Full Service Restaurants Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.47 Trillion |

| Market Size (2031) | USD 1.72 Trillion |

| Growth Rate (2026 - 2031) | 3.26% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Full Service Restaurants Market Analysis by Mordor Intelligence

The full-service restaurants market size is expected to grow from USD 1.42 trillion in 2025 to USD 1.47 trillion in 2026 and is forecast to reach USD 1.72 trillion by 2031 at 3.26% CAGR over 2026-2031. Structural shifts are emerging, with weight-loss medications reducing visit frequency while artificial intelligence helps operators recover margins through dynamic pricing. Competitive intensity is now driven by technology adoption rather than scale. AI-driven personalization and dynamic pricing platforms are adding 200 to 400 basis points of margin, while static menu boards face margin pressure from food cost inflation of 5% to 8% annually in key protein and produce categories. GLP-1 medication adoption is creating a split demand profile, with most users cutting restaurant spending but seeking higher-quality, portion-controlled options. This trend benefits operators with flexible supply chains over large chains tied to centralized distribution. Labor cost increases and tip-credit policy changes are reshaping unit economics in North America and Europe. California’s USD 20 per hour minimum wage for limited-service restaurants, implemented in 2024, is influencing full-service labor markets, while 72% of US consumers report tipping fatigue as gratuity prompts increase across payment terminals[1]Source: California Department of Industrial Relations, "Fast Food Minimum Wage Frequently Asked Questions", dir.ca.gov.

Key Report Takeaways

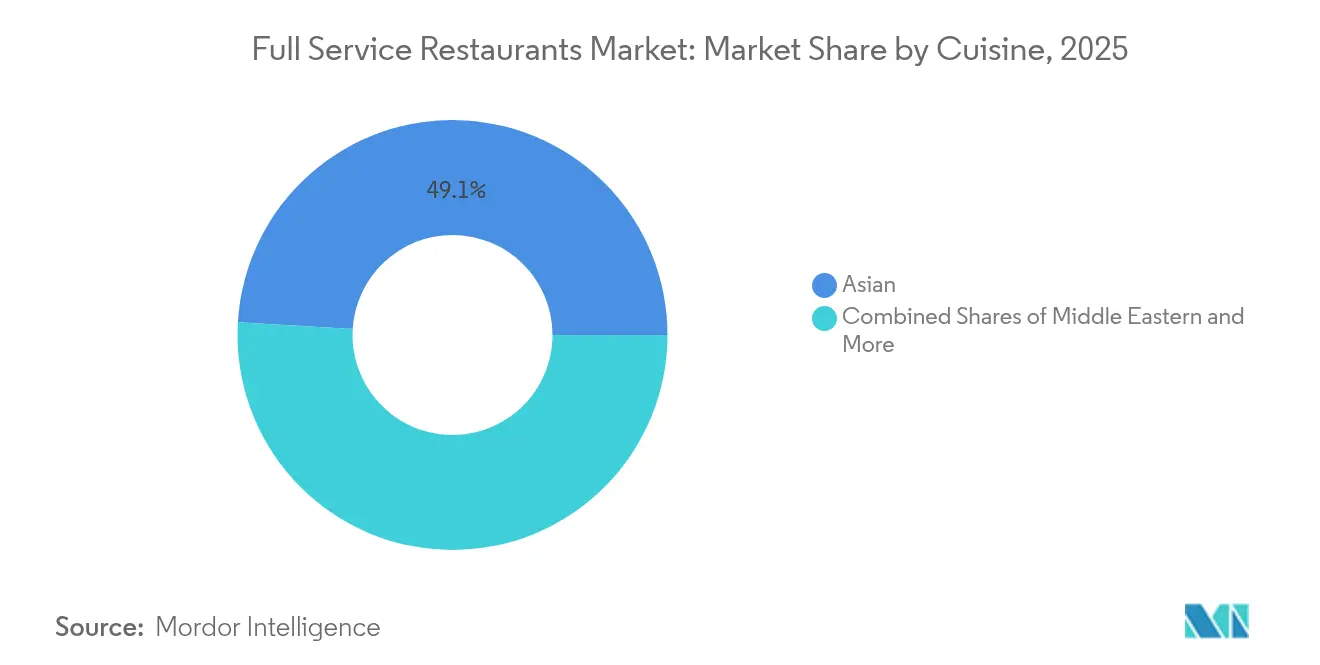

- By cuisine, Asian concepts held 49.05% of full-service restaurants market share in 2025, while Middle Eastern formats are expanding at a 5.57% CAGR through 2031.

- By outlet type, independents controlled 65.31% of 2025 revenue; chains are advancing at a 5.94% CAGR on the back of AI-driven customer analytics.

- By service type, delivery revenues are forecast to grow 7.15% annually, although dine-in still generated 65.83% of 2025 sales.

- By geography, North America is projected to post the fastest regional CAGR at 6.55% through 2031, surpassing Asia-Pacific’s growth despite holding a smaller 2025 base.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Full Service Restaurants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising disposable incomes and preference for dining out | +0.8% | Global, with concentration in North America, the Middle East, and urban Asia-Pacific | Medium term (2-4 years) |

| Digital ordering and delivery platforms are scaling off-premise demand | +1.2% | Global, led by North America and Europe, is expanding in Latin America and the Asia-Pacific | Short term (≤ 2 years) |

| Post-pandemic rebound of on-premise social occasions | +0.6% | Global, strongest in North America and Europe | Short term (≤ 2 years) |

| Chain franchising expansion in emerging markets | +0.5% | Latin America, the Middle East, Africa, and Southeast Asia | Long term (≥ 4 years) |

| GLP-1 driven menu downsizing and frequency uplift | +0.3% | North America and Europe, early adoption in affluent Asia-Pacific markets | Medium term (2-4 years) |

| AI-driven dynamic pricing and personalization boosting margins | +0.4% | North America and Europe, pilot deployments in the Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising disposable incomes and preference for dining out

Household discretionary spending on food away from home is expanding across developed and emerging markets, with the US Bureau of Economic Analysis reporting personal consumption expenditures on food services rising 6.2% year-over-year in Q3 2024[2]Source: U.S. Bureau of Economic Analysis, “Personal Consumption Expenditures, Q3 2024,” bea.gov. This growth is concentrated in households earning above USD 75,000 annually, where dining-out frequency increased from 3.2 to 3.8 occasions per week between 2024 and early 2025. Middle Eastern markets are witnessing parallel trends, as oil revenue stabilization in Gulf Cooperation Council nations lifts per-capita income and urbanization drives demand for Western and fusion dining concepts. The shift is structural rather than cyclical, as younger cohorts prioritize experiences over goods, allocating a greater portion of their discretionary budgets to dining compared to older generations. This demographic tilt favors full-service formats that offer ambiance and service differentiation over transactional quick-service alternatives.

Digital ordering and delivery platforms scaling off-premise demand

Third-party aggregators now facilitate 42% of all off-premise full-service restaurant orders in North America, with DoorDash commanding 67% market share and Uber Eats holding 23% as of Q4 2024. Commission rates averaging 28% to 32% compress operator margins, yet platforms are embedding subscription models such as DashPass and Uber One that drive order frequency among members, creating a volume-margin tradeoff that larger chains can absorb more readily than independents. Ghost kitchens are proliferating as a cost-mitigation strategy, with operators launching delivery-only brands from shared commissary spaces to bypass front-of-house labor and real estate expenses. This channel is projected to account for a significant share of full-service restaurant revenue by 2030, as platforms invest in proprietary logistics networks that reduce delivery times below 30 minutes in urban cores. The regulatory landscape remains fragmented, with the European Union proposing transparency mandates on algorithm-driven pricing and commission structures under the Digital Services Act, while US municipalities debate fee caps similar to San Francisco's 15% commission ceiling.

Post-pandemic rebound of on-premise social occasions

Dine-in traffic recovered to 97% of 2019 levels by mid-2024, yet the composition of visits has shifted toward celebratory and social occasions rather than routine weeknight meals, according to the National Restaurant Association. Consumers are consolidating dining-out frequency but increasing spend per visit, with average check sizes rising in full-service segments as parties opt for appetizers, desserts, and premium beverage pairings. This premiumization trend is most pronounced in leisure locations adjacent to entertainment venues, where pre-show and post-event dining generates 35% higher revenue per table turn than standalone locations. Operators are responding by redesigning floor plans to accommodate larger party sizes and investing in experiential elements such as open kitchens, tableside preparation, and chef's table formats. The shift suggests that full-service restaurants are evolving into destination venues rather than convenience options, a positioning that insulates them from quick-service competition but requires sustained investment in ambiance and service training.

Chain franchising expansion in emerging markets

International franchise agreements are accelerating in Latin America, Southeast Asia, and Africa, where rising middle-class populations and underdeveloped casual dining infrastructure create white-space opportunities. Yum! Brands reported opening 1,200 net new units across emerging markets in 2024, with full-service concepts such as The Habit Burger Grill entering Mexico and Brazil through master franchise partnerships. Franchising enables rapid geographic expansion without capital intensity, yet success hinges on menu localization and supply chain adaptation. In India, international chains are incorporating vegetarian and halal-certified options to align with dietary preferences, while in the Middle East, operators are extending operating hours to accommodate Ramadan dining patterns. Regulatory compliance varies widely, with Brazil requiring local majority ownership in franchise entities and China mandating joint ventures for foreign restaurant brands, adding complexity to expansion strategies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating food and labor costs | -0.9% | Global, most acute in North America and Europe | Short term (≤ 2 years) |

| Competitive pressure from QSR and fast-casual formats | -0.6% | Global, particularly North America and Europe | Medium term (2-4 years) |

| Tip-flation fatigue reduces visit frequency | -0.3% | North America, emerging in Europe | Short term (≤ 2 years) |

| Elimination of tip-credit and minimum-wage hikes in key states | -0.4% | North America, primarily the United States | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating food and labor costs

In Q4 2024, wholesale beef prices hit an average of USD 6.80 per pound, marking a 14% increase from 2023 levels. Concurrently, chicken breast prices saw a year-over-year uptick of 9%, reaching USD 3.20 per pound, as reported by the US Department of Agriculture. Produce prices are also on the rise, with tomatoes and lettuce seeing increases of 11% and 8% respectively, driven by drought conditions in California and Mexico. Labor costs are further fueling food inflation, highlighted by a 7.2% annual wage increase for restaurant workers in 2024[3]Source: U.S. Bureau of Labor Statistics, “Employment Situation in Leisure & Hospitality, 2024,” bls.gov. This surge outstrips the 4.1% average wage growth seen across all private-sector industries, per the US Bureau of Labor Statistics. In response, operators are employing menu engineering tactics, favoring higher-margin items and subtly reducing portion sizes, all without overt price hikes. This strategy not only maintains perceived value but also safeguards profit margins. Additionally, supply chain diversification is gaining traction as a strategic focus, with chains actively pursuing direct contracts with regional protein processors and produce distributors, aiming to sidestep the volatility of commodity markets.

Competitive pressure from QSR and fast-casual formats

Fast-casual concepts are capturing share from traditional full-service restaurants by offering elevated food quality and customization at lower price points, with no tipping expectations. Chains such as Chipotle and Panera Bread reported same-store sales growth of 8% to 11% in 2024, outpacing full-service peers by 400 to 600 basis points. The competitive threat is most acute among younger consumers aged 18 to 34, who prioritize speed and digital ordering convenience over table service. Full-service operators are countering by launching fast-casual offshoots and investing in curbside pickup and takeout infrastructure to compete on convenience. However, this channel shift dilutes the experiential differentiation that justifies full-service pricing, creating a strategic tension between defending market share and preserving brand positioning.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cuisine: Asian Dominance Meets Middle Eastern Acceleration

Asian cuisine held 49.05% of the full-service restaurant market share in 2025, reflecting decades of consumer acculturation to Chinese, Japanese, Thai, and Korean dining formats, yet Middle Eastern concepts are expanding at a 5.57% CAGR through 2031 as health-conscious consumers embrace Mediterranean diet principles. Fusion concepts blending Asian ingredients with Western techniques are proliferating in urban markets, with operators leveraging umami-rich profiles and plant-forward dishes to appeal to flexitarian diners. Middle Eastern cuisine is benefiting from celebrity chef endorsements and media coverage of longevity diets, positioning hummus, falafel, and grilled kebabs as nutrient-dense alternatives to traditional American fare. European cuisine maintains steady demand in mature markets, anchored by Italian and French bistro formats, while Latin American concepts are gaining traction in US Hispanic communities and coastal metropolitan areas. North American cuisine, encompassing steakhouse and barbecue formats, faces margin pressure from beef cost inflation yet retains loyalty among older demographics. Other FSR cuisines, including African and fusion categories, represent niche opportunities with limited scale but high differentiation potential.

Regulatory compliance frameworks such as FDA allergen labeling and Hazard Analysis Critical Control Points certification influence menu development across all cuisine types, with operators investing in traceability systems to document ingredient sourcing and preparation protocols. The proliferation of dietary restrictions such as gluten-free, dairy-free, and nut-free is driving menu complexity and kitchen labor requirements, a cost burden that larger chains can amortize across centralized research and development functions, while independents rely on chef expertise and supplier relationships. Asian cuisine's dominance is likely to persist through 2030, yet Middle Eastern formats offer the highest growth potential for operators willing to educate consumers and invest in authentic ingredient sourcing.

By Outlet: Chains Leverage Scale, Independents Defend Authenticity

In 2025, independent outlets held a commanding 65.31% share of the full-service restaurant market. However, chained formats are on track to expand at a 5.94% CAGR through 2031. This growth is fueled by technology investments and a negotiating prowess in real estate that independent outlets struggle to match. Chains are harnessing AI-driven customer data platforms to monitor ordering trends, allowing them to offer tailored promotions. This strategy has proven effective, boosting repeat visit rates compared to generic marketing. Meanwhile, independent operators leverage their menu adaptability and commitment to local ingredients, appealing to consumers who value authenticity and a sense of community. These attributes often command a price premium, especially in affluent neighborhoods. A 2024 survey by the James Beard Foundation revealed that 68% of diners favor chef-driven menus and locally sourced ingredients over brand recognition when choosing full-service restaurants.

Chained outlets enjoy the advantage of centralized supply chains, allowing them to cut food costs by 8% to 12% through bulk purchasing. However, this cost-saving efficiency often comes at the cost of menu uniqueness and regional customization. Representing about 70% of the 703,000 full-service establishments in the U.S., independent restaurants, as reported by the Independent Restaurant Coalition, rake in a substantial USD 280 billion annually. Yet, they often operate without the marketing heft and loyalty programs that chains routinely utilize. The competitive landscape is evolving. Third-party platforms are leveling the playing field, granting independents access to digital ordering and delivery systems. This newfound convenience doesn't come at the expense of their culinary uniqueness. Moreover, the rise of franchise models is blurring the distinctions between chains and independents. These hybrid formats provide the benefits of brand backing and purchasing leverage, all while affording operators the freedom of menu choices and localized marketing strategies.

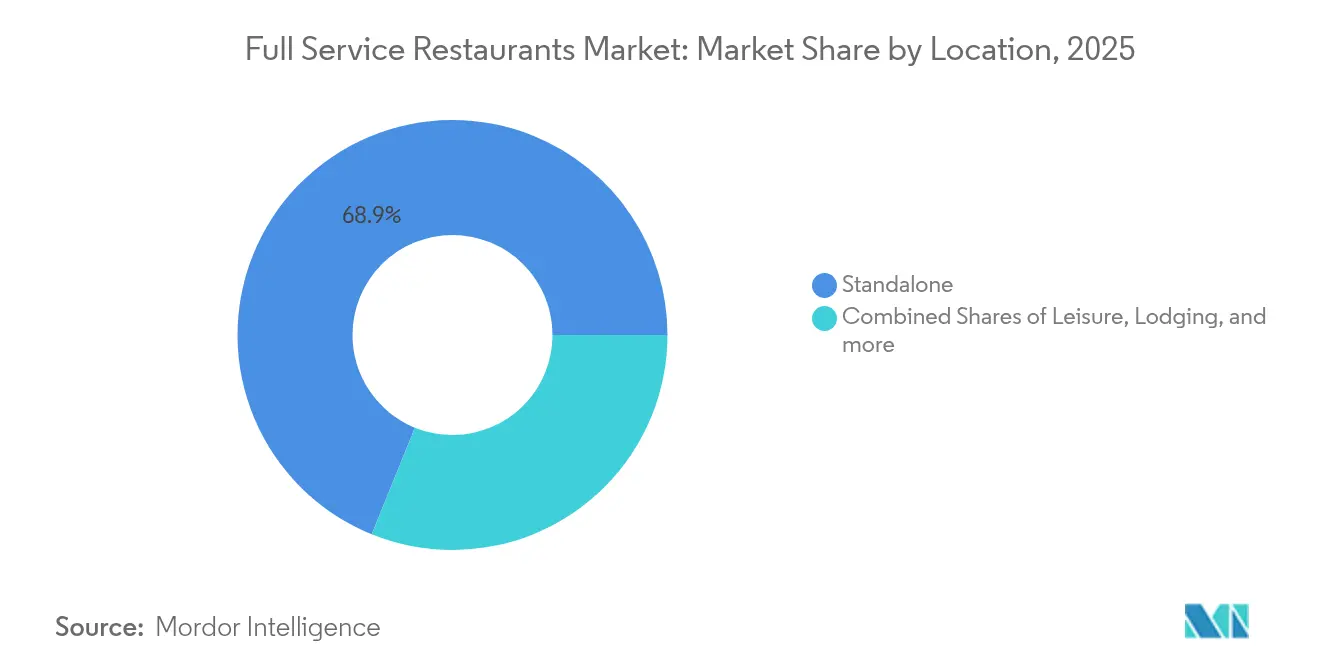

By Location: Standalone Dominance Faces Leisure Disruption

Experiential dining concepts in leisure locations are projected to grow at a 5.86% CAGR through 2031, challenging standalone restaurants' 68.87% market share in 2025. Consumers increasingly seek combined entertainment and dining experiences, with venues like Puttshack and Bowlero generating 35% higher revenue per square foot than traditional restaurants by integrating food service with activities like mini-golf, bowling, and arcade games. U.S. diners are willing to pay a premium for these experiences over conventional table service, justifying the higher real estate and build-out costs of leisure locations. Retail spots, including mall-based restaurants, are stabilizing after years of decline as landlords redevelop properties into mixed-use hubs with entertainment anchors and outdoor dining spaces.

Hotel restaurants are attracting business and leisure travelers through partnerships with online travel agencies and loyalty programs but hold a smaller market share due to limited local patronage. Travel-centric eateries, such as those at airports and highway rest stops, are growing modestly as passenger volumes recover to pre-pandemic levels but face challenges like shorter dwell times and limited menu customization. Standalone restaurants maintain dominance with lower occupancy costs and flexible site selection, enabling them to target high-traffic areas and residential neighborhoods. The shift toward leisure locations reflects a broader consumer preference for multi-sensory experiences that justify higher spending and longer visits, reshaping real estate strategies across the industry.

By Service Type: Delivery Surge Challenges Dine-In Dominance

Delivery service types are projected to grow at a 7.15% CAGR through 2031, the fastest among all service categories. However, dine-in services will hold a 65.83% market share in 2025, reflecting consumers' preference for social interaction and ambiance during celebrations. Urban markets are seeing increased order frequency as third-party platforms reduce delivery times to under 30 minutes using algorithmic routing and dedicated courier networks, a significant improvement from 45-minute windows. Ghost kitchens are expanding as delivery-only brands, with operators launching 3 to 5 virtual concepts from a single commissary kitchen to optimize assets and test menus without front-of-house costs. Subscription models like DashPass, charging USD 9.99 monthly for unlimited free delivery, are driving member order frequency to 4.2 times per month compared to 1.8 times for non-subscribers.

Takeaway services are growing moderately, appealing to consumers who avoid delivery fees and tipping but lacking time for dine-in. By Q4 2024, 78% of full-service chains offer curbside pickup and mobile order-ahead options, highlighting their importance. Dine-in services are focusing on unique experiences like tableside preparation, sommelier wine pairings, and chef interactions, which are hard to replicate at home. The divide between convenience-driven off-premise channels and experience-focused on-premise formats is creating distinct operational models. Some operators specialize in one service type, while others adopt omnichannel strategies. Delivery's rapid growth is reshaping kitchens, with operators adding separate prep lines for off-premise orders to avoid dine-in delays.

Geography Analysis

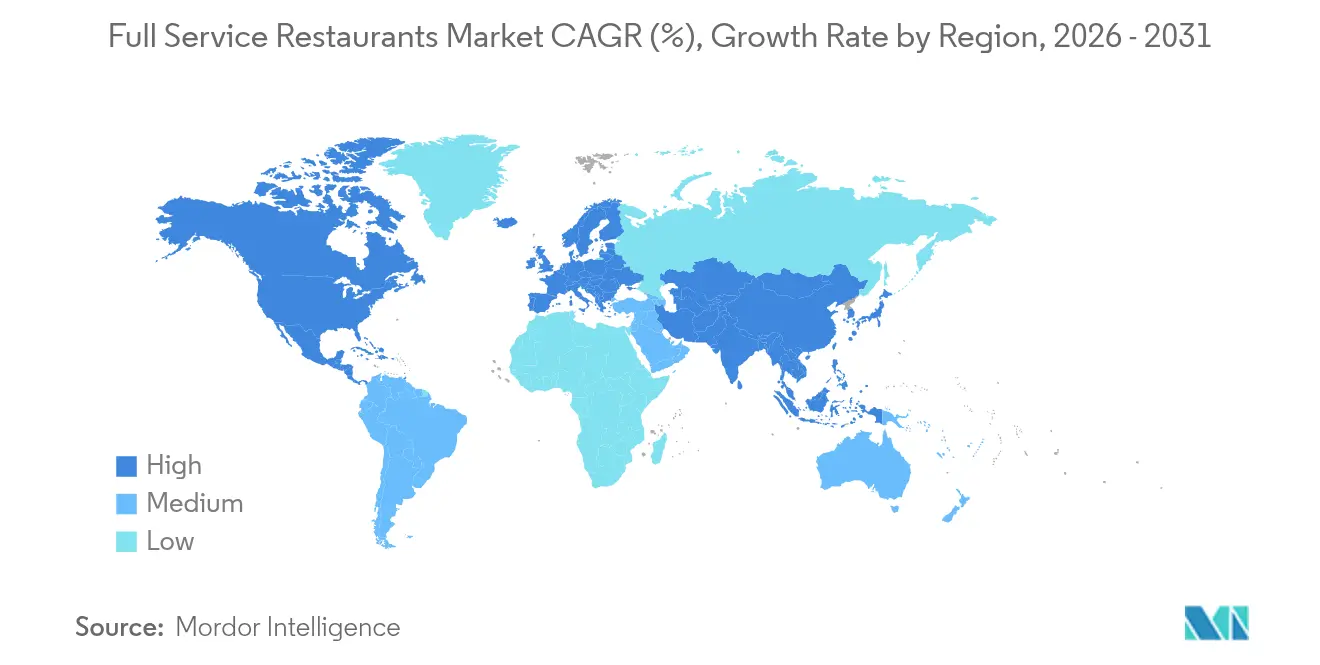

Asia-Pacific held 32.60% of the full-service restaurant market share in 2025, yet North America is projected to grow at a 6.55% CAGR through 2031, outpacing the region's expansion rate. North America's acceleration reflects post-pandemic recovery momentum, rising disposable incomes, and experiential dining premiums that offset labor cost inflation. The National Restaurant Association projects USD 1.5 trillion in total US foodservice sales for 2025, with full-service segments capturing 38% of that total. Canada and Mexico are contributing to regional growth through tourism recovery and expanding middle-class populations, with Mexico's restaurant industry benefiting from nearshoring trends that are lifting employment and wages in manufacturing hubs.

Europe is experiencing modest growth, constrained by economic uncertainty and elevated energy costs that compress operator margins. The United Kingdom's restaurant industry faces labor shortages following Brexit-related immigration restrictions, while Germany and France are navigating consumer preferences for sustainability and plant-based options that require menu reformulation and supplier diversification. South America is expanding steadily, led by Brazil's restaurant market and Argentina's post-inflation recovery, yet political instability and currency volatility create operational risks.

The Middle East and Africa represent the smallest regional share yet offer high growth potential, with Turkey, the United Arab Emirates, and South Africa attracting international chain investments and domestic entrepreneurship. The geographic divergence underscores that growth is concentrating in markets with stable regulatory environments, rising consumer purchasing power, and infrastructure that supports both on-premise and off-premise dining formats.

Competitive Landscape

The full-service restaurant industry remains fragmented, with most market share held by independent establishments and regional chains. This fragmentation intensifies margin pressures as operators compete on price, location, and experience differentiation rather than scale efficiencies. Technology adoption is becoming a key competitive advantage, as chains implement AI-driven personalization engines, dynamic pricing platforms, and kitchen automation systems to reduce labor costs. For instance, Brinker International's Chili's brand reported a 14.1% same-store sales growth in Q1 FY2025, attributing the success to mobile app enhancements and targeted digital promotions that increased visit frequency among loyalty program members. Growth opportunities are emerging in eatertainment formats, ghost kitchens, and health-focused concepts that cater to GLP-1-driven demand for portion-controlled, nutrient-dense menus.

Virtual restaurant brands launched by celebrity chefs and influencers are disrupting the market by leveraging existing kitchen infrastructure and third-party delivery platforms to reach consumers without requiring brick-and-mortar investments. These digital-native concepts are gaining traction in major metropolitan markets, with off-premise order share projected to double by 2028 as consumer awareness and platform discovery algorithms improve. Consolidation is also accelerating, with private equity firms acquiring regional chains to implement operational best practices and advanced technology platforms that independent operators often cannot afford. Regulatory compliance is emerging as a competitive advantage, as chains invest in food safety traceability systems and allergen management protocols that exceed FDA requirements, appealing to risk-averse consumers.

The competitive landscape is expected to bifurcate further, with technology-enabled chains and experiential independents capturing growth while mid-market concepts lacking differentiation face margin compression and market share erosion. Chains that prioritize innovation and operational efficiency are better positioned to thrive, while those unable to adapt to evolving consumer preferences and regulatory standards risk losing relevance. As the industry evolves, operators must balance the need for technological advancements with the delivery of unique dining experiences to remain competitive in a rapidly changing market.

Full Service Restaurants Industry Leaders

-

Darden Restaurants Inc.

-

Brinker International Inc.

-

Bloomin’ Brands Inc.

-

The Cheesecake Factory Inc.

-

Dine Brands Global Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Texas Roadhouse opened 28 new locations across the United States in 2024, expanding its footprint in secondary markets, where real estate costs are 40% to 50% lower than in primary metropolitan areas. The company reported Q3 2024 revenue of USD 1.27 billion, up 9.8% year-over-year, driven by same-store sales growth and new unit contributions.

- September 2024: The Cheesecake Factory internationally expanded into the Middle East through a master franchise agreement with M.H. Alshaya Co., targeting 15 locations across Saudi Arabia, Kuwait, and the United Arab Emirates by 2028. The company reported Q3 2024 revenue of USD 860 million and is leveraging franchise partnerships to enter high-growth markets without capital intensity.

- August 2024: Bloomin' Brands launched a USD 75 million remodeling initiative for its Outback Steakhouse locations, refreshing interiors and upgrading kitchen equipment to improve operational efficiency and guest experience. The investment is expected to lift same-store sales by 3% to 5% in remodeled locations through enhanced ambiance and faster table turns.

- July 2024: Darden Restaurants opened 50 new restaurants across its portfolio in fiscal year 2024, including Olive Garden, LongHorn Steakhouse, and Yard House locations, contributing to Q2 FY2025 sales of USD 2.9 billion. The company is prioritizing markets with favorable demographics and limited competitive intensity.

Global Full Service Restaurants Market Report Scope

Asian, European, Latin American, Middle Eastern, North American are covered as segments by Cuisine. Chained Outlets, Independent Outlets are covered as segments by Outlet. Leisure, Lodging, Retail, Standalone, Travel are covered as segments by Location.| Asian |

| European |

| Latin American |

| Middle Eastern |

| North American |

| Other FSR Cuisines |

| Chained Outlets |

| Independent Outlets |

| Leisure |

| Lodging |

| Retail |

| Standalone |

| Travel |

| Dine-In |

| Takeaway |

| Delivery |

| By Cuisine | Asian |

| European | |

| Latin American | |

| Middle Eastern | |

| North American | |

| Other FSR Cuisines | |

| By Outlet | Chained Outlets |

| Independent Outlets | |

| By Location | Leisure |

| Lodging | |

| Retail | |

| Standalone | |

| Travel | |

| By Service Type | Dine-In |

| Takeaway | |

| Delivery |

Market Definition

- FULL-SERVICE RESTAURANTS - A foodservice establishment where customers are seated at a table, give their order to a server and are served food at a table.

- QUICK SERVICE RESTAURANTS - A foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables.

- CAFES & BARS - A type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars.

- CLOUD KITCHEN - A foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers.

| Keyword | Definition |

|---|---|

| Albacore Tuna | It is one of the smallest species of tuna found in the six distinct stocks known globally in the Atlantic, Pacific, and Indian oceans, as well as the Mediterranean Sea. |

| Angus beef | It is beef derived from a specific breed of cattle indigenous to Scotland. It requires certification from the American Angus Association to receive the "Certified Angus Beef" quality mark. |

| Asian cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Chinese, Indian, Korean, Japanese, Bengali, Southeast Asian, etc. |

| Average Order Value | It is the average value of all orders made by the customers at a foodservice establishment. |

| Bacon | It is salted or smoked meat that comes from the back or sides of a pig. |

| Bars & Pubs | It is a drinking establishment that is licensed to serve alcoholic drinks for consumption on the premises. |

| Black Angus | It is beef derived from a black-hided breed of cows that don't have horns. |

| BRC | British Retail Consortium |

| Burger | It is a sandwich consisting of one or more cooked beef patties, placed inside a sliced bread roll or bun roll. |

| Café | It is a foodservice establishment serving various refreshments (mainly coffee) and light meals. |

| Cafes & Bars | It is a type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars. |

| Cappuccino | It is an Italian coffee drink that is traditionally prepared with equal parts double espresso, steamed milk, and steamed milk foam. |

| CFIA | Canadian Food Inspection Agency |

| Chained Outlet | It refers to a foodservice establishment that shares brands, operates in several locations, has central management, and standardized business practices. |

| Chicken Tender | It refers to chicken meat prepared from the pectoralis minor muscles of a chicken bird. |

| Cloud Kitchen | It is a foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers. |

| Cocktail | It is an alcoholic mixed drink made with either a single spirit or a combination of spirits, mixed with other ingredients such as juices, flavored syrups, tonic water, shrubs, and bitters. |

| Edamame | It is a Japanese dish prepared with soybeans (harvested before they ripen or harden) and cooked in its pod. |

| EFSA | European Food Safety Authority |

| ERS | Economic Research Service of the USDA |

| Espresso | It is a concentrated form of coffee, served in shots. |

| European cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Italian, French, German, English, Dutch, Danish, etc. |

| FDA | Food and Drug Administration |

| Fillet Mignon | It is a cut of meat taken from the smaller end of the tenderloin. |

| Flank Steak | It is a cut of beef steak taken from the flank, which lies forward of the rear quarter of a cow. |

| Foodservice | It refers to the part of the food industry which includes businesses, institutions, and companies which prepare meals outside the home. It includes restaurants, school and hospital cafeterias, catering operations, and many other formats. |

| Franks | Also known as frankfurter or Würstchen, it is a type of highly seasoned smoked sausage popular in Austria and Germany. |

| FSANZ | Food Standards Australia New Zealand |

| FSIS | Food Safety and Inspection Service |

| FSSAI | Food Safety and Standards Authority of India |

| Full service restaurant | It refers to a foodservice establishment where customers are seated at a table, give their order to a server, and are served food at a table. |

| Ghost Kitchen | It refers to a cloud kitchen. |

| GLA | Gross Leasable Area |

| Gluten | It is a family of proteins found in grains, including wheat, rye, spelt, and barley. |

| Grain-fed beef | It is beef derived from cattle that have been fed a diet supplemented with soy and corn and other additives. Grain-fed cows can also be given antibiotics and growth hormones to fatten them up more quickly. |

| Grass-fed beef | It is beef derived from cattle that have only been fed grass as feed. |

| Ham | It refers to the pork meat taken from the leg of a pig. |

| HoReCa | Hotels, Restaurants and Cafes |

| Independent Outlet | It refers to a foodservice establishment that operates with a single outlet or is structured as a small chain with no more than three locations. |

| Juice | It is a drink made from the extraction or pressing of the natural liquid contained in fruit and vegetables. |

| Latin American | It includes full-service offerings in restaurants that serve cuisines from cultures such as Mexican, Brazilian, Argentinian, Colombian, etc. |

| Latte | It is a milk-based coffee that is made up of one or two shots of espresso, steamed milk, and a thin layer of frothed milk. |

| Leisure | It refers to foodservice offered as a part of a recreation business, such as sports arenas, zoos, movie theaters, and museums. |

| Lodging | It refers to foodservice offerings at hotels, motels, guesthouses, holiday homes, etc. |

| Macchiato | It is an espresso coffee drink with a small amount of milk, usually foamed. |

| Meat-based cuisines | This inlcudes food items like fried chicken, steak, ribs, etc. where meat is the primary ingredient for the dish. |

| Middle Eastern cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Arabic, Lebanese, Iranian, Israeli, etc. |

| Mocktail | It is an non-alcoholic mixed drink. |

| Mortadella | It is a large Italian sausage or luncheon meat made of finely hashed or ground heat-cured pork, which incorporates at least 15% small cubes of pork fat. |

| North American | It includes full-service offerings in restaurants that serve cuisines from cultures such as American, Canadian, Caribbean, etc. |

| Pastrami | It refers to a highly seasoned smoked beef, typically served in thin slices. |

| PDO | Protected Designation of Origin: It is the name of a geographical region or specific area that is recognized by official rules to produce certain foods with special characteristics related to location. |

| Pepperoni | It is an American variety of spicy salami made from cured meat. |

| Pizza | It is a dish made typically of flattened bread dough spread with a savory mixture usually including tomatoes and cheese and often other toppings and baked. |

| Primal cuts | It refers to the major sections of the carcass. |

| Quick service restaurant | It refers to a foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables. |

| Retail | It refers to a foodservice outlet inside a mall. shopping complex or a commercial real estate building, where there are other businesses operating as well. |

| Salami | It is a cured sausage consisting of fermented and air-dried meat. |

| Saturated fat | It is a type of fat in which the fatty acid chains have all single bonds. It is generally considered unhealthy. |

| Sausage | It is a meat product made of finely chopped and seasoned meat, which may be fresh, smoked, or pickled and which is then usually stuffed into a casing. |

| Scallop | It is an edible shellfish that is a mollusk with a ribbed shell in two parts. |

| Seitan | It is a plant-based meat substitute made out of wheat gluten. |

| Self-service kiosk | It refers to a self-order point-of-sale (POS) system through which customers place and pay for their own orders at kiosks, enabling totally contactless and frictionless service. |

| Smoothie | It is a beverage made by placing all the ingredients in a container and processing them together, without removing the pulp. |

| Specialty coffee & tea shops | It refers to a foodservice establishment that serves only various types of tea or coffee. |

| Standalone | It refers to a restaurants that have an independent infrastructure setup and not connected to any other business. |

| Sushi | It is a Japanese dish of prepared vinegared rice, usually with some sugar and salt, accompanied by a variety of ingredients, such as seafood—often raw—and vegetables. |

| Travel | It refers to foodservice offerings such as airplane food, dining on long-distance trains, and foodservice on cruise ships. |

| Virtual Kitchen | It refers to a cloud kitchen. |

| Wagyu Beef | It is beef derived from any of four strains of a breed of black or red Japanese cattle that are valued for their highly marbled meat. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for the market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market size estimations for the forecast years are in nominal terms. Inflation is considered for average order value, and it is forecasted as per predicted inflation rates in the countries.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms