Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

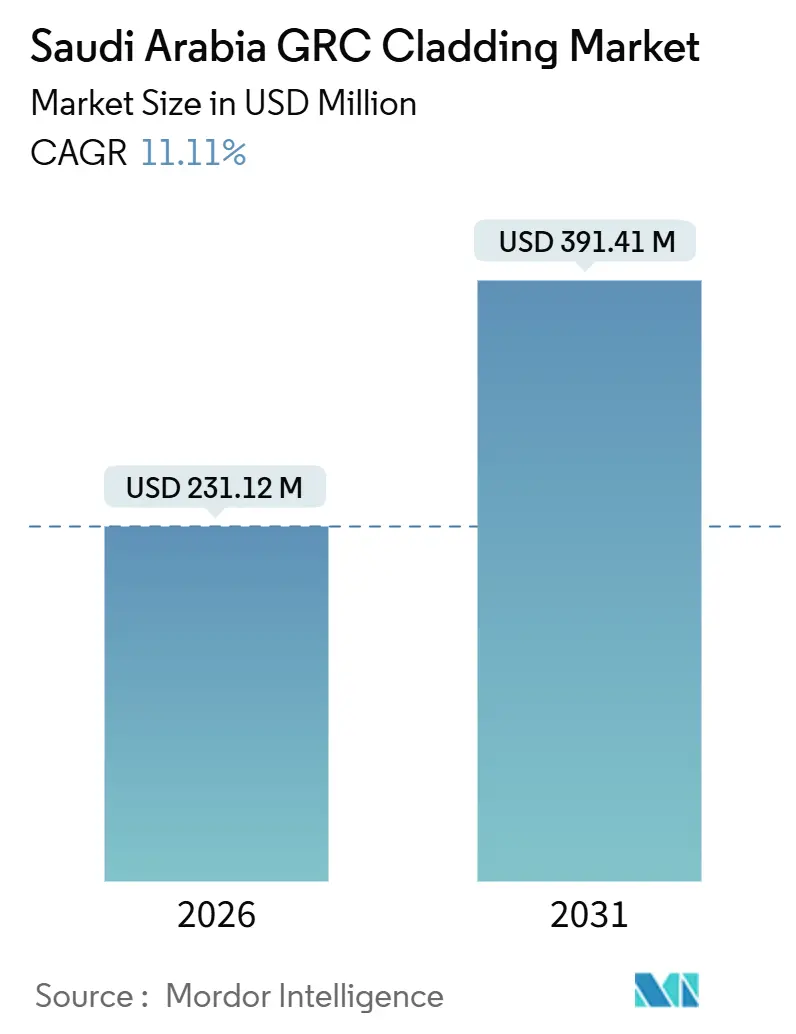

| Market Size (2026) | USD 231.12 Million |

| Market Size (2031) | USD 391.41 Million |

| Growth Rate (2026 - 2031) | 11.11% CAGR |

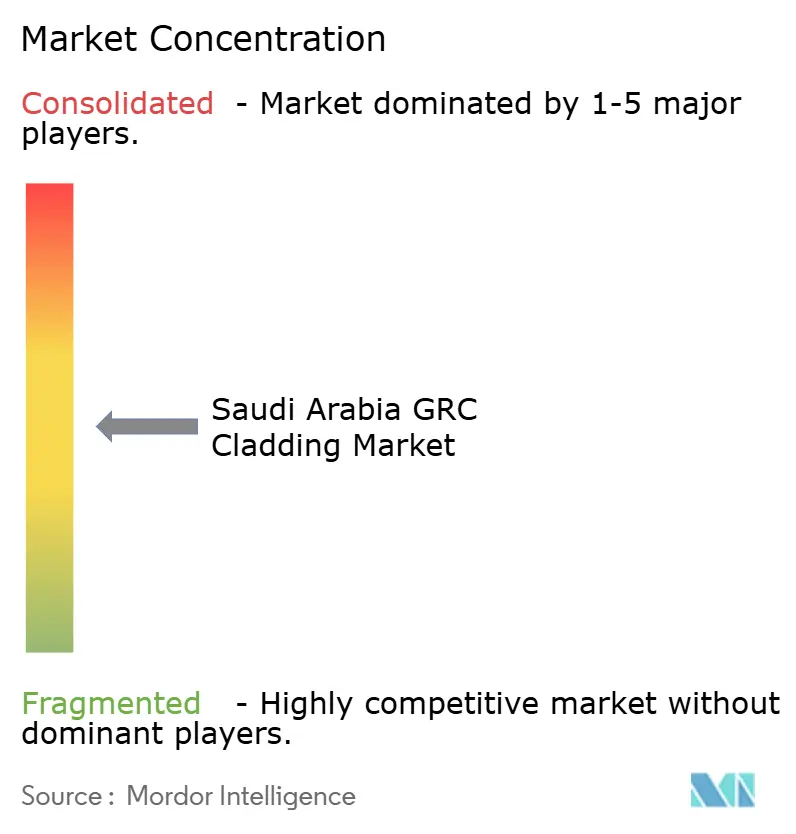

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia GRC Cladding Market Analysis by Mordor Intelligence

The Saudi Arabia GRC Cladding Market size is estimated at USD 231.12 million in 2026, and is expected to reach USD 391.41 million by 2031, at a CAGR of 11.11% during the forecast period (2026-2031). This acceleration reflects Vision 2030’s pivot from oil-centric spending toward mixed-use giga-projects, stricter façade fire-safety rules, and a nationwide push for passive-cooling retrofits in cities that routinely record summer temperatures above 45 °C[1]Vision 2030 Program, “Saudi Vision 2030,” Kingdom of Saudi Arabia, vision2030.gov.sa . Rainscreen systems benefit first from energy-efficiency mandates, while curtain walls gain traction in NEOM’s skyline-defining towers. Retrofit demand is also climbing as government landlords overlay new façades on pre-2010 structures to cut HVAC loads, and contractors with Saudi Building Code certifications win bids more readily. Despite rising import prices for alkali-resistant (AR) glass fiber, domestic capacity investments and 3D-printed moulding lines lower production costs, bolstering the Saudi Arabia GRC Cladding market expansion.

Key Report Takeaways

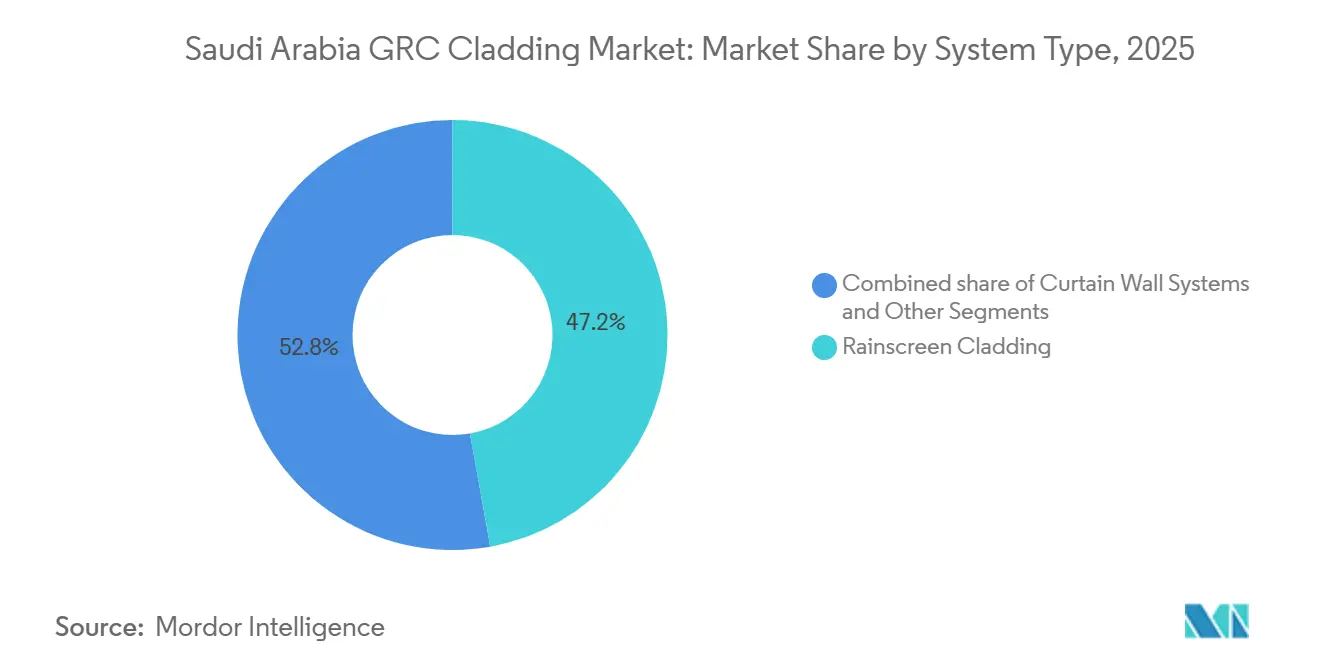

- By system type, rainscreen cladding led with 47.2% of revenue in 2025, while curtain wall assemblies are projected to expand at an 11.97% CAGR through 2031.

- By application, commercial projects accounted for 56.8% of revenue in 2025, whereas residential projects are set to grow at a 12.09% CAGR to 2031.

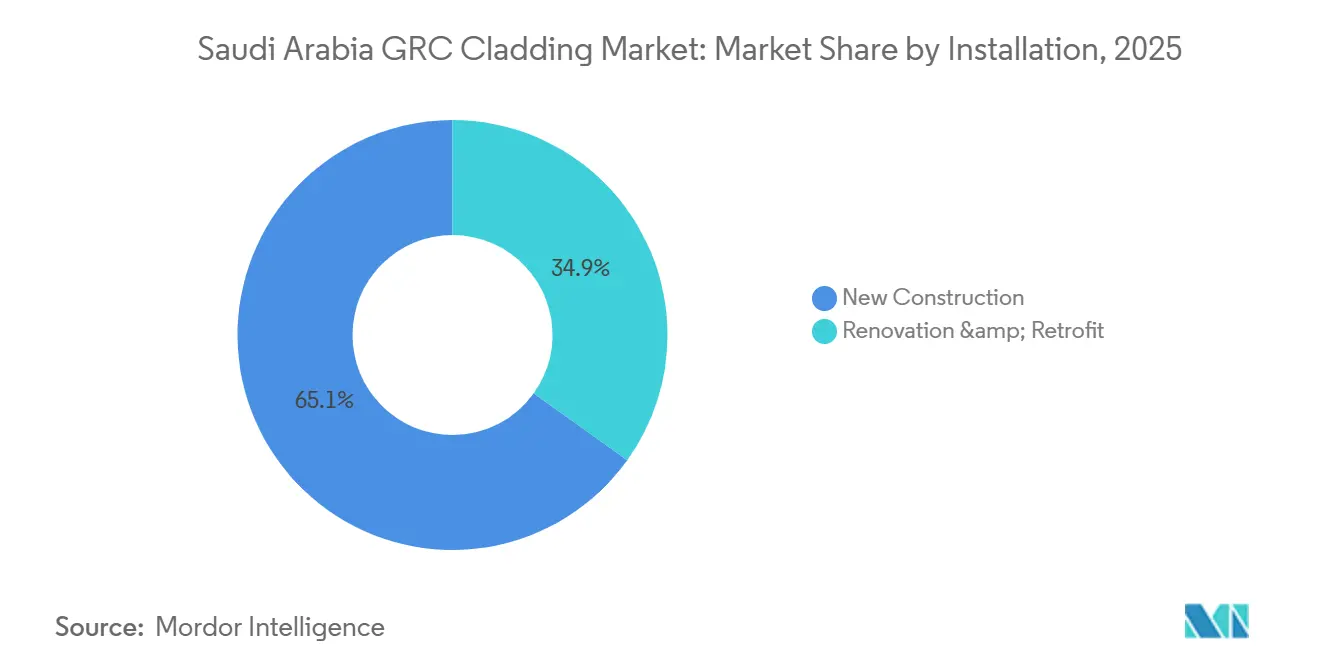

- By installation, new construction captured 65.1% of revenue in 2025, and renovation and retrofit activity is advancing at a 12.31% CAGR through 2031.

- By city, Riyadh commanded 44.8% demand in 2025, while the Dammam Metropolitan Area is forecast to expand at a 12.59% CAGR by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Saudi Arabia GRC Cladding Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 giga-projects needing iconic façades | +3.2% | Kingdom-wide, with clusters in NEOM, Qiddiya, Red Sea, Diriyah | Long term (≥ 4 years) |

| Harsh-climate performance requirements | +2.1% | Coastal Red Sea and interior deserts | Medium term (2–4 years) |

| Faster delivery via prefabricated, unitized panels | +2.0% | National mega-projects on tight schedules | Short term (≤ 2 years) |

| Design flexibility for Arabic and parametric geometries | +1.6% | Riyadh, Jeddah, NEOM | Medium term (2–4 years) |

| Durability and ESG focus over aluminum composite or plaster | +1.3% | Nationwide public and private portfolios | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Vision 2030 Giga-Projects Needing Iconic Façades at Scale

Massive mixed-use programs such as NEOM’s The Line, Qiddiya, Diriyah, and the Red Sea Project are bankrolling long pipeline visibility for the Saudi Arabia GRC Cladding market. These developments allocate 12%–18% of total construction budgets to façades, favoring lightweight panels that reduce crane hours and meet strict fire-rating codes. Approved local suppliers like Qanbar Dywidag leverage 6 million m² of annual capacity to ship panels inside eight-week windows, an advantage amplified by automated finishing lines that support integral colors and acid-etched textures. Stringent timelines and cultural-identity briefs ensure sustained double-digit growth in premium cladding packages.

Harsh-Climate Performance Requirements

Coastal sites battle salt-fog corrosion while inland deserts endure 50 °C peaks and sharp nighttime drops. GRC’s alkali-resistant glass fibers retain tensile strength after 5,000 hours of accelerated weathering, outlasting aluminum composite materials susceptible to delamination[2]Gulf Standardization Organization, “ASTM C1666 Adoption,” gso.org.sa. BFG Advanced Concrete Facades runs in-house salt-spray and UV-aging chambers to back twenty-year warranties, a proof point valued by Red Sea resort developers. SBC 801 mirrors the International Fire Code and mandates non-combustible façades on high-rise cores, pushing GRC further into the specification baseline for airports, petrochemical control rooms, and five-star hotels.

Design Flexibility for Arabic and Parametric Geometries

Thin-shell panels, typically 15–25 mm thick, allow deep reveals, mashrabiya patterns, and calligraphic relief at a fraction of stone’s weight. Diriyah’s Najdi-themed streetscapes rely on moldable GRC skins matched with mineral-wool cores to satisfy insulation targets. Roshn’s Sedra community showcases 12 façade typologies across 30,000 homes without escalating tooling fees, thanks to reusable molds and 3D-printed formworks. Iconic motifs embedded at the casting stage eliminate post-installation carving, trimming on-site labor by 40% compared with carved-stone alternatives.

Faster Delivery via Prefabricated, Unitized Panels

Factory-finished units cut installation cycles from twelve weeks to six and slash crane time by 60% when shipped as 3 × 4 m curtain-wall modules integrating glazing, mullions, and GRC spandrels. Qanbar Dywidag maintains 90-day finished-goods buffers, allowing just-in-time dispatch to The Line’s 170-km corridor. Technical and Vocational Training Corporation curricula cover panel handling, but field-competency gaps persist, making turnkey offsite fabrication a competitive edge through 2028[3]Technical and Vocational Training Corporation, “Graduate Statistics 2025,” tvtc.gov.sa.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher upfront cost and structural support needs | -0.8% | Price-sensitive housing and industrial sheds | Short term (≤ 2 years) |

| Skilled fabrication and installation shortages | -0.6% | Jeddah, Dammam, secondary cities | Medium term (2–4 years) |

| Logistics and large-panel handling in extreme heat | -0.4% | Long desert corridors to NEOM and Riyadh | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Higher Upfront Cost and Structural Support Needs

GRC panels weigh 40–70 kg/m², roughly triple the load of expanded-insulation finishes. That mass calls for thicker anchor plates and backup walls, inflating first costs by 20%–35%. Price-sensitive logistics parks in Dammam often default to metal sheets unless fire codes override budget limits. Until automated sprayers and fiber-dispersion controls trim labor content by 30%, the premium will confine GRC to projects where aesthetics, durability, or Class A fire resistance are non-negotiable.

Skilled Fabrication and Installation Shortages

Spray-up techniques, fiber dosing, and 28-day curing protocols restrict qualified labor to a small cohort concentrated in Riyadh. Smaller plants in Jeddah and Dammam poach certified technicians at 15%–25% wage uplifts, squeezing margins for retrofit jobs. Qanbar Dywidag trains 50 apprentices annually, but market demand outstrips supply by 30%, creating occasional schedule slippage on airport and petrochemical contracts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By System Type: Rainscreen Leadership with Curtain-Wall Upswing

Rainscreen assemblies captured 47.2% of 2025 revenue, confirming dominance in the Saudi Arabia GRC Cladding market share for their passive-cooling benefits and 30%–40% faster installation compared with render finishes. Qanbar Dywidag’s factory network delivers rainscreen panels to Riyadh and DMA job sites within eight weeks, cutting site manpower by 40%. The system also aligns with the Saudi Green Building Code target of 30% energy reduction, driving retrofit volume. Meanwhile, curtain walls are on track for an 11.97% CAGR to 2031, fueled by NEOM’s mirrored towers that blend floor-to-ceiling glass with GRC spandrels.

The wage premium for skilled curtain-wall installers currently sits 8% above rainscreen work, but automation and enhanced training will close this gap before 2029. Hybrid systems pairing GRC skins with foam cores find niche demand in industrial warehouses needing 180-minute fire ratings. Station Group’s lightweight hybrid panels supply King Salman Energy Park projects and weigh 40% less than solid alternatives. Over the forecast window, rainscreen stays volume leader, while curtain-wall value share rises in prestige towers, jointly sustaining the Saudi Arabia GRC Cladding market momentum.

By Application: Commercial Stronghold and Residential Surge

Commercial buildings held 56.8% revenue in 2025 as office towers, malls, and hotels in Riyadh and Jeddah mandated Class A façades under SBC 801. High-rise developers accept thicker 25-40 mm panels with acid-etched finishes that command price premiums. In contrast, residential cladding is advancing at a 12.09% CAGR to 2031, buoyed by Roshn’s goal to supply 400,000 homes and the National Housing Company’s 20,000-unit deal with CMEC in 2024. Villas and mid-rise apartments integrate 15-25 mm panels to hit cost targets yet still meet fire codes.

Commercial demand now shifts toward retrofit spending aimed at energy efficiency, which opens cross-selling prospects for rainscreen specialists. Residential developers employ 3D-printed moulds to accelerate bespoke façades, echoing Dar Al-Arkan’s modular homes that achieved 30% faster build cycles. As the population increases 2.4% annually, the Saudi Arabia GRC Cladding market sees residential volume outpace commercial, although premium commercial jobs preserve higher margins.

By Installation: New-Build Dominance and Retrofit Acceleration

New construction generated 65.1% of installation revenue in 2025, reflecting mega-project preference for greenfield sites that bypass integration issues with legacy structures. Retrofit activity grows at a 12.31% CAGR as landlords overlay ventilated façades to satisfy energy mandates. Engineering checks add 60–90 days to retrofit schedules, inflating consulting fees 12%–18%. Yet Station Group’s turnkey design-build model cuts overall timeline and secures repeat clients in Riyadh.

Retrofit scope widens as insurance premiums rise for non-compliant façades after SBC 801 enforcement. BFG incurred 8% margin compression by relocating crews, highlighting installer scarcity outside the capital. Over time, renovations will claim a larger share of Saudi Arabia GRC Cladding market size, but new-build giga-projects keep construction volumes high, ensuring balanced growth across segments.

Geography Analysis

Riyadh retained a 44.8% Saudi Arabia GRC Cladding market share in 2025, supported by active public spending on Diriyah, King Salman Park, and ongoing financial district towers that specify ASTM E84 Class A façades. Retrofit work has intensified because pre-2010 towers seek rainscreen overlays to achieve a mandated 30% energy reduction, a service niche captured by Station Group’s consulting arm. The city also benefits from the largest certified installer pool, cutting project lead times and reinforcing its production hub status.

The Dammam Metropolitan Area will grow at a 12.59% CAGR through 2031 as Aramco invests USD 500 billion in upstream, midstream, and petrochemical facilities that demand high-specification cladding. Qanbar Dywidag’s Jubail plant feeds this industrial belt with anchor-channel panels that cut site labor 30%, giving the supplier a logistical edge. Nevertheless, limited local installer certification drives cost premiums that some developers absorb to meet start-up timelines.

Jeddah balances heritage and modernity. Its UNESCO zone restricts modern façades, but citywide airport and waterfront schemes offset slower heritage approvals. NEOM in Tabuk, the Red Sea resorts, and Al-Ula cultural assets contribute to a growing Rest-of-Saudi segment, each specifying rainscreen or curtain-wall systems tailored to desert climates. The geographic spread of mega-projects ensures the Saudi Arabia GRC Cladding market gains resilience across distinct city profiles.

Competitive Landscape

Competition is moderately fragmented, with the top five players collectively controlling a substantial share of installed capacity. Local champion Qanbar Dywidag supplies more than 6 million m² annually through plants in Jubail, Rabigh, and Qatar, leveraging Aramco, SABIC, and NEOM approvals to secure long-term contracts. Station Group commands the retrofit niche by bundling waterproofing and rainscreen consulting, creating recurring revenue streams. International firms such as BFG Advanced Concrete Facades and Fibrobeton differentiate with PCI and GRCA certificates that appeal to global architects, yet face price pressure from lower-cost Chinese and Indian fiber inputs.

Strategic moves focus on vertical integration and technology. Station Group installed robotic finishing units in 2025 to apply nano coatings that add 10% price premiums, while BFG cut certification time by adopting on-site fire-testing rigs that shorten schedules by five weeks. Local players seek cost certainty by signing multi-year AR-glass fiber deals with Asian suppliers to hedge volatility. Mid-tier entrants embrace 3D-printed moulding, proven in Roshn’s villa, to win bespoke façades without European design mark-ups.

Future rivalry will intensify around retrofit contracts in Riyadh and Jeddah where strict energy codes drive compulsory upgrades. Companies partnering with regional training centers can offset the installer shortage and unlock secondary-city growth. As fire-safety audits tighten and durability testing localizes, certified capacity will consolidate, providing opportunity for well-capitalized firms to raise Saudi Arabia GRC Cladding market share while smaller fabricators form joint ventures or exit.

Saudi Arabia GRC Cladding Industry Leaders

Petra GRC

Qanbar Dywidag Precast Co.

Station Group

BFG Advanced Concrete Facades

Classic GRC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: ACWA Power closed USD 8.2 billion in renewable projects, adding cladding demand for control buildings.

- December 2024: NEOM opened Sindalah Island, the first destination to feature glass and GRC façades, signaling rapid project momentum.

- October 2024: NEOM awarded USD 186.7 million to Asas Al-Mohileb for a concrete factory in Oxagon to supply GRC panels.

- September 2024: Saudi Aramco and CNBM agreed to co-develop lower-carbon AR-glass fibers, aiming to localize supply.

Saudi Arabia GRC Cladding Market Report Scope

GRC cladding, also known as glass fiber reinforced concrete, is a highly versatile cladding product made up of numerous different ingredients and elements, including fiberglass. By molding GRC concrete into thin, lightweight panels, it can be shaped and altered into a variety of different and extensive structures. This makes it one of the ideal options for alternative prefabricated cladding.

Saudi Arabia's GRC cladding market is segmented by process(spray, premix, and hybrid) and by application(commercial construction, residential construction, and civil and other infrastructure construction). The report offers market size and forecasts for the Saudi Arabia's GRC cladding market in value (USD) for all the above segments.

By System Type

| Rainscreen Cladding |

| Curtain Wall Systems |

| Others |

By Application

| Residential |

| Commercial |

| Others |

By Installation

| New Construction |

| Renovation & Retrofit |

By City

| Riyadh |

| Jeddah |

| DMA (Dammam Metropolitan Area) |

| Rest of Saudi Arabia |

| By System Type | Rainscreen Cladding |

| Curtain Wall Systems | |

| Others | |

| By Application | Residential |

| Commercial | |

| Others | |

| By Installation | New Construction |

| Renovation & Retrofit | |

| By City | Riyadh |

| Jeddah | |

| DMA (Dammam Metropolitan Area) | |

| Rest of Saudi Arabia |

Key Questions Answered in the Report

How large is the Saudi Arabia GRC Cladding market in 2026?

It is valued at USD 231.12 million in 2026 and is set to reach USD 391.41 million by 2031 at an 11.11% CAGR.

Which system type holds the largest share of cladding demand?

Rainscreen systems lead with a 47.2% share in 2025 due to passive-cooling and quick installation advantages.

What drives the fastest growth within system types?

Curtain walls are projected to grow at an 11.97% CAGR as NEOM and other towers favor full glass façades with GRC spandrels.

Why are retrofit projects gaining traction in Saudi Arabia?

Energy-efficiency mandates under the Green Building Code require older buildings to lower HVAC loads, making rainscreen retrofits attractive.

Which city is the fastest-growing market for GRC cladding?

The Dammam Metropolitan Area is forecast to grow at a 12.59% CAGR through 2031, driven by large petrochemical investments by Aramco.

How is technology changing Saudi GRC fabrication?

3D-printed moulding cuts tooling costs by 60% and shortens lead times to ten days, enabling bespoke façades at competitive prices.

Page last updated on: