Saudi Arabia Data Center Networking Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

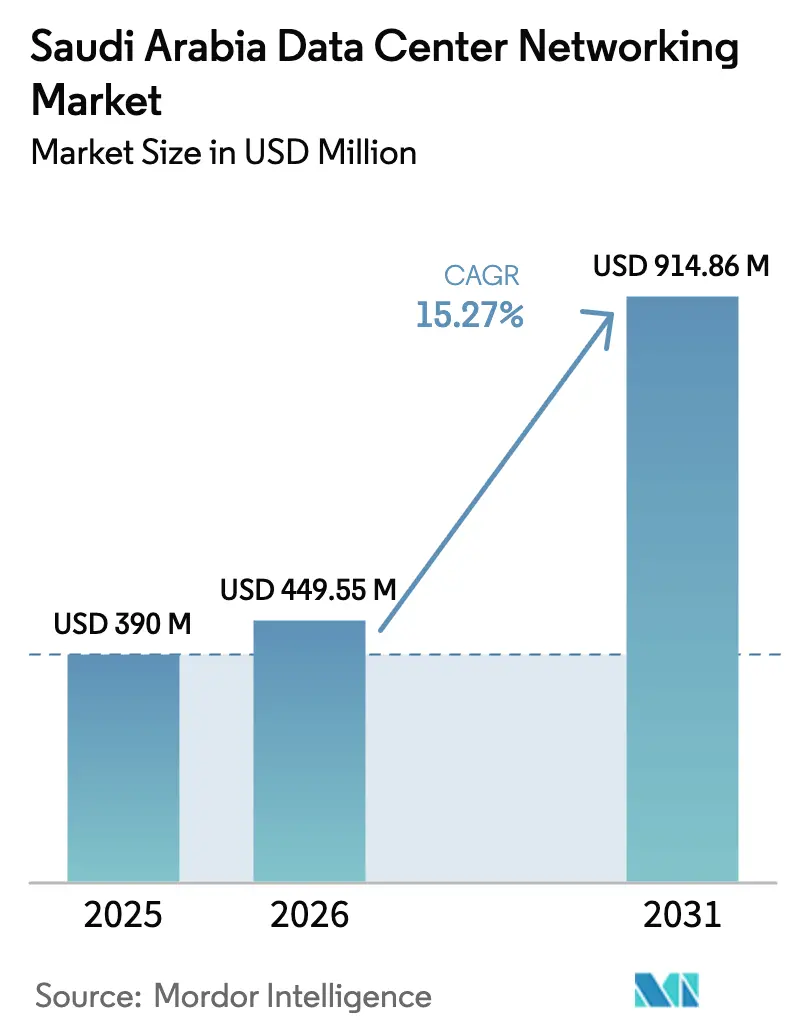

| Base Year Market Size (2025) | USD 390 Million |

| Market Size (2026) | USD 449.55 Million |

| Market Size (2031) | USD 914.86 Million |

| Growth Rate (2026 - 2031) | 15.27% CAGR |

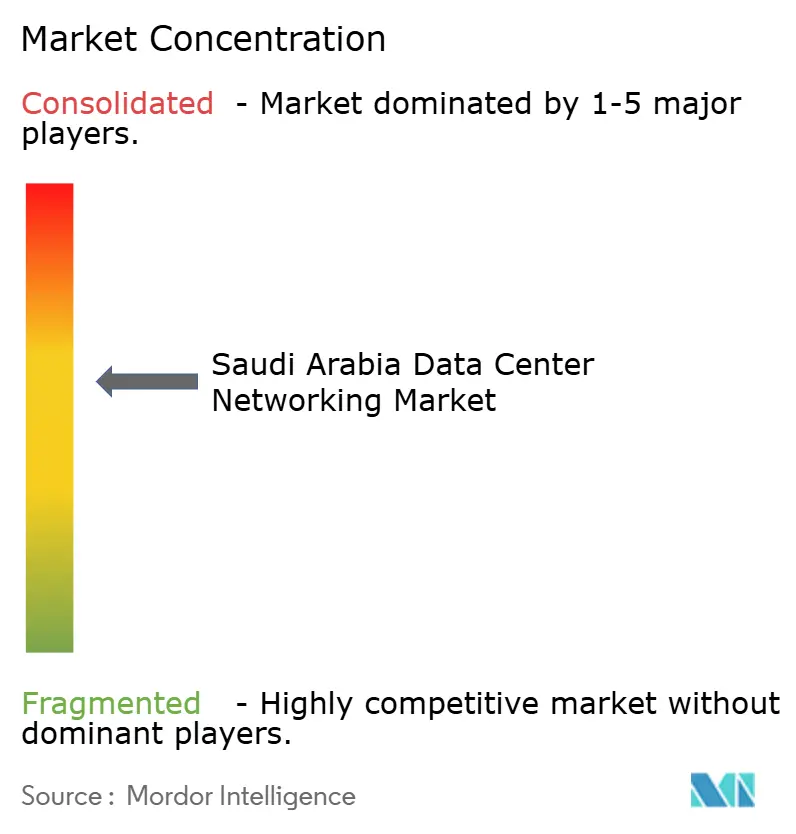

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Data Center Networking Market Analysis by Mordor Intelligence

The Saudi Arabia Data Center Networking market size is expected to grow from USD 390 million in 2025 to USD 449.55 million in 2026 and is forecast to reach USD 914.86 million by 2031 at 15.27% CAGR over 2026-2031. Strong policy support under Vision 2030, a USD 18 billion government data-center program, and hyperscale cloud region roll-outs are shifting capital from hydrocarbon assets to digital infrastructure. Rising AI and high-performance computing (HPC) workloads are accelerating upgrades to spine-leaf architectures and pushing demand for >100 GbE switching fabrics. Data-localization mandates under the Cloud Computing Regulatory Framework (CCRF) are forcing global providers to build in-country capacity, bolstering domestic networking spend. Renewable-energy power-purchase agreements (PPAs) attached to giga-projects like NEOM are simultaneously lowering operating costs and reinforcing sustainability goals, making green networking a differentiator for investors.

Key Report Takeaways

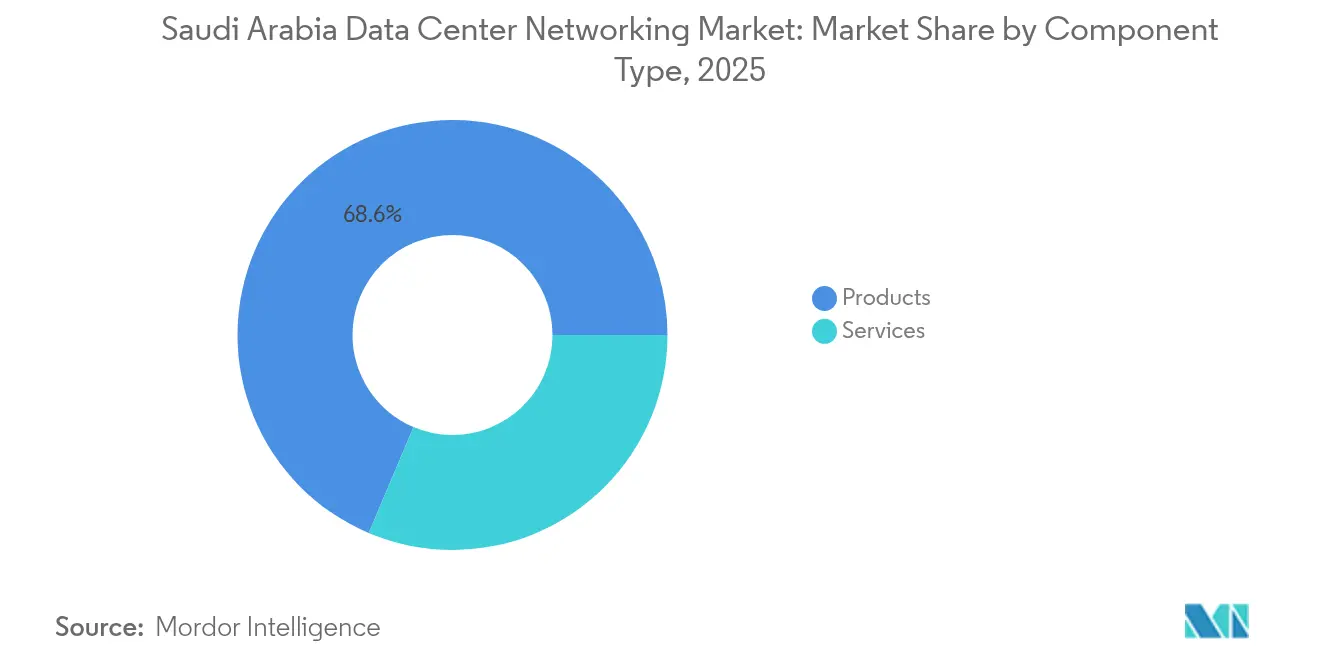

- By component, Products captured 68.63% of Saudi Arabia Data Center Networking market share in 2025, while Services are projected to expand at an 18.08% CAGR to 2031.

- By end-user, IT & Telecommunications led with 35.92% revenue share in 2025; Government & Defense is advancing at a 17.62% CAGR through 2031.

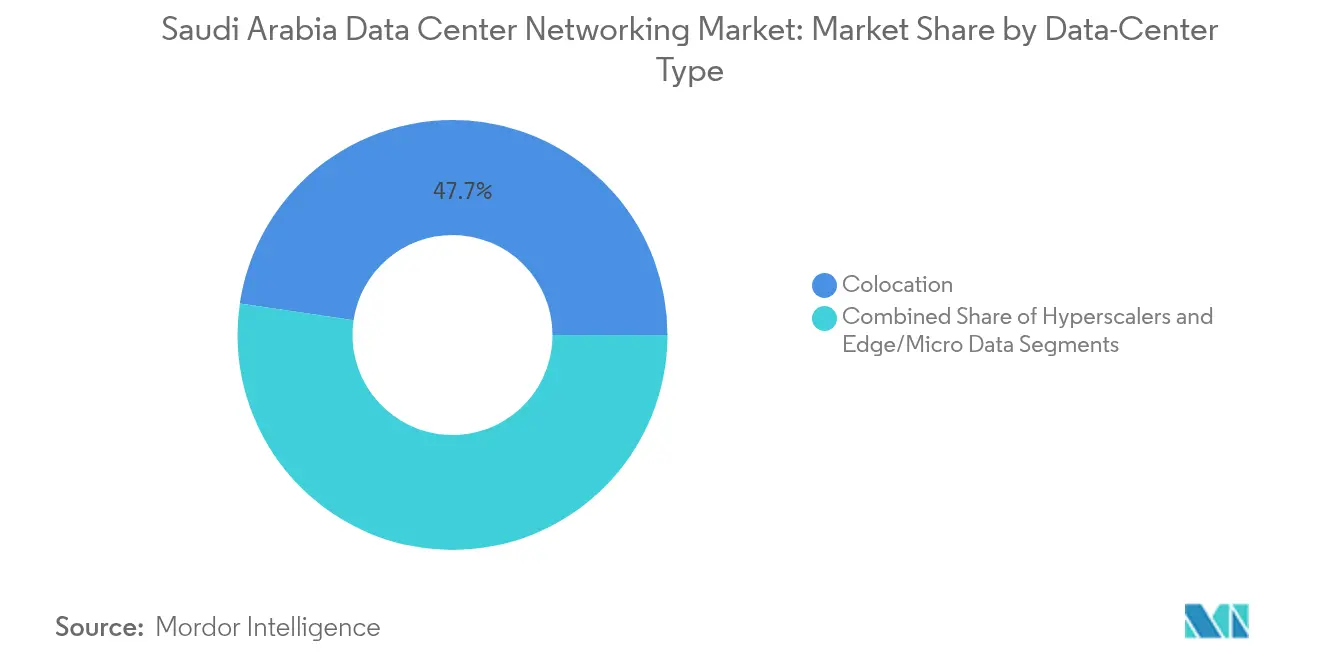

- By data-center type, Colocation achieved 47.66% share of the Saudi Arabia Data Center Networking market in 2025, whereas Hyperscalers/Cloud Service Providers are growing at 18.97% CAGR to 2031.

- By bandwidth, 25–40 GbE held 33.71% share of the Saudi Arabia Data Center Networking market size in 2025; >100 GbE is the fastest-rising segment at a 20.02% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

The contribution of Saudi arabia is incorporated into a multi-country and multi-region total that reflects the full breadth of industry. The data center networking market size by Mordor Intelligence expresses that combined magnitude.

Saudi Arabia Data Center Networking Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 USD 18 billion national data-center program | +4.2% | National, concentrated in Riyadh, Jeddah, Dammam | Long term (≥ 4 years) |

| Hyperscale cloud region roll-outs (AWS, Google, Oracle) | +3.8% | National, with primary hubs in major cities | Medium term (2-4 years) |

| AI/HPC build-outs (e.g., Aramco "Dammam-7") | +2.9% | Regional clusters in Eastern Province, expanding nationally | Medium term (2-4 years) |

| Renewable-energy PPAs enabling green DC networking | +1.7% | NEOM, Red Sea Project, national expansion | Long term (≥ 4 years) |

| Data-localization mandates (CCRF) | +2.1% | National, affecting all sectors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Vision 2030 USD 18 Billion National Data-Center Program

The program targets more than 1,300 MW of capacity by 2030, far exceeding the 360 MW gap projected for the next five years. Each additional megawatt drives 15–20% incremental networking spend, stimulating multi-vendor competition for Ethernet switching, optical transport, and software-defined networking (SDN) controllers. Local integrators such as Al Moammar Information Systems are scaling from 300 MW toward 1,000 MW, demonstrating how indigenous firms are repositioning to capture hyperscale demand.[1]Argaam, “Al Moammar Expands Capacity Above 1,000 MW,” argaam.com The initiative also embeds renewable-energy PPAs, forcing vendors to optimize for power budgets and heat management in desert climates.

Hyperscale Cloud Region Roll-Outs

Oracle’s second public cloud region went live in August 2024 with an explicit AI focus.[2]Oracle Corporation, “Oracle Opens Second Cloud Region in Saudi Arabia,” oracle.com Microsoft completed construction of its Saudi region in December 2024, while AWS confirmed a 2026 launch window. Hyperscalers favor spine-leaf fabrics, 400 GbE optics, and open-standard automation, accelerating the Saudi Arabia Data Center Networking market beyond traditional three-tier designs. Rapid adoption of programmable interfaces is also fostering local software ecosystems around intent-based networking and telemetry analytics.

AI/HPC Build-Outs (e.g., Aramco “Dammam-7”)

Aramco’s Dammam-7 supercomputer ranks among the world’s top systems, necessitating InfiniBand, Remote Direct Memory Access (RDMA) protocols, and terabit-scale backbones. HUMAIN’s partnership with NVIDIA to deploy 18,000 GPUs further fuels ultra-low latency requirements, heightening demand for congestion-aware routing and real-time performance monitoring. SDAIA’s 24 MW Riyadh AI facility reinforces AI-first network design principles such as non-blocking fabrics and GPU-to-GPU messaging.

Data-Localization Mandates (CCRF)

The CCRF compels sensitive workloads—especially in finance and government—to remain on Saudi soil, forcing cloud providers to build in-country zones and redundant interconnects. Resulting architectures replicate cloud availability-zone topologies domestically, boosting demand for metro fiber rings, encryption at rest and in transit, and sovereign key-management systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex and import-driven supply chain exposure | -2.8% | National, affecting all market segments | Short term (≤ 2 years) |

| Certified talent shortage in advanced networking | -1.9% | National, concentrated in technical hubs | Medium term (2-4 years) |

| Data-sovereignty and human-rights scrutiny | -1.4% | National, affecting international vendors | Short term (≤ 2 years) |

| Cooling-water scarcity and sustainability limits | -1.1% | Desert regions, affecting large-scale deployments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capex and Import-Driven Supply Chain Exposure

More than 85% of network hardware is imported, exposing operators to USD-SAR currency swings and logistics delays. Local-content rules require partial assembly inside the Kingdom, inflating cost structures for smaller firms. U.S. suppliers cite dual-use export controls and in-country testing mandates as barriers, extending deployment lead times and compressing margins.

Certified Talent Shortage in Advanced Networking

The National Strategy for Data & AI aims to skill 20,000 specialists by 2030, yet high-end SDN, AI fabric, and quantum-networking expertise remain scarce. C4IR Saudi Arabia’s 2024 survey of 150 SMEs noted deployment delays averaging three months due to engineering shortfalls. Reliance on foreign consultants pushes opex higher and limits the pace at which the Saudi Arabia Data Center Networking market can absorb next-generation platforms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Acceleration Outpaces Products

Products held 68.63% of the Saudi Arabia Data Center Networking market in 2025, anchored by Ethernet switches for spine-leaf fabrics. Routers and SAN gear are giving way to converged architectures, while SDN controllers are mainstreaming as automation becomes imperative. The Saudi Arabia Data Center Networking market size attached to Products is tracking a flatter curve as hyperscalers negotiate volume discounts and embrace open-switching hardware. Conversely, Services are growing 18.08% annually as operators seek integration assistance, proactive support, and managed network operations.

Demand for installation, integration, and consulting stems directly from skills gaps; large enterprises prefer turnkey blueprints that align with CCRF compliance. Managed Network Services monetize AI-driven analytics for congestion, latency, and power optimization, shifting revenue from one-off sales to recurring annuities. Training programs fetch premium rates as they address certifications in DevNet, Kubernetes networking, and Zero Trust segmentation. This service-led momentum is re-shaping vendor positioning in the Saudi Arabia Data Center Networking market.

By End-User: Government & Defense Surge Reshapes Priorities

IT & Telecommunications commanded 35.92% share in 2025 due to incumbents’ metro fiber and submarine-cable assets, but sovereign cloud mandates propel Government & Defense at 17.62% CAGR through 2031. Saudi Data & AI Authority initiatives require secure, GPU-dense clusters; thus, government tenders specify on-chip encryption and deterministic latency. Banking and financial services invest steadily yet remain constrained by compliance-driven architectures that value resilience over raw throughput.

Government momentum injects higher-spec procurement standards, compelling vendors to certify with national security agencies. Defense-grade segmentation, multi-factor cryptography, and air-gapped enclaves are now baseline features, raising the overall technical bar across the Saudi Arabia Data Center Networking market. As public-sector demand scales, price ceilings ease, benefiting premium hardware vendors and managed-service providers alike.

By Data-Center Type: Hyperscaler Momentum Challenges Colocation

Colocation providers retained 47.66% share in 2025, leveraging neutral facilities to serve enterprises, yet hyperscalers are expanding at 18.97% CAGR. Microsoft, Oracle, and AWS prefer bespoke campuses with 400 GbE backbones and direct-to-chip liquid cooling. Local hosters respond by adding AI-ready cages, higher power densities, and cloud-connect fabrics to stay relevant.

Edge and micro-data centers remain nascent but critical for 5G densification, smart-city surveillance, and real-time crowd management at events such as the Hajj. These micro-sites require compact, ruggedized switching capable of fan-less operation in harsh climates. The diversification of facility types broadens solution portfolios, enlarging the reachable Saudi Arabia Data Center Networking market size for vendors that span hyperscale cores and distributed edges.

By Bandwidth: Ultra-High Speed Adoption Accelerates

The less than or equals to 10 GbE segment is declining as legacy enterprises refresh their infrastructure. 25–40 GbE still leads with 33.71% share, covering mid-tier server links and storage interconnects. However, >100 GbE is surging at 20.02% CAGR, reflecting GPU cluster proliferation. Nokia and STC’s 1 Tbps DWDM field trial proves that backbone optics can already exceed workload demand, paving the way for terabit Ethernet.

Enterprises stepping from 40 GbE straight to 400 GbE aim to future-proof Capex and cut aggregation layers. Storage traffic, east-west AI traffic, and disaggregated databases drive the need for lossless fabrics and congestion-control algorithms. Dynamics in bandwidth tiers therefore underpin a volume swing toward optical modules, high-density QSFP-DD ports, and time-sensitive network telemetry across the Saudi Arabia Data Center Networking market.

Geography Analysis

Riyadh, Jeddah, and Dammam account for nearly 75% of capital deployment. Riyadh dominates due to federal agencies, hyperscale zones, and SDAIA’s 24 MW AI site, creating concentrated pull for low-latency metro fiber rings. Jeddah benefits from submarine-cable adjacency; AWS’s January 2025 CloudFront Edge node halves content latency for western users. Dammam anchors energy-sector HPC, with Aramco’s Dammam-7 and Groq’s planned inferencing cluster demanding deterministic, high-bandwidth fabrics.

NEOM and Red Sea Project locations introduce edge-heavy architectures, combining renewable-powered data hubs with smart-city sensors. DataVolt’s USD 5 billion net-zero campus in Oxagon integrates on-site solar and wind, forcing network gear to meet stringent temperature and vibration tolerances. Nationally, 13 submarine systems plus the Saudi Vision Cable extend routes to Europe and Asia, positioning the Kingdom as a regional transit node and multiplying the Saudi Arabia Data Center Networking market’s relevance for international traffic flows.

The geographic shift toward giga-projects and coastal transit hubs redistributes spend beyond legacy metro clusters, compelling vendors to tailor SKUs for desertized environments and modular edge enclosures. This dispersion broadens channel opportunities for system integrators versed in both hyperscale and edge-micro deployments, strengthening competitive intensity across regions within the Saudi Arabia Data Center Networking industry.

Mordor Intelligence provides coverage of the data center networking market across other key regional markets, including North America, South America, and Middle East, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to France, Sweden, United States, Brazil, Malaysia, and Vietnam incorporating local coverage and market participation, as required.

Competitive Landscape

Global incumbents such as Cisco, Huawei, Dell, and Juniper compete alongside regional telcos STC, Mobily, and Zain KSA, yielding a moderately concentrated field. Cisco reports 51% of its USD 54 billion FY 2024 revenue from subscriptions, reflecting a pivot toward software and managed solutions. Huawei’s share in government bids is constrained by security scrutiny, steering it toward private-sector and energy clients. Nokia’s planned USD 2.3 billion acquisition of Infinera underscores consolidation around optical interconnect excellence, an area critical for hyperscale inter-campus routes.

Local carriers exploit last-mile fiber and cross-connect privileges, bundling connectivity, colocation, and managed network services. STC’s 147,000 km fiber footprint backs its Sonic terrestrial corridor with Ooredoo, enhancing redundancy for hyperscale traffic bursts. Mobily’s USD 905 million subsea push co-funds new landing stations, locking in transit revenue from Asia-Europe latency optimizations.

White-space opportunities include quantum-ready key distribution, AI-optimized network operating systems, and immersion-cooling compliant switching. Start-ups offering open-network Linux stacks are gaining proof-of-concept traction at NEOM. Meanwhile, vendors unable to certify sovereign-cloud compliance risk disqualification from lucrative public-sector contracts, tightening barriers to entry and raising the strategic stakes in the Saudi Arabia Data Center Networking market.

Saudi Arabia Data Center Networking Industry Leaders

Cisco Systems, Inc.

Huawei Technologies Co., Ltd.

Dell Technologies Inc.

Hewlett Packard Enterprise Company

Arista Networks, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Super Micro Computer signed an MoU with DataVolt to build renewable-powered AI campuses, integrating ultra-dense GPU platforms

- May 2025: AWS and HUMAIN committed over USD 5 billion to create an AI Zone, coupled with training 100,000 citizens in cloud and AI skills

- May 2025: HUMAIN partnered with NVIDIA, AMD, Cisco, and Qualcomm to deploy 18,000 GPUs and 500 MW of AI compute by 2030

- May 2025: Cisco deepened its collaboration with Saudi agencies to enhance programmable networking for AI data centers.

- February 2025: Mobily launched a USD 905 million data center and subsea cable expansion with Sparkle to strengthen global routes.

- February 2025: STC Group and Ooredoo Oman initiated the 24-month SONIC fiber corridor linking submarine landings and inland data centers

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Saudi Arabian data-center networking market as the annual spend on active hardware and closely linked integration-centric services installed inside purpose-built, colocation, cloud, or edge facilities to interconnect servers, storage, and external networks. The tally covers Ethernet switches, routers, SAN fabrics, ADCs, network-security appliances, SDN controllers, and optical interconnects together with design, installation, support, and managed network services that keep these platforms running.

Scope exclusion: Campus LANs attached to office buildings, passive copper or fiber cabling, and generic telecom backbone gear sit outside this market.

Segmentation Overview

- By Component

- Products

- Ethernet Switches

- Routers

- Storage Area Network (SAN)

- Application Delivery Controllers (ADC)

- Network Security Appliances

- Software-Defined Networking (SDN) Controllers

- Optical Interconnects

- Services

- Installation and Integration

- Training and Consulting

- Support and Maintenance

- Managed Network Services

- Products

- By End-User

- IT and Telecommunications

- Banking, Financial Services and Insurance (BFSI)

- Government and Defense

- Media and Entertainment

- Healthcare and Life Sciences

- Manufacturing and Industrial

- Other End-Users

- By Data-Center Type

- Colocation

- Hyperscalers/Cloud Service Providers

- Edge/Micro Data Centers

- By Bandwidth

- LessThan equals to 10 GbE

- 25–40 GbE

- 50–100 GbE

- Greater Than 100 GbE

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with network architects at colocation operators, hyperscaler regional leads, and tier-one resellers across Riyadh, Jeddah, and Dammam. Their insights on port-density roadmaps, ASP discounts, and service-attach rates closed data gaps and let us reconfirm secondary findings.

Desk Research

We began with Saudi portals such as CITC import ledgers and MCIT Vision 2030 dashboards, and then tracked hyperscale launches through SDAIA briefings, ITU telecom indicators, and Uptime Institute outage logs. Annual filings from listed carriers, vendor press releases, and investor decks revealed pricing and uptake patterns, while financial detail on local suppliers flowed from D&B Hoovers and timely news on Dow Jones Factiva.

A second sweep drew rack-density norms from trade-association white papers, edge-facility counts from Arab Data Center Association surveys, and patent signals via Questel to spot looming optical-speed jumps. These touchpoints are illustrative, not exhaustive, and many additional sources informed our validation.

Market-Sizing & Forecasting

Top-down reconstruction starts with Customs-reported networking imports, mapped to data-center share, then adjusted for utilization and replacement cycles before volumes are priced. Select supplier roll-ups offer a bottom-up smell check. Key variables like planned white-space square meters, average rack power, cloud-subscriber growth, 5G additions, and price-erosion curves feed a multivariate regression that projects revenue through 2030, while scenario analysis captures upside from AI workloads.

Data Validation & Update Cycle

Outputs run through variance checks against independent indicators, followed by dual-analyst review. We refresh every year and issue interim updates when large colocation projects, policy shifts, or sharp currency swings arise.

Why Mordor's Saudi Arabia Data Center Networking Baseline Commands Reliability

Published figures often diverge because firms widen or shrink the component basket, assume flat prices, or refresh at uneven intervals.

Mordor's disciplined scoping, transparent import anchoring, and annual reconfirmation keep the baseline steady yet responsive.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 390 M (2025) | Mordor Intelligence | |

| USD 340 M (2025) | Regional Consultancy A | Omits managed services and >100 GbE optics |

| USD 401 M (2024) | Industry Association B | Straight-line CAGR, no primary validation |

| USD 7.2 M (2024) | Research Boutique C | Restricts scope to SDN software only |

The comparison shows how our model, anchored to transparent Customs data and hands-on expert feedback, delivers a balanced, reproducible view that executives can trust for strategic moves.

Key Questions Answered in the Report

What is the current value of the Saudi Arabia Data Center Networking market?

The Saudi Arabia Data Center Networking market size stands at USD 449.55 million in 2026 and is projected to reach USD 914.86 million by 2031.

Which component segment is growing fastest?

Services are expanding at an 18.08% CAGR as enterprises outsource integration, managed operations, and AI-driven optimization.

Why are Greater Than 100 GbE links gaining traction so quickly?

AI and HPC workloads demand massive east-west bandwidth; hyperscalers are skipping interim speeds and standardizing on 400 GbE and above.

How do data-localization rules affect international cloud providers?

CCRF mandates force global hyperscalers to establish in-country regions, driving local network build-outs and redundant interconnects.

What regions inside Saudi Arabia attract the most networking investment?

Riyadh leads due to government agencies and hyperscale zones, followed by Jeddah for submarine-cable access and Dammam for energy-sector HPC.

Which companies dominate optical interconnect solutions?

Nokia, Ciena, and Huawei head the optical segment, while STC Group leverages its fiber corridors for carrier-neutral capacity offerings.

Page last updated on: