Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

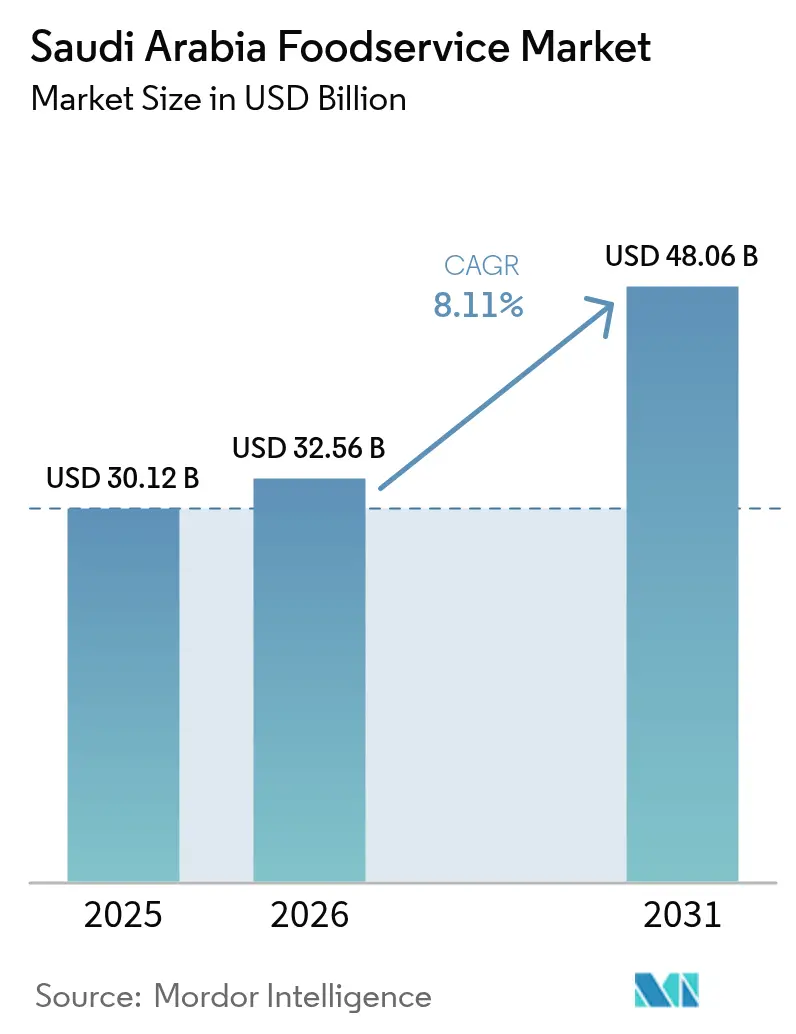

| Base Year Market Size (2025) | USD 30.12 Billion |

| Market Size (2026) | USD 32.56 Billion |

| Market Size (2031) | USD 48.06 Billion |

| Growth Rate (2026 - 2031) | 8.11% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Saudi Arabia Foodservice Market Analysis by Mordor Intelligence

The Saudi Arabia foodservice market size is expected to grow from USD 30.12 billion in 2025 to USD 32.56 billion in 2026 and is forecast to reach USD 48.06 billion by 2031 at 8.11% CAGR over 2026-2031. This growth aligns with Vision 2030, which highlights hospitality and dining as key drivers of economic diversification. Social media and food festivals are playing a significant role in shaping consumer preferences. Major urban projects like NEOM, Qiddiya, and the Red Sea destination are incorporating restaurants, cafés, and delivery-only kitchens into their designs. As lifestyles evolve toward convenience, there is a growing demand for takeaways and on-demand meals. Rising disposable incomes, a tech-savvy youth population, and gradually liberalizing social norms are expanding the market for out-of-home dining. Experiential dining and themed food concepts are gaining popularity among consumers. Supportive foodservice regulations and stringent food safety standards are fostering market growth. Substantial private and public investments in cold-chain logistics, last-mile delivery systems, and smart payment infrastructure are reducing operational challenges and enabling faster expansion into secondary cities. Simultaneously, government mandates promoting local sourcing and higher Saudi employment ratios are driving operators to restructure supply chains. While this introduces complexity, it also encourages vertically integrated ventures that capture more value within the Kingdom.

Key Report Takeaways

- By foodservice type, full-service restaurants held 53.62% of the Saudi Arabia foodservice market share in 2025, while Café and Bars posted the fastest growth at a 11.82% CAGR that is expected to continue through 2031.

- By outlet type, chained outlets expanded at an 11.18% CAGR and are on track to narrow the gap with independent operators, which retained 57.86% of the Saudi Arabia foodservice market in 2025.

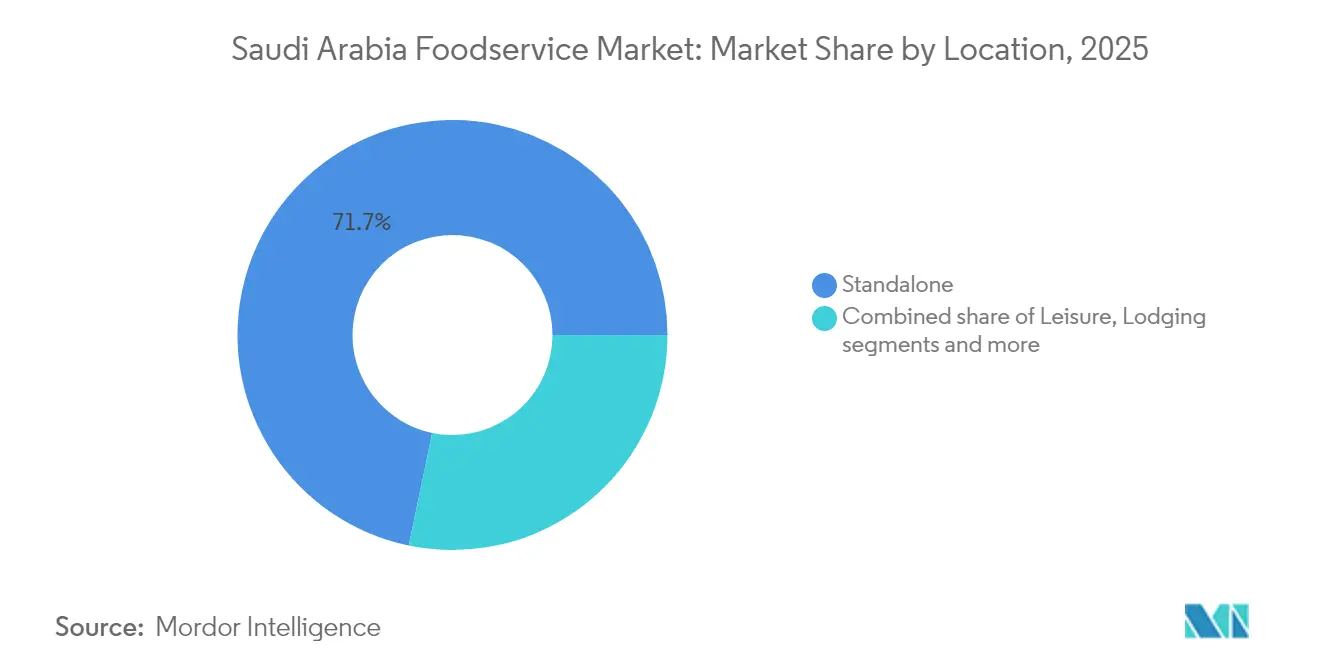

- Standalone locations accounted for 71.74% of the Saudi Arabia foodservice market size in 2025, whereas leisure venues returned the highest segment growth at an 10.93% CAGR.

- Dine-in dominated with a 75.66% share, but delivery services advanced at an 11.14% CAGR on the back of cloud kitchen proliferation and nationwide 5G rollout.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Foodservice Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion and modernization of urban infrastructure | +1.8% | National, early gains in Riyadh, NEOM, Red Sea | Long term (≥ 4 years) |

| Increasing influence of food-related social media and food festivals | +1.6% | Urban centers, especially Riyadh and Jeddah | Medium term (2-4 years) |

| Rise of cloud kitchens and virtual-only brands | +1.4% | Major cities with dense delivery networks | Short term (≤ 2 years) |

| Increasing consumer preference for convenience and ready-to-eat food | +1.2% | Nationwide with urban concentration | Medium term (2-4 years) |

| Strong coffee and café culture | +0.8% | Kingdom-wide, commercial districts | Medium term (2-4 years) |

| Expansion of quick-service and fast-casual chains | +0.6% | National, franchise-friendly sites | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expansion and modernization of urban infrastructure

Saudi Arabia's foodservice sector is experiencing significant growth, fueled by large-scale infrastructure projects such as NEOM and the Red Sea Project. These developments go beyond construction, creating self-sustaining communities where foodservice is a critical component. Saudi Arabia's Vision 2030 is a key driver behind this rapid expansion. A standout example is the Jeddah Food Cluster, which opened in November 2024. Covering 11 million square meters and backed by a SAR 20 billion investment[1]Source: Saudi Press Agency, "Saudi Arabia Sets World Record with Largest Food Cluster" spa.gov.sa, it is now the largest food park globally. Urban projects in Riyadh are increasing restaurant density, while new commercial districts focus on mixed-use designs to improve foodservice accessibility. The construction of modern malls, metro-connected food courts, and recreational hubs is creating new commercial zones, offering significant opportunities for quick-service restaurant (QSR) operators. Brands specializing in fast-casual and convenient dining formats are particularly benefiting. In 2024, the Public Investment Fund, through its Tourism Investment Enabler Program, invested SAR 42 billion in hospitality infrastructure[2]Source: Ministry of Tourism, "Invest in Saudi Arabia's Tourism Sector", cdn.mt.gov.sa, ensuring continued demand for QSRs in high-traffic areas. Upgrades to the transportation network, including the Riyadh Metro and expanded highways, are reducing delivery times and increasing the serviceable market areas for QSRs. Additionally, regulatory frameworks from the Saudi Food and Drug Authority ensure that these infrastructure investments adhere to food safety standards, supporting the market's long-term stability.

Increasing influence of food-related social media and food festivals

In Saudi Arabia, social media is significantly transforming food culture, going beyond traditional marketing approaches to fundamentally influence consumption patterns. Younger demographics are at the forefront of this shift, driving demand for experiential dining that values visual appeal and shareability on social platforms as much as the quality of taste. The growing prominence of food influencers and the role of Instagram in restaurant discovery have amplified the importance of aesthetically pleasing dishes and unique dining environments. Consequently, restaurant operators are increasingly investing in striking interior designs and innovative menus that are optimized for digital engagement and appeal. Additionally, food festivals and cultural events have become essential marketing channels, playing a critical role in promoting culinary experiences. The Saudi government’s support for culinary tourism, as part of its Vision 2030 initiative, highlights the integration of food culture into the broader strategy for economic development. This social media-driven influence has created rapid shifts in consumer demand, favoring agile operators who can quickly innovate their menus and adapt their concepts to align with evolving trends. On the other hand, traditional establishments face challenges in maintaining relevance without adopting effective digital engagement strategies. This phenomenon has been particularly beneficial for the café and specialty coffee segments, where a strong social media presence has been directly linked to increased foot traffic and the ability to command premium pricing. The interplay between digital visibility and consumer behavior underscores the growing importance of social media as a critical driver of success in Saudi Arabia’s evolving food culture.

Rise of cloud kitchens and virtual-only brands

In 2024, the Saudi foodservice industry experienced a significant transformation with the growing adoption of cloud kitchens. These innovative facilities enable operators to manage multiple virtual brands from a single location, optimizing operational efficiency. By eliminating the need for traditional brick-and-mortar establishments, cloud kitchens help operators avoid substantial real estate expenses, which can account for 20-35% of revenue in high-demand areas such as Riyadh and Jeddah. The Saudi Food and Drug Authority introduced a licensing framework for cloud kitchens in 2024, providing much-needed regulatory clarity. This framework not only fosters investment in the sector but also ensures that food safety standards remain on par with those of conventional restaurants. Virtual brand strategies empower established restaurants to explore and test new culinary concepts without the financial and logistical risks associated with physical expansion. At the same time, pure-play cloud kitchen operators can enter the market with significantly reduced capital requirements, making the model highly attractive. This approach aligns seamlessly with Saudi Arabia's predominantly young and tech-savvy population, who increasingly prefer online food ordering. The widespread use of smartphones in the country further supports advanced delivery logistics, ensuring efficient and timely service. Additionally, the International Telecommunication Union (ITU) reported that, as of 2024, 100% of individuals in Saudi Arabia were internet users[3]Source: International Telecommunication Union (ITU), "Individuals using the Internet (% of population) - Saudi Arabia", worldbank.org, highlighting the strong digital infrastructure that underpins the success of cloud kitchens.

Increasing consumer preference for convenience and ready-to-eat food

As traditional home cooking patterns continue to evolve, demographic changes such as the rise of dual-income households and longer working hours are significantly driving the demand for convenience-oriented food solutions, particularly ready-to-eat (RTE) meals. In Saudi Arabia, the increasing participation of women in the workforce, supported by Vision 2030 employment initiatives, has created a growing segment of time-constrained consumers who prioritize convenience over traditional meal preparation. This shift has led to an expanded variety of convenience and RTE food options, including health-focused, halal-certified, organic, and customizable offerings, which cater to the changing dietary preferences and nutritional needs of modern consumers. The growing penetration of convenience stores and the expansion of modern trade channels have provided robust distribution networks for grab-and-go foodservice concepts. Simultaneously, the rising adoption of online grocery platforms has enabled the development of hybrid retail-foodservice models, blending the convenience of online shopping with ready-to-eat meal solutions. Notably, younger consumers, particularly those under 30, are increasingly willing to pay a premium for convenience, reflecting a shift in consumer behavior that supports margin expansion for operators who successfully combine convenience with high-quality offerings. This trend is not limited to individual meal solutions but extends to family-sized convenience options. Operators are capitalizing on this opportunity by introducing bundled offerings that replace traditional home-cooked meals, allowing them to capture higher transaction values. These bundled solutions not only address the needs of busy households but also align with the broader shift toward convenience-driven consumption patterns.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply chain fragility and ingredient sourcing challenges | −0.9% | Nationwide, acute in remote cities | Medium term (2-4 years) |

| Pressure from multinational and domestic chains on smaller operators | −0.7% | Urban centers with dense chain penetration | Short term (≤ 2 years) |

| Quality consistency issues among independents | −0.5% | Nationwide, especially family-run outlets | Medium term (2-4 years) |

| Frequent policy or tax changes on food and beverages | −0.4% | National regulatory environment | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Supply chain fragility and ingredient sourcing challenges

Saudi foodservice operators, particularly independent ones lacking the advantage of procurement scale, face significant challenges due to currency fluctuations and supply disruptions. These issues are especially evident in coffee imports, where such disruptions can quickly diminish profit margins. The Kingdom's geographic remoteness from major agricultural regions exacerbates logistical difficulties, which become more severe during periods of regional conflict or global supply chain disruptions. As a result, operators are often forced to maintain higher inventory levels to mitigate risks, leading to a substantial tie-up of working capital. To address these vulnerabilities, the Saudi government has introduced initiatives aimed at bolstering food security through local production. For instance, partnerships like the joint venture between Hilton Foods and NADEC for meat processing are designed to reduce reliance on imports. However, achieving a meaningful scale in these efforts will take several years. Fresh produce sourcing presents additional hurdles, as ensuring consistent quality and managing shelf life require advanced cold chain infrastructure. Unfortunately, many independent operators lack the financial resources to invest in such systems. Moreover, the concentration of import facilities in major ports creates regional price disparities, placing operators in secondary cities at a competitive disadvantage. Adding to these complexities, halal certification requirements for international sourcing introduce further challenges, increasing both the cost and intricacy of procurement processes.

Pressure from multinational and domestic chains on smaller operators

Chain operators capitalize on their superior access to capital, standardized operations, and extensive marketing resources, which provide them with significant competitive advantages over independent restaurants. These advantages are particularly evident in prime locations, where lease negotiations often favor tenants with strong credit profiles due to their perceived financial stability. Multinational franchises benefit from well-established operational systems and widespread brand recognition, enabling them to lower customer acquisition costs. On the other hand, independent operators are compelled to make substantial investments in marketing efforts and maintaining quality consistency, often without the assurance of achieving desired returns. The growing prevalence of delivery platforms has further amplified the competitive edge of chain operators. They effectively utilize national marketing campaigns and maintain a consistent digital presence, which enhances their visibility in app-based discovery and customer engagement. Additionally, the adoption of advanced technologies, such as point-of-sale systems and inventory management tools, incurs significant costs. These costs create barriers that disproportionately impact smaller operators, while chain operators benefit from economies of scale and dedicated IT support teams. Independent operators face heightened challenges in high-traffic areas, such as malls and airports, where landlords increasingly prioritize chain tenants. This preference stems from the operational reliability and financial stability that chain operators bring, making them more attractive to landlords in these competitive and high-demand locations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Foodservice Type: Full Service Restaurants Lead Despite Café Acceleration

Full-service restaurants hold a 53.62% market share in 2025, highlighting Saudi consumers' preference for dining experiences that combine social engagement with a variety of cuisines. The dominance of Full Service Restaurants is rooted in cultural dining habits that prioritize family gatherings and business entertainment. This is particularly evident in the popularity of Asian, Middle Eastern, and North American cuisines, which appeal to both local tastes and expatriate communities. Meanwhile, Café and Bars are experiencing the fastest growth, with a 11.82% CAGR projected through 2031. This growth is driven by rapid urbanization and increasing disposable incomes, which are encouraging consumers to opt for casual yet stylish cafés that align with their modern, busy lifestyles. Cloud kitchens are emerging as a disruptive segment, utilizing delivery-first models to attract convenience-focused consumers while bypassing traditional real estate investments. These models are supported by SFDA licensing frameworks that facilitate quick market entry.

Quick Service Restaurants are maintaining steady growth, supported by franchise expansions and menu localization. Urban areas are seeing increased demand for burgers, pizzas, and meat-based dishes. This segment benefits from standardized operations that ensure consistent quality, addressing a key challenge faced by independent operators. Within the Café segment, specialty coffee and tea shops are driving premium positioning. Partnerships, such as Costa Coffee's collaboration with the Saudi Coffee Company, illustrate how international brands are incorporating local sourcing to enhance authenticity. Additionally, juice, smoothie, and dessert bars are capitalizing on health-conscious trends and their appeal on social media, particularly among younger demographics who value visually appealing presentations alongside nutritional benefits.

By Outlet: Independent Dominance Faces Chained Expansion

Independent outlets hold a 57.86% market share in Saudi Arabia in 2025, highlighting the country's entrepreneurial food culture and preference for local flavors. However, chained outlets are growing rapidly, achieving an 11.18% CAGR driven by the swift market penetration of franchise models. The sustained dominance of independent operators reflects consumer demand for authentic, locally-tailored dining experiences, which chain operators often struggle to replicate, particularly in segments where family recipes and regional specialties provide a competitive advantage. Conversely, chained outlets benefit from better access to capital, standardized training, and technology integration, enabling faster scaling, something independent operators can only achieve with substantial investments.

Franchise expansions are supported by government initiatives promoting small business growth and foreign investments. For instance, international brands like Café Barbera collaborate with local operators to enter the market quickly while maintaining operational control. At the same time, independent operators face growing challenges from delivery platform requirements, rising digital marketing costs, and quality standardization demands, which favor operators with strong support systems. The competitive landscape varies significantly by location: chained outlets perform better in malls, airports, and commercial areas, where standardized operations and brand recognition offer advantages. In contrast, independent operators excel in neighborhood locations and traditional dining districts, where local expertise and community connections drive customer loyalty.

By Location: Standalone Locations Dominate While Leisure Venues Accelerate

Standalone locations lead the market with a 71.74% share in 2025, highlighting the importance of traditional restaurant districts and neighborhood dining in Saudi culture. Restaurants in these areas serve as social hubs, often prompting dedicated visits rather than convenience-driven consumption. Leisure venues are experiencing a strong 10.93% CAGR, driven by the development of entertainment infrastructure that creates new consumption opportunities. Vision 2030's focus on enhancing the entertainment sector, including theme parks, cultural districts, and sports facilities, has cultivated a captive audience for leisure venues, enabling premium pricing and extended operating hours.

Travel locations, such as airports and transportation hubs, are seeing significant growth as passenger volumes rise toward the 2030 tourism goal of 150 million visitors. Avolta's contract at King Khalid International Airport exemplifies the sector's transformation into comprehensive dining destinations. Retail locations within malls and shopping centers benefit from steady foot traffic but face margin pressures due to high rental costs and competition from food courts. Lodging-based foodservice is gaining from the expansion of the hotel industry and increased business travel. However, it remains limited by a hotel room inventory that falls short of the country's ambitious tourism objectives.

By Service Type: Dine-in Leadership Challenged by Delivery Growth

Dine-in services hold a 75.66% market share in 2025, reflecting Saudi Arabia's cultural preference for communal dining and family gatherings. Delivery services, on the other hand, are growing at an 11.14% CAGR, driven by the rise of digital platforms and cloud kitchens. The continued dominance of dine-in services emphasizes the experiential nature of foodservice in Saudi culture, where restaurants fulfill important social roles, particularly for family meals and business entertainment, which delivery services cannot fully replicate. However, delivery services are expanding rapidly due to advancements in logistics, a wider range of payment options, and the increasing adoption of convenience-focused lifestyles.

Takeaway services occupy a distinct position, benefiting from the grab-and-go trend while avoiding the complexities of delivery logistics. This is especially evident in business districts and transportation hubs, where time-pressed consumers seek quick meal solutions. As operators increasingly integrate dine-in, takeaway, and delivery services through unified ordering systems and streamlined kitchen operations, the boundaries between these service types are becoming less defined. Despite this growth, delivery services face challenges such as commission fees, which typically range from 20-35% of the order value. To maintain profitability across all service channels, operators are focusing on higher-margin menu items and improving operational efficiency.

Geography Analysis

Saudi Arabia's foodservice market exhibits notable regional differences, with Riyadh and Jeddah hosting the highest concentration of dining establishments and leading in per-capita consumption. Secondary cities like Dammam, Al-Ahsa, and Hail display unique consumption trends influenced by local cultural preferences and economic factors. In Riyadh, households dine out approximately twice a week, driven by higher disposable incomes and a greater openness to international cuisines. Jeddah, on the other hand, features a significant focus on fiber-rich and seafood-based dining options, reflecting its coastal location and diverse demographic. The capital region benefits from consistent demand for casual and upscale dining, supported by government employment and business travel. Meanwhile, Jeddah's role as a commercial hub and a gateway for Hajj pilgrims ensures steady foodservice demand throughout the year, with peaks during religious tourism seasons.

In northern regions like Hail, traditional Saudi cuisine, particularly rice-based dishes such as Kabsa, is highly favored. This creates opportunities for operators who can deliver authentic traditional recipes while maintaining modern service standards. In the Eastern Province, cities like Dammam and Al-Ahsa show a preference for meat-heavy dishes and traditional specialties like Harees, highlighting cultural tastes that favor operators skilled in regional cuisine preparation. The alignment of foodservice demand with Vision 2030 development priorities is becoming more evident. Mega-projects in NEOM, the Red Sea, and Qiddiya are establishing new consumption hubs that require comprehensive foodservice infrastructure from the outset, rather than relying on organic market growth.

Major cities in Saudi Arabia benefit from advanced logistics networks, enabling diverse ingredient sourcing and efficient delivery operations. Smaller cities, however, face distribution challenges that limit menu variety and increase operational costs. The concentration of food processing facilities in Riyadh and Jeddah provides cost advantages for operators in these areas. In contrast, secondary cities often rely on more expensive distribution networks, which affect pricing strategies and profit margins. Government initiatives, such as MODON's food cluster development in Jeddah, aim to establish industrial cities across various regions, fostering more balanced regional supply chains and potentially reducing geographic cost disparities over the forecast period.

Competitive Landscape

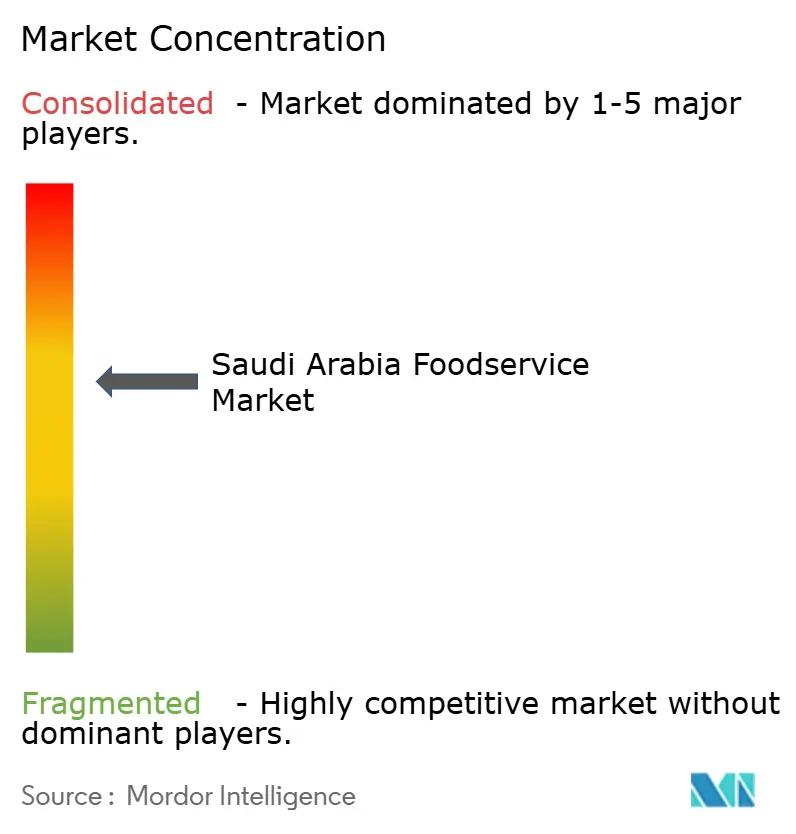

The Saudi Arabia foodservice market is moderately fragmented, with established local champions competing intensely against expanding international chains. Local players such as ALBAIK, Herfy, and Kudu leverage their cultural understanding and cost-efficient operations to maintain strong market positions. In contrast, international brands utilize standardized systems and global marketing resources to scale rapidly. Competition intensity varies across segments: quick-service restaurants experience aggressive expansion due to franchise models lowering entry barriers, while full-service dining remains more fragmented because of higher capital requirements and the need for local culinary expertise.

Key players in the market include ALBAIK Food Systems Company S.A., Americana Restaurants International PLC, McDonald's Corporation, Yum! Brands Inc, and Restaurant Brands International. The Saudi Arabian foodservice market is marked by strategic initiatives from major players focusing on expansion and innovation. Companies are increasingly investing in new production facilities and restaurant outlets, particularly in high-traffic urban areas and emerging commercial zones. Product innovation is a priority, with players introducing new menu items, healthier options, and localized offerings to meet changing consumer preferences. Market leaders are also emphasizing sustainability initiatives and quality certifications to strengthen their positions while expanding through franchise models and joint ventures. Notably, Saudi food companies are setting benchmarks in operational excellence.

Technology adoption has become a critical competitive differentiator, with operators investing in AI-driven personalization, automated ordering systems, and delivery optimization to enhance operational efficiency and customer experience. Cloud kitchen operators like Kaykroo and emerging virtual brands are reshaping the competitive landscape by enabling rapid concept testing and market entry without traditional real estate constraints. This shift is prompting established operators to reevaluate their location strategies and operational models. The regulatory environment, including SFDA licensing requirements and Saudization employment mandates, imposes compliance costs that benefit operators with strong administrative capabilities, while smaller independents struggle to balance regulatory compliance with operational demands. Strategic partnerships between international operators and local entities, such as Hilton Foods' joint venture with NADEC, highlight the increasing importance of local expertise and regulatory navigation over standalone brand expansion.

Saudi Arabia Foodservice Industry Leaders

-

ALBAIK Food Systems Company S.A.

-

Americana Restaurants International PLC

-

McDonald's Corporation

-

Yum! Brands Inc

-

Restaurant Brands International

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Tanmiah has entered into a partnership with McDonald’s Saudi Arabia to enhance poultry production standards in the Kingdom. This partnership highlights a shared focus on increasing the supply of locally sourced poultry to the globally recognized quick-service restaurant chain.

- April 2025: Pret A Manger has launched its first outlet in Saudi Arabia, located in the Olaya Towers of Riyadh. This initiative marks a key milestone in the brand's broader expansion strategy across the Gulf Cooperation Council (GCC) region.

- October 2024: Dunkin opened its 800th store in Saudi Arabia in collaboration with Shahia Food Limited Company. The store offers a variety of menus and food products.

- July 2024: Gong Cha brand opened its first store in Riyadh. Gong Cha is a Taiwanese bubble tea chain that partnered with Shahia Food Limited Company to expand its presence in Saudi Arabia.

Saudi Arabia Foodservice Market Report Scope

Cafes & Bars, Cloud Kitchen, Full Service Restaurants, Quick Service Restaurants are covered as segments by Foodservice Type. Chained Outlets, Independent Outlets are covered as segments by Outlet. Leisure, Lodging, Retail, Standalone, Travel are covered as segments by Location.

By Foodservice Type

| Cafe and Bars | By Cuisine | Bars and Pubs |

| Cafe | ||

| Juice/Smoothie/Desserts Bars | ||

| Specialist Coffee and Tea Shops | ||

| Cloud Kitchen | ||

| Full Service Restaurants | By Cuisine | Asian |

| European | ||

| Latin American | ||

| Middle Eastern | ||

| North American | ||

| Other FSR Cuisines | ||

| Quick Service Restaurants | By Cuisine | Bakeries |

| Burger | ||

| Ice Cream | ||

| Meat-based Cuisines | ||

| Pizza | ||

| Other QSR Cuisines |

By Outlet

| Chained Outlets |

| Independent Outlets |

By Locations

| Leisure |

| Lodging |

| Retail |

| Standalone |

| Travel |

By Service Type

| Dine-in |

| Takeaway |

| Delivery |

| By Foodservice Type | Cafe and Bars | By Cuisine | Bars and Pubs |

| Cafe | |||

| Juice/Smoothie/Desserts Bars | |||

| Specialist Coffee and Tea Shops | |||

| Cloud Kitchen | |||

| Full Service Restaurants | By Cuisine | Asian | |

| European | |||

| Latin American | |||

| Middle Eastern | |||

| North American | |||

| Other FSR Cuisines | |||

| Quick Service Restaurants | By Cuisine | Bakeries | |

| Burger | |||

| Ice Cream | |||

| Meat-based Cuisines | |||

| Pizza | |||

| Other QSR Cuisines | |||

| By Outlet | Chained Outlets | ||

| Independent Outlets | |||

| By Locations | Leisure | ||

| Lodging | |||

| Retail | |||

| Standalone | |||

| Travel | |||

| By Service Type | Dine-in | ||

| Takeaway | |||

| Delivery | |||

Market Definition

- FULL-SERVICE RESTAURANTS - A foodservice establishment where customers are seated at a table, give their order to a server and are served food at a table.

- QUICK SERVICE RESTAURANTS - A foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables.

- CAFES & BARS - A type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars.

- CLOUD KITCHEN - A foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers.

| Keyword | Definition |

|---|---|

| Albacore Tuna | It is one of the smallest species of tuna found in the six distinct stocks known globally in the Atlantic, Pacific, and Indian oceans, as well as the Mediterranean Sea. |

| Angus beef | It is beef derived from a specific breed of cattle indigenous to Scotland. It requires certification from the American Angus Association to receive the "Certified Angus Beef" quality mark. |

| Asian cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Chinese, Indian, Korean, Japanese, Bengali, Southeast Asian, etc. |

| Average Order Value | It is the average value of all orders made by the customers at a foodservice establishment. |

| Bacon | It is salted or smoked meat that comes from the back or sides of a pig. |

| Bars & Pubs | It is a drinking establishment that is licensed to serve alcoholic drinks for consumption on the premises. |

| Black Angus | It is beef derived from a black-hided breed of cows that don't have horns. |

| BRC | British Retail Consortium |

| Burger | It is a sandwich consisting of one or more cooked beef patties, placed inside a sliced bread roll or bun roll. |

| Café | It is a foodservice establishment serving various refreshments (mainly coffee) and light meals. |

| Cafes & Bars | It is a type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars. |

| Cappuccino | It is an Italian coffee drink that is traditionally prepared with equal parts double espresso, steamed milk, and steamed milk foam. |

| CFIA | Canadian Food Inspection Agency |

| Chained Outlet | It refers to a foodservice establishment that shares brands, operates in several locations, has central management, and standardized business practices. |

| Chicken Tender | It refers to chicken meat prepared from the pectoralis minor muscles of a chicken bird. |

| Cloud Kitchen | It is a foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers. |

| Cocktail | It is an alcoholic mixed drink made with either a single spirit or a combination of spirits, mixed with other ingredients such as juices, flavored syrups, tonic water, shrubs, and bitters. |

| Edamame | It is a Japanese dish prepared with soybeans (harvested before they ripen or harden) and cooked in its pod. |

| EFSA | European Food Safety Authority |

| ERS | Economic Research Service of the USDA |

| Espresso | It is a concentrated form of coffee, served in shots. |

| European cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Italian, French, German, English, Dutch, Danish, etc. |

| FDA | Food and Drug Administration |

| Fillet Mignon | It is a cut of meat taken from the smaller end of the tenderloin. |

| Flank Steak | It is a cut of beef steak taken from the flank, which lies forward of the rear quarter of a cow. |

| Foodservice | It refers to the part of the food industry which includes businesses, institutions, and companies which prepare meals outside the home. It includes restaurants, school and hospital cafeterias, catering operations, and many other formats. |

| Franks | Also known as frankfurter or Würstchen, it is a type of highly seasoned smoked sausage popular in Austria and Germany. |

| FSANZ | Food Standards Australia New Zealand |

| FSIS | Food Safety and Inspection Service |

| FSSAI | Food Safety and Standards Authority of India |

| Full service restaurant | It refers to a foodservice establishment where customers are seated at a table, give their order to a server, and are served food at a table. |

| Ghost Kitchen | It refers to a cloud kitchen. |

| GLA | Gross Leasable Area |

| Gluten | It is a family of proteins found in grains, including wheat, rye, spelt, and barley. |

| Grain-fed beef | It is beef derived from cattle that have been fed a diet supplemented with soy and corn and other additives. Grain-fed cows can also be given antibiotics and growth hormones to fatten them up more quickly. |

| Grass-fed beef | It is beef derived from cattle that have only been fed grass as feed. |

| Ham | It refers to the pork meat taken from the leg of a pig. |

| HoReCa | Hotels, Restaurants and Cafes |

| Independent Outlet | It refers to a foodservice establishment that operates with a single outlet or is structured as a small chain with no more than three locations. |

| Juice | It is a drink made from the extraction or pressing of the natural liquid contained in fruit and vegetables. |

| Latin American | It includes full-service offerings in restaurants that serve cuisines from cultures such as Mexican, Brazilian, Argentinian, Colombian, etc. |

| Latte | It is a milk-based coffee that is made up of one or two shots of espresso, steamed milk, and a thin layer of frothed milk. |

| Leisure | It refers to foodservice offered as a part of a recreation business, such as sports arenas, zoos, movie theaters, and museums. |

| Lodging | It refers to foodservice offerings at hotels, motels, guesthouses, holiday homes, etc. |

| Macchiato | It is an espresso coffee drink with a small amount of milk, usually foamed. |

| Meat-based cuisines | This inlcudes food items like fried chicken, steak, ribs, etc. where meat is the primary ingredient for the dish. |

| Middle Eastern cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Arabic, Lebanese, Iranian, Israeli, etc. |

| Mocktail | It is an non-alcoholic mixed drink. |

| Mortadella | It is a large Italian sausage or luncheon meat made of finely hashed or ground heat-cured pork, which incorporates at least 15% small cubes of pork fat. |

| North American | It includes full-service offerings in restaurants that serve cuisines from cultures such as American, Canadian, Caribbean, etc. |

| Pastrami | It refers to a highly seasoned smoked beef, typically served in thin slices. |

| PDO | Protected Designation of Origin: It is the name of a geographical region or specific area that is recognized by official rules to produce certain foods with special characteristics related to location. |

| Pepperoni | It is an American variety of spicy salami made from cured meat. |

| Pizza | It is a dish made typically of flattened bread dough spread with a savory mixture usually including tomatoes and cheese and often other toppings and baked. |

| Primal cuts | It refers to the major sections of the carcass. |

| Quick service restaurant | It refers to a foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables. |

| Retail | It refers to a foodservice outlet inside a mall. shopping complex or a commercial real estate building, where there are other businesses operating as well. |

| Salami | It is a cured sausage consisting of fermented and air-dried meat. |

| Saturated fat | It is a type of fat in which the fatty acid chains have all single bonds. It is generally considered unhealthy. |

| Sausage | It is a meat product made of finely chopped and seasoned meat, which may be fresh, smoked, or pickled and which is then usually stuffed into a casing. |

| Scallop | It is an edible shellfish that is a mollusk with a ribbed shell in two parts. |

| Seitan | It is a plant-based meat substitute made out of wheat gluten. |

| Self-service kiosk | It refers to a self-order point-of-sale (POS) system through which customers place and pay for their own orders at kiosks, enabling totally contactless and frictionless service. |

| Smoothie | It is a beverage made by placing all the ingredients in a container and processing them together, without removing the pulp. |

| Specialty coffee & tea shops | It refers to a foodservice establishment that serves only various types of tea or coffee. |

| Standalone | It refers to a restaurants that have an independent infrastructure setup and not connected to any other business. |

| Sushi | It is a Japanese dish of prepared vinegared rice, usually with some sugar and salt, accompanied by a variety of ingredients, such as seafood—often raw—and vegetables. |

| Travel | It refers to foodservice offerings such as airplane food, dining on long-distance trains, and foodservice on cruise ships. |

| Virtual Kitchen | It refers to a cloud kitchen. |

| Wagyu Beef | It is beef derived from any of four strains of a breed of black or red Japanese cattle that are valued for their highly marbled meat. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for the market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market size estimations for the forecast years are in nominal terms. Inflation is considered for average order value, and it is forecasted as per predicted inflation rates in the countries.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms