Supermarkets Reign While Online Surges

In 2025, supermarkets and hypermarkets dominated Saudi Arabia's snack bar distribution, capturing 67.88% of total sales. This dominance underscores deep-rooted consumer habits, with families gravitating towards these venues for a comprehensive grocery experience. The extensive product range, heightened promotional visibility, and trust in well-established retail brands bolster their position in the consumer packaged goods arena, snack bars included. Beyond mere shopping, many Saudis view these outlets as gateways to new snack discoveries, thanks to in-store promotions and sampling. Their robust cold-chain infrastructure offers superior storage for sensitive products, a distinct advantage over traditional outlets. While this supremacy is set to continue in the near future, the rise of digital channels is beginning to alter the dynamics.

Online retail, though currently a minor player, is the fastest-growing channel, with a projected CAGR of 7.73% through 2031. This surge is propelled by Saudi Arabia's swift retail modernization and significant e-commerce infrastructure investments, highlighted by iHerb’s climate-controlled fulfillment center in Riyadh and bolstered last-mile delivery networks. Online platforms not only broaden access to global snack bar selections but also introduce subscription services and tailored nutrition advice, setting them apart from brick-and-mortar stores. The booming e-grocery sector, anticipated to grow at a 15.2% CAGR through 2029, underscores the rising significance of digital retail in the snack bar market. However, hurdles persist, especially in maintaining temperature controls for sensitive ingredients like probiotics. Additionally, navigating the stringent licensing from the Saudi Food and Drug Authority and securing halal certifications pose challenges for global entrants. Yet, the unique blend of convenience and customization offered by online retail positions it as the most transformative and scalable channel for the future.

Geography Analysis

Urban centers dominate Saudi Arabia's snack bar market, with Riyadh, Jeddah, and the Eastern Province leading in consumption. This trend is fueled by higher disposable incomes, a surge in modern retail, and a lifestyle shift towards convenience foods. In the capital, government job stability and mega-projects boost demand for on-the-go nutrition, especially among busy professionals. Jeddah, serving as the commercial heart and a key entry point for Hajj pilgrims, reaps the benefits of a thriving travel retail scene. Meanwhile, the Eastern Province, bolstered by its oil industry, enjoys a workforce with steady purchasing power, even amidst economic shifts. Looking ahead, the government's Vision 2030, with its focus on economic diversification, NEOM development, and tourism growth, is reshaping the market landscape, pushing consumption centers beyond the usual urban hotspots.

While secondary cities and rural locales hold promise for growth, they're hampered by traditional snacking habits, a lack of cold-chain infrastructure, and price sensitivity. Rural areas, with their cultural leanings, still favor traditional snacks, relying on established supply chains that prioritize local over packaged options. Yet, with the government pouring investments into infrastructure like the cold storage at Jeddah's Food Cluster and enhanced logistics the market's reach is steadily broadening. Furthermore, the Kingdom's commitment to food security, underscored by a USD 10 billion agricultural investment and a push for local production, paves the way for homegrown snack bars. These bars can harness regional ingredients, curbing the reliance on imports.

Mecca and Medina, central to religious tourism, showcase distinct consumption trends, especially during pilgrimage seasons. These cities experience a significant influx of visitors during Hajj and Umrah, leading to heightened demand for goods and services tailored to the needs of pilgrims. As authorities aim to boost pilgrim numbers in the near future, a corresponding rise in demand for culturally and dietary diverse travel snacks is expected. This includes snacks that cater to halal requirements and regional taste preferences, ensuring convenience for travelers. Regions near borders and transport hubs thrive on transit-related consumption, driven by the movement of pilgrims and tourists. At the same time, with Vision 2030 propelling both population and commercial growth, new demand centers are emerging in economic zones and specially designated development areas, further diversifying consumption patterns and creating opportunities for businesses to cater to evolving needs.

Competitive Landscape

Saudi Arabia's snack bar market reflects a moderate consolidation, wherein established multinationals vie for dominance against a backdrop of rising local contenders. Almarai, a prominent player, is shifting its strategy. In March 2025, the company made headlines by purchasing Hamouda Food for SAR 263 million (USD 70.1 million). This acquisition marks a notable shift for Almarai, traditionally rooted in dairy, now setting its sights firmly on the snack sector. The move underscores Almarai's ambition to broaden its product range and seize a more substantial stake in the burgeoning snack bar market. Meanwhile, on the global stage, industry titans are making waves. Mars' monumental USD 36 billion acquisition of Kellanova and Ferrero's takeover of Power Crunch not only bolsters their portfolios but also grants them unparalleled scale advantages. Such strategic consolidations empower these giants to refine operations, bolster distribution channels, and fortify their market foothold, an endeavor that's a tall order for smaller players to achieve through organic growth.

Crafting culturally tailored products with traditional Saudi ingredients like dates, cardamom, and local nuts holds significant promise. These ingredients not only resonate with local tastes but also appeal to the growing global demand for authentic and exotic flavors. Companies leveraging these ingredients can tap into both domestic and international markets, creating a unique value proposition. Additionally, the use of traditional ingredients aligns with the increasing consumer preference for natural and heritage-based products, further driving growth opportunities. Disruptors are adopting direct-to-consumer models and subscription services, avoiding traditional retail margins. This approach allows them to build stronger customer relationships, gather direct feedback, and offer personalized experiences. By embracing technology, industry players are focusing on supply chain efficiencies, cold-chain management, and digital marketing, with a keen emphasis on engaging the youth through social media. These advancements not only reduce operational costs but also enhance customer outreach, particularly among tech-savvy younger demographics who are driving consumption trends.

Saudi Arabia's Food and Drug Authority upholds a rigorous regulatory framework, requiring halal certifications and allergen labeling. These regulations ensure that products meet the highest standards of safety and cultural compliance, fostering consumer trust in the market. For seasoned players, adhering to these standards strengthens their brand reputation and competitive edge. However, for newcomers, navigating these stringent requirements can be a significant barrier, often necessitating additional investments in compliance and certification processes. Despite these challenges, the regulatory environment also creates opportunities for innovation, as companies develop new methods to meet these standards efficiently. Furthermore, the emphasis on halal and allergen labeling aligns with global trends, enabling Saudi products to compete effectively in international markets where such certifications are increasingly valued.

Saudi Arabia Snack Bar Industry Leaders

-

PepsiCo Inc

-

Kellonova

-

General Mills, Inc

-

Simply Good Foods Co

-

Mondelez International, Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: MrBeast's Feastables snack brand announced plans for a comprehensive launch in Saudi Arabia by September 2025. This expansion moves beyond select Lulu Hypermarket locations, aiming for wider distribution channels. Targeting Saudi Arabia's USD 57 billion food and beverage market, this initiative presents a significant growth opportunity for Beast Industries. Feastables, which raked in over USD 250 million in revenue in 2024, is set to enter a competitive arena alongside a slew of international Food and Beverage brands, all eager to capture a slice of the Kingdom's burgeoning economy.

- November 2023: Tomoor unveiled its latest offering: pure energy bars crafted from dates and sweetened with date sugar. These energy bars are designed to cater to health-conscious consumers seeking natural and nutritious snack options.

Saudi Arabia Snack Bar Market Report Scope

The Saudi Arabian snack bar market is segmented on the basis of type including cereal bars, energy bars, and other snack bars. The cereal bars further includes granola bars and other cereal bars. Based on distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores, specialty stores, online stores, and other distribution channels.

By Product Type

| Cereal Bars | Granola Bars |

| Other Cereal Bars | |

| Protein Bars | |

| Other Snack Bars |

By Flavor Profile

| Chocolate-based |

| Fruit-based |

| Nuts and Seeds |

| Others |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Online Stores |

| Other Off-Trade Channels |

| By Product Type | Cereal Bars | Granola Bars |

| Other Cereal Bars | ||

| Protein Bars | ||

| Other Snack Bars | ||

| By Flavor Profile | Chocolate-based | |

| Fruit-based | ||

| Nuts and Seeds | ||

| Others | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Stores | ||

| Other Off-Trade Channels |

Key Questions Answered in the Report

How large is the Saudi Arabia snack bar market in 2026?

The Saudi Arabia snack bar market size is USD 28.43 million in 2026 and is forecast to reach USD 40.11 million by 2031.

What is the current growth rate for snack bars in Saudi Arabia?

The market is progressing at a 7.11% CAGR over the 2026-2031 forecast window, propelled by health initiatives and fitness culture.

Which product type sells the most bars today?

Cereal bars hold 43.62% of 2025 sales, benefiting from breakfast compatibility and broad supermarket availability.

Which flavor category is gaining the fastest momentum?

Nuts and seeds flavors are expanding at a 7.62% CAGR, driven by clean-label perceptions and higher protein content.

Page last updated on: